Australia Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

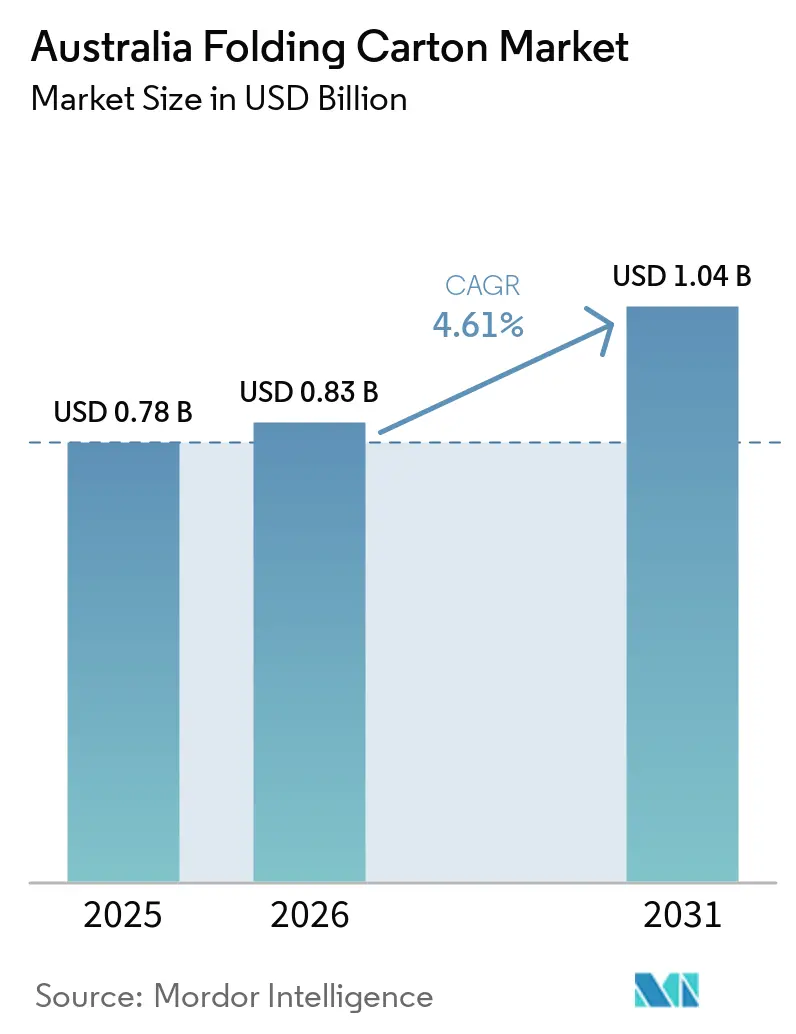

| Base Year Market Size (2025) | USD 0.78 Billion |

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.04 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

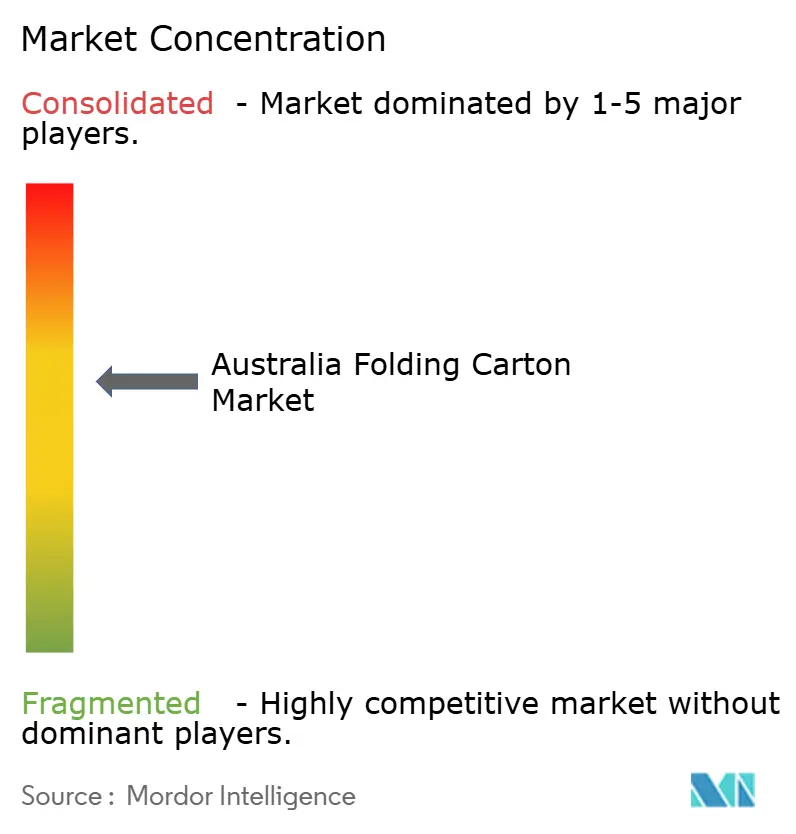

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Folding Carton Market Analysis by Mordor Intelligence

The Australia folding carton market size is expected to increase from USD 0.78 billion in 2025 to USD 0.83 billion in 2026 and reach USD 1.04 billion by 2031, growing at a CAGR of 4.61% over 2026-2031. A rebound in domestic converting activity is underway as brand owners pivot toward fiber-based formats that satisfy recycled-content mandates, while e-commerce fulfillment centers drive demand for crash-lock and shelf-ready designs that automate efficiently. Converters with vertically integrated mills enjoy a cost buffer against import price swings, yet smaller players remain exposed to pulp volatility and freight surcharges that compress margins. Automation investments, notably in HP Indigo and Hanway inkjet lines, are reshaping production economics by reducing setup times and labor dependence. Consolidation has narrowed the field to a handful of scale competitors, and the entrance of commercial printers such as IVE Group underscores the competitive stakes surrounding high-graphics, short-run contracts.

Key Report Takeaways

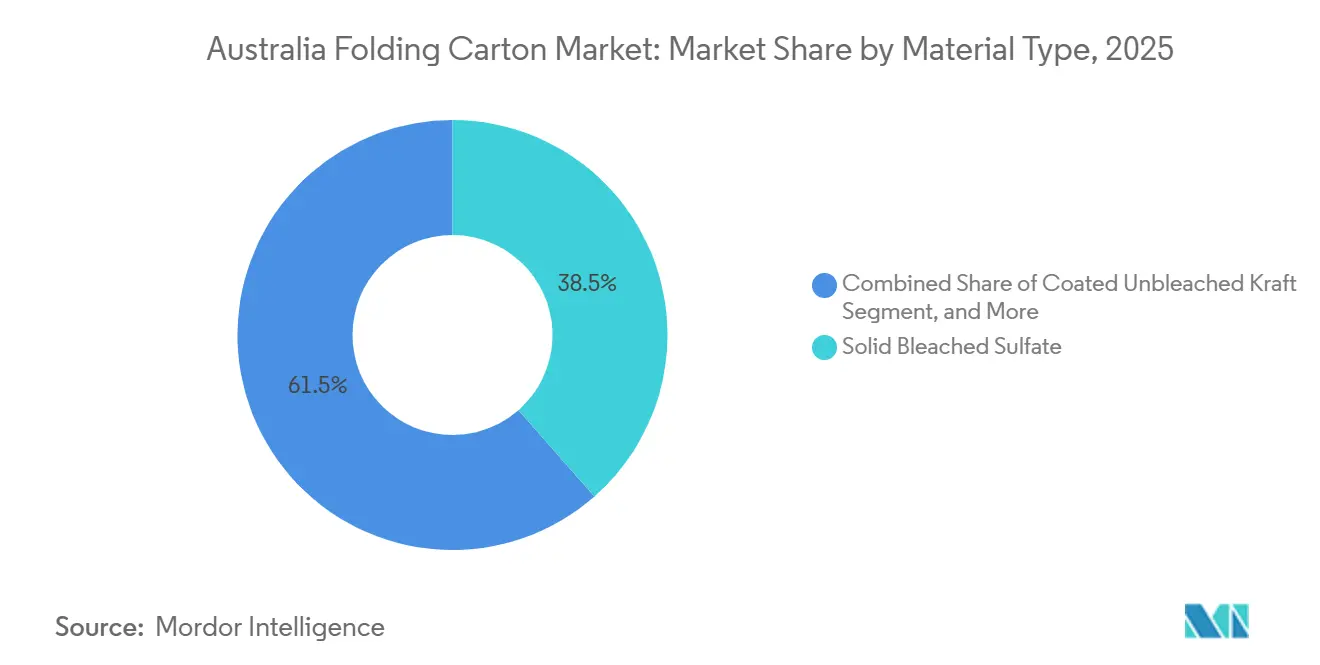

- By material type, solid bleached sulfate captured with 38.53% of the Australia folding carton market share in 2025.

- By printing technology, the Australia folding carton market size for digital printing is projected to grow at a 6.78% CAGR to 2031.

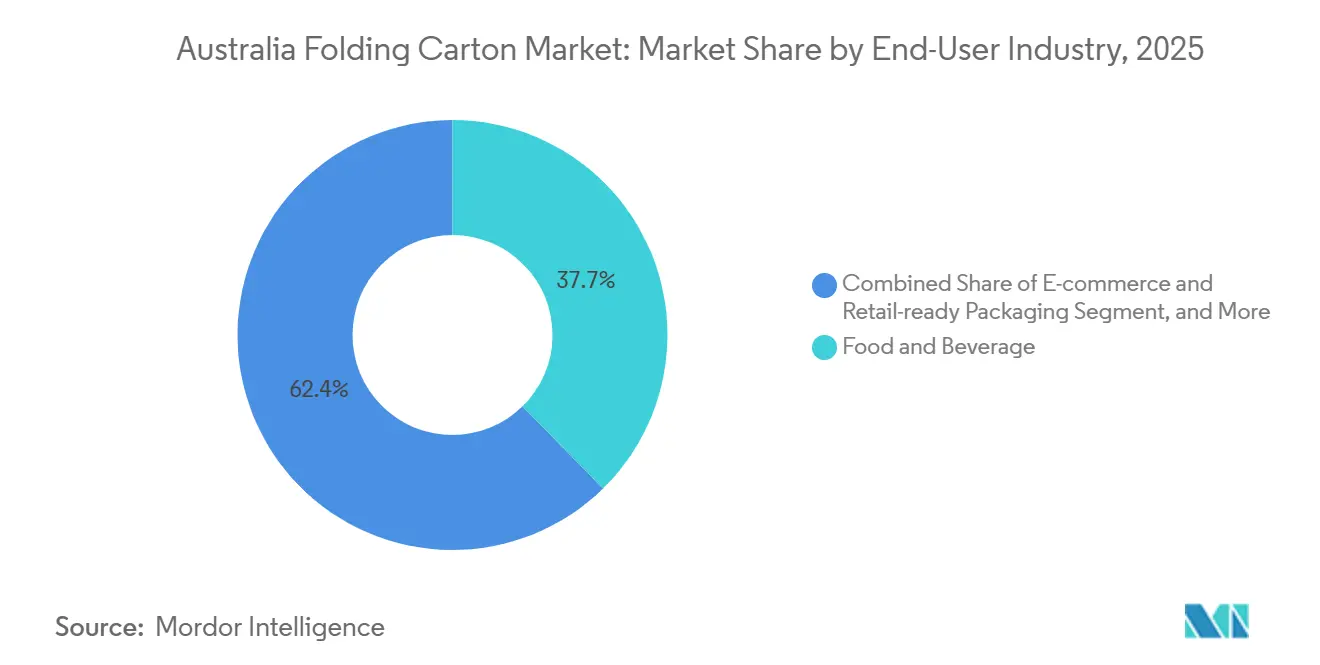

- By end-user industry, the food and beverage industry captured 37.65% of the Australia folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable Packaging Solutions | +1.2% | National, concentrated in Victoria and New South Wales | Medium term (2-4 years) |

| Growth of E-commerce Fulfillment Centers | +0.9% | Sydney, Melbourne, and Brisbane metro regions | Short term (≤ 2 years) |

| Increasing Investments in Automated Carton Converting Lines | +0.7% | Victoria and New South Wales manufacturing hubs | Medium term (2-4 years) |

| Expansion of Ready-to-Eat Meal Delivery Services | +0.6% | Capital-city catchments nationwide | Short term (≤ 2 years) |

| Brand Owner Shift Toward High-Graphics Shelf Displays | +0.5% | National retail channels | Medium term (2-4 years) |

| Government Procurement Targets for Recycled Content | +0.4% | Federal and state contracts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Packaging Solutions

Federal and state policy now requires a minimum 60% post-consumer recycled content in paper and paperboard by 2030, pressuring brands to specify FSC-certified or recycled-fiber boards for food, beverage, and personal-care SKUs. National tonnage data show cartonboard recovery trails target levels, positioning the Australia folding carton market as a pivotal lever for circular-economy gains. Converters such as Visy and Opal promote internally sourced recycled liners to reassure brand owners on supply continuity. Product launches like Visycell, a kerbside-recyclable insulation liner, illustrate how fiber innovations are displacing EPS foams in temperature-sensitive chains.[1]Visy, “Visy Opens Australia’s Most Advanced Corrugate Box Factory,” visy.com.au Compliance audits linked to ISO 14001 have become routine in retailer procurement scorecards, embedding environmental metrics into contract awards.

Growth of E-commerce Fulfilment Centers

Supply-chain redesign toward direct-to-consumer distribution elevates demand for crash-lock cartons tailored to automated erecting lines. Abbe Group’s post-acquisition footprint in Far North Queensland and New South Wales now feeds regional grocery fulfillment nodes, shortening lead times and trimming inventory buffers. IVE Group’s 42,000 m² Kemps Creek supersite integrates converting, 3PL and brand activation, enabling synchronized carton replenishment with warehouse management systems. Fanfold systems cut pallet requirements by up to 80%, freeing high-cost floor space for fast-moving inventory. These dynamics widen the service gap between digitally enabled converters and legacy plants that rely on manual packing lines.

Increasing Investments in Automated Carton Converting Lines

Digital presses such as the HP Indigo 35K and Hanway HighJet 2500 enable economical runs of 5,000 units or fewer and variable-data capabilities that meet pharmaceutical serialization requirements. Pakko reports job-to-dispatch cycles compressed from 10 days to 8 days after installing a HighJet printer, while Affinity Print’s Century die cutter and CartonFold gluer lift throughput to 7,500 sheets per hour and 500 m min-¹, respectively. These capital programs mitigate Fair Work Commission wage escalations by trimming manual stripping and gluing hours.

Expansion of Ready-to-Eat Meal Delivery Services

Meal-kit brands demand sleeves and ovenable cartons engineered for moisture control and tamper-evidence, pushing converters to validate hot-fill, stack, and courier motion tests before commercial release. CBS Printing and Platypus Print Packaging now quote 7-10 business-day lead times to satisfy weekly menu refresh cycles. Temperature-range composites such as Multisteps Industries’ CPET trays (-40 °C to +220 °C) pair with carton sleeves that must maintain structure during microwave reheating. Certifications including SQF, HACCP and ISO 22000 separate approved suppliers from general-commercial printers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Cartonboard Import Prices | -0.8% | Import-dependent converters nationwide | Short term (≤ 2 years) |

| Rising Labor Costs in Converting Operations | -0.6% | Victoria and New South Wales metro manufacturing zones | Medium term (2-4 years) |

| Competition From Flexible Pouches in Snack Formats | -0.4% | Confectionery and snack clusters nationwide | Medium term (2-4 years) |

| Capacity Constraints in Domestic Paperboard Mills | -0.3% | Specialty-grade supply bottlenecks nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Cartonboard Import Prices

IndustryEdge price indices recorded a 23.5% year-on-year spike to January 2023, followed by a 7.7% retreat by May 2024, underscoring exposure for converters locked into fixed-price agreements.[2]IndustryEdge, “Australian Packaging Paper Price Index Up 23.5% Quarter-Ended January,” industryedge.com.au Domestic mills cannot yet produce all specialty food-contact grades, so reliance on the spot market persists. Federal and state funding of USD 5.3 million to upgrade the Canning Vale MRF aims to tighten fiber contamination to 5% and boost local furnish quality, yet timelines stretch beyond immediate procurement cycles.

Rising Labor Costs in Converting Operations

The Manufacturing and Associated Industries Award sets minimum hourly rates at AUD 28.12 (USD 18.8) for trades, with overtime up to 200% and public-holiday penalties at 250%. Around-the-clock schedules needed for supermarket just-in-time delivery multiply those premiums. Converters are therefore accelerating robotics adoption on folder-gluer lines and installing automatic palletizers that reduce headcount on night shifts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Boards Accelerate in Foodservice

Solid Bleached Sulfate held 38.53% of revenue in 2025, securing prestige cosmetics, high-gloss beverage packs, and regulated pharmaceutical SKUs that demand brightness and purity. The Australia folding carton market size for Coated Unbleached Kraft is poised to grow the fastest, at a 5.86% CAGR through 2031, as restaurant chains and ready-meal labels adopt natural brown tones that signal sustainability without compromising grease resistance. Brand mandates for 60% recycled content are steering mid-tier confectionery and cereal brands toward Folding Boxboard blends that balance stiffness with print fidelity.

Growing recycled-fiber quotas require converters to certify that kraft substrates meet migration limits for direct food contact under Food Standards Australia New Zealand rules. Integrated producers such as Visy, which manufactures 100% recycled liner, enjoy an assured furnish, whereas independents must secure allocation from merchant mills, exposing them to price swings. Traceability audits tied to FSC and PEFC chain-of-custody have become default bid requirements, locking non-certified plants out of high-volume tenders. The Australian folding carton market share tied to specialty metalized or barrier-coated boards remains small, but demand persists in frozen food and pharmaceutical blister cards where puncture resistance is mandatory.

By Printing Technology: Digital Raises the Bar for Short Runs

Lithographic presses accounted for 44.89% of segment revenue in 2025, anchored by long-run beverage and confectionery work that values tight color control. Digital units are projected to notch a 6.78% CAGR, capturing SKU proliferation and variable-data jobs such as pharmaceutical serialization. The Australia folding carton market, now tied to digital output, benefits from water-based inks that meet direct food-contact rules. Flexographic lines hold mid-run volumes, where inline die-cutting and folder-gluing offset time lost during changeovers, yet the quality gap with offset has narrowed with high-definition plates.

HP Indigo 35K installations enable converters to run 250-micron boards with inline foil and spot varnish in a single pass, eliminating the need for separate embellishment stages. Case studies show converters raising job count per shift by 80% after integrating PrintOS AI scheduling. The Australia folding carton market share of gravure continues to erode because cylinder lead times clash with rapid campaign cycles, although ultra-high-volume tobacco packs still justify the upfront tooling. Hybrid flexo-inkjet lines are emerging for security coding, but they remain a niche.

By End-User Industry: Online Channels Outpace Legacy Segments

Food and beverage applications accounted for 37.65% of revenue in 2025, driven by supermarket private-label expansion and meal-kit services that require tamper-evident sleeves and ovenable trays. E-commerce and retail-ready packaging will see the quickest gains, with a 6.45% CAGR projected to 2031. The Australia folding carton market size tied to these online channels is buoyed by fulfillment centers that reward carton dimensions optimized for robotic picking. Pharmaceutical and personal-care converters leverage digital presses for lot coding, braille embossing, and premium textures that help products stand out on crowded shelves.

Electrical and electronics brands specify anti-static coatings and molded-fiber inserts that stabilize gadgets in parcel networks. Tobacco volumes are steady but highly regulated, while household goods face substitution from flexible pouches. The Australia folding carton market share linked to produce growers is improving, thanks to carton-based berry punnets that displace PET clamshells under retailer plastic-reduction targets.

Geography Analysis

Victoria and New South Wales anchor the bulk of Australia folding carton market capacity, aligning with dense consumer populations and proximity to integrated paperboard mills. Melbourne’s southeast corridor hosts IVE’s Keysborough plant, Abbe’s Noble Park operation, and Opal’s Wodonga facility, enabling same-day truck routes into supermarket DCs. New South Wales houses Smurfit WestRock’s 30,000-tonne Richmond converter and IVE’s Silverwater site, both plugged into Western Sydney’s logistics grid that serves the nation’s largest e-commerce hub.

Queensland gained share after Abbe folded in Oji’s Yatala plant and Visy opened a USD 117 million corrugated factory in Hemmant. These assets now dispatch cartons north into the horticulture belts of Far North Queensland and south to fulfillment centers in Brisbane. Tasmania, traditionally reliant on mainland supply, now benefits from Visy’s USD 13.4 million Devonport hub, which cuts lead times for berry growers and dairy processors.[3]Visy, “Visy Opens New Tasmanian Packaging Hub,” visy.com.au

State-based deposit-return schemes prompt regional design tweaks, and the Western Australia fiber-quality upgrade, funded in 2026, should lower contamination to below 5%, improving furnish suitability for coated boards. Pharmaceutical and cosmetics work clusters in Victoria, leveraging a specialist labor pool and multiple GMP-certified co-packers. Produce and seafood shippers dominate in Queensland and Tasmania, valuing moisture-resistant liners and rapid turnaround over luxury finishing.

Competitive Landscape

Consolidation has produced a moderately concentrated Australia folding carton market, with the five largest players controlling an estimated 81% of sector revenue. Vertically integrated Visy and Opal secure furnish self-sufficiency, while Abbe’s November 2025 purchase of Oji Fiber Solutions Australia lifted its share to roughly 16% of combined corrugated and folding-carton sales.[4]Abbe Group, “Abbe Expands National Capability with Acquisition of Oji’s Cardboard Manufacturing Business,” abbe.com.au Smurfit WestRock’s 2026 merger embeds its Richmond plant within a USD 34 billion global network that wields scale procurement for inks, plates, and digital systems.

IVE Group is converting commercial-print relationships into packaging contracts; its USD 23 million JacPak buyout, along with the Kemps Creek supersite, signals ambitions to reach USD 150 million in carton revenue by 2028. Smaller independents, such as Platypus Print Packaging, Pakko, Networkpak, and Labelmakers, differentiate via rapid lead times, digital embellishment, and pharmaceutical serialization. Barriers to entry include ISO 9001, HACCP, and FSC chain-of-custody, as well as Federal import testing for recycled-content migration.

White-space growth lies in e-commerce fanfold systems, fiber-based alternatives to plastic insulation, and water-based barrier coatings for frozen foods. Converters with HP Indigo-enabled versioning capabilities win tender points on SKU proliferation, while robotics on gluer lines offset double-time wage rates. Strategic partnerships with recovered-fiber aggregators will increasingly influence bid competitiveness as government procurement shifts to closed-loop criteria.

Australia Folding Carton Industry Leaders

Visy Industries Holdings Pty Ltd

Opal Packaging Australia Pty Ltd

Orora Limited

Abbe Corrugated Pty Ltd

Smurfit Westrock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Australian and Western Australian governments awarded USD 5.3 million to Re. Group to upgrade the Canning Vale MRF, aiming for 5% fiber contamination by July 2026.

- March 2026: IVE Group brought its 42,000 m² Kemps Creek supersite online, combining carton converting with 3PL services.

- February 2026: Visy inaugurated a USD 13.4 million packaging hub in Devonport, Tasmania, strengthening supply to berry growers and breweries.

- February 2026: Orora reported USD 757 million half-year revenue, with can volumes up 11.2%, intensifying cross-substrate rivalry.

Australia Folding Carton Market Report Scope

The folding carton market in Australia refers to the industry that produces, distributes, and uses folding cartons, paper-based packaging solutions widely used across industries such as food and beverage, personal care, healthcare, and others. The study analyzes market trends, growth drivers, challenges, and opportunities in the Australian folding carton market. It also examines the competitive landscape, supply chain dynamics, and key developments influencing the market during the forecast period.

The Australia Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Australia folding carton market size and projected growth?

The market stands at USD 0.78 billion in 2025, is expected to reach USD 1.04 billion by 2031, advancing at a 4.61% CAGR.

Which material type leads sales in Australian folding cartons?

Solid Bleached Sulfate currently delivers 38.53% of revenue, making it the dominant substrate for premium applications.

How fast is digital printing growing in Australian carton converting?

Digital printing is forecast to expand at a 6.78% CAGR through 2031 as converters target short-run, versioned work.

Which end-user segment shows the fastest demand growth?

E-commerce and retail-ready packaging are projected to grow at a 6.45% CAGR, driven by the expansion of direct-to-consumer logistics.

What are the major cost pressures facing converters?

Import price volatility for virgin cartonboard and rising wage rates under the Manufacturing Award are compressing margins and accelerating automation.

Who are the key players holding the largest shares?

Visy, Opal, Abbe Group, Smurfit WestRock and IVE Group collectively control just over 80% of sector revenue, indicating moderate concentration.

Page last updated on: