Hemostasis Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

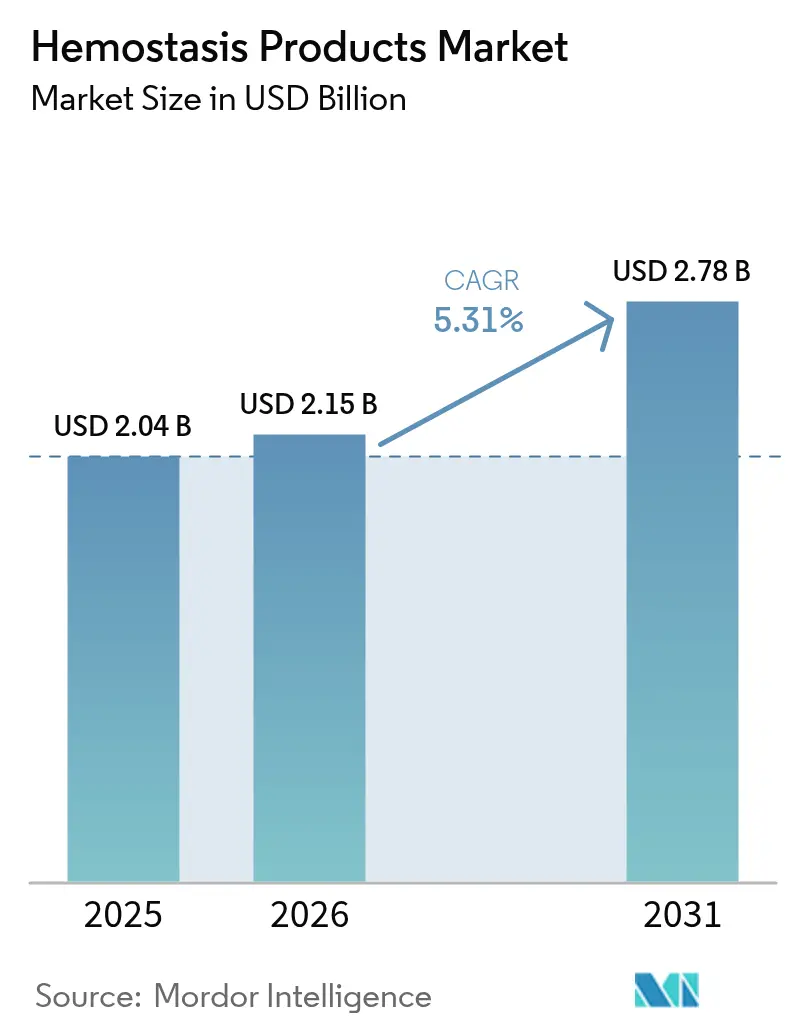

| Market Size (2026) | USD 2.15 Billion |

| Market Size (2031) | USD 2.78 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemostasis Products Market Analysis by Mordor Intelligence

Hemostasis products market size in 2026 is estimated at USD 2.15 billion, growing from 2025 value of USD 2.04 billion with 2031 projections showing USD 2.78 billion, growing at 5.31% CAGR over 2026-2031. Steady demand for rapid bleeding control in trauma, emergency care, and minimally invasive surgery is shifting the Hemostasis products market toward synthetic and active agents that shorten procedure time and reduce transfusion needs. Regulatory greenlights for next-generation solutions—such as FDA-cleared Traumagel for severe bleeding—confirm a robust clinical pipeline and accelerate product launches. Hospitals are prioritizing agents with proven operating-room efficiency, while surgeons favour liquid and spray formats that deliver precise coverage in confined fields. Consolidation among large med-tech firms seeking full-spectrum bleeding management portfolios underlines the strategic value of differentiated technology. Meanwhile, policymakers have begun scrutinising supply resilience after hurricane-linked shortages exposed the fragility of single-site manufacturing for critical inputs.

Key Report Takeaways

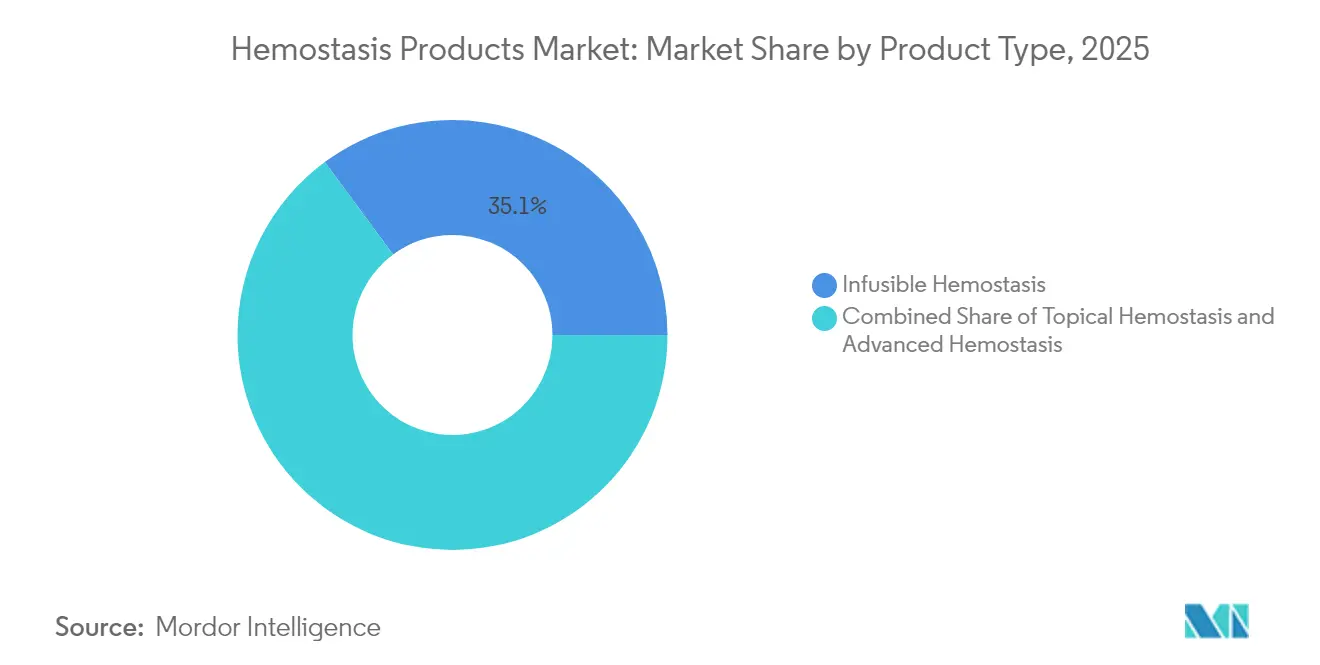

- By product type, infusible solutions led with 35.12% revenue share in 2025, while advanced solutions are projected to expand at a 9.84% CAGR to 2031.

- By formulation, liquid and spray products commanded 38.11% of 2025 revenues; matrix-gel formats are forecast to grow at 7.84% CAGR through 2031.

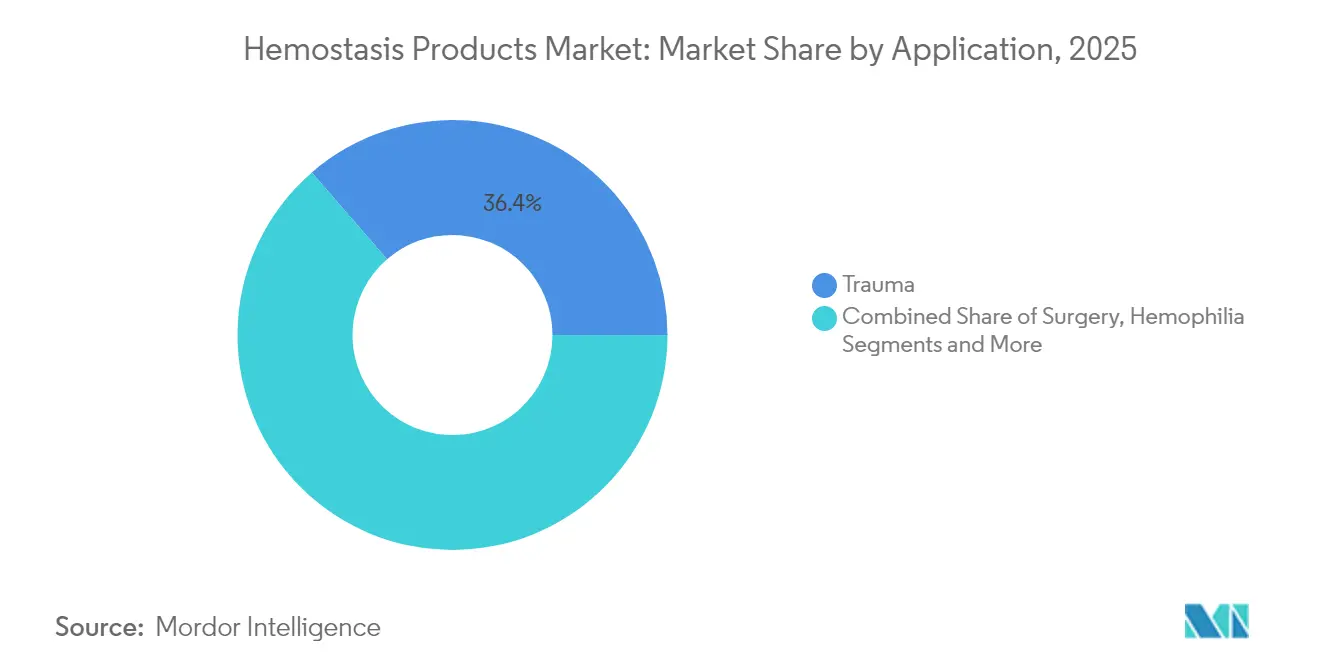

- By application, trauma care captured 36.35% of demand in 2025 and surgical applications are advancing at 7.31% CAGR to 2031.

- By end user, hospitals accounted for 65.05% of consumption in 2025, whereas clinics and ambulatory centres are forecast to grow fastest at 8.91% CAGR.

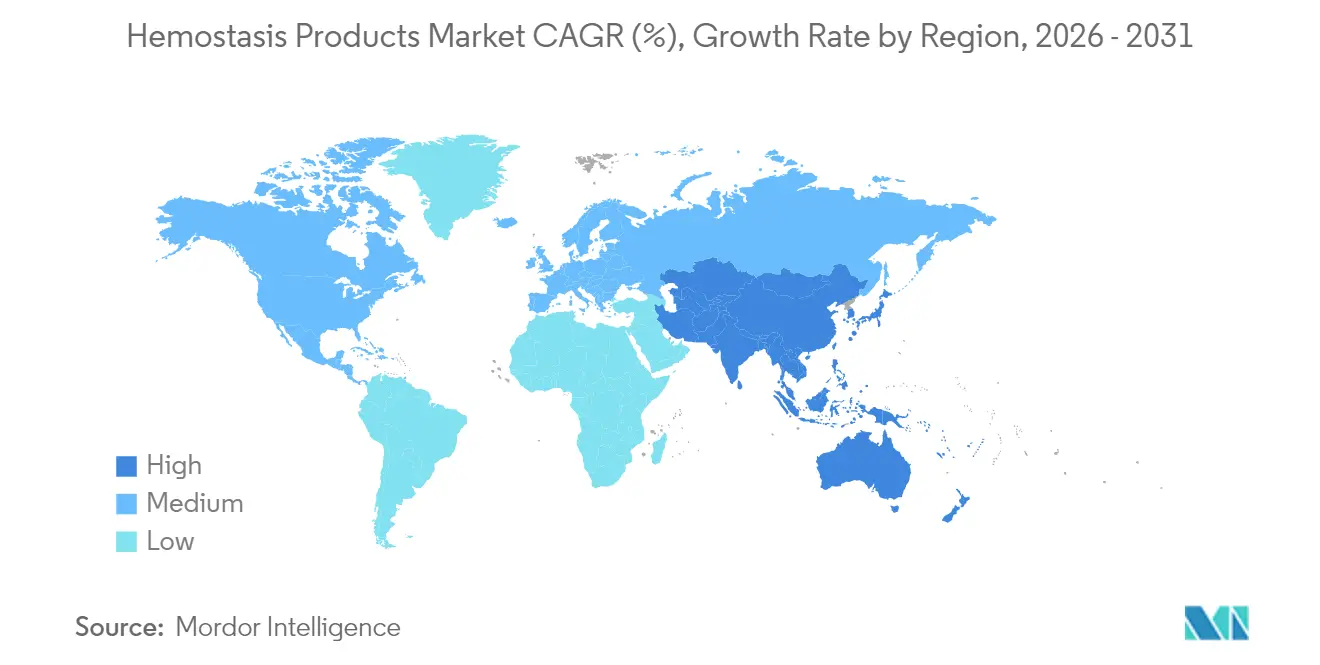

- By geography, North America held 42.38% of 2025 revenue; Asia-Pacific is the fastest-growing region with an 9.46% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemostasis Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume Of Trauma & Surgical Procedures | +1.2% | Global, with APAC leading growth | Medium term (2-4 years) |

| Rapid Product Innovation In Topical & Advanced Hemostats | +1.8% | North America & EU innovation hubs | Short term (≤ 2 years) |

| Growing Adoption Of Minimally-Invasive & Robotic Surgeries | +1.1% | North America, EU, select APAC markets | Medium term (2-4 years) |

| Aging Population-Linked Comorbidities Expanding Target Pool | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Military Demand For Shelf-Stable Plasma & Synthetic Blood | +0.4% | US, NATO allies, conflict regions | Short term (≤ 2 years) |

| Breakthrough Self-Assembling Peptide Gels For GI Bleeding | +0.3% | Global, early adoption in advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Trauma & Surgical Procedures

Global surgical caseload is climbing, with South Asia alone facing a 1.6 billion patient access deficit that is now a policy priority. Updated damage-control resuscitation guidelines place hemorrhage control ahead of airway management, cutting exsanguination mortality by 65% and expanding front-line demand for rapid topical agents[1]Kluger, Yoram, “Prioritizing Circulation Over Airway to Improve Survival in Trauma Patients,” World Journal of Emergency Surgery, biomedcentral.com. Military field medicine—particularly the Joint Trauma System—has normalised early blood-product use, and its protocols are diffusing into civilian trauma networks. These changes enlarge the Hemostasis products market by embedding bleeding control into every step of patient management, from roadside triage to advanced operating suites. Suppliers offering integrated kits that combine diagnostics, topical gels, and factor concentrates will capture hospitals seeking streamlined procurement.

Rapid Product Innovation in Topical & Advanced Hemostats

Self-assembling peptide hydrogels reach hemostasis in seconds, remain transparent for visualisation, and avoid pathogen transmission risks tied to animal tissue. Sequential-crosslinking fibrin glues form dual-network seals within 15 seconds, outperforming legacy fibrin sealants that need minutes to polymerise. Covalently reactive microparticles create fortified clots even under arterial pressure, achieving sub-20-second control in preclinical models[2]Zhu, Linyong, “Covalently reactive microparticles imbibe blood to form fortified clots for rapid hemostasis,” nature.com. FDA clearance of plant-derived Traumagel validates the commercial pathway for biomimetic actives. This innovation wave lifts the Hemostasis products market by replacing slow, plasma-based agents with agile formulations that integrate seamlessly into modern surgical workflows.

Growing Adoption of Minimally Invasive & Robotic Surgeries

Competitive robotic systems such as Senhance, Revo-i, and Hugo are reducing per-procedure costs and expanding access beyond early adopter centres. Smaller access ports, however, restrict instrument reach, making sprayable or flowable hemostats indispensable for covering diffuse bleeding surfaces. Artificial-intelligence modules that predict bleeding risk in real time allow surgeons to stage hemostatic deployment earlier, shortening operating time and improving outcomes. Hospitals procuring new robotic platforms are simultaneously revising formularies to include compatible hemostats, increasing average order values for suppliers.

Aging Population-Linked Comorbidities Expanding Target Pool

Older patients frequently combine anticoagulant regimens with frail vascular integrity, raising intraoperative bleeding complexity. Targeted reversal agents such as andexanet alfa and idarucizumab have increased physician confidence in aggressive anticoagulation management. Factor XI inhibitors promise lower bleeding risk yet will not eliminate the need for topical control inside the surgical field. Bio-engineered heparin reduces dependence on porcine supply chains and offers batch consistency that supports evidence-based dosing. Together these developments enlarge the Hemostasis products market as surgeons treat an expanding cohort of high-risk elderly patients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Regulatory & Reimbursement Hurdles | -1.4% | Global, varying by regulatory jurisdiction | Long term (≥ 4 years) |

| High Cost Of Active Sealants In Low-Resource Settings | -0.8% | Emerging markets, rural healthcare systems | Medium term (2-4 years) |

| Fragile Biologic Supply Chains (Bovine/Porcine Thrombin) | -0.6% | Global, concentrated in animal-sourcing regions | Short term (≤ 2 years) |

| FXIa Inhibitor Pipeline Cannibalizing Infusible Products | -0.4% | Developed markets with advanced anticoagulation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Regulatory & Reimbursement Hurdles

The FDA recently shifted viscoelastic coagulation analysers into Class II, adding quality-system and clinical-data burdens for device makers. Europe’s Medical Device Regulation has lengthened review queues, delaying small-company launches and tilting the Hemostasis products market toward incumbents with regulatory infrastructure. Payment reform is equally challenging; new CMS bundling rules could narrow coverage for autologous blood-derived dressings, forcing hospitals to justify premium spend through hard outcomes.

High Cost of Active Sealants in Low-Resource Settings

Advanced sealants can cost multiple hundreds of USD per unit, a steep hurdle where public budgets are thin. Cardinal Health places direct bleeding-episode costs above USD 10,000, but decision-makers still balk at high up-front product prices. A US academic centre saved USD 1 million by standardising hemostat selection, proving economic value yet also highlighting the need for utilisation governance. Plant-based powders and peptide gels promise cost relief, but formulary committees demand head-to-head evidence before substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Advanced Solutions Outpace Traditional Categories

Infusible therapies retained 35.12% of the Hemostasis products market share in 2025 because factor concentrates remain essential during major bleeds and hemophilia management. Demand, however, is plateauing as gene therapy and FXIa inhibitors progress. The Hemostasis products market is pivoting toward synthetic and biomimetic active sealants that address performance gaps in speed, adhesion, and immunogenicity.

Advanced offerings are projected to grow at 9.84% CAGR through 2031, setting the pace for market expansion. FDA approval of VISTASEAL and plant-based Traumagel illustrates regulatory willingness to endorse novel actives. Competitive intensity is rising as multinationals acquire start-ups for technology access, with Stryker’s USD 4.9 billion Inari acquisition broadening peripheral vascular reach.

By Formulation: Liquid Applications Drive Precision Medicine

Liquid and spray formats captured 38.11% of 2025 revenues, reflecting surgeon preference for no-mix systems that can be deployed through laparoscopic ports or robotic arms. This slice of the Hemostasis products market size benefits from delivery-device innovation, including battery-powered applicators that modulate flow rates for complex anatomy.

Matrix-gel systems are advancing at 7.84% CAGR as sequential-crosslinking chemistries deliver 15-second seals even on moist tissue. Instantly adhesive patches using ultra-elastic substrates extend the Hemostasis products industry to thoracic and cardiac repairs where organ motion frustrates traditional pads.

By Application: Trauma Protocols Reshape Market Dynamics

Trauma accounted for 36.35% of the Hemostasis products market size in 2025 as civilian emergency networks adopt combat-proven gauze and injectable sponges. Introduction of CAB resuscitation protocols is driving earlier and wider topical use, particularly in prehospital settings.

Surgical use is forecast to grow 7.31% CAGR to 2031 as robotic and minimally invasive procedures proliferate. Real-time viscoelastic testing allows tailored product selection inside the operating room, increasing consumption of premium hemostats that shorten closure time.

By End User: Hospital Economics Drive Premium Adoption

Hospitals held 65.05% Hemostasis products market share in 2025, supported by bundled-payment incentives that reward complication reduction. Budget committees increasingly approve higher-priced sealants when data show shorter intensive-care stays and fewer blood transfusions.

Clinics and ambulatory centres will post 8.91% CAGR as payers push procedures out of inpatient settings. These facilities value room-temperature stable patches such as Baxter’s new Hemopatch, which avoid cold-chain costs and speed turnover. Broader EMS adoption of shelf-stable synthetic platelets will further widen the Hemostasis products market footprint beyond hospital walls.

Geography Analysis

North America captured 42.38% of 2025 revenues, a position reinforced by high surgical density, rigorous clinical-trial infrastructure, and sizeable defence R&D funding for synthetic blood programmes. FDA fast-track pathways and the Defence Production Act have together promoted domestic production resilience after supply shocks, helping stabilise regional availability of critical hemostats.

European markets continue to set safety benchmarks; EMA approvals for marstacimab and efanesoctocog alfa confirm the region’s leadership in hemophilia therapeutics. Adoption varies, however, with southern economies scrutinising cost-effectiveness before broad rollout. Medical Device Regulation timelines favour firms with mature quality systems, encouraging partnerships between mid-caps and large strategics seeking contiguous portfolios.

Asia–Pacific is the fastest growing area of the Hemostasis products market as hospital infrastructure modernises and elective surgery backlogs unwind. Japan’s announcement of a two-year shelf-life synthetic blood underscores regional innovation capability. South Asia’s surgical access gap creates latent demand likely to unlock as universal health-coverage schemes expand. Local manufacturing incentives are attracting investment into plasma fractionation and peptide synthesis plants, reducing import reliance and diversifying global supply.

Competitive Landscape

Market consolidation is accelerating as diversified device makers pursue technology adjacency. Merit Medical’s USD 120 million purchase of Biolife secured proprietary plant-based powder technology that complements its access products, allowing bundling across trauma and vascular portfolios. Stryker’s Inari acquisition adds thrombectomy expertise, positioning the company to offer an end-to-end bleeding and clot-removal platform attractive to hybrid cath-lab suites.

Werfen’s move into point-of-care coagulation via Accriva Diagnostics signals interest in diagnostic-therapeutic convergence, a theme echoed by Teleflex’s planned vascular-intervention purchase that broadens its tool set for bleeding management. Large groups with distribution muscle can fast-track innovative assets through shared sales channels, raising entry barriers for stand-alone start-ups.

White-space persists in low-resource markets where cost remains a gating factor. NIH-funded work on Nano-RBC synthetic blood and DARPA’s universal plasma projects may ultimately spawn licensed spin-outs focused on emerging-market indications. Suppliers that align with regional manufacturing incentives and build robust cold-chain-free portfolios will differentiate as procurement policies emphasise resilience.

Hemostasis Products Industry Leaders

Abbott Laboratories

Baxter International, Inc.

Medtronic plc

Becton Dickinson (BD)

CSL Behring

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Baxter International launched a room-temperature Hemopatch Sealing Hemostat, enabling rapid application without refrigeration and extending shelf life.

- March 2025: The FDA approved Qfitlia (fitusiran) for routine prophylaxis in hemophilia A and B patients aged 12 and older, showing a 73% reduction in bleeding episodes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hemostasis products market as all topical, infusible, and next-generation bioactive agents that clinicians apply systemically or locally to arrest bleeding during trauma care and surgical procedures. According to Mordor Intelligence, this market will reach about USD 2.04 billion in 2025, with growth driven by advanced sealants and higher procedure volumes.

Scope Exclusions: Diagnostic analyzers, vascular closure devices, and reusable surgical instruments that do not directly deliver a hemostatic medium are excluded.

Segmentation Overview

- By Product Type

- Topical Hemostasis (Collagen, ORC, Gelatin, Polysaccharides)

- Infusible Hemostasis (FFP, Platelet Conc, Factor VIII, PCC)

- Advanced Hemostasis (Flowable, Thrombin, Fibrin, Synthetic)

- By Formulation

- Matrix & Gel

- Sponge & Pad

- Powder

- Liquid / Spray

- By Application

- Trauma

- Surgery

- Hemophilia

- Myocardial Infarction

- Thrombosis

- Others

- By End User

- Hospitals

- Clinics & ASCs

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviews surgeons, hospital procurement heads, and material scientists across North America, Europe, Asia-Pacific, and Latin America. Conversations verify usage rates, average selling prices, conversion from legacy gauze to advanced polymer agents, and anticipated reimbursement shifts, allowing us to refine volume assumptions that secondary data alone cannot expose.

Desk Research

We start with wide screening of respected, non-paywalled sources such as the United States CDC surgical statistics, Eurostat procedure data, WHO Global Health Observatory, and trade association yearbooks from the International Alliance for Patient Blood Management. Company filings and 10-Ks add price and unit clues, while news flows from Dow Jones Factiva and product clearance records from the FDA and EMA illustrate launch timing. IMTMA production digests and Volza shipment logs yield baseline manufacturing and trade footprints. These materials underpin initial demand curves.

Mordor analysts then reference subscription assets like D&B Hoovers for hospital spending indicators and Questel patent counts to judge innovation momentum. The sources listed are illustrative, not exhaustive, and many more repositories support data collection, cross-checks, and contextual clarity.

Market-Sizing & Forecasting

We construct a top-down demand pool from procedure counts and average units consumed per surgery, which are then matched with global import-export and production statistics. Supplier roll-ups and sampled ASP × volume checks provide a selective bottom-up view to validate totals before adjustments. Key modeling inputs include trauma incidence, elective surgery backlog clearance rates, price erosion trajectories, material cost inflation, and hospital penetration of minimally invasive techniques. Forecasts blend multivariate regression with scenario analysis, and variable paths are stress-tested with expert feedback. Where bottom-up gaps emerge, we interpolate using regional consumption ratios that earlier interviews confirm.

Data Validation & Update Cycle

Outputs undergo anomaly scans, peer reviews, and a senior sign-off. Models reconcile against independent procedure trackers and trade data. Reports refresh annually, and interim updates are triggered when regulatory approvals, recalls, or macro events materially shift demand.

Why Our Hemostasis Products Baseline Earns Decision-Maker Trust

Published numbers diverge because firms frame the product universe differently, apply varied baseline years, and refresh at unequal cadences.

External publications place 2024 values anywhere between USD 1.60 billion and USD 1.75 billion, depending on whether advanced polymer sealants are counted.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.04 B (2025) | Mordor Intelligence | - |

| USD 1.75 B (2024) | Global Consultancy A | Excludes next-generation bioactive agents and uses older baseline year |

| USD 1.60 B (2023) | Industry Journal B | Focuses mainly on topical dressings and applies conservative ASP progression |

The comparison shows that scope selection, baseline alignment, and price tracking drive most variation. By integrating procedure-level demand logic, validated ASP trends, and an annual refresh cycle, Mordor Intelligence delivers a balanced baseline that executives can trace to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the current value of the Hemostasis products market?

The Hemostasis products market was valued at USD 2.15 billion in 2026 and is projected to reach USD 2.78 billion by 2031.

Which product category is growing fastest?

Advanced synthetic and biomimetic solutions are posting the highest growth, with a 9.84% CAGR forecast through 2031.

Why are liquid and spray hemostats so popular among surgeons?

They allow precise, one-handed application through laparoscopic or robotic ports and deliver rapid polymerisation, reducing procedure time.

How significant is trauma care to overall market demand?

Trauma applications represented 36.35% of 2025 demand and continue to expand as prehospital protocols prioritise early hemorrhage control.

Which region leads in market share?

North America remains the largest regional market, accounting for 42.38% of 2025 global revenue.

Page last updated on: