Hemoglobinopathy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.21 Billion |

| Market Size (2031) | USD 20.73 Billion |

| Growth Rate (2026 - 2031) | 15.22% CAGR |

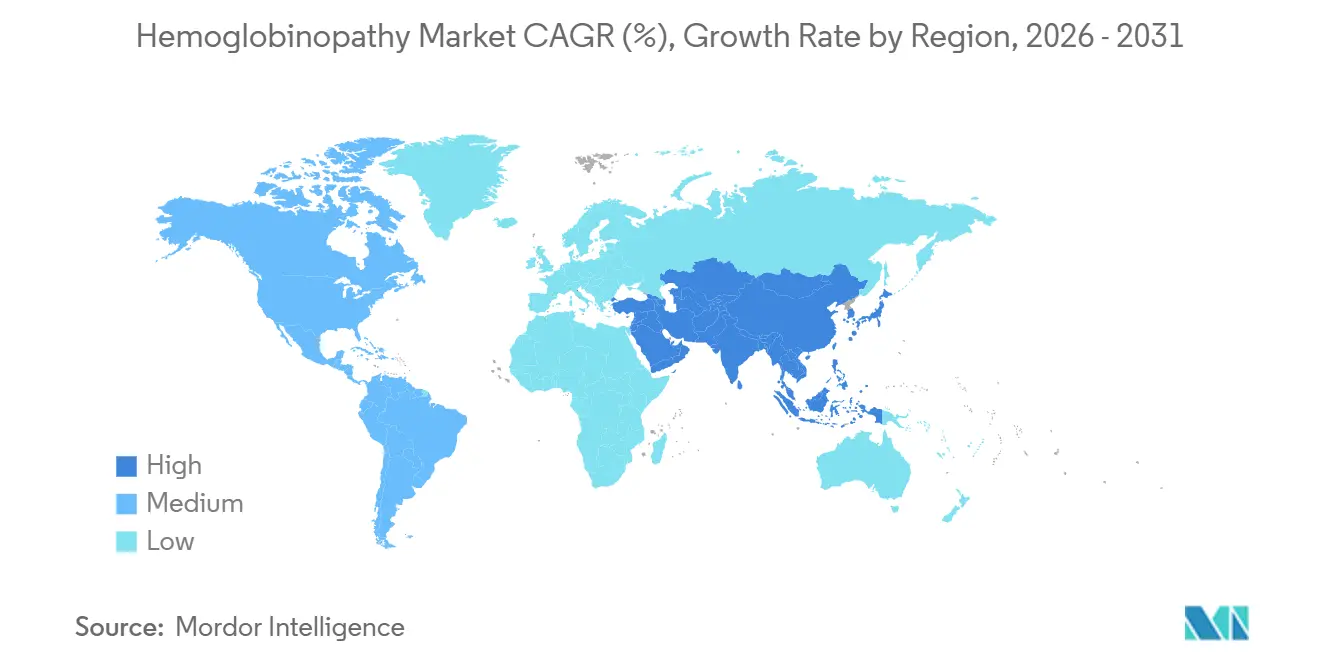

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemoglobinopathy Market Analysis by Mordor Intelligence

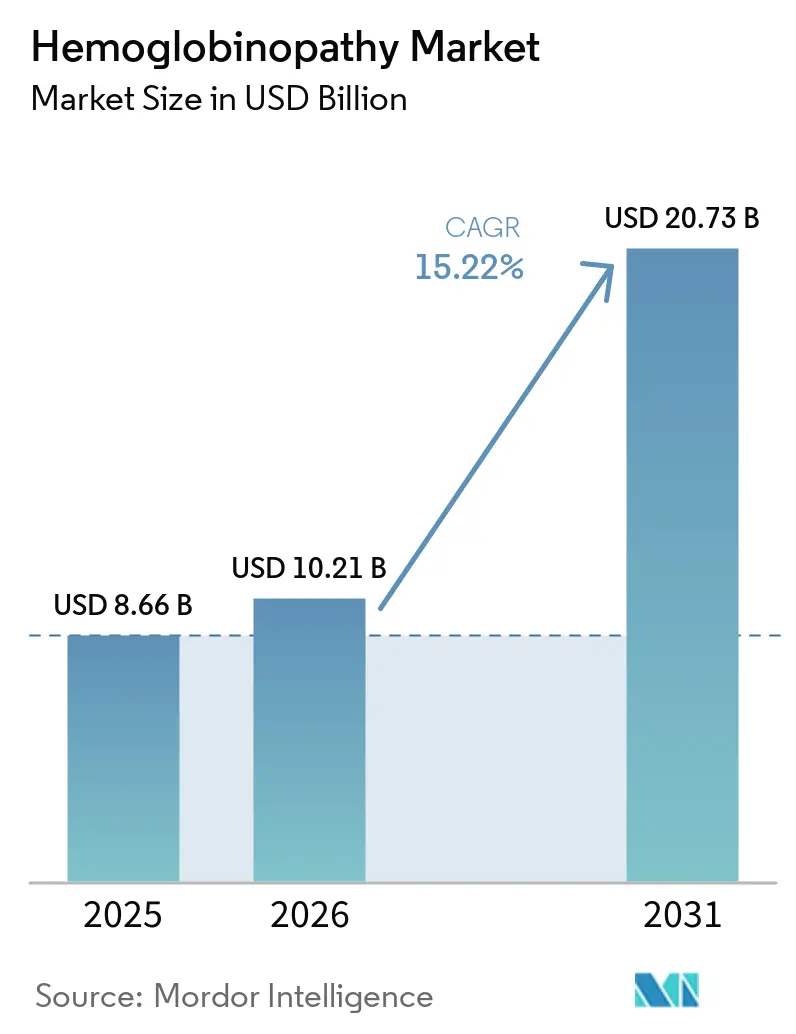

The Hemoglobinopathy Market size is expected to increase from USD 8.66 billion in 2025 to USD 10.21 billion in 2026 and reach USD 20.73 billion by 2031, growing at a CAGR of 15.22% over 2026-2031.

Strong clinical evidence for one-time gene-editing cures, expanding newborn-screening programs, and value-based reimbursement pilots are accelerating therapeutic adoption across major healthcare systems. Early commercial uptake of Casgevy and Lyfgenia, priced at USD 2.2 million and USD 3.1 million, respectively, confirms payer willingness to fund curative options when outcomes-linked contracts are in place. North America remains the primary revenue generator owing to concentrated specialist centers and Medicaid-driven access schemes, while the Asia Pacific is adding the largest absolute patient volumes on the back of national elimination missions and low-cost molecular diagnostics. Competitive strategies now revolve around manufacturing scale-outs, real-world evidence collection, and multi-stakeholder financing models that limit budget shocks yet preserve innovation incentives. The resulting environment gives incumbents and pure-play gene-therapy developers a sizable runway to embed next-generation assets and capture incremental share within the widening hemoglobinopathy market.

Key Report Takeaways

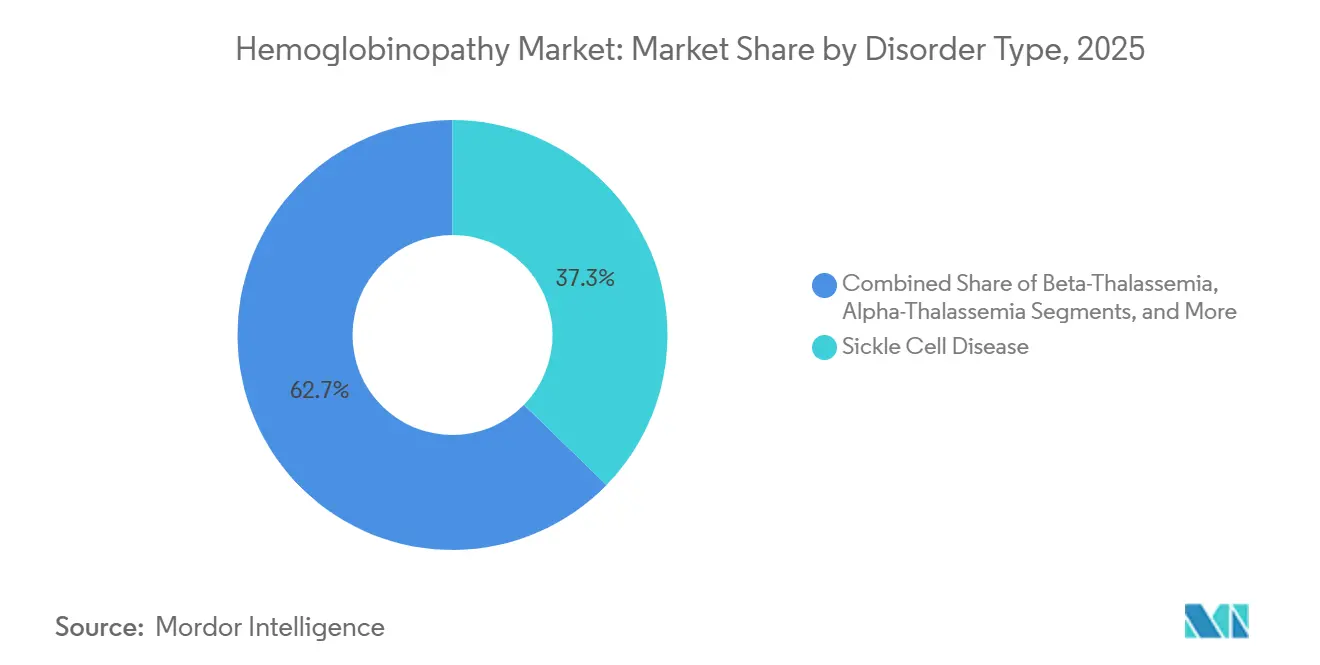

- By disorder type, sickle cell disease held 37.31% of the hemoglobinopathy market share in 2025, while β-thalassemia is projected to record the fastest 16.03% CAGR through 2031.

- By product, therapy type accounted for 56.84% of the hemoglobinopathy market size in 2025; the diagnosis technique segment is advancing at a 22.05% CAGR to 2031.

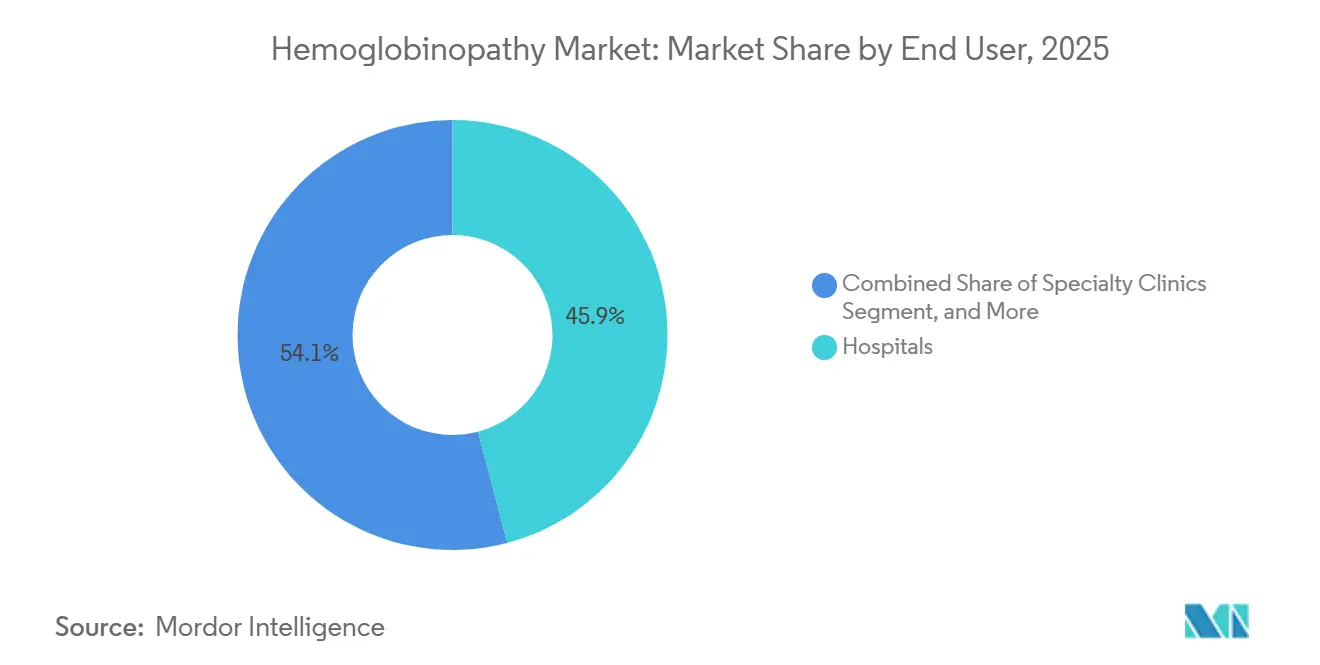

- By end user, hospitals captured a 45.88% share of the hemoglobinopathy market in 2025, and specialty clinics and transfusion centers posted the highest 19.35% CAGR to 2031.

- By geography, North America commanded 29.84% of the hemoglobinopathy market share in 2025; Asia Pacific exhibits the quickest 17.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hemoglobinopathy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of SCD & Thalassemia | +2.10% | Global, with concentration in Sub-Saharan Africa, Mediterranean, Middle East | Long term (≥ 4 years) |

| Regulatory Approvals Of Disease-Modifying Drugs | +2.80% | North America & EU, expanding to Asia Pacific | Medium term (2-4 years) |

| Breakthrough Gene-Editing Cures Attract Investment | +3.20% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion Of National Newborn-Screening Programs | +1.90% | Global, with rapid adoption in emerging markets | Long term (≥ 4 years) |

| Annuity-Based Reimbursement For Gene Therapies | +2.40% | North America & EU, pilot programs in select markets | Short term (≤ 2 years) |

| AI-Enabled Low-Cost Carrier Screening Platforms | +1.80% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of SCD & Thalassemia

Rising birth rates, migration, and better disease detection keep pushing global hemoglobinopathy numbers upward. Close to 8 million people now live with sickle cell disease, and the toll is heaviest in Sub-Saharan Africa, where more than 500 children die each day for lack of timely care.[1]World Health Organization, “Sickle-cell disease,” who.int Population growth in high-burden regions keeps the treatment gap wide even as new screening programs uncover cases that once went unnoticed. For drug makers, this unmet need translates into a sizeable and growing market, especially for therapies that can be delivered in settings with limited resources.

Regulatory Approvals of Disease-Modifying Drugs

Between 2023 and 2024, the U.S. FDA cleared several first-in-class therapies—including CRISPR-based products—that act on the root cause of hemoglobinopathies instead of masking symptoms. Final guidance on genome-editing products, issued in January 2024, gives developers a clearer path to approval.[2]Federal Register, “Human Gene Therapy Products Incorporating Genome Editing,” federalregister.gov Similar moves by the European Medicines Agency, coupled with orphan-drug and accelerated-review incentives, trim development time and strengthen the business case for niche but high-impact treatments.

Breakthrough Gene-Editing Cures Attract Investment

CRISPR-Cas9’s transition from lab to clinic has unlocked record funding for hemoglobinopathy programs. Gene editing now posts the fastest growth rate in the field at 22% CAGR. Vertex Pharmaceuticals, for example, has begun booking revenue from its one-time therapy Casgevy while adding treatment centers worldwide. Durable follow-up data reinforce investor confidence, and partnering with contract manufacturers such as Lonza reduces scale-up risk.

Annuity-Based Reimbursement for Gene Therapies

Million-dollar price tags once threatened access, but outcomes-linked payment plans are changing the equation. In the United States, the CMS Cell and Gene Therapy Access Model lets states negotiate collective deals and spread payments over six years, tying them to real-world results.[3]Centers for Medicare & Medicaid Services, “Cell and Gene Therapy Access Model Fact Sheet,” cms.govMichigan’s agreement with bluebird bio for Lyfgenia rebates the drug’s cost if hospitalizations fail to drop, easing budget pressure while keeping patients covered.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-million-dollar therapy prices strain payers | -2.70% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Weak hematology infrastructure in LMICs | -1.90% | Sub-Saharan Africa and other low-income regions | Long term (≥ 4 years) |

| Regulatory uncertainty on off-target edits | -1.40% | Global, variable by regulatory agency | Medium term (2-4 years) |

| Manufacturing scalability constraints | -1.03% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-Million-Dollar Therapy Prices Strain Payers

List prices for approved gene therapies fall between USD 2.2 million and USD 3.1 million per patient, a level that many budgets cannot absorb without cutting other services. Faced with such costs, payers often impose strict coverage criteria and multi-step authorization reviews, slowing treatment starts even when the clinical need is urgent. Medicaid bears much of the burden because a large share of sickle-cell patients rely on that program, yet state budgets leave limited room for high-ticket therapies. Outcomes-based contracts help, but hospitals must still finance the full procedure upfront, squeezing cash flows and discouraging additional treatment-center build-outs.

Weak Hematology Infrastructure in Low- And Middle-Income Countries

Many countries with the highest sickle-cell and thalassemia rates lack enough trained hematologists, advanced labs, or certified infusion suites. Gene therapies require clean-room handling, cold-chain logistics, and close post-procedure monitoring—capabilities that few facilities in these regions can provide. Supply bottlenecks further impede access when vector shipments or apheresis kits cannot clear customs quickly. This gap between need and delivery capacity widens global health disparities and limits the commercial reach of next-generation cures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disorder Type: SCD Dominance Drives Market Growth

Sickle cell disease held 37.31% hemoglobinopathy market share in 2025, a level supported by the immediate eligibility of this patient group for the first approved CRISPR-based curative therapies. Newborn-screening mandates in high-income countries and large Medicaid pools in the United States sustain demand visibility. At the same time, private-equity-backed programs aim to replicate this model in Latin America and the Caribbean. β-thalassemia, projected to grow at 16.03% CAGR through 2031, benefits from the same therapeutic platforms adapted to different globin-gene mutations, and pilot sites are already onboarding adult patients before expanding to pediatric cohorts. Alpha-thalassemia remains small but attractive for pipeline expansion as diagnostic resolution improves.

Market entrants are building consortia with regional reference laboratories to triage patients directly into clinical sites, a move that compresses referral times and maximizes procedure capacity. Novartis’s collaboration with the Bill & Melinda Gates Foundation illustrates further commitment to simplified in-vivo editing intended for low-resource settings, potentially repositioning the company as a gateway provider when large-volume, lower-price opportunities emerge.

By Product: Gene Therapy Transforms Treatment Paradigms

Pharmacological agents retained 56.84% of the hemoglobinopathy market size in 2025, owing to established guidelines and oral dosing convenience. Hydroxyurea remains the first-line disease-modifier in many national formularies, but pay-for-performance contracts are tilting mindshare toward curative interventions. Nonetheless, diagnosis techique is scaling at a 22.05% CAGR because gene-therapy eligibility requires single-nucleotide resolution of underlying mutations. Central laboratories are deploying high-throughput next-generation sequencing while regional hospitals adopt PCR-based panels validated under the Clinical Laboratory Improvement Amendments framework. AI-assisted interpretation software now provides mutation reports within hours, compressing the diagnostic-to-treatment timeline and creating a self-reinforcing cycle of demand for both tests and therapies.

Bone marrow transplantation continues as an option for matched-sibling cases. Still, it is constrained by donor availability and graft-versus-host risk profiles, driving interest in autologous edited stem-cell regimens. Supportive blood transfusions and iron-chelation protocols serve as transitional care pathways, preserving patient health until definitive therapies are feasible. Point-of-care rapid kits, often smartphone-connected, target rural clinics and community screening events, increasing diagnostic penetration in areas with minimal laboratory infrastructure. High-performance liquid chromatography remains a complementary method for quantitative hemoglobin sub-typing, ensuring clinicians can corroborate genetic findings with functional data.

By End User: Specialty Centers Drive Advanced Care

Hospitals accounted for 45.88% hemoglobinopathy market size in 2025 because acute pain crises and transfusion management still anchor many patient journeys. That said, specialty clinics and transfusion centers are posting the fastest 19.35% CAGR as payers insist on credentialed facilities for high-cost gene-therapy infusions. Vertex authorized roughly 75 global centers within twelve months of Casgevy approval, a template that bluebird bio and emerging competitors are replicating. Diagnostic laboratories act as both referral hubs and long-term monitoring partners, especially under six-year outcomes-tracking clauses in Medicaid agreements.

Academic institutes fulfill two roles: hosting first-in-human trials for next-generation editing techniques and training the hematology workforce necessary to keep pace with rising global procedure volumes. The dual research-clinical function allows rapid translation of novel protocols into commercial practice, further fueling the growth of the hemoglobinopathy market.

Geography Analysis

North America’s 29.84% revenue share in 2025 reflects robust Medicaid coverage for sickle cell disease, concentration of certified gene-therapy centers, and a well-established philanthropic ecosystem that subsidizes travel and lodging for eligible patients. Federal support through the Cell and Gene Therapy Access Model lowers payer risk, encouraging additional states to sign outcomes-based contracts and thereby enlarging the treated population.

Europe follows with steady adoption, aided by the European Medicines Agency’s conditional approval pathway that allowed earlier market entry for ex vivo gene additions. Budget discipline tempers procedure counts, yet multi-country tender frameworks give manufacturers visibility into volume commitments. Notably, four national health services are piloting annuity payments where budgets are reimbursed over time, replicating the United States model to manage headline prices.

Asia Pacific is advancing at a 17.28% CAGR. India and China together account for the region’s bulk demand due to high birth prevalence, government-funded newborn screening, and emergent middle-class willingness to self-pay for premium care. Public-private partnerships are converting tertiary hospitals into specialized editing centers, ensuring future scale. Southeast Asian nations are also adopting AI-enabled carrier-screening to inform family planning, enlarging the catchment for the hemoglobinopathy market.

The Middle East and Africa host the highest disease prevalence yet the lowest procedure penetration. Opportunities exist for modular clean-room suites and mobile apheresis units that can leapfrog legacy infrastructure constraints. Brazil anchors South American growth with a unified hemoglobinopathy registry and a fast-growing transplant network, signaling rising regional demand as regulatory approvals expand.

Competitive Landscape

Vertex Pharmaceuticals commands lead visibility through the first CRISPR-Cas9 approval, complemented by a co-development pact with CRISPR Therapeutics that distributes risk and manufacturing burden. Novartis retains a strong pharmacological franchise and is developing in vivo editing assets to hedge against ex vivo displacement. Pfizer leverages a broad hematology sales force to maintain hydroxyurea and voxelotor uptake.

Bluebird Bio, now controlled by Carlyle and SK Capital, offers two commercial gene-addition therapies and a pipeline of lentiviral upgrades. Private equity backing accelerates plant retrofits for suspension culture, cutting the cost of goods and positioning the company for volume expansion under value-based contracts. Smaller innovators like Graphite Bio and Beam Therapeutics are pursuing base-editing approaches that promise reduced off-target risk, though commercial timelines extend beyond 2027.

Strategic moves center on supply security and payer alignment. Vertex’s long-term supply deal with Lonza secures vector capacity for anticipated scale-up. Bluebird Bio entered state-by-state outcomes-based agreements that rebate costs if hospitalization rates fail predefined thresholds. Novartis collaborates with Gates Foundation researchers to engineer simplified one-shot in-vivo edits for high-burden, low-income markets, a program that could unlock new volume segments and soften price-sensitivity concerns.

Technology adoption trends favor CRISPR platforms for their modular design and manufacturing reproducibility. As follow-up data accumulate, existing label-holders are expected to file for expansion into pediatric cohorts, further entrenching their competitive positions within the hemoglobinopathy market.

Hemoglobinopathy Industry Leaders

Pfizer Inc.

Bluebird Bio

Vertex Pharmaceuticals

Bristol Myers Squibb

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CRISPR Therapeutics outlined its strategic priorities and anticipated milestones for 2026, reinforcing its focus on advancing transformative gene-based medicines for serious diseases.

- January 2025: bluebird bio announced a definitive agreement to be acquired by Carlyle and SK Capital for USD 3.00 per share plus contingent value rights, providing capital to scale commercial delivery of gene therapies

- January 2025: bluebird bio confirmed participation in the CMS Cell and Gene Therapy Access Model, offering outcomes-based agreements for LYFGENIA through state Medicaid agencies, with more than half of U.S. states affirming coverage.

Global Hemoglobinopathy Market Report Scope

The Hemoglobinopathy Market refers to the global industry ecosystem encompassing the diagnosis, treatment, and management of inherited blood disorders caused by structural abnormalities or reduced production of hemoglobin. These conditions include sickle cell disease, beta-thalassemia, alpha-thalassemia, and other rare hemoglobin variants.

The hemoglobinopathy market report is segmented by disorder type, product, end user, and geography. By disorder type, the market is segmented into sickle cell disease, beta-thalassemia, alpha-thalassemia, and other Hb variants. By product, the market is segmented into therapy type (pharmacological agents, gene therapy, bone-marrow/stem-cell transplant, blood transfusion & iron chelation), diagnosis technique (hemoglobin electrophoresis, high-performance liquid chromatography (HPLC), molecular genetic testing (PCR / NGS), point-of-care rapid tests, others). By end user, the market is segmented into hospitals, specialty clinics, diagnostic laboratories, and academic and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Sickle Cell Disease (SCD) |

| Beta-Thalassemia |

| Alpha-Thalassemia |

| Other Hb Variants (Hb C, Hb E, etc.) |

| Therapy Type | Pharmacological Agents |

| Gene Therapy | |

| Bone-Marrow / Stem-Cell Transplant | |

| Blood Transfusion & Iron Chelation | |

| Diagnosis Technique | Hemoglobin Electrophoresis |

| High-Performance Liquid Chromatography (HPLC) | |

| Molecular Genetic Testing (PCR / NGS) | |

| Point-of-Care Rapid Tests | |

| Others |

| Hospitals |

| Specialty Clinics & Transfusion Centers |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disorder Type | Sickle Cell Disease (SCD) | |

| Beta-Thalassemia | ||

| Alpha-Thalassemia | ||

| Other Hb Variants (Hb C, Hb E, etc.) | ||

| By Product | Therapy Type | Pharmacological Agents |

| Gene Therapy | ||

| Bone-Marrow / Stem-Cell Transplant | ||

| Blood Transfusion & Iron Chelation | ||

| Diagnosis Technique | Hemoglobin Electrophoresis | |

| High-Performance Liquid Chromatography (HPLC) | ||

| Molecular Genetic Testing (PCR / NGS) | ||

| Point-of-Care Rapid Tests | ||

| Others | ||

| By End User | Hospitals | |

| Specialty Clinics & Transfusion Centers | ||

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the hemoglobinopathy market?

The hemoglobinopathy market size reached USD 10.21 billion in 2026 and is projected to hit USD 20.73 billion by 2031.

Which product segment is growing the fastest?

Diagnostic segment is expanding at a 22.05% CAGR through 2031, driven by one-time CRISPR-based cures gaining regulatory approval and payer acceptance.

How large is the sickle cell disease sub-market?

Sickle cell disease captured 37.31% hemoglobinopathy market share in 2025, making it the single largest disorder segment.

Why is Asia Pacific considered the most attractive growth region?

Asia Pacific posts a 17.28% CAGR through 2031 thanks to high disease prevalence, government-funded newborn screening and rapid expansion of molecular diagnostic capacity.

What are the main barriers limiting wider gene-therapy adoption?

Up-front treatment prices exceeding USD 2 million, limited specialist centers in low-income countries and ongoing regulatory scrutiny over off-target edits remain key constraints.

Page last updated on: