AI in Oncology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

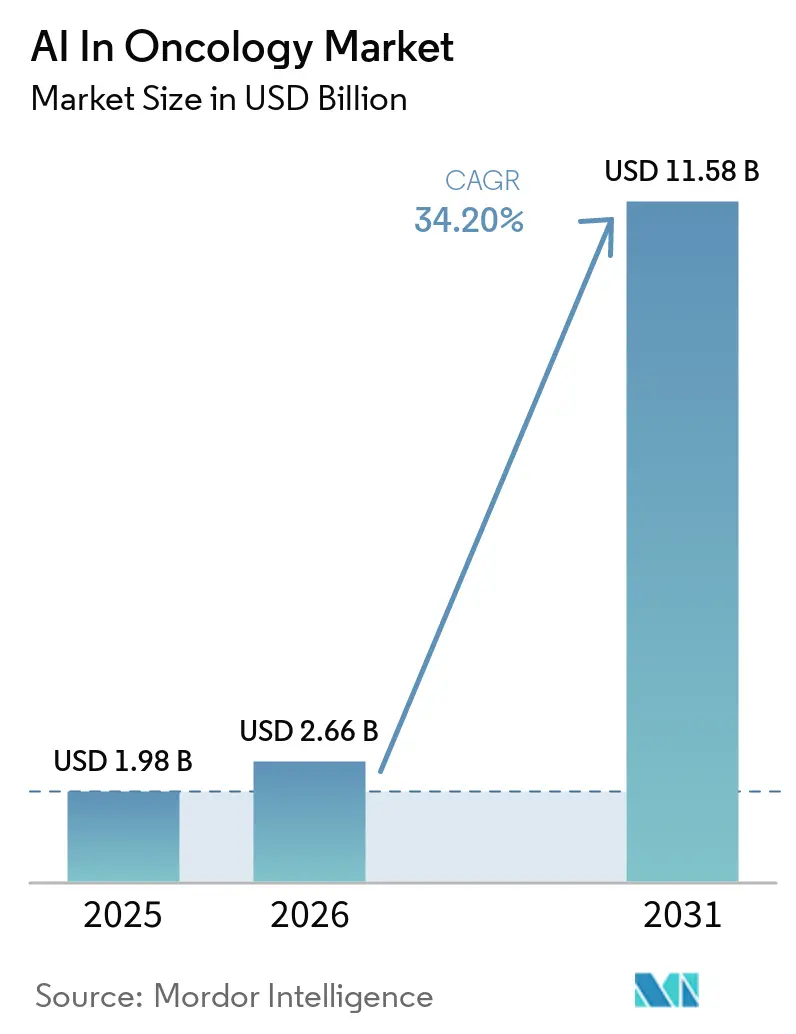

| Market Size (2026) | USD 2.66 Billion |

| Market Size (2031) | USD 11.58 Billion |

| Growth Rate (2026 - 2031) | 34.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI in Oncology Market Analysis by Mordor Intelligence

AI in oncology market size in 2026 is estimated at USD 2.66 billion, growing from 2025 value of USD 1.98 billion with 2031 projections showing USD 11.58 billion, growing at 34.20% CAGR over 2026-2031. This exceptional expansion rests on three intertwined forces: the mounting global cancer burden, the scramble to offset shortages of oncology specialists and radiologists, and the clinical pivot toward precision-medicine strategies that demand rapid data interpretation across genomics, imaging and real-world evidence. Radiology and pathology departments are embracing cloud-based AI tools that overlay seamlessly on existing scanners, avoiding large capital expenditure and shortening deployment cycles. Regulators are simultaneously streamlining approvals, with the US FDA already listing more than 1,000 AI/ML-enabled medical devices—77% of them in radiology—thereby creating clear precedents for oncology-specific submissions[1]US Food and Drug Administration, “List of AI/ML-Enabled Medical Devices,” fda.gov.

Developers that pair high-quality multi-modal datasets with robust clinical validation now enjoy privileged access to venture funding, epitomised by multi-hundred-million-dollar rounds for Tempus, PathAI and Pathos AI. Yet adoption still hinges on demonstrable return on investment: providers want evidence that earlier detection lowers treatment costs and improves survival, and they expect software-as-a-service models that align AI spending with patient volumes rather than fixed hardware budgets. Overall, the AI in oncology market is racing toward mainstream clinical use as payers, regulators and clinicians converge on a common goal—diagnose earlier, treat smarter, and do both at scale.

Key Report Takeaways

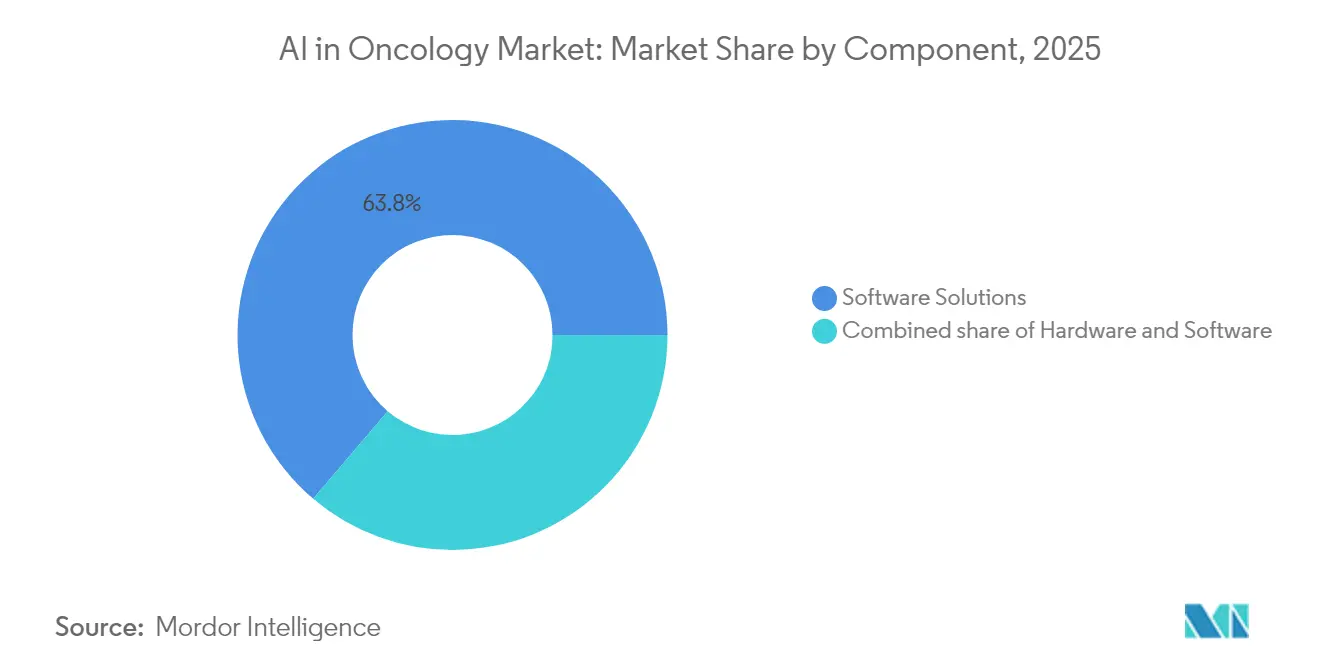

- By component, Software Solutions held 63.78% of the AI in oncology market share in 2025; Services are set for the fastest growth at a 36.10% CAGR to 2031.

- By cancer type, Breast Cancer led with 28.05% revenue share in 2025, whereas Brain Tumor applications are forecast to expand at a 36.85% CAGR through 2031.

- By treatment type, Radiotherapy accounted for 41.02% of the AI in oncology market size in 2025, while Immunotherapy-focused solutions are projected to grow at a 35.90% CAGR between 2026-2031.

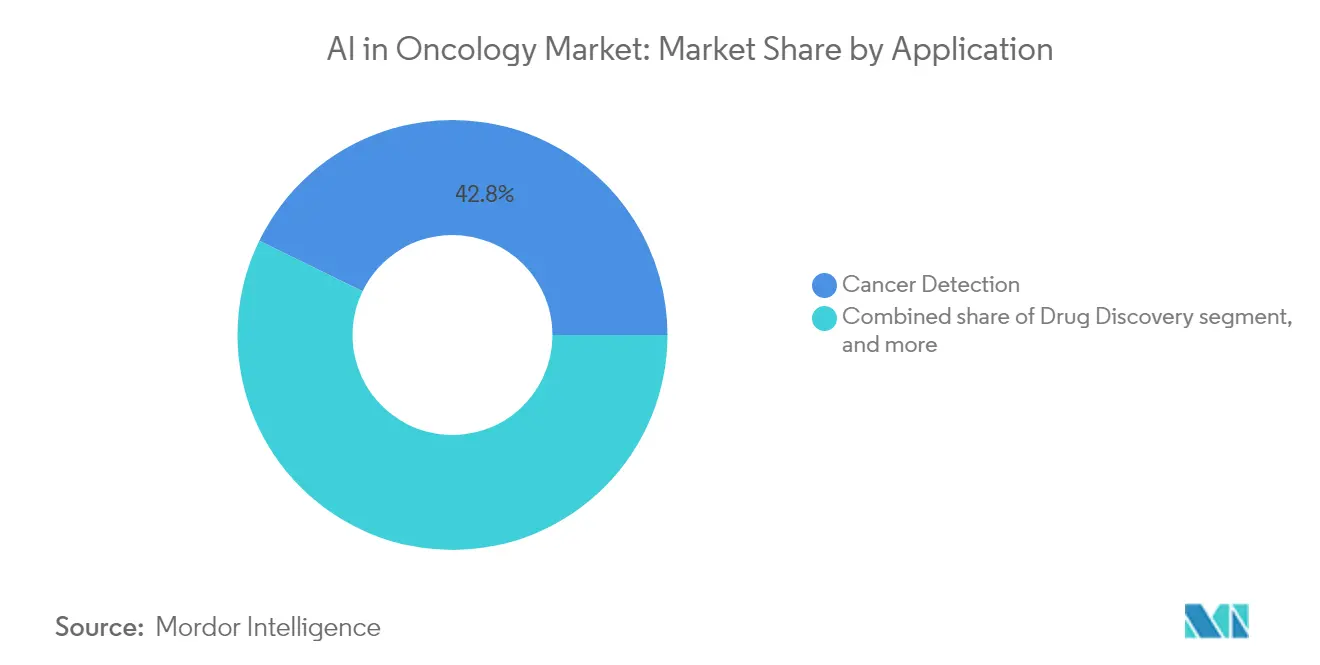

- By application, Cancer Detection captured 42.78% of 2025 revenues; Drug Discovery is expected to post the highest CAGR at 37.10% over the same horizon.

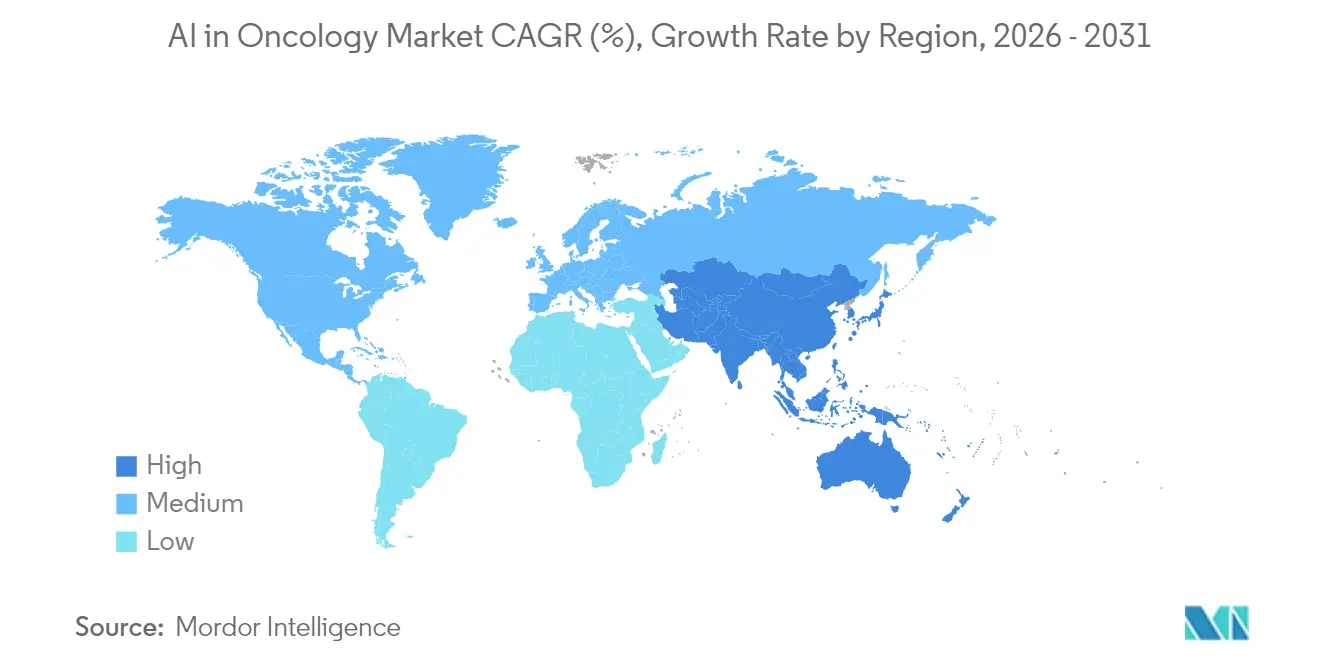

- By geography, North America commanded 44.12% of 2025 revenue, supported by the largest installed base of FDA-cleared AI devices and strong venture funding pipelines.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI in Oncology Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Cancer Burden Worldwide | +8.2% | Global | Long term (≥ 4 years) |

| Expanding Precision Medicine Programs | +7.1% | North America, EU, APAC core | Medium term (2-4 years) |

| Integration of AI With Medical Imaging Modalities | +6.8% | Global, earliest in North America & Europe | Short term (≤ 2 years) |

| Accelerated Approvals of AI-Based Oncology Devices | +5.3% | Primarily North America & EU; spill-over into APAC | Medium term (2-4 years) |

| Rising Investments From Big Tech and Pharma | +4.9% | Global, funding clusters in United States and China | Short term (≤ 2 years) |

| Proliferation of Cloud-Based Healthcare Data | +3.2% | Worldwide, faster uptake in high-income markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Cancer Burden Worldwide

New cancer diagnoses are projected to swell by more than 12 million cases annually by 2050, a trend most acute in lower-income countries that lack specialist capacity[2]International Agency for Research on Cancer, “Global Cancer Statistics 2024,” iarc.who.int. Rising incidence magnifies the appeal of lightweight AI tools that operate on commodity laptops, enabling radiologists to triage images rapidly and spot tumours that conventionally slip through busy reading rooms. Global spend on oncology therapeutics and supportive care hit USD 223 billion in 2023 and is on course to top USD 409 billion by 2028, prompting payers to reward technologies that can shave costs through earlier detection. Early-stage AI systems such as National Taiwan University Hospital’s PANCREASaver, which detects sub-2 cm pancreatic lesions with 86.4% accuracy, illustrate how algorithmic innovation can redirect care pathways toward prevention.

Expanding Precision Medicine Programs

AI has become the analytical engine of precision oncology, sifting through whole-genome sequencing, RNA expression, and digital pathology images to craft tailored regimens. The National Comprehensive Cancer Network’s endorsement of the ArteraAI Prostate Test, backed by randomised trials and level 1B evidence, has legitimised algorithmic prognostics in mainstream guidelines[3]National Comprehensive Cancer Network, “NCCN Adds ArteraAI Prostate Test,” nccn.org. In Europe, the €28 million Thera4Care consortium is establishing pan-EU protocols that link imaging, genomics, and treatment planning across 29 institutions, demonstrating how concerted funding can speed translational adoption. These programmes heighten demand for interoperable software frameworks that insert AI outputs directly into tumour-board workflows, trimming iteration cycles between sequencing results and treatment initiation.

Integration of AI With Medical Imaging Modalities

Radiology remains the gateway for clinical AI, accounting for more than three quarters of FDA-authorised algorithms. Devices such as CLAIRITY BREAST, the first tool cleared to forecast five-year breast-cancer risk from routine mammograms, show how AI bolsters incumbent hardware without necessitating new scanners. Siemens Healthineers has embedded seventy-plus AI applications—trained on 1.4 billion studies—into its imaging portfolio, giving providers turnkey access to advanced analytics at the console. Meanwhile, ultra-compact models from academic labs now achieve 92% lung-nodule accuracy on ordinary laptops using fewer than 70 training cases, a leap that widens global reach.

Accelerated Approvals of AI-Based Oncology Devices

Regulators are dismantling procedural bottlenecks. The US FDA intends to deploy AI-assisted dossier review systems by mid-2025, compressing clearance times for machine-learning devices. Breakthrough designation has become a fast lane for oncology tools such as Roche’s VENTANA TROP2 companion diagnostic for non-small-cell lung cancer, which marries immunohistochemistry with digital pathology. Europe’s Medical Device Regulation is likewise aligning AI technical dossiers around transparency and post-market surveillance, allowing firms to leverage CE marks as stepping-stones to multi-region launches.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation costs and ROI uncertainty | −3.7% | Global | Short term (≤ 2 years) |

| Stringent data privacy and security regulations | −2.9% | United States, Europe | Medium term (2-4 years) |

| Limited interoperability across oncology IT systems | −2.4% | Global | Medium term (2-4 years) |

| Shortage of AI-literate oncology workforce | −2.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs and ROI Uncertainty

Deploying enterprise-grade oncology AI often costs mid-sized cancer centres more than USD 1 million once specialised GPUs, data-integration bridges and staff training are tallied. Management teams struggle to balance these outlays against invisible savings from avoided late-stage treatments, especially because only 15 prospective studies between 2013-2023 have provided real-world outcome data for oncology AI. Hardware risk compounds the challenge: rapid algorithmic efficiency gains can make dedicated inference chips obsolete within two equipment cycles. Consequently, smaller providers favour pay-per-use cloud models but still face temporary workflow slowdowns during integration, lengthening their payback horizon.

Stringent Data Privacy and Security Regulations

Frameworks such as Europe’s GDPR oblige developers to embed privacy-by-design functions—data minimisation, encryption at rest and audit trails—into every pipeline. These safeguards extend development timelines by 12-18 months and raise costs for multi-centre studies that must harmonise consent forms across jurisdictions. Only 14.5% of FDA-authorised algorithms report race or ethnicity data, reflecting the difficulty of assembling diverse training sets under privacy constraints. Upcoming explainability mandates will require providers to show clinicians how black-box neural networks arrive at decisions, further stretching development budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Market Evolution

Software Solutions accounted for a 63.78% AI in oncology market share in 2025, underscoring hospitals’ preference for subscription-based algorithms that install on existing PACS viewers and radiation-planning consoles. The Services segment, projected to post a 36.10% CAGR to 2031, shows that many institutions are outsourcing data curation, algorithm tuning and post-deployment monitoring to specialised vendors rather than hiring in-house machine-learning engineers. ConcertAI’s Patient360™ projects illustrate the shift: more than 1,000 projects completed and 72% of revenue sourced from recurring managed services. Hardware, meanwhile, remains a niche purchase linked to ultra-high-resolution digital-pathology scanners or on-premise GPU clusters; buyers hesitate because successive neural-network generations run on ever-cheaper chips, threatening asset obsolescence.

In the medium term, value will migrate toward “platform” vendors that bundle data-management middleware, algorithm marketplaces and regulatory documentation templates. Such ecosystems lower integration friction and compress validation timelines, making them attractive to community hospitals that lack specialised IT departments. By 2031, software subscription fees and managed-service retainers together are forecast to out-earn hardware sales by more than 4:1, cementing software’s structural primacy in the AI in oncology market.

By Cancer Type: Brain Tumor Innovation Accelerates Growth

Breast Cancer retained the largest slice of 2025 revenue at 28.05%, buoyed by nationwide mammography programmes and regulatory acceptance of risk-stratification AI such as CLAIRITY BREAST. Yet Brain Tumor solutions are clocking the sector’s fastest CAGR at 36.85%, propelled by real-time surgical guidance algorithms like FastGlioma that identify residual tumour tissue within 10 seconds. Paediatric glioma recurrence models now reach 89% predictive accuracy through spatio-temporal learning, exemplifying the clinical depth of next-gen algorithms. Lung and Prostate Cancer applications are advancing too: the ArteraAI Prostate Test’s guideline inclusion demonstrates how rigorous evidence unlocks reimbursement, and lightweight lung-nodule classifiers make CT screening feasible in mobile clinics.

Collectively, emerging brain, prostate and lung applications will push the AI in oncology market size for under-served tumour groups from less than USD 420 million in 2026 to more than USD 2.45 billion in 2031, giving vendors an incentive to widen disease coverage. Vendors that master small-data techniques, such as CURATE.AI’s single-patient dose-optimisation engine, could secure first-mover advantage in rare malignancies where traditional big-data methods stall.

By Treatment Type: Immunotherapy AI Applications Surge

Radiotherapy dominated 2025 revenue, securing 41.02% of the AI in oncology market size through automated contouring, dose planning and respiratory-motion tracking that together cut planning time from hours to minutes. Yet Immunotherapy-focused AI shows a 35.90% CAGR to 2031 as checkpoint inhibitors and CAR-T treatments demand precise biomarker selection and toxicity forecasting. PERception, for instance, analyses single-cell RNA-seq to predict responses to 44 FDA-approved drugs within minutes, slashing trial screening costs. Chemotherapy and targeted-therapy tools are also evolving: AI-generated molecules entering Phase 1 trials exhibit 80-90% success, double historical norms, suggesting a coming wave of algorithm-designed drugs.

As reimbursement agencies increasingly link payment to biomarker-validated outcomes, software that pinpoints responders will capture a premium. Integration with electronic health records will allow real-time adjustment of dosing schedules, enhancing tolerability and extending progression-free survival.

By Application: Drug Discovery Innovation Drives Expansion

Cancer Detection applications supplied 42.78% of 2025 revenues, reflecting two decades of imaging-AI refinement. Drug Discovery, though, will be the headline growth story, racing at a 37.10% CAGR as hyperscale compute and quantum-accelerated pipelines screen hundreds of millions of molecules against in-silico tumour targets. The Stargate programme’s first USD 100 billion tranche to build AI-optimised data centres signals unprecedented capital commitments to in-silico oncology research. Large-language-model-driven clinical-trial matching already achieves 93.3% protocol-level and 88% patient-level accuracy, hinting at future fully digital trial recruitment that shrinks timelines and costs.

Beyond discovery and development, decision-support dashboards that integrate radiology, lab results and genomics onto a single timeline will shift AI value toward longitudinal patient management. Vendors able to wrap explainable-AI layers around complex recommendations will differentiate as regulators tighten transparency rules.

Geography Analysis

North America held 44.12% of 2025 revenue, underpinned by the world’s most mature approval environment, broad reimbursement of digital pathology and a dense network of AI-first oncology start-ups. The FDA’s rolling guidance updates give US vendors clarity on real-time learning systems, encouraging continuous-update algorithms that improve post-market. Mega-deals such as GE HealthCare’s seven-year pact with Sutter Health to blanket 300 facilities with AI-enabled imaging reinforce a virtuous cycle of clinical data generation and product refinement.

Asia-Pacific is the velocity leader with a 35.10% regional CAGR expected between 2026-2031. South Korea’s national AI-health strategy, China’s Healthy China 2030 plan and Singapore’s secure-data-sandbox regulations collectively speed clinical pilots. Nearly 600 health-AI start-ups now operate across Australia, China, Japan and Singapore, funnelling local datasets into disease-specific models attuned to regional genetics and care protocols. National Taiwan University Hospital’s PANCREASaver underscores how indigenous innovation can secure both domestic deployment and US regulatory recognition.

Europe continues to prioritise cross-border research networks and ethical AI. The €28 million Thera4Care project, running across 29 sites, typifies the continent’s collaborative template that pairs algorithm trials with standard-setting for explainability and data stewardship. While GDPR adds compliance overhead, the unified Medical Device Regulation shortens multinational launch sequencing once CE approval is obtained. Emerging regions—Middle East & Africa and South America—are still nascent but show accelerating interest as cloud connectivity widens. Pilot programmes with the World Health Organization that port ultra-compact lung-cancer detectors onto mobile X-ray vans illustrate the adaptability of contemporary AI stacks to infrastructure-light settings.

Competitive Landscape

Competition is intensifying yet remains moderately fragmented. Siemens Healthineers and GE Healthcare leverage enormous installed bases to embed AI directly into scanners, capturing recurring software revenue while shielding hardware franchises. Siemens has accumulated more than 70 cleared AI solutions trained on 1.4 billion scans, a scale no start-up can match. GE Healthcare couples similar modality depth with Amazon Web Services’ cloud reach, accelerating global roll-outs.

Specialist firms, however, punch above their weight through data advantage and niche focus. Tempus curates multi-omics and clinical outcomes for more than 7 million cancer patients, fuelling risk-stratification models that large pharmas use for trial design. PathAI dominates computational pathology, winning breakthrough status for algorithms that quantify complex biomarkers on whole-slide images. ArteraAI showed that rigorous clinical trials can vault a pure-play AI company straight into NCCN guidelines, setting a new bar for evidence.

Strategically, the sector favours partnerships over outright takeovers. AstraZeneca’s USD 200 million collaboration with Tempus and Pathos AI bundles pharma pipelines, clinical data warehouses and algorithm expertise without diluting equity stakes. Mergers still occur—Recursion’s union with Exscientia created an end-to-end AI-drug-design giant—but deeper integration often happens via shared-risk revenue models rather than acquisitions. Competitive differentiation increasingly revolves around explainability, regulatory fluency and post-market data pipelines rather than raw model accuracy, which is becoming commoditised.

AI in Oncology Industry Leaders

Siemens Healthineers AG

GE Healthcare

IBM Corp.

NVIDIA Corp.

Varian Medical Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Pathos AI raised USD 365 million in Series D financing at a USD 1.6 billion valuation to scale data-driven oncology drug discovery.

- April 2025: Roche secured FDA Breakthrough Device Designation for the VENTANA TROP2 AI-driven companion diagnostic for non-small-cell lung cancer.

- April 2025: AstraZeneca, Tempus AI and Pathos AI announced a USD 200 million collaboration to build multimodal oncology models.

- January 2025: GE HealthCare signed a seven-year agreement with Sutter Health to roll out AI imaging across 300 California facilities.

- June 2025: FDA granted De Novo authorisation to the Clairity Breast platform for five-year breast-cancer risk prediction.

Global AI in Oncology Market Report Scope

Oncology uses artificial intelligence (AI) to diagnose cancer more quickly and accurately, which improves patient outcomes and is expected to fuel market growth over the next five years. AI uses computer programs that examine enormous volumes of data to predict cancer. AI applications in oncology may enhance cancer detection, diagnosis, and therapy planning.

The AI in Oncology market is segmented by Component (Software Solutions, Hardware, and Services), Cancer Type (Breast Cancer, Lung Cancer, Prostate Cancer, Colorectal Cancer, Brain Tumor, and Other Cancer Types), Treatment Type (Chemotherapy, Radiotherapy, Immunotherapy, and Other Treatment Types), Application (Cancer Detection, Drug Discovery, Drug Development, and Other Applications), and Geography (North America (United States, Canada, and Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe) Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, and Rest of Middle East and Africa), and South America (Brazil, Argentina, and Rest of South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Software Solutions |

| Hardware |

| Services |

| Breast Cancer |

| Lung Cancer |

| Prostate Cancer |

| Colorectal Cancer |

| Brain Tumor |

| Other Cancer Types |

| Radiotherapy |

| Chemotherapy |

| Immunotherapy |

| Other Treatment Types |

| Cancer Detection |

| Drug Discovery |

| Drug Development |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Solutions | |

| Hardware | ||

| Services | ||

| By Cancer Type | Breast Cancer | |

| Lung Cancer | ||

| Prostate Cancer | ||

| Colorectal Cancer | ||

| Brain Tumor | ||

| Other Cancer Types | ||

| By Treatment Type | Radiotherapy | |

| Chemotherapy | ||

| Immunotherapy | ||

| Other Treatment Types | ||

| By Application | Cancer Detection | |

| Drug Discovery | ||

| Drug Development | ||

| Other Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the AI in Oncology Market?

The AI in Oncology Market size is USD 2.66 billion in 2026 and is projected to reach USD 11.58 billion by 2031.

Which segment holds the largest AI in Oncology Market share today?

Software Solutions account for 63.78% of 2025 revenue, making it the dominant component category.Software Solutions account for 63.78% of 2025 revenue, making it the dominant component category.

Which application area is growing fastest within the AI in Oncology Market?

Drug Discovery shows the highest forecast growth at a 37.10% CAGR for 2026-2031, driven by heavy investment in AI-enhanced molecule screening.

Which is the fastest growing region in AI in Oncology Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Why is North America the leading region for the AI in Oncology Market?

North America benefits from the largest pool of FDA-cleared AI devices, substantial venture financing and early-adopter health systems that accelerate commercial uptake.

What are the main barriers to wider AI adoption in oncology?

High implementation costs, uncertain return on investment and stringent data-privacy regulations collectively slow deployment, especially in smaller or resource-constrained hospitals.

How are regulators influencing the AI in oncology industry?

The FDA’s expanding list of AI/ML-enabled devices and streamlined breakthrough pathways are shortening approval cycles, while European MDR frameworks harmonise requirements across EU member states.

Page last updated on: