Notebook Computer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

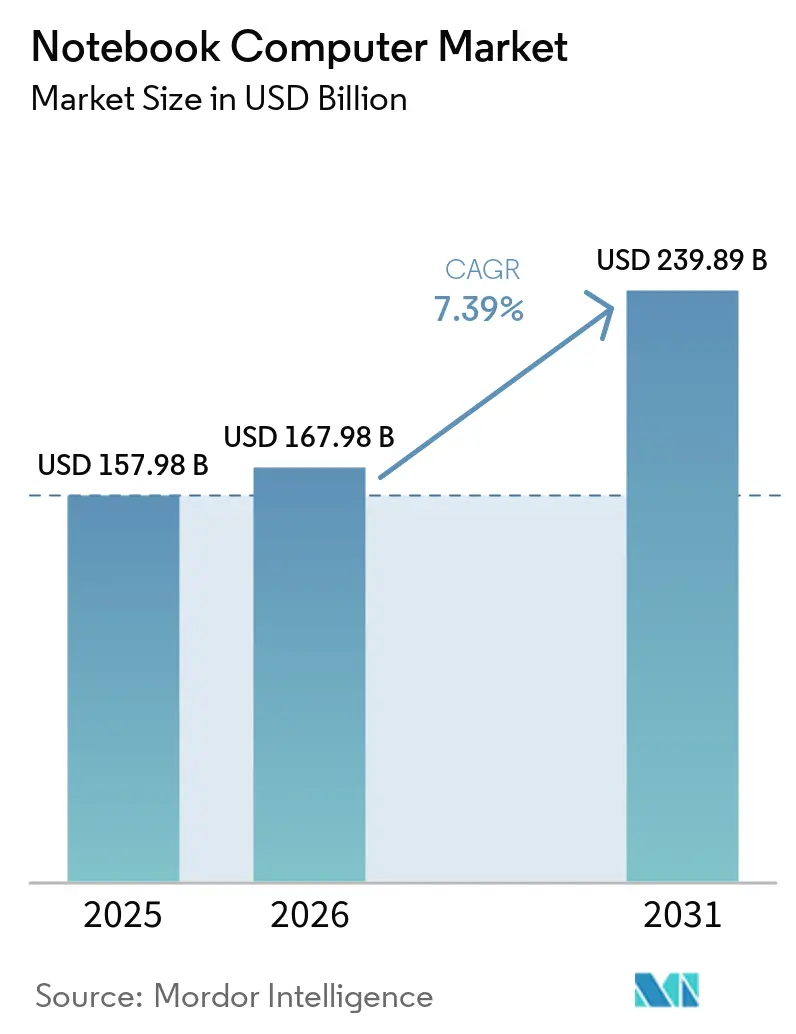

| Market Size (2026) | USD 167.98 Billion |

| Market Size (2031) | USD 239.89 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

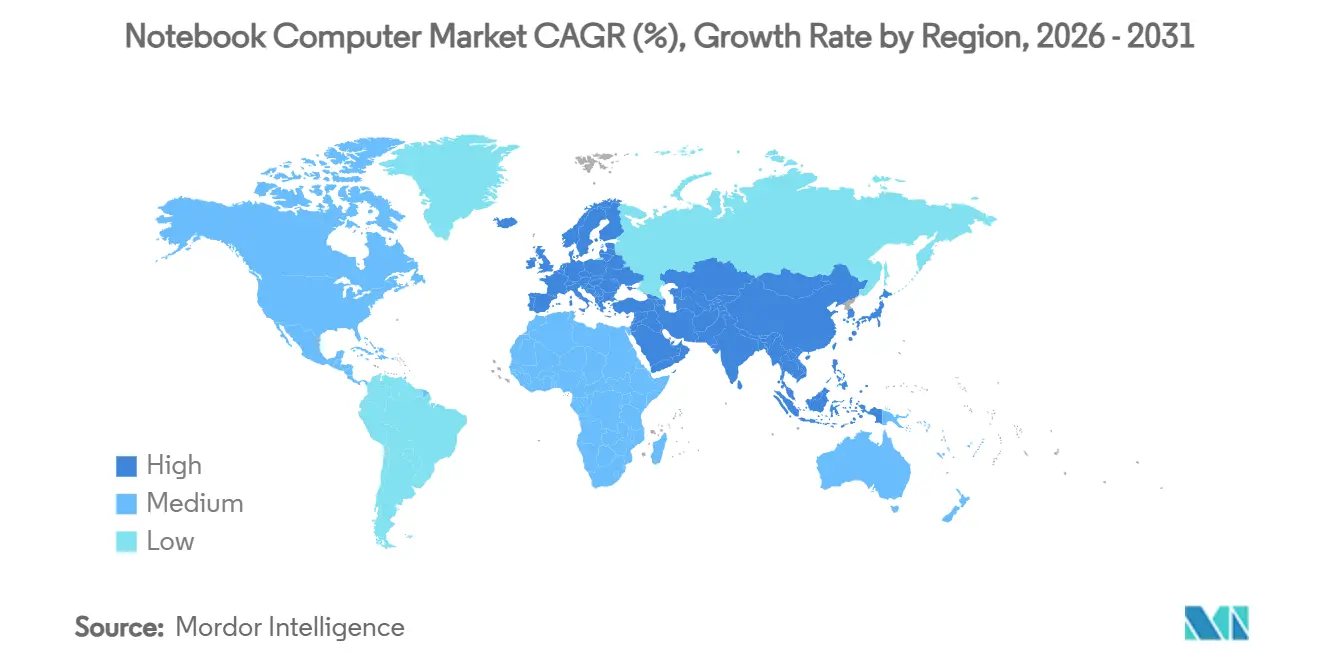

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

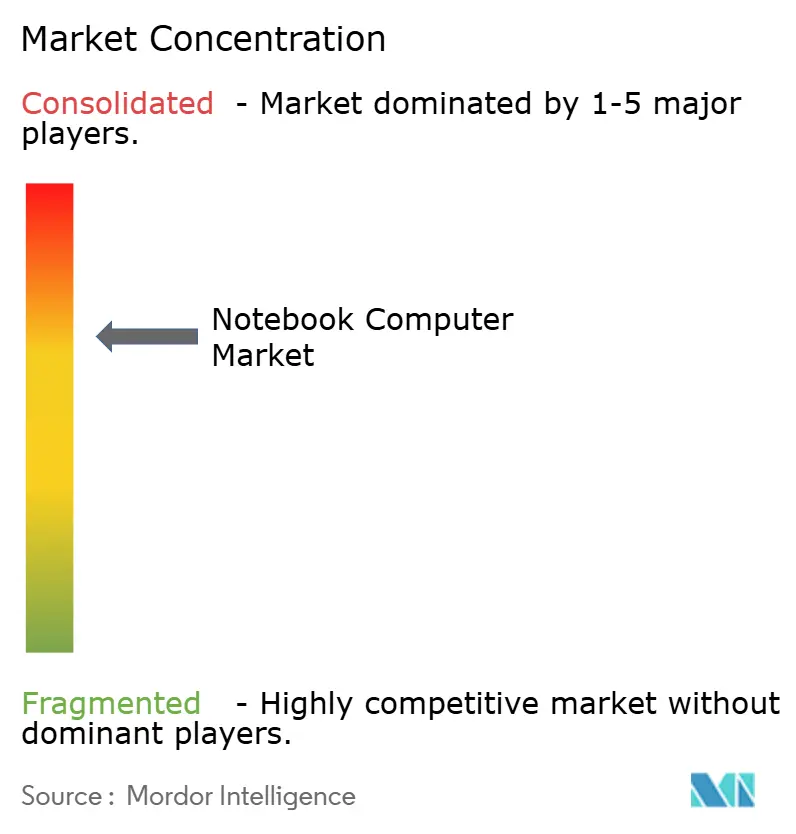

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Notebook Computer Market Analysis by Mordor Intelligence

The Notebook computer market size is projected to expand from USD 157.98 billion in 2025 and USD 167.98 billion in 2026 to USD 239.89 billion by 2031, registering a CAGR of 7.39% between 2026 and 2031. Commercial buyers are replacing fleets in advance of the October 2025 Windows 10 end-of-support deadline, while AI-centric processors have created a high-margin premium tier that brings inference workloads on device. Component shortages have lifted memory’s share of the bill of materials beyond 20% and accelerated supply-chain shifts toward India, Vietnam, and Mexico. At the same time, hybrid work models fuel demand for always-connected designs, and esports growth expands the addressable base for mid-priced gaming systems. Sustainability regulation in the European Union is also shaping designs toward greater repairability and energy efficiency.

Key Report Takeaways

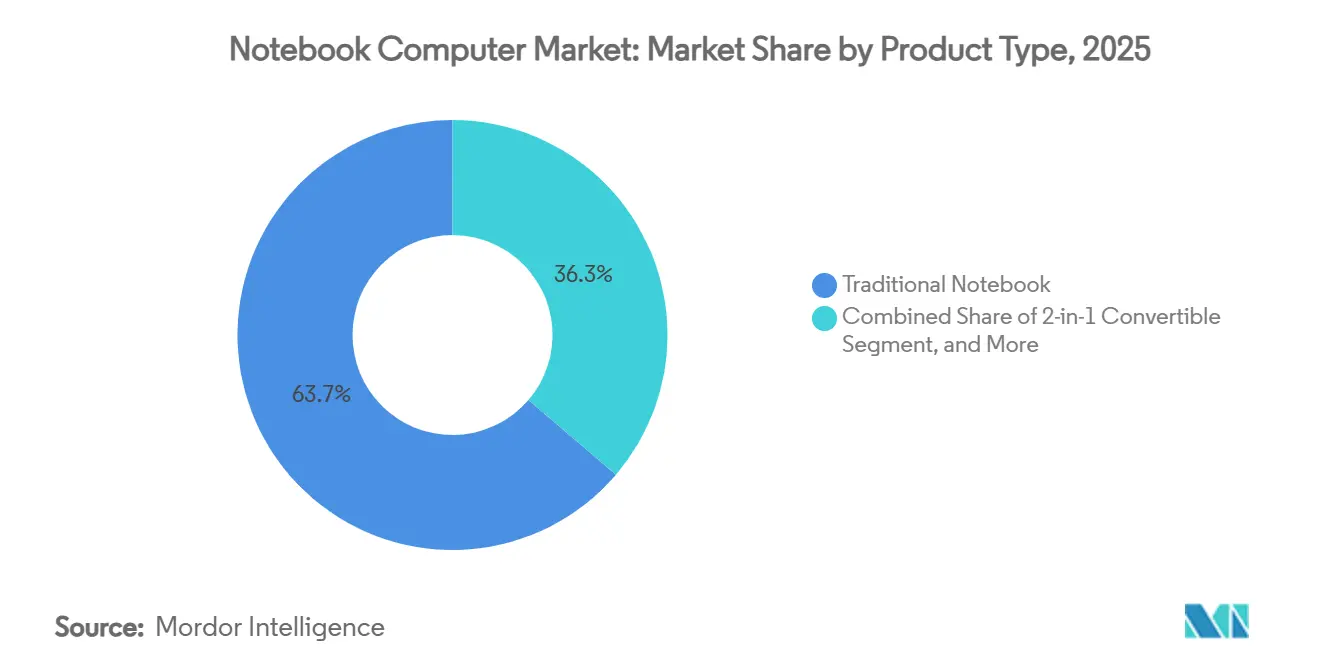

- By product type, traditional notebooks held 63.74% of the Notebook computer market share in 2025, while 2-in-1 convertibles are projected to record an 8.19% CAGR through 2031.

- By operating system, Windows commanded 69.21% share of the Notebook computer market size in 2025, whereas Chrome OS is forecast to expand at an 8.21% CAGR to 2031.

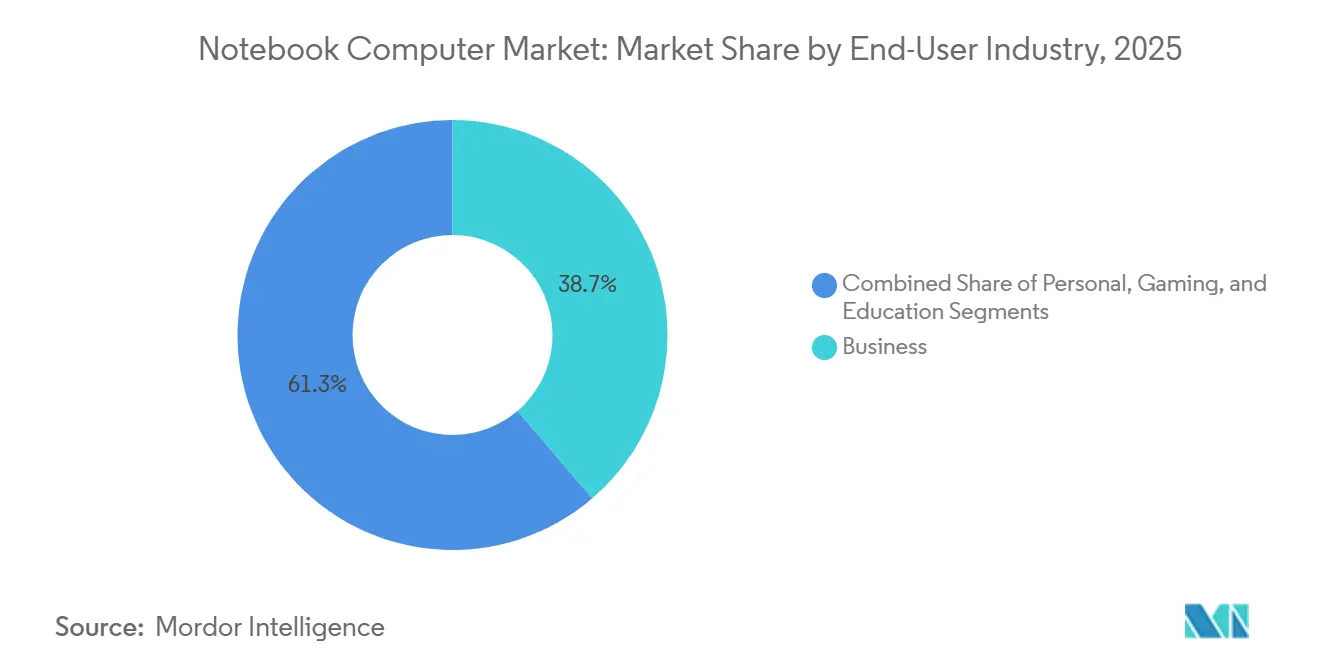

- By end user, the business segment accounted for 38.73% of shipments in 2025, while gaming is expected to register a 7.27% CAGR over 2026-2031.

- By screen size, the 15-16.9 inch category captured 31.49% share of the Notebook computer market size in 2025, whereas 17 inches and above is set to grow at an 8.37% CAGR through 2031.

- By geography, Asia-Pacific led with 46.39% revenue share in 2025 and Europe is projected to deliver the fastest 8.12% regional CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Notebook Computer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Windows 10 End-Of-Support Triggering Commercial Refresh Cycle | +2.1% | Global, concentration in North America and Europe | Short term (≤ 2 years) |

| AI-Centric Processors Enabling New Premium Use Cases | +1.8% | North America, Europe, Asia-Pacific (China, Japan, South Korea) | Medium term (2-4 years) |

| Remote And Hybrid Work Cultivating Always-Connected Notebooks | +1.3% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Rising Gaming And Esports Notebook Demand In Emerging Markets | +0.9% | Asia-Pacific (India, Southeast Asia), South America (Brazil) | Long term (≥ 4 years) |

| Government Education Procurement Programs | +0.7% | Asia-Pacific (India, Indonesia), Africa, South America | Medium term (2-4 years) |

| Supply-Chain Diversification Incentives In India, Vietnam, And Mexico | +0.5% | Asia-Pacific (India, Vietnam), North America (Mexico) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Windows 10 End-of-Support Triggering Commercial Refresh Cycle

Microsoft will cease security updates for Windows 10 on 14 October 2025, creating significant compliance risks for enterprises operating under stringent regulations such as GDPR and HIPAA. Without these updates, organizations may face vulnerabilities that could lead to data breaches or non-compliance penalties. According to Dell research, 62% of IT departments in Fortune 500 companies plan to replace their existing devices rather than opt for extended paid support services. This trend indicates a major refresh cycle, with the peak expected to occur in 2026. Vendors with robust commercial distribution channels are likely to benefit the most from this surge in demand. However, it is important to note that this refresh wave is anticipated to provide a temporary boost in shipments rather than establishing a sustained long-term growth trajectory for the market.

AI-Centric Processors Enabling New Premium Use Cases

Intel Core Ultra, AMD Ryzen AI 300 series, and Qualcomm Snapdragon X Elite each feature neural engines capable of exceeding 40 TOPS, aligning with Microsoft’s Copilot+ PC baseline requirements. These processors are designed to handle advanced AI workloads efficiently, enabling seamless performance across a wide range of applications. Devices such as HP’s OmniBook Ultra Flip and Lenovo’s Yoga Slim 7x showcase how on-device inference technology enables real-time transcription, background blur, and chatbot functionality without relying on cloud-based processing, thereby eliminating latency. This advanced capability not only enhances user experience but also justifies a 20-30% price premium for these devices. Additionally, it significantly reduces lifetime cloud expenditure for enterprises managing large device fleets, making these systems a cost-effective solution for businesses.

Remote and Hybrid Work Cultivating Always-Connected Notebooks

Integrated 5G or LTE modems are now standard on flagship models such as the Microsoft Surface Laptop 7th Edition, which features a Snapdragon X Elite processor and Verizon 5G support.[1]Microsoft Corporation, “Surface Laptop 7th Edition,” MICROSOFT.COM These modems deliver sub-30 ms latency, enabling users to conduct video meetings and run SaaS workloads with performance comparable to wired broadband connections. Additionally, eSIM provisioning enables IT teams to centrally manage data plans, streamlining operations and enhancing security for distributed workforces. This feature is particularly beneficial for organizations with remote or hybrid work models, as it ensures seamless connectivity and reduces the risk of data breaches associated with traditional SIM cards.

Rising Gaming and Esports Notebook Demand in Emerging Markets

ASUS ROG Strix and MSI Katana devices feature NVIDIA GeForce RTX 4060 GPUs and 144 Hz panels, priced between USD 800 and USD 1,500. These devices cater to the growing demand for affordable yet high-performance gaming laptops, particularly in price-sensitive markets such as India and Southeast Asia. The expansion of e-sports venues and the availability of installment financing options have further broadened access to these devices, enabling a wider audience to invest in gaming hardware. However, the segment continues to face challenges, including susceptibility to fluctuations in memory and GPU prices, which could impact overall affordability and market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Component Shortages Driving ASP Inflation And Purchase Deferrals | -1.4% | Global, acute in price-sensitive Asia-Pacific and South America | Short term (≤ 2 years) |

| Escalating Geopolitical Tariffs On Chinese-Made Notebooks | -1.1% | North America, spillover to Europe and Asia-Pacific | Medium term (2-4 years) |

| Substitution Threat From High-End Tablets With Keyboards | -0.6% | North America, Europe, Asia-Pacific (premium segments) | Medium term (2-4 years) |

| Energy-Efficiency Regulations Raising Compliance Costs | -0.3% | Europe, emerging influence in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Component Shortages Driving ASP Inflation and Purchase Deferrals

DRAM and NAND now account for over 20% of notebook costs, driven by the increasing demand for AI workloads, which have established 16 GB of RAM and 512 GB of storage as standard requirements. In late 2025, spot memory prices surged by 18% quarter over quarter, compelling manufacturers to either implement 5-15% average selling price (ASP) increases or absorb the cost, thereby impacting profit margins. Consumers in price-sensitive markets such as India, Indonesia, and Brazil have responded to these price hikes by delaying device replacements or opting for refurbished units. This trend is expected to limit shipment growth in 2026 until additional manufacturing capacity for memory components becomes operational.

Escalating Geopolitical Tariffs on Chinese-Made Notebooks

Section 301 List 4A imposes a 7.5% tariff on consumer electronics, while batteries and certain semiconductor chips are subject to additional levies that can reach up to 60% when Section 122 surcharges are included. In response to these trade barriers, companies like HP and Dell are actively relocating portions of their production to Vietnam and Mexico to mitigate the impact of these tariffs. Similarly, Lenovo is increasing its manufacturing capacity in India, leveraging a 5% production-linked incentive scheme offered by the Indian government.[2]Government of India, “Production Linked Incentive Scheme for IT Hardware,” INDIA.GOV.IN However, the relocation process involves lead times of 18 to 24 months, which means elevated landed costs are expected to continue affecting the market until at least 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Convertibles Advance Within Hybrid Workspaces

In 2025, traditional clamshells accounted for 63.74% of the Notebook computer market share, driven by consistent demand from the education sector and entry-level businesses that prioritize affordability and functionality. However, 2-in-1 convertibles are projected to grow at a robust 8.19% CAGR, gradually increasing their share of the Notebook computer market. This growth is fueled by employers adopting hot-desking solutions that emphasize flexibility and adaptability in workplace setups.

Gaming notebooks continue to hold a premium position in the market, supported by the integration of advanced discrete RTX 40-series GPUs and high-refresh-rate displays, which cater to the needs of gamers and content creators. Meanwhile, ultrabooks remain competitive by focusing on lightweight designs, typically weighing under 1.5 kg, appealing to professionals who prioritize portability. Manufacturers are increasingly merging product categories by incorporating features such as 360-degree hinges and stylus support into mainstream models, enhancing their versatility. Additionally, the growing adoption of USB-C docking solutions and wireless peripherals further accelerates this convergence, making devices more adaptable to various user requirements.

By Operating System: Chrome OS Gains in Education and SMB

Windows remained dominant, accounting for 69.21% of shipments in 2025, primarily due to its widespread legacy application support and compatibility with enterprise systems. This dominance is further reinforced by its widespread adoption across industries, including education, healthcare, and government, where reliance on traditional software ecosystems remains high. Chrome OS, however, is projected to achieve an 8.21% CAGR as governments in emerging markets such as India, Indonesia, and Brazil increasingly specify sub-USD 300 Chromebook Plus devices in tenders. This shift is gradually capturing a measurable portion of the Notebook computer market, driven by affordability and ease of deployment.

Google’s zero-touch enrollment feature significantly reduces IT overhead, making it an attractive option for institutions and enterprises looking to streamline device management. Additionally, ARM-based silicon now meets the performance requirements for video conferencing and other productivity applications, further boosting Chrome OS adoption. macOS continues to sustain a high-margin niche among creative professionals who prioritize features such as extended battery life, seamless ecosystem integration, and advanced software capabilities tailored for design and multimedia tasks. Meanwhile, Linux, although maintaining a market share of under 5%, is experiencing growth within developer communities. This growth is attributed to brands like System76 and distributions such as Pop!_OS, which are optimized for AI frameworks and cater to the specific needs of developers working on machine learning and artificial intelligence projects.[3]System76, “Lemur Pro with Pop!_OS Launch,” SYSTEM76.COM

By End-User Industry: Gaming Outpaces Consumer Replacement

Business users accounted for 38.73% of 2025 shipments, primarily driven by compliance-driven refresh cycles and the need to upgrade systems to meet evolving business requirements. However, the gaming segment is projected to grow at a robust 7.27% CAGR through 2031, steadily increasing its share of the overall Notebook computer market. The growing popularity of e-sports leagues and the rise of streaming culture have significantly boosted demand for high-performance devices equipped with 240 Hz screens and hardware ray tracing capabilities, which are essential for competitive gaming and immersive experiences.

In the education sector, buyers remain highly cost-conscious, often opting for ruggedized Chromebooks that can withstand the wear and tear of daily student use. This preference has also led to extended refresh intervals, as educational institutions aim to maximize the lifespan of their devices. Meanwhile, personal usage exhibits the slowest growth among all segments, as advancements in browsers, cloud-based productivity tools, and video streaming services have made older devices sufficient for longer periods, reducing the urgency for frequent upgrades.

By Screen Size: Larger Panels Serve Creation and Competition

Panels sized 15-16.9 inches accounted for 31.49% of the market share in 2025, reflecting their popularity among users seeking a balance between portability and screen size. However, 17-inch and larger models are projected to grow at a compound annual growth rate (CAGR) of 8.37% by 2031, driven by increasing demand for larger screens that enhance productivity and entertainment experiences. This growth is expected to significantly boost revenue in the Notebook computer market. Advanced display technologies, such as 4K OLED and Mini LED with full DCI-P3 color gamut coverage, are gaining traction among professionals like designers, photographers, and esports casters who require high-quality visuals for their work and activities.

Meanwhile, mobility-focused buyers continue to favor 13-14.9-inch ultralight laptops for their lightweight, compact design, which makes them ideal for on-the-go use. Additionally, sub-12-inch convertible laptops cater to a niche market, primarily serving field-service professionals who prioritize portability and versatility. This segmentation underscores two distinct value propositions in the market, one emphasizing portability and convenience, and the other emphasizing an immersive, expansive visual workspace for users.

Geography Analysis

Asia-Pacific generated 46.39% of 2025 revenues, firmly establishing itself as both a key supplier and a major consumer in the Notebook computer market. India’s 5% production-linked rebate has incentivized companies like HP and ASUS, along with their local partner, Dixon Technologies, to commit to an annual production capacity of 10 million units by 2027. This initiative aims to reduce USD 8 billion worth of notebook imports while simultaneously increasing domestic value addition. Meanwhile, China’s state sector continues to drive demand by refreshing its fleets with hardware stacks that comply with domestic cybersecurity directives, ensuring steady growth even as consumer replacement cycles slow down.

Europe is projected to be the fastest-growing region, with an anticipated CAGR of 8.12% between 2026 and 2031. The introduction of Regulation 2025-2052 will enforce stricter external power-supply limits starting in 2028, while Ecodesign rules will mandate higher repairability standards by 2027.[4]European Commission, “EU Regulation 2025/2052 and Ecodesign Working Plan 2025-2030,” EC.EUROPA.EU Vendors offering modular batteries and serviceable SSDs are expected to gain a competitive edge in procurement processes. Countries such as Germany, France, and the United Kingdom are leading the adoption of AI-capable notebook models, aligning with GDPR requirements that emphasize local data processing capabilities

North America remains the largest single-country cluster in the market. However, tariffs have increased retail prices, prompting manufacturers to shift assembly operations to Mexican plants that benefit from USMCA trade agreements. In South America, Brazil is emerging as a key player in the gaming segment, although currency fluctuations temper its growth. The Middle East and Africa are witnessing the selective adoption of high-end notebooks, particularly premium ultrabooks targeted at executive users. Gradual improvements in infrastructure and rising disposable incomes in the region support this trend.

Competitive Landscape

The top five suppliers accounted for approximately 70% of 2025 shipments, indicating a moderately concentrated Notebook computer market. This dominance highlights the competitive landscape where leading players continue to shape market trends. Microsoft’s Copilot+ PC specification, which mandates a 40 TOPS neural engine baseline, has effectively set the benchmark for the high-end tier. This requirement is driving vendors to integrate advanced silicon technologies such as Intel Core Ultra, AMD Ryzen AI, or Qualcomm Snapdragon X Elite processors to meet these standards. HP’s 2026 OmniBook and EliteBook families are leveraging features like real-time transcription and gaze correction to create differentiation in the enterprise segment, catering to the evolving needs of professional users.

Smaller, niche specialists are focusing on innovation in thermal management and offering greater configuration flexibility to carve out their market share. Companies like Razer and MSI are targeting the gaming segment by incorporating vapor-chamber cooling systems alongside RTX 40-series GPUs, ensuring optimal performance for high-end gaming. Meanwhile, System76 is addressing the developer community by prioritizing Linux-first builds and open firmware, appealing to a specific user base that values customization and open-source solutions. Additionally, nearshoring trends are providing Indian EMS firms, such as Dixon Technologies, with a significant competitive edge. These firms benefit from an 8-12% landed-cost advantage over Chinese imports, enabling them to offer cost-effective private-label manufacturing solutions for multinational brands seeking to optimize their supply chains.

Looking ahead, competition in the market is expected to shift towards advancements in battery chemistry, the use of recycled materials, and extended firmware support lifecycles. As sustainability becomes a critical factor in procurement decisions, companies that proactively invest in modular and repairable architectures are likely to gain a competitive advantage. These efforts not only align with growing environmental regulations but also position such companies to secure European tenders and reduce supply-chain carbon footprints, addressing both market demands and sustainability goals.

Notebook Computer Industry Leaders

Lenovo Group Limited

HP Inc.

Dell Technologies, Inc.

Apple Inc.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: HP Inc. unveiled the OmniBook Ultra Flip, OmniBook X Flip, and EliteBook X Flip, all featuring Intel Core Ultra processors and AI collaboration features aimed at hybrid workers.

- January 2026: Microsoft launched Surface Laptop 7th Edition with Snapdragon X Elite and integrated 5G, offering always-connected performance.

- December 2025: Samsung Electronics gained ENERGY STAR 9.0 certification for the Galaxy Book4 series, demonstrating compliance with updated efficiency standards.

- November 2025: Lenovo introduced the ThinkPad X1 Carbon Gen 12 with Intel Core Ultra chips and enhanced AI security features.

Global Notebook Computer Market Report Scope

The Notebook Computer Market refers to the global industry encompassing the design, manufacturing, distribution, and sale of portable personal computers that integrate a display, keyboard, processing, storage, and a battery into a single, compact device. These systems are designed to deliver computing functionality on the go, supporting a wide range of personal, professional, educational, and entertainment applications.

The Notebook Computer Market Report is Segmented by Product Type (Traditional Notebook, 2-in-1 Convertible, Gaming Notebook, and Ultrabook), Operating System (Windows, macOS, Chrome OS, Linux, and and Other OS), End-User Industry (Personal, Business, Gaming, and Education), Screen Size (Up to 12 inches, 13-14.9 inches, 15-16.9 inches, and 17 inches and Above), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Traditional Notebook |

| 2-in-1 Convertible |

| Gaming Notebook |

| Ultrabook |

| Windows |

| macOS |

| Chrome OS |

| Linux and Other OS |

| Personal |

| Business |

| Gaming |

| Education |

| Up to 12 inches |

| 13-14.9 inches |

| 15-16.9 inches |

| 17 inches and Above |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Traditional Notebook | ||

| 2-in-1 Convertible | |||

| Gaming Notebook | |||

| Ultrabook | |||

| By Operating System | Windows | ||

| macOS | |||

| Chrome OS | |||

| Linux and Other OS | |||

| By End-User Industry | Personal | ||

| Business | |||

| Gaming | |||

| Education | |||

| By Screen Size | Up to 12 inches | ||

| 13-14.9 inches | |||

| 15-16.9 inches | |||

| 17 inches and Above | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Notebook computer market by 2031?

It is forecast to reach USD 239.89 billion by 2031.

How fast is the gaming notebook segment expanding?

Gaming notebooks are projected to grow at a 7.27% CAGR from 2026 to 2031.

Which region is expected to post the fastest growth through 2031?

Europe is set to record an 8.12% CAGR due to upcoming sustainability regulations.

Why are AI-centric processors important for new notebooks?

Neural engines above 40 TOPS enable local inference, reducing cloud costs and latency, and justify higher ASPs.

How will European Ecodesign rules influence notebook design?

They will reward vendors offering modular, easily repairable devices and energy-efficient power supplies.

Page last updated on: