AI In Pathology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

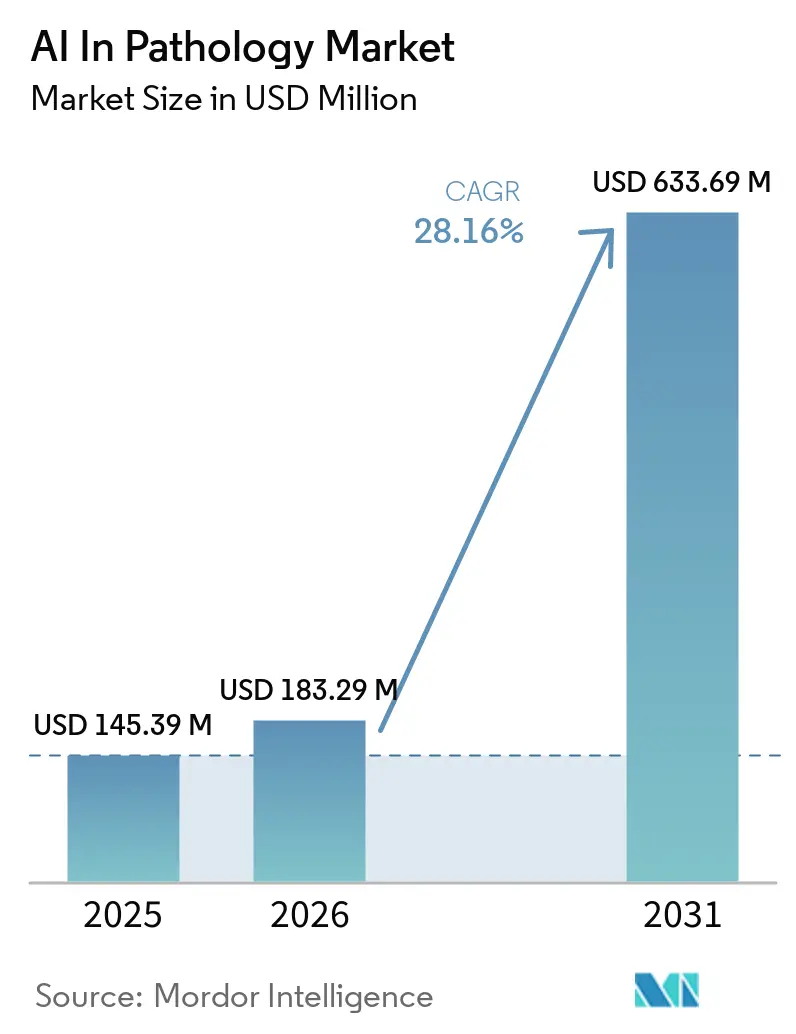

| Market Size (2026) | USD 183.29 Million |

| Market Size (2031) | USD 633.69 Million |

| Growth Rate (2026 - 2031) | 28.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Pathology Market Analysis by Mordor Intelligence

The AI in Pathology market size was USD 145.39 million in 2025 and is projected to reach USD 633.69 million by 2031 at a 28.16% CAGR during 2026-2031. The trajectory reflects maturing regulatory frameworks that are enabling clinical deployment as seen in FDA decisions that clear platform-level systems and novel computational pathology diagnostics, reducing uncertainty for hospital and laboratory buyers. FDA Breakthrough Device Designation for the VENTANA TROP2 RxDx Device validated that companion diagnostics can incorporate AI-based image analysis as core decision support for therapy selection, which is reshaping how pathology data are used across oncology workflows. Large health networks are standardizing digital workflows and scaling AI-enabled platforms across distributed sites, signaling that deployment is moving from isolated pilots to enterprise rollouts. Guidance clarifying how AI is categorized in clinical services, combined with active code updates, is also informing how providers integrate decision support in care pathways, even as reimbursement remains a gating factor for many use cases. Cloud-enabled platforms and modern file standards are helping labs manage compute and storage demands, further reducing friction that previously slowed digitization at scale.

Key Report Takeaways

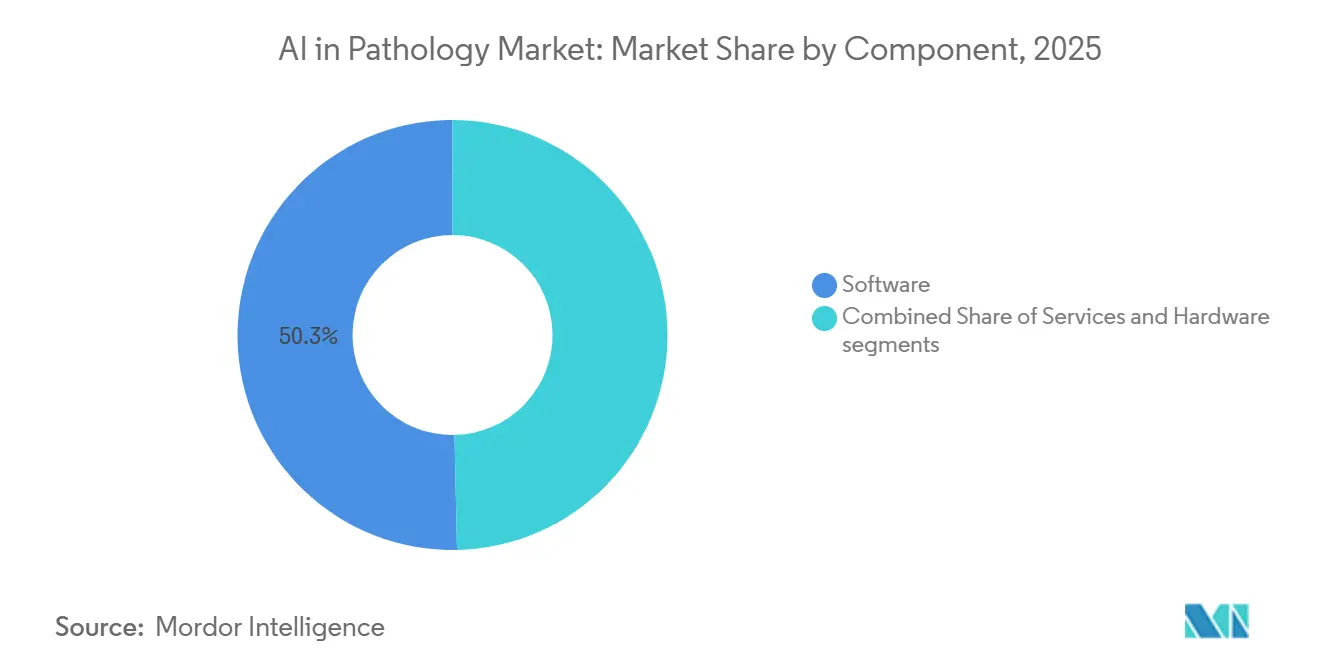

- By component, software led with 50.33% share in 2025, while services is forecast to grow at 29.20% CAGR through 2031.

- By function, image analysis and pattern recognition held 48.38% share in 2025, and diagnostic decision support is projected to expand at 29.46% CAGR through 2031.

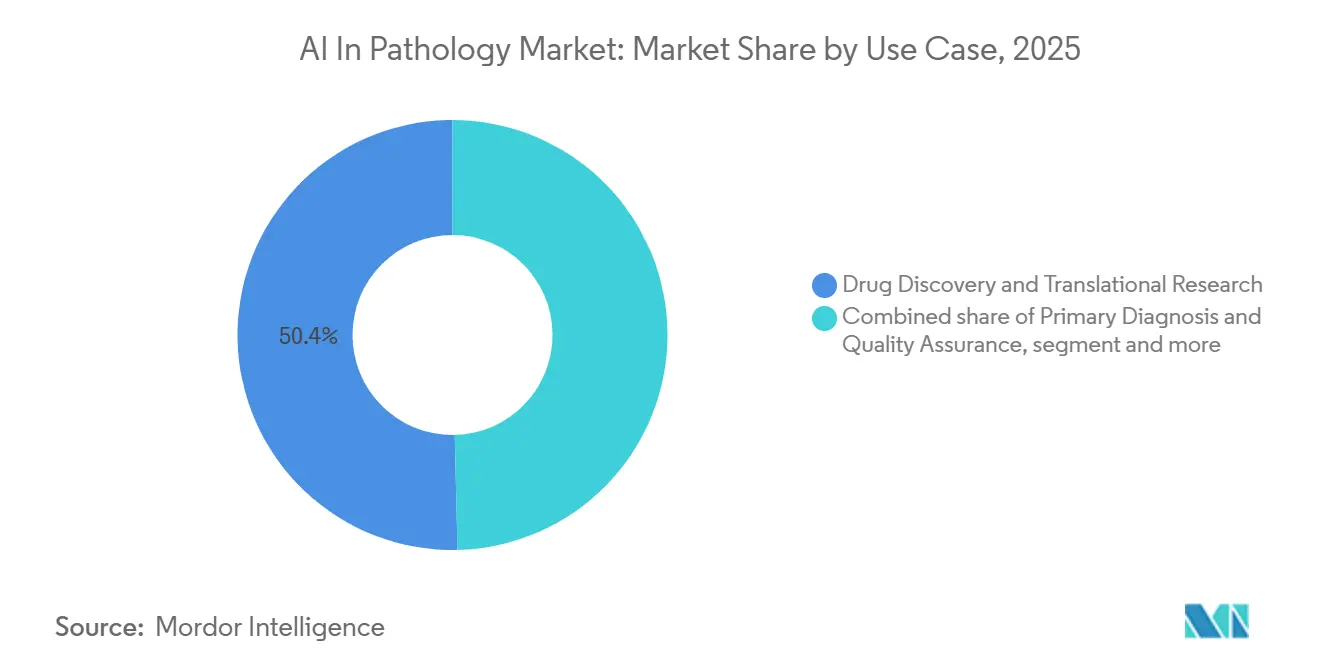

- By use case, drug discovery and translational research represented 50.37% of revenue in 2025, with primary diagnosis and quality assurance set to grow at 30.14% CAGR through 2031.

- By end user, hospitals accounted for 46.35% share in 2025, and diagnostic laboratories are forecast to record 31.11% CAGR through 2031.

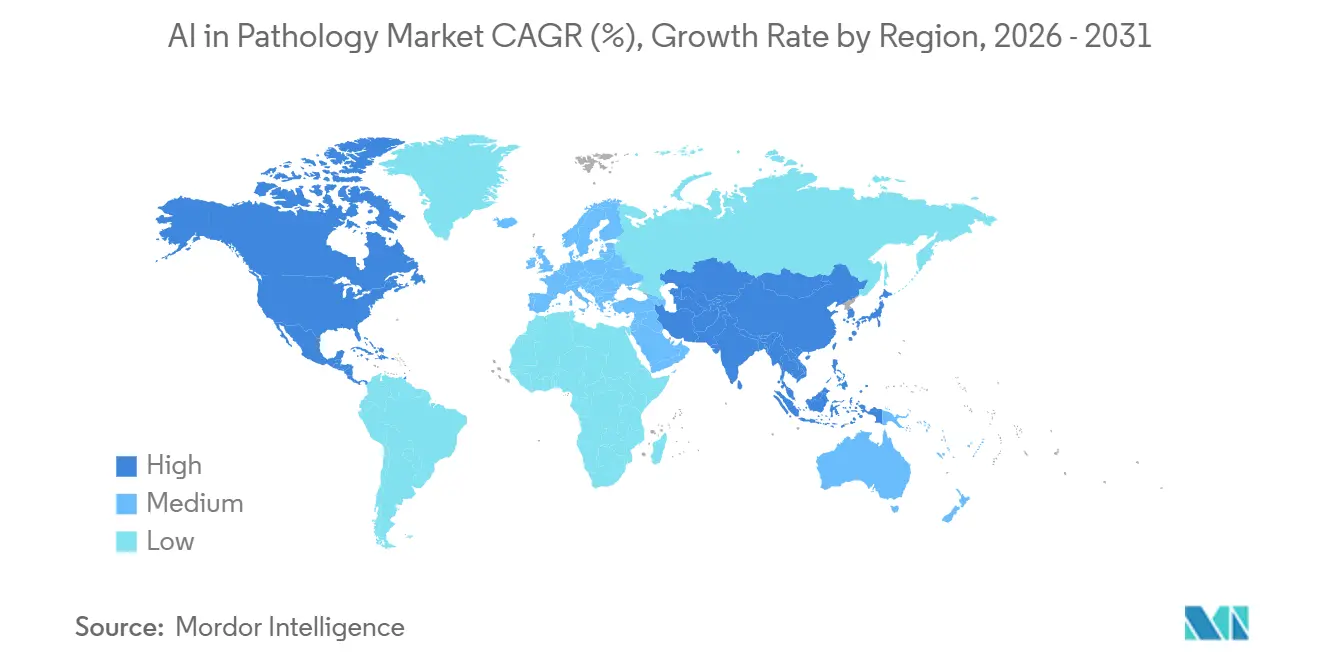

- By geography, North America held 50.13% share in 2025, while the Asia-Pacific is expected to grow at 31.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Pathology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical Approvals Enabling Adoption (FDA/CE-IVDR Progress) | +7.2% | Global, with early gains in US, EEA, UK | Medium term (2-4 years) |

| Oncology Biomarker Surge and Need for Standardized IHC Quantification | +6.8% | Global, concentrated in North America, Western Europe | Short term (≤ 2 years) |

| AI-Ready Digital Pathology Platforms Easing Deployment | +5.4% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Pharma–CDx Partnerships Embedding AI in Assay Workflows | +4.7% | Global, with concentration in US, Switzerland, UK | Medium term (2-4 years) |

| Foundation and Embedding Models Improving Scalability and Domain Robustness | +4.9% | Global, with research concentration in North America, EU | Long term (≥ 4 years) |

| Automated Slide QC Reducing Rescans and Enabling Reliable AI at Scale | +3.8% | North America & EU, gradual APAC adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Clinical Approvals Enabling Adoption (FDA/CE-IVDR Progress)

Regulatory milestones between 2025 and 2026 lowered adoption risk by enabling clinical-grade platforms and targeted computational diagnostics. In June 2025, PathAI’s AISight Dx became the first FDA-cleared digital pathology image management system that included a Predetermined Change Control Plan, setting a practical precedent for iterative software improvements within regulated practice.[1]PathAI, “PathAI Receives FDA Clearance for AISight Dx Platform for Primary Diagnosis,” PathAI, pathai.comIn April 2025, the FDA granted Breakthrough Device Designation to Roche’s VENTANA TROP2 RxDx Device, marking the first computational pathology companion diagnostic to receive this recognition and evidencing that AI-derived scoring can guide therapy selection in non-small cell lung cancer.[2]Roche granted FDA Breakthrough Device Designation for first AI-driven companion diagnostic for non-small cell lung cancer,” Roche, roche.com The intent of such decisions is to align clinical validation, analytical performance, and postmarket oversight with the realities of learning systems. The effect for the AI in Pathology market is a tangible reduction in perceived regulatory risk as digital platforms become the operating system for enterprise workflows while AI modules connect to well-defined clinical tasks. In parallel, EU IVDR certifications across digital pathology are expanding, with vendors demonstrating quality management systems, multi-site validation, and technical documentation that support long-term compliance. This momentum collectively signals maturing oversight that aligns with software-based innovation cycles and accelerates enterprise procurement in the AI in Pathology market.

Oncology Biomarker Surge and Need for Standardized IHC Quantification

Therapy access increasingly hinges on precise biomarker thresholds, which magnifies the need to standardize immunohistochemistry scoring. A January 2026 multi-model evaluation of AI methods for HER2 scoring highlighted variability across independently developed algorithms, reinforcing the value of consistent quantitative methods when treatment eligibility depends on cutoffs like HER2-low. At the same time, clinical-grade tools like Lunit’s PD-L1 scoring suite seek to reduce reading time and improve reproducibility, addressing pressure points in immuno-oncology workflows.[3]Lunit, “AI PD-L1 IHC Scoring and Quantification,” Lunit, lunit.io The American Medical Association’s Appendix S taxonomy update clarifies how to categorize AI-enabled clinical services across assistive, augmentative, and autonomous functions, which informs how these tools are positioned in care pathways and how coverage determinations may evolve. Together, these advances support the ongoing transition from manual visual estimation toward standardized quantitative scoring. This transition fosters a clearer role for decision support in pathology practice, improving clinical confidence and accelerating trials and treatment selection in the AI in Pathology market.

Pharma–CDx Partnerships Embedding AI in Assay Workflows

Pharmaceutical and diagnostics alliances are embedding algorithmic scoring into companion diagnostic development instead of treating AI as a post-hoc add-on. PathAI’s exclusive collaboration with Roche Tissue Diagnostics positions co-developed, AI-enabled assays for global commercialization, aligning algorithm development with regulated assay workflows and pharma clinical endpoints. Lunit’s agreements with Agilent Technologies and CellCarta extend the reach of AI across tissue-based diagnostics and lab-developed test pathways that can accelerate trial timelines for targeted therapies. The FDA’s Breakthrough Device Designation for Roche’s VENTANA TROP2 RxDx Device underscores that computational approaches can underpin CDx decision rules when supported by clinical evidence. Vendors are expanding beyond algorithm licensing by aligning development processes with pharma quality systems, which positions AI capabilities as integral infrastructure for trial enrollment, endpoint measurement, and regulatory submissions. This broader alignment accelerates the feedback loop between assay performance, trial design, and clinical adoption in the AI in Pathology market.

Foundation and Embedding Models Improving Scalability and Domain Robustness

Foundation models pretrained on large, diverse slide corpora are improving task performance across cancer subtyping, mutation prediction, and other clinically relevant endpoints. Microsoft’s Prov-GigaPath, pretrained on over 1.3 billion tiles from real-world slides, achieved state-of-the-art results across benchmarking tasks, demonstrating how scale and data diversity can generalize to multiple clinically meaningful targets. A 2025 Nature Communications benchmark showed that while larger pretraining datasets do not always correlate with gains on downstream clinical tasks, tissue prevalence in the pretraining data positively correlates with performance in tissue-specific biomarker prediction, a finding that points to focused pretraining strategies for indication-led development. These results reinforce that representation quality and curation strategy are as important as raw scale for clinical performance. The implication is that platform vendors and clinical AI developers can leverage embedding models for faster development cycles while managing domain shift risks with tissue-specific design choices. As health systems standardize digital slide formats and cloud deployment patterns, the AI in Pathology market is better positioned to exploit foundation models at the point of care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unclear Reimbursement and ROI Pathways for AI Pathology | -4.3% | US (acute impact), gradual spread to other markets | Short term (≤ 2 years) |

| Domain Shift Across Scanners/Stains/Sites Limiting Generalizability | -3.6% | Global | Long term (≥ 4 years) |

| IVDR Notified-Body Capacity and Evidentiary Burden Raising Time-to-Market | -2.9% | EU, EEA, UK, Switzerland | Medium term (2-4 years) |

| Compute, Storage, and IT Overhead for WSI-Scale AI Inference | -2.4% | Global, acute in resource-constrained markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Unclear Reimbursement and ROI Pathways for AI Pathology

Coverage and coding policies shape how quickly hospitals can justify investment in AI. CMS payment integrity and anti-duplication rules restrict separate payment for multiple methods that assess the same analyte, which creates ambiguity about whether an algorithmic pathology service is distinct or bundled into an existing code.[4]Centers for Medicare & Medicaid Services, “2025 Complete Table of Contents Medicare NCCI Coding Policy Manual,” Centers for Medicare & Medicaid Services, cms.gov Category III CPT codes for digital pathology slide digitization provide tracking but do not carry assigned RVUs, requiring payer-by-payer engagement that delays predictable reimbursement. AMA’s Appendix S taxonomy creates a framework to classify AI-enabled services as assistive, augmentative, or autonomous, which informs how these tools are documented and billed within care pathways. In the near term this limits the speed at which providers can reclaim direct revenue for AI-supported tasks, shifting the justification toward productivity, turnaround time, and quality gains. Operational complexity is a material concern as well, since Medicare’s fee-for-service improper payment estimates show coding errors are a persistent source of risk for health systems. Until clearer payment pathways mature, adoption in the AI in Pathology market will skew toward large systems and labs that can fund AI as infrastructure and recoup value through scale.

Compute, Storage, and IT Overhead for WSI-Scale AI Inference

Whole-slide image analysis imposes demanding compute and storage requirements that stress hospital IT budgets. Inference and training for modern models drive investment in high-performance compute, as seen in large-scale GPU infrastructure at leading life sciences firms that pursue digital pathology and other AI workloads in one ecosystem. Even with model efficiency gains, clinical-grade deployments must handle tiled inference, high-resolution image rendering, and secure data exchange at enterprise scale. Storage budgets are also significant, with multi-year retention obligations for patient data, although hybrid architectures leveraging cold tiers and on-premises-first workflows can lower the annual unit costs for multi-petabyte archives. File format improvements that preserve quality at lower storage footprints, such as configurable DICOM JPEG XL outputs on next-generation scanners, can further ease infrastructure pressure for digitizing large volumes. These constraints have nudged many health systems toward cloud-enabled, vendor-managed platforms that convert capital expenditure into operating expenditure while maintaining performance and compliance for the AI in Pathology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gains as Implementation Complexity Outpaces Pure Software Sales

Software commanded the largest share at 50.33% in 2025 as enterprise platforms integrated image management and AI modules for validated clinical and research tasks in the AI in Pathology market. Services is projected to grow at 29.20% CAGR through 2031 as hospitals and labs require implementation support, workflow design, LIS integration, and continuous model validation to maintain regulated use. Multi-year collaborations with large health systems pair platform deployment with managed services, training, and algorithm co-development, reflecting how organizations buy solutions rather than point tools. These services often include quality assurance, policy templates, and documentation that streamline compliance for digital primary diagnosis across distributed sites. Hardware choices increasingly align with cloud-enabled workflows and next-generation file outputs that ease transmission and storage load at scale. Over time, the services mix supports repeatable outcomes by embedding governance structures, model monitoring practices, and continuous updates into routine operations for the AI in Pathology market.

Service-led growth also reflects how buyers de-risk transformation with vendor-managed deployments and lifecycle support. Platform releases increasingly enable multi-algorithm workflows, flexible slide ingestion, and collaborative review, which accelerates standardization across multi-site networks. Cloud-first deployments reduce on-premises overhead and speed adoption across labs with heterogeneous IT capabilities. Structured rollouts with executive sponsorship and governance boards create durable pathways for algorithm updates and validation cycles. Implementation partners also help facilities align SOPs with accreditation expectations for digital workflows. These operating practices strengthen the services thesis for the AI in Pathology market as organizations prioritize dependable outcomes over license-only models.

By Function: Diagnostic Decision Support Overtakes Pattern Recognition as Clinical Validation Matures

Image analysis and pattern recognition held 48.38% AI in Pathology market share in 2025, reflecting historical reliance on segmentation, detection, and classification engines that supported research and early-stage clinical tasks. Diagnostic decision support is forecast to grow at 29.46% CAGR through 2031 as clinical-grade solutions inform therapy selection and reporting with validated scoring outputs. FDA Breakthrough Device Designation for the VENTANA TROP2 RxDx Device established a precedent for AI-derived metrics to guide therapy selection in non-small cell lung cancer, signaling the rising role of decision support tools within regulated CDx frameworks. Momentum for decision support is reinforced by taxonomy updates that specify how augmentative tools fit within physician workflows, reducing adoption friction while enabling methodical evaluation of value and risk. Validated QC workflows are also gaining traction, raising the reliability of downstream decision support and limiting rescans that delay reporting.

As health systems operationalize AI, tools that connect quantitative scoring with clinical reporting pathways gain clear priority. Multi-algorithm orchestration and specimen-level reporting features streamline how case evidence is assembled for pathologists across large networks. The ability to deliver prompt, reproducible quantification for IHC targets and to integrate with LIS workflows represents a practical bridge from pattern recognition to decision support at scale. QC automation layers catch input issues before human review, preventing recuts and rescans that diminish productivity. Collectively, these shifts align with a measured but steady pivot toward tools that affect patient management, reinforcing the growth prospects for this function within the AI in Pathology market.

By Use Case: Primary Diagnosis Accelerates as Reimbursement Clarity and Hospital Networks Scale Deployment

Drug discovery and translational research represented 50.37% of AI in Pathology market size in 2025, reflecting robust demand from biopharma for AI-enabled biomarker discovery, trial endpoints, and pre-market assay development. Primary diagnosis and quality assurance are projected to grow at 30.14% CAGR through 2031 as regulated platforms for primary diagnosis roll out across large networks and workflow-embedded QC reduces variance in inputs. Enterprise deployments that standardize platforms across sites show how validated image management, scanner compatibility, and integrated algorithms can be scaled within anatomic pathology networks. Companion diagnostic momentum further encourages clinical use cases where quantitative scores feed into treatment selection. As vendor roadmaps increase scanner interoperability, hospital networks gain a more flexible backbone for adoption at scale.

CDx-related use cases also deepen ties between vendors and pharma, embedding pathology AI closer to clinical development. AI-derived endpoints can streamline trial enrollment for targeted agents by providing reproducible, quantitative measures aligned with protocol criteria. Cloud-enabled deployment and open platform strategies broaden interoperability with LIS and third-party applications. Collectively, the balance of near-term ROI drivers favors standardized primary diagnosis and QA where digitization can reduce turnaround time and enable multi-site load balancing, anchoring durable growth for this use case in the AI in Pathology market.

By End User: Diagnostic Laboratories Surge as Outreach Networks Adopt AI to Manage Volume Without Hiring

Hospitals accounted for 46.35% share in 2025, reflecting sustained investment in digital infrastructure, platform deployment, and multi-site governance as providers target operational scale in the AI in Pathology market. Diagnostic laboratories are forecast to grow at 31.11% CAGR through 2031 as outreach networks leverage platform standardization, multi-site triage, and cloud deployment to manage rising volumes. Strategic system-wide partnerships show how large health systems and lab networks can operationalize AI through shared image management, standardized SOPs, and joint algorithm roadmaps. In parallel, vendors and labs are using vendor-managed cloud infrastructure to reduce local IT complexity while ensuring performance benchmarks for WSI-scale workloads.

Central lab groups are also becoming innovation hubs by aligning platform choices with enterprise interoperability and scanner compatibility. Solutions that combine FDA-cleared enterprise platforms with validated scanner configurations are helping labs harmonize operations and training across multi-state footprints. Reference laboratories are adopting cloud-based configurations to minimize on-premises infrastructure while scaling case throughput. Market momentum is amplified as labs update quality systems, implement slide QC automation, and deploy decision support for high-volume cancer types, which collectively strengthens the growth outlook for diagnostic laboratories in the AI in Pathology market.

Geography Analysis

North America held 50.13% of AI in Pathology market share in 2025, supported by regulatory clearances that de-risked enterprise deployment and by large system rollouts that validated digital primary diagnosis at scale. FDA-cleared enterprise platforms converged with hospital and lab network deployments, which modernized workflows and created shared infrastructure for algorithmic decision support. System-wide adoption by large networks established governance baselines and reinforced purchasing confidence across additional providers. Advances in platform interoperability and scanner compatibility, together with cloud-enabled architecture, gave North American providers a practical path to scale. These elements stabilized the foundation for broader clinical AI use and underpin the region’s leadership position in the AI in Pathology market.

Europe progressed under IVDR with vendors demonstrating certified quality systems, clinical performance, and postmarket surveillance plans that support sustainable clinical use. Certifications that cover both models and the supporting quality management infrastructure reflect a maturing regulatory environment that emphasizes lifecycle rigor. Labs in European health systems also benefit from cloud-enabled platform strategies that align with strict data governance, helping organizations manage deployment complexity without enlarging internal IT teams. The combination of IVDR guardrails and enterprise-grade platforms positions Europe for steady expansion across primary diagnosis, QA, and algorithmic scoring embedded in clinical reporting. As scanner vendors iterate on file formats that reduce storage overhead, European networks can scale digitization more efficiently and sustain multi-year archives that satisfy retention mandates.

Asia-Pacific is projected to record 31.24% CAGR through 2031, with demand driven by workforce capacity constraints and the need to standardize workflows across high-volume centers. In regions where the ratio of pathologists to population is low, AI-augmented processes for triage, QC, and quantitative scoring can help scale diagnostic throughput in a controlled and auditable manner. Growth in cloud-enabled platforms further expands access by reducing up-front capital requirements and by facilitating uniform deployments across multi-site systems. As foundation and embedding models improve performance for tissue-specific tasks, regional providers can adopt decision support that meets local disease burden needs, advancing the case for investment. Vendor partnerships with global diagnostics and pharma ecosystems also accelerate knowledge transfer and standard-setting, accelerating uptake across oncology programs in the AI in Pathology market.

Competitive Landscape

The AI in Pathology market features a diverse mix of digital pathology platform vendors, computational pathology specialists, and diagnostics conglomerates with integrated AI strategies. Competitive differentiation centers on regulatory progress for clinical-grade platforms, pharma–CDx collaborations that embed AI into regulated assay workflows, and the performance of foundation models and embedding approaches at scale. System-wide rollouts by leading health networks show an increasing preference for enterprise-grade platforms with clear upgrade paths, validated scanner compatibility, and multi-algorithm orchestration. Cloud-enabled offerings that reduce on-premises IT lift are also gaining traction as organizations target reproducible deployment across distributed sites.

Vertical integration and data consolidation strategies are reshaping how pathology AI capabilities are brought to clinical practice. Health system partnerships that combine platform deployment with governance and algorithm co-development are strengthening vendor relationships and structuring roadmaps around clinical priorities. Large diagnostics organizations are also using acquisitions and partnerships to concentrate digital and AI resources, as seen when a national reference laboratory integrated AI and digital R&D assets to support innovation across its network. Clinically oriented platform enhancements that expand scanner support, optimize slide ingestion, and standardize reporting are improving day-to-day efficiency in anatomic pathology workflows.

Technology roadmaps address both performance and reliability. Rapid progress in foundation models, including real-world pretrained architectures validated across multicenter cohorts, continues to set performance baselines for future clinical tools. QC automation and artifact detection tools help maintain reliability and prevent rescans, safeguarding clinician time and preserving scanner capacity. Enterprise interoperability through standardized file formats and cloud-native platform APIs further reduces integration friction, improving extensibility for third-party AI apps and assays. Collectively, these strategies underscore a competitive race defined by regulated platform depth, reliable multi-site operations, and embedded decision support aligned with oncology and CDx needs in the AI in Pathology industry.

AI In Pathology Industry Leaders

Proscia

Indica Labs

PathAI

Ibex Medical Analytics

Paige

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ViewsML completed a USD 4.9 million seed funding round led by Wittington Ventures, with participation from Mayo Clinic and Continuum Health Ventures, to commercialize its AI-driven virtual biomarker staining platform that generates spatial biomarker insights from standard H&E slides without traditional laboratory staining, preserving scarce tissue samples and accelerating biomarker analysis from days/weeks to minutes.

- April 2026: Waiv (formerly Owkin Dx) achieved dual CE marking under IVDR for RlapsRisk BC (breast cancer prognostic risk profiling from histopathology slides) and MSIntuit CRC (colorectal cancer microsatellite instability screening from H&E slides), enabling clinical deployment across EU member states with interoperability via Destra digital pathology platform compatible with Proscia, Roche Diagnostics, Sectra, and Tribun Health systems.

- March 2026: Roche launched its NVIDIA AI factory, bringing combined on-premises and cloud infrastructure to over 3,500 Blackwell GPUs, to accelerate therapeutics and diagnostics development, including digital pathology pattern detection at scale.

- March 2026: PathAI released AISight Dx v2.19 with multi-algorithm support per slide, enhanced slide ingestion, expanded sharing, and structured reporting templates to improve flexibility and workflow precision for anatomic pathology labs.

Global AI In Pathology Market Report Scope

According to the report’s scope, AI in pathology refers to the application of machine‑learning algorithms and image‑analysis models to interpret digital pathology slides, identify patterns in tissue samples, and support diagnostic decision‑making. It enhances accuracy, speeds up case review, and helps pathologists detect abnormalities, quantify biomarkers, and streamline workflows across clinical and research settings.

The AI in pathology market is segmented into component, function, use case, end user, and geography. By component, the market is segmented into software, services, and hardware. By function, the market is segmented into image analysis and pattern recognition, diagnostic decision support, workflow/quality control automation, and others. By use case, the market is segmented into drug discovery and translational research, primary diagnosis and quality assurance, clinical trials and companion diagnostics, and others. By end user, the market is segmented into hospitals, diagnostic laboratories, pharmaceutical and biopharmaceutical companies, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Hardware (WSI scanners, AI-enabled microscopes) |

| Image Analysis and Pattern Recognition |

| Diagnostic Decision Support |

| Workflow/Quality Control Automation |

| Others |

| Drug Discovery and Translational Research |

| Primary Diagnosis and Quality Assurance |

| Clinical Trials and Companion Diagnostics |

| Others |

| Hospitals |

| Diagnostic Laboratories |

| Pharmaceutical and Biopharmaceutical Companies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware (WSI scanners, AI-enabled microscopes) | ||

| By Function | Image Analysis and Pattern Recognition | |

| Diagnostic Decision Support | ||

| Workflow/Quality Control Automation | ||

| Others | ||

| By Use Case | Drug Discovery and Translational Research | |

| Primary Diagnosis and Quality Assurance | ||

| Clinical Trials and Companion Diagnostics | ||

| Others | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Pharmaceutical and Biopharmaceutical Companies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the AI in Pathology market growth outlook through 2031?

The AI in Pathology market size is projected to increase from USD 145.39 million in 2025 to USD 633.69 million by 2031, reflecting a 28.16% CAGR during 2026-2031.

Which functions are leading and growing fastest in the AI in Pathology space?

Image Analysis and Pattern Recognition led in 2025, while Diagnostic Decision Support is forecast to grow fastest through 2031 as validated decision-support tools integrate in reporting and CDx workflows.

Which use cases will expand most for AI in Pathology by 2031?

Drug Discovery and Translational Research led revenue in 2025, and Primary Diagnosis and Quality Assurance is projected to expand fastest through 2031 as enterprise networks scale digitization and validated AI.

Which end users will adopt AI in Pathology fastest?

Diagnostic laboratories are expected to grow fastest due to outreach volumes, cloud-enabled deployments, and standardized workflows, while hospitals maintain the largest installed infrastructure base.

Page last updated on: