Antibody Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 336.79 Billion |

| Market Size (2031) | USD 605.53 Billion |

| Growth Rate (2026 - 2031) | 12.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibody Therapy Market Analysis by Mordor Intelligence

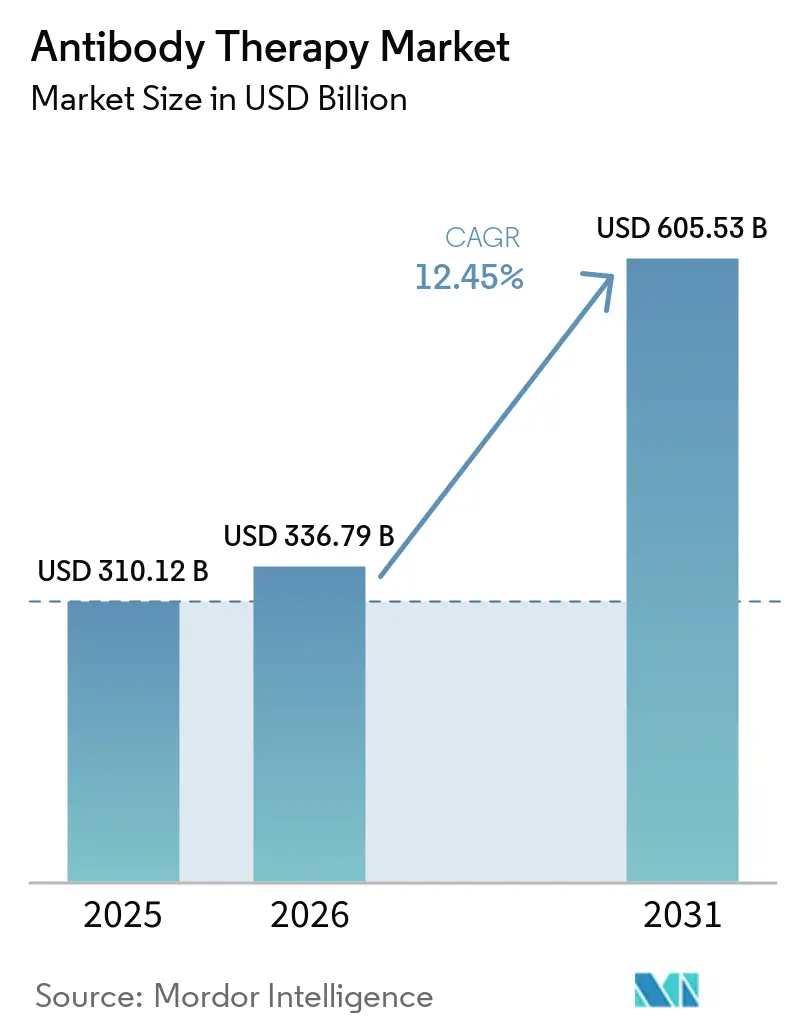

The Antibody Therapy Market size is projected to be USD 310.12 billion in 2025, USD 336.79 billion in 2026, and reach USD 605.53 billion by 2031, growing at a CAGR of 12.45% from 2026 to 2031.

Continued label expansions in oncology, the rise of bispecifics and antibody-drug conjugates, and the steady rollout of subcutaneous formats are shaping both pipeline priorities and commercial execution across the antibody therapy market. Home-centered delivery is gaining ground as regulators and payers look for value in settings of care that improve adherence and reduce burden on infusion centers, a trend that aligns with new long-acting options for infant RSV prevention. Dealmaking remains active as leaders secure platforms and late-stage assets to bolster oncology portfolios and life cycle strategies. Health technology assessment requirements are also rising, which tightens evidence standards for high-cost biologics while rewarding formats that expand access through self-administration.

Key Report Takeaways

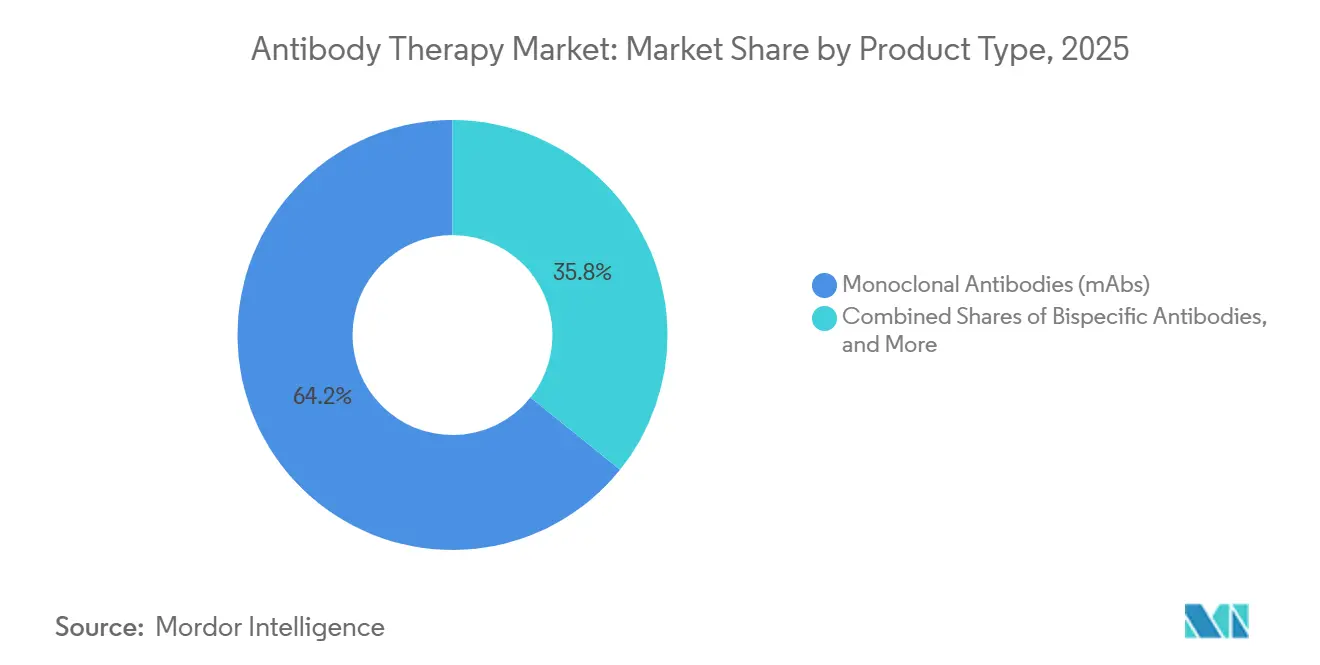

- By product type, monoclonal antibodies led with 64.23% revenue share in 2025, while bispecific antibodies are projected to expand at a 16.84% CAGR through 2031.

- By disease area, oncology captured 48.62% in 2025, while respiratory is forecast to grow at a 16.09% CAGR to 2031.

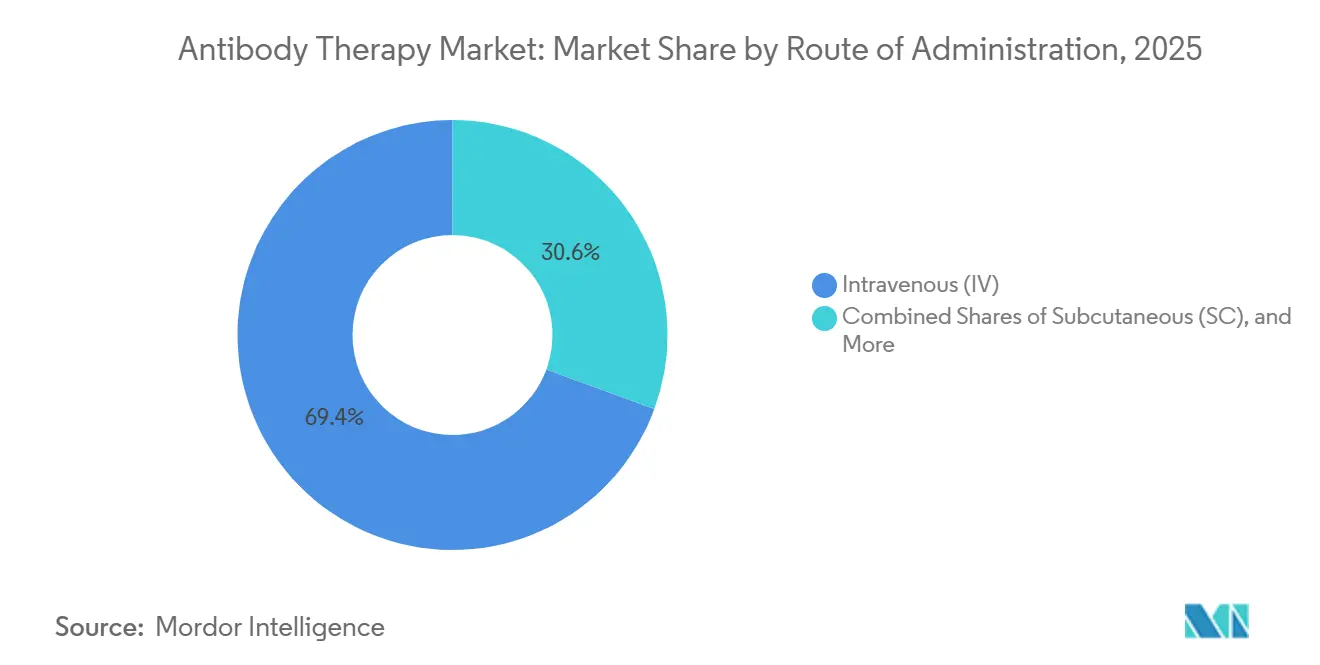

- By route of administration, intravenous accounted for 69.41% in 2025, while subcutaneous is expected to advance at a 15.19% CAGR through 2031.

- By end user, hospitals held 52.34% in 2025, while homecare and self-administration are anticipated to grow at a 15.11% CAGR to 2031.

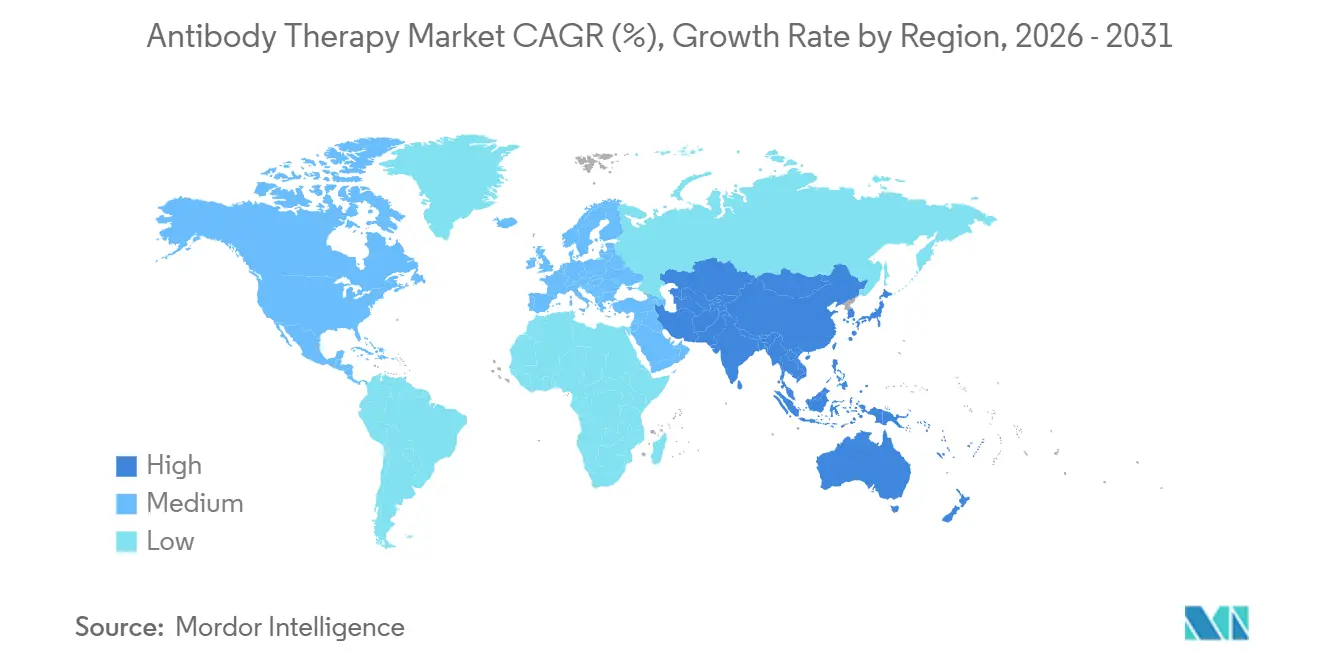

- By geography, North America accounted for 42.44% in 2025, while Asia-Pacific is set to post a 15.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antibody Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Checkpoint inhibitors and oncology label expansions accelerate patient pools | +2.8% | Global, with North America & EU leading | Medium term (2-4 years) |

| Immunology IL-23/IL-4/IL-13 class growth sustains chronic-use volumes | +2.4% | Global, APAC core with spill-over to MEA | Long term (≥ 4 years) |

| Subcutaneous and long-acting formats enable home/self-administration | +2.1% | North America & EU, early gains in Japan | Short term (≤ 2 years) |

| Biosimilar monoclonal antibodies expand access in mature categories | +1.9% | Europe (mature), USA & APAC (emerging) | Medium term (2-4 years) |

| ADCs and bispecifics open high-value oncology niches | +1.8% | Global, with concentration in USA, EU, APAC advanced markets | Long term (≥ 4 years) |

| Long-acting antibodies for infectious disease prevention (e.g., RSV) | +1.5% | Global, priority in North America, EU pediatric segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Checkpoint Inhibitors And Oncology Label Expansions Accelerate Patient Pools

Regulatory momentum is widening checkpoint inhibitor reach, including perioperative use in muscle-invasive bladder cancer, where PADCEV plus pembrolizumab secured FDA Priority Review based on EV-304 results that reduced event-free survival risk and improved pathological complete response versus chemotherapy.[1]Astellas Pharma Inc., “U.S. FDA Grants Priority Review to sBLA for PADCEV + Keytruda,” PR Newswire, prnewswire.com Specialty players also opened new niches, such as cosibelimab-ipdl for metastatic cutaneous squamous cell carcinoma, which delivered durable responses and later received a label update based on longer-term outcomes[2]Sun Pharma, “FDA Approves Label Update for UNLOXCYT,” PR Newswire, prnewswire.com. Autoimmune pathways are expanding as well, with guselkumab approvals that now span inflammatory bowel disease segments, further reinforcing chronic-use volumes for immune-modulating biologics.

These approvals increase per-asset revenue potential and strengthen oncology backbones across major tumor types, which keeps the antibody therapy market focused on both perioperative and metastatic settings. At the same time, payer and policy demands are pulling in more real-world evidence for oncology pricing and coverage decisions, which encourages manufacturers to plan for outcomes beyond traditional clinical endpoints.

Immunology IL-23/IL-4/IL-13 Class Growth Sustains Chronic-use Volumes

The immunology backbone is broadening with oral and subcutaneous options that improve access and adherence for chronic conditions. Icotrokinra became the first oral IL-23 inhibitor approved for plaque psoriasis in 2026, supporting clear or almost clear skin targets in pivotal studies and positioning oral peptides as alternatives to injectables in dermatology[3]Rose McNulty, “FDA Approves Icotrokinra, First Oral IL-23 Inhibitor,” AJMC, ajmc.com. Subcutaneous biologics continue to shift administration patterns as illustrated by Saphnelo’s EU approval for self-administration with a pre-filled pen, which aligns with patient preferences for non-infusion formats in diseases such as lupus.

Adherence advantages in home settings are also well documented in immunoglobulin therapy, where subcutaneous regimens achieve very high adherence in real-world use, which indicates the broader behavioral pull toward convenient administration. Payers and HTA bodies are in turn benchmarking high-cost immunology biologics against more affordable comparators, which heightens both price discipline and evidence standards in the antibody therapy market.

Subcutaneous And Long-Acting Formats Enable Home/Self-Administration

Long-acting antibodies have changed RSV prevention by enabling a single-dose approach that provides season-long protection for infants, as seen with clesrovimab’s regulatory progress and recommendations that endorse widespread use[4]Merck, “Merck Announces FDA Acceptance of Biologics License Application for Clesrovimab,” Merck Newsroom, merck.com. Real-world rollouts in Europe reported sharp reductions in RSV-related hospitalizations, reinforcing the value proposition for population-level prophylaxis even as programs work through demand surges and supply planning. In oncology and autoimmune conditions, sponsors are prioritizing subcutaneous options that cut time in clinic and shift use toward home and ambulatory settings, including SC regimens for lupus and ulcerative colitis that allow home initiation and maintenance.

Capacity remains a constraint for complex injectables, which pushes lead times for sterile fill-finish and heightens the need to prioritize device choices early in development. Manufacturers are also optimizing upstream and downstream processes, including the adoption of single-use systems in targeted steps to improve speed and flexibility, even as consumable costs rise at commercial scale.

Biosimilar Monoclonal Antibodies Expand Access In Mature Categories

Entry by more biosimilars is widening access in core categories and broadening the antibody therapy market across payer types. In the United States, interchangeable denosumab options entered in 2026 after a series of biosimilar launches in 2025, which positions osteoporosis and oncology supportive care for increased competition. European availability continues to extend as more companies launch monoclonal biosimilars across member states, with strategic emphasis on patient access and budget impact.

Global partnerships are also addressing development and commercialization needs for oncology biosimilars across regions, which supports broader uptake as tenders and hospital policies align. In Canada, rebranding and relaunches of established biosimilar franchises signal continued effort to normalize physician and patient switching.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy and biomanufacturing costs constrain access | -2.2% | Global, acute in APAC emerging and MEA | Long term (≥ 4 years) |

| Patent expiries and biosimilar price erosion | -1.7% | North America, Europe mature markets | Medium term (2-4 years) |

| Biologics/ADC supply chain and capacity bottlenecks | -1.3% | Global, with concentration in North America & EU manufacturing hubs | Medium term (2-4 years) |

| HTA and real-world evidence hurdles to reimbursement | -1.1% | Europe (NICE, HAS, IQWiG), expanding to APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Therapy And Biomanufacturing Costs Constrain Access

Over the long term, cost structures continue to influence access as commercial-scale antibody production depends on high-titer mammalian cell culture and capital-heavy facilities. Process advances have reduced per-gram costs over time, but complex modalities like ADCs bring new development and CMC burdens that include high-potency payload controls and critical quality attributes such as drug-to-antibody ratio. Failures linked to conjugation and scale-up reinforce the need for early CMC risk mitigation and platform consistency for growing ADC pipelines.

Sponsors and CDMOs are also navigating lead times and competition for sterile fill-finish capacity as many brands target pre-filled syringes and autoinjectors to support subcutaneous use. Single-use systems can improve flexibility in selected steps, which helps reduce facility footprint and speed transfers, although consumables add meaningful operating costs at scale.

Patent Expiries And Biosimilar Price Erosion

Loss of exclusivity across large brands brings price pressure as biosimilars enter, which intensifies competition in hospital and specialty channels in the antibody therapy market. Originators are pursuing device innovations and new formulations to sustain share and support home-based use, which can protect revenue while improving patient convenience. New biosimilar launches in immunology and oncology supportive care categories are broadening patient choice and signaling ongoing multi-entrant dynamics in mature segments. HTA scrutiny remains high for expensive therapies, which means manufacturers must plan for real-world outcomes and value frameworks as part of launch strategies. Sponsors also continue to invest in partnerships that share risk and accelerate access in key markets, including licensing structures that allocate development and commercialization roles by geography.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Next-Generation Modalities Drive Innovation Premium

Monoclonal antibodies commanded 64.23% of the antibody therapy market share in 2025 as checkpoint inhibitors and chronic immunology brands anchored use across large patient populations and treatment lines. Bispecific antibodies are the fastest-growing product class with a projected 16.84% CAGR over 2026-2031, supported by robust late-stage pipelines and strategic alliances that combine immune engagement with angiogenesis modulation and other tumor microenvironment targets.

Regeneron’s linvoseltamab received accelerated approval in 2025 for relapsed or refractory multiple myeloma after at least four prior lines, which illustrates the potential for T-cell-engaging bispecifics to become hematology backbones under defined risk management programs. Antibody-drug conjugates also continue to expand in solid tumors and lymphomas as sponsors push payload and linker diversity and execute confirmatory programs. Platform partnerships and acquisitions underscore the pace of innovation and the intent to secure modality leadership ahead of patent expiries.

Manufacturing and CMC factors shape scale-up for newer modalities in the antibody therapy market as ADCs require specialized containment, reliable conjugation controls, and reproducible drug-to-antibody ratios at commercial scale. These requirements raise cost and complexity but are being met by process design, platform standardization, and investments in external capacity. Sponsors are balancing facility flexibility and cost when adopting single-use systems, which can shorten timelines yet add consumable costs as commercial volumes rise.

Meanwhile, innovation in next-generation ADC payloads and tumor-selective designs is expanding therapeutic windows and renewing interest in targets once thought to be saturated. As pipelines grow, portfolio rationalization and selective partnering remain central to sustaining capital efficiency across the antibody therapy industry.

By Disease Area: Oncology Dominance Meets Respiratory Surge

The oncology segment accounted for a 48.62% share of the antibody therapy market size in 2025 as checkpoint inhibitors, ADCs, and emerging bispecifics expanded use across perioperative and relapsed settings. FDA Priority Review for PADCEV plus pembrolizumab in perioperative muscle-invasive bladder cancer highlights deepening use of antibodies outside metastatic-only settings based on strong EV-304 outcomes. Label progress in cutaneous squamous cell carcinoma with cosibelimab-ipdl and the conversion of bispecific programs to broader hematology use reflect the breadth of oncology demand.

ADC programs also continued to advance in lymphomas, which supports targeted therapy backbones and second-line strategies. Respiratory is the fastest-growing disease area with a projected 16.09% CAGR from 2026 to 2031 on the strength of long-acting RSV monoclonal antibodies and supportive pediatric recommendations. Clesrovimab’s clinical progress and ACIP guidance that endorses preventive use in infants broaden seasonal protection at a population level. Real-world experience in Europe shows large reductions in RSV hospitalizations during initial rollouts, which reinforces health-system value while prioritizing reliable supply and planning across seasons. Collectively, these dynamics support sustained growth for respiratory prevention and treatment in the antibody therapy market through 2031.

By Route of Administration: Subcutaneous Transition Reshapes Care Delivery

Intravenous administration accounted for a 69.41% share of the antibody therapy market size in 2025, reflecting the continued need for hospital-level monitoring in oncology and other complex care pathways. Protocol control and adverse event management remain important considerations for routes that require infusion centers and structured observation in early cycles for new therapies.

Subcutaneous is the fastest-growing route with a projected 15.19% CAGR through 2031 as high-concentration formulations and home-ready devices move care to more convenient settings. EU approval for Saphnelo self-administration and a fully subcutaneous regimen for Tremfya in ulcerative colitis highlight the shift to home-based starts and maintenance schedules. RSV prophylaxis also reinforces the role of intramuscular options that offer single-dose season-long coverage for infants, which eases caregiver burden and clinic throughput. Sponsors that align route strategy and device design with real-world preferences are best placed to capture durable share in the antibody therapy market.

By End User: Homecare Decentralization Accelerates

Hospitals held 52.34% of end-user share in 2025 as oncology regimens, bispecific monitoring, and infusion workflows under risk management programs remain concentrated in certified settings. Operational readiness for adverse event management and reimbursement coordination supports hospital and specialty-center roles in early adoption of cutting-edge therapies.

Homecare and self-administration are the fastest-growing end-user settings with a projected 15.11% CAGR, which reflects subcutaneous expansion and device innovation that simplify at-home therapy. Evidence from immunoglobulin therapy shows very high adherence with home-based subcutaneous regimens, which bolsters the case for decentralized care models for eligible patients. EU approvals for self-administered lupus therapy and fully subcutaneous IBD induction allow starts and maintenance outside infusion centers, which reduces visits and can improve patient experience. Coverage and utilization management continue to evolve, which influences whether subcutaneous options are reimbursed under pharmacy or medical benefits in the United States. Providers and payers are also piloting digital monitoring to support adherence and safety in home settings for the antibody therapy market.

Geography Analysis

North America accounted for 42.44% of global revenue in 2025 as accelerated development paths, subcutaneous innovations, and steady biosimilar entry shaped uptake in oncology and immunology. Priority Review for PADCEV plus pembrolizumab in perioperative bladder cancer underscores the region’s leadership in first-in-class and new-setting indications for antibody combinations. Regeneron’s 2025 accelerated approval for linvoseltamab in advanced multiple myeloma further demonstrates the path for T cell engaging bispecifics in hematology-oncology. U.S. launches of interchangeable denosumab biosimilars in 2026 add competition in osteoporosis and oncology supportive care. In parallel, real-world evidence plays a larger role in policy and negotiation for oncology drugs, which influences pricing dynamics in the antibody therapy market. RSV prophylaxis policy also supports demand through clear recommendations for infant protection, which sustains seasonal planning.

Europe shows sustained progress in biosimilar adoption and access as more companies launch monoclonal biosimilars across member states and extend category depth. Commercial availability of ustekinumab biosimilar options and ongoing oncology collaborations with manufacturers such as Henlius point to continued competition in immune and cancer pathways. As more subcutaneous indications receive approval, European systems can reduce infusion burden and align with patient preferences, which supports decentralization of care. Real-world practice and policy in Europe also maintain a strong focus on value evidence to sustain coverage for high-cost biologics.

Asia-Pacific is the fastest-growing region at a projected 15.27% CAGR from 2026 to 2031, supported by local development, manufacturing partnerships, and cross-border licensing that broaden category availability. Partnerships such as Henlius and Dr. Reddy’s for investigational daratumumab biosimilar coverage across many countries expand access pathways for oncology. Indian developers have also moved into the United States with denosumab biosimilars, which demonstrates APAC’s rising role in global launches. Additional Asia-based programs in bispecific antibodies and ADCs highlight regional pipelines that complement multinational development, including NMPA-cleared studies that add to global evidence generation. ultinational alliances such as the BMS and BioNTech partnership for BNT327 include large pan-regional programs that touch APAC centers, which reinforces global reach for new modalities in the antibody therapy market.

Competitive Landscape

Competition is shaped by R&D intensity, platform acquisitions, and selective partnering to secure category leadership in oncology and chronic immunology. Gilead’s acquisition of Tubulis added a next-generation ADC platform and clinical assets in ovarian and lung cancer, while Genmab’s purchase of Merus brought late-stage bispecific programs for head and neck cancers. Portfolio resilience in the antibody therapy market also reflects life cycle strategies for subcutaneous formulations and device advances that keep assets relevant amid biosimilar pressure. Partnership models remain central to scaling discovery and development, with modular ADC and bispecific platforms out-licensed to larger partners for late-stage investment and commercialization. Sandoz and Henlius entered a collaboration to commercialize oncology therapy ipilimumab in multiple indications, which illustrates how originator-biosimilar expertise can intersect in complex biologics.

Ustekinumab biosimilar availability in the United States adds pressure in immunology categories, and broader EU biosimilar launches extend competition across therapeutic classes. The antibody therapy industry is also advancing subcutaneous readiness as a core differentiator to meet payer and patient demand for convenient use.

New entrants and focused biotech innovators continue to shape the frontier in target selection, payload engineering, and tumor-selective designs that aim to improve the therapeutic window. Financing milestones for next-generation ADC pipelines support diverse payloads and targeted development strategies across solid tumors and hematologic cancers. Approvals such as linvoseltamab highlight the pivotal role of risk evaluation and mitigation strategies for T cell engagers, which shapes site-of-care readiness and training for sustainable uptake. Together, these developments point to a dynamic competitive environment that supports sustained growth for the antibody therapy market through 2031.

Antibody Therapy Industry Leaders

F. Hoffmann-La Roche Ltd

Johnson & Johnson

Merck & Co., Inc.

AbbVie Inc.

Sanofi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Biocon launched Bosaya and Aukelso, denosumab biosimilars to Prolia and Xgeva, in the United States following interchangeable designation.

- April 2026: Astellas and Pfizer Inc., received FDA Priority Review for PADCEV plus Keytruda perioperative use in muscle-invasive bladder cancer regardless of cisplatin eligibility based on EV-304 data.

Global Antibody Therapy Market Report Scope

As per the scope of the report, antibody therapy is a medical treatment that uses antibodies, proteins produced by the immune system, to identify and neutralize specific pathogens, such as viruses or bacteria, or target diseased cells, such as cancer cells.

The antibody therapy market is segmented by product type, including monoclonal antibodies (mAbs), bispecific antibodies, antibody–drug conjugates (ADCs), polyclonal antibodies, and others such as antibody fragments and radiolabeled antibodies. By disease area, the market is categorized into oncology, autoimmune and inflammatory disorders, infectious diseases, respiratory diseases, hematology, cardiometabolic disorders, and others, including ophthalmology and neurology. Based on route of administration, the market is segmented into intravenous (IV), subcutaneous (SC), intramuscular (IM), and intravitreal delivery. In terms of end users, the market is classified into hospitals, specialty clinics, and homecare or self‑administration settings. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Monoclonal Antibodies (mAbs) |

| Bispecific Antibodies |

| Antibody-Drug Conjugates (ADCs) |

| Polyclonal Antibodies |

| Others (Antibody Fragments, Radiolabeled antibodies) |

| Oncology |

| Autoimmune & Inflammatory Disorders |

| Infectious Diseases |

| Respiratory |

| Hematology |

| Cardiometabolic |

| Others (Ophthalmology, Neurology) |

| Intravenous (IV) |

| Subcutaneous (SC) |

| Intramuscular (IM) |

| Intravitreal |

| Hospitals |

| Specialty Clinics |

| Homecare / Self-administration |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Monoclonal Antibodies (mAbs) | |

| Bispecific Antibodies | ||

| Antibody-Drug Conjugates (ADCs) | ||

| Polyclonal Antibodies | ||

| Others (Antibody Fragments, Radiolabeled antibodies) | ||

| By Disease Area | Oncology | |

| Autoimmune & Inflammatory Disorders | ||

| Infectious Diseases | ||

| Respiratory | ||

| Hematology | ||

| Cardiometabolic | ||

| Others (Ophthalmology, Neurology) | ||

| By Route of Administration | Intravenous (IV) | |

| Subcutaneous (SC) | ||

| Intramuscular (IM) | ||

| Intravitreal | ||

| By End-user | Hospitals | |

| Specialty Clinics | ||

| Homecare / Self-administration | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the growth outlook for the global antibody therapy market to 2031?

The antibody therapy market is set to rise from USD 336.79 billion in 2026 to USD 605.53 billion by 2031, reflecting a 12.45% CAGR after a 2025 base of USD 310.12 billion.

Which product categories will lead growth through 2031?

Monoclonal antibodies held 64.23% share in 2025, while bispecific antibodies are projected to grow at 16.84% CAGR over 2026-2031, with ADCs expanding alongside late-stage pipelines.

Which therapy areas will drive the most demand in 2026-2031?

Oncology accounted for 48.62% in 2025, while respiratory indications are set to grow at 16.09% CAGR through 2031 supported by season-long infant RSV prophylaxis from long-acting antibodies such as clesrovimab and nirsevimab.

How is the route of administration shifting and what does it mean for access?

Intravenous accounted for 69.41% in 2025, while subcutaneous is the fastest-growing route at 15.19% CAGR through 2031, enabled by self-administered formats such as Saphnelo and fully subcutaneous Tremfya regimens.

Which regions offer the strongest near-term opportunities for antibody therapy?

North America held 42.44% in 2025, while Asia-Pacific is projected to post a 15.27% CAGR through 2031 as local capacity and partnerships expand.

What risks could alter the 2026-2031 outlook?

Price erosion from biosimilars, sterile fill-finish capacity constraints, and stricter HTA evidence requirements present key headwinds for high-cost biologics.

Page last updated on: