Hemoglobinopathies Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.45 Billion |

| Market Size (2031) | USD 16.72 Billion |

| Growth Rate (2026 - 2031) | 7.88% CAGR |

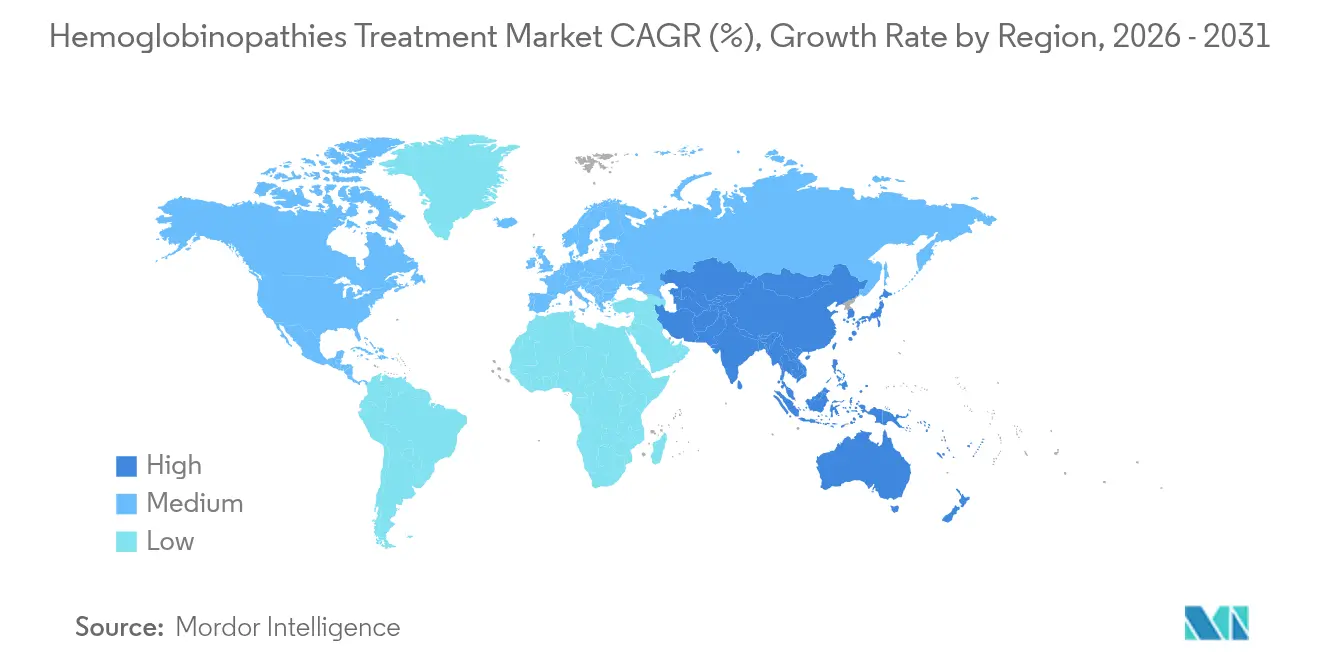

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

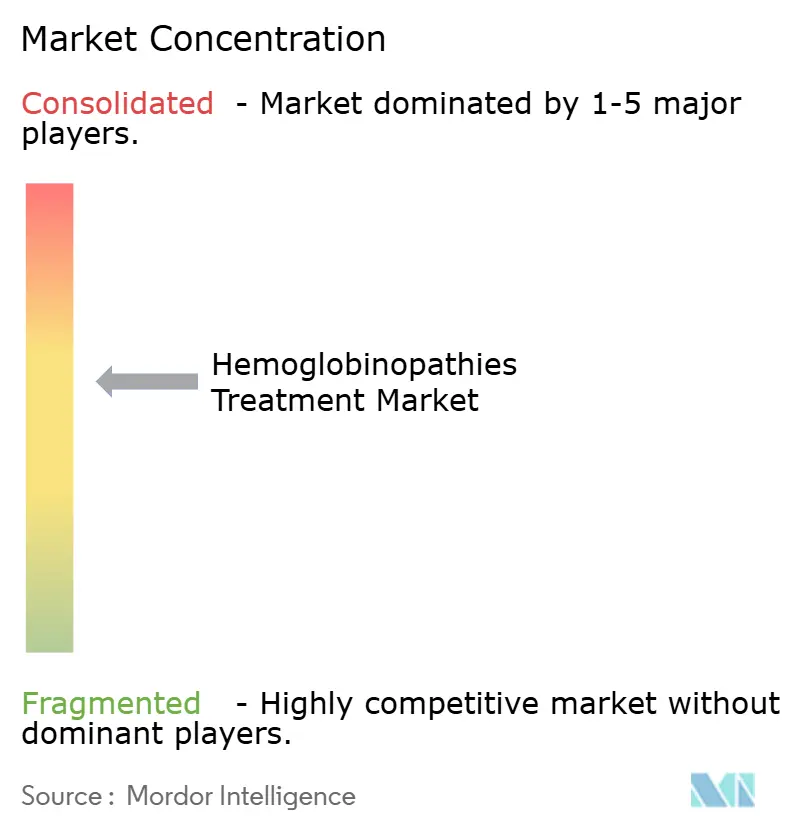

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemoglobinopathies Treatment Market Analysis by Mordor Intelligence

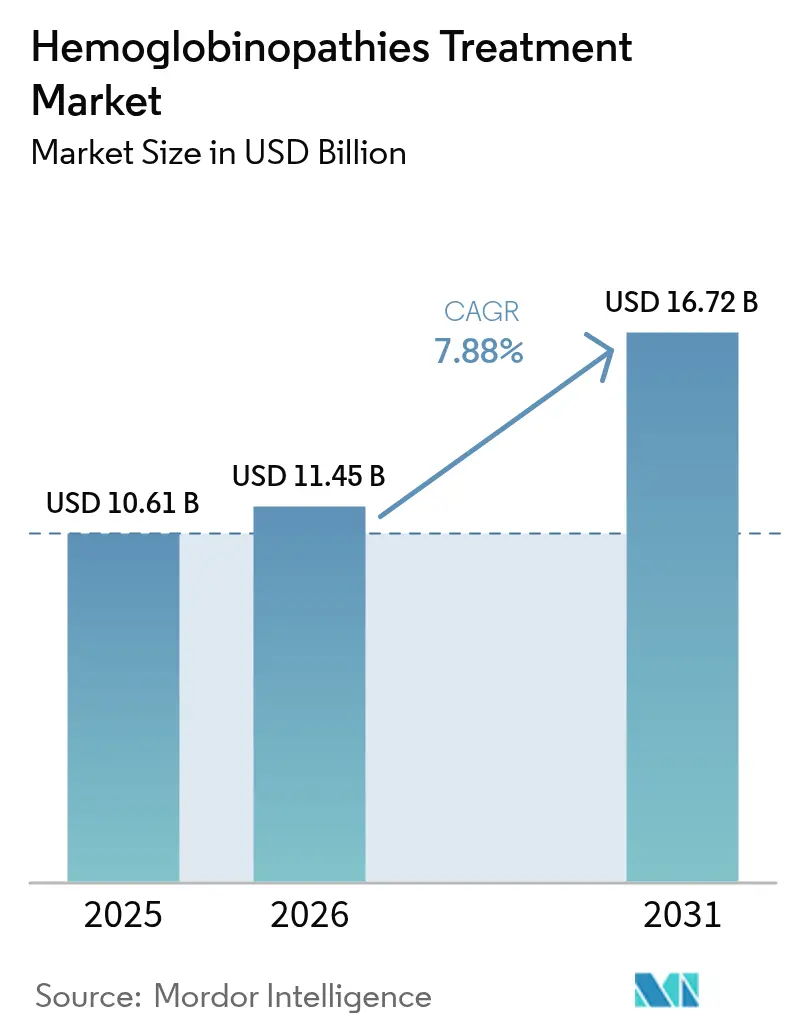

Hemoglobinopathies treatment market size in 2026 is estimated at USD 11.45 billion, growing from 2025 value of USD 10.61 billion with 2031 projections showing USD 16.72 billion, growing at 7.88% CAGR over 2026-2031. This expansion reflects rapid uptake of first-in-class gene therapies, wider newborn screening coverage, and steady investment in specialized care infrastructure. Blood transfusion therapy remains the largest treatment modality, yet physicians increasingly recommend gene-editing options as regulatory approvals build clinical confidence. Rising reimbursement support for rare-disease drugs in middle-income economies is enlarging the eligible patient pool, while artificial-intelligence diagnostics shorten time to diagnosis and treatment initiation. Regional growth differentials persist: North America captures premium revenue through early adoption of curative therapies, whereas Asia–Pacific delivers the fastest incremental volume gains on the back of government-funded screening programs.

Key Report Takeaways

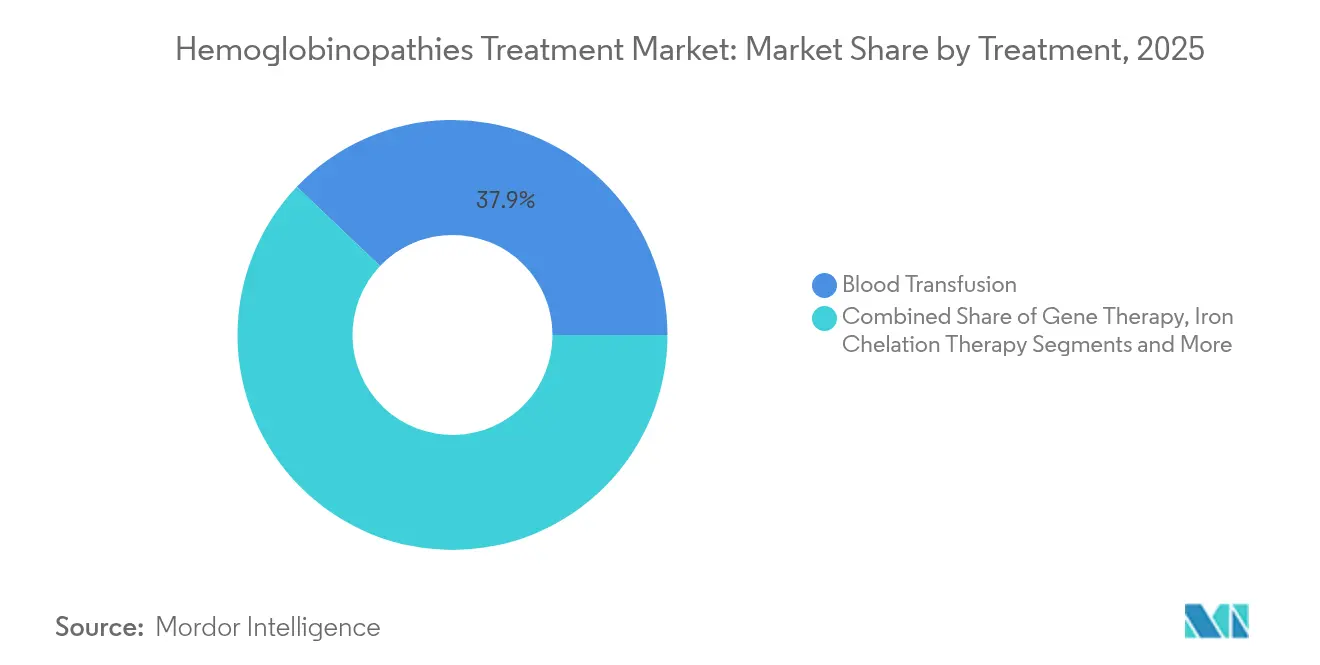

- By treatment, blood transfusion therapy led with 37.89% of hemoglobinopathies treatment market share in 2025; gene therapy is projected to record the highest 19.06% CAGR through 2031.

- By application, sickle cell disease accounted for 48.03% share of the hemoglobinopathies treatment market size in 2025, while thalassemia is forecast to expand at a 10.73% CAGR to 2031.

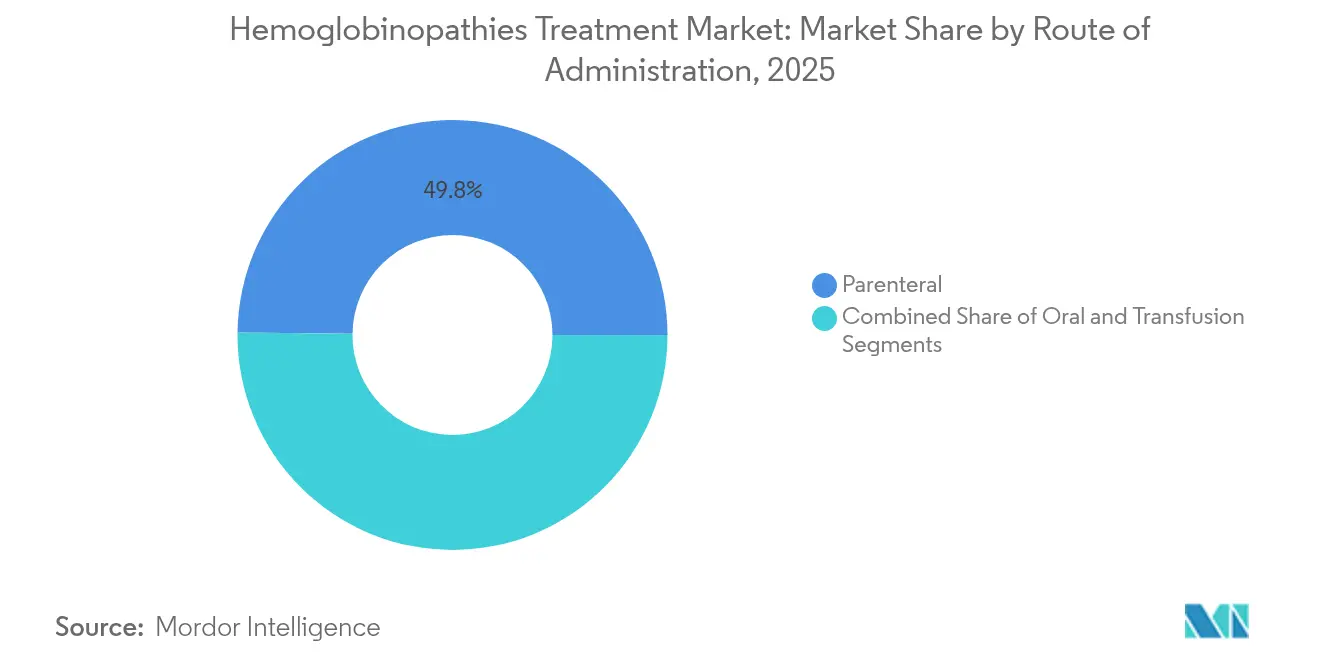

- By route of administration, parenteral formulations dominated with 49.81% share in 2025; subcutaneous and other minimally invasive routes are advancing at an 8.74% CAGR through 2031.

- By end user, hospitals captured 64.23% of hemoglobinopathies treatment market size in 2025, yet specialty clinics exhibit the fastest 9.54% CAGR through 2031.

- By geography, North America held 34.92% revenue share in 2025; Asia-Pacific is on track to post the highest 9.43% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemoglobinopathies Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of hemoglobinopathies | +1.5% | Sub-Saharan Africa, Mediterranean, Middle East | Long term (≥ 4 years) |

| Expanding newborn & antenatal screening | +2.1% | Asia–Pacific core, spill-over to MEA & South America | Medium term (2-4 years) |

| First-in-class gene-therapy approvals | +1.8% | North America & EU, early uptake in developed Asia–Pacific markets | Short term (≤ 2 years) |

| Rare-disease reimbursement roll-outs | +1.2% | Latin America, Eastern Europe, Southeast Asia | Medium term (2-4 years) |

| Decentralized blood-transfusion networks | +0.9% | Sub-Saharan Africa, pilot programs in West Africa | Long term (≥ 4 years) |

| AI-enabled point-of-care diagnostics | +0.7% | Urban centers worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

First-in-class gene-therapy approvals accelerate adoption

FDA clearance of CASGEVY and LYFGENIA between late-2023 and early-2024 has reshaped clinician expectations around curative options. Post-approval real-world data show 94% of evaluable patients eliminating severe vaso-occlusive events within the first 18 months of follow-up. European Medicines Agency authorization widens access across 27 member states and signals a harmonized regulatory pathway for subsequent CRISPR platforms. Early clinical success is driving referral patterns toward definitive therapy, particularly among adolescents who aim to avoid lifelong transfusions and chelation. Treatment centers report rising wait-lists, prompting investments in vector-manufacturing capacity and apheresis infrastructure. The acceleration of gene-therapy uptake is expected to lift the hemoglobinopathies treatment market through premium pricing and extended survival benefits.

Expanding newborn & antenatal screening programs

Mandated screening across high-burden states in India, coupled with roll-outs in Nigeria and Brazil, is enabling earlier diagnosis and linkage to care. India’s multicentric cohort initiative spans seven tertiary hospitals and integrates digital registries for longitudinal follow-up. WHO modeling indicates universal screening could avert 70% of sickle-cell-related mortality, galvanizing donor-funded laboratory upgrades across Sub-Saharan Africa. Rapid diagnostics such as the Gazelle multispectral reader achieve 96.8% accuracy within 3 days of birth[1]HemaSphere, “Multispectral Imaging for Microchip Electrophoresis,” hemasphere.org. In advanced markets, dual-review antenatal protocols standardize result interpretation and improve counseling uptake. Earlier identification expands the candidate pool for curative therapies and supports sustainable volume growth in the hemoglobinopathies treatment market.

Rare-disease reimbursement roll-outs in middle-income nations

Outcome-based payment schemes are emerging to bridge affordability gaps for USD 2 million gene-editing products. The US CMS Cell and Gene Therapy Access Model links reimbursement to predefined clinical milestones, while Thailand and Malaysia have introduced tiered coverage linked to disease severity. Value-based price modeling suggests 80–90% list-price reductions are required for broad access in lower-income settings. Early adopter programs in Brazil include risk-sharing contracts that cap payer exposure if post-infusion transfusion independence is not achieved. These policy shifts widen the hemoglobinopathies treatment market addressable base and de-risk manufacturer revenue streams.

AI-enabled point-of-care diagnostics integration

Machine-vision algorithms embedded in microchip electrophoresis systems cut diagnostic cycle times from days to under one hour, allowing same-visit clinical decision-making. Automated venipuncture robots improve vein localization and reduce pediatric procedural anxiety. Field deployment studies in Ghana show 25% higher screening throughput versus manual approaches. Integration of electronic medical-record interfaces ensures seamless data capture for population registries, strengthening surveillance and research initiatives. Faster diagnosis feeds directly into higher therapy uptake, reinforcing growth in the hemoglobinopathies treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of curative therapies | −1.8% | Global, sharpest in middle-income nations | Short term (≤ 2 years) |

| Donor-match scarcity for stem-cell grafts | −0.9% | Worldwide, amplified in genetically diverse populations | Long term (≥ 4 years) |

| Cold-chain gaps for biologics | −0.6% | Sub-Saharan Africa, Southeast Asia, Latin America | Medium term (2-4 years) |

| Regulatory ambiguity for CRISPR products | −0.4% | Emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of curative therapies

List prices above USD 2 million constrain immediate uptake, prompting insurers to demand long-horizon cost-effectiveness analyses[2]Anthem, “Gene Therapy for Beta Thalassemia,” anthem.com. In several EU states, pay-for-performance models defer 70% of payment until patients remain transfusion-free for two years. Low-income settings negotiate deep discounts but still face supply-chain mark-ups tied to cold-storage logistics. Manufacturer assistance programs mitigate some patient liability yet are limited by budget caps. Until biosimilar or allogeneic off-the-shelf options emerge, sticker shock will temper the upward curve of the hemoglobinopathies treatment market.

Donor-match scarcity for stem-cell transplantation

Only 20–25% of eligible sickle cell patients locate an HLA-matched sibling donor, with the lowest match rates among individuals of African descent[3]Hassan Hammad & Rajput Sheerien, “Blood Pharming: In-Vitro Red Blood Cells,” frontiersin.org. Haploidentical grafts expand eligibility but introduce higher graft-versus-host-disease risk and conditioning toxicity. The International Hemoglobinopathy Research Network’s 45-country GWAS aims to refine eligibility criteria and potentially relax strict HLA thresholds. Meanwhile, autologous gene-editing approaches sidestep donor constraints, redirecting transplant candidates into the gene-therapy funnel and partly offsetting the restraint on the hemoglobinopathies treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment: Gene therapy disrupts traditional care models

The hemoglobinopathies treatment market size for gene therapy is projected to rise at a 19.06% CAGR, whereas blood transfusion maintains a 37.89% share in 2025. Regulatory wins for CRISPR-based products validate one-time curative economics and ignite global pipeline investment. Vertex-CRISPR Therapeutics intend to scale vector capacity by three times to meet US and EU demand waves. Stem-cell transplantation remains curative but is limited by donor availability and graft-versus-host risks, preserving a role for gene-edited autologous options.

Pharmacological disease-modifiers such as voxelotor and crizanlizumab preserve value in regions where reimbursement for gene therapy lags. Iron chelation therapy, indispensable for transfusion-dependent thalassemia, grows steadily alongside decentralized transfusion networks. Emerging base-editing candidates from CorrectSequence illustrate the geographic broadening of innovation as China and Singapore accelerate trial approvals. Overall, treatment-mix evolution favors technologies offering durable benefit, positioning curative platforms as the primary driver of qualitative change in the hemoglobinopathies treatment market.

By Application: Sickle cell dominance faces thalassemia growth

Sickle cell disease controls 48.03% of hemoglobinopathies treatment market share in 2025 and benefits from decades of standardized care pathways in North America and Europe. Nonetheless, thalassemia’s 10.73% CAGR leads the application set, propelled by Mediterranean and South-East Asian screening mandates that convert latent carriers into managed patients. Luspatercept trials for alpha-thalassemia HbH disease highlight ongoing therapeutic diversification beyond transfusion reliance. The Thalassemia International Federation’s digital patient registry improves adherence monitoring and underpins payer negotiations for high-cost therapies. Rare variants, including hemoglobin E disorders, gain visibility through next-generation sequencing programs but remain commercialization niches. With distinct epidemiological footprints, application growth vectors hinge on regional policy implementation and culturally tailored outreach, reinforcing divergent yet complementary flows within the hemoglobinopathies treatment market.

By Route of Administration: Parenteral dominance reflects complexity

Parenteral delivery retained 49.81% revenue share in 2025 as gene therapies, biologics, and exchange transfusions all rely on intravenous access. Subcutaneous innovation lowers clinic burden: Sanofi’s once-monthly fitusiran regimen in hemophilia suggests similar possibilities for anti-P-selectin antibodies in vaso-occlusive-crisis prevention. Oral hydroxyurea and chelators support chronic management but face adherence hurdles tied to gastrointestinal tolerability. Home-infusion models trialed in Germany reduce hospital days by 15% for stable transfusion-dependent adults, signaling future shift of routine care into community settings. Cold-chain resilience remains a gating factor for wider biologic adoption in tropical climates. Across the hemoglobinopathies treatment market, administration-route diversification aims to balance efficacy, safety, and patient convenience without compromising clinical oversight.

By End User: Specialty clinics emerge as growth leaders

Hospitals delivered 64.23% of 2025 revenues, yet specialty clinics will rise at 9.54% CAGR as gene-therapy centers of excellence proliferate. The United Kingdom’s USD 1.9 million investment in apheresis machines across 22 National Health Service trusts exemplifies infrastructure targeting higher procedure volumes. Multidisciplinary clinics integrate hematologists, genetic counselors, and psychosocial support, enhancing adherence and outcome tracking. Academic institutes remain pivotal in early-phase trials, while home-health providers pilot remote chelation management using IoT pumps. As payer contracts transition to value-based metrics, stakeholder alignment around integrated clinics is set to lift quality-adjusted life-year performance, steering incremental revenue to the specialty segment of the hemoglobinopathies treatment market.

Geography Analysis

North America leads the hemoglobinopathies treatment market size with 34.92% share in 2025, benefiting from robust insurance coverage and early adoption of FDA-approved curative options. Gene-therapy infusion centers have doubled since 2023, and outcome-based reimbursement pilots underpin continued premium pricing. Europe follows, leveraging EMA regulatory cohesion and public health systems that swiftly incorporated CASGEVY into rare-disease formularies. Pan-EU joint procurement discussions aim to secure bulk-buy discounts, potentially widening hospital adoption while preserving manufacturer margins.

Asia-Pacific will post the fastest 9.43% CAGR through 2031, driven by high carrier prevalence in India, Thailand, and southern China. India’s National Health Mission funds state-level newborn screening which, coupled with public-private partnerships, funnels newly diagnosed infants into treatment pipelines. China’s National Medical Products Administration granted priority review to domestic base-editing therapies, signaling policy support for indigenous innovation and import alternatives. Southeast Asian nations expand thalassemia day-care units, concentrating transfusion services and accelerating chelation sales. Collectively these initiatives elevate both volume and complexity of care, amplifying regional influence on global supply-chain planning for the hemoglobinopathies treatment market.

Middle East & Africa face infrastructural gaps: Nigeria’s national sickle-cell policy sets ambitious targets, yet cold-chain deficits limit biologic penetration. Pilot decentralized transfusion hubs in Ghana cut rural travel times by 40%, indicating scalable blueprints for broader implementation. South America maintains moderate growth; Brazil’s rare-disease ordinance and inclusion of hydroxyurea in the national formulary stimulate steady demand. Across regions, heterogeneity in healthcare financing, genetic prevalence, and technology adoption will continue to shape disparate yet interlinked trajectories for the hemoglobinopathies treatment market.

Competitive Landscape

The hemoglobinopathies treatment industry comprises legacy pharma, niche biotech, and emerging gene-editing start-ups, yielding moderate fragmentation. Novartis markets hydroxyurea and voxelotor while reinvesting profits into CRISPR alliances. Bluebird bio and Vertex leverage proprietary lentiviral and CRISPR platforms, respectively, positioning themselves as category leaders in curative therapy. Sanofi’s pipeline integrates mRNA-based silencers targeting erythroid maturation regulators, illustrating incumbent diversification beyond small-molecule franchises.

Strategic partnerships proliferate: CSL Behring collaborates with Apellis on complement pathway inhibitors to mitigate transfusion side-effects, and Pfizer co-funds AI-powered diagnostic ventures to capture upstream patient identification. Geographic expansion remains a core tactic; Chinese biotech CorrectSequence partners with Singaporean hospitals to accelerate regional pivotal trials. Manufacturing scalability constitutes a major differentiator: companies owning in-house vector capacity secure shorter turnaround times, an advantage under high-demand scenarios.

Competitive intensity is heightened by payer scrutiny of cost-effectiveness. Firms thus emphasize long-term transfusion independence data and real-world evidence repositories to strengthen value propositions. As curative therapies gain traction, follow-on products face higher efficacy benchmarks, leading to a consolidation wave where capital-rich pharmas acquire late-stage start-ups. Overall, technology leadership, manufacturing agility, and payer engagement will separate winners and laggards within the hemoglobinopathies treatment market.

Hemoglobinopathies Treatment Industry Leaders

Sanofi SA

Novartis AG

Pfizer Inc.

bluebird bio

CSL Behring

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The US FDA granted orphan-drug designation to rilzabrutinib, an oral Bruton's tyrosine kinase inhibitor targeting inflammation-driven vaso-occlusive crises in sickle cell disease.

- April 2025: Under India’s National Health Mission, new funding was released to bolster thalassemia prevention and management infrastructure.

Global Hemoglobinopathies Treatment Market Report Scope

As per the scope of the report, hemoglobinopathies is the group of blood disorders which are inheritable, including thalassemia, sickle cell anaemia and others.

| Stem Cell Transplantation |

| Blood Transfusion |

| Iron Chelation Therapy |

| Pharmacological Agents |

| Gene Therapy |

| Other Supportive Treatments |

| Thalassemia |

| Sickle Cell Disease |

| Other Hemoglobinopathies |

| Oral |

| Parenteral |

| Transfusion |

| Hospitals |

| Specialty Clinics |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment | Stem Cell Transplantation | |

| Blood Transfusion | ||

| Iron Chelation Therapy | ||

| Pharmacological Agents | ||

| Gene Therapy | ||

| Other Supportive Treatments | ||

| By Application | Thalassemia | |

| Sickle Cell Disease | ||

| Other Hemoglobinopathies | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Transfusion | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Academic & Research Institutes | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the hemoglobinopathies treatment market?

The hemoglobinopathies treatment market size reached USD 11.45 billion in 2026 and is projected to hit USD 16.72 billion by 2031.

Which treatment segment is growing the fastest?

Gene therapy is the fastest-growing segment, forecast to expand at a 19.06% CAGR through 2031 thanks to recent CRISPR-based approvals.

Why is Asia–Pacific the most rapidly expanding region?

Asia-Pacific’s 9.43% CAGR stems from government-funded newborn screening, high carrier prevalence, and rising reimbursement support for advanced therapies.

How do high therapy costs affect market growth?

Prices exceeding USD 2 million per patient slow adoption in middle-income nations, moderating the global CAGR by an estimated 1.8 percentage points.

What role do specialty clinics play in future care delivery?

Specialty clinics combine multidisciplinary expertise and dedicated infrastructure, enabling them to deliver complex gene-therapy protocols and achieve the segment’s leading 9.54% CAGR.

Page last updated on: