Austria Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

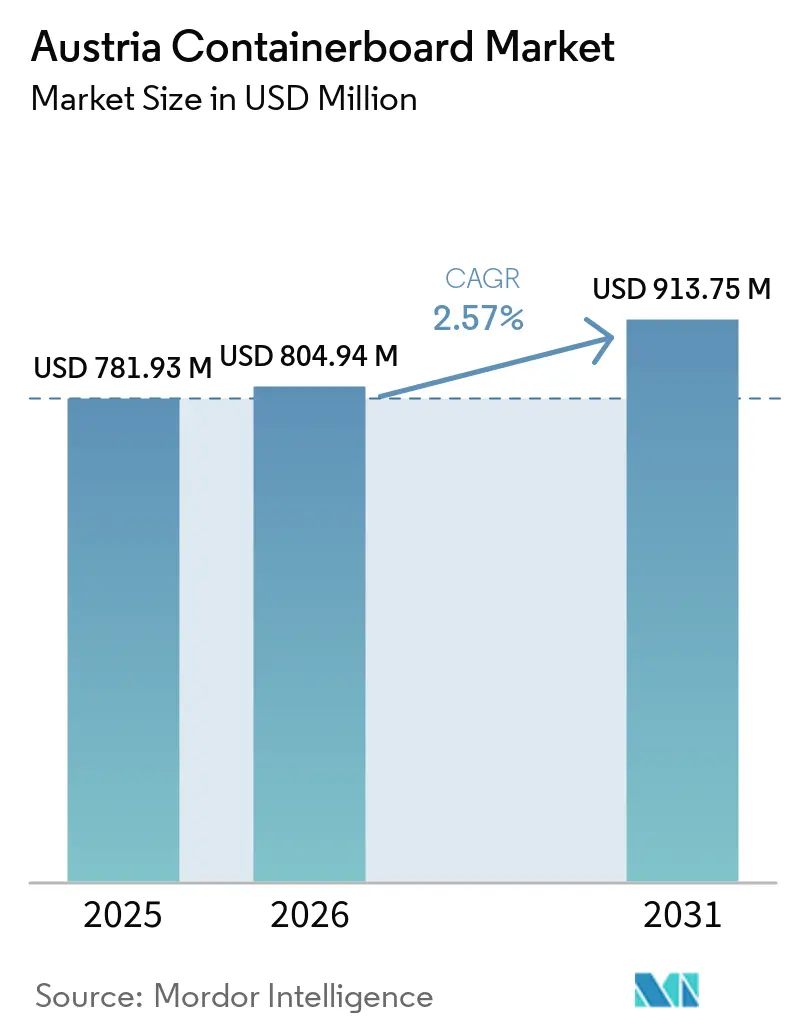

| Base Year Market Size (2025) | USD 781.93 Million |

| Market Size (2026) | USD 804.94 Million |

| Market Size (2031) | USD 913.75 Million |

| Growth Rate (2026 - 2031) | 2.57% CAGR |

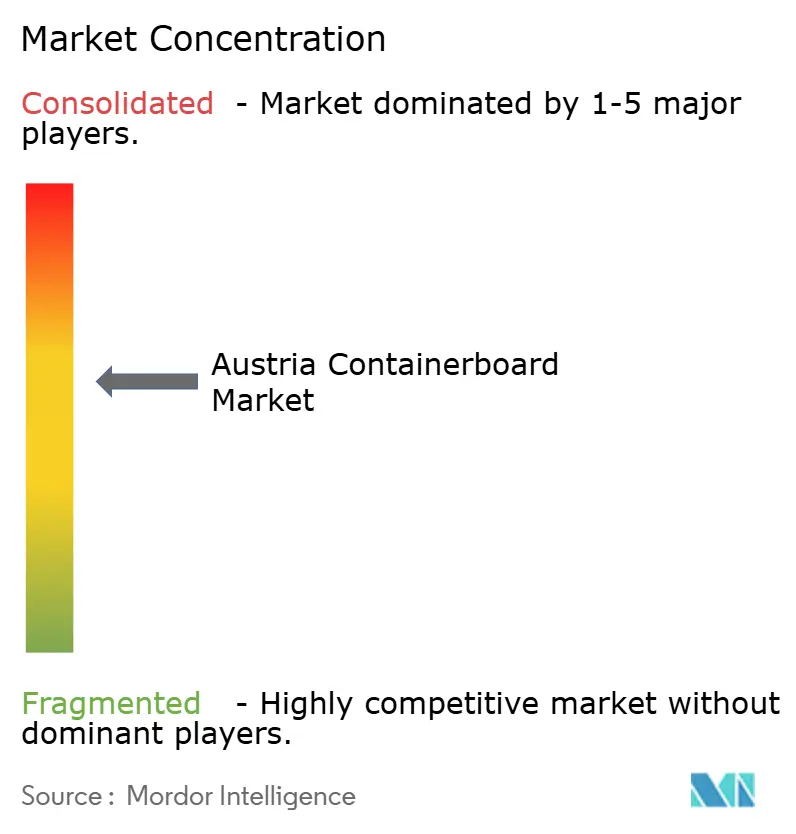

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Containerboard Market Analysis by Mordor Intelligence

The Austria containerboard market size is expected to grow from USD 781.90 million in 2025 to USD 804.94 million in 2026 and is forecast to reach USD 913.75 million by 2031 at 2.57% CAGR over 2026-2031. The market is moving on a steadier path after the recent pricing correction, and that reset is bringing more attention to structural demand than to short-term price swings. Recycled-fiber intensity remains a defining strength, with containerboard drawing on the deepest paper-for-recycling stream in Europe, while Austria also plays an outsized role in regional paper and board output relative to its economy. Demand is supported by record distance-trade spending, rising parcel activity, and the fact that food and beverage remains the largest corrugated application in the country, keeping the volume base resilient even as industrial activity softens. Regulation also supports the outlook because the EU packaging framework places heavier compliance pressure on competing packaging formats, while cardboard transport boxes avoid mandatory reuse quotas. Competition remains moderate at the mill level, and the conversion of graphic-paper capacity into packaging grades has increased domestic recycled-fiber supply and reduced reliance on German imports.

Key Report Takeaways

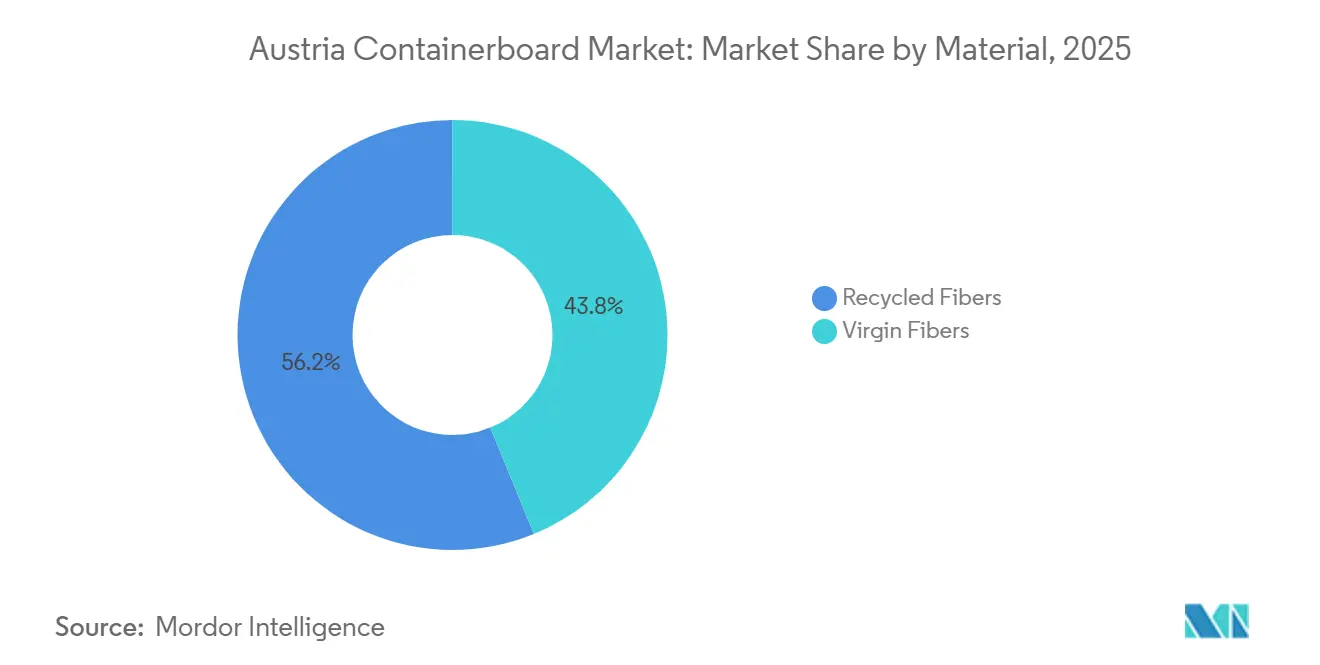

- By material, recycled fibers captured 56.18% of the Austria containerboard market share in 2025.

- By product type, the Austria containerboard market size for the testliners segment is forecast to advance at a 2.96% CAGR through 2031.

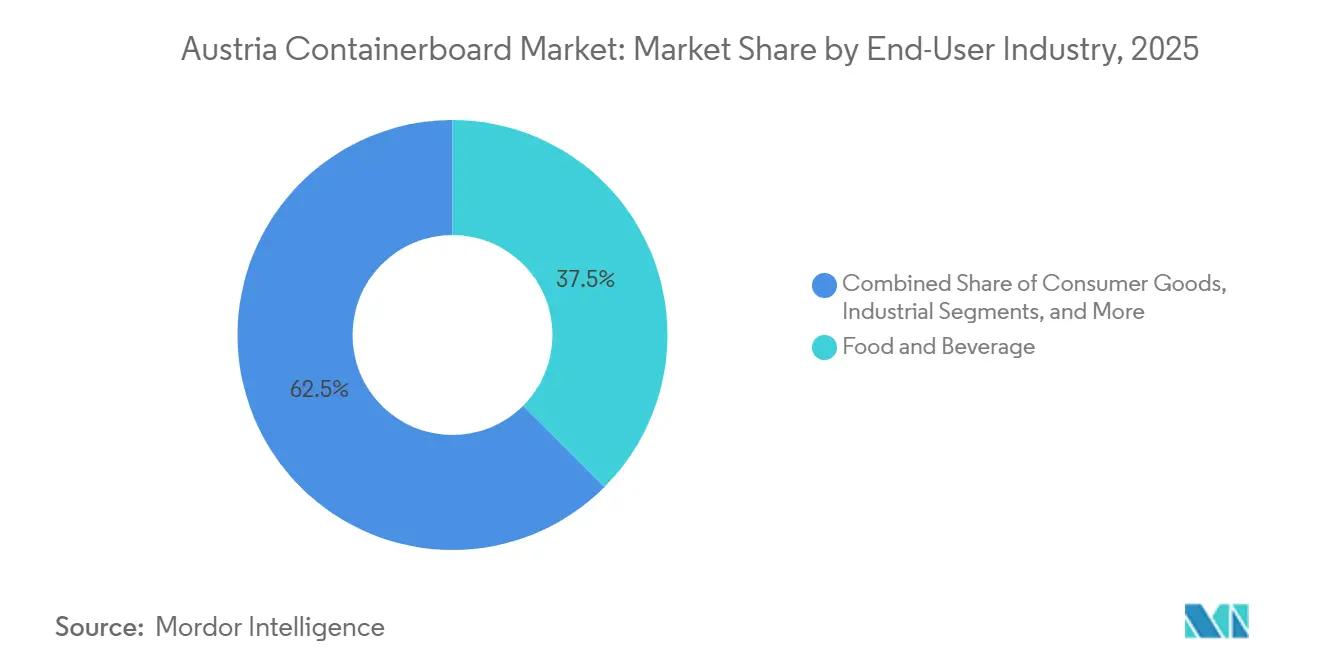

- By end-user industry, food and beverage captured 37.51% of the Austria containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Austria Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-To-Paper Substitution Under PPWR | +0.8% | Global, with primary compliance obligations active across all EU member states including Austria from August 2026 | Short term (≤ 2 years) |

| Food And Beverage Corrugated Demand Leadership | +0.6% | National, concentrated in Vienna, Upper Austria, and Styria agri-food processing clusters | Short term (≤ 2 years) |

| High Recycled-Fiber Circularity Advantage | +0.5% | National, with CEPI-wide spill-over through integrated paper-for-recycling supply chains | Medium term (2-4 years) |

| Shelf-Ready And E-Commerce Format Premiumization | +0.4% | National, with early gains in Vienna, Graz, and major logistics corridors | Short term (≤ 2 years) |

| Graphic-Paper Machine Conversions Expanding Domestic Supply | +0.3% | National, primarily Upper Austria, including Laakirchen and Steyrermühl | Short term (≤ 2 years) |

| Advanced Deinking Improving Recycled-Fiber Quality | +0.2% | National and EU-wide, with highest relevance at OCC-based recycled-fiber containerboard mills | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic-To-Paper Substitution Under PPWR

Plastic-to-paper substitution remains the strongest policy-led tailwind for the Austria containerboard market because Regulation (EU) 2025/40 will apply from August 12, 2026, and ties packaging design more closely to recyclability, fee modulation, and waste-reduction targets.[1]Publications Office of the European Union, “Regulation (EU) 2025/40 of the European Parliament and of the Council on Packaging and Packaging Waste,” Publications Office of the European Union, op.europa.eu This framework favors fiber formats because cardboard already fits high-circulation recovery systems more easily than multilayer and coated plastic alternatives. Austria enters that shift from a strong base because household collection reached 1.02 million tonnes of packaging and waste paper in 2024, and recycled corrugated packaging achieved an 85% recycling rate.[2]Austrian Federal Economic Chamber, “Paper and Packaging Sector, Key Statistics,” Advantage Austria, advantageaustria.org That raises the appeal of mono-material corrugated formats in procurement decisions where recyclability grades and future EPR cost exposure are becoming more important. In the Austrian containerboard market, this means compliance becomes part of the value proposition rather than just a regulatory cost. It also supports earlier switching decisions in transport, e-commerce, and food-service packaging, where competing materials now face a clearer redesign burden.

Food And Beverage Corrugated Demand Leadership

Food and beverage demand provides a stable base for the Austrian containerboard market, as this sector accounted for 46% of Austrian corrugated board production volume in 2025, up from 45% in 2024. That consistency matters because food shipments keep moving even when industrial packaging orders slow, so mills and converters retain a dependable floor for volume. Austrian agri-food exports also require food-safe transit packs and shelf-ready formats that often call for stronger liners and better print quality than those for commodity shipping cases. The deposit system for PET bottles and metal cans, introduced in January 2025, adds another packaging adjustment point because beverage distribution formats are being reworked around reuse and return logistics. In the Austrian containerboard market, food-led demand is tied not only to volume but also to specification quality. DS Smith’s recyclable beer-delivery solution for Privatbrauerei Hirt demonstrated that even narrower beverage channels are now producing packaging designs specifically tailored to corrugated performance needs.

High Recycled-Fiber Circularity Advantage

High recycled-fiber circularity is one of the deepest structural strengths of the Austrian containerboard market because recovered paper is both readily available and already embedded in industrial-scale paper production. Across CEPI countries, the paper-for-recycling utilization rate for containerboard grades reached 94.7% in 2024, the highest among paper categories, accounting for 66.4% of total paper-for-recycling volume consumed in paper and board manufacturing. Austria reinforces that system with strong household collection volumes and an 85% recycling rate for corrugated packaging, which improves supply visibility for OCC-based mills. Sorting quality is also improving, which supports lighter grammage production and better yield from old corrugated containers. Heinzelpaper Laakirchen started up Europe’s largest FibreFlow drum pulper in May 2025, with a capacity to process up to 2,000 admt per day, demonstrating that Austria's containerboard market players are investing in upstream efficiency rather than relying solely on spot-market fiber. This matters because the Austrian containerboard market can better absorb input volatility when fiber processing, paper production, and downstream converting are integrated within the same domestic system.

Shelf-Ready And E-Commerce Format Premiumization

Shelf-ready and e-commerce packaging is pushing the Austria containerboard market toward higher-value grades because box performance now matters more across more handling cycles and consumer-facing use cases. Austria’s e-commerce return rate rose to 44% in 2025 from 42% in 2024, increasing the share of shipments that require stronger boxes or re-boxing before resale.[3]Handelsverband Austria and KMU Forschung Austria, “E-Commerce Studie Österreich 2025,” OTS, ots.at Distance-trade spending reached EUR 12.5 billion (USD 14.1 billion), with mobile commerce at EUR 4.1 billion (USD 4.62 billion) in 2025, indicating continued demand for packaging across apparel, electronics, and personal care orders. That shift is important because it favors heavier liner grades, double-wall formats, and better visual presentation in both transit and shelf-ready use. Mondi’s brown kraftliner pack with white digital printing for Riedel Glas showed that premium graphics can now be delivered on uncoated brown substrates without moving away from recyclable paper-based formats. For the Austria containerboard market, this adds a value layer that sits above simple box volume growth and helps support selective premiumization even in a low-CAGR environment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Recovered-Paper And Energy Costs | -0.8% | National, most acute in Upper Austria and Styria, where energy-intensive mill clusters face grid-fee and ETS double-cost structures | Short term (≤ 2 years) |

| High Austrian Labor And Network Costs | -0.4% | National, particularly affecting converting plants in Lower Austria, Vienna, and Styria | Medium term (2-4 years) |

| Waste Classification Friction In Recovered-Paper Logistics | -0.2% | National, with early gains in Vienna and major logistics corridors | Medium term (2-4 years) |

| Reuse Quotas Threatening Fiber-Based Transport Packaging | -0.2% | EU-wide, with concentrated impact in fresh-produce and B2B logistics segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Recovered-Paper And Energy Costs

Cost volatility remains the largest near-term drag on the Austrian containerboard market because high electricity prices, grid fees, ETS burdens, and recovered paper movements all press on margins simultaneously. Austropapier reported that Austrian paper industry revenue fell 5.7% in 2025 to EUR 4.37 billion (USD 4.72 billion) while total paper production declined 7.6% to 4.09 million tonnes. In Upper Austria, industrial electricity averaged EUR 16.7 (USD 18.8) cents per kWh in 2025 versus EUR 8.8 (USD 9.9) cents in neighboring Bavaria, and grid fees were 75% higher than the Bavarian equivalent.[4]Austropapier, “Papierindustrie Fordert Strompreiskompensation Bis 2030,” Energy News Magazine, energynewsmagazine.at Austropapier also stated that the Austrian paper industry paid EUR 375 million (USD 406 million) in ETS-related costs in 2024 and received only EUR 185 million (USD 200 million) back in allocations. Heinzelpaper Laakirchen then raised corrugated case material prices in March 2024 and again in October 2025, showing how board-price adjustments continue to ripple through the value chain when costs remain elevated. In the Austria containerboard market, integrated players can absorb more of this pressure than open-market buyers, but converters without captive supply remain exposed to every new round of input inflation.

High Austrian Labor And Network Costs

Labor and logistics costs create a second structural brake for the Austrian containerboard market, as converting remains labor-intensive and Austria’s geography does not favor low-cost transport. Forum Wellpappe Austria reported that wage costs in the Austrian converting sector increased 27% over the 5 years through 2025. That rise outpaced productivity gains for many smaller plants, so cost competitiveness weakened even where shipment volumes held up. Export exposure makes the issue more serious because a large share of corrugated output still needs to compete on delivered cost against producers in Germany and Italy. DS Smith invested EUR 13 million (USD 14.1 million) across its Margarethen am Moos and Kalsdorf plants in 2024 to lift output by 20% through automation and line upgrades. In the Austrian containerboard market, this points to a clear divide: larger groups can protect margins through automation, while smaller, independent converters face rising pressure to consolidate or narrow their product focus.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Depth Meets Virgin Specification Premium

Recycled fibers held 56.18% of the Austria containerboard market share in 2025, which reflects the long shift of Austrian paper capacity away from graphic grades and toward OCC-based corrugated case material. This lead is supported by strong recovered paper collection and the country’s 85% recycling rate for corrugated packaging, which makes recycled furnish more secure and often more cost-effective than virgin input sourced from Nordic pulp markets. The Austria containerboard industry, therefore, keeps its largest value pool in recycled grades, especially where buyers prioritize circularity, cost visibility, and domestic fiber access. Heinzel Group strengthened that position in April 2025 when it completed the PM 11 conversion at Laakirchen and confirmed the site’s full transition to recycled corrugated base paper production.

Virgin fibers are still forecast to grow faster at a 2.91% CAGR through 2031, suggesting selective premiumization rather than a reversal of recycled-grade dominance. Demand is coming from applications where burst strength, stacking performance, or moisture resistance matters more than maximum recycled content, including export packaging, automotive parts transit, and pharmaceutical cold-chain use. The PPWR-linked restriction on PFAS-containing packaging solutions from August 2026 will further this shift, as compliant barrier and strength performance will matter more in specification decisions. Smurfit WestRock’s Nettingsdorf mill remains central to this part of the Austrian containerboard market, with 507,000 tonnes of annual kraftliner capacity and a cost position that ranks among the strongest in Western Europe. The material mix is therefore becoming more specialized, with recycled fiber retaining the larger base and virgin fiber gaining where higher-performance packaging earns a premium.

By Product Type: Kraftliner Scale Anchors Market, Testliner Drives Growth

Kraftliners accounted for 38.87% of market value in 2025, making them the leading product type in the Austrian containerboard market. Their position is tied to export-oriented corrugated packaging that needs a strong outer facing and reliable print performance for retail and logistics use. Nettingsdorf provides Austria with a durable base in this grade because Smurfit Kappa identified the mill as one of the 3 largest and lowest-cost kraftliner sites in Western Europe. That scale matters because the Austria containerboard market can supply demanding domestic and export customers without depending heavily on imported virgin-fiber linerboard.

Testliners are forecast to grow fastest at a 2.96% CAGR through 2031 as recycled-grade capacity expands and sustainable secondary packaging moves further into mainstream procurement. Heinzel’s PM 11, backed by EUR 140 million (USD 151.2 million) of investment, was built around lightweight recycled corrugated base paper in the 70-160 g/m² range under the Starboard brand. Norske Skog’s Bruck mill adds another pillar with 210,000 tonnes of annual recycled testliner and fluting capacity and record containerboard deliveries in 2025. Voith’s XcelLine technology on PM 11 also helps reduce energy use per tonne, which is important in Austria's containerboard market, where electricity costs remain unusually high. The result is a product mix where kraftliner anchors scale and testliner captures most of the incremental growth.

By End-User Industry: Food Anchors Demand, Consumer Goods Accelerates

Food and beverage accounted for 37.51% of the Austria containerboard market size by value in 2025, and it remained the largest end-user segment because food transit packaging is less cyclical than most other box demand. The same sector also accounted for 46% of Austrian corrugated board production volume in 2025, confirming how deeply food demand supports the volume base for the Austrian containerboard market. This demand is shaped by both domestic distribution and export flows into nearby retail networks, where shelf-ready trays and high-graphic packs often carry higher board-value intensity than plain transport boxes. That makes food demand important not only because it is large, but also because it supports a better mix in premium liners and display-ready structures.

Consumer goods are forecast to grow fastest at a 3.02% CAGR through 2031, driven by distance trade expansion and packaging changes in electronics, personal care, toys, and other online-led categories. Austria’s distance-trade spending increased 14% to EUR 12.5 billion (USD 13.5 billion) in 2025, and the online return rate reached 44%, which raises both first-use and secondary packaging needs. That matters because returned items often need new corrugated packs before resale, so demand rises faster than one-way order counts alone suggest. Industrial end users still accounted for close to 20% of corrugated volume in 2025, but their share moved lower as Central European manufacturing remained soft. In the Austria containerboard market, this leaves food as the stabilizer, consumer goods as the faster mover, and industrial packaging as the main segment that depends on a wider manufacturing recovery after 2026.

Geography Analysis

Austria accounted for 5.6% of total CEPI paper and board production and 5.0% of paper-for-recycling utilization in 2024, underscoring the country’s significant role in Europe relative to its economic size. Paper and cardboard production reached 4.4 million tonnes in 2024, and 87.5% of that output went to export markets, keeping the Austrian containerboard market closely tied to wider European demand conditions. Germany remained the main cross-border anchor for sales and sourcing, reflecting the close operational link between Austrian mills and the DACH packaging network. Upper Austria is the core production region because it hosts Heinzel’s Laakirchen complex, Smurfit Kappa’s Nettingsdorf kraftliner mill, and Norske Skog’s Bruck mill, creating a dense containerboard manufacturing cluster in one state.

Lower Austria and Styria add different roles to this geography. Lower Austria includes Hamburger Containerboard’s Pitten mill, where Prinzhorn Group commissioned a new gas turbine power plant in September 2025, investing more than EUR 50 million (USD 54 million). Styria supports the Austrian containerboard market by converting capacity that serves automotive, electronics, and consumer goods export corridors to southeastern Europe. Vorarlberg also matters because Rondo Ganahl launched a new BHS SPEED Line in Frastanz in January 2025, increasing site capacity by 10% to 220 million m² annually. Carinthia contributes through Mondi Frantschach and Mondi Neusiedler’s wider Austrian sustainability footprint, while Vienna remains the main logistics and distribution hub for finished corrugated packaging.

The Austria containerboard market also benefits from an energy and sustainability profile that helps in procurement discussions with brand owners. Austropapier reported that the Austrian paper industry’s renewable energy share stood at 69.2%, and new wastewater and biogas systems at major sites are strengthening mill-level environmental performance. Export dependence still makes the market sensitive to German and Central European industrial conditions, especially when packaging demand from machinery and automotive customers slows. At the same time, the Austrian containerboard market remains competitive because quality certifications, food-safe paper standards, and circular-fiber credentials align well with the packaging requirements becoming more common under the EU regulatory framework.

Competitive Landscape

The Austria containerboard market is moderately concentrated at the mill level, with 3 producers accounting for most of the domestic paper output, even though the converting base is broader and more fragmented. Smurfit Westrock anchors virgin-fiber supply at Nettingsdorf with 507,000 tonnes of annual kraftliner capacity, while Heinzel Group operates up to 1 million tonnes per year of recycled corrugated base paper capacity across 2 machines in Laakirchen, and Norske Skog adds 210,000 tonnes of recycled testliner and fluting at Bruck. That scale creates a meaningful barrier for mid-sized European entrants because Austria's containerboard market demand can already be served by mills with strong capacity positions and established regional customer ties. It also means competitive advantage is shaped as much by integration and cost structure as by simple paper-machine capacity.

Vertical integration remains the clearest strategic pattern in the Austria containerboard market. Prinzhorn Group combines recycling, paper production, and converting assets, and its validated Science Based Targets add a procurement advantage amid customers' tightening decarbonization requirements. Heinzel’s April 2025 PM 11 start-up and the linked ANDRITZ pulping system simultaneously expanded the domestic recycled-fiber scale and improved feedstock processing depth. Smurfit Westrock’s 2024 combination turned Nettingsdorf into a more important node within a much larger European corrugated system, strengthening customer reach and supply flexibility for the Austrian containerboard market. Rondo Ganahl is also broadening its position through fiber-cast molded pulp packaging, which complements corrugated board in protective applications and extends its role beyond conventional box converting.

Competitive pressure remains because Western Europe added fresh containerboard capacity in 2024 and 2025, and Billerud reported weaker regional demand in the second and third quarters of 2025. That overcapacity risk is more difficult for non-integrated converters in the Austria containerboard market, since open-market board prices can move against them even when their own order books are steady. Larger Austrian groups are responding with acquisition and automation rather than retreat, as seen in Dunapack Packaging’s April 2026 agreement to acquire 3 German corrugated plants from Stora Enso. The likely outcome is a market where mill-level concentration stays firm, converter consolidation continues, and technology-led efficiency becomes more important to preserving margins than simple volume growth alone.

Austria Containerboard Industry Leaders

PRINZHORN HOLDING GmbH

W. Hamburger GmbH

Rondo Ganahl Aktiengesellschaft

Mondi plc

Heinzel Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Dunapack Packaging (Prinzhorn Group) agreed to acquire Stora Enso's 3 German corrugated packaging plants (Gaster Wellpappe, Wellpappe Sausenheim, and PTI), with a combined 2025 turnover of approximately EUR 74 million (USD 83.6 million) and 350 employees. The deal, pending merger clearance and expected to close in 2026, enhances Prinzhorn Group's paper-integration rate and extends its geographic footprint into southwestern Germany.

- April 2026: Mondi Neusiedler (Austria) reached 1 year of Zero Waste to Landfill operations, diverting wood ash to the cement industry as a raw material additive. The milestone marks Neusiedler's alignment with Mondi's MAP2030 sustainability framework and follows Frantschach's years-long landfill-free record.

- September 2025: Prinzhorn Group published its Sustainability Report 2024, highlighting Dunapack Packaging's use of over 90% recycled paper in its corrugated packaging and progress on decarbonization and renewable-energy targets.

- September 2025: Hamburger Containerboard (Prinzhorn Group) commissioned a new gas-fired power plant at its Pitten, Austria containerboard site, representing an investment of over EUR 50 million (USD 54 million) to secure long-term energy supply and stabilize operating costs.

Austria Containerboard Market Report Scope

The Austria Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The increasing demand for sustainable, lightweight, and durable packaging solutions drives the market.

The Austria Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Austria containerboard market size in 2026 and what is the 2031 outlook?

The Austria containerboard market is estimated at USD 804.94 million in 2026 and is projected to reach USD 913.75 million by 2031 at a 2.57% CAGR.

What is driving demand for containerboard in Austria?

The main demand drivers are food and beverage packaging, distance-trade growth, stronger e-commerce packaging needs, and regulatory support for recyclable fiber-based formats.

Which material type leads demand in Austria?

Recycled fibers led with 56.18% share in 2025 because Austria has strong recovered-paper collection and a well-developed recycled-fiber supply chain.

Which product type is growing fastest in Austria containerboard?

Testliners are the fastest-growing product type, with a projected 2.96% CAGR through 2031, supported by new recycled-grade capacity and sustainability-led procurement.

Why is food and beverage so important to containerboard consumption in Austria?

Food and beverage held 37.51% of market value in 2025 and accounted for 46% of corrugated board production volume, which gives the market a stable demand base.

What are the main risks facing producers and converters in Austria?

The main risks are high electricity and ETS costs, volatile recovered-paper pricing, rising labor costs, and weaker industrial packaging demand in Central Europe.

Page last updated on: