Autoimmune Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

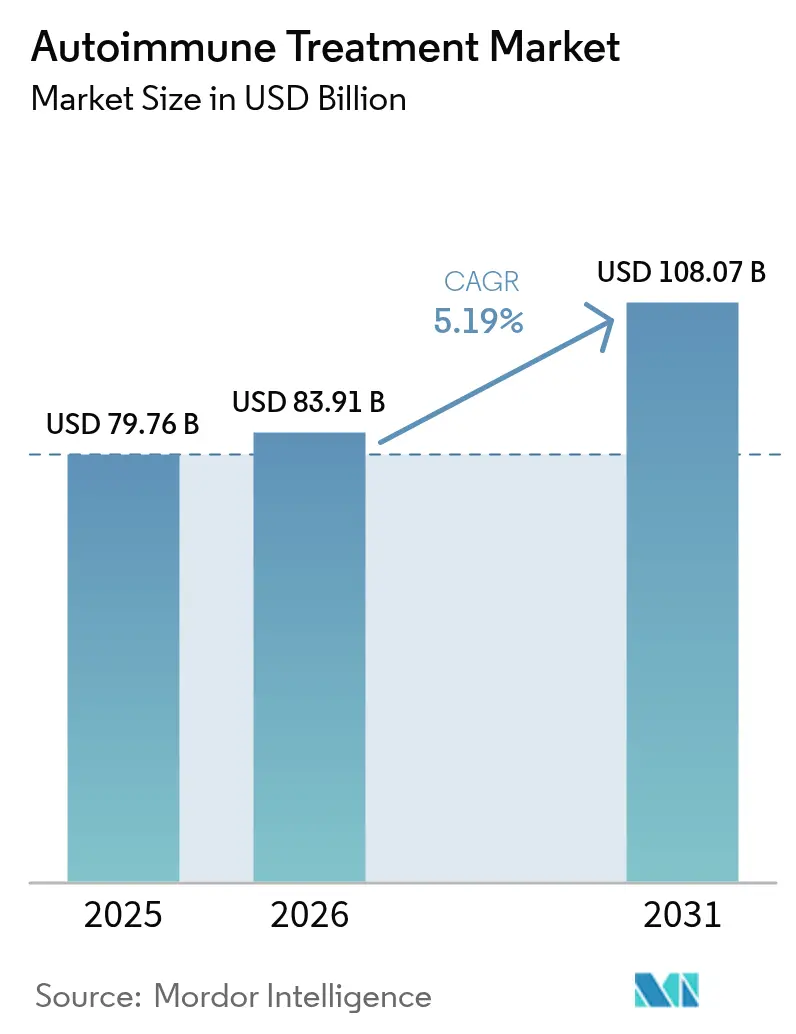

| Market Size (2026) | USD 83.91 Billion |

| Market Size (2031) | USD 108.07 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autoimmune Treatment Market Analysis by Mordor Intelligence

The autoimmune treatment market size is expected to grow from USD 79.76 billion in 2025 to USD 83.91 billion in 2026 and is forecast to reach USD 108.07 billion by 2031 at 5.19% CAGR over 2026-2031. The rising early-onset incidence, rapid uptake of biosimilars, and accelerated approvals of cell-based therapies are shifting the treatment model from broad immunosuppression to precision intervention. Breakthrough CAR-T applications in lupus and multiple sclerosis, combined with payer acceptance of outcome-based pricing, signal a reset in value perception across the autoimmune treatment market. At the same time, digital therapeutics enhance adherence and reduce relapse rates, adding a behavioral dimension to disease management. Regional dynamics remain pronounced, with North America accounting for the largest revenue pool, while the Asia-Pacific region delivers the fastest incremental growth, driven by expanding specialty-care infrastructure.

Key Report Takeaways

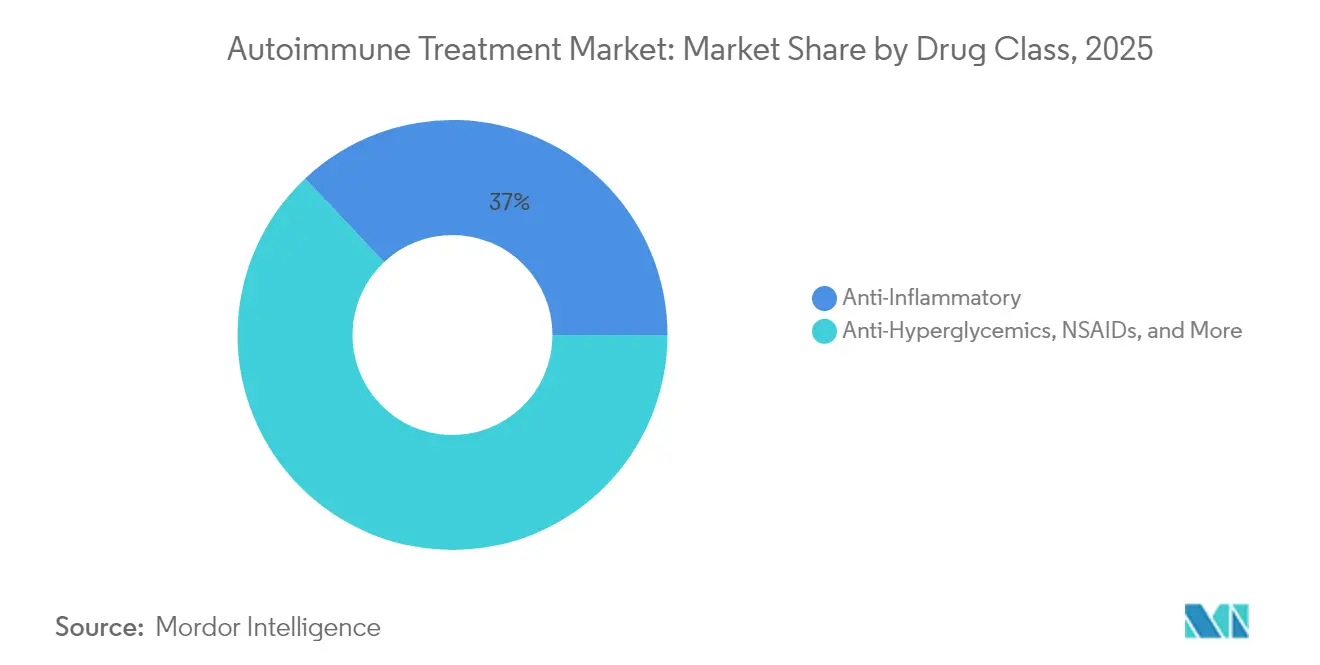

- By treatment type, anti-inflammatory agents held a 37.02% market share in the autoimmune treatment market in 2025, within the overall drug class segment; interferons were projected to have the highest CAGR at 8.69% through 2031.

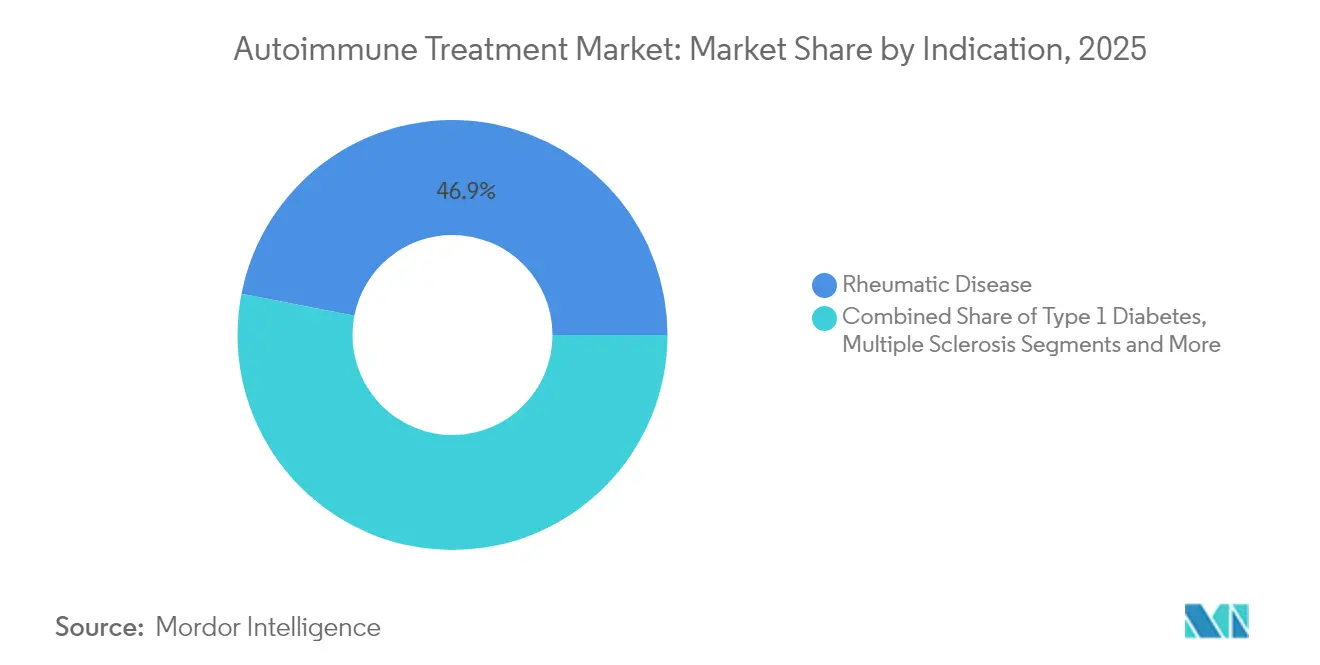

- By indication, rheumatic diseases led the autoimmune treatment market, accounting for a 46.92% share of the market size in 2025. In contrast, inflammatory bowel disease is forecast to expand at an 8.12% CAGR through 2031.

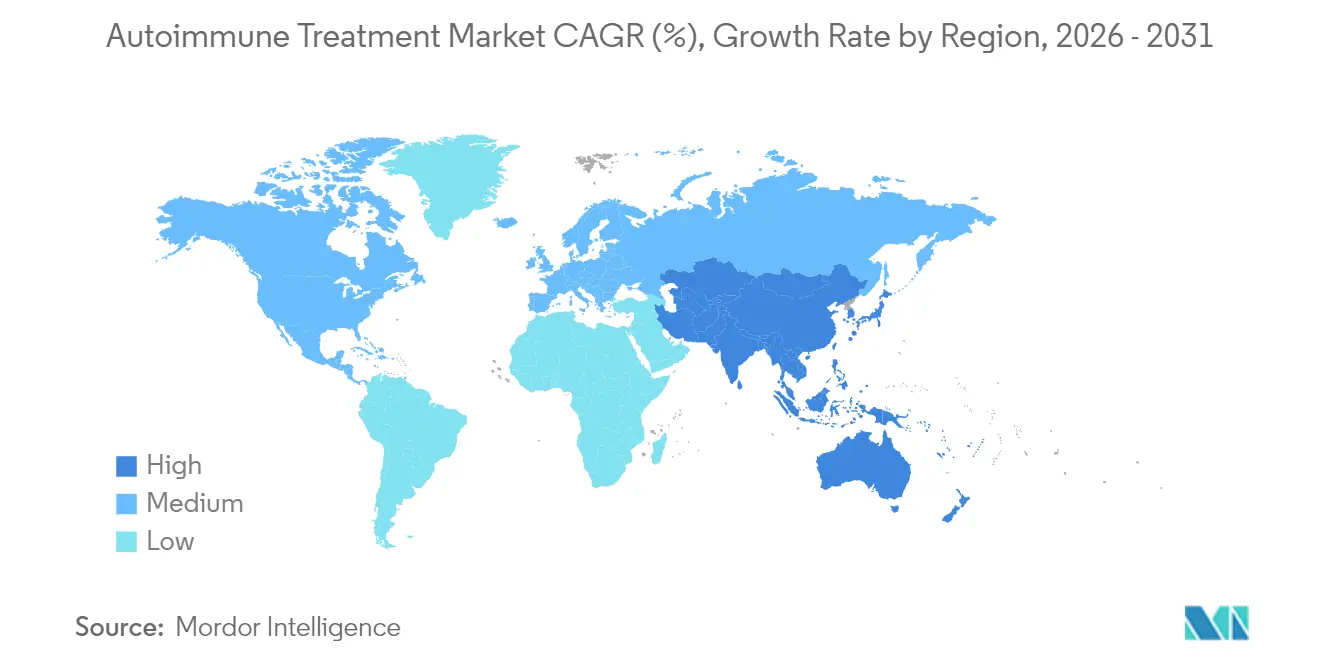

- By geography, North America contributed 42.35% of the 2025 revenue, while the Asia-Pacific region is expected to advance at an 8.46% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autoimmune Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Age-Standardised Rise In Early-Onset Autoimmune Incidence | +1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Biosimilar Wave Lowering Therapy Cost-Barriers | +0.8% | Global, with accelerated adoption in Asia-Pacific & emerging markets | Short term (≤ 2 years) |

| Oral Biologics Achieving Phase III Read-Outs | +0.6% | North America & EU core markets, expanding to APAC | Medium term (2-4 years) |

| Digital-Therapeutic-Plus-Drug Adherence Programs | +0.4% | North America & Europe leading, gradual APAC adoption | Long term (≥ 4 years) |

| Bispecific Antibody Approvals For Multi-Pathway Control | +0.3% | Global, with regulatory leadership in US & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Age-standardised rise in early-onset autoimmune incidence

Incidence among individuals aged 15-39 has climbed across rheumatoid arthritis, inflammatory bowel disease, and multiple sclerosis, extending lifetime therapy needs and magnifying the long-run value of safer chronic regimens[1]Syreen Goulmamine et al., “Autoimmune Health Crisis: An Inclusive Approach to Addressing Disparities in Women in the United States,” International Journal of Environmental Research and Public Health, mdpi.com. Screening programs now target adolescents, while payers prioritise treatments with proven durability. Manufacturers positioned with low-toxicity mechanisms gain larger cumulative revenue because patients initiate therapy earlier. The trend enlarges the addressable population for next-generation biologics and cell therapies, pushing the autoimmune treatment market toward higher long-term volumes.

Biosimilar wave lowering therapy cost-barriers

Adalimumab biosimilars seized 85% of dispensed volume within 18 months of launch, yielding projected system savings of USD 38.4 billion through 2025. Savings free payer budgets for novel assets such as bispecific antibodies or CAR-T constructs. Originators respond with value-added formulations and service packages, raising competitive intensity. Emerging markets that once relied on steroids are now integrating advanced biologics, thereby widening the global penetration of the autoimmune treatment market.

Oral biologics achieving Phase III read-outs

JAK inhibitors and other oral formats deliver injectable-level efficacy minus administration burden. AbbVie’s upadacitinib secured a giant cell arteritis label expansion in 2024, while Pfizer readies next-generation oral candidates for lupus and dermatomyositis[2]Pfizer Pipeline Update, “Pipeline Update_30JAN2024,” pfizer.com. Oral delivery supports sequential or combination regimens that were unworkable with parenteral dosing. Payers support adoption because reduced infusion costs offset higher drug spend, tightening alignment between clinical and economic value.

Digital-therapeutic-plus-drug adherence programs

AI-guided mobile platforms record symptoms, schedule dosing reminders, and connect patients with pharmacists, cutting avoidable flares and hospitalisations. Retail pharmacy layouts now feature digital-health kiosks next to specialty products, reflecting an ecosystem shift. Data generated by apps feed back into real-world evidence dossiers, accelerating reimbursement for newer agents. Over the forecast horizon, digital adjuncts evolve from optional add-ons to embedded elements of standard care across the autoimmune treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Payer Budget Fatigue Amid Oncology Biologic Spend | -0.7% | North America & Europe primarily, spreading to developed APAC markets | Short term (≤ 2 years) |

| Slow Guideline Updates For Novel MOAs In Emerging Markets | -0.5% | Emerging markets in APAC, Latin America, and MEA | Medium term (2-4 years) |

| Biomanufacturing Capacity Crunch For Cell-Based Therapies | -0.3% | Global, with acute impact in regions with limited CDMO infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Payer budget fatigue amid oncology biologic spend

Median oncology CAR-T invoice prices exceed USD 400,000 per course, diverting funds from chronic autoimmune lines[3]U.S. Department of Health and Human Services, “Pharmaceutical Supply Chain Intermediary Margins,” hhs.gov. The US and EU formularies are tightening prior-authorization criteria for high-cost biologics, introducing step-therapy hurdles that slow uptake. Manufacturers counter with outcomes-based rebates, but near-term volume can lag forecasts, shaving growth from the autoimmune treatment market.

Slow guideline updates for novel MOAs in emerging markets

Regulators in China and Brazil accelerate approvals, yet clinical practice committees often take two to three years to embed new mechanisms into local protocols, delaying broad prescribing. This gap prolongs use of conventional immunosuppressants even when superior options exist. Firms invest in physician-training roadshows and local data generation, but the lag still curbs addressable demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: entrenched anti-inflammatories versus surging interferons

Anti-inflammatory modalities, including TNF blockers, IL-6 antagonists, and JAK inhibitors, accounted for 37.02% of the 2025 global sales. Their broad efficacy across joint, skin, and bowel inflammation cements first-line placement. Fixed-dose subcutaneous pens and once-daily oral tablets reinforce adherence, protecting incumbents from immediate biosimilar cannibalisation. Interferons, however, register an 8.69% CAGR through 2031, driven by novel pegylated and oral formulations entering dermatomyositis and lupus pipelines. New-generation interferons exhibit improved tolerability, extending real-world persistence. The autoimmune treatment market size for interferon-based regimens is expected to climb to USD 9.74 billion by 2031, mirroring label expansions.

Concurrently, bispecific antibodies are emerging as dual-pathway suppressors, attracting blockbuster valuations; Merck paid USD 700 million for Curon’s B-cell depleter, CN201, in 2024. Pipeline diversity now includes tolerogenic cell therapies aimed at resetting immune balance instead of chronic suppression. First-in-class candidates in Type 1 diabetes aim to preserve beta-cell function, introducing a preventative approach within the autoimmune treatment market. Although early-stage, these modalities could reshape drug-class mix beyond the forecast window.

By Indication: rheumatic strength meets IBD momentum

The autoimmune treatment market allocates 46.92% of 2025 revenue to rheumatic disorders such as rheumatoid and psoriatic arthritis, supported by clear diagnostic criteria and long clinical experience. Disease-modifying antirheumatic drugs, TNF-α inhibitors, and JAK inhibitors sustain joint integrity, making rheumatology a predictable revenue pillar. Yet inflammatory bowel disease grows at an 8.12% CAGR through 2031, outpacing all other indications as biologics and novel gut-targeted small molecules gain traction. Positive long-term remission data and expanded reimbursement widen clinical adoption. The autoimmune treatment market size for IBD is projected to reach USD 23.41 billion by 2031, reflecting sustained double-digit uptake in Asia-Pacific urban centres. CAR-T investigations in refractory systemic lupus add a breakthrough narrative, as Adicet Bio’s ADI-100 won FDA Fast Track in February 2025. Emerging sub-segments such as autoimmune hepatitis and myasthenia gravis remain niche, yet they underscore the continuous broadening of the autoimmune treatment market.

A parallel shift emerges in multiple sclerosis, where high-efficacy B-cell depleters prolong relapse-free intervals. Although legacy interferon regimens persist, payer preference tilts toward agents with MRI-confirmed neuroprotection. Advanced imaging and blood-based biomarkers refine cohort selection, creating a foundation for precision dosing. These trends collectively stabilise overall indication diversity, cushioning revenue even when single lines face biosimilar erosion. As a result, the autoimmune treatment market sustains balanced exposure across high-volume and high-growth conditions.

Geography Analysis

North America delivered 42.35% of global revenue in 2025, supported by rapid diffusion of innovative modes of action, favourable reimbursement, and a dense clinical-trial ecosystem. The region’s flexible accelerated-approval frameworks placed nine autoimmune biologics on the market in the past two years, cementing first-mover advantage. Breakthrough CAR-T programs progress swiftly under FDA Fast Track designations, catalysing investor capital toward next-wave immunomodulation. Digital-health reimbursement parity laws encourage co-prescription of behaviour-change apps, reinforcing medication adherence and lowering relapse-associated costs.

Europe maintains balanced growth as price-volume agreements offset rising treatment intensity. The European Medicines Agency’s PRIME pathway shortens approval timelines for high-need assets such as bispecific antibodies, yet national health systems still impose budget caps that lengthen access negotiations. Biosimilar penetration tempers spending, freeing capacity for advanced options. Cross-country consortiums now aggregate demand for niche autoimmune indications, enhancing negotiating leverage and smoothing supply continuity.

Asia-Pacific stands out with an 8.46% CAGR through 2031, driven by demographic expansion, urbanisation, and regulatory harmonisation. China’s volume-based procurement slashes biologic prices, yet adds clauses for originators to supply real-world data, fostering evidence-led adoption. Japan’s early implementation of cell-processing standards underpins regional CAR-T trials beyond oncology. India and South-East Asia progress slower due to reimbursement fragmentation, but public-private partnerships invest in biologic manufacturing parks that promise local supply resilience. By 2031 the autoimmune treatment market in Asia-Pacific is forecast to reach USD 30.12 billion, providing a vital counterweight to mature regions.

South America and the Middle East & Africa contribute smaller revenue, yet steady health-budget growth and guideline modernisation improve uptake of biosimilars and select originator biologics. Strategies that bundle drug supply with physician-training modules accelerate diffusion in these price-sensitive settings. As a result, the global autoimmune treatment market achieves broader geographic balance, lowering dependence on single-region performance.

Competitive Landscape

Industry structure remains moderately concentrated. AbbVie, Pfizer, Johnson & Johnson, and other major players commanded significant revenue in 2024, while mid-cap innovators supplied differentiated pipelines, keeping competitive pressure intact. Over USD 15 billion in autoimmune-focused M&A closed between 2024 and 2025, underscoring a premium on first-in-class assets. Sanofi’s USD 1.9 billion purchase of Dren Bio’s CD20-targeting bispecific brought a dual-mechanism contender into late-stage lupus evaluation.

Platform convergence defines strategy; major firms embed machine-learning platforms to predict responder sub-groups, pruning attrition risk. Merck’s alliance network links academic cell-therapy labs with contract development and manufacturing organisations (CDMOs) to offset capacity bottlenecks for autologous products. Strategic rationale centres on assembling “toolbox” capabilities—ranging from nanoparticle delivery to synthetic biology switches—that support modular expansion across multiple autoimmune diseases. Smaller disruptors such as Kyverna and Cabaletta Bio focus on allogeneic CAR-T approaches that target chronic indications with single-dose curative intent.

Competitive differentiation increasingly involves service layers. Pfizer bundles adherence apps and pharmacogenomic testing with late-stage agents, aiming to reduce time-to-response variance. AbbVie pilots value-based contracts pegging rebates to sustained DAS-28 remission in rheumatoid arthritis, aligning economic incentives with functional outcomes. As biosimilars widen, originators cultivate brand stickiness via nurse-hotline access, at-home infusion services, and digital dashboards for physicians. Such holistic offerings shape the autoimmune treatment market beyond molecule-centric competition and reinforce moderate but stable concentration.

Autoimmune Treatment Industry Leaders

Pfizer Inc.

AbbVie Inc

Amgen Inc

Johnson & Johnson (Janssen)

Eli Lilly & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sanofi completed acquisition of Dren Bio's DR-0201, a CD20-directed bispecific antibody, for up to USD 1.9 billion to strengthen its immunology pipeline for refractory B-cell-mediated autoimmune diseases. The deal includes USD 600 million upfront with milestone-based payments, positioning Sanofi to compete in the emerging bispecific antibody market segment.

- February 2025: FDA granted Fast Track designation to Adicet Bio's CAR T-cell therapy ADI-100 for systemic lupus erythematosus treatment, recognizing the significant unmet medical need in refractory autoimmune conditions. This designation expedites regulatory review and reflects growing confidence in CAR-T applications beyond oncology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the autoimmune treatment market as worldwide prescription revenues from biologics, small-molecule drugs, and next-gen cell or gene therapies approved for chronic systemic and organ-specific autoimmune disorders and sold through hospital, retail, and online settings. We include innovator as well as biosimilar brands.

Scope exclusion: Devices, laboratory diagnostics, and over-the-counter anti-inflammatory remedies are outside this study.

Segmentation Overview

- By Treatment Type

- Drug Class

- Anti-Inflammatory

- Anti-Hyperglycemics

- NSAIDs

- Interferons

- Other Drugs

- Surgery

- Joint Replacement (Arthroplasty)

- Arthrodesis (Joint Fusion)

- Tendon Reconstruction

- Drug Class

- By Indication

- Rheumatic Disease

- Proctocolectomy / Colectomy

- Type 1 Diabetes

- Thyroidectomy

- Multiple Sclerosis

- Others

- Inflammatory Bowel Disease

- Other Indications

- Rheumatic Disease

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Over the past quarter, we interviewed rheumatologists, gastroenterologists, payors, and hospital pharmacy buyers across the United States, Germany, Japan, Brazil, and India. Their feedback on adherence, biosimilar switch rates, and likely uptake of JAK and CAR-T options filled data gaps and tuned key model assumptions.

Desk Research

Analysts began by pulling prevalence, incidence, and treated-patient counts from WHO Global Health Observatory, OECD health data, and United Nations population files. They then cross-checked guideline updates from bodies such as the American College of Rheumatology and the Crohn's & Colitis Foundation. We also reviewed national claims extracts that show biologic use by indication. Company 10-Ks, FDA labeling, patent families, and pricing disclosures were mapped against revenue splits taken from D&B Hoovers and Dow Jones Factiva. These sources anchor dosage strength, launch timing, and life-cycle price curves. The list is illustrative; many other reputable datasets fed our evidence stack.

Market-Sizing & Forecasting

Using a top-down prevalence-to-treated-patient framework, we started with country disease incidence, applied diagnosis and therapy penetration ratios, and multiplied by average selling prices to generate revenue pools. Supplier roll-ups and channel checks served as selective bottom-up mirrors that helped us adjust totals where gaps appeared.

Inputs such as biologic price erosion, biosimilar launch cadence, guideline-driven treatment duration, pipeline approval counts, insurance coverage shifts, and regional currency trends feed the model. Multivariate regression, stress-tested through three expert-validated scenarios, projects values to 2030.

Data Validation & Update Cycle

Each iteration passes anomaly flags, patient-based reasonableness checks, and peer review before sign-off. Our team refreshes the model annually, with interim updates triggered by major approvals, withdrawals, or reimbursement shocks, so clients receive the latest view.

Why our Autoimmune Treatment Baseline commands trust

Published numbers often diverge because firms bundle different drug baskets, apply varied discount curves, or refresh on dissimilar cadences.

Key gap drivers include whether transplant immunosuppressants or broad immunology drugs are counted, the aggressiveness of biosimilar deflation assumptions, and exchange-rate methodologies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 79.76 B (2025) | Mordor Intelligence | |

| USD 199.40 B (2023) | Global Consultancy A | Counts all immunology drugs plus transplant agents |

| USD 231.15 B (2025) | Industry Research Firm B | Uses list-price revenues and double counts pipeline sales |

| USD 103.18 B (2024) | Trade Journal C | Extrapolates U.S. growth globally and omits biosimilar erosion |

In short, Mordor Intelligence anchors its baseline on clearly defined therapies, patient-centric modeling, and an annual refresh cadence, giving decision-makers a balanced, transparent starting point that is easy to interrogate and repeat.

Key Questions Answered in the Report

What is the current size of the autoimmune treatment market?

The market generated USD 83.91 billion in 2026 and is projected to reach USD 108.07 billion by 2031.

Which indication is growing fastest within autoimmune therapeutics?

Inflammatory bowel disease leads with an expected 8.12% CAGR through 2031, surpassing growth in rheumatic and neurologic conditions.

How are biosimilars affecting market growth?

Biosimilar penetration, exemplified by adalimumab copies capturing 85% of prescriptions, frees up payer budgets and accelerates access to innovative treatments.

What role do CAR-T therapies play in autoimmune diseases?

CAR-T constructs, such as Adicet Bio’s ADI-100, have entered clinical trials for systemic lupus erythematosus and multiple sclerosis, offering potential remission in refractory cases.

Which region is expected to contribute most to future growth?

Asia-Pacific is set to post an 8.46% CAGR to 2031, driven by healthcare infrastructure upgrades and streamlined regulatory pathways.

Page last updated on: