All-in-One (AIO) Personal Computer (PC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

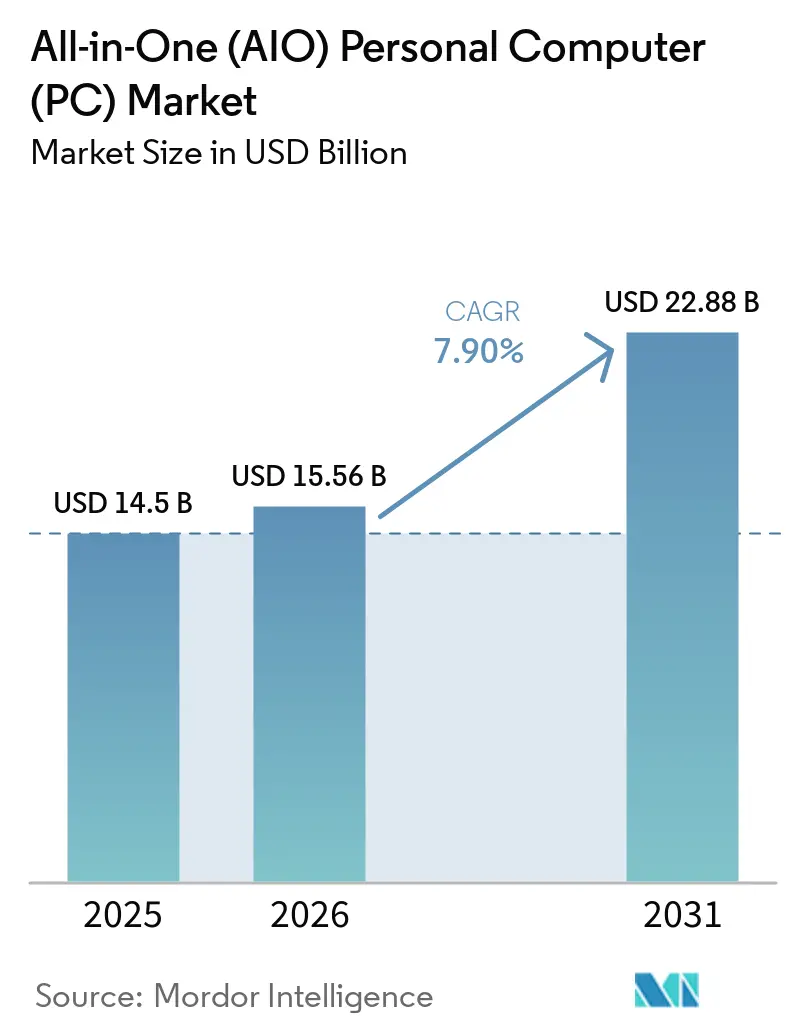

| Market Size (2026) | USD 15.56 Billion |

| Market Size (2031) | USD 22.88 Billion |

| Growth Rate (2026 - 2031) | 7.90% CAGR |

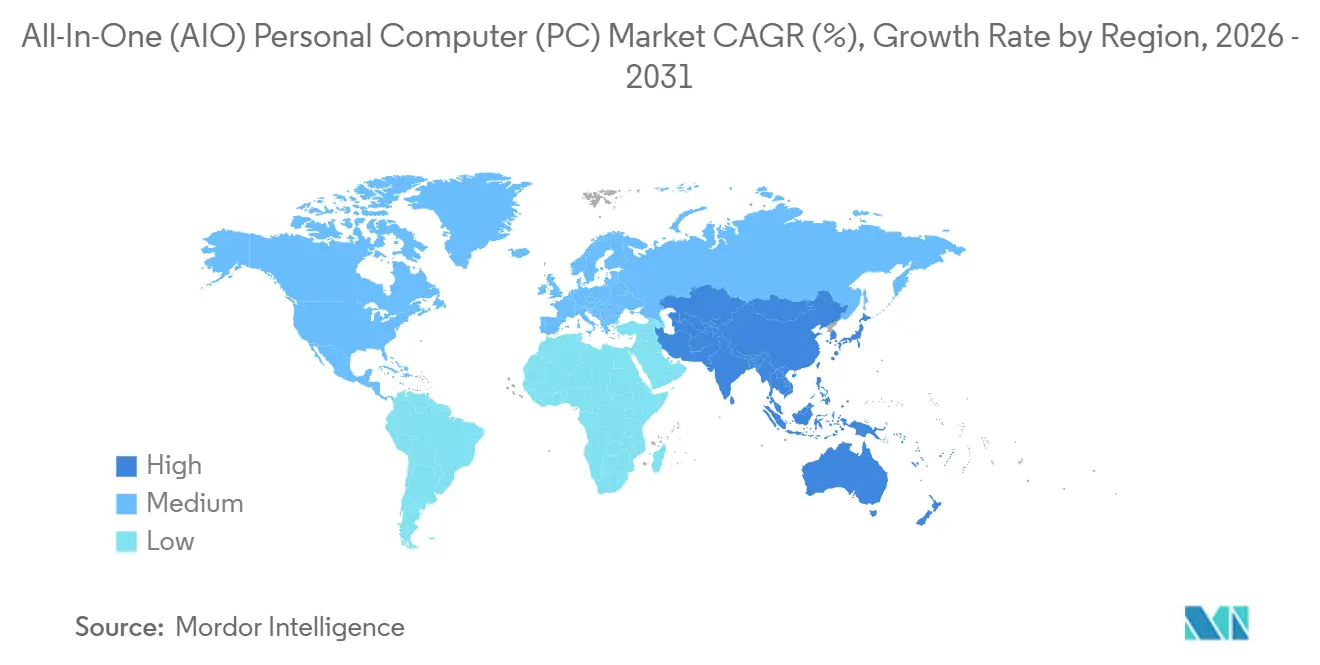

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

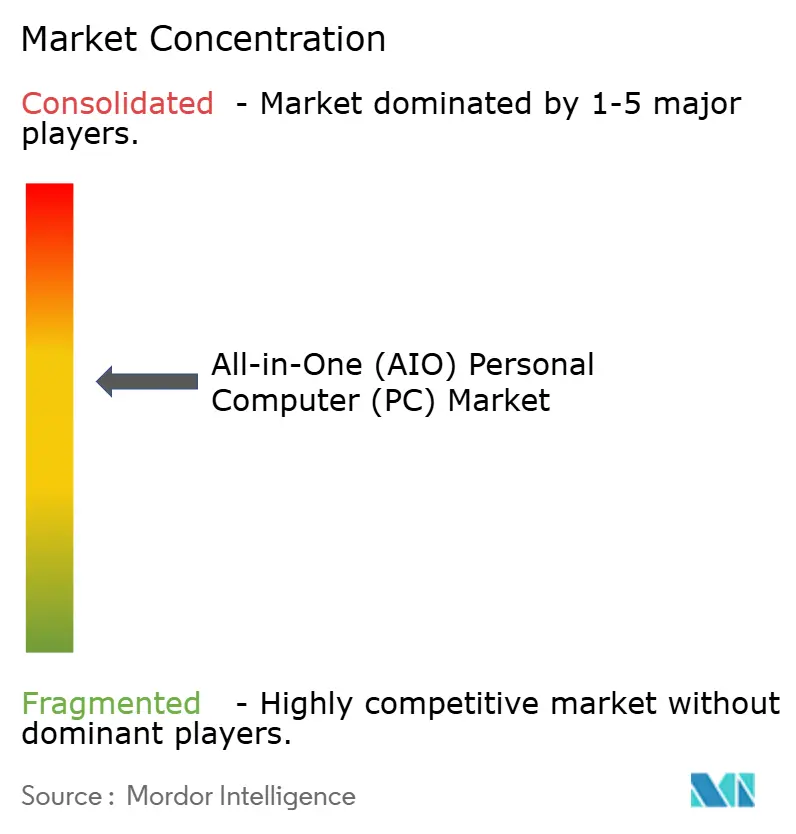

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

All-in-One (AIO) Personal Computer (PC) Market Analysis by Mordor Intelligence

The all-in-one pc market size is expected to grow from USD 14.5 billion in 2025 to USD 15.65 billion in 2026 and is forecast to reach USD 22.88 billion by 2031 at 7.9% CAGR over 2026-2031. Surging hybrid-work adoption is reshaping workspace layouts toward compact, cable-free systems, while component cost inflation is nudging original equipment manufacturers to justify higher prices through on-board neural processing rather than modular upgradeability. ENERGY STAR 9.0 regulations that took effect in October 2025 are accelerating refresh cycles because many 2023 units fail new idle-power thresholds. Supply-chain tariffs imposed in 2025 extended DRAM lead times beyond 40 weeks, pushing buyers toward integrated designs with guaranteed component availability. As gaming-grade displays and digital learning initiatives multiply, the all-in-one pc market continues to migrate from North America toward faster-growing Asia-Pacific demand centers.

Key Report Takeaways

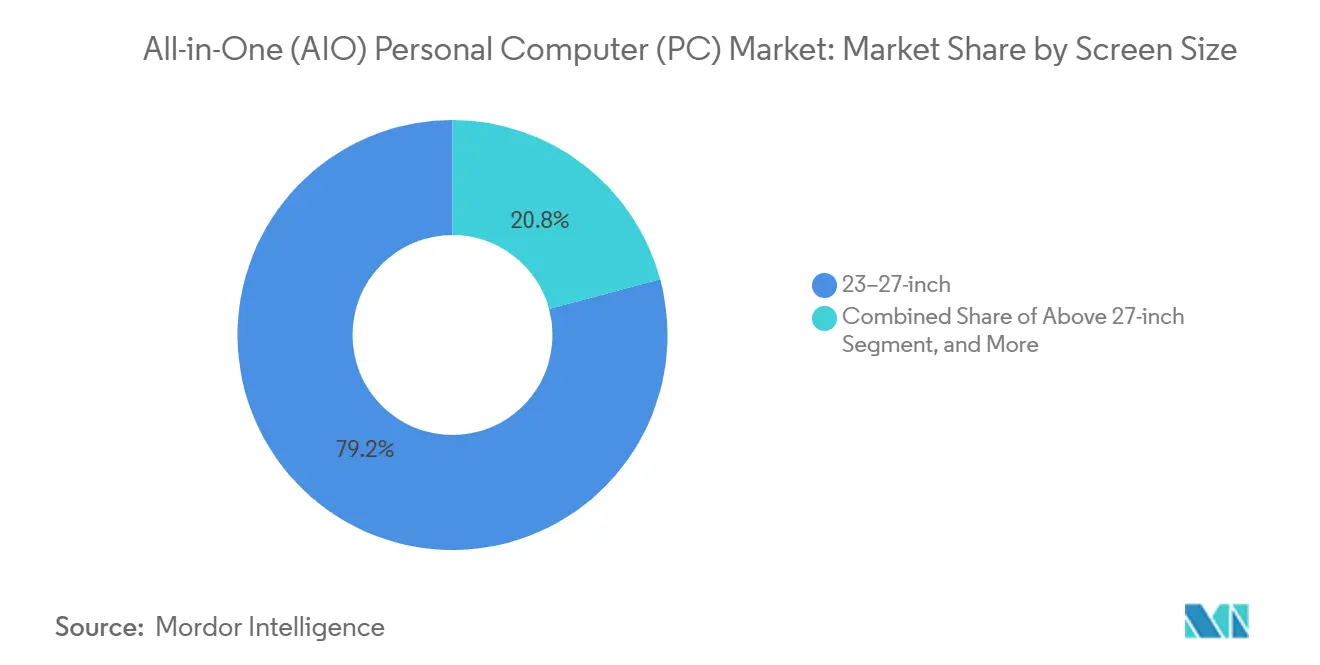

- By screen size, the 23-to-27-inch category led with 42.2% all-in-one PC market share in 2025, while the above-27-inch group is projected to advance at an 11.1% CAGR through 2031.

- By end user, commercial buyers accounted for 37.9% of the all-in-one PC market in 2025; educational institutions are set to expand at a 10.6% CAGR to 2031.

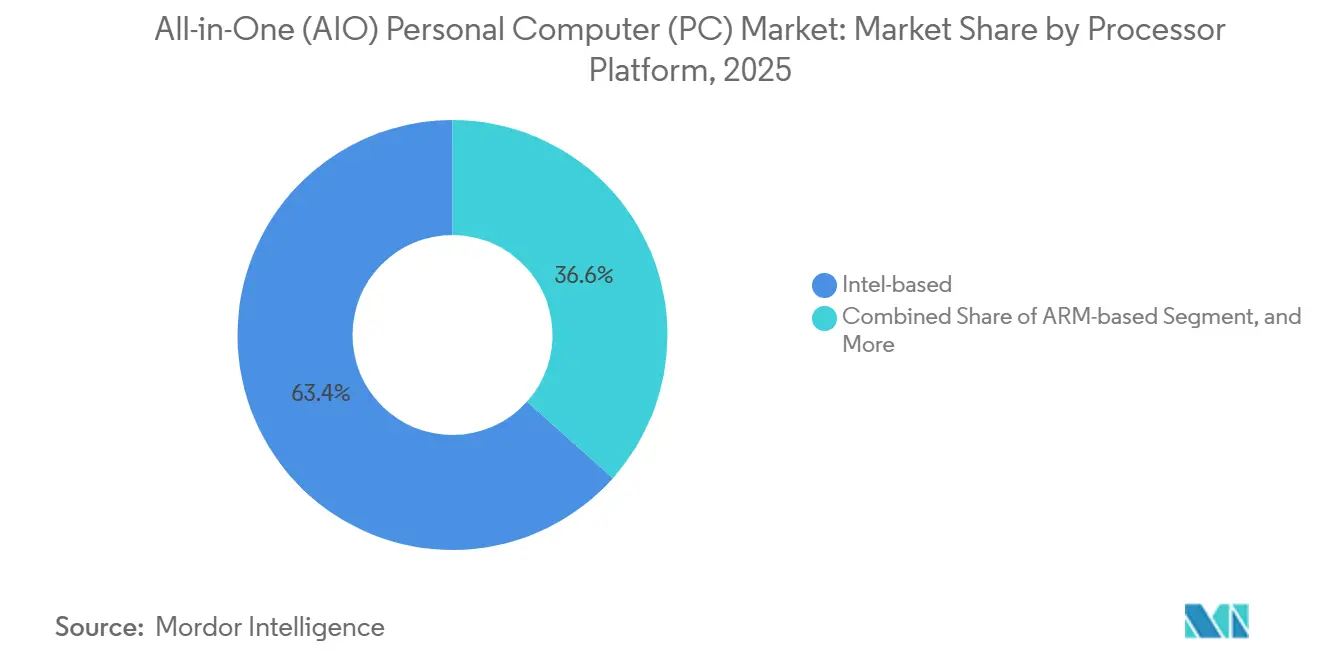

- By processor platform, Intel-based models retained 63.4% share of the all-in-one PC market in 2025, whereas ARM-based systems are forecast to grow at a 12.3% CAGR.

- By distribution channel, offline retail captured 51.8% of the all-in-one PC market in 2025 sales, but online retail is on track for an 11.7% CAGR through 2031.

- By geography, North America held a 32.7% revenue share of the all-in-one PC market in 2025, yet Asia-Pacific is poised to post a 9.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global All-in-One (AIO) Personal Computer (PC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Compact Workstations in Hybrid Work Models | +2.1% | Global, North America and Europe focus | Medium term (2-4 years) |

| Growing Digital Learning Infrastructure Investments | +1.8% | Asia-Pacific core, Middle East and Africa spill-over | Long term (≥4 years) |

| Technological Advances in Display and Thermal Design | +1.5% | Global, early uptake in North America and Asia-Pacific | Short term (≤2 years) |

| Energy-Efficient Regulations Fueling Device Replacement | +1.3% | North America and Europe, expanding into Asia-Pacific | Medium term (2-4 years) |

| OEM Shift Toward AI-Enabled AIO PCs | +1.0% | Global, led by North America and China | Short term (≤2 years) |

| Growth of 27-Inch and Larger Gaming-Grade AIOs | +0.9% | Asia-Pacific, especially China, South Korea, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Compact Workstations in Hybrid Work Models

Permanent hybrid-work policies are anchoring demand for space-efficient desktops that blend residential aesthetics with enterprise security. HP’s EliteBoard G1a integrates an entire Windows 11 Pro client into a wireless keyboard, letting staff turn any HDMI display into a workstation.[1]HP Inc., “HP Unveils New AI PCs and Displays at CES 2026,” hp.comMicrosoft reports 29% faster task completion when teams adopt devices that embed neural processing units for on-device AI. Silent cooling now ranks alongside compute power, leading Lenovo to pair a 32-inch OLED with dual asymmetric fans that hold noise below 30 dB.[2]Lenovo Group, “Lenovo Unveils AI-Powered PCs at CES 2025,” lenovo.comThe commercial slice of the all-in-one pc market stood at 37.9% in 2025, and education buyers are translating the same clutter-free logic into classrooms as touchscreen stations replace shared desktop rows.

Growing Digital Learning Infrastructure Investments

School systems are budgeting for one-to-one computers that support synchronous and asynchronous instruction. China’s provincial bureaus lifted desktop shipments 35% year-over-year in 4Q 2025 to ready labs for AI-driven curricula. South Korea earmarked incremental funds for endpoints with on-board NPUs that keep student data on site, conforming with sovereignty rules. The education segment’s 10.6% growth forecast reflects demand for stylus-enabled screens between 23 and 27 inches that let pupils watch a video lesson on one side while annotating on the other. These deployments underpin the 9.8% regional CAGR projected for Asia-Pacific.

Technological Advances in Display and Thermal Design

Mini-LED and OLED are now key differentiators as CPU gains plateau. HP’s OmniStudio X 27 introduced NEO:LED backlighting with 1,000 dimming zones and 1,000 nits peak luminance. Lenovo’s Yoga AIO i counters with 4K OLED at 165 Hz, supporting color-critical edits and motion graphics. Vapor-chamber cooling borrowed from gaming laptops allows a slim chassis to sustain turbo clocks without breaking 30 dB, addressing legacy throttling concerns. These boosts make larger panels viable for single-screen workflows, driving the above-27-inch slice of the all-in-one pc market at 11.1% CAGR.

Energy-Efficient Regulations Fueling Device Replacement

ENERGY STAR 9.0, effective October 2025, tightened idle-power ceilings and immediately disqualified many 2023 models from public tenders.[3]ENERGY STAR, “Computer Specification Version 9.0,” energystar.gov The European Union is preparing Ecodesign amendments that will force every desktop to carry energy labels by late 2026. China expanded its Energy Conservation Product Certification in 2025 to cover displays above 24 inches. Vendors are converging on low-power ARM and hybrid x86 silicon to stay under the new bars. Apple’s M4 iMac idles below 10 W, giving procurement teams an easy compliance win.[4]Apple Inc., “Apple Introduces M4 Pro and M4 Max,” apple.com Regulatory pull thus feeds a rolling replacement wave inside the all-in-one pc market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Average Selling Price Versus Modular Desktops | -2.90% | Global | Medium term (2–4 years) |

| Limited Hardware Upgradeability | -2.20% | Global | Long term (≥ 4 years) |

| Intensifying Competition from High-End Laptops | -2.50% | Global | Short term (≤ 2 years) |

| Component Supply-Chain Volatility Post-2025 Tariffs | -1.60% | North America, Asia-Pacific, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Higher Average Selling Price Versus Modular Desktops

All-in-one PCs usually carry a higher upfront price because the display, computing components, and compact design are integrated into a single unit. This makes them less cost-competitive than modular desktops, which can often be assembled or upgraded at lower initial expense. Price-sensitive buyers, especially in education, small offices, and budget-conscious households, may therefore choose traditional desktops instead. The premium pricing can also limit adoption in markets where value for money is a primary purchase factor. In addition, consumers may compare AIOs with desktop towers that offer stronger specifications at similar or lower prices. As a result, higher selling prices can restrict mass-market penetration.

Limited Hardware Upgradeability

All-in-one PCs have restricted upgrade options because most core components are tightly integrated into the slim chassis. Unlike desktops, users often cannot easily replace the processor, graphics card, or motherboard without major disassembly or service support. This reduces the product’s long-term flexibility and makes it less attractive to power users who want to extend system life through incremental upgrades. Businesses may also hesitate to invest in AIOs if they expect changing workload requirements over time. The limited upgrade path can increase replacement frequency, but it also raises concerns about total ownership cost. Overall, weaker upgradeability remains a key restraint on wider AIO adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Screen Size: Premium Panels Drive Above-27-Inch Surge

Revenue leadership rested with 23-to-27-inch models at 42.2% in 2025, reflecting their ergonomic fit for standard desks and the broad availability of panel supply. These models cater to a wide range of users, from professionals to casual users, due to their balance of size and functionality. Meanwhile, the above-27-inch tier is advancing at an 11.1% growth rate and is expected to capture a larger share of the all-in-one PC market, particularly for creative and financial workloads that demand enhanced screen real estate. HP’s NEO: LED debut and Lenovo’s 32-inch 4K OLED offerings highlight the growing consumer willingness to invest in single-monitor setups that boost productivity. Larger screens are also becoming a staple in Asia-Pacific gaming cafés, where they help reduce clutter from dual-monitor rigs and enhance the gaming experience. Despite the growing demand for larger screens, entry-level models under 23 inches continue to compete primarily on price, targeting education and call-center refreshes.

As display manufacturers scale mini-LED yields, the cost base for 23-to-27-inch products is expected to decline, making these models more accessible to a broader audience. However, above-27-inch panels remain a niche segment, sustaining high margins due to their premium positioning and specialized use cases. These larger panels are particularly appealing to professionals in creative industries and gamers seeking immersive experiences. Vendors are leveraging advancements in display technology to differentiate their offerings, with features like higher resolutions and improved color accuracy. The market dynamics indicate that while the mid-sized segment will continue to dominate in terms of volume, the premium tier will drive significant revenue growth. This dual-market approach allows vendors to cater to both cost-conscious buyers and those willing to pay a premium for advanced features.

By End User: Educational Institutions Accelerate Touchscreen Adoption

In 2025, commercial deployments accounted for 37.9% of total shipments, highlighting their significant contribution to the all-in-one PC market. However, educational institutions are expected to experience a robust annual growth rate of 10.6% through 2031, driven by increasing adoption of touch-enabled devices. This growth is anticipated to expand the market share of such devices within the education sector. China's notable desktop surge in Q4 2025 reflects the growing demand for these systems, while South Korea's focus on AI literacy emphasizes the importance of equipping students with advanced technology. These developments illustrate a broader shift towards one-device-per-student strategies, which are becoming a key trend in the education market.

Residential demand is evolving in response to hybrid work trends, with households increasingly choosing mid-priced all-in-one PCs. These devices are valued for their versatility, serving as both study hubs for students and media centers for families. This dual functionality has made them a popular choice among consumers seeking cost-effective solutions for home use. In the industrial sector, adoption remains niche but is steadily growing as fanless, rugged all-in-one PCs replace traditional panel PCs on factory floors. These devices offer enhanced durability and performance, making them suitable for demanding industrial environments. Additionally, schools are addressing budgetary risks associated with soldered components by adopting warranty programs that include accidental-damage coverage, ensuring long-term cost efficiency.

By Processor Platform: ARM Architecture Gains Enterprise Foothold

In 2025, Intel maintained a dominant 63.4% share of the market. However, ARM platforms are experiencing significant momentum, driven by an annual growth rate of 12.3%. This growth is supported by Apple's M4 iMac, which claims to deliver 4.5 times the performance of its previous generation while consuming less idle power. The shift towards ARM platforms is also enhancing compliance with energy-label standards and aligning with government procurement incentives, which prioritize energy-efficient technologies. On the other hand, AMD continues to attract price-performance-conscious buyers. Despite this, its progress is somewhat hindered by a limited range of models, which restricts its ability to compete more aggressively in the market.

Cloud-optimized Windows 365 partnerships with ASUS and Dell, scheduled for late 2026, emphasize the growing importance of thin-client solutions. These partnerships reflect the increasing demand for devices that rely on cloud computing while still requiring local NPUs to handle video conferencing efficiently. As ARM silicon achieves performance parity with office benchmarks, x86 incumbents are accelerating efforts to integrate inference engines capable of delivering over 40 TOPS. This development underscores the shift in focus within the all-in-one PC market, where comparative AI performance is becoming a critical factor in purchasing decisions. Buyers are now prioritizing AI capabilities over traditional CPU performance metrics, signaling a significant change in market dynamics.

By Distribution Channel: Direct-to-Consumer Models Reshape Retail

Offline stores retained 51.8% of the market share in 2025, primarily driven by enterprise solution sales. However, online revenue is growing at a compound annual growth rate (CAGR) of 11.7%, as vendors increasingly adopt built-to-order checkout flows to minimize inventory risks. The global desktop e-commerce market reached USD 28.9 billion in 2025, highlighting the shift toward online channels. This growth is supported by the convenience and customization options offered by online platforms. Despite the dominance of offline channels, the rapid expansion of e-commerce is reshaping the distribution landscape. Vendors are leveraging digital platforms to cater to evolving consumer preferences and streamline operations.

White-glove last-mile services are now addressing a key barrier to online purchases by installing large all-in-one PCs directly in customers' living rooms. This service eliminates logistical challenges that previously deterred buyers from opting for online channels. Retail showrooms are transforming into experience hubs, where customers can explore premium units before being directed to web stores for final configuration and purchase. However, price differences of 10-15% between web-only SKUs and store-stocked models could create profitability challenges for brick-and-mortar stores. As the forecast period progresses, traditional retail outlets may face increasing pressure to adapt to the growing dominance of online sales. This trend underscores the need for retailers to innovate and integrate omnichannel strategies to remain competitive.

Geography Analysis

North America commanded 32.7% of the 2025 market value, driven by early adoption of hybrid-work policies that encouraged corporate upgrades. The region also leads in ENERGY STAR adoption, which has fueled compliant refreshes to maintain the installed base of the all-in-one PC market. Additionally, gaming-oriented SKUs with discrete graphics continue to enjoy strong margins, as U.S. consumers show a preference for premium builds. The demand for energy-efficient and high-performance systems further supports the region's dominance. North America’s established infrastructure and consumer spending power make it a key market for all-in-one PCs.

Asia-Pacific demonstrates the highest growth potential, with a projected CAGR of 9.8% through 2031. The region benefits from diverse catalysts, including China’s large-scale education tenders and South Korea’s launches of 165 Hz gaming systems. Lenovo’s USD 2 billion joint venture in Saudi Arabia, set to begin in 2026, will redirect part of Asia’s production to the Middle East, reducing lead times and mitigating tariff impacts. The region’s growing middle class and increasing digital adoption further contribute to its rapid expansion. Asia-Pacific remains a critical market for manufacturers aiming to capitalize on its dynamic growth.

Europe’s stricter energy regulations are moderating overall market volume but are simultaneously driving up average selling prices. Buyers in the region are increasingly opting for low-power premium designs, aligning with sustainability goals. South America and Africa, while remaining price-sensitive markets, are witnessing emerging opportunities through NGO-funded school deployments in countries like Brazil and South Africa. These initiatives are helping to expand market penetration in underserved regions. Meanwhile, the Middle East is evolving into a manufacturing hub, with localized assembly enabling cost efficiencies and re-exports to Gulf markets. This shift is reshaping the cost dynamics of the all-in-one PC market.

Competitive Landscape

In 2025, the all-in-one PC market showcased a moderate fragmentation. Leading players, including Apple, HP, Lenovo, Dell, and ASUS, held a significant share of the revenue, curbing any single vendor's pricing power. Apple’s vertical integration strategy enables it to capture margins from both silicon and software, but this approach restricts its ability to address cross-platform compatibility. HP and Dell, in contrast, focus on building long-term customer loyalty by offering device-as-a-service bundles, which include lifecycle support and maintenance services. These strategies have allowed the top players to maintain a stronghold in the market, despite the presence of smaller competitors. The competitive dynamics in this market are shaped by the balance between innovation, pricing strategies, and customer retention efforts.

Key technological advancements in the all-in-one PC market are centered around NPUs, mini-LED backlights, and vapor-chamber cooling systems. These innovations aim to enhance performance, energy efficiency, and user experience. Recent patent filings for detachable displays and liquid-metal heat spreaders suggest that manufacturers are striving to combine sleek aesthetics with the flexibility of upgradeable components. Smaller players, such as CyberPowerPC and iBUYPOWER, are carving out a niche in the gaming segment by offering factory-overclocked systems directly to consumers. This direct-to-consumer approach allows them to compete effectively with larger brands by targeting specific customer needs. The focus on technology and niche markets highlights the diverse strategies employed by companies to gain a competitive edge.

Manufacturing diversification is becoming increasingly important in the all-in-one PC market. Lenovo plans to open a new facility in Saudi Arabia in the near future, aiming to reduce its exposure to tariffs and geopolitical risks. At the same time, industry reports suggest that HP is conducting feasibility studies for potential manufacturing operations in Mexico, which could further diversify its supply chain. Samsung and LG are leveraging their expertise in display technology to develop all-in-one PCs with 5K resolution and webOS, blurring the lines between monitors and PCs. These innovations are intensifying competition and driving the need for continuous advancements in the market. The push for regional manufacturing and technological innovation reflects the evolving strategies of companies to address global challenges and meet consumer demands.

All-in-One (AIO) Personal Computer (PC) Industry Leaders

Apple Inc.

HP Inc.

Lenovo Group Limited

Dell Technologies Inc.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: HP rolled out the HyperX gaming line in South Korea, aiming at a market where gaming PCs account for 30% of consumer sales and are projected to reach 40% by 2028.

- January 2026: HP revealed the OmniStudio X 27 at CES 2026, featuring NEO:LED backlighting with 1,000 dimming zones and a 1,000,000:1 contrast ratio.

- January 2026: Lenovo launched the Yoga AIO i at CES 2026, coupling a 32-inch 4K OLED at 165 Hz with vapor-chamber cooling.

- January 2026: HP introduced the EliteBoard G1a, embedding a full Windows 11 Pro client inside a wireless keyboard.

Global All-in-One (AIO) Personal Computer (PC) Market Report Scope

The All-in-One (AIO) Personal Computer (PC) Market refers to desktop computing systems that integrate the core hardware components, such as the processor, memory, storage, and graphics, directly into the display unit, eliminating the need for a separate tower. These systems are designed for space efficiency, simplified setup, and aesthetic appeal while delivering standard desktop functionality. AIO PCs are widely used in homes, offices, education, retail, and front-desk environments where compact design and ease of use are prioritized. The market includes consumer and commercial AIO systems across various performance and display configurations.

The All-in-One PC Report is Segmented by Screen Size (Up to 23-inch, 23–27-inch, Above 27-inch), End User (Residential, Commercial, Educational, Industrial), Processor Platform (Intel-based, AMD-based, ARM-based), Distribution Channel (Online Retail, Offline Retail), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Up to 23-inch |

| 23-27-inch |

| Above 27-inch |

| Residential |

| Commercial |

| Educational |

| Industrial |

| Intel-based |

| AMD-based |

| ARM-based (Apple Silicon and Others) |

| Online Retail |

| Offline Retail |

| North America | United States |

| Canada | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Screen Size | Up to 23-inch | |

| 23-27-inch | ||

| Above 27-inch | ||

| By End User | Residential | |

| Commercial | ||

| Educational | ||

| Industrial | ||

| By Processor Platform | Intel-based | |

| AMD-based | ||

| ARM-based (Apple Silicon and Others) | ||

| By Distribution Channel | Online Retail | |

| Offline Retail | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the all-in-one pc market in 2026?

The all-in-one pc market size is valued at USD 15.65 billion in 2026.

What is the projected CAGR for all-in-one desktops between 2026 and 2031?

The market is forecast to expand at a 7.9% CAGR during 2026-2031.

Which screen size bracket is growing fastest?

Panels above 27 inches are advancing at an 11.1% CAGR through 2031.

Why are ARM-based all-in-ones gaining traction?

ARM systems like Apple's M4 iMac meet tighter energy rules and deliver strong AI performance, fueling a 12.3% annual growth outlook.

Which region will add the most incremental revenue?

Asia-Pacific is projected to grow at 9.8% CAGR as gaming and education demand accelerate.

How are ENERGY STAR 9.0 rules influencing refresh cycles?

The 2025 standards disqualify many 2023 models from public procurement, pushing enterprises to adopt newer, low-idle-power units sooner.

Page last updated on: