Artificial Intelligence In Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 9.32 Billion |

| Growth Rate (2026 - 2031) | 31.88% CAGR |

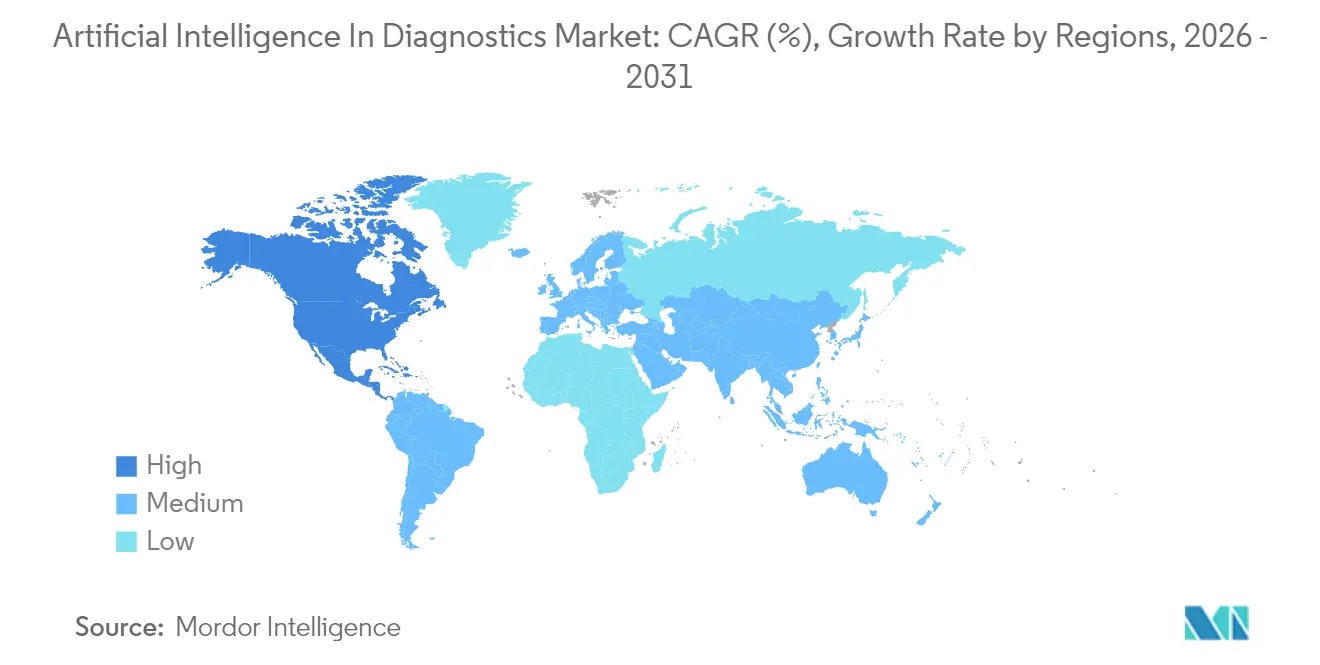

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

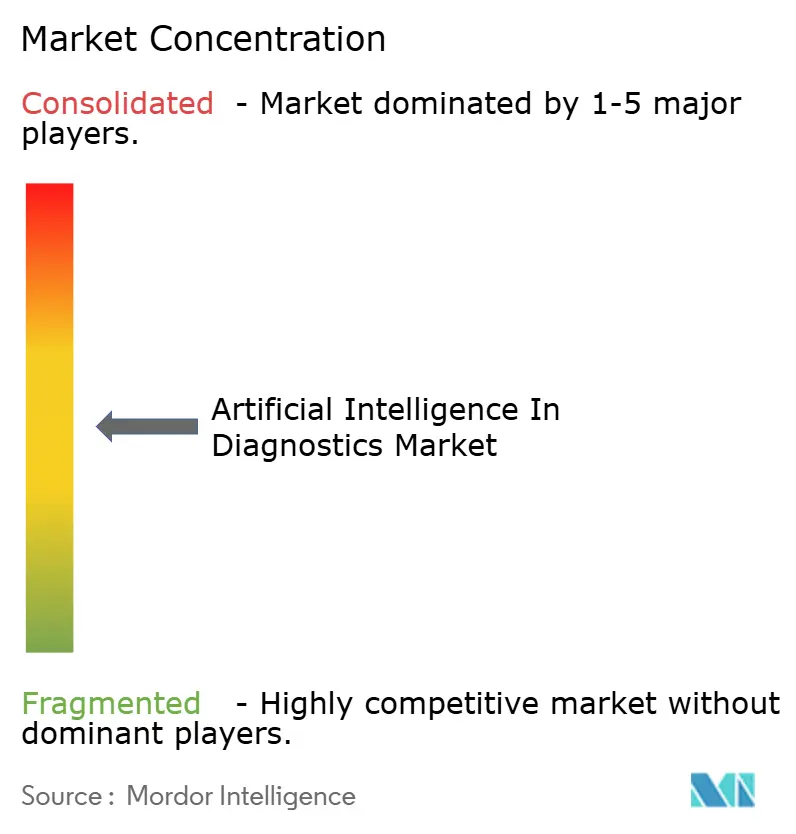

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence In Diagnostics Market Analysis by Mordor Intelligence

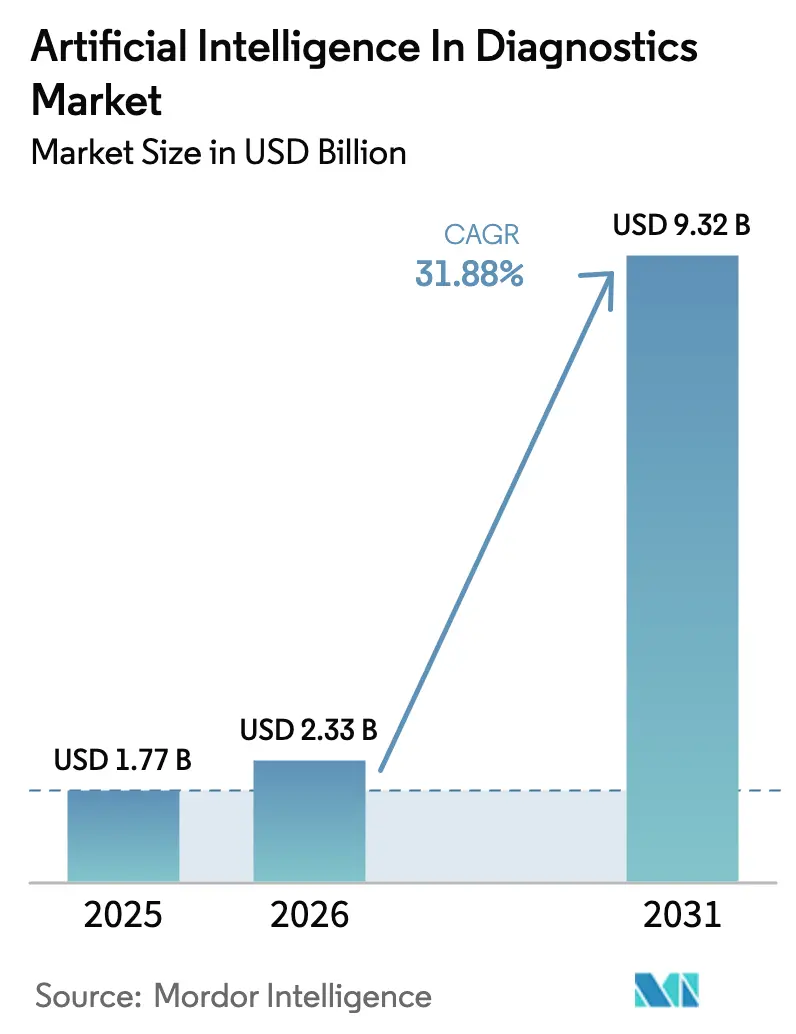

The Artificial Intelligence in Diagnostics market size was valued at USD 1.77 billion in 2025 and estimated to grow from USD 2.33 billion in 2026 to reach USD 9.32 billion by 2031, at a CAGR of 31.88% during the forecast period (2026-2031). Expansion rests on three intertwined factors: maturing regulation, the arrival of dedicated reimbursement codes, and accelerating algorithmic performance gains. In January 2025 the FDA issued comprehensive draft guidance for AI-enabled medical devices, clarifying clinical study design and post-market monitoring expectations. At nearly the same time, the Centers for Medicare & Medicaid Services (CMS) finalized the first permanent payment codes for stand-alone AI algorithms used in radiology, transforming once-pilot deployments into billable clinical services. Venture funding floods the field; a sample of 2024–2025 deals shows Imagen Technologies, AZmed and ThinkSono raising a combined USD 50 million for expansion and regulatory submissions. Meanwhile, technology leaders such as GE HealthCare and Siemens Healthineers are embedding NVIDIA’s MONAI Deploy toolkit in their scanners, shortening the path between model development and bedside deployment. Hospitals adopt these tools to counter rising imaging volumes and radiologist shortages, while diagnostic laboratories deploy AI to scale high-throughput screening and remote interpretation.

Key Report Takeaways

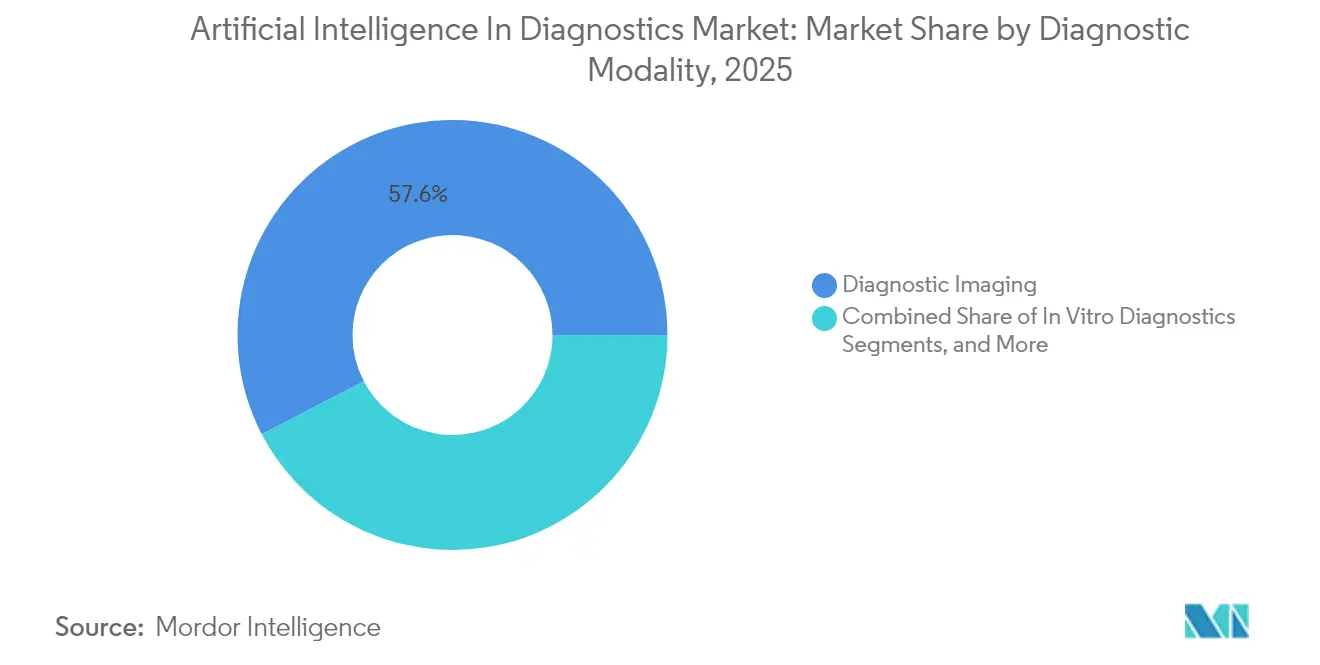

- By diagnostic modality, imaging accounted for 57.64% of the Artificial Intelligence in Diagnostics market share in 2025; in vitro diagnostics is forecast to expand at a 32.9% CAGR through 2031.

- By application, neurology led with a 25.21% revenue share in 2025, while oncology is tracking a 33.2% CAGR to 2031.

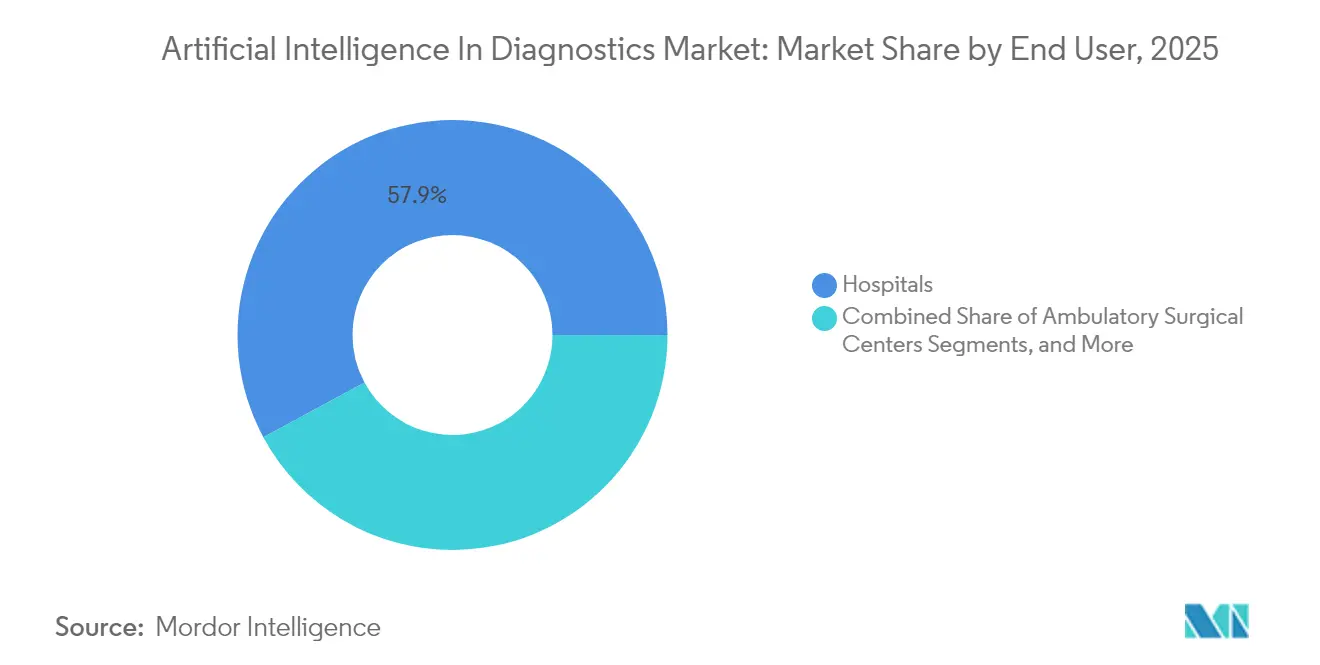

- By end-user, hospitals held 57.88% of the Artificial Intelligence in Diagnostics market share in 2025; diagnostic laboratories post the fastest 32.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Intelligence In Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for AI tools in medical imaging & workload reduction | +8.5% | Global, highest in North America & Europe | Medium term (2–4 years) |

| Government incentives accelerating AI adoption | +6.2% | North America & European Union; emerging impact in Asia-Pacific | Long term (≥ 4 years) |

| Surge in venture & strategic funding for AI-diagnostics start-ups | +5.8% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| FDA fast-track 510(k) clearances for AI diagnostic devices (post-2024) | +4.9% | Global, primary impact in North America | Medium term (2–4 years) |

| Foundation-model integration enabling multimodal diagnostics | +4.1% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Emergence of CMS reimbursement codes for AI algorithms | +3.9% | North America, with spillover to other developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for AI tools in medical imaging & workload reduction

Worldwide shortages of radiologists intensify interest in automation. Siemens Healthineers reports that its AI-Rad Companion Chest CT reduces report preparation time by up to 74%, freeing specialists for complex cases [1]Siemens Healthineers, “AI-Rad Companion Chest CT Delivers 74% Time Savings,” Siemens Healthineers, siemens-healthineers.com. Emergency departments see similar gains: RapidAI’s stroke-triage model delivers 98% sensitivity, accelerating door-to-needle decisions. Imaging networks such as RadNet spent more than USD 54 million on AI acquisitions in 2024 alone to preserve turnaround speed and referral loyalty.

Administrators also cite reduced burnout and fewer repetitive stress injuries among sonographers after AI-guided scanning protocols. As imaging volumes keep rising faster than staff rosters, the Artificial Intelligence in Diagnostics market becomes core infrastructure rather than optional add-on.

Government incentives accelerating AI adoption

National policies now combine grants, standards and payment reform. The U.S. HHS AI Strategy earmarks funding for hospital pilots and codifies an HHS AI Council for ongoing governance. In Europe, the EU AI Act classifies diagnostic imaging algorithms as “high-risk,” but offers regulatory sandboxes and harmonized conformity assessment, lowering multi-country launch costs. Legislatures in 34 U.S. states debated over 250 AI-related healthcare bills in 2025, many mandating coverage or setting liability shields for AI-guided diagnosis. In emerging Asian markets, public procurement programs subsidize cloud-hosted inference services so rural clinics can access city-grade image reading without on-site radiologists.

Surge in venture & strategic funding for AI-diagnostics start-ups

Capital flows speed commercialization. Imagen Technologies secured USD 32 million in Series C financing; AZmed raised USD 16.2 million; and ThinkSono attracted GBP 2.1 million to advance ultrasound AI. Corporate investors mirror this activity: GE HealthCare purchased Intelligent Ultrasound’s clinical AI business for USD 53 million to deepen point-of-care offerings [2]GE HealthCare, “NVIDIA Partnership To Deliver Autonomous Imaging,” GE HealthCare, gehealthcare.com. Aidoc reserved USD 30 million specifically to train foundation models that span multiple imaging organs within a single architecture. Ready access to cash translates into faster regulatory submissions and broader geographic roll-outs, fuelling compound growth in the Artificial Intelligence in Diagnostics market.

FDA fast-track 510(k) clearances for AI diagnostic devices

Post-2024, the FDA granted breakthrough designation to algorithms such as Cleerly’s coronary artery disease staging platform and icometrix’s tool for amyloid-related imaging abnormality detectioN. January 2025 draft guidance underscores continuous performance monitoring and bias audits, but also outlines a clear pre-submission workflow, cutting uncertainty for innovators. The streamlined route encourages early alignment between developers and reviewers, shrinking average submission-to-clearance timelines and reinforcing investor confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reluctance among medical practitioners to adopt AI | −4.2% | Global, steeper in traditional healthcare systems | Medium term (2–4 years) |

| High procurement & lifecycle-maintenance costs | −3.8% | Global, toughest for small providers | Short term (≤ 2 years) |

| Algorithmic bias triggering regulatory scrutiny | −2.9% | Global, stricter oversight in EU & North America | Long term (≥ 4 years) |

| Fragmented data-interoperability standards | −2.1% | Global, acute challenges in multi-vendor environments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Reluctance among medical practitioners to adopt AI

Clinicians worry about loss of autonomy, liability exposure and algorithmic opacity. A 2024 survey of Polish physicians found that only 32% were fully comfortable delegating image interpretation to AI, despite 68% agreeing it improves throughput [3]Ewelina Kowalewska, “Physicians and AI in Healthcare: Insights From a Mixed-Methods Study in Poland on Adoption and Challenges,” Frontiers in Digital Health, frontiersin.org. Experienced radiologists voice concerns that atypical cases fall outside training data, requiring nuanced human judgment. Cost adds friction: department chairs identified procurement expense as the primary roadblock even when quality benefits were acknowledged. Finally, job-security fears linger; almost half of surveyed nurses expressed unease about AI replacing certain tasks, though structured training programs significantly improved acceptance rates.

High procurement & lifecycle-maintenance costs

Initial licensing, GPU infrastructure and PACS integration often exceed USD 1 million for multi-site deployments. Annual support contracts can reach 30% of the upfront price as vendors roll out iterative model updates to meet evolving FDA performance expectations. Smaller laboratories struggle to amortize these expenses across limited procedure volumes. Cloud-based subscription models promise relief but raise data-sovereignty and latency issues in markets with fragile connectivity. As standardization improves, cost curves are expected to drop, yet near-term adoption remains skewed toward well-capitalized health systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnostic Modality: Imaging Dominates Despite IVD Acceleration

Diagnostic imaging captured 57.64% of the Artificial Intelligence in Diagnostics market share in 2025, leveraging decades of archived DICOM files that enable supervised deep-learning at scale. Foundation models, pre-trained on millions of X-ray, CT and MRI slices, now deliver organ-agnostic workflows that read multiple pathologies in one pass. Vendors such as GE HealthCare pair these algorithms with edge processors embedded directly in detectors, cutting latency and reducing data-center fees. The Artificial Intelligence in Diagnostics market size for imaging is projected to expand steadily as autonomous acquisition protocols reduce retakes and standardize quality, making AI indispensable in resource-tight departments.

In vitro diagnostics (IVD) is the fastest-growing modality, set to scale at a 32.9% CAGR through 2031. Pattern-recognition networks classify genomic variants, metabolomic spectra and microbial signatures with higher specificity than rule-based analyzers. The Artificial Intelligence in Diagnostics market size for IVD will benefit from turnkey cloud APIs that deliver assay interpretation to small labs without dedicated data scientists. Digital pathology sits at the intersection of imaging and IVD; slide scanners feed whole-slide images into convolutional nets that mark tumor margins and grade inflammation, allowing pathologists to focus on complex differential diagnoses.

By Application: Oncology Disrupts Neurology’s Leadership

Neurology held 25.21% of Artificial Intelligence in Diagnostics market share in 2025, underpinned by stroke, epilepsy and dementia workloads that demand rapid intervention. Real-time CT perfusion mapping shortens door-to-thrombolysis times, while 3D volumetry quantifies multiple sclerosis lesion load with sub-millimeter precision. Yet oncology is advancing at a 33.2% CAGR to 2031, propelled by tools such as Clairity BREAST, the first device authorized to predict five-year breast-cancer risk from a single mammogram. Multimodal fusion of radiology, pathology and genomic data further elevates accuracy, shifting oncology from image-centric detection to holistic prognostication.

Cardiology continues steady adoption as HeartFlow’s AI-derived plaque analysis gains Medicare coverage, validating reimbursement-driven uptake. Infectious-disease algorithms classify pathogen species directly from chest X-rays or broad-spectrum sequencing, a priority in antimicrobial-resistance stewardship. Meanwhile, obstetric AI tracks fetal growth curves in motion-compensated 3D ultrasound, expanding prenatal care access in low-resource regions.

By End-User: Laboratories Challenge Hospital Dominance

Hospitals commanded 57.88% of the Artificial Intelligence in Diagnostics market share in 2025 thanks to large scanner fleets, enterprise PACS and in-house IT teams capable of supporting GPU clusters. Integrated AI raises scanner utilization, creating headroom without capital expansion. The Artificial Intelligence in Diagnostics market size attributable to hospitals will keep growing as reimbursement stabilizes and bundled-payment models reward diagnostic accuracy.

Diagnostic laboratories post the fastest 32.85% CAGR by leveraging AI to automate high-volume studies ranging from full-body CT screenings to multiplex PCR interpretation. The Artificial Intelligence in Diagnostics market size for laboratories is lifted by remote-read services that route images through secure clouds to subspecialists thousands of miles away. Partnerships such as Integral Diagnostics’ expansion of Aidoc workflows across Australia and New Zealand show how independent chains level the playing field against tertiary hospitals. Ambulatory centers and tele-imaging platforms round out the user base, exploiting software-as-a-service models that eliminate on-site GPU ownership.

Geography Analysis

North America remains the epicenter, accounting for 53.48% of global revenue in 2025. Early FDA clearances—129 radiology AI devices since 2015—established a precedent that de-risked pilot budgets, while new CMS codes ensure monetization for stroke detection, cardiac CTA analysis and breast-cancer triage. Strategic collaborations are a hallmark: GE HealthCare and NVIDIA co-develop autonomous imaging suites to offset staff shortages, and Siemens Healthineers inks decade-long “value partnerships” bundling scanners, AI software and managed service agreements.

Europe follows closely. The EU AI Act mandates risk-based classification, model transparency and bias testing but also provides common technical documentation templates, accelerating cross-border market entry. Vendors like ThinkSono obtained CE marking for point-of-care ultrasound AI that guides novice operators through DVT scans, broadening the sonographer pool. National health systems in Germany, France and the Nordics run reimbursement pilots that tie AI performance to outcome-based bonuses.

Asia-Pacific is the fastest-growing territory. Government-backed electronic medical-record rollouts in India, Japan and South Korea generate structured image archives ideal for machine-learning. The National Health Authority of India and IIT Kanpur launched open-access datasets under IndiaAI to spur domestic algorithm development. Regional leaders like Qure.ai deployed tuberculosis triage across more than 90 districts, reporting 15 million cumulative patient scans. In China, hospital groups bundle AI lung-nodule detection with annual physicals, illustrating consumer-direct monetization outside insurance frameworks.

Regulatory Landscape

Regulation for AI in diagnostics continues shifting from one-time premarket review toward lifecycle oversight grounded in quality systems, change management, and post-market performance monitoring. In the United States, the FDA expanded its AI/ML framing for software as a medical device, including the use of Predetermined Change Control Plans (PCCP) to govern certain model updates within defined limits (finalized in December 2024), and issued draft guidance in January 2025 clarifying expectations for clinical evidence, marketing submissions, and ongoing monitoring for AI-enabled medical device software.

In Europe, the EU AI Act overlays the existing Medical Device Regulation (MDR) and In Vitro Diagnostic Regulation (IVDR) for many diagnostic algorithms treated as high-risk systems. MDCG 2025-6 describes this complementarity and the resulting documentation interplay. In April 2026, the IMDRF AIML Working Group released draft N93, Technical Framework for Artificial Intelligence Life Cycle Management, for public consultation through July 10, 2026, reinforcing convergence on lifecycle controls and traceability across jurisdictions.

Value Chain Analysis

The value chain runs from data origination and governance (hospitals, diagnostic laboratories, imaging networks, and biobanks) to model development and validation (AI vendors, academic centers, and contract research partners), then to clinical deployment inside operational workflows (PACS/RIS, LIS, EHR integration, and reporting). Platform and infrastructure providers supply compute and MLOps tooling for training and inference, while modality OEMs for imaging and lab instrumentation increasingly embed AI into scanners, detectors, or companion software. This tightens the link between device service contracts and algorithm updates.

Key bottlenecks center on dataset normalization, evidence generation across sites, and the compliance documentation needed for change control and auditability, rather than physical manufacturing capacity. That constraint is driving more consolidation and partnering across the chain. For example, Roche signed a definitive agreement to acquire PathAI in May 2026, aiming to bring AI deeper into digital pathology and companion diagnostics workflows, while health systems adopt enterprise deployment layers to operationalize third-party and homegrown models under shared governance and monitoring.

Competitive Landscape

Moderate fragmentation defines the Artificial Intelligence in Diagnostics market. Incumbent equipment makers—GE HealthCare, Siemens Healthineers and Philips—integrate proprietary algorithms at the firmware layer, selling scanners as analytics platforms rather than hardware appliances. GE HealthCare has more than 40 FDA-cleared AI applications embedded in its Revolution CT line, while Siemens Healthineers holds over 450 active imaging-AI patents. Pure-play vendors such as Aidoc, Viz.ai and RapidAI compete on triage speed and breadth of FDA-cleared indications; Aidoc alone covers 13 acute findings across the neuro and chest domains.

Strategic alliances blur boundaries. GE HealthCare’s 2025 tie-up with NVIDIA grants access to accelerated inference libraries and MONAI DevKit, halving development cycles for autonomous X-ray positioning. Cleerly and HeartFlow specialize in cardiovascular imaging, while Nanox pairs low-dose digital X-ray hardware with cloud AI that screens for bone fragility at population scale. Standards bodies such as IHE release workflow profiles that govern how AI results populate radiology reports, enhancing vendor interoperability and customer lock-in.

M&A pressures rise as start-ups confront elongating sales cycles and higher validation costs. RadNet’s USD 103 million purchase of iCAD in April 2025 bolsters its breast-imaging AI stack and demonstrates provider appetite for captive algorithm teams. Health-system venture funds increasingly trade minority stakes for exclusive deployment rights, signaling a pivot from vendor-centric to buyer-centric bargaining power. Overall, competitive intensity centers on pipeline breadth, regulatory agility and proof of economic value delivered.

Artificial Intelligence In Diagnostics Industry Leaders

Nanox Imaging LTD (Zebra Medical Vision, Inc.)

Riverain Technologies

Aidoc

Siemens Healthineers

Vuno, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reimbursement and workflow integration create the most visible gap between pilots and scaled, repeatable clinical service lines. In the United States, CMS establishing permanent payment codes for stand-alone radiology AI algorithms has strengthened the business case for hospitals and imaging networks to standardize deployment, monitoring, and reporting at the enterprise level, rather than procuring isolated point solutions. This also supports opportunities for vendors offering model lifecycle services (drift detection, bias audits, and controlled updates) aligned with FDA expectations such as PCCP-based change governance.

Product-market expansion is increasingly tied to embedding AI into modality platforms and diagnostic pathways beyond acute triage, including cardiology, ultrasound automation, and digital pathology. In 2026, several in-scope, regulated product actions show this shift: Abbott received FDA clearance and CE Mark for Ultreon 3.0 (April 2026) for AI-assisted coronary imaging, Philips launched the Alturion ultrasound system with AI-powered workflows (July 2026), and Aidoc received FDA Breakthrough Device Designation for First Read (June 2026) to draft preliminary radiology reports from chest X-rays. Together, these actions expand addressable use from detection-only tools toward end-to-end workflow assistance that can be packaged with hardware refresh cycles, managed services, and cross-department governance programs.

Recent Industry Developments

- April 2026: Nanox signed a distribution agreement with Radiology Oncology Systems to expand access to its Nanox.ARC imaging systems in the United States. The agreement strengthens channel reach for a hardware-plus-cloud model where AI-enabled software capabilities are part of the product value proposition, supporting broader deployment outside early-adopter sites.

- December 2025: Riverain Technologies announced an expansion of its Ohio operations to support growth and advance health technology innovation. Additional operational footprint supports scaling of ClearRead AI delivery, customer support, and clinical collaboration capacity, which are critical as buyers move from pilot contracts to multi-site adoption.

- November 2024: The FDA finalized guidance enabling Predetermined Change Control Plans (PCCP) for certain AI-enabled device software, outlining how predefined updates can be managed within an approved framework. This clarified a practical route for regulated performance improvements without repeated full submissions, shaping how developers design update pipelines and post-market monitoring for diagnostic algorithms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market includes AI software and embedded algorithms that take clinical inputs such as medical images, lab values, and electronic records, and then support disease detection, classification, or rule-out decisions used in diagnostic workflows.

Scope exclusions: Hardware-only sales, general administrative AI tools, and broad care coordination platforms that do not produce a patient-facing diagnostic output are excluded.

Segmentation Overview

- By Diagnostic Modality

- In Vitro Diagnostics

- Molecular Diagnostics

- Immunoassays & Clinical Chemistry

- Point-of-Care Tests

- Diagnostic Imaging

- MRI

- CT

- X-ray

- Ultrasound

- PET/SPECT & Others

- Digital Pathology

- Other Modalities

- In Vitro Diagnostics

- By Application

- Oncology

- Cardiology

- Neurology

- Infectious Disease

- Obstetrics & Gynecology

- Respiratory & Pulmonology

- Other Applications

- By End-User

- Hospitals

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public, trusted sources to set the boundaries and build the first demand map for AI-enabled diagnostics. We referred to items such as FDA device databases and guidance, CMS coverage and payment updates, OECD and World Bank health system indicators, and publications from groups such as WHO, along with peer-reviewed journals that track AI diagnostic performance and adoption.

We also reviewed company annual reports, investor decks, product documentation, and reputable press to understand where solutions are actually deployed and how they are priced (license, subscription, or usage-linked). To fill gaps on company revenue splits and deal activity, we used paid subscriptions focused on company financials and intelligence, news and financials, patent databases, and selective contracts and tenders tracking. These desk sources are not exhaustive, and many other public and paid references were used for data collection, cross-checks, and clarification during the study.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test the sizing inputs that desk research cannot reliably standardize, such as active clinical usage versus pilot installs and the way pricing changes by workflow and department. We spoke with a mix of diagnostic workflow stakeholders, including hospital imaging leaders, diagnostic lab managers, clinical specialists, and product and commercial leaders from solution providers across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 43% |

| Mid tier: 61% | Functional/Unit leaders: 41% | EMEA: 31% |

| Smaller Players: 14% | Managers: 47% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where diagnostic procedure pools and clinical adoption signals were used to reconstruct the addressable spend, and then checked against supplier-side revenue patterns to keep the totals realistic. In practice, the top-down path started from diagnostics activity indicators and AI readiness signals, which were then filtered through adoption rates by workflow and weighted pricing to arrive at market value.

A few inputs that mattered a lot in this market were the number of imaging and lab tests performed, the share of sites using AI in live reading or triage, the average contract value by department, the pace of regulatory clearances for diagnostic algorithms, and the reimbursement and coverage posture in major countries. Because gaps show up quickly in early-stage markets, we used conservative rules to handle missing pricing or volume points, and we adjusted assumptions only when interview feedback and observed deal patterns aligned.

For forecasting, scenario analysis was used with near-term adoption and pricing expectations gathered from experts, and then translated into a yearly build that reflects rollout cycles in hospitals and labs. Where adoption looked uneven, the model allowed slower uptake until operational triggers were met, such as workflow integration maturity and budget cycle timing.

Data Validation & Update Cycle

Validation was done through several checks so the final totals do not rely on one single input. Outputs were compared with independent signals such as clearance activity, public reimbursement moves, and the observed mix of enterprise versus departmental deployments, and then any large variances were reviewed again before sign-off.

A second analyst review was applied to the key assumptions, followed by selective re-contact with primary respondents when an input moved meaningfully or a regional pattern looked inconsistent. Reports are refreshed annually, and interim updates are made when material events occur, such as policy changes or major shifts in pricing. Before delivery, we do a final pass to make sure clients receive the most current view available at that time.

Mordor Intelligence's Diagnostics Artificial Intelligence Market Size Compared With Other Published Estimates

Published market sizes for AI in diagnostics often differ because each study draws the market boundary in its own way and uses different adoption and pricing logic. The biggest swings usually come from what gets counted as diagnostics, how software versus services are treated, and whether the estimate leans on installed base assumptions or on active clinical usage.

By tracking regulatory clearances, reimbursement signals, and active workflow deployment checks, Mordor Intelligence keeps the estimate centered on AI software and embedded algorithms used in real diagnostic decisions, which reduces inflation from adjacent IT budgets or non-diagnostic AI tools.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.77 B (2025) | |

| Industry Publisher A | USD 2.60 B (2024) | Uses a broader clinical and molecular diagnostics scope, which can pull in adjacent analytics and platform spend beyond patient-facing diagnostic decision support, and it anchors the curve on a different base year. |

| Global Research Group B | USD 1.47 B (2024) | Typically applies a narrower revenue capture lens focused on core software across selected specialties, which can undercount enterprise deployments and bundled pricing that is reported at department or network level. |

Overall, the spread in published values is mostly explained by scope boundaries and how adoption is translated into revenue, not by disagreement on the direction of growth. Our approach stays traceable to clear inputs like diagnostic activity, real deployment status, and pricing structures that can be rechecked as the market evolves.

Key Questions Answered in the Report

How big is the Global Artificial Intelligence in Diagnostics Market?

The Global Artificial Intelligence in Diagnostics Market size is expected to reach USD 2.33 billion in 2026 and grow at a CAGR of 31.88% to reach USD 9.32 billion by 2031.

What is the current Global Artificial Intelligence in Diagnostics Market size?

Imaging modalities hold 57.64% share, supported by vast DICOM-based datasets and embedded GPU workflows.

Who are the key players in Global Artificial Intelligence in Diagnostics Market?

Nanox Imaging LTD (Zebra Medical Vision, Inc.), Riverain Technologies, Aidoc, Siemens Healthineers and Vuno, Inc. are the major companies operating in the Global Artificial Intelligence in Diagnostics Market.

Which is the fastest growing region in Global Artificial Intelligence in Diagnostics Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Why is North America ahead in adoption?

Streamlined FDA clearances, CMS reimbursement codes and strong venture funding give North America 53.48% revenue share.

Page last updated on: