AI In Patient Care And Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.45 Billion |

| Market Size (2031) | USD 6.22 Billion |

| Growth Rate (2026 - 2031) | 20.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Patient Care And Management Market Analysis by Mordor Intelligence

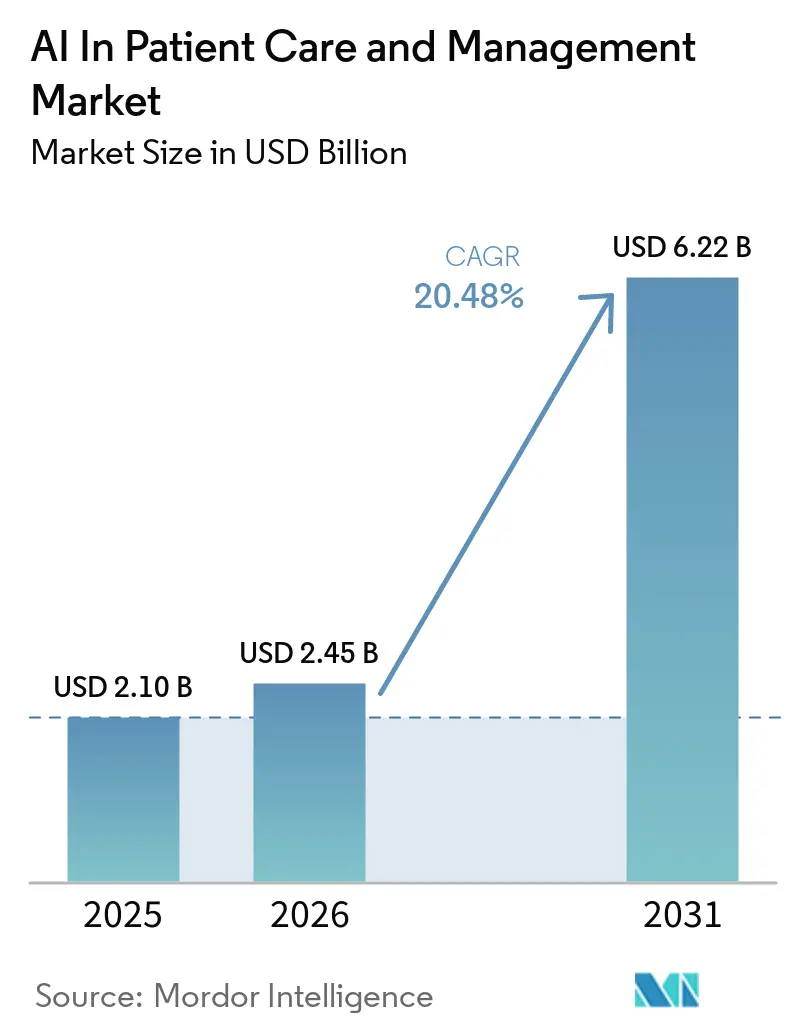

The AI in Patient Care and Management market size is expected to grow from USD 2.10 billion in 2025 to USD 2.45 billion in 2026 and is forecast to reach USD 6.22 billion by 2031 at 20.48% CAGR over 2026-2031. The market is shifting from pilots to enterprise-scale automation as hospitals and payers standardize workflows for intake, triage, documentation, and member services. Regulatory milestones in the United States, including operational provisions of the CMS Interoperability and Prior Authorization rule in 2026 with full payer APIs due in 2027, are unlocking structured data access and time-bound decisions that AI systems can automate at scale. National network connectivity under TEFCA expanded record exchange to a multi-hundred-million scale in 2025, which strengthens the data liquidity that AI assistants and analytics require to add value across care settings. Maturing FHIR-based integration is lowering barriers for third-party developers embedding patient engagement and documentation tools directly in EHR workflows. Persistent staffing gaps are pushing health systems to adopt ambient scribing and automated front-office workflows that compress documentation time and reduce manual tasks for care teams.

Key Report Takeaways

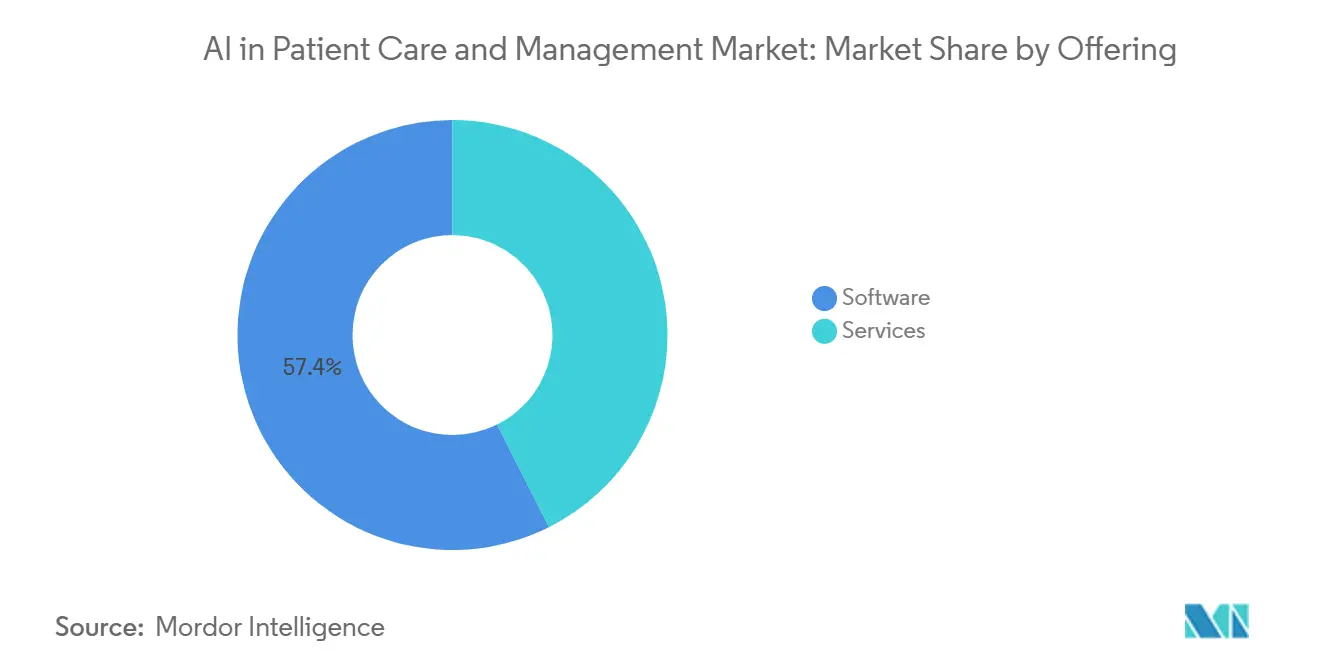

- By offering, software led with 57.42% revenue share in 2025, and software is projected to expand at a 22.34% CAGR through 2031.

- By deployment mode, cloud accounted for 45.34% share in 2025, while hybrid architectures are projected to grow at a 21.65% CAGR over 2026-2031.

- By technology, natural language processing held 39.62% share in 2025, and chatbots or conversational agents are expected to post the fastest growth at a 24.33% CAGR.

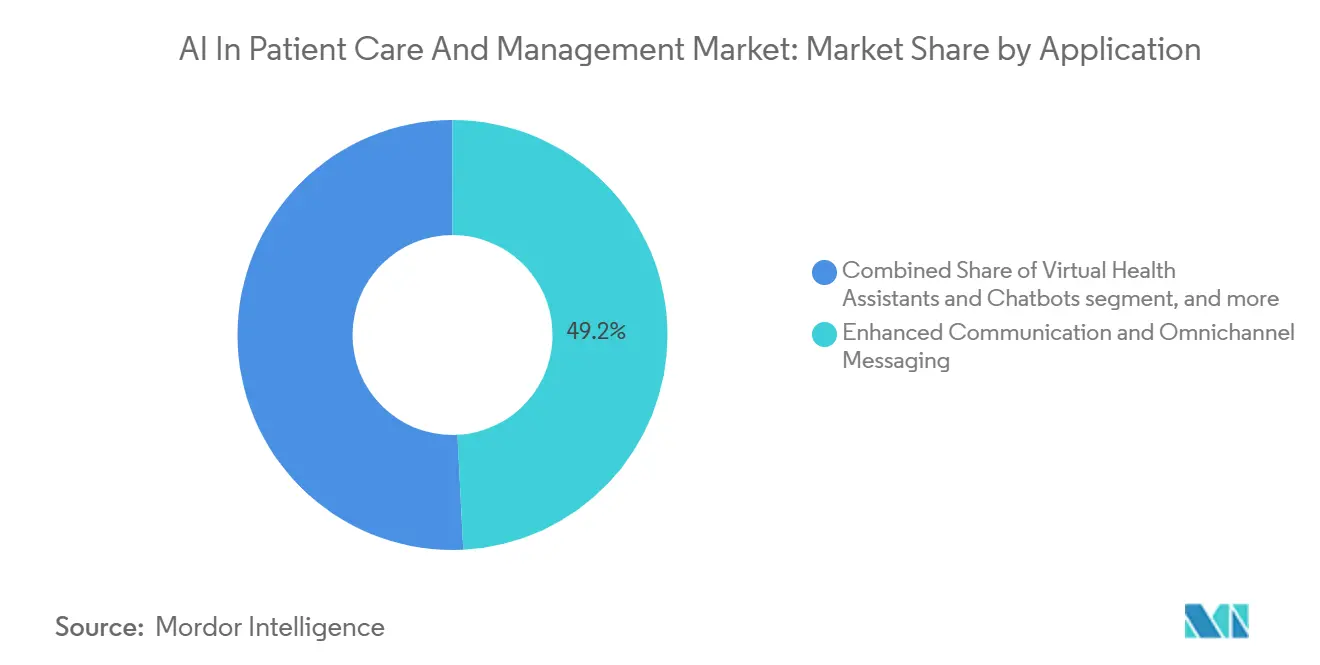

- By application, enhanced communication and omnichannel messaging commanded 49.23% share in 2025, while virtual health assistants and chatbots are set to expand at a 23.55% CAGR over 2026-2031.

- By end user, healthcare providers led with 47.44% share in 2025, and healthcare payers are forecast to grow the fastest at a 21.86% CAGR.

- By geography, North America contributed 48.26% share in 2025, while Asia-Pacific is expected to record the highest growth at a 23.37% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Patient Care And Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CMS Interoperability and Prior Authorization APIs Accelerate Digital Patient Access and Status Automation | +4.2% | North America core, spill-over to EU payer systems | Medium term (2-4 years) |

| Rising Consumer Adoption of Virtual Care and Preference for 24/7 Self-Service Digital Front Doors | +3.8% | Global, early gains in US metropolitan, Singapore, Australia | Short term (≤ 2 years) |

| Acute Healthcare Labor Shortages Push Automation of Front Desk and Contact-Center Workflows | +5.1% | North America & EU, acute in rural US markets | Medium term (2-4 years) |

| Growth in Patient Portal Usage and FHIR APIs Enables Personalized AI Assistants | +3.5% | North America, Singapore, Australia | Medium term (2-4 years) |

| On-Device and Privacy-Preserving AI Enables PHI-Safe Assistants in Apps and Kiosks | +2.1% | EU (GDPR-sensitive markets), US privacy-forward segments | Long term (≥ 4 years) |

| TEFCA-Enabled National Exchange Improves Record Location and Identity Matching for Assistants | +1.7% | US national, pilots in select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CMS Interoperability and Prior Authorization APIs Accelerate Digital Patient Access and Status Automation

The CMS Interoperability and Prior Authorization Final Rule requires impacted payers to stand up FHIR-based Patient Access, Provider Access, Payer-to-Payer, and Prior Authorization APIs, with operational provisions live on January 1, 2026 and full API compliance by January 1, 2027. The rule introduces firm turnaround times for prior authorization, including a seven-day standard decision window and reporting obligations that increase transparency and accountability. These provisions transform prior authorization from a manual and opaque process into a dataset that AI agents can query, pre-populate, and monitor, which reduces back-and-forth communications and shrinks call volumes. Patient-facing assistants gain new value when prior authorization status becomes accessible through the Patient Access API, since members can self-serve updates rather than wait for callbacks. Industry surveys in 2025 showed a slow start on implementation for many payers and providers, which points to a ramp that intensifies through 2027 as APIs stabilize across networks.[1]Centers for Medicare & Medicaid Services, “CMS Interoperability and Prior Authorization Final Rule (CMS-0057-F),” Centers for Medicare & Medicaid Services, cms.gov As these APIs scale, the AI in Patient Care and Management market benefits from lower friction in accessing structured data that supports timely automation of eligibility checks, documentation assembly, and status notifications.

Rising Consumer Adoption of Virtual Care and Preference for 24/7 Self-Service Digital Front Doors

Consumer expectations for always-on engagement are spilling into healthcare, and virtual touchpoints are becoming the default entry for scheduling, messaging, and triage. Hospitals expanded secure messaging and electronic access capabilities through 2024, which laid the groundwork for scalable digital front doors that integrate with AI chatbots and intake tools. Providers deploying after-hours digital scheduling and multi-channel reminders report stronger appointment capture and fewer no-shows as automated outreach meets patients on their preferred channels.[2]Isaac Correa, “Digital Front Door in Healthcare: Strategy Guide 2025,” Hellomatik, hellomatik.comSoutheast Asian hospitals have also rolled out WhatsApp-based virtual assistants for booking and patient navigation, showing how conversational interfaces can match regional communication habits. On the supply side, virtual urgent care has continued to evolve with platform upgrades that emphasize 24/7 availability and faster resolution, which reinforces consumer habits that favor immediate access. These factors widen the addressable surface for the AI in Patient Care and Management market as providers and payers align their engagement models with real-time digital expectations.

Acute Healthcare Labor Shortages Push Automation of Front Desk and Contact-Center Workflows

Time savings from ambient documentation and AI-powered intake are becoming practical levers for increasing capacity without expanding headcount. Clinics using AI scribes and workflow automation report meaningful reductions in documentation time per encounter, which allows clinicians to redirect minutes toward patient care during the day.[3]Groovy Web Team, “AI Chatbots in Healthcare in 2026: Transform Patient Engagement & Reduce Costs,” Groovy Web, groovyweb.coPractices applying scheduling and intake automation report measurable weekly hour savings at the front desk, which compounds across multi-location organizations managing higher patient volumes. Workforce tools now embed AI to predict staffing needs and autofill shifts, which reduces administrative burden for frontline leaders and curbs overtime spending. As change management and integration patterns mature, these use cases are reaching enterprise scale, particularly where EHR write-back and secure messaging are already in place. The shift from pilots to standardized automation creates predictable payback periods, which improves budget confidence for clinical leaders and CFOs. These operational dynamics support expansion of the AI in Patient Care and Management market as organizations target repetitive tasks that can be reliably automated across clinics and service lines.

TEFCA-Enabled National Exchange Improves Record Location and Identity Matching for Assistants

Record exchange at national scale improves AI’s ability to assemble longitudinal views of a patient’s history at the point of need. TEFCA established common policies and connectivity that replace hundreds of bilateral agreements, which simplifies how systems discover and request records across regions.[4]Steven Posnack, “TEFCA Priorities and Plans for the Remainder of 2025,” Office of the National Coordinator for Health Information Technology, healthit.gov The emergence of Qualified Health Information Networks and expansion of use cases are building the foundation for cross-network record location and identity matching, both of which are critical for AI tools that need context beyond a single EHR. ONC updates through 2025 highlighted progress on FHIR-based query pilots and interoperability priorities that strengthen the data backbone for digital assistants and care coordination tools. As more participants connect, AI agents can reduce duplicate testing, surface historical imaging or labs, and deliver more accurate triage based on comprehensive histories. Federal agencies and large systems joining TEFCA signal a move toward broad utility that extends beyond treatment-only scenarios, which will support a wider set of automated workflows over time. This maturing exchange fabric expands the reachable data for the AI in Patient Care and Management market, which improves assistant accuracy and trust for both clinicians and patients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Risk AI Compliance and Privacy Obligations (EU AI Act, HIPAA) Raise Implementation Costs | -3.2% | EU (high), US healthcare (moderate), global MedTech | Short term (≤ 2 years) |

| Safety, Hallucinations, and Validation Burdens Slow Deployment in Patient-Facing Use Cases | -2.8% | Global, acute in US malpractice-sensitive markets | Medium term (2-4 years) |

| EHR Integration Complexity and Vendor Gating Increase Time-To-Value | -2.5% | North America, Europe | Medium term (2-4 years) |

| A2P SMS 10DLC Registration and Carrier Filtering Reduce Outreach Deliverability | -0.9% | US national, potential RCS extension | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EHR Integration Complexity and Vendor Gating Increase Time-To-Value

The gap between standards availability and operational deployment remains a bottleneck, which slows the pace at which AI applications can go live inside production EHR workflows. Industry surveys in 2025 indicated that a large share of payers and providers had yet to start required API implementations, which underscores the distance between policy goals and technical reality. Even where FHIR R4 support is present, access occurs through governed APIs with scopes, rate limits, and consent metadata that AI vendors must design around, which adds engineering complexity and lengthens testing cycles. Health IT buyers also apply strict marketplace approvals and workflow validation, which can require months of joint testing to ensure safe embedding in clinician tools. Organizations planning comprehensive interoperability rollouts estimate multi-month timelines and significant direct costs, and they reserve budget for ongoing maintenance and vendor management. These factors favor partners with proven integration tooling and governance, which shapes procurement toward vendors that can demonstrate safe EHR write-back and audit trails. The result is a slower and more resource-intensive path to value for new AI entrants, which can delay wider benefits for the AI in Patient Care and Management market.

A2P SMS 10DLC Registration and Carrier Filtering Reduce Outreach Deliverability

Carriers now block unregistered A2P 10DLC traffic, which forces all automated SMS programs to complete brand and campaign registration before launch. Registration involves fees and review windows, and throughput is tied to trust scores that limit daily sending capacity for new or small brands. Content filtering algorithms compare live traffic to approved samples, and deviations can be silently dropped, which creates operational risk for clinics that rely on SMS for reminders or triage notifications. Compliance obligations remain high because healthcare messages must satisfy TCPA standards and use HIPAA-eligible providers, with clear opt-in flows and content restrictions that exclude marketing inside transactional threads. Per-message carrier surcharges and content penalties add financial risk, while deliverability ceilings reduce the reach of SMS-first engagement programs even after registration. RCS rollouts may create alternatives with richer media support in 2026, but verification rules and registration steps will likely mirror 10DLC, which limits how quickly organizations can pivot channels. These constraints affect patient outreach at scale, which nudges adoption toward portal messaging and in-app assistants that operate within authenticated channels for the AI in Patient Care and Management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Ascendancy Driven by Platform Consolidation Economics

Software accounted for 57.42% in 2025 and is projected to lead growth at a 22.34% CAGR through 2031, reflecting a shift to unified platforms that bundle intake, triage, engagement, and documentation under a single governance model for the AI in Patient Care and Management market. Health systems are consolidating vendors to streamline security reviews and simplify contracting, which reduces integration risk and lowers the indirect costs tied to managing multiple point tools across similar workflows. Platform providers now package ambient documentation, EHR search, and patient messaging in one stack, which reduces handoffs and speeds time-to-value for clinical teams that need end-to-end automation. Salesforce announced new Agentforce Health agents that integrate medical histories and device data to automate tasks across referral triage and engagement, which illustrates how software vendors are shipping multi-agent capabilities as part of broader suites. Microsoft expanded healthcare tooling that streamlines triage and prior authorization operations, which strengthens the software core that customers can activate without standing up extensive custom builds. Oracle launched an AI Center of Excellence for healthcare to accelerate embedded use cases across its customer base, which aligns with the consolidation trend as EHR-aligned platforms bring AI natively into clinical workflows. These moves reflect the center of gravity in the AI in Patient Care and Management market as buyers prefer fewer, deeper software relationships that connect clinical and operational teams to one data and orchestration layer.

The AI in Patient Care and Management industry still uses services for complex integration, data governance, and model-risk management, yet code-light configuration now covers many common tasks. EHR marketplaces and secure connectors shorten deployment cycles for standard features, which reduces reliance on large implementation projects for front-office and documentation flows. Platform roadmaps emphasize compliance guardrails and explainability for clinical adoption, which supports growth in hospital and payer settings that require auditable changes. Software-led automation also scales across service lines once initial templates are proven, which compounds return on investment across multi-specialty provider groups. As a result, software increases its strategic importance as buyers seek multi-year partners with interoperable suites that reduce workflow fragmentation in the AI in Patient Care and Management market.

By Deployment Mode: Hybrid’s Rapid Rise Balances Sovereignty with Scalability

Cloud held 45.34% in 2025 and hybrid is projected to grow at a 21.65% CAGR through 2031 as organizations combine on-premise control with elastic cloud inference. This pattern aligns with PHI stewardship goals while preserving access to state-of-the-art models delivered as managed services in cloud environments. Customers use cloud services for language and search while they pre-process prompts on-premise to minimize PHI exposure, which balances privacy with the need for scale. Microsoft’s healthcare-specific tooling illustrates how managed services provide secure model access and workflow components without building everything in-house. Oracle’s focus on embedded AI patterns shows how EHR vendors are enabling inference wrapped in clinical context, which reduces the lift for hospital IT teams. These approaches support migration paths that move sensitive workloads behind the firewall and burst compute-heavy tasks to the cloud. In this model, the AI in Patient Care and Management market reinforces security posture while retaining the option to use new capabilities as they are released by cloud providers.

Hybrid topologies also help with EHR integration, since local services can handle identity, consent, and write-back using hospital policies, while cloud models process de-identified context. The resulting pattern allows IT to set guardrails, manage traffic spikes, and audit events without constraining teams to on-premise-only deployments. Many buyers adopt hybrid incrementally, starting with ambient scribing and messaging assistants where model calls are stateless and auditable. As organizations prove success in one department, they extend the same infrastructure to additional use cases such as intake and referral management. Over time, hybrid becomes the default for larger health systems that must meet security and performance targets while keeping access to the latest capabilities in the AI in Patient Care and Management market.

By Technology: NLP’s Current Lead Cedes Growth Momentum to Conversational Agents

Natural language processing accounted for 39.62% in 2025 and conversational agents are projected to grow at a 24.33% CAGR as patient-facing and staff-facing chat expands the reachable use cases in the AI in Patient Care and Management market. NLP underpins ambient documentation and EHR data extraction, which remain high-volume tasks with clear productivity gains. Conversational interfaces add memory, turn-taking, and task orchestration that support multi-step flows, including intake, scheduling, benefits questions, and care-plan coaching. Tooling from hyperscalers is making these patterns more accessible through packaged components tailored for healthcare triage and administrative tasks. Oracle’s embedded AI initiatives align with this trend as they bring language models into clinical contexts that clinicians already use. These developments help conversational agents handle more complex requests while preserving auditability and safety checks.

Predictive analytics continues to mature in parallel, with vendors reporting stronger performance on readmission and resource optimization tasks as data pipelines improve. Kumo.ai highlights case studies that show improvements in classification performance for patient risk modeling, which supports care management programs when paired with human review. Customer adoption patterns often start with language-based workflows and expand to forecasting once data readiness grows. As integration and governance stabilize, providers and payers bring conversational, NLP, and predictive components together into unified assistants. This integration reflects a broader move toward care orchestration platforms that combine these technologies in one governed environment for the AI in Patient Care and Management industry.

By Application: Virtual Assistants Overtake Communication as Growth Frontier

Enhanced communication and omnichannel messaging accounted for 49.23% in 2025 as organizations continued to scale reminder systems, secure messaging, and portal outreach for the AI in Patient Care and Management market. Hospitals expanded patient engagement capabilities through 2024, which improved the baseline for secure messaging and record access that modern assistants can build upon. Virtual assistants and chatbots are set to outgrow communications at a 23.55% CAGR because bidirectional interactions handle triage, scheduling, coverage questions, and care navigation. Vendors are productizing these assistants as packaged agents that combine knowledge retrieval, task execution, and handoffs to staff when necessary. Teladoc’s continuous updates to 24/7 virtual urgent care show how assistants operate within clinician-led workflows to route patients and resolve common issues quickly. These shifts expand the AI in Patient Care and Management market as more value moves from one-way messages to guided conversations that complete tasks in context.

The AI in Patient Care and Management market size for virtual assistant use cases is projected to expand in line with the 23.55% CAGR where deployments focus on triage, benefits questions, and intake form capture. Hospitals are blending conversational flows with structured intake data to remove redundant forms and reduce front-desk workload, which improves patient experience during check-in. Tools that route to care also reduce misdirected visits by pointing patients to the right site of care, which saves time and reduces costs for both patients and providers. As assistants integrate with appointment books, eligibility checks, and EHR messaging, they become the front door for many common interactions. Communication platforms still matter for reach, yet their incremental gains now come from personalization and timing rather than new deployments. The long-term arc points to assistants as the growth frontier within the AI in Patient Care and Management market as organizations replace static menus with conversational navigation.

By End User: Healthcare Payers’ Regulatory Mandate Accelerates AI Adoption Velocity

Healthcare providers held 47.44% in 2025, while payers are projected to grow fastest at a 21.86% CAGR as regulatory timelines create operational deadlines for automation in the AI in Patient Care and Management market. The CMS Interoperability and Prior Authorization rule sets specific timelines for payer APIs, which drives investments in prior authorization automation, member status updates, and provider access tools. Payers are using AI to triage documentation, surface policy rules, and generate communications that reduce cycle times for prior authorization and appeals. Vendors have introduced agentic workflows for payers to manage benefits questions, claims review steps, and cross-channel member engagement, which shortens time-to-resolution. Providers continue to expand ambient scribing, virtual triage, and portal messaging, which support their share leadership through embedded clinician workflows. The AI in Patient Care and Management industry is moving toward integrated platforms that serve both payer and provider needs with shared governance and interoperable data.

As payer APIs mature, assistant experiences extend across member, provider, and pharmacy touchpoints with consistent status visibility. This reduces call volumes for benefit checks and improves provider satisfaction during documentation and follow-up. Provider organizations still drive early adoption for clinical-facing tools, yet payer-facing tools are now catching up because regulatory requirements are explicit and time-bound. Partnerships between platform vendors and large enterprises show how shared components can support both sides of prior authorization and care management. This alignment accelerates enterprise procurement and deployment for the AI in Patient Care and Management market as joint governance and security models are proven in production.

Geography Analysis

North America accounted for 48.26% in 2025, while Asia-Pacific is projected to grow at a 23.37% CAGR over 2026-2031 for the AI in Patient Care and Management market. The region benefits from regulatory clarity and infrastructure that supports secure data sharing, including CMS mandates and TEFCA-based exchange at national scale. Adoption gains come from embedded assistants and ambient documentation inside incumbent EHR workflows that reduce cognitive load and documentation time for clinicians. Platform vendors deliver healthcare-specific AI capabilities that hospital IT teams can activate under existing agreements, which reduces procurement friction for new use cases. The AI in Patient Care and Management market share leadership in North America reflects a mix of regulatory pull and vendor ecosystem depth that speeds deployment cycles relative to other regions.

Asia-Pacific is the fastest-growing region as governments and providers scale digital health initiatives and AI-enabled engagement. National priorities around technology and healthcare modernization are helping organizations test and expand AI in triage, intake, and navigation. Southeast Asian health systems have deployed messaging-based assistants aligned with local channel preferences, which supports rapid uptake without extensive portal migrations. In parallel, platform vendors are extending healthcare solutions into the region through cloud marketplaces and partner networks, which shortens lead times for pilots and rollouts. China’s push to deepen AI healthcare commercialization in 2026 signals strong policy interest in scaling digital capabilities within care delivery. These trends support multi-year adoption momentum and set a foundation for continued growth in the AI in Patient Care and Management market.

Europe is expanding AI deployments within data protection and clinical safety frameworks that influence architecture and validation. Health systems emphasize explainability, risk controls, and integration with existing clinical governance, which favors models embedded in incumbent platforms. Multinational vendors continue to localize capabilities to meet EU data handling standards and language requirements. Over time, standardization and cross-border exchange efforts will help providers and payers align assistant workflows with national systems. Regions in the Middle East, Africa, and South America are adding pilots and targeted rollouts as infrastructure and policy frameworks mature. These deployments often concentrate on patient engagement and virtual triage to address access constraints, and they extend reach where specialist staffing is limited. As capabilities prove in one service line, neighboring use cases follow, which reinforces steady growth for the AI in Patient Care and Management market.

Competitive Landscape

The AI in Patient Care and Management market features many point-solution vendors by use case and a parallel consolidation around platform providers that integrate assistants, documentation, and analytics in one suite. EHR-aligned platforms are embedding AI features that clinicians can use without shifting context, which reduces training time and builds trust in day-to-day use. Oracle launched an AI Center of Excellence for healthcare to accelerate embedded adoption patterns across provider and payer workflows. Microsoft introduced healthcare-specific tooling for triage, prior authorization steps, and operational automation, which positions cloud infrastructure as the base layer for vertical solutions. Salesforce announced Agentforce Health agents that integrate medical histories and device data to streamline engagement and referral workflows. These examples show how large vendors are competing to become the orchestration layer for assistants and workflow automation in the AI in Patient Care and Management market.

Specialist entrants continue to focus on intake, scheduling, triage, and billing automation in provider settings, while payer-focused tools handle benefits questions, prior authorization, and appeals. Capital flows support new operational automation in large health systems, including funding rounds for companies focused on scaling end-to-end processes that reduce administrative burden. Workforce orchestration solutions are addressing staffing and schedule complexity by applying demand forecasting and collaboration to reduce manual administrative tasks. Payer and provider segments are converging on shared capabilities for status visibility and document assembly, which favors platforms with both API and EHR integrations. Vendors differentiate with governance and auditability as buyers require clear controls around model behavior, evidence sources, and data handling. This strategic emphasis aligns with enterprise risk frameworks and procurement checklists that prioritize safe embedding for the AI in Patient Care and Management market.

Selective acquisitions and partnerships broaden feature coverage inside platform portfolios. Payment and patient intake vendors have expanded capabilities through M&A, which consolidates front-door experiences under one vendor relationship for providers. Platform alliances bring wearable, imaging, and exchange data into unified agent experiences, which enables richer context for assistants that navigate appointments and guide care utilization. Virtual urgent care and telehealth expansions also signal how AI is embedded in services that deliver around-the-clock access, which reinforces demand for triage and navigation assistants. Across these moves, the competitive field remains fragmented by workflow, yet the momentum favors platforms that unify assistants, ambient documentation, and analytics with strong governance in the AI in Patient Care and Management market.

AI In Patient Care And Management Industry Leaders

Microsoft

Phreesia

Artera

Notable Health

Luma Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: San Francisco-based Luminai closed a USD 38 million Series B led by Peak XV Partners, with participation from Define Ventures, General Catalyst, and Y Combinator, bringing total raised to USD 60 million. The AI-native automation platform targets large provider organizations automating administrative workflows (access, revenue cycle, compliance) amid cost pressure and staffing constraints, combining talent from Palantir, Cruise, Google, Epic, and Banner Health to execute full end-to-end processes reliably at enterprise scale.

- April 2026: South Korea's Ministry of Health and Welfare partnered with Indonesia's Coordinating Ministry for Human Development and Culture to pilot AI-based teleconsultation in remote Indonesian island communities, focusing on universal health coverage via AI-based public health, digital wellness, AI-driven maternal/child healthcare, and mental health services. The collaboration, part of South Korea's "Global AI Universal Basic Society" framework, involves university hospitals, major technology firms, and academic institutions, with plans to expand the model to Vietnam and Thailand.

- March 2026: Salesforce announced six new Agentforce Health agents integrating HealthEx’s TEFCA and FHIR digital health wallet for comprehensive medical histories, Verily’s wearables and lab data for predictive care, and Viz.ai’s medical imaging and EHR data for disease detection and automated workflows. MIMIT Health reported 459% ROI and USD 1.5 million savings with Agentforce Health, with referral triage, root cause analysis, and engagement campaigns available in June 2026, and hospital operations capabilities plus integrations generally available later in 2026.

Global AI In Patient Care And Management Market Report Scope

As per the scope of the report, AI in patient care and management refers to the use of machine‑learning, natural‑language processing, and automation tools to support clinical decision‑making, personalize care pathways, predict risks, streamline triage, and enhance communication between patients and care teams. It enables proactive monitoring, early intervention, and more efficient coordination across the care continuum, improving both outcomes and operational efficiency.

The AI in patient care and management market is segmented into offering, deployment mode, technology, application, end user, and geography. By component, the market is segmented into software and services. By deployment mode, the market is segmented into cloud-based, on-premise, and hybrid. By technology, the market is segmented into natural language processing (NLP), chatbots / conversational agents, computer vision, and predictive analytics engines. By application, the market is segmented into Enhanced Communication and omnichannel messaging, virtual health assistants and chatbots, patient intake, forms, and pre-registration, triage and symptom checking, care-plan adherence and remote coaching, medication support and refill assistants, and others. By end user, the market is segmented into healthcare providers, healthcare payers, and retail-health and digital-front-door platforms. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Cloud |

| On-Premise |

| Hybrid |

| Natural Language Processing (NLP) |

| Chatbots / Conversational Agents |

| Computer Vision |

| Predictive Analytics Engines |

| Enhanced Communication and Omnichannel Messaging |

| Virtual Health Assistants and Chatbots |

| Patient Intake, Forms, and Pre-Registration |

| Triage and Symptom Checking |

| Care-Plan Adherence and Remote Coaching |

| Medication Support and Refill Assistants |

| Others |

| Healthcare Providers |

| Healthcare Payers |

| Retail-Health and Digital-Front-Door Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Technology | Natural Language Processing (NLP) | |

| Chatbots / Conversational Agents | ||

| Computer Vision | ||

| Predictive Analytics Engines | ||

| By Application | Enhanced Communication and Omnichannel Messaging | |

| Virtual Health Assistants and Chatbots | ||

| Patient Intake, Forms, and Pre-Registration | ||

| Triage and Symptom Checking | ||

| Care-Plan Adherence and Remote Coaching | ||

| Medication Support and Refill Assistants | ||

| Others | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Retail-Health and Digital-Front-Door Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the AI in Patient Care and Management market?

The AI in Patient Care and Management market size is USD 2.10 billion in 2025, USD 2.45 billion in 2026, and is set to reach USD 6.22 billion by 2031 at a 20.48% CAGR over 2026-2031.

Which segment accounts for the largest share in 2025 and which is growing fastest?

Software leads by offering with 57.42% in 2025 and is projected to grow at a 22.34% CAGR, while virtual health assistants and chatbots are the fastest-growing application at a 23.55% CAGR.

Where is regional momentum strongest through 2031?

North America leads with 48.26% share in 2025, and Asia-Pacific is the fastest-growing region with a projected 23.37% CAGR during 2026-2031.

Which technologies are gaining the most traction?

NLP remains foundational for documentation and extraction, while chatbots/conversational agents post the fastest growth as assistants handle scheduling, benefits questions, and navigation across digital front doors.

Page last updated on: