AI In Precision Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

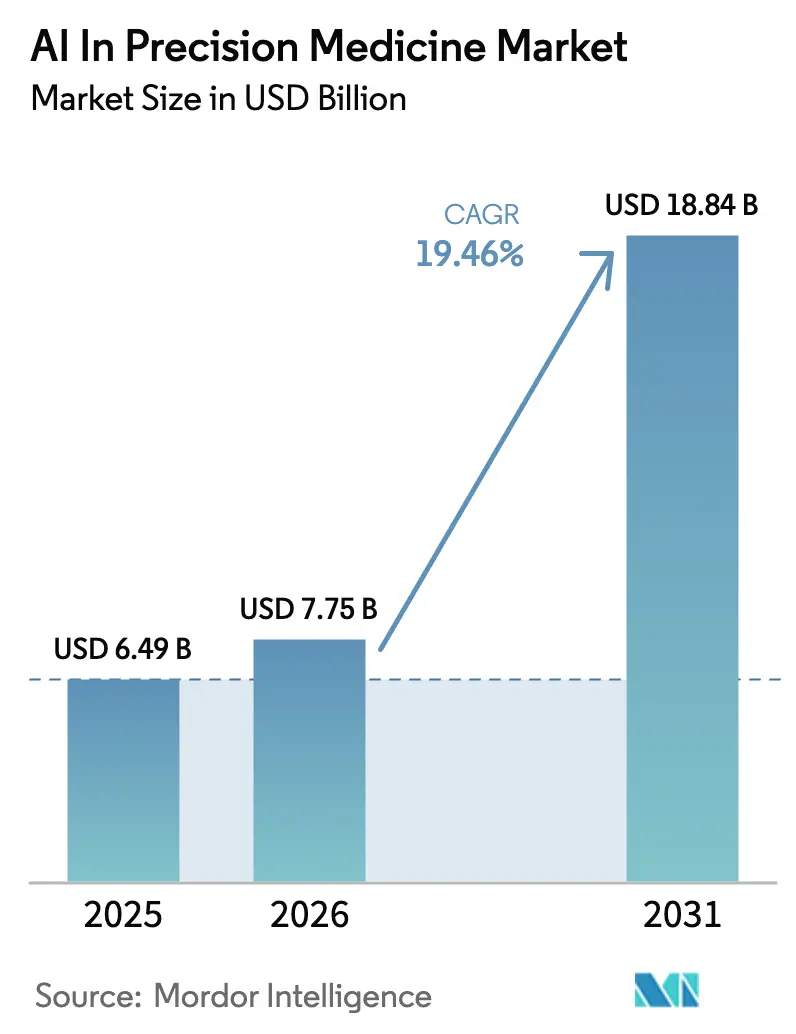

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 18.84 Billion |

| Growth Rate (2026 - 2031) | 19.46% CAGR |

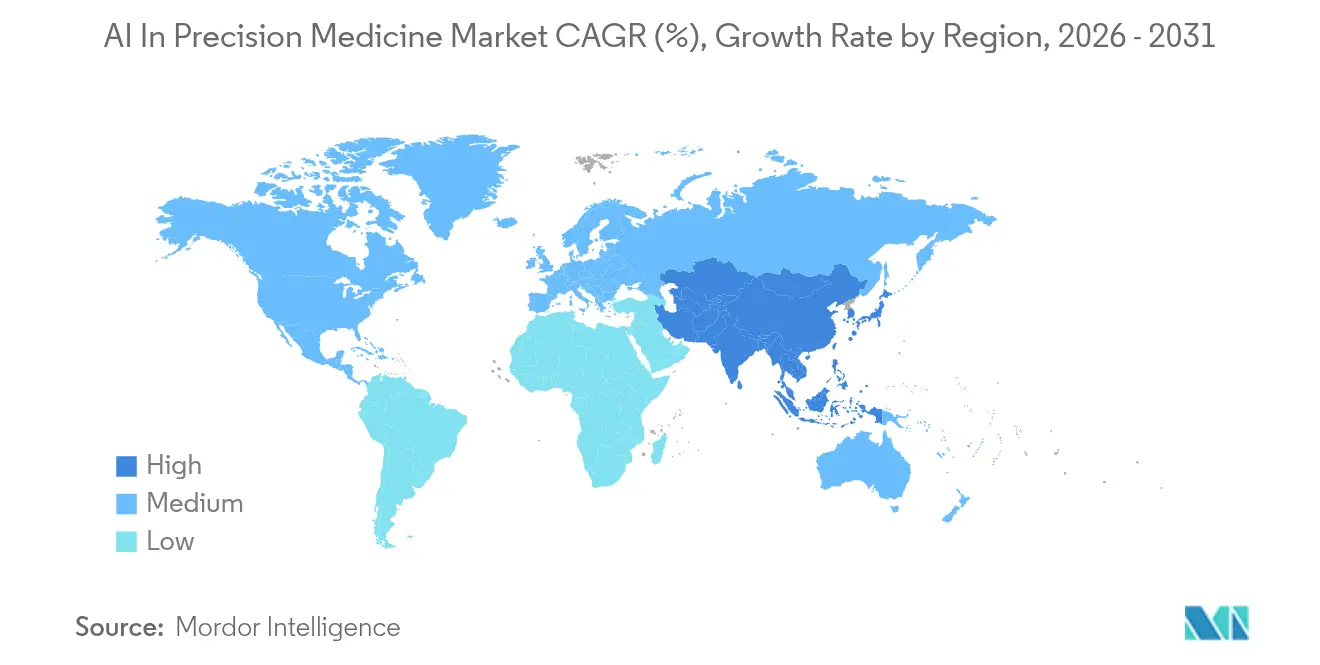

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

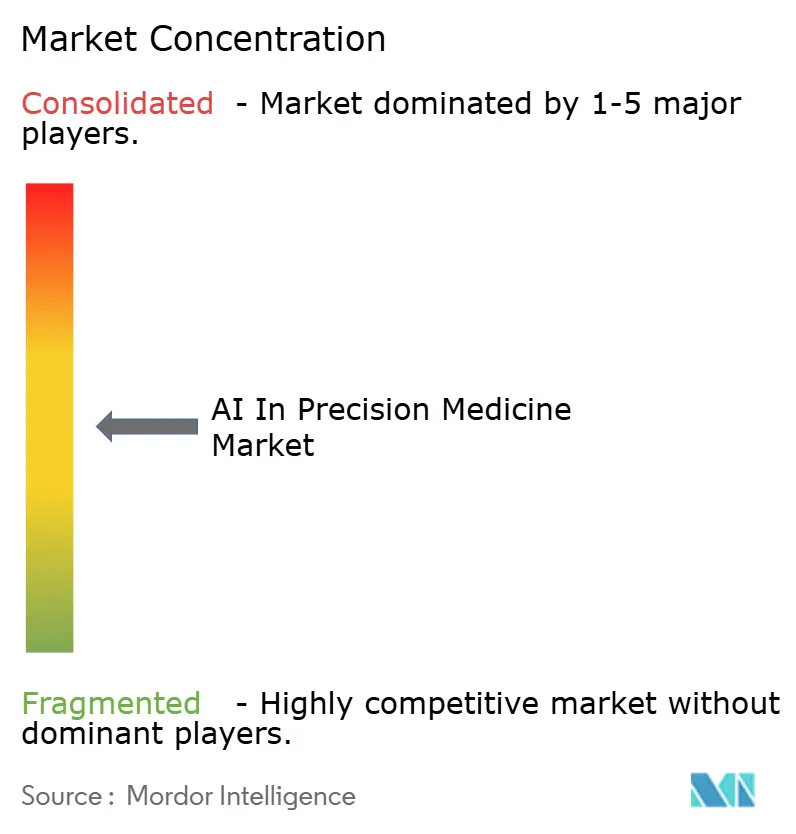

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Precision Medicine Market Analysis by Mordor Intelligence

The AI in precision medicine market size was valued at USD 6.49 billion in 2025 and estimated to grow from USD 7.75 billion in 2026 to reach USD 18.84 billion by 2031, at a CAGR of 19.46% during the forecast period (2026-2031). This trajectory reflects a decisive pivot toward data-driven personalization that places artificial intelligence at the heart of genomic interpretation, clinical decision support, and targeted therapeutics. Converging trends—including large-scale genomic sequencing programs, mandated electronic health records, and a rising chronic disease burden—create fertile ground for AI engines that tailor treatment plans instead of relying on standardized protocols. Market participants respond by accelerating algorithm development, cementing partnerships with pharmaceutical companies, and investing in cloud-native platforms that compress discovery timelines. Competitive intensity grows as global regulators establish clearer pathways for AI validation, reinforcing commercial confidence and drawing sustained venture capital flows into the AI in precision medicine market.

Key Report Takeaways

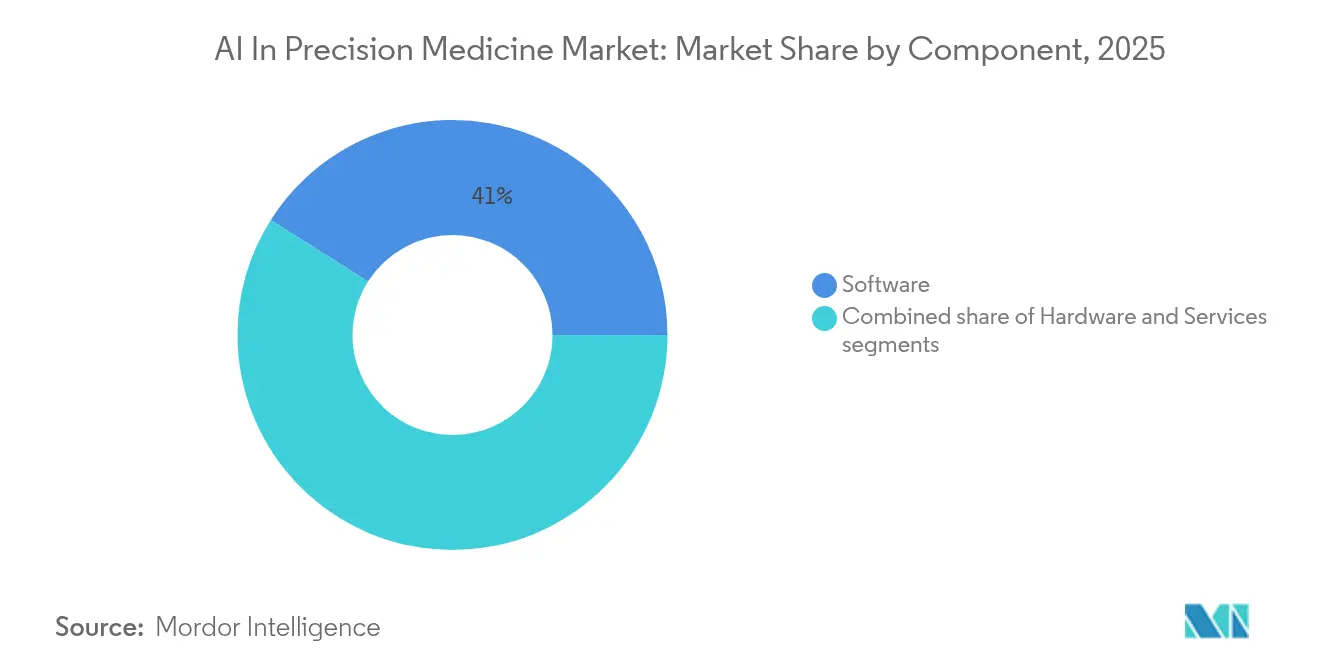

- By component, software retained 41.02% revenue share in 2025; services are projected to record the fastest 21.95% CAGR through 2031.

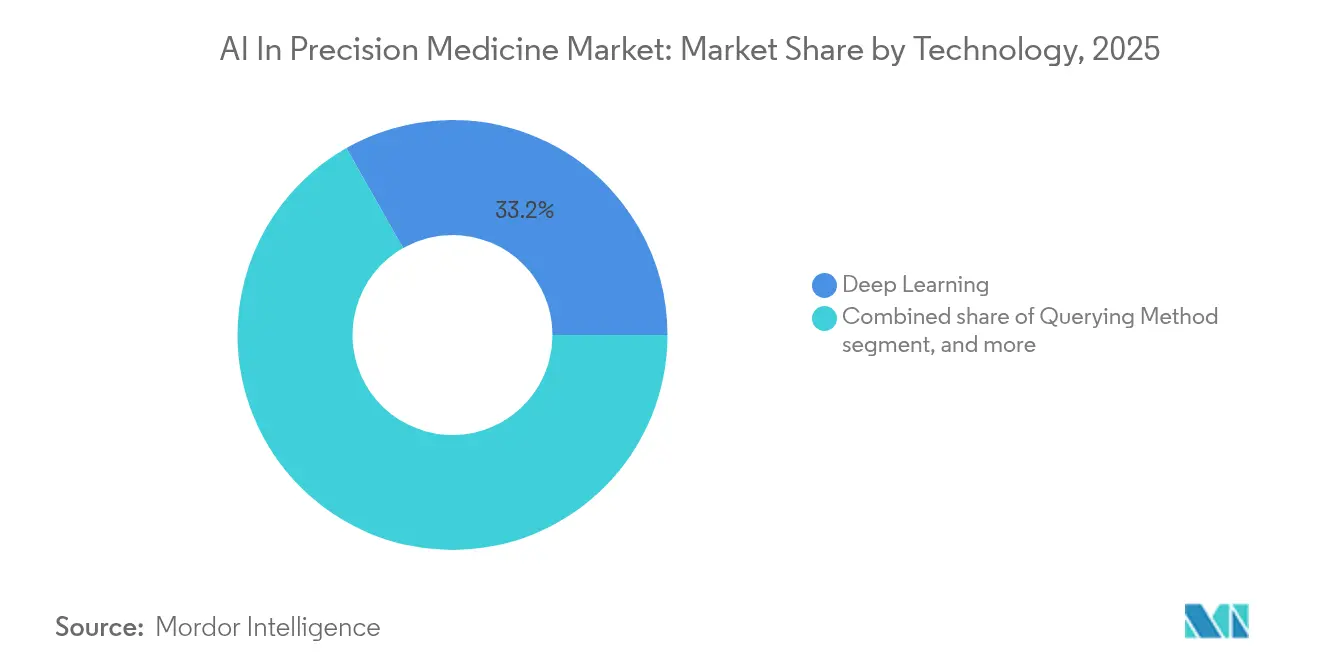

- By technology, deep learning led with 33.22% of AI in precision medicine market share in 2025, whereas natural language processing is set to expand at 21.90% CAGR by 2031.

- By therapeutic application, oncology captured 30.88% of the AI in precision medicine market size in 2025, while respiratory applications will advance at a 22.60% CAGR over the forecast period.

- By geography, North America accounted for 42.05% revenue share in 2025; Asia-Pacific is forecast to grow at 20.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of AI In Precision Medicine Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding genomic sequencing adoption | +3.5% | Global; North America & EU leading | Medium term (2-4 years) |

| Increasing healthcare data digitization | +2.1% | Global; acceleration in Asia-Pacific | Short term (≤2 years) |

| Rising prevalence of chronic diseases | +1.8% | Global; concentrated in aging populations | Long term (≥4 years) |

| Growing government funding initiatives | +1.2% | North America, EU, China, Japan | Medium term (2-4 years) |

| Advancements in cloud computing infrastructure | +0.9% | Global; enterprise-centric | Short term (≤2 years) |

| Strategic collaborations among stakeholders | +0.6% | Global; pharma-tech convergence zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Genomic Sequencing Adoption

Population-scale sequencing programs drive a surge of raw omics data that only advanced AI models can translate into actionable insights. Sequencing costs now sit below USD 1,000 per genome, enabling projects such as NIH’s Bridge2AI, which funds AI-ready data sets across diverse populations through 2025[1]National Institutes of Health, “Bridge2AI Program Overview,” nih.gov. As multi-omic integration becomes standard, healthcare systems rely on deep learning architectures to resolve complex biological networks and predict patient-specific responses—elevating the AI in precision medicine market as a linchpin of clinical genomics.

Increasing Healthcare Data Digitization

Mandated electronic health record rollouts under the EU Digital Health Strategy and China’s national health informatization plan accelerate structured data availability that fuels algorithm training[2]Advanced Research Projects Agency-H, “ARPA-H Precision Programs,” arpa-h.gov. Harmonized interfaces such as FHIR let AI engines ingest real-time vitals, imaging, and lab results across institutions, reinforcing clinical decision support accuracy. This digital infrastructure underpins rapid adoption across payers and providers seeking seamless precision workflows.

Rising Prevalence of Chronic Diseases

Chronic conditions now affect more than 60% of adults and impose USD 47 trillion in economic losses through 2030, intensifying demand for individualized therapies[3]National Institute of Diabetes and Digestive and Kidney Diseases, “Global Impact of Chronic Disease,” niddk.nih.gov. Diabetes, cardiovascular disease, and COPD manifest heterogeneous pathways that AI platforms can map to optimal drug regimens, bolstering the value proposition of the AI in precision medicine market. Value-based reimbursement models further reward early detection and tailored interventions.

Growing Government Funding Initiatives

The United States earmarked USD 3.3 billion for AI R&D in fiscal 2025, with ARPA-H’s PRECISE-AI program focusing on model robustness in clinical settings. Similar commitments across Europe and Asia fund infrastructure, workforce training, and regulatory science, creating fertile policy environments that accelerate commercial scaling of precision platforms.

Restraints Impact Analysis of AI In Precision Medicine Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and maintenance costs | −1.4% | Global; most acute in emerging markets | Short term (≤2 years) |

| Data privacy and security concerns | −0.8% | Global; stringent in EU & California | Medium term (2-4 years) |

| Limited skilled workforce availability | −0.7% | Global; pronounced in developing regions | Medium term (2-4 years) |

| Regulatory and ethical uncertainties | −0.5% | Global; heightened where AI rules are evolving | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Maintenance Costs

Enterprise-grade deployments often exceed USD 10 million, covering specialized compute, cloud storage for petabyte-scale genomic data, and long-term model retraining. These outlays consume up to 20% of large hospital IT budgets, while smaller providers struggle to justify returns, slowing penetration in cost-sensitive segments.

Data Privacy and Security Concerns

Regulations like GDPR impose strict consent and processing conditions. Breach penalties surpass USD 20 million, prompting cautious data-sharing behavior that can limit multi-site training cohorts. Techniques such as federated learning and differential privacy mitigate risk, yet add computational overhead that can temper performance gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

AI In Precision Medicine Market Segment Analysis

By Technology:

Deep Learning Dominates Advanced AnalyticsDeep learning held 33.22% share of AI in precision medicine market size in 2025 and remains foundational for decoding non-linear genomic patterns. AstraZeneca’s MILTON model, trained on 500,000 UK Biobank genomes, predicts over 1,000 diseases pre-diagnosis, validating deep learning’s clinical impact. Natural language processing grows at 21.90% CAGR, extracting insights from unstructured notes that constitute 80% of medical data. Large language models paired with biomedical knowledge graphs empower clinicians to interrogate patient histories conversationally. Emerging multimodal systems blend imaging, genomics, and EHR text, foreshadowing the next performance leap for the AI in precision medicine market.

Complementary techniques such as knowledge-based querying support specialty tasks like drug–gene interaction alerts. Their integration into mainstream platforms expands the AI in precision medicine industry toolkit without diluting deep learning’s central role.

By Component:

Software Leadership Drives Platform InnovationSoftware accounted for 41.02% revenue in 2025, reflecting rapid iterative cycles and cloud-first deployments that sidestep hardware refresh constraints. Scalable codebases allow vendors to push frequent model upgrades, protecting customers against algorithmic obsolescence and reinforcing subscription economics in the AI in precision medicine market. Services exhibit the strongest 21.95% CAGR, mirroring hospitals’ need for integration, compliance, and model validation expertise. Hardware remains essential for training acceleration but shifts off-premises as hyperscale data centers democratize GPU access, lowering capital barriers for mid-tier health systems.

By Therapeutic Application:

Oncology Scale Meets Respiratory InnovationOncology retained 30.88% share of the AI in precision medicine market in 2025, buoyed by established biomarker panels and targeted therapy paradigms. AI models optimize drug combinations and predict tumor evolution, sharpening response rates and minimizing toxicity. Respiratory use cases register a 22.60% CAGR, harnessing AI to parse spirometry, imaging, and wearable data for COPD and asthma management. Breakthroughs in cardiology and neurology follow closely as algorithms identify arrhythmic patterns or detect prodromal neurodegeneration. Rare-disease pipelines also benefit; ARPA-H’s MATRIX repurposing project mines molecular descriptors to match orphan conditions with existing compounds.

Geography Analysis

North America AI In Precision Medicine Market

North America, holding 42.05% of AI in precision medicine market share in 2025, leverages NIH grants, FDA’s AI device clearances, and a dense concentration of biotech hubs to sustain leadership. Flagship health networks such as Mayo Clinic integrate AI genomics into routine oncology boards, accelerating clinical validation cycles. Multiplier effects arise from proximity to cloud titans and semiconductor suppliers, reinforcing supply-chain resilience.

APAC AI In Precision Medicine Market

Asia-Pacific generates the fastest 20.85% CAGR. China’s national sequencing pushes, Japan’s super-aged demographics, and India’s digital health mission cultivate vast data lakes and pilot sites for algorithm tuning. Cross-border alliances give Western developers access to heterogeneous genomic signatures, enriching training diversity and boosting model robustness for the AI in precision medicine market.

Europe, GCC and Singapore AI In Precision Medicine Market

Europe contends with GDPR-driven complexity yet benefits from Horizon Europe grants and EMA adaptive pathways. Compliance frameworks differentiate European vendors by showcasing responsible AI. Elsewhere, the Gulf states and Singapore deploy sovereign wealth to modernize tertiary centers, signaling nascent opportunities despite workforce shortages.

Competitive Landscape

The AI in precision medicine market exhibits moderate fragmentation. NVIDIA controls roughly 78% of AI infrastructure GPUs, underpinning most hospital compute clusters. Cloud incumbents Google and Microsoft bundle analytics suites with managed compliance, widening barriers to smaller rivals. Specialist companies such as Tempus AI, armed with the world’s largest clinico-genomic library, monetize insights through SaaS and companion diagnostics. IPO proceeds of USD 410.7 million in 2024 funded expansion into multimodal generative AI.

Strategic alliances dominate as pharmaceutical firms trade compound libraries for algorithm expertise. Sanofi partnered with Formation Bio and OpenAI to streamline target discovery; Eli Lilly collaborates with OpenAI to deploy large language models across R&D. New entrants like Xaira Therapeutics, flush with USD 1 billion in Series A capital, aim to imbue discovery workflows with AI-native architectures. Success hinges on demonstrating regulatory clearance and real-world efficacy, pushing contenders to amass prospective data and publish peer-reviewed evidence.

Mid-tier innovators including Qure.ai in medical imaging and PathAI in digital pathology concentrate on niche workflows that plug directly into hospital systems. Owkin applies federated learning across European cancer centers, safeguarding patient privacy while enriching algorithm training data. These specialists monetize modular models that integrate with existing electronic health records, enabling hospitals to gain precision capabilities without full-stack replacements. Growing pressure for validated real-world evidence is prompting large pharmaceutical and cloud vendors to target such firms for tuck-in acquisitions. As consolidation accelerates, competitive standing will depend on data depth, cloud economics, and the speed at which companies secure regulatory approvals.

AI In Precision Medicine Industry Leaders

IBM Corp.

Google (Alphabet incl. DeepMind)

NVIDIA Corporation

Tempus AI

Illumina Inc.

- *Disclaimer: Major Players sorted in no particular order

AI In Precision Medicine Market Companies Covered in this Report

- NVIDIA

- Google (Alphabet incl. DeepMind)

- Tempus AI

- AstraZeneca

- BioXcel Therapeutics

- Flatiron Health

- Enlitic Inc.

- Qure.ai

- IBM Corp.

- Intel Corp.

- Illumina

- Sanofi

- Exscientia PLC

- DeepMind (Alphabet)

- Valar Labs

- Owkin

- Microsoft

- Amazon AWS Health

- Foundation Medicine

- Roche Holding

- PathAI

- Zephyr AI

- PictureHealth

- Tempus Labs

Recent Industry Developments in AI In Precision Medicine Market

- January 2025: Tempus AI introduced generative AI in Tempus One to interrogate millions of unstructured documents, elevating clinical query speed.

- January 2025: Danaher Corporation invested in Innovaccer to expand AI-enabled diagnostics and population-health analytics.

- September 2024: AstraZeneca revealed MILTON, a model predicting 1,000+ diseases before onset using UK Biobank genomes.

- August 2024: ARPA-H launched PRECISE-AI to autonomously detect model drift in clinical practice.

- June 2024: Tempus AI raised USD 410.7 million in an IPO, valuing the company at USD 6.1 billion.

Global AI In Precision Medicine Market Report Scope

As per the scope of the report, precision medicine designs and optimizes the pathway for diagnosis, therapeutic intervention, and prognosis by using large multidimensional biological datasets that capture individual variability in gene function and environment. These datasets can be analyzed by artificial intelligence to predict risk in various diseases for tailored treatment plans.

The AI in precision medicine market is segmented by technology, components, therapeutic applications, and geography. By technology, the market is segmented into deep learning, querying methods, natural language processing, and context-aware processing. By component, the market is segmented into hardware, software, and services. By therapeutic application, the market is segmented into oncology, cardiology, neurology, respiratory, and others (ophthalmology and dentistry). By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

Segmentation Overview

| Deep Learning |

| Querying Method |

| Natural Language Processing |

| Context-Aware Processing |

| Hardware |

| Software |

| Service |

| Oncology |

| Cardiology |

| Neurology |

| Respiratory |

| Other Therapeutic Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Deep Learning | |

| Querying Method | ||

| Natural Language Processing | ||

| Context-Aware Processing | ||

| By Component | Hardware | |

| Software | ||

| Service | ||

| By Therapeutic Application | Oncology | |

| Cardiology | ||

| Neurology | ||

| Respiratory | ||

| Other Therapeutic Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the AI in precision medicine market?

The market is valued at USD 7.75 billion in 2026 and is projected to reach USD 18.84 billion by 2031 at a 19.46% CAGR.

Which component leads the market?

Software leads with 41.02% revenue share, underscoring the centrality of algorithms and data platforms.

Which geographic region is growing fastest?

Asia-Pacific is expanding at a 20.85% CAGR, driven by large-scale government digitization and genomic initiatives.

What therapeutic area commands the largest share?

Oncology dominates with 30.88% of AI in precision medicine market size, reflecting mature biomarker infrastructure.

How do data privacy regulations impact adoption?

Strict rules such as GDPR increase compliance costs and necessitate privacy-preserving techniques, slightly dampening CAGR growth by 0.8%.

Page last updated on: