AI In Radiology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 7.19 Billion |

| Growth Rate (2026 - 2031) | 25.38% CAGR |

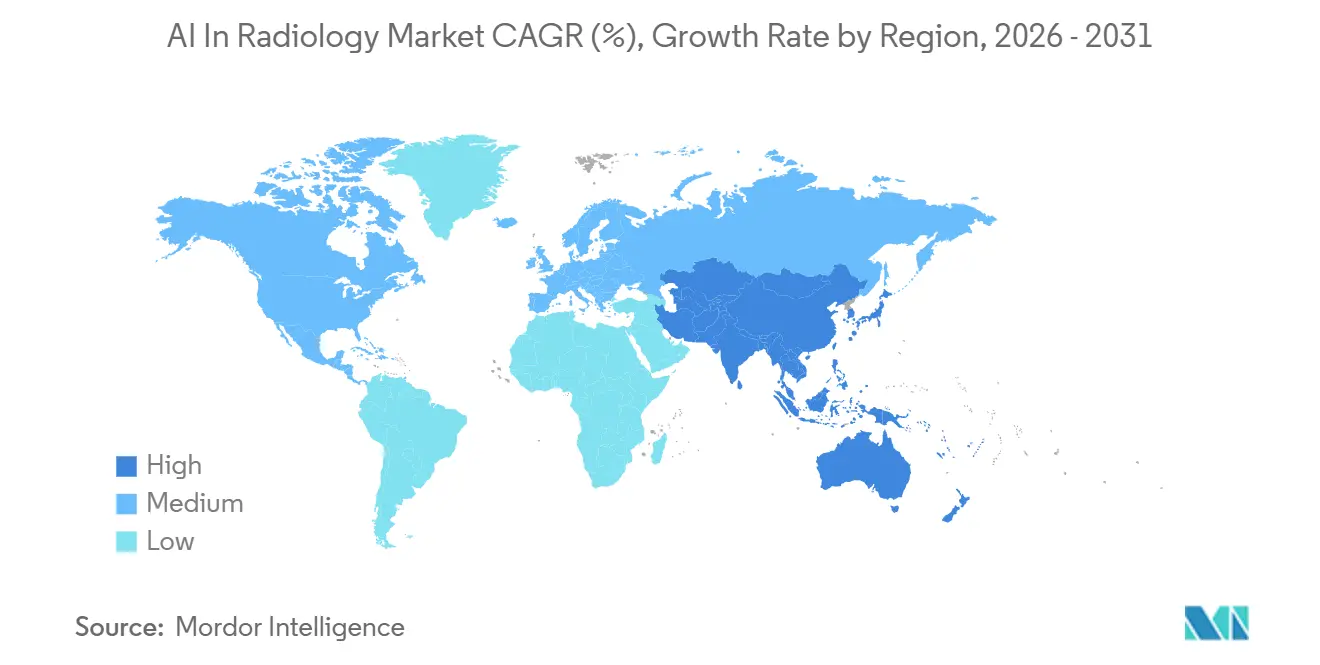

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

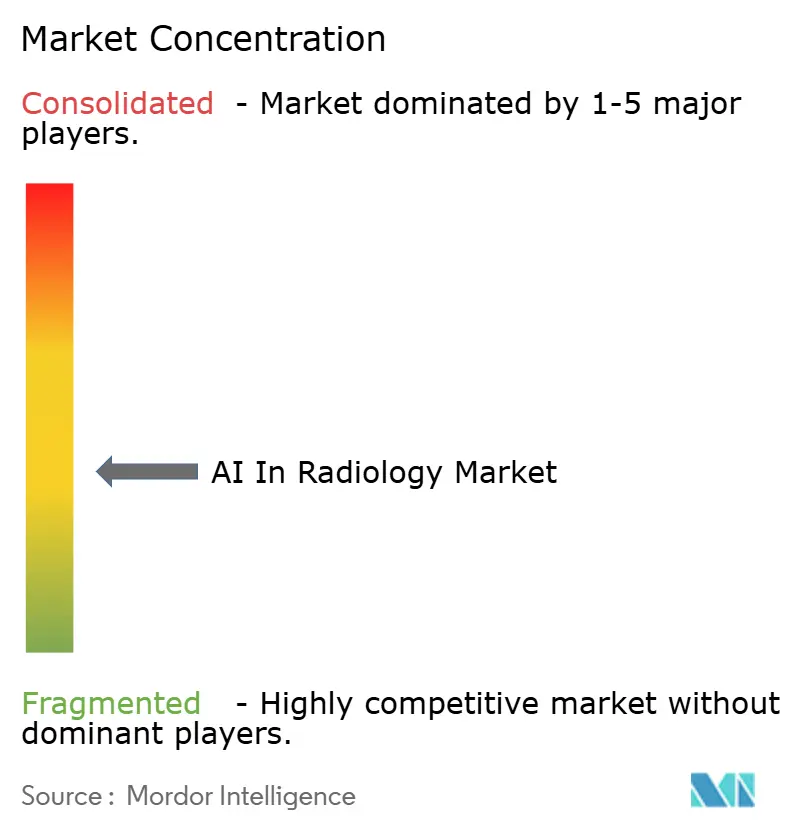

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Radiology Market Analysis by Mordor Intelligence

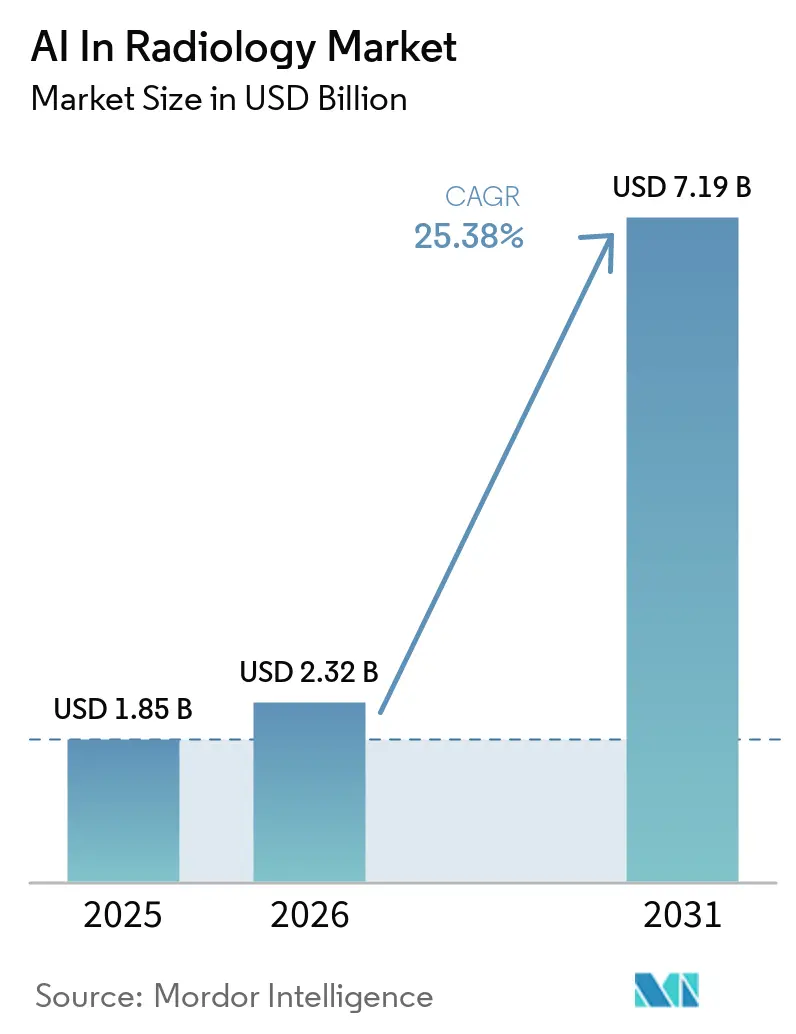

The AI In Radiology Market size is expected to grow from USD 1.85 billion in 2025 to USD 2.32 billion in 2026 and is forecast to reach USD 7.19 billion by 2031 at 25.38% CAGR over 2026-2031.

The market is being shaped by a capacity gap that is now structural, because imaging demand is rising faster than the radiologist pipeline in several major healthcare systems. A study in the American Journal of Neuroradiology documented a cumulative diagnostic radiology graduate deficit of 21,645 positions in the United States between 2014 and 2023, which keeps demand for assisted interpretation and workflow support firm in the AI in radiology market. The AI in radiology market is also moving from stand-alone pilots to wider platform deployment, as health systems want governance, interoperability, and post-deployment monitoring across multiple imaging workflows. The commercial advantage is shifting toward vendors that can show faster turnaround, lower repeat-scan risk, and easier integration into existing imaging and clinical systems, rather than only strong algorithm performance. That is why the AI in radiology market is expanding through both mature hospital networks and high-growth outpatient and digital imaging settings.

Key Report Takeaways

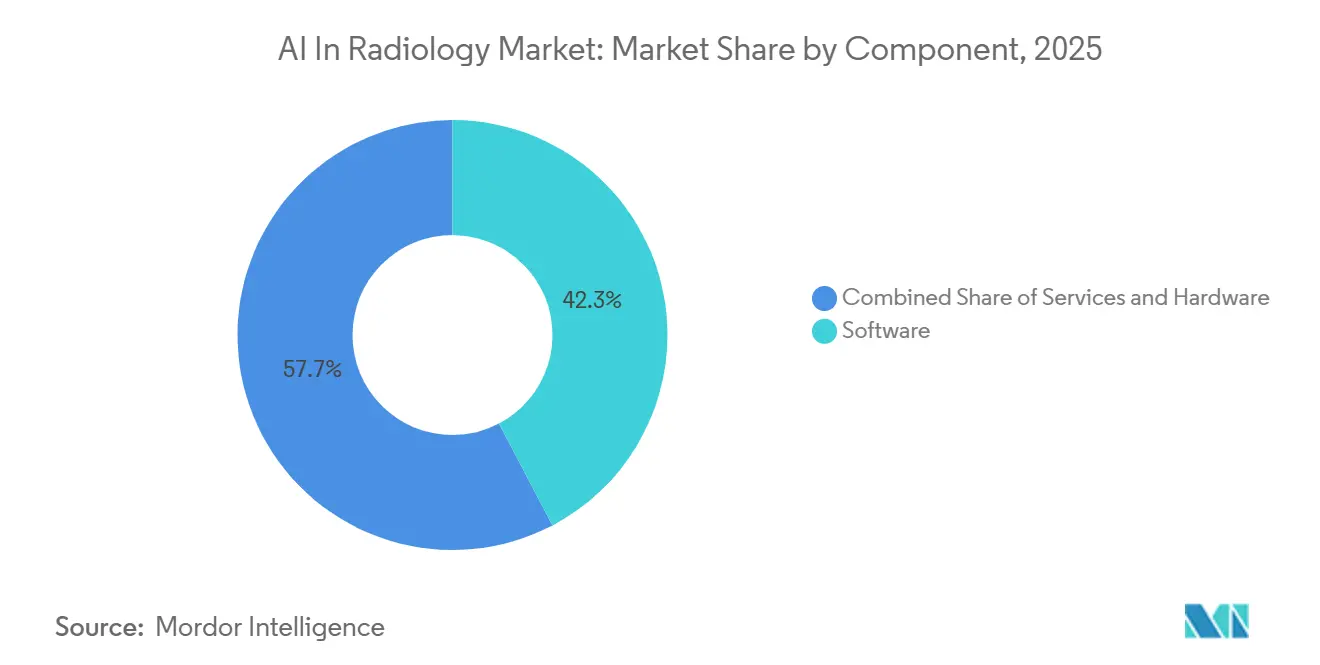

- By component, software held 42.31% of revenue in 2025, while services are expected to record the highest CAGR at 27.38% through 2031.

- By technology, deep learning led with 55.24% of revenue in 2025, while natural language processing is forecast to grow at 26.52% CAGR through 2031.

- By modality, computed tomography accounted for 35.52% of revenue in 2025, while X-ray is projected to expand at 26.25% CAGR through 2031.

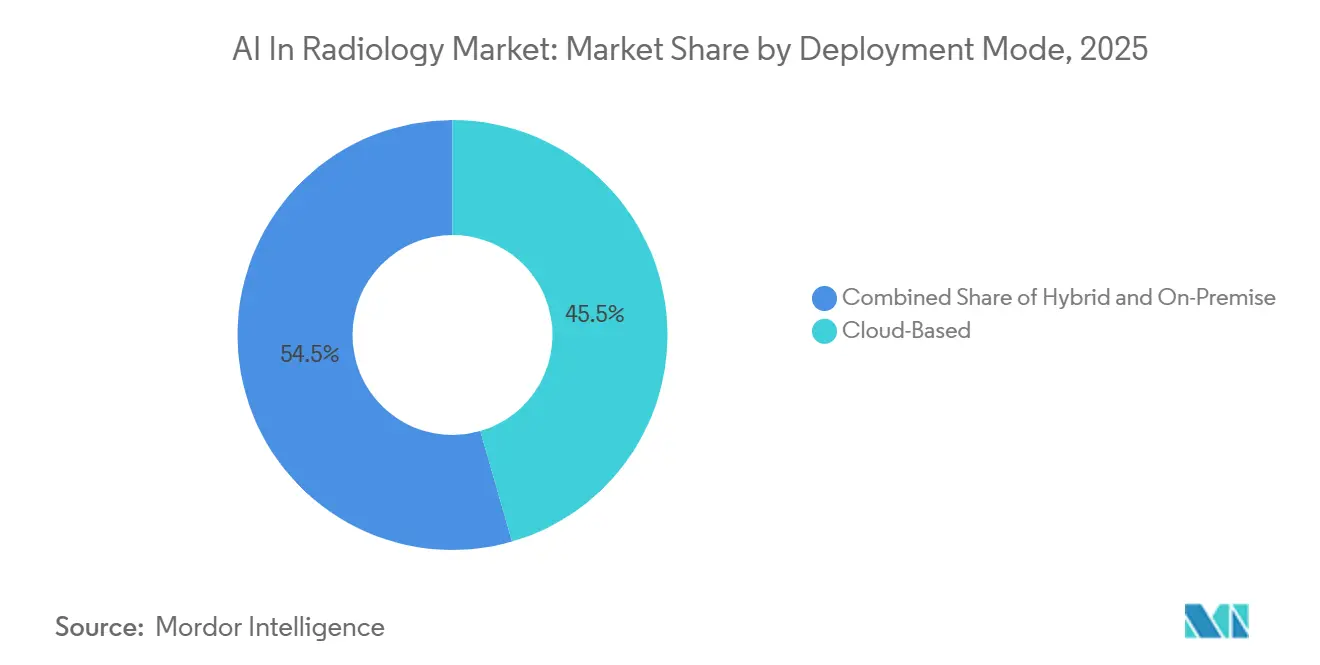

- By deployment mode, cloud-based deployment held 45.54% of revenue in 2025, while hybrid deployment is expected to grow at 27.15% CAGR through 2031.

- By application, detection and diagnosis captured 32.42% of revenue in 2025, while workflow optimization and triage is projected to advance at 27.25% CAGR through 2031.

- By end user, hospitals and clinics held 51.52% of revenue in 2025, while diagnostic imaging centers are forecast to grow at 26.55% CAGR through 2031.

- By geography, North America held 43.22% of revenue in 2025, while Asia-Pacific is projected to expand at 27.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Radiology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Imaging Volumes and Scan Backlogs | +5.2% | Global, acute in North America, UK, India | Medium term (2-4 years) |

| Radiologist Shortage and Burnout Relief | +4.8% | Global, particularly US, UK, Germany, Australia | Long term (≥ 4 years) |

| Demand for Faster Triage and Turnaround Times | +4.5% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Regulatory Support for AI SaMD Approvals | +3.8% | US (FDA 510k), EU (MDR/EU AI Act), China (NMPA) | Medium term (2-4 years) |

| Enterprise PACS and EHR Interoperability Push | +3.2% | North America and EU, spill-over to APAC and MEA | Medium term (2-4 years) |

| Value-Based Care Pressure on Repeat-Scan Reduction | +2.5% | North America, emerging in Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Imaging Volumes and Scan Backlogs

The AI in radiology market is expanding because scan volumes continue to rise faster than reading capacity in many health systems. In the United Kingdom, diagnostic imaging demand grows at more than 5% annually, while workforce supply has been expanding at close to 3%, and a 33% radiology staffing shortfall was documented in 2023. Aging populations, oncology surveillance, and wider use of advanced CT are keeping imaging workloads elevated across both developed and emerging care settings. This makes queue control a direct purchasing argument in the AI in radiology market, because providers want tools that can prioritize urgent studies and keep reporting delays from widening. The result is that buyers are looking beyond stand-alone detection and are asking whether a tool can reduce backlogs across the full imaging workflow. That demand pattern supports broader platform adoption in the AI in radiology market instead of narrow point-solution deployment.

Radiologist Shortage and Burnout Relief

The radiologist workforce gap is a long-term driver for the AI in radiology market because the training pipeline is not expanding fast enough to match care demand. Between 2014 and 2023, radiology job listings on the ACR Career Center totaled 31,825 against 10,180 anticipated residency graduates, leaving a cumulative deficit of 21,645 positions in the United States. A 2025 review also noted projections of a 122,000 radiologist shortage by 2032, which reinforces the view that this supply issue is structural rather than cyclical. In a 2025 Journal of the American College of Radiology survey, 100% of academic radiology department chairs planned AI implementation to improve quality and efficiency, and 95% planned it to reduce burnout[1]“Artificial Intelligence in Radiology: A Leadership Survey,” Journal of the American College of Radiology, jacr.org. The practical value in the AI in radiology market is not only task automation, because cognitive offloading through prioritization, structured outputs, and draft support can lower fatigue without changing the radiologist’s clinical role. That keeps adoption interest high across hospital networks that need productivity gains but still want physician oversight.

Demand for Faster Triage and Turnaround Times

The AI in radiology market is also gaining support from the need to shorten time to diagnosis in urgent imaging conditions. A 2025 structured narrative review found that AI-enabled triage reduced time to diagnosis by as much as 90% in some hospital settings through faster prioritization and automated alerting. Stroke, intracranial hemorrhage, and pulmonary embolism remain the clearest use cases because clinical value is immediate when the reading list is reordered around urgent findings. Vendors are now winning more of the AI in radiology market when results appear directly inside PACS, RIS, and EHR workflows, because radiologists and emergency teams do not want another isolated interface. This makes workflow design just as important as model performance when systems compare vendors. It also explains why throughput improvement is becoming a stronger commercial message than diagnostic novelty in the AI in radiology market.

Regulatory Support for AI SaMD Approvals

Regulatory normalization is supporting the AI in radiology market because imaging software is moving through clearer approval pathways in major countries. In Japan, the Japan Radiological Society published the revised second edition of its management guidelines for AI-based imaging diagnostic support software in April 2025, which reflected a more formalized operating environment for radiology AI tools. In China, the National Medical Products Administration approved 76 innovative medical devices in 2025, up 17% year on year, and also launched a second batch of AI medical device innovation selection tasks. These developments matter in the AI in radiology market because they expand the number of approved products and improve institutional confidence in procurement. At the same time, faster approvals do not remove the need for proof on workflow value, reimbursement fit, and deployment support. That is why regulatory progress is helping the AI in radiology market most when vendors can pair approvals with a clear operating and integration model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Cost and ROI Uncertainty | -3.5% | Global, acute in smaller systems and emerging markets | Short term (≤ 2 years) |

| Data Quality, Label Scarcity, and Annotation Cost | -2.8% | Global, acute for rare disease and non-CT modalities | Long term (≥ 4 years) |

| Regulatory Fragmentation Across Countries | -1.5% | EU vs. US vs. APAC jurisdictions | Medium term (2-4 years) |

| Low Trust in Black-Box Outputs for Edge Cases | -1.2% | Global, especially pronounced in Europe under MDR | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation Cost and ROI Uncertainty

Implementation cost is still a real brake on the AI in radiology market, especially for smaller health systems and imaging providers outside top-tier institutions. The cost issue goes beyond software licenses because buyers also face integration testing, workflow changes, staff retraining, and ongoing monitoring after deployment. In the 2025 Journal of the American College of Radiology survey, cost was identified as the leading concern among academic radiology department chairs evaluating AI deployment. Smaller providers often have less room to absorb uncertain returns, so the AI in radiology market can move more slowly where digital imaging infrastructure is still limited. The challenge is stronger when procurement teams cannot compare outcomes across similar facilities with a consistent cost-benefit model. That is why shared-risk pricing and managed service structures are gaining attention in the AI in radiology market, because they shift some of the commercial burden back to vendors.

Data Quality, Label Scarcity, and Annotation Cost

The AI in radiology market still faces a data problem because strong model performance depends on large, diverse, and well-annotated imaging datasets. This is easier to achieve in high-volume use cases, but it remains harder in rare pathologies, lower-volume modalities, and settings with uneven reporting quality. Annotation adds cost because clinical labeling must be done carefully and then maintained through model updates, validation work, and documentation. The burden is higher for smaller developers in the AI in radiology market because they have fewer internal resources to sustain repeated evidence generation. This can narrow innovation toward common diseases and well-studied modalities where data availability is stronger. It also means that progress in the AI in radiology market depends not only on algorithm design, but also on the ability to build durable data and validation pipelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Commands Revenue, Services Accelerate on Platform Economics

Software accounted for 42.31% of AI in radiology market share in 2025, while services are projected to grow at 27.38% CAGR through 2031. The current revenue lead reflects the installed base of cleared tools used for detection, classification, prioritization, and reporting support across hospital and imaging networks. In the AI in radiology market, software remains the first layer buyers evaluate because it directly affects reading workflow, case routing, and operational throughput. The installed base also gives software vendors a recurring opportunity to expand into adjacent imaging indications within the same health system. As a result, the software layer still anchors procurement decisions in the AI in radiology market.

Services are gaining faster because deployment is no longer limited to a single algorithm or a narrow pilot program. Enterprise buyers now want implementation support, model monitoring, retraining, governance, and change management as standard parts of the contract. The AI in radiology market therefore creates room for managed services that help hospitals run multiple clinical algorithms under one operating structure. Hardware continues to support growth through AI-accelerated scanner upgrades, but the revenue mix is shifting toward software and services as institutions prioritize flexible deployment and long-term support. That shift also reflects the wider move in the AI in radiology industry toward repeatable platform economics instead of one-time tool purchases.

By Technology: Deep Learning Anchors Deployments, NLP Defines the Reporting Frontier

Deep Learning held 55.24% of revenue in 2025, which kept it as the core technology foundation in the AI in radiology market. Its lead comes from established use in image classification, anomaly detection, segmentation, and organ quantification across CT and X-ray workflows. Because most deployed imaging algorithms still depend on these tasks, deep learning is likely to remain central to the installed base over the forecast period. Machine learning also supports the AI in radiology market through predictive models and risk stratification use cases that extend beyond direct image reading. Computer vision tools are increasingly being used during image acquisition to help assess quality and reduce the need for repeat studies.

Natural language processing is the fastest-growing technology in the AI in radiology market at 26.52% CAGR through 2031. That growth shows that the next control point is shifting toward reporting support, structured documentation, and automatic population of routine findings. A 2026 paper in Information Systems Frontiers described concept-enhanced multimodal retrieval-augmented generation as a viable path toward more interpretable and accurate radiology report generation. The reporting layer matters because radiologists need speed, consistency, and lower cognitive load, not only better image classification. This is one of the clearest areas where the AI in radiology industry can move from assisting image review to supporting the full reporting workflow.

By Modality: CT Leads Clinical Deployment, X-ray Drives Population-Level Reach

Computed tomography held 35.52% of modality revenue in 2025, which made CT the leading clinical base for the AI in radiology market. CT remains the most established modality for emergency triage, oncology staging, multi-organ assessment, and quantitative interpretation support. In April 2026, Philips received FDA 510(k) clearance for Verida, its detector-based spectral CT system with AI-powered reconstruction, showing that AI is now being embedded into scanner performance as well as post-processing software[2]“Philips Receives FDA 510(k) Clearance for Verida, the World’s First AI-Powered Detector-Based Spectral CT,” Philips Press Release, philips.com. CT also benefits from clearer clinical pathways and broader evidence generation than several other imaging modalities. This keeps CT at the center of commercial deployment in the AI in radiology market.

X-ray is projected to grow at 26.25% CAGR through 2031, giving it the fastest modality expansion in the AI in radiology market. Growth is being supported by community hospitals and imaging centers that need scalable screening and triage tools without the same cost base as advanced cross-sectional imaging. A June 2026 study in Scientific Reports found that deep-learning based image reconstruction enabled reduced-dose CT pulmonary angiography with non-inferior image quality, which strengthens the wider case for AI-assisted imaging quality and efficiency. MRI development remains active in targeted areas such as brain and musculoskeletal imaging, but model development is more selective where data generation and validation are harder to scale. Mammography is advancing through screening use cases, while ultrasound and PET remain smaller but valuable opportunities in the AI in radiology market.

By Deployment Mode: Cloud Leads, Hybrid Emerges as the Preferred Enterprise Architecture

Cloud-based deployment held 45.54% of the AI in radiology market size in 2025, while hybrid deployment is projected to grow at 27.15% CAGR through 2031. Cloud has led adoption because multi-site imaging networks need elastic storage, shared worklists, and centralized visibility across radiology operations. That model also supports faster scaling when a health system wants to add new algorithms across multiple facilities under one operating framework. In the AI in radiology market, cloud deployment is closely tied to the broader push for enterprise PACS and EHR interoperability, because hospitals want AI results to move through systems already used by radiologists and referring clinicians. This keeps cloud as the leading starting point for digital imaging modernization.

Hybrid deployment is growing faster because many institutions want cloud flexibility without giving up local control over sensitive imaging operations. Philips expanded its cloud-based enterprise imaging services to Europe in 2025 after earlier migrations across more than 150 sites in North and Latin America, which shows how large imaging networks are building cloud-enabled operating models around AI workflows. RapidAI stated in December 2025 that its Rapid Edge Cloud supported hospitals in more than 100 countries, which highlights the appeal of combining local continuity with distributed analytics. On-premise deployment remains relevant in systems with strict data localization rules, but the AI in radiology market is clearly moving toward mixed architectures that balance compliance, uptime, and scale. That makes hybrid the most practical long-term design choice for many large providers.

By Application: Detection Anchors the Installed Base, Workflow Optimization Captures the Next Wave

Detection and diagnosis held 32.42% of application revenue in 2025, which kept it as the largest installed base in the AI in radiology market. The lead comes from years of deployment in lung nodule detection, mammography support, chest X-ray screening, and stroke-related triage workflows. These tools remain important because they are easier to connect to defined clinical decisions and established imaging protocols. They also gave early vendors a clear route into the AI in radiology market through measurable use cases that radiology departments could test and validate. This explains why detection still represents the most established commercial category.

Workflow optimization and triage are projected to grow at 27.25% CAGR through 2031, making them the fastest application area in the AI in radiology market. Buyers increasingly want evidence that AI can reduce reading delays, speed routing, and improve radiologist capacity during peak imaging demand. Image segmentation and classification continue to matter in oncology and procedure planning, but procurement attention is shifting toward time saved and throughput gained. Pressure to limit repeat scans and unnecessary downstream work also supports tools that improve image quality, prioritize urgent findings, and standardize reporting steps. That is why premium contract value is moving toward workflow platforms in the AI in radiology market, while basic detection tools face a more competitive pricing environment.

By End User: Hospitals Anchor the Installed Base, Imaging Centers Accelerate

Hospitals and clinics accounted for 51.52% of the AI in radiology market size in 2025, while diagnostic imaging centers are projected to expand at 26.55% CAGR through 2031. Hospitals remain the largest end users because they handle emergency imaging, inpatient complexity, and high-acuity case mixes where triage and prioritization tools deliver clear operational value. The concentration of advanced modalities and larger IT teams also makes hospitals the first environment for multi-tool AI governance. Aidoc announced that Asklepios completed a 28-hospital AI rollout in radiology by the end of 2025, with the program linked to Germany’s Hospital Future Act funding. This kind of network-scale deployment shows why hospitals still anchor the installed base of the AI in radiology market.

Diagnostic imaging centers are growing faster because outpatient networks need throughput gains without matching increases in radiologist headcount. In December 2025, Lunit announced a partnership with SimonMed Imaging to deploy custom chest X-ray foundation models across a network of more than 175 locations. That move matters because it shows the AI in radiology market is expanding well beyond large academic centers into scaled outpatient imaging operations. Ambulatory surgical centers remain a smaller segment, but they are adding AI in perioperative imaging support and remote reading workflows. Teleradiology providers and research institutions add volume at lower average selling prices, which broadens the commercial base of the AI in radiology market without changing hospital leadership.

Geography Analysis

North America held 43.22% of AI in radiology market share in 2025, which kept it as the largest regional base for the AI in radiology market. The region has moved further than others from pilot testing into enterprise procurement, especially in hospital systems with strong digital imaging infrastructure. The United States remains the main driver because it combines large imaging volumes, active academic deployment, and a dense vendor base spanning OEMs and software specialists. In March 2026, GE HealthCare completed its USD 2.3 billion acquisition of Intelerad, which expanded its cloud-first enterprise imaging footprint across the United States, Canada, the United Kingdom, and Oceania. Canada and Mexico remain smaller contributors, but they benefit from proximity to the same interoperability standards and vendor ecosystem that support the AI in radiology market in the United States.

Europe remains the second-largest regional block in the AI in radiology market, with Germany, the United Kingdom, France, Italy, and Spain forming the core demand base. Germany has been especially important because hospital modernization funding accelerated imaging AI rollout at scale, including the 28-hospital Asklepios deployment reported by Aidoc in 2025. As of January 2025, at least 219 radiology AI products held EU CE certification, which shows the breadth of available products in the region[3]“Laut Health AI Register, Mindestens 219 Produkte mit KI CE-zertifiziert,” MD-BUND, md-bund.de. This gives the AI in radiology market in Europe a wide product base, even though compliance demands remain layered across national and EU-level requirements.

Asia-Pacific is the fastest-growing region in the AI in radiology market at 27.15% CAGR through 2031. China, Japan, South Korea, India, and Australia are the main growth engines because they combine healthcare digitalization with expanding imaging capacity and a rising number of local and imported AI products. China’s National Medical Products Administration approved 76 innovative medical devices in 2025, up 17% year on year, which points to stronger product availability for advanced care technologies. In August 2025, Shanghai United Imaging Healthcare’s uCT Ultima, described as the first domestically developed photon-counting spectral CT, received NMPA approval and entered clinical testing at major Shanghai hospitals. Japan also formalized its operating environment in 2025 through revised guidance from the Japan Radiological Society. Middle East and Africa are gaining traction through national digital health programs, while South America remains earlier stage, with Brazil and Argentina as the main openings for the AI in radiology market.

Competitive Landscape

The AI in radiology market is moderately fragmented, with large imaging OEMs, specialized software vendors, and platform-focused firms all competing across different modalities and workflows. No single company controls the full field because hospitals buy differently for scanner integration, triage, reporting support, cloud imaging, and outpatient workflow automation. OEMs retain an advantage in the AI in radiology market when AI is embedded into hardware, reconstruction, and enterprise imaging systems already used by hospitals. GE HealthCare’s March 2026 completion of the Intelerad acquisition shows how major players are expanding beyond equipment into cloud-first imaging and software orchestration. Philips also strengthened this position in 2026 with Verida, which tied AI directly to scanner-level reconstruction and exam throughput.

Pure-play vendors are competing differently in the AI in radiology market by building platforms that can sit across multiple algorithms, facilities, and clinical use cases. Aidoc’s 28-hospital Asklepios rollout shows how software specialists are winning through network-scale deployment and centralized governance rather than through a single diagnostic point solution. Lunit’s December 2025 partnership with SimonMed Imaging shows another route, where a vendor uses foundation models and a large outpatient network to secure scaled distribution in the AI in radiology market. These moves suggest that workflow reach, installed network depth, and recurring operational support are becoming stronger advantages than isolated algorithm claims.

Competition in the AI in radiology market is also being shaped by architecture choices. Vendors that can fit into existing PACS, cloud archives, and clinical systems are better positioned than those that require separate operational pathways. Philips’ 2025 expansion of cloud-based enterprise imaging services to Europe and RapidAI’s scale across more than 100 countries both show that deployment architecture is now part of competitive positioning. The next separation point is likely to come from reporting support, multimodal orchestration, and measurable workflow outcomes, because buyers increasingly want proof that AI improves radiologist capacity and clinical operations. That keeps the AI in radiology market open to both established OEMs and focused software vendors, but it favors those that can connect approval, deployment, and workflow value in one commercial package.

AI In Radiology Industry Leaders

Siemens Healthineers AG

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Aidoc Medical Ltd.

Viz.ai, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Subtle Medical received FDA clearance for SubtleHD (CT), its 11th FDA-cleared product and first CT offering, expanding its AI-powered image enhancement platform already deployed across 1,300+ scanners into CT imaging to address consistency needs across mixed scanner generations.

- April 2026: Philips received FDA 510(k) clearance for Verida, the world's first AI-powered detector-based spectral CT system, capable of reconstructing 145 images per second and supporting up to 270 exams per daily shift through its deep-learning reconstruction engine and always-on spectral imaging architecture.

Global AI In Radiology Market Report Scope

As per the scope of the report, AI in radiology refers to the application of artificial intelligence technologies, such as machine learning and deep learning, to improve various aspects of medical imaging. It involves developing algorithms that can analyze radiological images (like X-rays, CT scans, MRI scans) to assist in diagnosing diseases, detecting abnormalities, and enhancing image interpretation accuracy and efficiency.

The segmentation for the AI in radiology market is categorized by component, technology, modality, deployment mode, application, end user, and geography. By component, the market is divided into software, services, and hardware. By technology, it includes deep learning, machine learning, natural language processing, and computer vision. By modality, the segmentation covers computed tomography, magnetic resonance imaging, X-ray, ultrasound, mammography, positron emission tomography, and other modalities. By deployment mode, the market is segmented into cloud-based, on-premise, and hybrid. By application, it encompasses detection and diagnosis, image segmentation and classification, workflow optimization and triage, predictive and prognostic analytics, disease risk assessment, and other applications. By end user, the market is divided into hospitals and clinics, diagnostic imaging centers, ambulatory surgical centers, and other end users. By geography, the segmentation includes North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software |

| Services |

| Hardware |

| Deep Learning |

| Machine Learning |

| Natural Language Processing |

| Computer Vision |

| Computed Tomography |

| Magnetic Resonance Imaging |

| X-ray |

| Ultrasound |

| Mammography |

| Positron Emission Tomography |

| Other Modalities |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Detection and Diagnosis |

| Image Segmentation and Classification |

| Workflow Optimization and Triage |

| Predictive and Prognostic Analytics |

| Disease Risk Assessment |

| Other Applications |

| Hospitals and Clinics |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware | ||

| By Technology | Deep Learning | |

| Machine Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| By Modality | Computed Tomography | |

| Magnetic Resonance Imaging | ||

| X-ray | ||

| Ultrasound | ||

| Mammography | ||

| Positron Emission Tomography | ||

| Other Modalities | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Application | Detection and Diagnosis | |

| Image Segmentation and Classification | ||

| Workflow Optimization and Triage | ||

| Predictive and Prognostic Analytics | ||

| Disease Risk Assessment | ||

| Other Applications | ||

| By End User | Hospitals and Clinics | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the AI in radiology market by 2031?

The AI in radiology market is forecast to reach USD 7.19 billion by 2031, up from USD 2.32 billion in 2026, at a 25.38% CAGR over 2026-2031.

Why is radiology AI adoption accelerating in 2026?

Adoption is being driven by sustained imaging backlogs, structural radiologist shortages, and stronger demand for triage, faster reporting, and enterprise workflow integration.

Which region leads the AI in radiology market?

North America led with 43.22% of 2025 revenue, supported by mature hospital IT environments, active enterprise procurement, and a strong vendor base.

Which region is growing fastest through 2031?

Asia-Pacific is projected to grow at 27.15% CAGR through 2031 as China, Japan, India, South Korea, and Australia expand digital imaging and regulatory support.

Which technology area is growing fastest in radiology AI?

Natural language processing is the fastest-growing technology at 26.52% CAGR through 2031 because reporting support, structured outputs, and documentation automation are becoming more important.

Why do hospitals still account for the largest share of spending?

Hospitals and clinics held 51.52% of 2025 revenue because they manage emergency imaging, complex inpatient workflows, and the largest need for integrated triage and reporting tools.

Page last updated on: