Hematuria Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.37 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

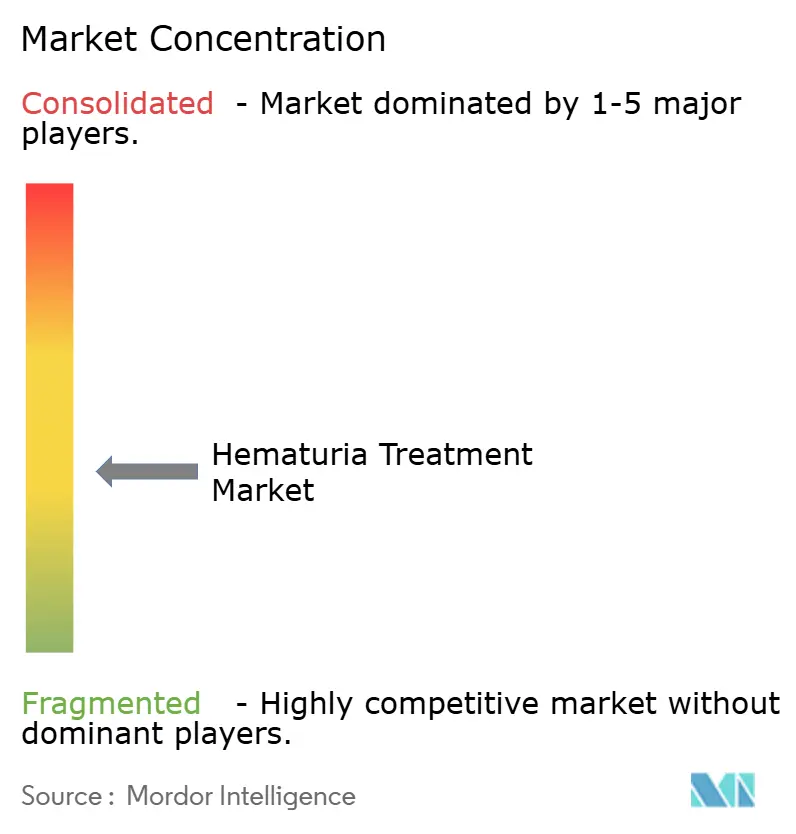

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hematuria Treatment Market Analysis by Mordor Intelligence

The Hematuria Treatment Market size is projected to expand from USD 1.14 billion in 2025 and USD 1.18 billion in 2026 to USD 1.37 billion by 2031, registering a CAGR of 3.12% between 2026 to 2031.

The hematuria treatment market is driven by the prevalence of common urological conditions such as urinary tract infections, benign prostatic hyperplasia, urolithiasis, and bladder cancer. In 2025, urinary tract infections accounted for 449.1 million new cases, while benign prostatic hyperplasia had an age-standardized prevalence rate of 2,782.59 per 100,000 persons.[1]American Urological Association, “American Urological Association Releases Microhematuria Guideline Amendment,” American Urological Association, auanet.org The AUA/SUFU 2025 guideline amendment has further influenced the market by introducing a four-tier risk framework and allowing urine-based tumor markers as an alternative to immediate cystoscopy for appropriately counseled intermediate-risk patients.

Key Report Takeaways

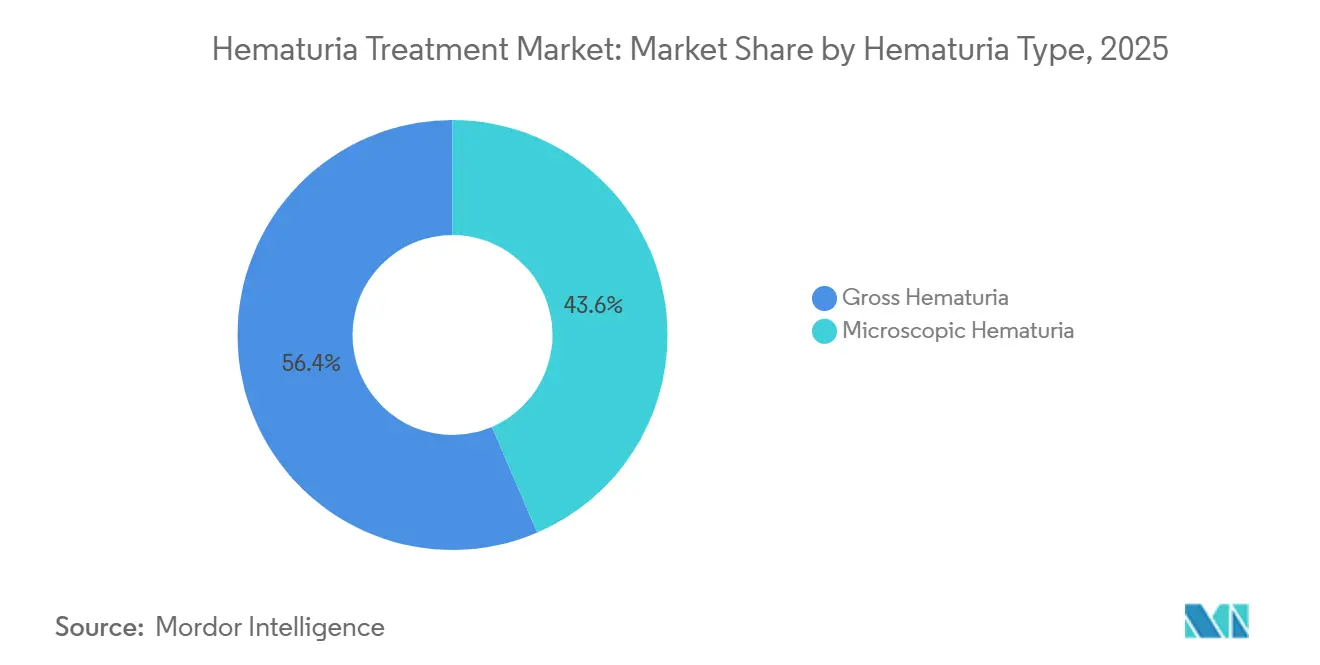

- By hematuria type, gross hematuria accounted for 56.45% of the hematuria treatment market size in 2025, while microscopic hematuria is projected to grow at a 3.66% CAGR through 2031.

- By treatment type, pharmacotherapy held 36.75% share of the hematuria treatment market size in 2025, while procedural and interventional therapies are projected to expand at a 3.95% CAGR through 2031.

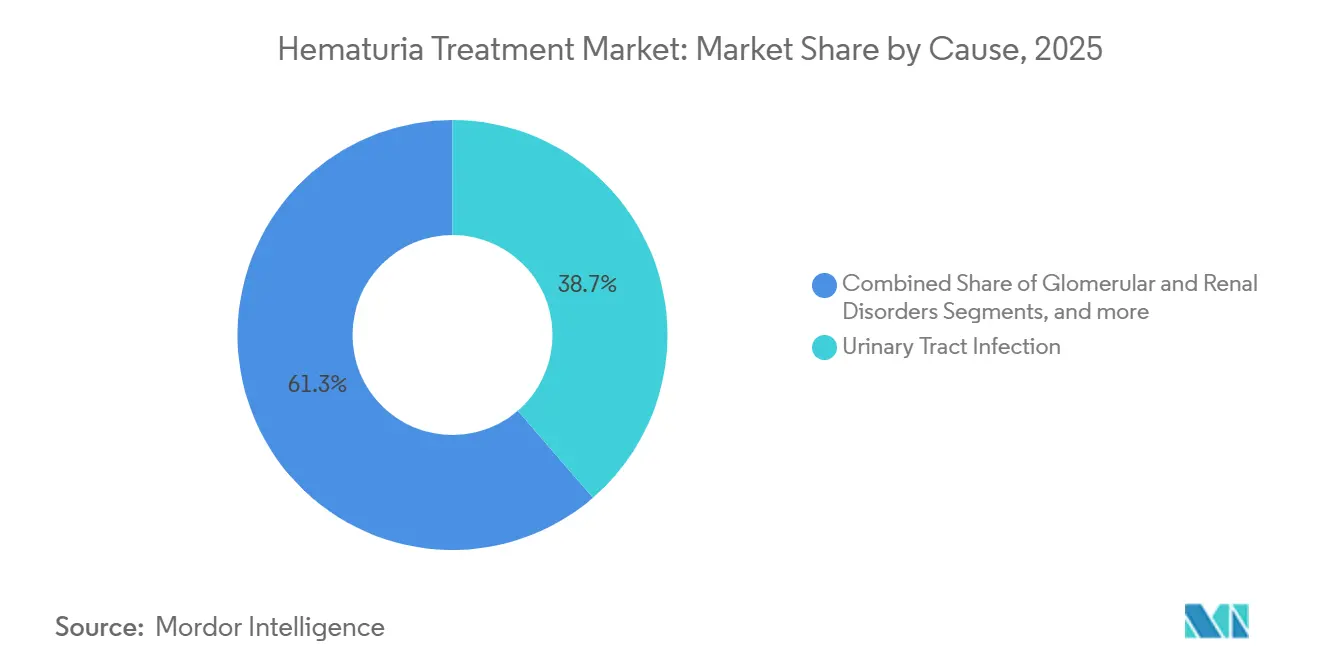

- By cause, urinary tract infection represented 38.65% of the hematuria treatment market size in 2025, while bladder cancer and upper tract urothelial cancer are expected to grow at a 4.55% CAGR through 2031.

- By end user, hospitals captured 46.93% share in 2025, while ambulatory surgical centers are expected to record the fastest growth at a 4.12% CAGR through 2031.

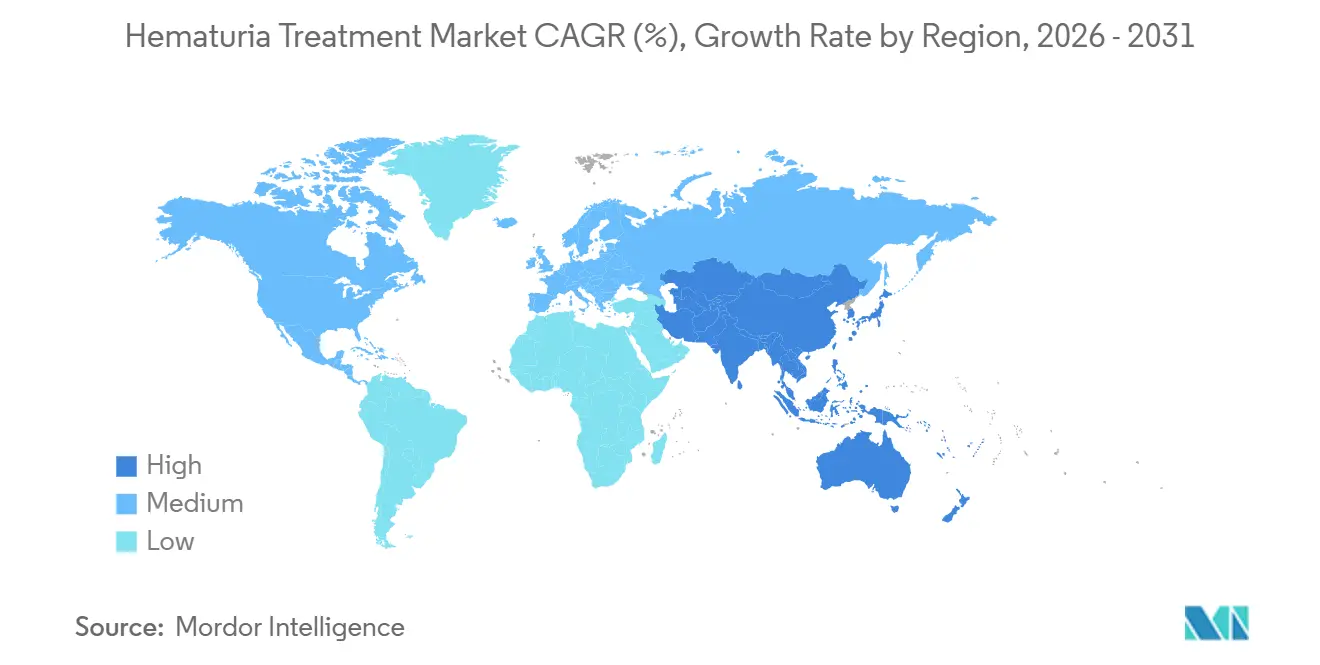

- By geography, North America held 41.25% of the hematuria treatment market share in 2025, while Asia-Pacific is projected to post the highest regional CAGR at 4.88% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hematuria Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burden of urological disorders and hematuria-linked conditions | +0.9% | Global, highest in South Asia, East Asia, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Wider use of risk-stratified hematuria pathways in routine care | +0.7% | North America and Western Europe, emerging uptake in East Asia | Medium term (2-4 years) |

| Expansion of urine-based biomarker use in intermediate-risk hematuria patients | +0.6% | North America, EU, Australia and New Zealand | Medium term (2-4 years) |

| Growth of outpatient, lower-acuity evaluation pathways | +0.5% | North America, urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Delayed referral and under-evaluation of women driving downstream treatment demand | +0.4% | Global, prominent in North America and Europe | Long term (≥ 4 years) |

| Rising need for cause-specific management beyond basic symptomatic care | +0.4% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Urological Disorders and Hematuria-Linked Conditions

The hematuria treatment market is driven by the high prevalence of conditions associated with blood in urine. In 2025, bladder cancer had an age-standardized incidence rate of 6.35 per 100,000 persons.[2]Urolithiasis, Bladder Cancer, Kidney Cancer, and Prostate Cancer From 1990 to 2021,” Military Medical Research, springer.com Urinary tract infections were the only major urological disease among six studied to show both rising incidence and mortality from 1990 to 2025. Urolithiasis affected 105.98 million people globally in 2025, with the disease burden concentrated in the 50 to 65 age group, aligning with those undergoing hematuria evaluations. Smoking caused 26.48% of global bladder cancer deaths and 28.15% of bladder cancer DALYs in 2025, linking future demand for hematuria treatments to tobacco-heavy regions like Southeast Asia and Sub-Saharan Africa. Additionally, high BMI contributed to 20.07% of kidney cancer deaths in 2025, reinforcing the need for evaluations and treatments in the hematuria market.

Wider Use of Risk-Stratified Hematuria Pathways in Routine Care

The hematuria treatment market is evolving with the adoption of risk-based evaluations. The AUA/SUFU 2025 Microhematuria Guideline Amendment categorized evaluations into negligible, low, intermediate, and high-risk groups. This approach reduced unnecessary cystoscopies for lower-risk patients while focusing on those with higher malignancy risks. The updated framework supports repeat urinalysis at six months for negligible-risk patients, extending outpatient contact points and reducing reliance on immediate procedural escalation. This shift emphasizes structured triage and follow-up testing, reshaping the market dynamics.

Expansion of Urine-Based Biomarker Use in Intermediate-Risk Hematuria Patients

Urine-based biomarkers are becoming a key component of the hematuria treatment market. The AUA 2025 update introduced urine-based tumor markers as alternatives to immediate cystoscopy for intermediate-risk patients, formalizing non-invasive testing in routine care. The STRATA trial showed that Cxbladder Triage reduced cystoscopies by up to 59% in microhematuria patients without compromising tumor detection.[3]Yair Lotan, et al., “A Multicenter Prospective Randomized Controlled Trial Comparing Cxbladder Triage to Cystoscopy in Patients With Microhematuria, The STRATA Study,” Journal of Urology, pubmed.ncbi.nlm.nih.gov A 2024 study highlighted a 3-gene methylation panel achieving an AUC of 0.94 and 84% sensitivity for bladder cancer detection. With intermediate-risk patients forming a significant portion of the microhematuria population, this trend strengthens the market's non-invasive diagnostic segment.[4]Daniel A. Barocas, Yair Lotan, Rachel S. Matulewicz, et al., “Updates to Microhematuria, AUA/SUFU Guideline (2025),” Journal of Urology, auajournals.org

Growth of Outpatient, Lower-Acuity Evaluation Pathways

The hematuria treatment market benefits from the shift of lower-acuity evaluations to outpatient settings. The updated guidelines streamline repeat urinalysis, biomarker testing, and selective cystoscopic follow-ups through ambulatory pathways, reducing dependence on hospital-based care. This transition aligns with the growing adoption of biomarkers, as laboratories and office-based practices are better equipped for repeated monitoring. By enabling standardized evaluations in outpatient settings, the market expands its delivery base and improves patient adherence.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Guideline-driven reduction in unnecessary testing for low-risk patients | -0.2% | North America, EU | Short term (≤ 2 years) |

| Limited clinical acceptance of urinary biomarkers in institutional settings | -0.1% | Global, most pronounced in low-to-middle-income Asia-Pacific and Latin America | Medium term (2-4 years) |

| High dependence on cystoscopy and imaging infrastructure for definitive workup | -0.1% | Sub-Saharan Africa, South Asia, Southeast Asia | Long term (≥ 4 years) |

| Treatment heterogeneity linked to the underlying cause of hematuria | -0.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Guideline-Driven Reduction in Unnecessary Testing for Low-Risk Patients

A key restraint in the hematuria treatment market is the strategic reduction of invasive testing for low-risk patients. The AUA 2025 amendment recommends repeat urinalysis within 6 months instead of immediate cystoscopy for negligible-risk patients, directly reducing near-term procedure demand in this group. The guideline also highlights that cancer detection rates in low-risk groups range from 0% to 0.4% over a median follow-up of 26 months, weakening the justification for broad invasive workups at initial presentation. While this does not eliminate demand, it shifts spending toward observation, repeat urinalysis, and selective escalation, slowing procedural revenue growth in lower-risk populations while higher-risk pathways remain active.

High Dependence on Cystoscopy and Imaging Infrastructure for Definitive Workup

The hematuria treatment market heavily relies on cystoscopy and imaging for definitive evaluations, particularly for intermediate and high-risk patients. The AUA guidelines continue to prioritize these methods, maintaining the need for procedural infrastructure despite advancements in diagnostics. This reliance creates challenges in regions with limited access to flexible cystoscopy equipment, radiology services, and trained urology professionals, such as parts of South Asia, Southeast Asia, and Sub-Saharan Africa. Consequently, the market's growth remains uneven across geographies, with infrastructure availability significantly influencing the conversion of clinical needs into commercial demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hematuria Type: Microscopic Hematuria Creates a Larger Long-Term Monitoring Base

In 2025, gross hematuria accounted for a 56.6% market share, highlighting its tendency to prompt immediate referrals and evaluations in emergency and urology settings. Patients with gross hematuria often undergo cystoscopy and upper-tract imaging, leading to a more intense procedural focus. However, the market sees greater long-term growth potential in microscopic hematuria, projected to expand at a 3.66% CAGR through 2031. A 2024 prevalence study highlighted that 34.1% of a surveyed adult cohort exhibited asymptomatic microscopic hematuria, a finding echoed by managed care data over a two-year span.

This is significant as the microscopic hematuria demographic offers the treatment market a broader base for recurring follow-ups compared to its gross counterpart. The 2025 AUA guideline shifted its approach, suggesting a 6-month repeat urinalysis for low-risk microhematuria, rather than an immediate invasive evaluation. This change potentially extends the duration patients remain within monitored care pathways. Given the emphasis on consistent urine microscopy and evaluations, standardized laboratory handling becomes paramount. Thus, while microscopic hematuria may seem less urgent initially, it proves to be a more sustainable focus for the treatment industry, as patients frequently return for monitoring, reclassification, and potential escalation of care.

By Treatment Type: Procedural Growth Improves as Intravesical Therapy Options Expand

In 2025, pharmacotherapy dominated the market with a 36.75% share, driven by antibiotics for urinary tract infections, agents for symptom relief, and intravesical therapies for bladder-cancer-related hematuria. Despite this lead, procedural and interventional therapies are growing faster, with a projected 3.95% CAGR through 2031. The FDA approved Zusduri, an intravesical mitomycin solution from UroGen Pharma, in 2025 for recurrent low-grade, intermediate-risk, non-muscle invasive bladder cancer. This approval was supported by the ENVISION trial, which reported a 78% complete response rate at 3 months, with 79% maintaining their status for a year or more.

Later in 2025, the FDA approved Inlexzo, a gemcitabine intravesical system from Janssen Biotech, for BCG-unresponsive, non-muscle invasive bladder cancer with carcinoma in situ. The SunRISe-1 trial highlighted an 82% complete response rate, marking it as the highest for any approved therapy in this category at the time. These approvals broaden treatment options and enhance pricing leverage for patients needing more than just antibiotics or basic care. Supportive therapies like bladder irrigation and anticoagulant management play a crucial role, bridging the gap between standard infection treatments and premium cancer interventions.

By Cause: UTI Anchors Volume While Bladder Cancer Drives Higher-Value Growth

In 2025, urinary tract infections (UTIs) constituted 38.65% of the hematuria treatment market's value, solidifying their status as the leading cause segment. This dominance stems from the global UTI burden, which saw 449.1 million new cases in 2025 and an upward trend in age-standardized incidence. Many UTI cases are initially addressed in primary care, ensuring consistent prescription demand, repeat consultations, and potential referrals for persistent hematuria. However, the UTI segment faces challenges from antibiotic resistance, fueling ongoing interest in advanced anti-infective strategies and tailored management.

Bladder cancer, alongside upper tract urothelial cancer, is the fastest-growing segment in the hematuria treatment market, with a projected CAGR of 4.55% through 2031. This growth aligns with recent regulatory approvals for intravesical bladder cancer therapies, notably Zusduri and Inlexzo in 2025, both of which broaden the treatment landscape for hematuria-related malignancies. Furthermore, global studies indicate a rising absolute caseload of bladder cancer, particularly in regions like China and affluent areas of East Asia, bolstering long-term demand. The industry sees more specialized investment in this segment compared to UTI, given the resource-intensive diagnosis and significantly higher treatment value per patient.

By End User: Hospitals Remain the Core Setting While Diagnostic Laboratories Gain Importance

In 2025, hospitals commanded a 46.93% market share, underscoring their pivotal role in managing patients with visible bleeding or malignancy concerns. This dominance persists as many patients require comprehensive evaluations that smaller outpatient facilities cannot provide. Concurrently, the market is gradually shifting parts of its evaluation process to specialty clinics and laboratories, especially for structured risk stratification. This transition is most pronounced in testing stages, like repeat urinalysis and urine microscopy, that don't necessitate inpatient resources.

Ambulatory surgical centers, projected to grow at a 4.12% CAGR through 2031, are the fastest-expanding segment in the hematuria treatment market. Their rising significance stems from the 2025 AUA framework, which formalizes urine-based biomarker testing for intermediate-risk patients, bolstering lab networks' roles in initial triage. Supporting this trend, the STRATA trial demonstrated that a urine test could reduce the need for cystoscopy without compromising tumor detection in microhematuria cases. In essence, while laboratories don't replace hospitals in the hematuria treatment market, they play an increasingly decisive role in determining patient pathways to specialized care.

Geography Analysis

In 2025, North America led the hematuria treatment market with a 41.25% share, driven by high awareness of urological cancers, better access to specialists, and rapid adoption of new therapies. The United States remained the primary revenue contributor, supported by two FDA approvals for intravesical therapies critical to managing bladder cancer-associated hematuria. Additionally, hematuria affected 8% to 11% of men over 40 with benign prostatic hyperplasia, ensuring steady demand for treatments beyond oncology.

Asia-Pacific is the fastest-growing region in the hematuria treatment market, with a projected 4.88% CAGR through 2031. Japan plays a key role, as national health checks identify 5% to 10% of the population as urine dipstick positive for hematuria, creating a consistent diagnostic funnel. In 2025, Ferring reported a 75% complete response rate for ADSTILADRIN in Phase 3 trials for BCG-unresponsive non-muscle invasive bladder cancer, enhancing the treatment outlook. China also contributes significantly, with Phase 3 data showing blue light cystoscopy with Hexvix improves bladder cancer detection compared to white light cystoscopy.

Europe remains a major market due to reimbursement systems in large countries that support cystoscopy, pathology, and intravesical therapies in routine care. The region benefits from established hospital and laboratory networks, ensuring smooth transitions from detection to treatment. Although growth is slower than in Asia-Pacific, standardized clinical pathways and high specialist evaluation rates maintain Europe’s market appeal. The Middle East, Africa, and South America, while smaller in market value, offer growth potential as urology infrastructure improves and more patients transition from underdiagnosis to formal treatment.

Competitive Landscape

The hematuria treatment market is moderately fragmented, with no single company controlling the entire process from initial urine testing to endoscopic evaluation and definitive therapy. Competition spans molecular diagnostics, imaging and endoscopy equipment, intravesical pharmacotherapy, and broader oncology or renal treatment portfolios. This structure ensures market diversity, as success in one area does not guarantee leadership across the care continuum. Pharmaceutical companies gain traction when a specific underlying cause is diagnosed, while device and diagnostics firms compete earlier in the patient journey. As a result, the market rewards focused category expertise over broad cross-segment scale.

Recent developments highlight how companies are strengthening their positions in the hematuria pathway. Photocure reported an increase in Hexvix and Cysview revenue from NOK 125.3 million in Q1 2025 to NOK 139.0 million in Q1 2026, reflecting continued growth in bladder cancer detection tools closely tied to hematuria evaluation. In June 2026, Photocure acquired Vesica Health and its AssureMDx multi-omic urine biomarker test, expanding its presence into non-invasive detection and triage. UroGen Pharma and Janssen Biotech enhanced their relevance in bladder-cancer-associated hematuria treatment in 2025 through FDA approvals for Zusduri and Inlexzo, moving beyond general urology.

Care gaps in the hematuria treatment market create opportunities for targeted expansion. Women with hematuria are often under-evaluated, delaying referrals and diagnoses in high-value bladder cancer pathways. There is also a need for better tools in managing anticoagulant-associated bleeding, repeat monitoring, and primary care triage. In October 2025, Ferring supported the competitive landscape by publishing expanded real-world evidence for ADSTILADRIN from private urology practice, advocating its use beyond controlled clinical trials. The hematuria treatment market remains active and opportunity-rich but lacks a dominant supplier across diagnostics, devices, and therapeutics.

Hematuria Treatment Industry Leaders

Pfizer Inc.

Sanofi

Novartis AG

Astellas Pharma Inc.

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Photocure ASA acquired Vesica Health Inc., enhancing its leadership in bladder cancer and urinary tract diseases with the addition of the AssureMDx multi-omic urine biomarker test.

- June 2025: The FDA approved UroGen Pharma's Zusduri, a mitomycin intravesical solution, for recurrent low-grade intermediate-risk NMIBC, with a 78% complete response rate at 3 months and 79% of responders maintaining results for 12 months or more.

- April 2025: Ferring presented Phase 3 data at the 112th Annual Meeting of the Japanese Urological Association, reporting a 75% complete response rate at 3 months for ADSTILADRIN in Japanese NMIBC patients.

Global Hematuria Treatment Market Report Scope

As per the scope of the report, hematuria is the medical term for the presence of blood in urine. It can be visible to the naked eye (gross hematuria, where urine appears pink, red, or cola-colored) or detectable only under a microscope (microscopic hematuria). It is not a disease itself but a symptom of an underlying condition, ranging from minor issues like vigorous exercise to serious problems such as infections, kidney stones, or cancers.

The hematuria treatment market is segmented by hematuria type, treatment type, cause, end-user, and geography. By hematuria type, the market includes gross hematuria and microscopic hematuria. By treatment type, the market is segmented into pharmacotherapy, procedural and interventional therapies, and adjunctive and supportive therapies. By cause, the market is categorized into urinary tract infection, urolithiasis, bladder cancer and upper tract urothelial cancer, benign prostatic hyperplasia, glomerular and renal disorders, and iatrogenic and anticoagulant-associated hematuria. By end-user, the market is segmented into hospitals, specialty urology clinics, ambulatory surgical centers, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Gross Hematuria |

| Microscopic Hematuria |

| Pharmacotherapy |

| Procedural and Interventional Therapies |

| Adjunctive and Supportive Therapies |

| Urinary Tract Infection |

| Urolithiasis |

| Bladder Cancer and Upper Tract Urothelial Cancer |

| Benign Prostatic Hyperplasia |

| Glomerular and Renal Disorders |

| Iatrogenic and Anticoagulant-Associated Hematuria |

| Hospitals |

| Specialty Urology Clinics |

| Ambulatory Surgical Centers |

| Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Hematuria Type | Gross Hematuria | |

| Microscopic Hematuria | ||

| By Treatment Type | Pharmacotherapy | |

| Procedural and Interventional Therapies | ||

| Adjunctive and Supportive Therapies | ||

| By Cause | Urinary Tract Infection | |

| Urolithiasis | ||

| Bladder Cancer and Upper Tract Urothelial Cancer | ||

| Benign Prostatic Hyperplasia | ||

| Glomerular and Renal Disorders | ||

| Iatrogenic and Anticoagulant-Associated Hematuria | ||

| By End User | Hospitals | |

| Specialty Urology Clinics | ||

| Ambulatory Surgical Centers | ||

| Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hematuria treatment market?

The hematuria treatment market stands at USD 1.18 billion in 2026 and is projected to reach USD 1.37 billion by 2031 at a CAGR of 3.12%.

Which region leads hematuria treatment demand?

North America leads with 41.25% share in 2025 because of stronger specialist infrastructure, payer coverage, and faster uptake of new therapies and diagnostic pathways.

Which region is growing the fastest for hematuria-related treatment?

Asia-Pacific is the fastest-growing region, with a 4.88% CAGR through 2031, supported by structured screening and stronger adoption in countries such as Japan and China.

Which hematuria type offers the strongest long-term opportunity?

Gross hematuria led with 56.45% share in 2025, but microscopic hematuria is expected to grow faster at a 3.66% CAGR because it creates a larger repeat-monitoring population.

What is driving growth in treatment options for bladder-cancer-related hematuria?

FDA approvals for Zusduri in June 2025 and Inlexzo in September 2025 widened intravesical treatment options and increased momentum in bladder-cancer-associated care.

Why are diagnostic laboratories gaining importance in this space?

Ambulatory Surgical Centers are expected to grow at a 4.12% CAGR through 2031 because urine-based biomarker testing now has a more formal role in triaging intermediate-risk patients.

Page last updated on: