AI-Powered Diagnostic Radiogenomics Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.37 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 19.65% CAGR |

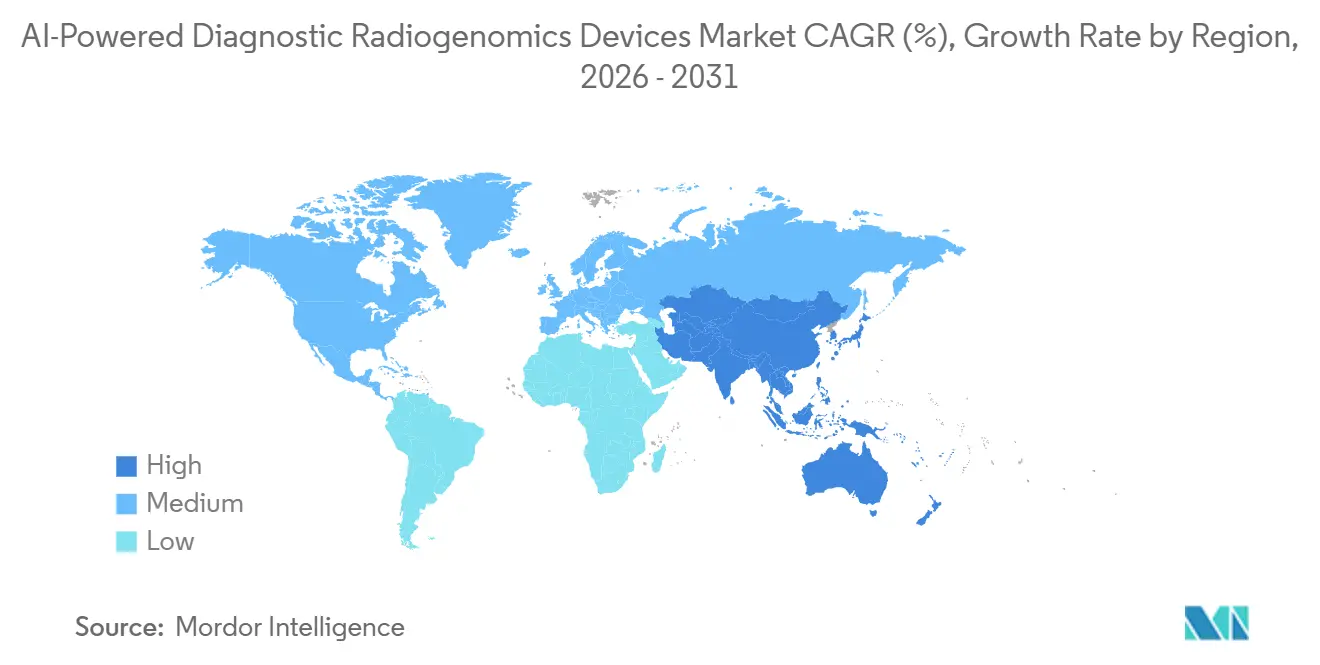

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

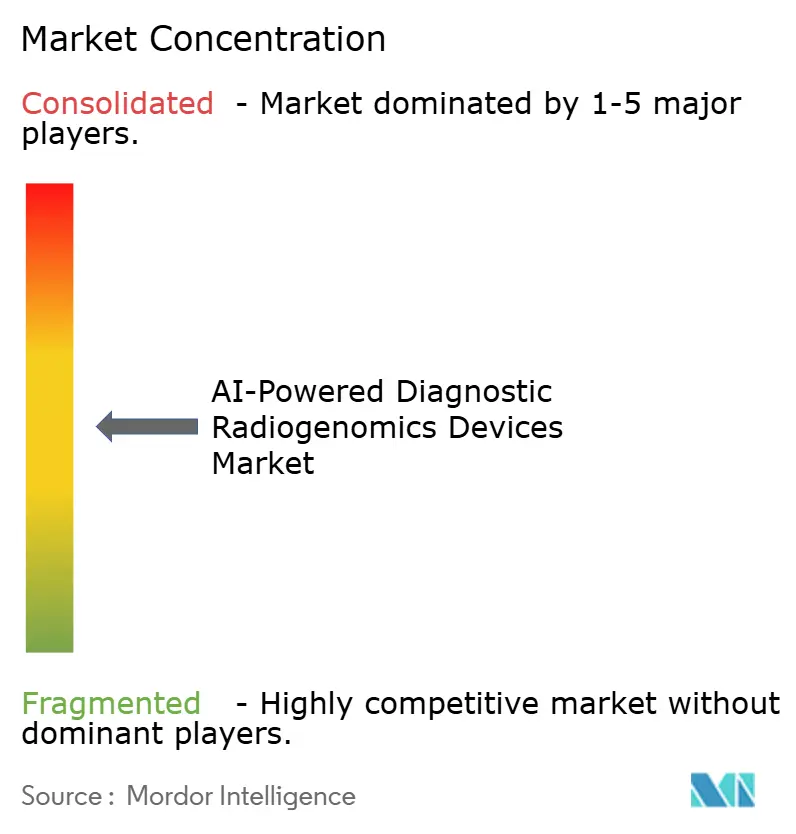

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Powered Diagnostic Radiogenomics Devices Market Analysis by Mordor Intelligence

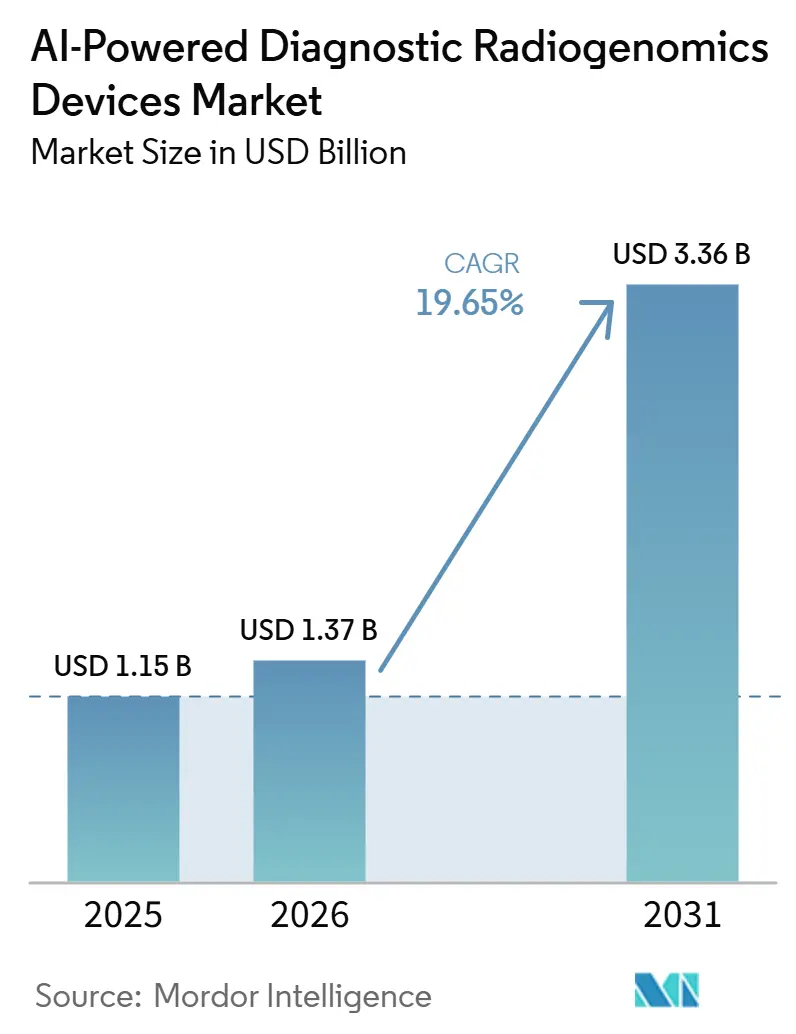

The AI-Powered Diagnostic Radiogenomics Devices Market size is projected to expand from USD 1.15 billion in 2025 and USD 1.37 billion in 2026 to USD 3.36 billion by 2031, registering a CAGR of 19.65% between 2026 to 2031.

Growth in the AI-powered diagnostic radiogenomics devices market is being shaped by the tighter link between genomic sequencing and image analysis, which is making noninvasive molecular assessment more practical in routine oncology workflows. Reported model performance of 85% to 92% in predicting common cancer mutations from imaging has strengthened clinical interest because it can shorten the path from scan review to treatment planning in settings where tissue access is limited. Demand is also widening beyond a narrow oncology use case because multimodal AI frameworks can now combine imaging, omics, and clinical records even when some patient data are incomplete, which lowers the deployment barrier for hospitals that do not yet have full genomics coverage. The competitive position of the AI-powered diagnostic radiogenomics devices market is increasingly tied to access to large linked imaging genomic datasets, because those data assets improve model training, support validation, and make later entrants harder to scale at the same pace. At the same time, growth in the AI-powered diagnostic radiogenomics devices market is still being checked by interoperability gaps across PACS, EHR, and omics systems and by reimbursement pathways that remain uneven for AI-enabled companion diagnostic use cases.

Key Report Takeaways

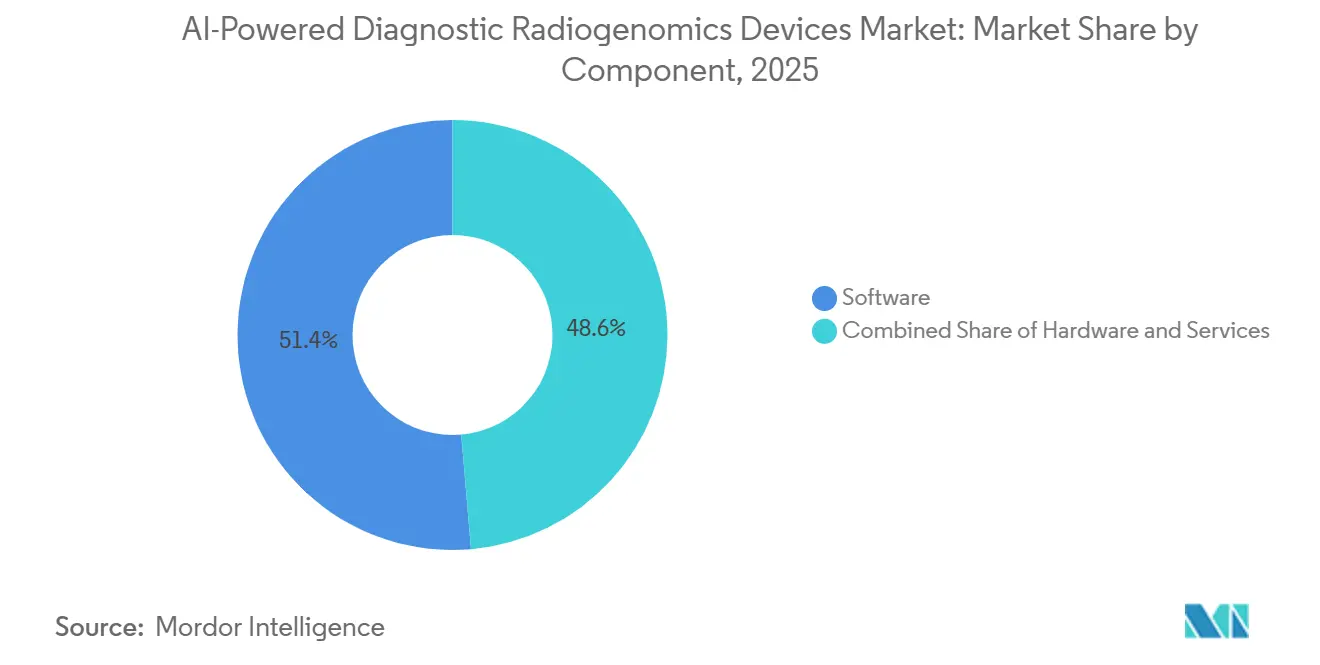

- By component, software held 51.38% share in 2025, while services is forecast to expand at a 23.87% CAGR through 2031.

- By imaging modality, MRI held 38.13% share in 2025, while multi-modal fusion is forecast to expand at a 24.15% CAGR through 2031.

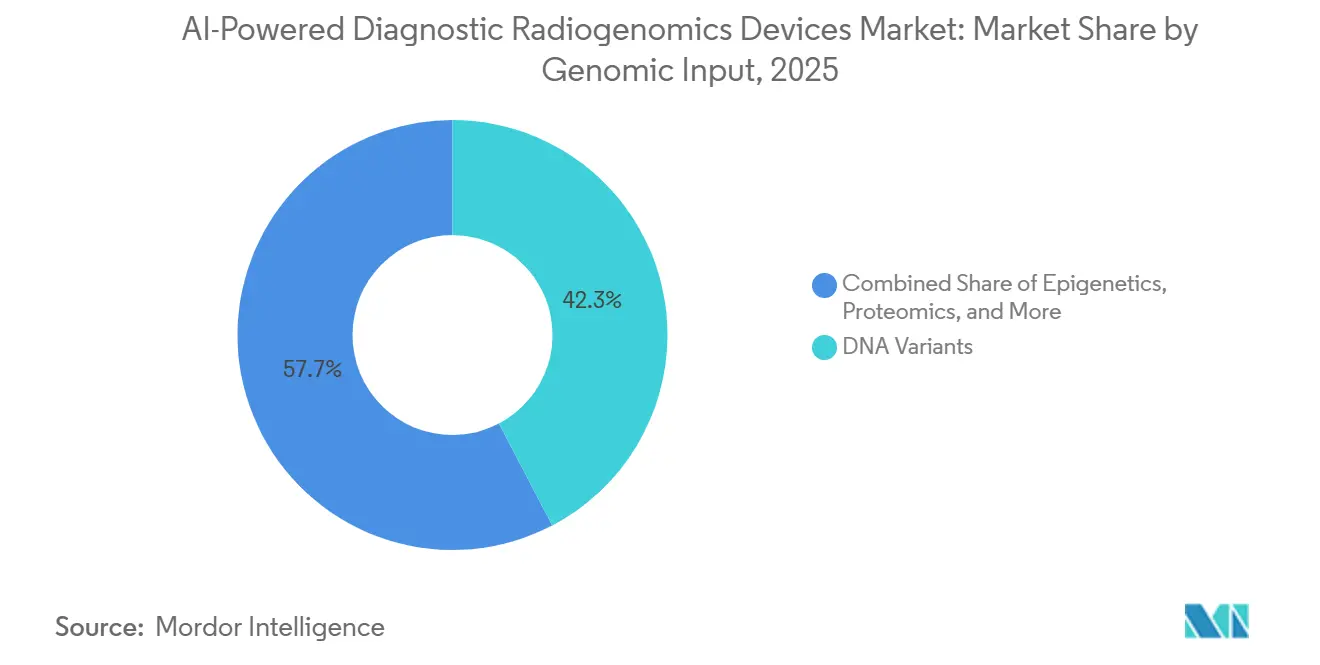

- By genomic input, DNA variants held 42.32% share in 2025, while liquid biopsy signals is forecast to expand at a 25.11% CAGR through 2031.

- By clinical application, mutation and biomarker status prediction held 34.16% share in 2025, while therapy response prediction and monitoring is forecast to expand at a 24.33% CAGR through 2031.

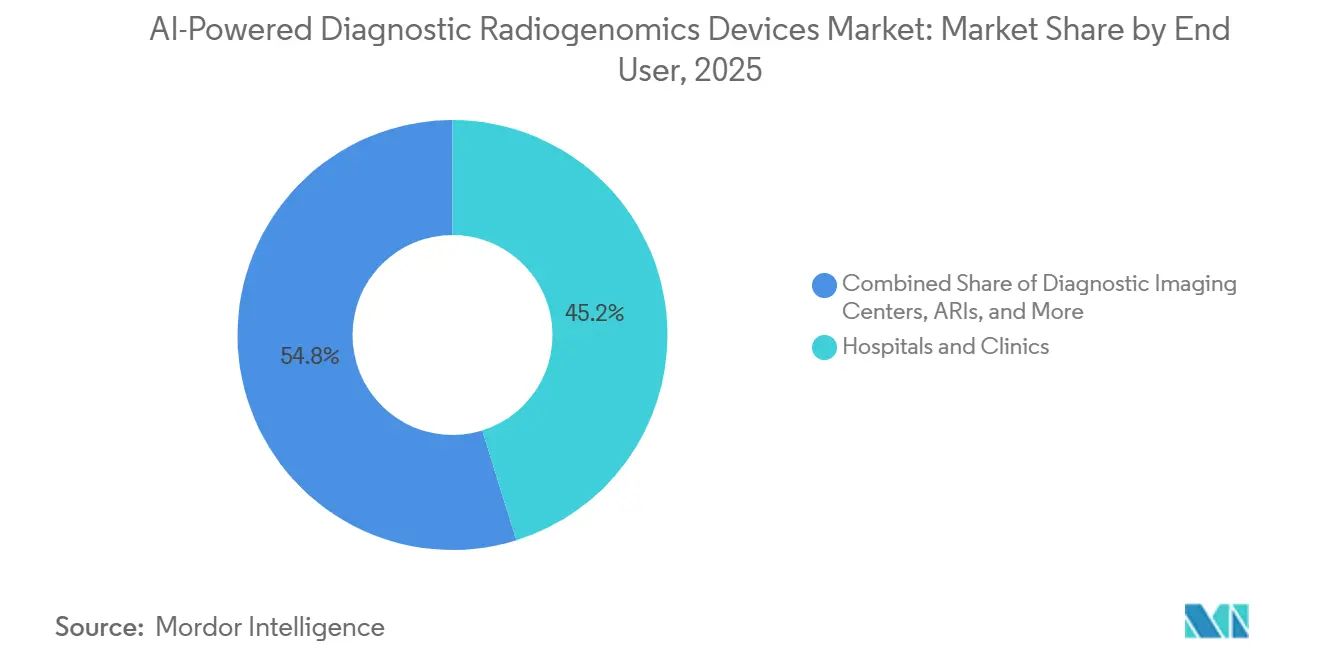

- By end user, hospitals and clinics held 45.19% share in 2025, while pharma, biotech, and CROs is forecast to expand at a 24.61% CAGR through 2031.

- By geography, North America held 44.64% share in 2025, while Asia-Pacific is forecast to expand at a 25.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Powered Diagnostic Radiogenomics Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Multimodal Precision Diagnostics | +5.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Expanding Oncology-First Clinical Use Cases | +3.5% | North America, Europe, APAC core, including Japan and South Korea | Medium term (2-4 years) |

| Increasing Hospital-Level AI Workflow Integration | +3.2% | Global, highest adoption velocity in North America | Medium term (2-4 years) |

| Growing Genomic Data Availability for Model Training | +2.5% | North America and APAC, with spillover to MEA through biobank partnerships | Medium term (2-4 years) |

| Wider Use in Therapy Response and Trial Stratification | +2.1% | North America, Europe, APAC core | Long term (≥ 4 years) |

| Cross-Validation Pressure From Explainability and Auditability | +1.4% | North America and EU, with early gains in Japan and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Multimodal Precision Diagnostics

The AI-powered diagnostic radiogenomics devices market is moving away from single-source analysis because clinicians increasingly want one workflow that can combine imaging, genomic, transcriptomic, proteomic, and patient record data. Multimodal AI systems are showing better performance in molecular subtype prediction and treatment response assessment than models built on one data type alone, which is making them more relevant for precision care pathways. A major shift is that these systems no longer depend on complete cross-modal data from every patient, because newer model designs can infer missing inputs from the data that are already available. That change is widening access for hospitals with partial genomics coverage, and it is bringing more institutions into the AI-powered diagnostic radiogenomics devices market without forcing them to rebuild their entire diagnostic pathway at once. The HONeYBEE framework also shows how modular embeddings across DNA methylation, gene expression, and somatic mutations can support lower-cost deployment at the institution level.[1]Nature Portfolio, “HONeYBEE, Enabling Scalable Multimodal AI in Oncology Through Foundation Model-Driven Embeddings,” npj Digital Medicine, nature.com As demand comes from oncology, neurology, and cardiovascular teams at the same time, the AI-powered diagnostic radiogenomics devices market is gaining a broader clinical base than a pure oncology tool set would normally deliver.

Expanding Oncology-First Clinical Use Cases

The AI-powered diagnostic radiogenomics devices market is still led by oncology, but the use case is moving past detection toward treatment selection, trial enrollment, and ongoing response assessment. Lunit presented data at AACR 2025 showing AI-based prediction of EGFR mutations in non-small cell lung cancer from stained tissue images, which supports faster early screening before full molecular workup is completed. Drug developers are helping push this adoption because they need biomarker-linked tools that can support companion diagnostic development and reduce uncertainty in patient selection. A registered 2026 ClinicalTrials.gov study in esophageal cancer shows that radiomics, pathomics, genomics, and other multi-omics layers are already being combined to predict treatment response and prognosis beyond the most established tumor settings. A 2025 hepatocellular carcinoma publication also showed that a machine learning radiogenomics biomarker could separate prognosis across major imaging modalities with a hazard ratio range of 1.415 to 1.890.[2]National Library of Medicine, “Radiogenomics Predicts Immune Microenvironment Heterogeneity and Response to Combination Immunotherapy in Hepatocellular Carcinoma,” PubMed, pubmed.ncbi.nlm.nih.gov As this indication set extends from lung, brain, and breast into GI, prostate, and hepatic cancers, the AI-powered diagnostic radiogenomics devices market gains revenue potential that is larger than a narrow mutation screening model would suggest.

Increasing Hospital-Level AI Workflow Integration

Hospital adoption in the AI-powered diagnostic radiogenomics devices market now depends less on standalone algorithm quality and more on whether the tool fits into day-to-day clinical operations. Aidoc stated in June 2026 that its clinical AI platform was active across nearly 2,000 hospitals and had analyzed more than 120 million patient cases, which shows how buyers are favoring platforms that can operate across multiple workflow steps instead of isolated reads.[3]Aidoc, “Aidoc Receives FDA Breakthrough Device Designation for AI That Drafts Radiology Reports,” Aidoc, aidoc.com The same announcement also highlighted FDA Breakthrough Device Designation for First Read, a tool that analyzes chest radiographs and drafts preliminary report text, which reflects growing acceptance of AI within the reporting workflow itself. The practical bottleneck remains system integration, because radiology information systems, PACS, EHRs, and genomic reporting layers often sit on different standards and demand ongoing IT support. Vendors that can support DICOM and HL7 FHIR aligned output reduce that burden and are better placed to win enterprise contracts in the AI-powered diagnostic radiogenomics devices market. This same pressure is helping services grow faster than hardware or one-time licensing, because hospitals want validation, monitoring, updates, and integration support bundled into one operational contract.

Growing Genomic Data Availability for Model Training

Training scale remains a core advantage in the AI-powered diagnostic radiogenomics devices market because model performance depends on large linked datasets rather than imaging volume alone. Tempus stated in January 2026 that Paige Predict was trained on a combined multimodal cohort of more than 200,000 patients and could predict 123 biomarkers and oncogenic pathways across 16 cancer types from whole-slide images. Tempus also reported expanded strategic agreements in May 2026 to build a larger multimodal oncology foundation model, which signals that companies are using data partnerships to widen both model scope and validation depth. SOPHiA GENETICS has followed a similar path through collaborations with MD Anderson, Mount Sinai, and Memorial Sloan Kettering, which strengthens both institutional reach and the volume of clinically useful oncology data. Academic centers are also adding to the training base, including work from the University of Tokyo on explainable AI for pathogenic structural genomic anomalies in cancer. This data advantage compounds over time because better-performing models attract more partners, and that cycle is reinforcing scale leadership across the AI-powered diagnostic radiogenomics devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Clinical-Grade Labelled Radiogenomics Datasets | -2.8% | Global, most acute in MEA and South America | Long term (≥ 4 years) |

| Interoperability Gaps Across PACS, EHR, and Omics Systems | -2.1% | Global, with particular severity in fragmented multi-system hospital environments | Medium term (2-4 years) |

| High Validation Burden for Multi-Site Regulatory Clearance | -1.8% | North America, Europe, Japan, with spillover to APAC | Long term (≥ 4 years) |

| Reimbursement Uncertainty for AI-Enabled Companion Diagnostics | -2.2% | North America and EU, with earlier gains in Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Clinical-Grade Labelled Radiogenomics Datasets

The AI-powered diagnostic radiogenomics devices market still faces a basic supply problem because high-quality labeled datasets that connect imaging features with confirmed molecular pathology remain scarce. Many current models are built on retrospective cohorts where imaging and genomic data were collected at different times and for different clinical purposes, which introduces noise and weakens transferability across sites. The issue is more severe for transcriptomic and proteomic layers, because those assays are not part of most routine imaging encounters and cannot be added retrospectively without extra cost. Federated learning helps by allowing model development across institutions without moving patient data, but it does not remove the challenge of inconsistent labels and uneven data quality. The European Cancer Imaging Initiative had connected 83 imaging datasets across 9 cancer types, covering 107,000 subjects by September 2025, which shows progress but still falls short of what broad clinical-grade generalization needs. Until prospective multimodal data collection becomes routine rather than research-led, this limitation will continue to cap model performance and slow scaling in the AI-powered diagnostic radiogenomics devices market.

Reimbursement Uncertainty for AI-Enabled Companion Diagnostics

Commercial adoption in the AI-powered diagnostic radiogenomics devices market is also limited by uneven reimbursement pathways for AI-enabled companion diagnostics. The problem is most visible in North America, where AI-based imaging outputs linked to genomic decision support still do not have one broadly resolved payment route across the care pathway. This creates a delay between technical validation and scalable use, because hospitals and imaging centers need billing clarity before they can expand deployment beyond pilots. Japan shows a more supportive example, where reimbursement for Illumina's TruSight Oncology Comprehensive cancer genomic profiling panel system became effective on June 1, 2026 and expanded access to clinical-grade genomic profiling that can feed AI-linked workflows. In Europe, the same issue is being shaped by tighter compliance expectations for high-risk medical AI, which means economic adoption and validation design are moving together rather than separately. As long as payer frameworks lag product capability, the AI-powered diagnostic radiogenomics devices market will continue to see slower conversion from clinical promise to routine budgeted use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Masking a Services-Led Revenue Shift

Software accounted for 51.38% of revenue in 2025, which made it the largest component in the AI-powered diagnostic radiogenomics devices market. That position reflects the central role of inference engines, model management layers, and clinical decision support platforms, because these elements sit at the point where imaging and genomic signals are turned into usable clinical output. The software lead also shows that buyers continue to prioritize flexible deployment over fixed equipment replacement, especially where hospitals already own core imaging assets. Even so, the product layer is becoming less exclusive as more open architectures and foundation model frameworks enter the field, which means simple access to an algorithm is no longer enough to protect margins in the AI-powered diagnostic radiogenomics devices market. The stronger differentiator is whether a vendor can place that software into a live hospital environment and keep it compliant, stable, and useful over time.

Services is projected to advance at a 23.87% CAGR through 2031, which makes it the fastest-growing component in the AI-powered diagnostic radiogenomics devices market. Hospitals are increasingly favoring managed contracts that cover validation, deployment, monitoring, and regulatory updates because those tasks stretch local IT and clinical operations teams. This shift matters because it moves value from the software license alone toward the full operating model that keeps multimodal AI functioning in routine care. Hardware remains important, especially where imaging OEMs embed AI acceleration and neural processing capabilities into MRI, CT, and PET systems, but its growth is slower because replacement cycles are longer and many AI functions can still be added through upgrades. In practical terms, the AI-powered diagnostic radiogenomics devices industry is moving toward service-backed platforms where revenue durability depends on integration depth rather than on one-time installation.

By Imaging Modality: MRI Anchors Revenue While Fusion Architectures Lift Growth

MRI held 38.13% share in 2025, which kept it as the leading modality in the AI-powered diagnostic radiogenomics devices market. Its lead comes from strong soft-tissue contrast and its established use in brain, prostate, and breast cancer workflows, where genomic correlation has clearer clinical relevance. These settings continue to support high-value use cases such as glioma mutation prediction, multiparametric prostate imaging, and breast lesion characterization. GE HealthCare presented Decipher-MR in 2026 as a clinical-grade 3D MRI foundation model trained on 200,000 MRI series, which underlines how MRI remains a major development focus for broad AI imaging applications.[4]European Commission, “European Cancer Imaging Initiative,” European Commission Digital Strategy, digital-strategy.europa.eu As a result, MRI still sets the revenue floor for the AI-powered diagnostic radiogenomics devices market even while other modalities expand around it.

Multi-modal fusion is forecast to grow at a 24.15% CAGR through 2031, which makes it the fastest-moving modality layer in the AI-powered diagnostic radiogenomics devices market. The key change is that clinically useful fusion no longer requires every data source to be acquired in the same session, because retrospective combination across timepoints is becoming more practical. That greatly increases the number of patients and institutions that can be included in AI workflows. Spanish work presented through VHIO showed that simultaneous PET and MRI can produce anatomical and functional tumor information that single modalities cannot replicate in prostate and hepatocellular carcinoma settings. CT, PET, ultrasound, and X-ray or mammography still contribute meaningful revenue, but fusion architectures are raising the clinical ceiling because they support richer radiomic phenotypes and closer links to genomic interpretation. This is where the AI-powered diagnostic radiogenomics devices industry is shifting from a modality-led structure toward a data-combination structure.

By Genomic Input: DNA Variants Lead While Liquid Biopsy Signals Accelerate

DNA variants captured 42.32% of revenue in 2025, giving this segment the largest position in the AI-powered diagnostic radiogenomics devices market. That leadership reflects stronger clinical validation and a more established role in mutation prediction for targets such as EGFR, IDH, and KRAS. The commercial logic is straightforward because DNA-based outputs are easier to connect with known therapeutic decisions and existing molecular pathology workflows. Published evidence in non-small cell lung cancer has shown that deep learning models can predict EGFR status from CT imaging with strong discriminative performance, helping reduce dependence on invasive tissue sampling in some patient groups. RNA expression, transcriptomics, epigenetics, and proteomics remain important sub-segments, but they depend more heavily on expanded assay use and wider routine access to multi-omics data.

Liquid biopsy signals are projected to expand at a 25.11% CAGR through 2031, which makes it the fastest-growing genomic input in the AI-powered diagnostic radiogenomics devices market. Its rise is tied to a different clinical value proposition, because it supports longitudinal monitoring rather than a one-time tissue snapshot. That matters in oncology settings where tumor evolution, treatment response, and recurrence risk change over time. A 2026 Journal of Liquid Biopsy study found that combining CT-based radiomics with ctDNA analysis improved prognostic stratification in advanced non-small cell lung cancer, with each modality helping offset the other's false-positive tendency. This combination makes liquid biopsy especially relevant to integrated platforms, because it strengthens the case for repeated noninvasive assessment rather than isolated molecular confirmation. Within segment-level reporting, liquid biopsy signals are one of the clearest examples where the AI-powered diagnostic radiogenomics devices market size is being lifted by a use case that expands with every follow-up point rather than at first diagnosis alone.

By Clinical Application: Biomarker Prediction Leads While Therapy Response Gains Pace

Mutation and biomarker status prediction held 34.16% share in 2025, making it the largest application in the AI-powered diagnostic radiogenomics devices market. It serves as the clearest commercial entry point because the value proposition is easy to understand, the clinical question is specific, and the benefit of reducing invasive biopsy is immediate for oncologists. That clarity has helped vendors secure adoption even when broader radiogenomics use cases are still under validation. Tumor detection, prognosis and survival risk stratification, and recurrence versus treatment effect discrimination all build on the same radiomic foundation, which means once one application is embedded, adjacent use cases become easier to add. This layered adoption pattern is helping the AI-powered diagnostic radiogenomics devices market deepen usage inside existing accounts rather than relying only on new customer acquisition.

Therapy response prediction and monitoring is forecast to grow at a 24.33% CAGR through 2031, which makes it the fastest-growing clinical application in the AI-powered diagnostic radiogenomics devices market. The opportunity is larger because this use case affects drug selection, timing, and continuation decisions across the course of care. Even so, hospitals are still cautious, because response prediction tools need prospective multi-site evidence before they can be embedded into standard treatment protocols. Findings presented by ECOG-ACRIN and Caris Life Sciences in December 2025 showed that combining imaging, clinical data, and molecular profiling improved prognostic information beyond tumor gene expression analysis alone in breast cancer. Trial patient selection is also becoming more relevant as pharmaceutical developers look for molecularly pre-qualified cohorts, although it is still earlier as a standalone revenue stream. At the application level, therapy response tools are where AI-powered diagnostic radiogenomics devices market share is likely to shift most visibly as evidence moves from pilot validation into routine care pathways.

By End User: Hospitals Lead While Pharma and CRO Demand Rises Faster

Hospitals and clinics held 45.19% share in 2025, which made them the largest end-user group in the AI-powered diagnostic radiogenomics devices market. Their lead reflects the installed base of imaging equipment, the concentration of oncology care, and the use of AI triage and detection tools as entry points to broader multimodal adoption. Hospitals also remain the place where imaging, pathology, and therapeutic decisions are most likely to be connected in one workflow, which makes them the natural first buyers for integrated radiogenomics systems. This shared position does not mean adoption is simple, because hospitals still face the heaviest burden around IT integration, validation governance, and workflow redesign. Even so, they continue to anchor volume and credibility in the AI-powered diagnostic radiogenomics devices market because successful deployment in a hospital setting becomes a reference point for the rest of the care network.

Pharma, biotech, and CROs are projected to grow at a 24.61% CAGR through 2031, making it the fastest-growing end-user segment in the AI-powered diagnostic radiogenomics devices market. These buyers use radiogenomics differently because their goal is to improve trial efficiency, refine inclusion criteria, and shorten companion diagnostic development timelines rather than support routine patient throughput. That makes them less constrained by local hospital workflow friction and more focused on biomarker yield, cohort quality, and reproducibility across sites. SOPHiA GENETICS expanded work with AstraZeneca around PIK3CA, AKT1, and PTEN testing in breast and prostate cancer, which illustrates how pharmaceutical demand is directly shaping vendor roadmaps. Academic and research institutes, biobanks, diagnostic imaging centers, and public health programs remain important supporting buyers. Still, pharma-linked demand is rising faster because it ties radiogenomics to both drug development and future commercial diagnostics. In end-user terms, the AI-powered diagnostic radiogenomics devices industry is broadening from hospital procurement toward a mixed demand base that includes research and clinical development budgets.

Geography Analysis

North America accounted for 44.64% of revenue in 2025, which gave it the largest regional position in the AI-powered diagnostic radiogenomics devices market. The region benefits from a dense concentration of academic cancer centers, established imaging infrastructure, and close collaboration between vendors and reference institutions. GE HealthCare and Mayo Clinic launched the MI-BET theranostics collaboration in July 2026, combining StarGuide SPECT/CT, MIM LesionID Pro, and blood-based biomarkers for advanced prostate cancer, which shows how imaging and biomarker integration are moving into high-priority treatment settings. Hospital networks in the United States also provide a favorable base for service-led deployment, because enterprise contracts can cover validation, reporting, and follow-up model management together. This keeps North America central to both product testing and commercial proof in the AI-powered diagnostic radiogenomics devices market.

Europe remained the second-largest region in the AI-powered diagnostic radiogenomics devices market, supported by coordinated imaging data programs and strong oncology research infrastructure. Germany's approval of low-dose CT lung cancer screening for statutory health insurance created a larger real-world setting for AI-assisted reading and biomarker extraction from April 2026 onward, as referenced in the supplied draft. At the same time, GDPR and EU AI Act requirements are pushing vendors toward privacy-preserving and more tightly governed deployment models, which can slow implementation but strengthen long-term trust.

Asia-Pacific is projected to expand at a 25.72% CAGR through 2031, making it the fastest-growing region in the AI-powered diagnostic radiogenomics devices market. Japan stands out because reimbursement for Illumina's TruSight Oncology Comprehensive system took effect on June 1, 2026, which broadens access to genomic profiling that can feed AI-supported oncology workflows. Japan is also contributing to explainable genomic AI through work at the University of Tokyo on structural anomaly interpretation in cancer genomes. China offers scale because AI imaging is being used to address radiologist shortages and uneven access between urban and rural settings. At the same time, South Korea continues to build export-facing oncology imaging capability through its AI companies. South America, the Middle East, and Africa are still early-stage markets. Still, public health programs, biobank partnerships, and national genomics institutes are gradually creating entry points for the AI-powered diagnostic radiogenomics devices market. Across geography, the AI-powered diagnostic radiogenomics devices market size is becoming more evenly influenced by policy support, data availability, and workflow readiness rather than by imaging infrastructure alone.

Competitive Landscape

The AI-powered diagnostic radiogenomics devices market remains moderately fragmented. Still, the direction of competition is becoming clearer as vendors build durable positions through data access, workflow integration, and institutional partnerships. Large imaging and diagnostics groups compete with AI-native specialists. Yet, the strongest positions are forming around platforms that can connect imaging, pathology, and genomic interpretation rather than around one device type alone. This means the AI-powered diagnostic radiogenomics devices market is not consolidating around a single technical feature, because no single layer fully controls clinical adoption. Instead, companies are strengthening their place through combinations of software depth, research partnerships, and service capability. The field is moving toward a platform contest where the value of a product depends on how much of the diagnostic pathway it can influence.

Several companies have already made strategic moves that show how this competition is developing in the AI-powered diagnostic radiogenomics devices market. GE HealthCare's July 2026 Mayo Clinic collaboration tied imaging hardware, lesion analysis, and blood-based biomarkers into one theranostics trial, which supports the company's effort to stay relevant beyond image acquisition alone. Aidoc's June 2026 Breakthrough Device Designation for First Read showed another route, where a workflow-focused company is extending its role from prioritization into preliminary reporting and broader operational integration. SOPHiA GENETICS deepened its U.S. oncology footprint through collaborations with MD Anderson, Mount Sinai, and Memorial Sloan Kettering, which strengthens its data access and validation network at the same time. Tempus has also moved to expand its multimodal foundation model position through broader strategic agreements in oncology, reinforcing the role of data scale and partnership depth in the AI-powered diagnostic radiogenomics devices market.

Competitive openings still exist in the AI-powered diagnostic radiogenomics devices market, especially in rare cancer workflows, real-world evidence services, and cost-sensitive deployments where cloud-heavy models are harder to support. Vendors that can produce strong multi-site validation without relying on the largest proprietary datasets may still win share in specialized indications. Explainability, auditability, and device classification rules are also becoming more important because they influence how easily hospitals can trust and govern these systems over time. The June 2026 Federal Register classification of radiological machine learning-based quantitative imaging software adds a clearer regulatory baseline, which favors companies with stronger quality and submission capability. Overall, the AI-powered diagnostic radiogenomics devices market is still open enough for specialist entrants. Still, the barriers are rising fastest around linked data ownership, institutional credibility, and the ability to operate at the workflow level rather than the algorithm level.

AI-Powered Diagnostic Radiogenomics Devices Industry Leaders

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Siemens Healthineers AG

Tempus AI, Inc.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: GE HealthCare and Mayo Clinic launched the MI-BET (Molecular Imaging Biomarker-Based End of Therapy Trial) theranostics research collaboration, combining StarGuide SPECT/CT and MIM LesionID Pro with blood-based biomarkers to personalize radioligand therapy for advanced prostate cancer, the first multi-modality biomarker-imaging adaptive treatment trial of this scope at a US institution.

- June 2026: Aidoc received FDA Breakthrough Device Designation for First Read, its AI that analyzes chest radiographs and auto-generates preliminary radiology reports, its second BDD in under 12 months, building on a platform deployed across nearly 2,000 hospitals that had analyzed over 120 million cases. The company also disclosed a USD 150 million Series E financing.

- June 2026: SOPHiA GENETICS signed an MOU with Memorial Sloan Kettering Cancer Center to form a joint venture aimed at building a next-generation precision oncology hub, leveraging the SOPHiA DDM Platform for AI and bioinformatics and MSK's clinical and scientific leadership, extending SOPHiA's US academic anchor network to a third major cancer center within six months.

- June 2026: Japan's National Health Insurance approved reimbursement for Illumina's TruSight Oncology Comprehensive cancer genomic profiling panel system, one of the most significant payer coverage decisions for integrated genomic profiling in Asia, effective June 1, 2026, expanding clinical-grade genomic data availability for AI radiogenomics workflows.

- April 2026: SOPHiA GENETICS and Mount Sinai Health System announced collaboration at AACR 2026, with Mount Sinai adopting the SOPHiA DDM Platform for cancer research and genomic testing, its third major US academic partnership in four months, establishing a significant institutional data network in US oncology.

Global AI-Powered Diagnostic Radiogenomics Devices Market Report Scope

The AI-Powered Diagnostic Radiogenomics Devices Market comprises advanced diagnostic solutions that integrate artificial intelligence with radiogenomics to correlate medical imaging data with genomic and molecular profiles for improved disease characterization and clinical decision-making. These systems leverage machine learning and advanced image analytics to identify imaging biomarkers, predict genetic alterations, and support personalized diagnosis and treatment planning. The market is driven by the growing adoption of precision medicine, increasing use of AI in medical imaging, and rising demand for non-invasive, data-driven diagnostic approaches across oncology and other complex diseases.

The AI-powered diagnostic radiogenomics devices market is segmented by component, imaging modality, genomic input, clinical application, end user, and geography. By component, it is further divided into hardware, software, and services. By imaging modality, it is segmented into MRI, CT, PET, ultrasound, X-Ray, and mammography, and multi-modal fusion. By genomic input, the market is segmented into DNA variants, RNA expression and transcriptomics, epigenetics, proteomics, and liquid biopsy signals. By clinical application, the market is segmented intoMutation and biomarker status prediction, tumor detection, prognosis and survival risk stratification, therapy response prediction and monitoring, recurrence versus treatment effect discrimination, and patient selection for trials. By end user, the market is segmented into hospitals and clinics, diagnostic imaging centers, academic and research institutes and biobanks, pharma and biotech and CROs, and government and public health programs. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Hardware |

| Software |

| Services |

| MRI |

| CT |

| PET |

| Ultrasound |

| X-Ray and Mammography |

| Multi-Modal Fusion |

| DNA Variants |

| RNA Expression and Transcriptomics |

| Epigenetics |

| Proteomics |

| Liquid Biopsy Signals |

| Mutation and Biomarker Status Prediction |

| Tumor Detection |

| Prognosis and Survival Risk Stratification |

| Therapy Response Prediction and Monitoring |

| Recurrence Versus Treatment Effect Discrimination |

| Patient Selection for Trials |

| Hospitals and Clinics |

| Diagnostic Imaging Centers |

| Academic and Research Institutes and Biobanks |

| Pharma and Biotech and CROs |

| Government and Public Health Programs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Imaging Modality | MRI | |

| CT | ||

| PET | ||

| Ultrasound | ||

| X-Ray and Mammography | ||

| Multi-Modal Fusion | ||

| By Genomic Input | DNA Variants | |

| RNA Expression and Transcriptomics | ||

| Epigenetics | ||

| Proteomics | ||

| Liquid Biopsy Signals | ||

| By Clinical Application | Mutation and Biomarker Status Prediction | |

| Tumor Detection | ||

| Prognosis and Survival Risk Stratification | ||

| Therapy Response Prediction and Monitoring | ||

| Recurrence Versus Treatment Effect Discrimination | ||

| Patient Selection for Trials | ||

| By End User | Hospitals and Clinics | |

| Diagnostic Imaging Centers | ||

| Academic and Research Institutes and Biobanks | ||

| Pharma and Biotech and CROs | ||

| Government and Public Health Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the AI-powered diagnostic radiogenomics devices space?

The sector stands at USD 1.37 billion in 2026 and is forecast to reach USD 3.36 billion by 2031 at a 19.65% CAGR.

Which component leads revenue and which one is growing fastest?

Software led with a 51.38% share in 2025, while services is the fastest-growing component with a 23.87% CAGR through 2031.

Which imaging modality has the strongest current position?

MRI held the largest modality share at 38.13% in 2025 because of its strong role in brain, prostate, and breast cancer workflows.

Why is liquid biopsy becoming more important in radiogenomics?

Liquid biopsy signals is projected to grow at a 25.11% CAGR because it supports longitudinal tumor monitoring and improves value when paired with radiomics.

Which region is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing region with a 25.72% CAGR, supported by reimbursement progress in Japan and broad AI imaging deployment momentum across major markets.

What is the main commercial barrier to wider adoption?

Reimbursement uncertainty and weak interoperability remain the main barriers because hospitals need billing clarity and smooth integration across imaging, EHR, and omics systems before scaling deployment.

Page last updated on: