Global Radiology Information Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

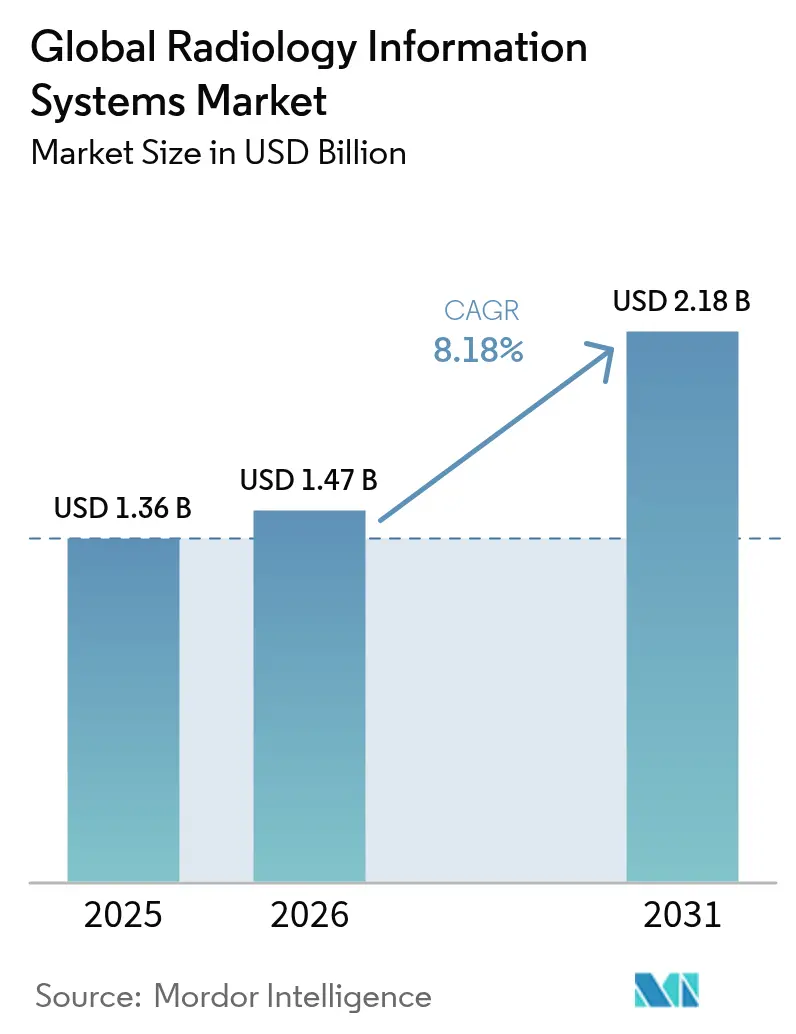

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Radiology Information Systems Market Analysis by Mordor Intelligence

Radiology information system market size in 2026 is estimated at USD 1.47 billion, growing from 2025 value of USD 1.36 billion with 2031 projections showing USD 2.18 billion, growing at 8.18% CAGR over 2026-2031. Growth is fueled by nationwide interoperability mandates, mounting radiologist shortages that amplify workflow pressures, and heightened cybersecurity requirements that encourage cloud-native architectures. Integrated enterprise platforms continue to dominate procurement decisions because they synchronize scheduling, reporting, and billing inside a unified record, yet stand-alone solutions are carving a niche in outpatient imaging and teleradiology networks that prefer modular, pay-as-you-go deployments. Cloud adoption is accelerating as providers seek scalable capacity and lower capital risk, even while many still rely on on-premise installations for data-sovereignty compliance. Vendors that bundle implementation services, AI-enabled analytics, and robust zero-trust security are best placed to win new contracts as hospitals re-platform antiquated infrastructure to meet real-time data-sharing rules.

Key Report Takeaways

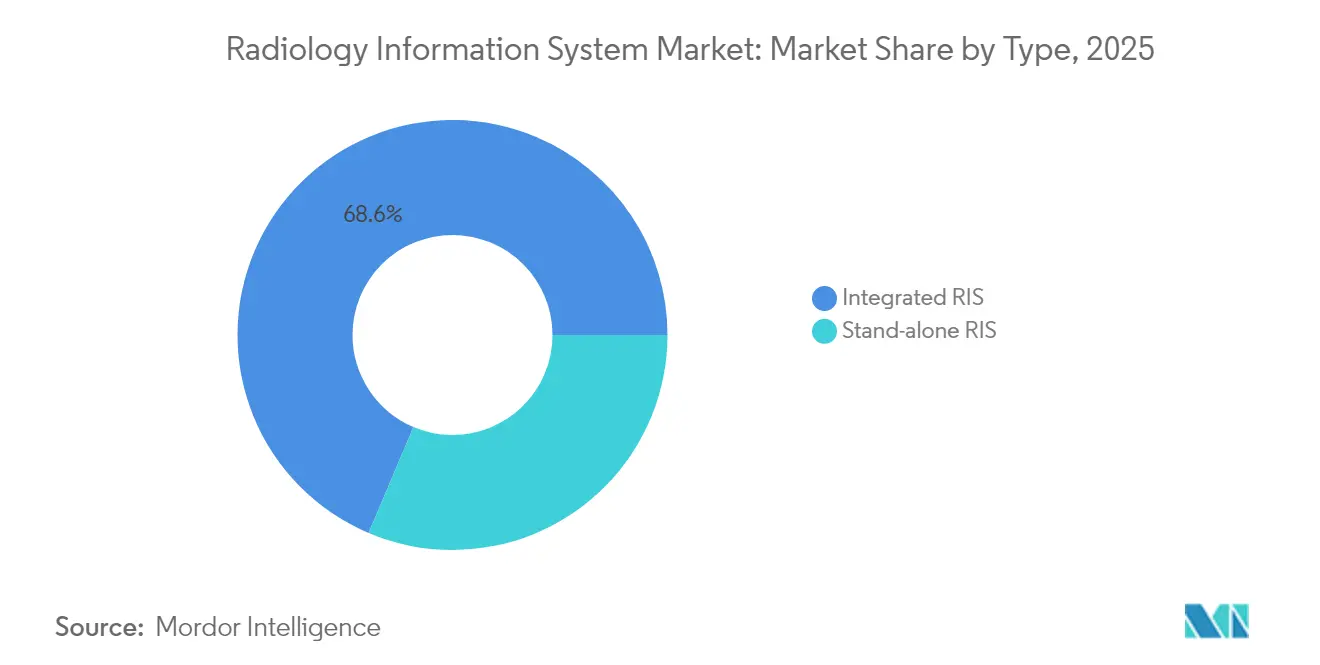

- By type, integrated solutions led with 68.62% of the radiology information system market share in 2025, while stand-alone systems are projected to expand at a 9.21% CAGR through 2031.

- By deployment mode, on-premise deployments held 64.88% share of the radiology information system market size in 2025, and cloud-based options are forecast to grow at 9.34% CAGR to 2031.

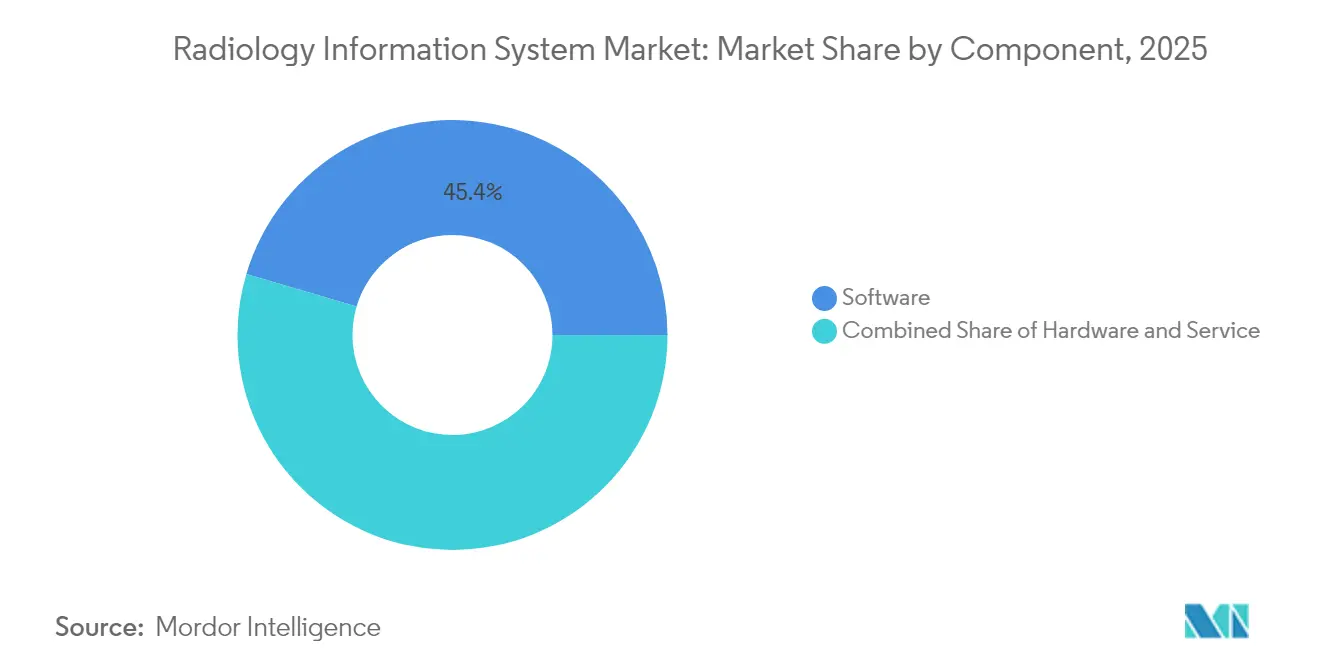

- By component, software captured 45.42% of total 2025 revenue; services will grow the fastest at 9.88% CAGR through 2031.

- By end user, hospitals commanded 72.02% of industry revenue in 2025, while teleradiology providers record the highest projected CAGR at 9.36% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Radiology Information Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global burden of chronic diseases | +2.8% | Global, with highest impact in aging populations of North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Enterprise-wide digitization and tight integration with electronic health record | +2.1% | Global, led by North America and Europe regulatory requirements | Medium term (2-4 years) |

| Emerging interoperability mandates such as the US ONC Information-Blocking Rule and planned EU Health Data Space | +1.9% | North America and EU, with spillover to other regions adopting similar frameworks | Medium term (2-4 years) |

| Value-based-care incentives rewarding radiology throughput | +1.4% | Primarily North America, expanding to Europe and select Asia-Pacific markets | Long term (≥ 4 years) |

| National cancer-screening expansions (e.g., low-dose CT) | +1.2% | Global, with accelerated adoption in developed markets and emerging economies | Medium term (2-4 years) |

| Rise of teleradiology service aggregators in Tier-2/3 hospitals | +0.8% | Global, particularly impactful in rural and underserved regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Burden of Chronic Diseases

Cancer incidence is forecast to climb 42% by 2045, a trend that places sustained pressure on imaging throughput and information management [1]Nature Editorial Team, “Global Cancer Burden Outlook 2025,” Nature, nature.com. Hospitals and outpatient centers are deploying AI-ready RIS environments that catalogue rising study volumes and automate longitudinal follow-up, ensuring clinicians detect subtle disease progression early. The National Cancer Institute’s 2024 launch of a multi-cancer detection screening network covering 24,000 participants emphasizes why scalable data infrastructure is indispensable. Vendors now embed advanced analytics that flag risk cues hidden in prior images, improving personalized surveillance programs that align with value-based reimbursement.

Enterprise-wide Digitization and Tight Integration with Electronic Health Record

Seventy-two percent of health-system executives report tangible workflow gains from digital transformation initiatives that hinge on RIS-EHR convergence. Real-time image, order, and results exchange trims redundant data entry and lowers clerical error rates. Epic Systems grew to 39.1% EHR market share in 2023 and is building over 100 imaging-focused AI features to tighten informatics integration, illustrating how platform leaders create lock-in through seamless radiology modules. RIS suppliers complement these ecosystems with standardized FHIR APIs that preserve vendor differentiation through specialty-specific analytics.

Emerging Interoperability Mandates Such as the US ONC Information-Blocking Rule and Planned EU Health Data Space

The US Health IT Final Rule effective March 2024 requires algorithm transparency and cross-vendor data exchange that directly affects RIS specifications. July 2024 penalties for withholding radiology reports within 24 hours place financial risk on non-compliant providers. Europe’s Health Data Space regulation, adopted January 2025, mandates interoperable electronic health records across all EU states, expanding market opportunity for RIS platforms that meet rigorous privacy safeguards [2]Stella Kyriakides, “European Health Data Space: Empowering Citizens,” European Commission, ec.europa.eu. Vendors that ship robust audit trails and encryption stand to capitalize on multi-country rollouts.

Value-based-care Incentives Rewarding Radiology Throughput

Outcome-oriented payment models reward departments that cut turnaround times without sacrificing accuracy. CMS will require electronic prior authorization checks from 2027, incentivizing automated scheduling and decision support inside RIS workflows. Private imaging networks illustrate the commercial upside: SimonMed Imaging’s USD 40 AI breast-cancer program improved detection by 21% and unlocked premium reimbursement tiers. Providers now request predictive analytics that balance scanner utilization against staffing limits to maximize billable studies per day.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity insurance premiums for imaging data | -1.8% | Global, with highest impact in North America and Europe due to regulatory scrutiny | Short term (≤ 2 years) |

| Large upfront licence fees, workflow re-engineering costs and interface work | -1.2% | Global, particularly affecting smaller healthcare organizations and emerging markets | Medium term (2-4 years) |

| Radiologist staffing shortages limiting system utilisation | -1.0% | Global, with acute impact in North America, Europe, and rural Asia-Pacific regions | Long term (≥ 4 years) |

| Data-sovereignty rules complicating multi-country cloud roll-outs | -0.7% | Global, with highest impact in Europe, China, and regions with strict data localization requirements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Cybersecurity Insurance Premiums for Imaging Data

Eighty-eight percent of providers endure at least one cyberattack yearly, and imaging archives are prized ransomware targets. The 2020 breach at University of Vermont Health Network triggered USD 63 million in losses and 39 days of downtime, highlighting the hidden cost of inadequate security controls. Insurers respond with steep premiums that inflate total cost of ownership. Cloud hyperscalers counter by bundling zero-trust features and managed detection services, yet data-residency rules keep some hospitals tethered to local data centers.

Large Upfront Licence Fees, Workflow Re-engineering Costs and Interface Work

Traditional RIS rollouts require six- or seven-figure licence fees, bespoke HL7 interfaces, and extensive staff retraining that push smaller hospitals to delay modernization. Integration with legacy PACS often demands custom code that extends projects beyond planned timelines. Cloud-native subscriptions ease capital shock, cutting total cost by as much as 30% according to diagnostic-imaging executives. The USD 30 million, seven-year Visage agreement with Duly Health and Care demonstrates predictable opex models that shift spend from CapEx budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Integrated Solutions Drive Market Consolidation

Integrated platforms commanded 68.62% of 2025 revenue, proof that health-systems value a single vendor for registration, scheduling, worklist, and billing. Their economies of scale reduce interface maintenance and centralize governance. Stand-alone solutions grow at 9.21% CAGR because specialty imaging centers and teleradiology networks crave lightweight, cloud-first tools without the overhead of enterprise licensing. Vendor consolidation is accelerating as RIS suppliers embed advanced orchestration to attract enterprise buyers.

Epic Systems added 153 acute hospitals in 2023, while Oracle Health introduced AI-powered prior authorization that trims denials. These moves show that analytics is the new battleground. Nimbler firms counter with modular, API-centric designs that plug into mainstream EHRs, reducing the switching friction that once locked customers into monolithic stacks.

By Deployment Mode: Cloud Migration Accelerates Despite Security Concerns

On-premise installations still dominate at 64.88% because CTOs remain wary of off-site data storage mandates. Yet cloud subscriptions post 9.34% CAGR as CIOs prioritize elastic scaling and outsourced security. Providers spend USD 38 million per year on average for infrastructure contracts but only tap 44% of provisioned capacity, indicating headroom for optimization within the current spend envelope.

The COVID-19 emergency exposed vulnerabilities in fixed data centers when staff shifted to remote reading. Health-systems now hedge with hybrid models that burst excess load to the cloud during peak demand. Strategic alliances such as GE HealthCare with Amazon Web Services and Microsoft’s imaging cloud for Epic accelerate this transition by packaging compliance controls and regional data stores.

By Component: Services Growth Reflects Implementation Complexity

Software represented 45.42% of 2025 billings as facilities upgraded to workflow-centric versions with embedded analytics and natural-language report creation. Services, however, outpace every other line item at 9.88% CAGR. Hospitals hire consultants for gap analysis, change-management coaching, and cybersecurity hardening, underscoring that technology alone cannot guarantee operational gains.

Hardware demand is tapering because virtualization and browser-based workstations reduce the necessity for dedicated radiology consoles. Vendors respond with managed-service bundles that eliminate separate licensing, support, and hosting invoices, streamlining budgeting for finance teams under strain from reimbursement cuts.

By End User: Teleradiology Providers Emerge as Growth Catalyst

Hospitals and multihospital systems absorbed 72.02% of RIS spending in 2025 as they rushed to unify enterprise imaging. Diagnostic imaging centers maintain steady out-patient traction, while ambulatory surgery centers create new demand for micro-PACS connectivity. Teleradiology firms expand the fastest at 9.36% CAGR by filling night-call gaps and offering subspecialty coverage across time zones.

ONRAD’s purchase of Direct Radiology from Philips produced the largest independent US teleradiology entity, proving scale economies matter in remote reading. Persistent radiologist shortages projected through 2055 magnify the need for unified platforms that route studies seamlessly among on-site and remote clinicians without breaking audit trails.

Geography Analysis

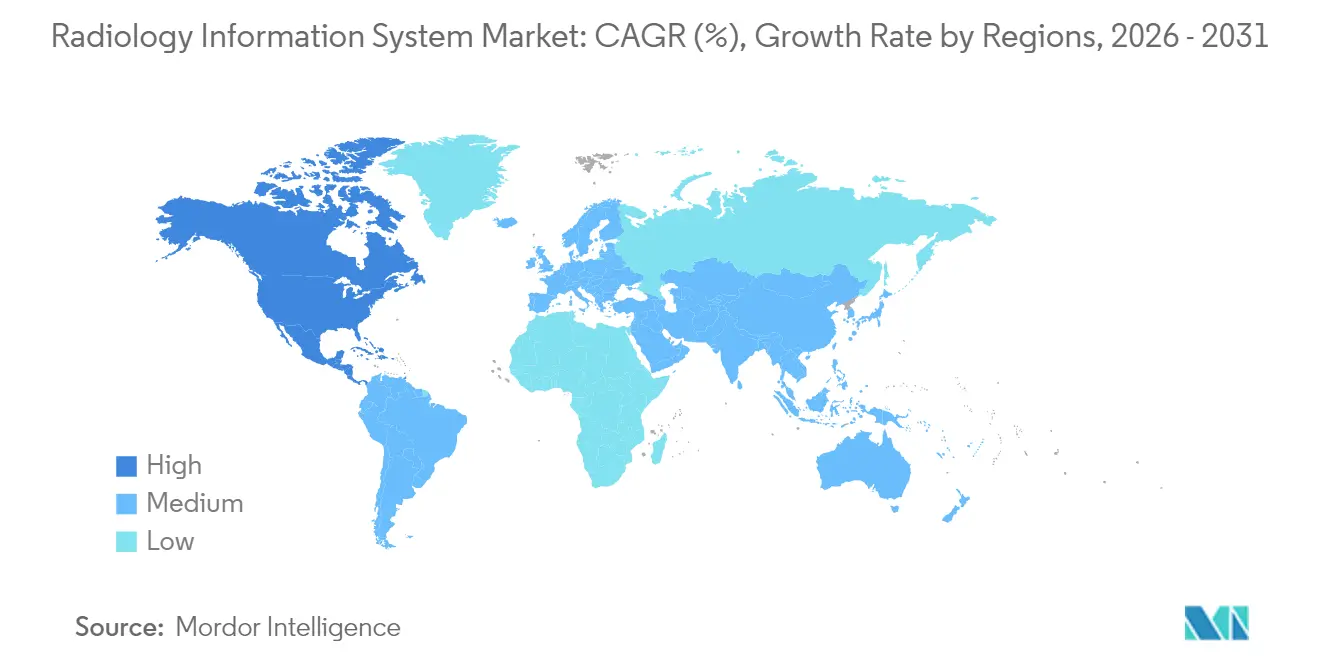

North America delivered 49.11% of 2025 worldwide revenue, buoyed by the 21st Century Cures Act and robust venture funding that bankrolls cloud pilots and AI trials. Sutter Health’s USD 1 billion imaging AI partnership typifies the investment scale. Mandatory 24-hour report release windows, enforced since July 2024, forced hospitals to overhaul legacy RIS queues, supporting incremental license upgrades.

Asia-Pacific is the fastest climber with a 10.01% CAGR. Japan’s DX program sets national quality standards for structured image data, encouraging hospital consortia to migrate to interoperable platforms . China channels large public budgets into provincial cloud data centers, pushing demand for RIS that localize language yet maintain HL7 compatibility. India’s telehealth initiatives, laced with incentive payments for rural diagnostics, stimulate purchases of web-based RIS that adapt to low-bandwidth settings.

Europe’s regulatory landscape transformed in January 2025 when the European Health Data Space regulation took effect. The rule prescribes common data specifications that will be phased in through 2029, giving RIS vendors a defined roadmap for certification. GE HealthCare’s USD 249 million AI imaging deal with Nuffield Health covering 31 UK hospitals signals how providers are future-proofing infrastructure ahead of full EHDS enforcement.

Regulatory Landscape

In the United States, radiology information system (RIS) requirements increasingly align with national health IT interoperability policy. In January 2026, ASTP/ONC issued a Request for Information on diagnostic imaging interoperability standards and potential certification direction, pointing to a tighter link between imaging workflows and the Health IT Certification Program. ONC also advanced its 2026 Standards Version Advancement Process (SVAP), which supports voluntary adoption of newer interoperability standard versions beginning August 2026, reinforcing procurement emphasis on FHIR-aligned APIs and standardized exchange across RIS, EHR, and image-access pathways.

For medical-device-adjacent software functions, suppliers are working through evolving quality and assurance expectations. The FDA finalized guidance on Computer Software Assurance for production and quality system software in September 2025, shaping validation approaches for software used in regulated environments. In Europe, software that qualifies as medical device software remains governed by MDR (2017/745) and IVDR (2017/746), and vendors deploying AI-enabled functionality in imaging workflows must align technical documentation and risk management with EU AI Act requirements where applicable, which increases the focus on auditability, cybersecurity controls, and lifecycle change management across RIS ecosystems.

Value Chain Analysis

The RIS value chain starts with core platform development (workflow, scheduling, reporting, billing, analytics) and integration engineering that links RIS to PACS/VNA and EHR environments using DICOM, HL7, FHIR, and DICOMweb. Upstream inputs include cloud infrastructure and cybersecurity tooling, identity and access management, and developer ecosystems for AI algorithms that plug into clinical workflows. Midstream execution is concentrated in implementation, interface buildout, data migration, validation, and change management, which is visible in rising services demand as providers re-platform legacy environments and add AI-enabled productivity layers.

Downstream monetization is driven by enterprise software licensing, SaaS subscriptions, and managed services sold to hospitals and imaging networks, with channel partners bundling imaging informatics with modality and enterprise platforms. Recent activity points to consolidation and cloud enablement as key value-chain levers: GE HealthCare completed its acquisition of Intelerad in March 2026 to expand enterprise imaging and cloud-first capabilities, while health systems such as Emory Healthcare completed migration to Sectra One Cloud in June 2026, shifting more ongoing value capture to hosting, security, and continuous optimization services. Multi-country deployments and teleradiology networks also raise the need for standardized interoperability and localized compliance, increasing reliance on cloud regions, data-residency controls, and configurable workflow orchestration.

Competitive Landscape

The sector features moderate concentration as the ten largest suppliers account for roughly 55% of global revenue. Epic Systems, Oracle Health, and GE HealthCare leverage vast R&D budgets and installed EHR footprints to cross-sell imaging modules that ride existing interoperability gateways. Siemens Healthineers, Sectra, and INFINITT Healthcare compete on subspecialty workflow, embedded analytics, and high-availability cloud architectures.

Strategic alliances are replacing pure acquisitions. GE HealthCare partnered with RadNet to co-develop SmartTechnology solutions that fuse AI scheduling with patient-specific imaging protocols. Amazon’s investment in Aidoc’s multimodal foundation model exemplifies hyperscaler interest in domain-specific AI that accelerates large-language-model accuracy for radiology use cases. Private equity groups such as WindRose Health Investors aggregated RIS and PACS assets under Collaborative Imaging to build scale in managed-services contracts and strengthen negotiation power against large health-systems.

Emerging contenders focus on zero-trust cybersecurity, predicting ransomware risk scoring per study and offering hold-harmless indemnity. Others target low-cost, browser-only RIS aimed at ambulatory surgery centers that operate with thin IT teams. Competitive differentiation now hinges on balancing rapid cloud deployment, bulletproof compliance, and AI-powered productivity without escalating operating expenses.

Global Radiology Information Systems Industry Leaders

Allscripts Healthcare Solutions Inc.

Cerner Corporation

IBM (Merge Healthcare Incorporated)

Koninklijke Philips N.V.

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Radiology departments are modernizing reporting and workflow layers around the RIS to address radiologist workload pressure and turnaround-time requirements. One near-term whitespace is AI-assisted reporting that integrates with existing dictation and RIS workflows without requiring full platform replacement: HOPPR launched Presto in June 2026 to generate AI draft reporting within established reporting environments, and DeepHealth launched Reporting Pro in June 2026 with automated reporting, speech recognition, and structured reporting in the United States and United Kingdom. These launches expand the buyer pool beyond large enterprise replacements to include add-on productivity deployments for outpatient imaging and teleradiology networks that want modular adoption.

Interoperability compliance and certification readiness also support a defined opportunity for vendors with standards-forward architectures and audit-ready data exchange. ASTP/ONC’s January 2026 RFI on diagnostic imaging interoperability standards, together with ONC’s 2026 SVAP pathway for adopting updated standards starting August 2026, increases the commercial value of RIS platforms that ship FHIR-native interfaces and can participate cleanly in cross-vendor data sharing. Alongside this, FDA clearance activity tied to enterprise imaging functionality, including CliniComp’s July 2026 510(k) clearance for a PACS Viewer (MIMPS) embedded within its EHR environment, reflects provider demand for tighter clinical integration, pulling RIS vendors toward deeper workflow and reporting integration with enterprise EHRs and image-access tooling.

Recent Industry Developments

- July 2026: CliniComp announced FDA 510(k) clearance of its PACS Viewer as a Medical Image Management and Processing System (MIMPS), enabling diagnostic image viewing within its EHR environment with native AI integration options. The clearance supports provider efforts to reduce workflow fragmentation between imaging review and the longitudinal patient record, reinforcing market momentum toward integrated enterprise imaging stacks that connect RIS-adjacent workflows with EHR-native experiences.

- June 2026: Philips and WellSpan Health announced a long-term AI-driven innovation alliance, naming Philips as the preferred vendor for imaging modalities across WellSpan hospitals and centers. The partnership structure indicates a continued shift from one-time procurement to multi-year lifecycle and innovation programs, which elevates the importance of interoperable informatics layers (including RIS and reporting workflows) that can scale across a health system footprint.

- July 2024: DeepHealth, a RadNet subsidiary, opened an office in Bengaluru to expand its technology and market presence in India. The move adds product-development and deployment capacity closer to fast-growing Asia-Pacific buyer segments, where web-based and cloud-first RIS and reporting workflows are adopted to support distributed reading and multi-site imaging operations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues earned from radiology information systems (RIS) used to run radiology operations, including patient scheduling, worklist and workflow steps, reporting, basic analytics, and billing-related tasks within imaging departments.

Scope exclusions: We exclude RIS-related hardware and any wider hospital IT bundles where RIS is not priced separately.

Segmentation Overview

- By Type

- Integrated RIS

- Stand-alone RIS

- By Deployment Mode

- On-premise

- Cloud-based / Web-hosted

- By Component

- Hardware

- Software

- Services

- By End User

- Hospitals & Health Systems

- Diagnostic Imaging Centers

- Ambulatory Surgical Centers

- Teleradiology Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with setting the market boundary and collecting consistent reference indicators that can be tracked year to year for radiology workflow adoption. We rely on public healthcare and digital health statistics, along with imaging utilization signals, so the demand pool is grounded in observable service volumes and provider activity.

Common inputs include sources such as the World Health Organization, OECD Health Statistics, US CDC health data, CMS utilization and payment files, and national radiology or hospital association publications, along with peer-reviewed articles on radiology workflow and informatics adoption. We also review company annual reports, investor presentations, product brochures, and reputable press to understand packaging models (license, subscription, and services). Where needed, we use paid subscriptions for company financials and intelligence, a patent database, and tender tracking to cross-check vendor activity and contract patterns. These examples are not exhaustive, and other public sources were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what we see in public data, especially around how RIS is sold, what is counted as RIS versus adjacent imaging IT, and how pricing changes with cloud migration. We speak with a mix of hospital imaging leaders, radiology administrators, IT implementers, and supplier-side roles across APAC, EMEA, and the Americas, and then we correct assumptions when field feedback consistently points to a different reality.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 39% |

| Mid tier: 44% | Functional/Unit leaders: 27% | EMEA: 37% |

| Smaller Players: 17% | Managers: 59% | Americas: 24% |

Market-Sizing & Forecasting

The sizing model is built using a top-down approach, where imaging procedure volumes, facility counts, and IT spending signals are used to reconstruct the addressable RIS demand pool by region, then converted into revenues using realistic adoption and pricing assumptions. We corroborate the result with selective bottom-up approximations, including sampled contract values, a supplier revenue roll-up for the most visible vendors, and channel checks on typical implementation and support attachments. These cross-checks are then used to adjust totals when gaps show up.

Key inputs include imaging exam growth (CT, MRI, X-ray, and ultrasound as proxies for workflow load), the share of imaging sites running digital scheduling and reporting tools, cloud versus on-premises deployment mix, average annual software subscription or license levels by facility type, and implementation plus support intensity by renewal cycle. When vendor revenues are not disclosed, we fill the gap through proxy pricing bands shared by interviewees and by mapping the likely customer base using facility and procedure indicators. Forecasts are developed using scenario analysis supported by short trend lines on procedure growth, cloud adoption, and healthcare IT budget direction, and then aligned to what experts expect to change in buying cycles and replacement timing.

Data Validation & Update Cycle

Validation is done in layers so that a single assumption does not drive the final number. We cross-check totals against independent signals, such as imaging utilization trends, provider digitization benchmarks, and observed contract activity, then investigate outliers that do not match regional realities.

Before sign-off, the model goes through multi-step analyst reviews, with re-contact triggers when an input shifts materially, or when a new regulation, reimbursement change, or major deployment wave is seen in the market. The report is refreshed annually, with interim updates when material events occur. Right before delivery, a fresh data pass is completed so clients receive the latest updated view.

Mordor Intelligence's Radiology Information Systems Market Estimate Compared With Other Published Estimates

Published RIS market numbers often differ because firms do not count the same revenue items, they use different base years, and they handle deployment shifts and pricing changes over time using different methods. Differences also come from whether implementation and support are treated as part of RIS revenue, and how tightly the definition stays within RIS versus broader imaging IT.

The benchmark table shows a spread that mainly comes from scope and packaging choices, plus how each publisher treats bundled deals and conversion timing. In Mordor Intelligence's model, RIS revenue includes software licenses or subscriptions, plus directly linked implementation and support. It excludes hardware and any all-in hospital IT bundles where RIS is not priced as a separate line item, which can pull some larger enterprise contracts out of the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.47 B (2026) | |

| Global Research Publisher A | USD 1.19 B (2025) | Uses an earlier base year and does not clearly separate stand-alone RIS revenue from nearby imaging IT modules in every region, which can shift what is treated as core RIS versus adjacent software. |

| Industry Portal B | USD 1.40 B (2024) | Anchors the estimate on a 2024 base and appears to apply a broader product view that can mix deployment and end-user splits without consistently clarifying whether services and bundled enterprise agreements are counted the same way. |

Taken together, the comparison shows that the largest swings are usually caused by what is counted as priced RIS software and services, and by the year used to anchor the model. By keeping the inputs tied to imaging workload signals, adoption levels, and realistic pricing progression, our estimate stays traceable to a clear demand pool and repeatable steps.

Key Questions Answered in the Report

How big is the Global Radiology Information Systems Market?

The Global Radiology Information Systems Market size is expected to reach USD 1.47 billion in 2026 and grow at a CAGR of 8.18% to reach USD 2.18 billion by 2031.

Which solution segment currently commands the largest market share?

Integrated radiology information systems lead with 68.62% global revenue share in 2025, reflecting hospital demand for end-to-end workflow platforms.

Who are the main competitors in the radiology information system landscape?

Key vendors include Epic Systems, Oracle Health, GE HealthCare, Siemens Healthineers, Sectra, INFINITT Healthcare, and a cohort of focused teleradiology and cloud-native specialists that supply modular, API-driven solutions.

Which is the fastest growing region in Global Radiology Information Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Radiology Information Systems Market?

In 2025, the North America accounts for the largest market share in Global Radiology Information Systems Market.

Why are healthcare providers increasingly adopting cloud-based RIS deployments?

Cloud subscriptions offer scalable capacity, lower upfront capital outlay, embedded cybersecurity safeguards, and easier disaster-recovery options—all critical as imaging volumes rise and data-sharing mandates tighten.

Page last updated on: