Warm Autoimmune Hemolytic Anemia Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

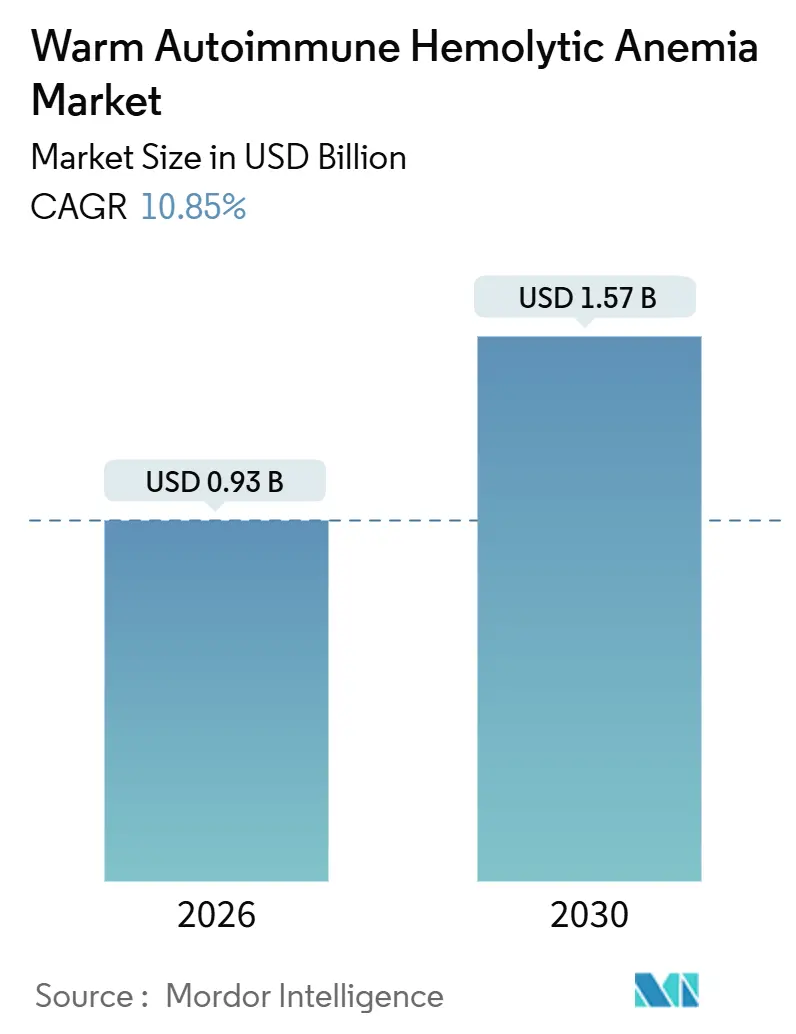

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2030) | 10.85% CAGR |

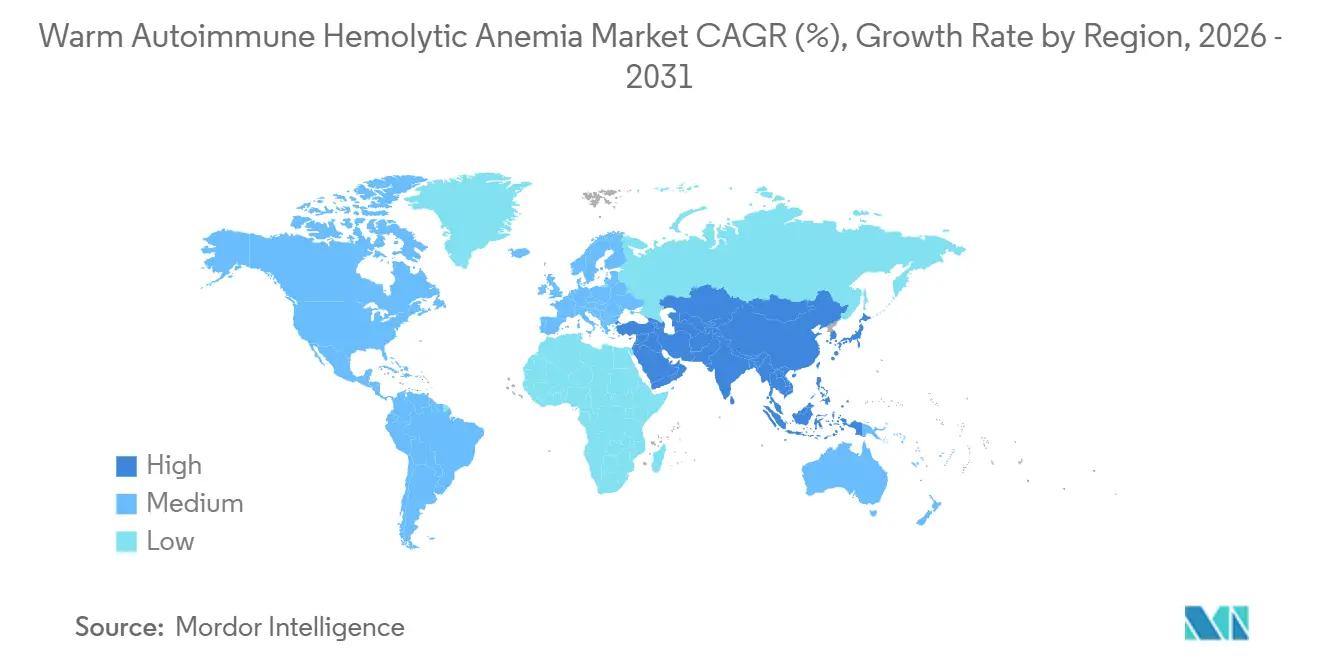

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Warm Autoimmune Hemolytic Anemia Market Analysis by Mordor Intelligence

The Warm Autoimmune Hemolytic Anemia Market size is estimated at USD 0.93 billion in 2026, and is expected to reach USD 1.57 billion by 2031, at a CAGR of 10.85% during the forecast period (2026-2031).

Mounting adoption of targeted biologics, faster orphan-drug review lanes, and AI-enabled laboratory workflows together create an inflection point that is accelerating diagnosis and treatment uptake. The shift from empiric corticosteroid monotherapy toward neonatal Fc receptor and Bruton tyrosine kinase inhibition is reshaping clinical pathways as physicians look for durable, steroid-sparing responses. Hospital reliance declines as outpatient infusion centers master rituximab protocols and subcutaneous FcRn inhibitors, while regional insurance reforms in China and India start to subsidize second-line biologics. Competitive momentum intensifies as mid-sized biotechs leverage orphan exclusivity to challenge legacy immunosuppressants, and real-world registry data sharpen epidemiological assumptions, expanding the pool of treatable patients.

Key Report Takeaways

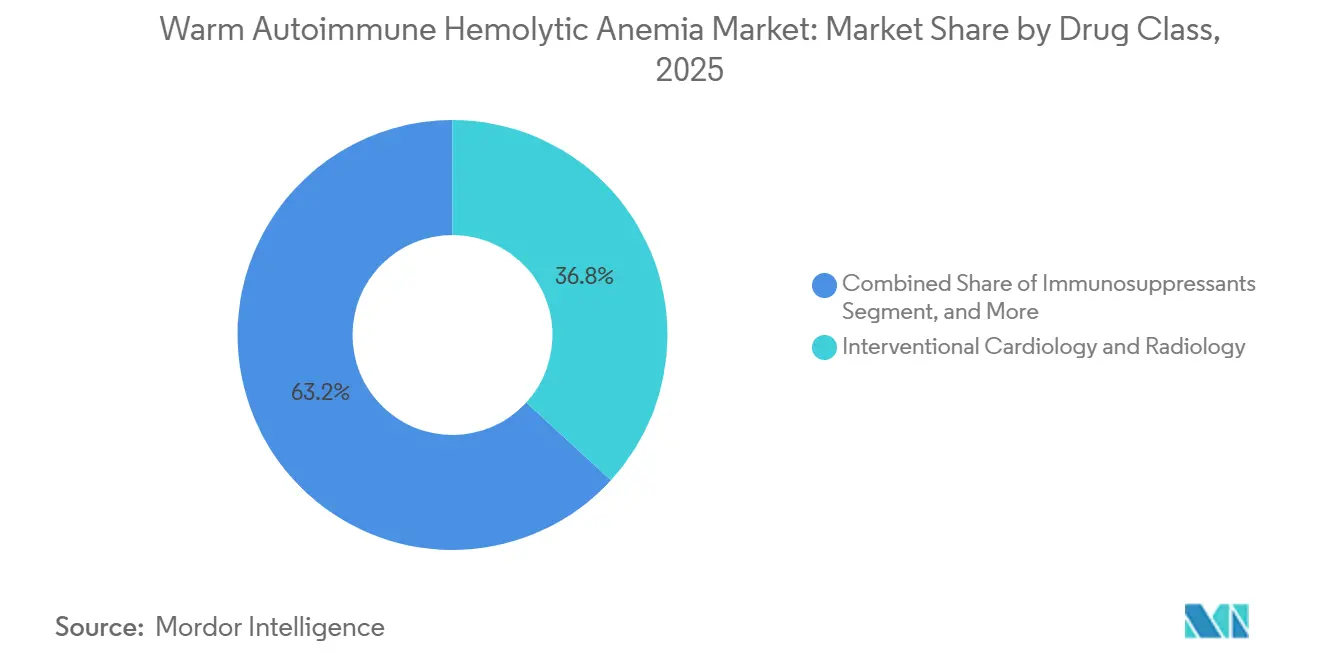

- By drug class, corticosteroids held 36.81% of the warm autoimmune hemolytic anemia market share in 2025, yet monoclonal antibodies are advancing at a 11.07% CAGR through 2031.

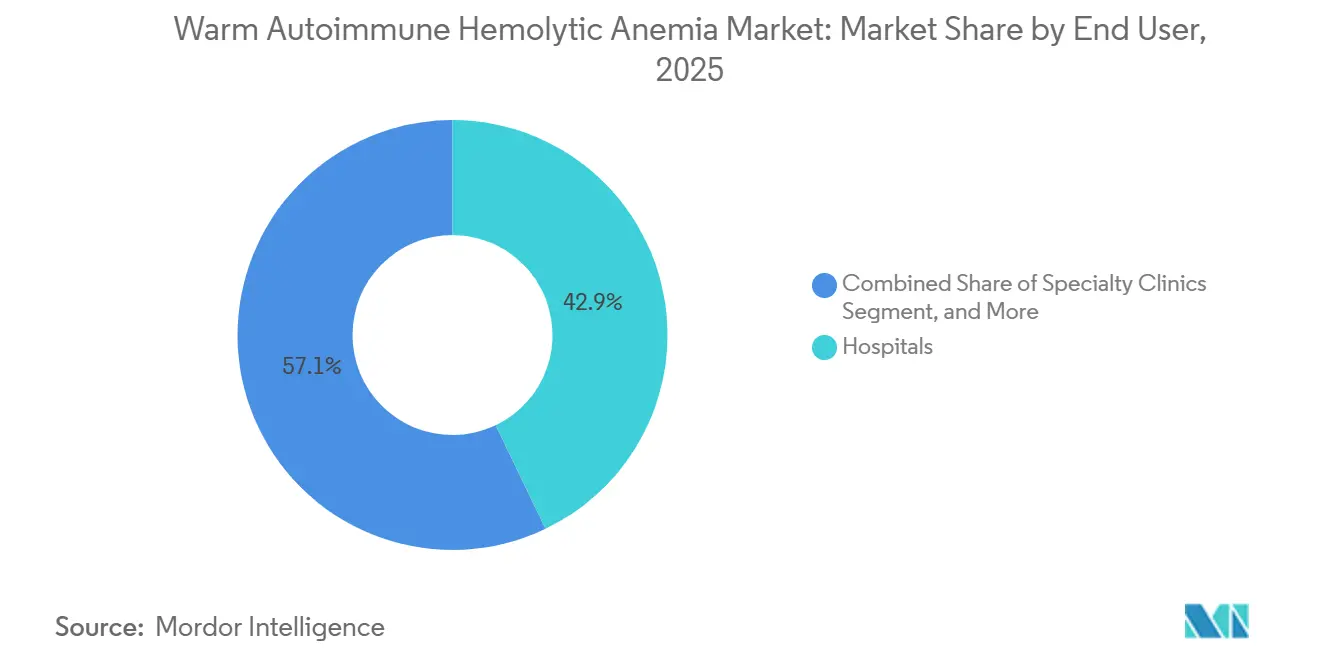

- By end user, hospitals captured 42.87% of the warm autoimmune hemolytic anemia market size in 2025, while specialty clinics are forecast to expand at a 12.15% CAGR to 2031.

- By geography, North America led with 41.93% market share for warm autoimmune hemolytic anemia in 2025, but Asia-Pacific is poised for a 13.03% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Warm Autoimmune Hemolytic Anemia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Off-Label Biologics | +1.8% | North America and Europe, spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Accelerated FDA Orphan-Drug Incentives | +2.1% | Global, with precedent in United States and European Union | Short term (≤ 2 years) |

| Increasing Autoimmune Prevalence in Aging Cohorts | +1.5% | Global, most pronounced in high-income aging societies | Long term (≥ 4 years) |

| Launch of FcRn and Complement Inhibitors | +2.3% | North America and Europe first, Asia-Pacific after approvals | Medium term (2-4 years) |

| AI-Driven Earlier Diagnosis in Hematology Labs | +1.2% | North America, Europe, urban China and India | Medium term (2-4 years) |

| Growing Patient-Advocacy Registries | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Off-Label Biologics

Rituximab is prescribed off-label in close to 40% of second-line cases across North America and Europe, a pattern grounded in randomized data that showed 75% complete responses at 12 months when combined with prednisolone compared with 36% for steroids alone. Growing confidence in anti-CD20 activity now shortens the interval between steroid failure and biologic initiation. Uptake of obinutuzumab and ofatumumab expands the anti-CD20 class as clinicians rotate antibodies to salvage incomplete responders. Splenectomy referrals at tertiary European centers fell by 30% between 2020 and 2025, as durable biologic regimens delayed irreversible surgery. Recognition by the FDA through Breakthrough Therapy status for nipocalimab codifies this off-label momentum by signaling a clear regulatory pathway toward formal indications.[1]U.S. FDA, “Breakthrough Therapy Designations,” fda.gov

Accelerated FDA Orphan-Drug Incentives

Seven-year exclusivity, tax credits, and fee waivers have spurred a surge in rare-disease filings. Sanofi’s rilzabrutinib received orphan drug designation in April 2025 after Phase 2b data showed 64% hemoglobin response rates without rescue steroids.[2]Sanofi, “Rilzabrutinib Orphan Designation,” sanofi.com Comparable incentives in Europe supply 10-year exclusivity, motivating mid-size developers who can recoup costs in small populations. Complement inhibitor pegcetacoplan illustrates both promise and challenge: early signals, yet variable benefit, in an 11-patient cohort underscore how modest sample sizes can compromise statistical power.

Increasing Autoimmune Prevalence in Aging Cohorts

Immunosenescence drives a second incidence peak after age 60, and Western registries recorded a 25% rise in diagnoses among adults over 65 between 2015 and 2024. Roughly half of cases remain idiopathic, but lymphoid malignancies that co-manifest with warm AIHA grow with age, magnifying demand for therapies that limit steroid toxicity. Japan’s health ministry documented a 15% annual increase in hospital admissions for patients 70-plus in 2024, prompting guidelines that encourage the earlier use of steroid-sparing agents.

Launch of FcRn & Complement Inhibitors

FcRn blockade accelerates IgG catabolism and offers a mechanistic alternative to B-cell depletion. Interim Phase 3 data from the ENERGY study showed a 60% median IgG drop within four weeks, translating to 2 g/dL hemoglobin gains in responders. Case reports of efgartigimod in rituximab-refractory patients strengthen the appeal of this class. Complement inhibition brings mixed results because warm AIHA is largely extravascular, yet pegcetacoplan maintains momentum under orphan protection, and clinicians now stratify DAT patterns to forecast complement responsiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Commercial Attractiveness for Big Pharma | -1.4% | Global, deters mega-cap entrants | Long term (≥ 4 years) |

| Diagnostic Complexity and Under-Diagnosis | -1.1% | Asia-Pacific, Latin America, Middle East and Africa, rural U.S. | Medium term (2-4 years) |

| Safety Concerns Over Chronic Immunosuppression | -0.8% | Global, amplified in elderly cohorts | Medium term (2-4 years) |

| High Cost of Biologics in Emerging Markets | -1.3% | Asia-Pacific outside Japan, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Commercial Attractiveness for Big Pharma

Global prevalence of about 17 per 100,000 yields a tiny addressable base, discouraging mega-cap firms that target blockbuster returns. Rigel’s fostamatinib generated only USD 42 million in 2024 despite orphan exclusivity and then failed to meet its Phase 3 endpoint, illustrating financial and clinical risk.[3]Rigel Pharmaceuticals, “Form 10-K,” ir.rigel.com Larger companies have diverted resources toward higher-prevalence immunology, leaving room for agile biotechs, yet their smaller sales teams slow penetration in emerging economies.

Diagnostic Complexity & Under-Diagnosis

DAT-negative cases require flow cytometry or monocyte monolayer assays, which are scarce outside tertiary centers. An Indian study reported 47% misclassification of hemolytic anemia as iron-deficiency or thalassemia trait in community hospitals, delaying treatment. Even in the United Kingdom, a 28-day median delay persists between primary presentation and diagnosis, leading to unnecessary transfusions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Steroid-Sparing Shift Accelerates Biologic Uptake

Monoclonal antibodies are projected to grow at 11.07% CAGR from 2026 to 2031, outpacing the overall warm autoimmune hemolytic anemia market. Corticosteroids maintained a 36.81% share in 2025 but now decline as hematologists prize durable remission and reduced toxicity. The Danish trial that combined rituximab with prednisolone delivered a 39-point absolute increase in complete responses, anchoring anti-CD20 agents as standard second-line therapy. Immunosuppressants cede ground as FcRn inhibitors and BTK blockers promise targeted mechanisms with fewer off-target effects. IVIG remains a niche bridge during hemolytic crises, yet plasma shortages limit volume gains. Splenectomy keeps waning because biologics defer irreversible surgery.

Emerging therapies reshape expectations. Sanofi’s oral rilzabrutinib offers convenience that could tilt share if Phase 3 data confirm efficacy and safety. Johnson & Johnson’s nipocalimab introduces an FcRn blueprint that accelerates IgG clearance and may dominate relapsed settings. Pipeline CAR-T constructs aim for one-time cellular re-education, though the feasibility in low-incidence diseases remains to be proven. Collectively, these modalities expand therapeutic options, supporting steady growth in the autoimmune hemolytic anemia market.

By End User: Specialty Clinics Gain Share Through Outpatient Infusion

Hospitals accounted for 42.87% of 2025 revenue because acute hemolytic crises require transfusion and intensive monitoring, yet specialty clinics are advancing at a 12.15% CAGR through 2031. Payer steering is decisive. A U.S. claims study showed that outpatient rituximab cost USD 12,400 per course, compared with USD 18,700 in hospital settings, motivating insurers to favor freestanding infusion centers. Subcutaneous FcRn inhibitors further shift care from inpatient to ambulatory environments, and same-day discharge suits elderly patients wary of nosocomial infection. Consequently, warm autoimmune hemolytic anemia market size linked with specialty clinics will surpass USD 0.63 billion by 2031.

Academic and research centers, though smaller in share, anchor innovation. They concentrate on DAT-negative diagnostics and enroll patients in BTK, FcRn, and CAR-T trials. Their contribution to evidence generation feeds back into community protocols, closing the translation gap. Reimbursement frameworks also matter. Medicare’s OPPS still pays hospitals more for the same infusion, but bundled-payment pilots in Europe now reward providers that cut inpatient days, accelerating decentralization.

Geography Analysis

North America held 41.93 of % warm autoimmune hemolytic anemia market share in 2025, driven by dense academic networks, generous orphan-drug reimbursement, and regulatory frameworks that champion accelerated review. Breakthrough Therapy and orphan designations compress launch timelines, enabling new entrants to reach the market within 18 months of pivotal readout. Canada lags the United States because reimbursement is province-specific, while Mexico’s Seguro Popular adds warm AIHA drugs to essential lists yet grapples with hematologist shortages outside major metros.

Europe has a mature orphan framework with 10-year exclusivity, which supports high prices for low-volume diseases. Germany’s IQWiG deemed rituximab moderately beneficial, strengthening its reimbursement stance, whereas Southern Europe’s tighter budgets curb utilization. The United Kingdom maintains evidence summaries because biosimilars still lack robust AIHA data, which constrains competition. Registry data reveal heterogeneity: only 22% of Italian patients receive rituximab within 6 months of steroid failure, compared with 64% in France, a disparity linked to regional funding envelopes.

Asia-Pacific is forecast to register a 13.03% CAGR from 2026 to 2031, the fastest worldwide. China’s NRDL listing of rituximab biosimilars slashed out-of-pocket expense by 68%, lifting infusion volumes beyond tier-1 cities. Japan issued the region’s first formal warm AIHA rituximab indication in 2024, harmonizing coverage across prefectures. India’s flow cytometry scarcity still drives underdiagnosis, yet private chains invest in hematology centers, thereby shrinking referral delays. Australia reimburses off-label rituximab but requires specialist authorization, which limits rural access.

Competitive Landscape

The warm autoimmune hemolytic anemia industry remains moderately fragmented. Roche and Amgen offer originator and biosimilar rituximab, but upcoming FcRn and BTK agents threaten to dilute their hold. Mid-cap innovators like Argenx, Sanofi, and Apellis exploit orphan exclusivity to establish category leadership. Argenx filed an sBLA in January 2026, leveraging real-world data from 47 off-label patients that showed a 68% response rate, highlighting a regulatory shift toward pragmatic evidence. Sanofi’s rilzabrutinib offers oral convenience, while Johnson & Johnson is exploring biomarker-guided dosing in the ENERGY trial.

White space persists in DAT-negative and pediatric segments, which lack approved therapies. CAR-T developers Kyverna and Cabaletta are piloting autologous CD19 constructs; proof-of-concept data in systemic lupus have opened discussion about their curative potential. AI-enabled diagnostics provide another competitive lever, as lab equipment firms embed proprietary algorithms that may bundle with companion therapeutics. Market entry barriers include clinical-trial recruitment in a low-incidence disease and payer skepticism for six-digit annual costs, yet orphan exclusivity offsets generic erosion.

Warm Autoimmune Hemolytic Anemia Industry Leaders

Amgen Inc.

GlaxoSmithKline plc

F. Hoffmann-La Roche Ltd

Johnson & Johnson

Pfizer Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Argenx filed a supplemental BLA for efgartigimod in warm AIHA, supported by a 68% overall response rate from 47 real-world patients, with an accelerated-approval PDUFA date in Q3 2026.

- January 2026: Johnson & Johnson completed enrollment in the Phase 3 ENERGY trial of nipocalimab, with topline data expected in Q4 2026.

- November 2025: CSL Behring allocated USD 150 million to expand its plasma-collection network, adding 25 centers to mitigate IVIG shortages by 2026.

- June 2025: Sanofi secured FDA orphan-drug designation for rilzabrutinib and began the global Phase 3 RIDGELINE study targeting 180 participants across three continents.

Global Warm Autoimmune Hemolytic Anemia Market Report Scope

Warm Autoimmune Hemolytic Anemia (wAIHA) is the most common form of autoimmune hemolytic anemia, a rare acquired hematologic disorder characterized by the production of autoantibodies (primarily IgG) that bind to red blood cell (RBC) surface antigens at body temperature, leading to extravascular hemolysis (mainly in the spleen and liver) via Fc receptor-mediated phagocytosis by macrophages.

The Warm Autoimmune Hemolytic Anemia Market Report is Segmented by Drug Class (Corticosteroids, Immunosuppressants, Monoclonal Antibodies, Intravenous Immunoglobulin, Splenectomy & Surgical, Emerging Therapies), End User (Hospitals, Specialty Clinics, Academic & Research Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Corticosteroids |

| Immunosuppressants |

| Monoclonal Antibodies |

| Intravenous Immunoglobulin (IVIG) |

| Splenectomy & Surgical |

| Emerging Therapies |

| Hospitals |

| Specialty Clinics |

| Academic & Research Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Corticosteroids | |

| Immunosuppressants | ||

| Monoclonal Antibodies | ||

| Intravenous Immunoglobulin (IVIG) | ||

| Splenectomy & Surgical | ||

| Emerging Therapies | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Academic & Research Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the warm autoimmune hemolytic anemia market in 2026?

It reached USD 0.93 billion in 2026 and is forecast to grow swiftly through 2031.

What CAGR is expected for the warm autoimmune hemolytic anemia market to 2031?

The market is set to post a 10.85% CAGR over the 2026-2031 period.

Which therapy class is growing fastest?

Monoclonal antibodies are projected to expand at 11.07% CAGR, outpacing all other classes.

Why are specialty clinics gaining share?

Outpatient infusion protocols and payer incentives reduce costs compared with hospital settings, boosting specialty-clinic uptake.

Which region will see the highest growth?

Asia-Pacific is projected to have a 13.03% CAGR, driven by insurance expansion and improved diagnostics.

Page last updated on: