AI In Clinical Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

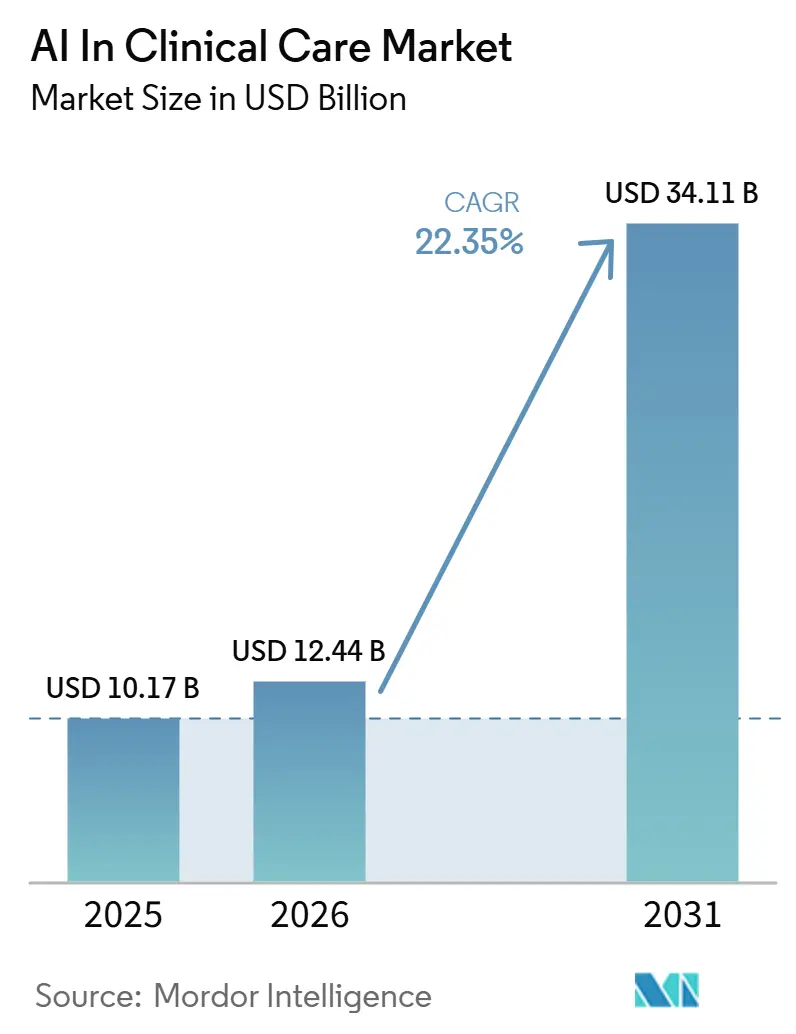

| Market Size (2026) | USD 12.44 Billion |

| Market Size (2031) | USD 34.11 Billion |

| Growth Rate (2026 - 2031) | 22.35% CAGR |

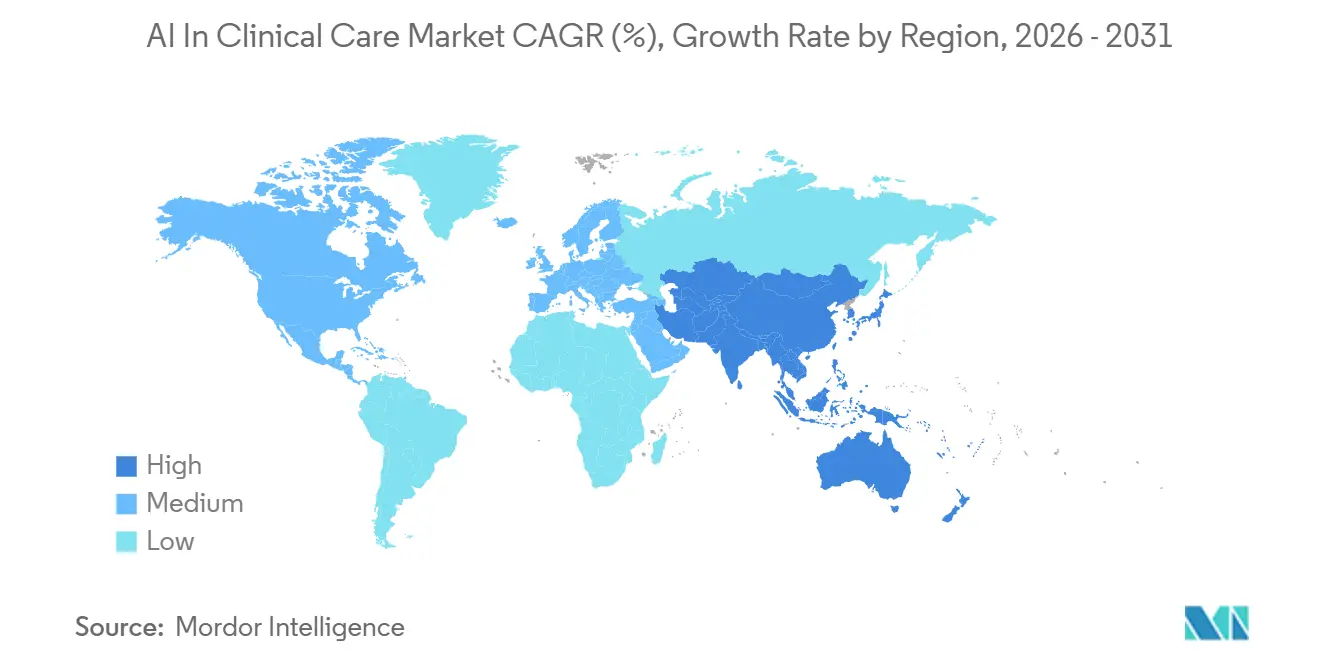

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

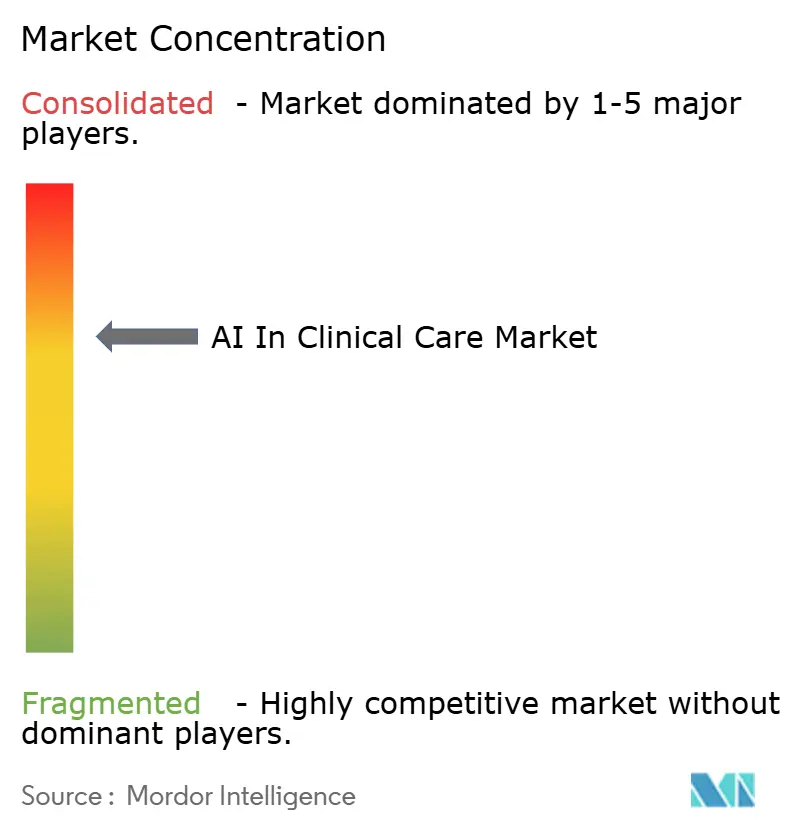

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Clinical Care Market Analysis by Mordor Intelligence

The AI In Clinical Care Market size is expected to increase from USD 10.17 billion in 2025 to USD 12.44 billion in 2026 and reach USD 34.11 billion by 2031, growing at a CAGR of 22.35% over 2026-2031.

The AI in clinical care market is expanding as hospitals place decision support, documentation, and diagnostic tools directly inside daily workflows, which removes many of the adoption barriers that slowed earlier point solutions. Ambient documentation is also becoming a practical buying priority because health systems now link it to clinician retention, lower after-hours work, and better documentation consistency. Value-based reimbursement is adding another push because providers are under greater pressure to reduce avoidable variation, improve outcomes, and defend the quality of clinical records. In 2026, 70% of healthcare and life sciences organizations actively used AI, up from 63% in 2025, and 69% deployed generative AI and large language models, which shows that operational use has moved well beyond pilot programs. Competition in the AI in clinical care market is therefore shifting toward broader clinical intelligence platforms that combine documentation, decision support, payer workflow support, and governance into a single enterprise relationship.

Key Report Takeaways

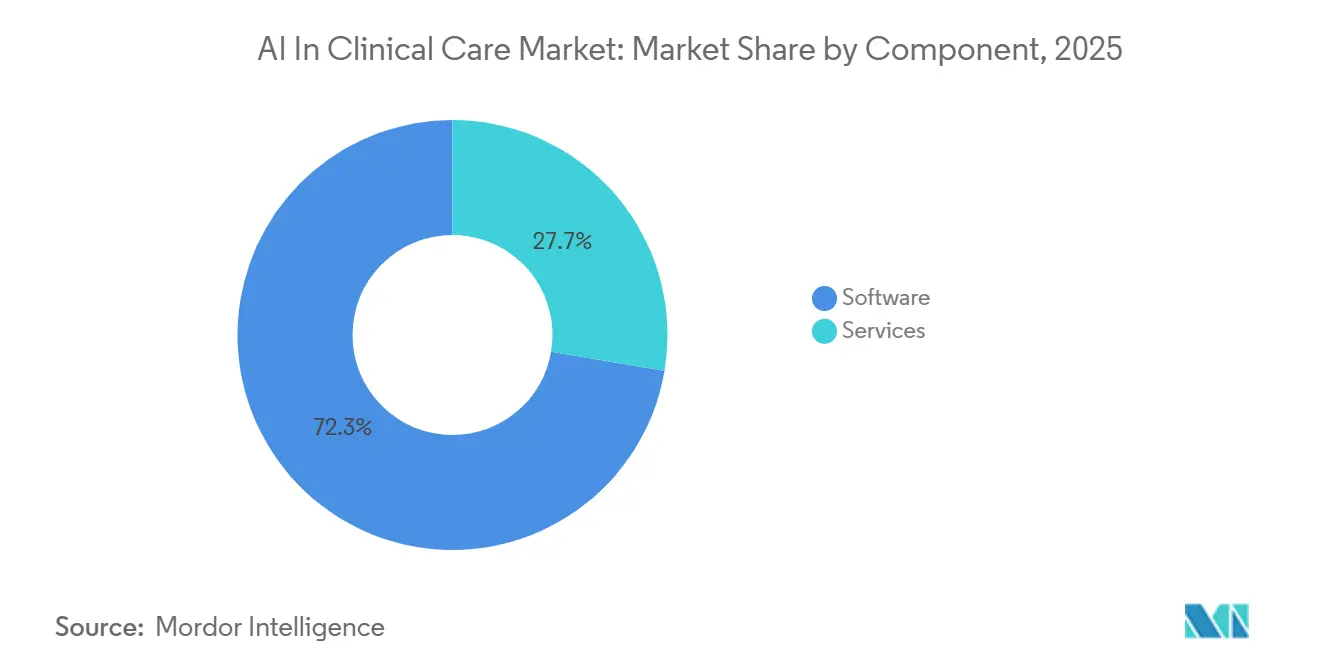

- By component, software led with 72.34% revenue share in 2025, while services are forecast to expand at 23.56% CAGR through 2031.

- By deployment mode, cloud-based systems held 68.43% share in 2025, while on-premise deployments are projected to grow at 24.91% CAGR through 2031 in AI in clinical care market.

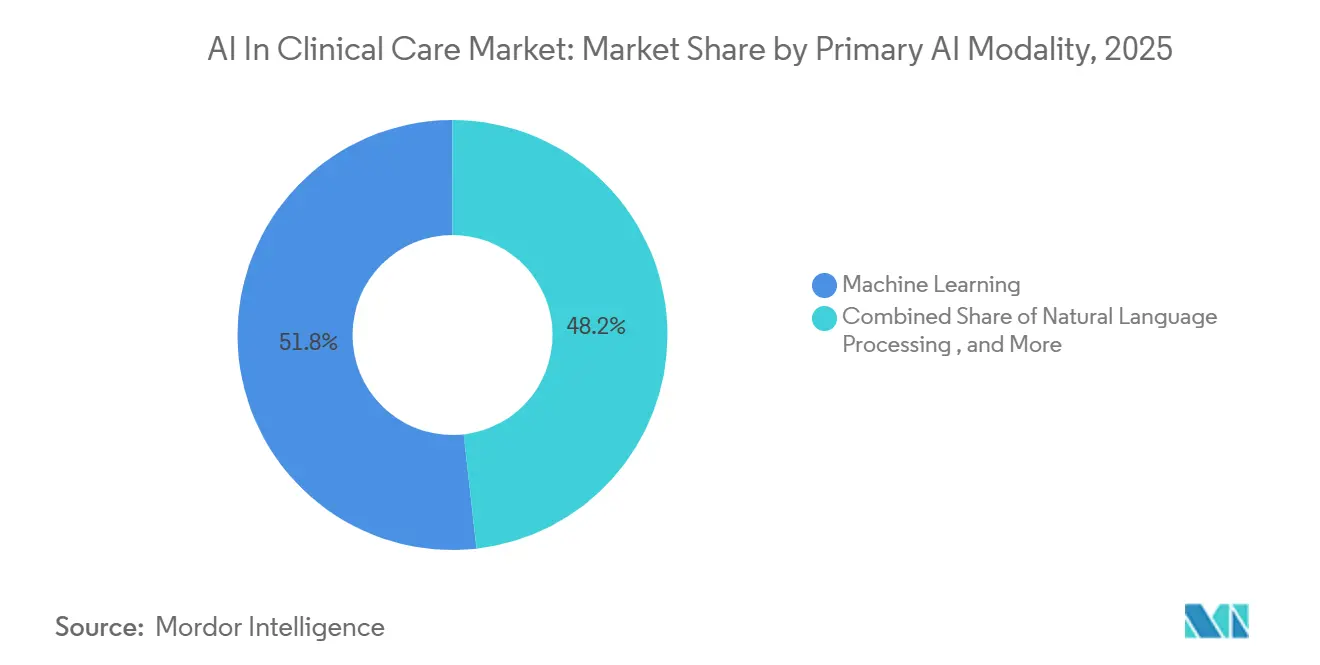

- By primary AI modality, machine learning accounted for 51.78% share in 2025, while Natural Language Processing (NLP) is expected to advance at 25.48% CAGR through 2031.

- By application, medical diagnosis captured 36.94% share in 2025, while treatment planning and personalization are projected to grow at 23.94% CAGR through 2031 in AI in clinical care market.

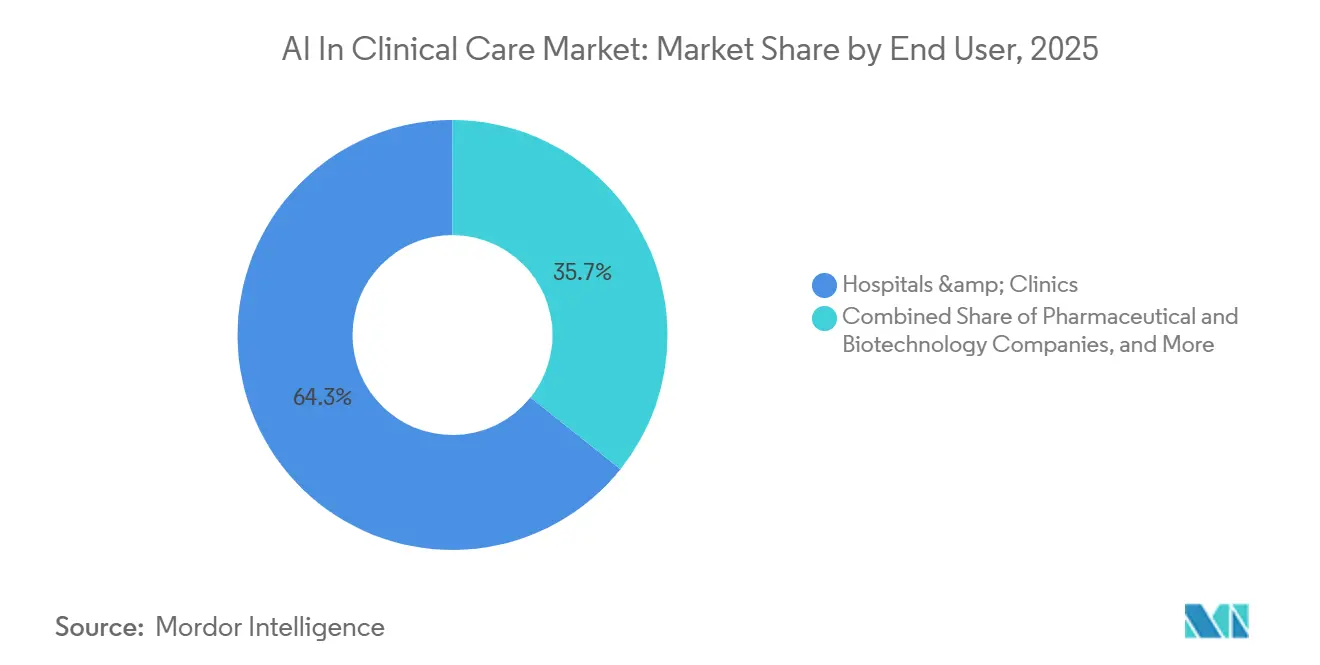

- By end user, hospitals and clinics held 64.26% share in 2025, while pharmaceutical and biotechnology companies are expected to grow at 26.73% CAGR through 2031.

- By geography, North America captured 39.47% of the AI in clinical care market share in 2025, while Asia-Pacific is projected to expand at 27.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Clinical Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of EHR-Embedded AI Clinical Decision Support | +4.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Burnout Relief Through Ambient Clinical Documentation | +3.8% | North America, Western Europe | Short term (≤ 2 years) |

| Need to Reduce Diagnostic Errors and Care Variation | +3.2% | Global | Medium term (2-4 years) |

| Value-Based Care and Precision Treatment Economics | +2.9% | North America, Western Europe | Medium term (2-4 years) |

| Frontline Use of FDA-Cleared Imaging and Triage AI | +3.5% | North America, EU, APAC | Short term (≤ 2 years) |

| Multilingual Specialty-Tuned Clinical AI for Underserved Settings | +1.8% | APAC, MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of EHR-Embedded AI Clinical Decision Support

The AI in clinical care market is benefiting from the shift toward tools that work inside the clinician’s normal EHR workflow rather than outside it. A 2026 study in Scientific Reports described AIDx as a locally deployable system that retrieves patient context from the EHR and produces structured recommendations inside the user’s native environment.[1]“AIDx: A Locally Deployable AI System for Physician Clinical Decision Support,” That matters because it reduces switching between screens, which has long limited the real use of clinical software even when technical performance was strong. A pragmatic cluster-randomized trial published in Nature Medicine also showed that generative AI-enabled decision support in primary care improved guideline adherence, which supports broader rollout in routine care settings.[2]“Generative AI-Enabled Clinical Decision Support System in Primary Care: A Pragmatic, Cluster-Randomized Trial,” Technology is no longer the main barrier in many health systems, while governance, training, and policy awareness have become the harder part of scaling adoption, with only 27% of clinicians aware of a formal organizational AI policy in 2026.

Burnout Relief Via Ambient Clinical Documentation

The AI in clinical care market is also being lifted by the strong commercial case for ambient documentation. A multicenter quality improvement study across 6 U.S. health systems found that 30 days of ambient AI scribe use reduced clinician burnout from 51.9% to 38.8%, while also improving cognitive task load and after-hours documentation time.[3]“Use of Ambient AI Scribes to Reduce Administrative Burden and Professional Burnout,” Mass General Brigham expanded its program to more than 3,000 providers by April 2025 and reported a 21.2% absolute reduction in burnout at 84 days, which gave health systems a concrete deployment model. The commercial model is also widening because Abridge said in June 2026 that its platform connected documentation, payer workflows, and evidence-based treatment and was deployed across more than 300 health systems supporting over 100 million annual clinical conversations. This moves the value proposition from narrow scribing into enterprise clinical intelligence, which supports larger contracts and deeper system integration.

Need to Cut Diagnostic Errors and Care Variation

The AI in clinical care market is gaining support from the need to reduce diagnostic inconsistency across specialties and sites of care. Diagnostic errors affect 1 in 14 general medical hospital patients, which keeps diagnostic support high on provider priorities within the AI in clinical care market. At the same time, a 2025 study in the International Journal of Medical Informatics found that the correctness of AI recommendations materially affected physician diagnostic accuracy, which raises the importance of reliable model performance and strong clinical validation. This creates a clear separation between vendors that provide auditable reasoning and peer-reviewed evidence, and vendors that rely on black-box outputs with weaker clinical trust. Specialized tools in pathology, imaging, and disease-specific decision support are therefore gaining adoption faster than broad general-purpose systems because they address known diagnostic gaps with clearer evidence thresholds.

Value-Based Care and Precision-Treatment Economics

The AI in clinical care market is also being shaped by payment models that reward measurable outcomes instead of procedural volume. CMS launched the TEAM mandatory bundled payment model in 2026, which strengthens the case for tools that predict readmissions, optimize pathways, and support chronic care management. A published evaluation of an AI readmission-risk model in a safety-net system showed that a USD 1 million investment returned USD 7.2 million in retained at-risk funding, while cutting 30-day readmissions by 4 percentage points and closing racial equity gaps in outcomes. As reimbursement pressure rises, providers are more willing to buy systems that help them standardize care decisions and document those choices clearly. The same logic is drawing pharmaceutical partners toward frontline clinical platforms because prescribing guidance and trial matching are becoming part of the routine workflow rather than standalone programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, Cybersecurity, and AI Governance Burden | -2.4% | Global, with particular intensity in North America and EU | Short term (≤ 2 years) |

| Workflow Integration Friction and Alert Fatigue Risk | -1.9% | Global | Medium term (2-4 years) |

| Payer Downcoding and Reimbursement Recalibration | -1.6% | North America primarily | Short term (≤ 2 years) |

| Model Drift, Monitoring Gaps, and Liability Exposure | -1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Cybersecurity, and AI Governance Burden

The AI in clinical care market still faces a heavy trust burden because protected health data sits at the center of every deployment. Healthcare data breaches reached a record 772 large incidents listed on the HHS OCR breach portal in 2025, which kept cybersecurity risk high for hospital buyers. Vendors that build HIPAA-ready architectures with audit trails, role-based access, and continuous monitoring hold an advantage in regulated environments, but those controls also raise product cost and lengthen procurement cycles. Formal governance on paper does not fully solve the issue because clinician awareness of organizational AI policy remained only 27% in 2026.[4]“Patients, Doctors, and Nurses: 2026 Future Ready Healthcare Survey Report,” This gap between enterprise controls and frontline behavior can slow deployment even when the underlying technology is ready.

Workflow Integration Friction and Alert-Fatigue Risk

The AI in clinical care market also faces resistance when tools add to the alert load instead of reducing it. A 2026 qualitative study in JMIR found that alert fatigue was driven by poor alert design, bad timing, and weak customization as much as by individual clinician tolerance. Another study in Applied Clinical Informatics showed that efforts to reduce alert burden across 2 major commercial EHRs were limited by vendor restrictions on decision support customization. This means the deployment burden often falls back on the AI vendor, which increases integration work, extends rollout timelines, and reduces margin. At the same time, a 2026 NEJM AI report from Stanford Health Care showed that machine learning-driven support for laboratory utilization could reduce non-critical volume and improve efficiency when implementation is carefully designed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue, Services Broaden the Engagement Model

Software held 72.34% of revenue in 2025, which made it the largest part of the AI in clinical care market size by component. The scale advantage is clear because one cloud update can reach many hospital users at once, while subscription pricing fits annual provider budgeting better than large one-time purchases. This has made software the fastest route for hospitals that want to adopt clinical AI without a major infrastructure change. In the AI in clinical care industry, software also benefits from shorter release cycles that let vendors improve models and interfaces continuously.

Services are projected to grow at 23.56% CAGR through 2031, which makes them the fastest-growing component. Buyers are moving toward managed AI relationships that include retraining, integration, auditing, and governance support because deployment now extends far beyond initial licensing. The American Medical Association said in 2026 that more than 75% of physicians saw AI as offering a patient-care advantage, up from 65% in 2023, which helps internal champions support these longer service engagements. This shift suggests that many health systems now want accountability for outcomes and model performance, not only access to software. In practical terms, services are becoming the layer that helps vendors defend margins as the AI in clinical care market matures.

By Deployment Mode: Cloud Leads Adoption While On-Premise Supports Control

Cloud-based systems commanded 68.43% of 2025 revenue and represented the largest share of the AI in clinical care market by deployment mode. Their lead reflects lower upfront capital needs, faster implementation, and easier support for distributed care settings. Cloud delivery also fits the product logic of continuous updates, centralized monitoring, and multi-site health system rollout. For many buyers, that mix of speed and cost control keeps cloud as the default procurement path in the AI in clinical care market.

On-premise deployment is forecast to grow at 24.91% CAGR through 2031, which makes it the fastest-moving model despite its smaller base. The driver is not volume alone, but the tighter control it offers over data perimeters, oversight, and compliance workflows in sensitive clinical environments. This is why some providers accept a premium for on-premise deployment when governance demands are high or infrastructure rules are strict. On-premise systems, therefore, hold a strategically important place even though cloud still dominates the AI in clinical care market share in current revenue terms. Vendors that can deliver similar functionality across both models are better positioned to win hybrid health system contracts.

By Primary AI Modality: Machine Learning Leads, NLP Gains Momentum Fast

Machine learning held 51.78% of 2025 revenue, which made it the largest modality across the AI in clinical care market size breakdown. Its lead comes from the long clinical history of imaging analysis, pattern recognition, and triage support, where model-based prediction has already shown practical value. Machine learning also benefits from clearer validation pathways in narrow use cases, which helps hospitals buy with more confidence. That stable installed base gives this modality a strong anchor position in the AI in clinical care market.

Natural Language Processing (NLP) is projected to grow at 25.48% CAGR through 2031, making it the fastest-growing modality. The rise of ambient documentation, note structuring, coding support, and longitudinal record summarization is pushing NLP into more daily workflows. A 2026 AAAI study showed that grounding large language models in clinical guidelines for longitudinal cancer EHR decision support improved performance over retrieval-only approaches, which points to the architecture many vendors are now following. This suggests that the strongest NLP systems will be the ones that combine language generation with clinical grounding and governance. In the AI in clinical care industry, that makes NLP a growth engine even though it still trails machine learning in current revenue.

By Application: Diagnosis Holds the Base While Personalization Expands Faster

Medical diagnosis retained 36.94% share in 2025, which gave it the largest position in the AI in clinical care market size by application. This lead rests on years of development in imaging and diagnostic support, where health systems already understand the workflow and the clinical value. Diagnostic use cases are also easier to prioritize because they connect directly to patient safety, reading efficiency, and specialist capacity. That keeps diagnosis as the commercial foundation of the AI in clinical care market.

Treatment planning and personalization are expected to grow at 23.94% CAGR through 2031, which places it ahead of other application areas in growth. The segment is expanding because providers want tools that combine genomics, imaging, treatment history, and other patient data into more individualized recommendations. A 2026 review in Frontiers in Medicine described how AI can synthesize multimodal data to support individualized therapy protocols at a scale that manual workflows cannot match. Patient monitoring, early warning, and risk prediction remain important adjacent areas, but their growth still depends on careful integration into bedside and post-acute workflows. Over time, the application mix should broaden as the AI in clinical care market moves from detection into active care pathway design.

By End User: Hospitals Hold the Largest Base While Pharma and Biotech Grow Fastest

Hospitals and clinics accounted for 64.26% of demand in 2025, which gave them the largest role in the AI in clinical care market. Their lead is expected because they are the main setting for imaging, documentation, monitoring, and decision support deployment. They also hold the EHR infrastructure and clinical workflow control that most AI vendors need for scale. This makes hospitals the core commercial base of the AI in clinical care market across nearly every product category.

Pharmaceutical and biotechnology companies are projected to grow at 26.73% CAGR through 2031, making them the fastest-growing end-user group. Their momentum comes from AI-supported drug discovery, trial operations, and partnerships that place evidence-based prescribing guidance closer to frontline clinicians. Research and academic institutes remain a critical validation layer because they generate peer-reviewed evidence that providers often need before procurement. GE HealthCare’s lead industrial role in the EU-funded COMPASS initiative also shows how public-private research programs are helping translate advanced cardio-oncology AI into broader clinical use. The end-user mix is therefore widening even as hospitals continue to dominate the AI in clinical care market size today.

Geography Analysis

North America held 39.47% of 2025 revenue, which gave it the largest regional position in the AI in clinical care market. The region leads because it has a dense installed base of EHR-connected hospital systems, a mature regulatory path for clinical AI, and early movement on reimbursement. As of January 2026, 26 CPT codes existed for clinical AI solutions, including 3 Category I codes for tools that assess cardiovascular risk and diabetic retinopathy. That coding base helps reduce provider uncertainty because it gives hospitals a clearer route to payment and adoption. Coverage expansion also matters, and HeartFlow said in January 2026 that its Plaque Analysis tool had gained Aetna coverage across all lines of business, extending access through another major national insurer.

Asia-Pacific is the fastest-growing region with a projected 27.94% CAGR through 2031, which shows how quickly the AI in clinical care market is widening outside its most mature bases. The region’s growth reflects strong digital health investment, rising openness to AI-enabled care delivery, and a practical need to stretch clinical capacity. Adoption also benefits from the fact that many systems in the region are building new digital layers now rather than modifying older legacy environments. This creates room for AI vendors that can localize clinical workflows and meet regional policy expectations. The result is that Asia-Pacific is becoming one of the most important expansion corridors in the AI in clinical care market.

Europe remains a significant revenue contributor to the AI in clinical care market size because Germany, the United Kingdom, and France continue to anchor procurement and validation activity. Germany’s KHZG hospital digitalization program has directed EUR 4.3 billion into hospital IT modernization, which supports a real pipeline for clinical AI buying. The United Kingdom’s NHS AI Lab continues to back imaging and pathology deployments, which gives vendors a structured entry path into public system use. Beyond Europe, the Middle East and Africa region is expanding from a smaller base through sovereign digital health investment, while South America is building gradual momentum through digital health modernization and interest in value-based care models.

Competitive Landscape

The AI in clinical care market is moderately concentrated, with major imaging and healthcare technology vendors such as GE HealthCare, Siemens Healthineers, and Philips leveraging broad hospital relationships and multi-modality capabilities. At the same time, specialist vendors often move faster in narrow indications because they can focus development, validation, and commercial effort on a smaller clinical problem. This mix keeps the AI in the clinical care market competitive, even though scale advantages still matter.

Specialists are using regulatory progress and focused clinical evidence to build defensible positions. Aidoc received its second FDA Breakthrough Device Designation in less than 12 months for First Read, which drafts preliminary radiology report text from chest X-rays. Abridge used a different playbook by expanding in June 2026 from ambient documentation into a clinician intelligence platform that links documentation, payer workflows, and evidence-based treatment. Roche signaled the strategic value of pathology AI when it entered a definitive agreement in May 2026 to acquire PathAI for USD 750 million upfront with up to USD 300 million in milestones. These moves show that leadership in the AI in clinical care market is being built through platform depth, clinical proof, and workflow ownership rather than scale alone.

Platform convergence is becoming the defining theme in the AI in clinical care market. Standalone scribes, imaging triage tools, and decision support modules are increasingly being pulled into broader enterprise layers that can support multiple workflows. GE HealthCare’s March 2026 acquisition of Intelerad for USD 2.3 billion also reflects this direction because imaging software, cloud delivery, and AI capability are being tied more closely together. Regulatory expectations will continue to shape competition because vendors with stronger evidence packages and dedicated compliance capability will find it easier to scale across large health systems. Smaller point solution providers can still win, but they need clear clinical outcomes and strong interoperability to hold position as consolidation advances.

AI In Clinical Care Industry Leaders

Aidoc Medical Ltd.

athenahealth, Inc.

Epic Systems Corporation

Koninklijke Philips N.V.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Aidoc Medical Ltd. received FDA Breakthrough Device Designation for First Read, an AI system that analyzes chest radiographs and generates preliminary radiology report text. This is Aidoc's second Breakthrough Designation in under twelve months, following CARE Triage.

- April 2026: GE HealthCare expanded its mammography AI collaboration with RadNet's DeepHealth subsidiary to broaden the distribution of AI-powered breast cancer screening tools, including cancer detection, automated density assessment, and prioritized worklist capabilities.

- March 2026: GE HealthCare completed the acquisition of Intelerad, a leading medical imaging software provider, for USD 2.3 billion, expanding its reach into high-growth ambulatory care environments and accelerating its cloud-first, AI-enabled imaging strategy.

- March 2026: Viz.ai partnered with Alnylam Pharmaceuticals to launch an AI care pathway for cardiac amyloidosis, utilizing an FDA-cleared echocardiography AI algorithm to automatically flag subtle imaging findings and trigger coordinated diagnostic workflows across Viz.ai's 2,000+ hospital platform.

Global AI In Clinical Care Market Report Scope

As per the scope of the report, the AI in Clinical Care market comprises artificial intelligence solutions that support healthcare professionals in delivering patient care across diagnosis, treatment planning, clinical decision-making, patient monitoring, and workflow automation. These solutions use technologies such as machine learning, natural language processing (NLP), and computer vision to improve clinical accuracy, reduce administrative burden, and enhance patient outcomes. The market includes software, platforms, and AI-enabled clinical applications used by hospitals, clinics, health systems, and other healthcare providers.

The AI in clinical care are segmented by component, deployment mode, primary AI modality, application, end user, and geography. By component, the market is segmented into software and services. By deployment mode, the market is segmented into cloud-based and on-premise. By primary AI modality, the market is segmented into machine learning, natural language processing, computer vision, and generative AI. By application, the market is segmented into medical diagnosis, treatment planning and personalization, patient monitoring and early warning, alerts, reminders, and risk prediction, and others. By end user, the market is segmented into hospitals & clinics, research & academic institutes, pharmaceutical & biotechnology companies, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Machine Learning |

| Natural Language Processing |

| Computer Vision |

| Generative AI |

| Medical Diagnosis |

| Treatment Planning and Personalization |

| Patient Monitoring and Early Warning |

| Alerts, Reminders, and Risk Prediction |

| Others |

| Hospitals & Clinics |

| Research & Academic Institutes |

| Pharmaceutical & Biotechnology Companies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By Primary AI Modality | Machine Learning | |

| Natural Language Processing | ||

| Computer Vision | ||

| Generative AI | ||

| By Application | Medical Diagnosis | |

| Treatment Planning and Personalization | ||

| Patient Monitoring and Early Warning | ||

| Alerts, Reminders, and Risk Prediction | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Research & Academic Institutes | ||

| Pharmaceutical & Biotechnology Companies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is AI in clinical care expected to become by 2031?

The AI in clinical care market is forecast to reach USD 34.11 billion by 2031 from USD 12.44 billion in 2026, supported by a 22.35% CAGR over 2026-2031.

What is the main reason hospitals are adopting these tools now?

Hospitals are moving faster because AI now fits directly into EHR workflows, supports documentation, and helps reduce burnout and care variation.

Which component generates the most revenue today?

Software led with 72.34% share in 2025 because it scales easily across connected hospitals and matches subscription-based purchasing patterns.

Which area is growing fastest by application?

Treatment planning and personalization is projected to expand at 23.94% CAGR through 2031 as providers use AI to combine multimodal patient data into individualized care decisions.

Which end users are expanding fastest?

Pharmaceutical and biotechnology companies are projected to grow at 26.73% CAGR through 2031 as AI becomes more important in drug discovery, trial execution, and prescribing support.

Which region leads adoption and which grows fastest?

North America held the largest share at 39.47% in 2025, while Asia-Pacific is projected to record the fastest growth at 27.94% CAGR through 2031.

Page last updated on: