AI In Patient Scheduling Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

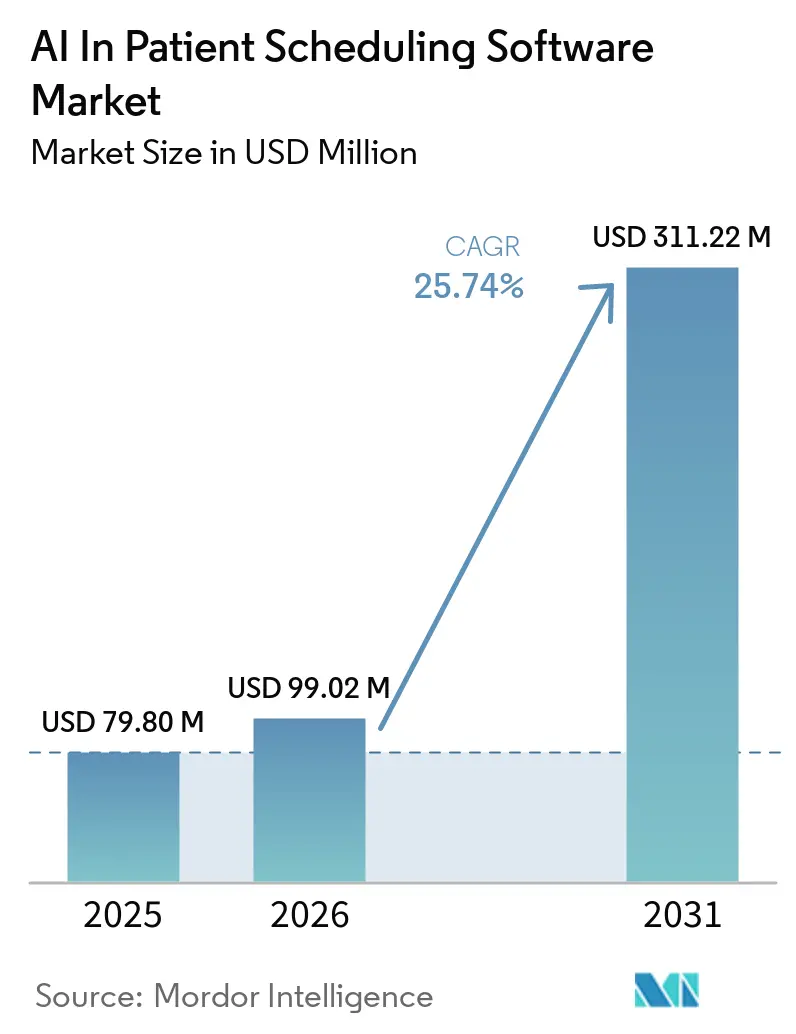

| Market Size (2026) | USD 99.02 Million |

| Market Size (2031) | USD 311.22 Million |

| Growth Rate (2026 - 2031) | 25.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Patient Scheduling Software Market Analysis by Mordor Intelligence

The AI in patient scheduling software market is expected to grow from USD 79.80 million in 2025 to USD 99.02 million in 2026 and is forecasted to reach USD 311.22 million by 2031 at 25.74% CAGR over 2026-2031. Health systems are adopting these tools because manual scheduling still creates avoidable delays, wasted staff time, and rising administrative costs at a point when providers are being asked to handle more patients with tighter margins. The AI in patient scheduling software market is gaining momentum as healthcare organizations increasingly adopt automation technologies to improve operational efficiency and patient access. AI-powered scheduling solutions can significantly reduce administrative workload, optimize appointment allocation, minimize scheduling conflicts, and lower no-show rates through predictive analytics and automated patient engagement. As healthcare providers face rising patient volumes, staffing constraints, and growing demand for digital health services, AI-driven scheduling platforms are becoming essential tools for enhancing workflow efficiency, resource utilization, and patient experience. The AI in patient scheduling software market is also being shaped by tighter bundling from EHR vendors, faster product release cycles from specialist platforms, and persistent integration friction across legacy systems that still slows deployment in complex provider environments.

Key Report Takeaways

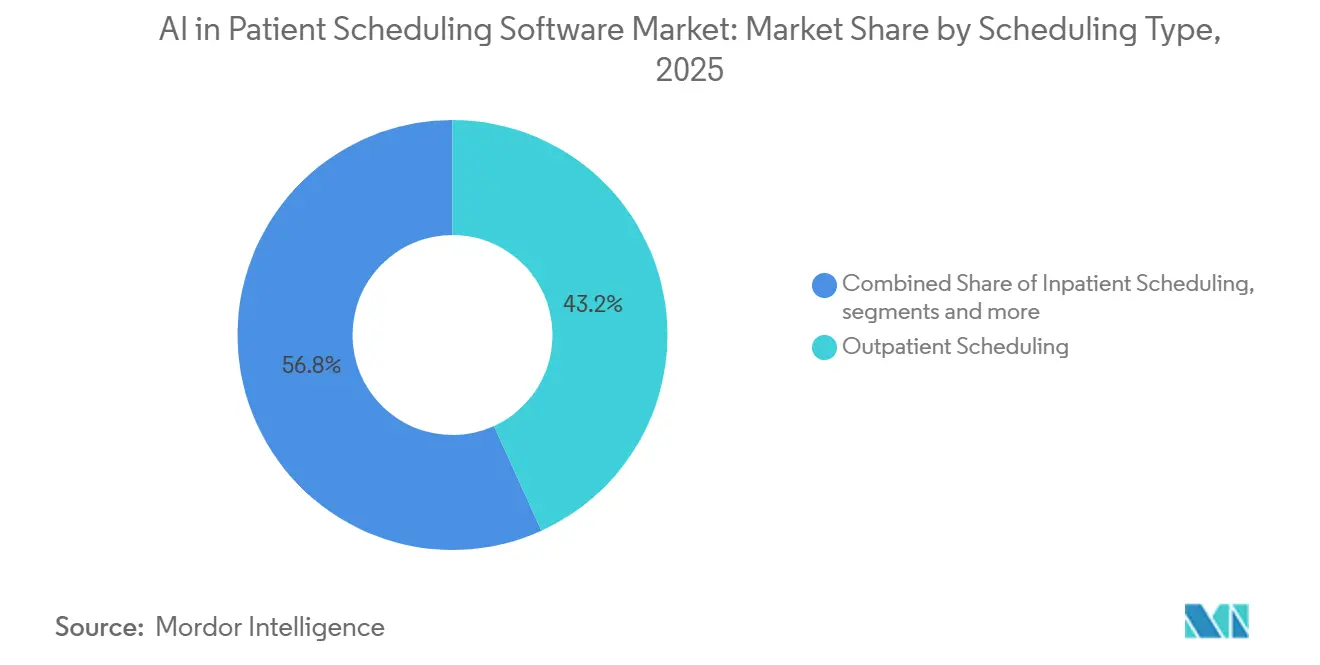

- By scheduling type, outpatient scheduling held 43.17% of the AI in patient scheduling software market in 2025, while inpatient scheduling is projected to grow at the fastest 26.91% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 79.73% of the AI in patient scheduling software market in 2025 and is also projected to be the fastest-growing segment with a 27.36% CAGR through 2031.

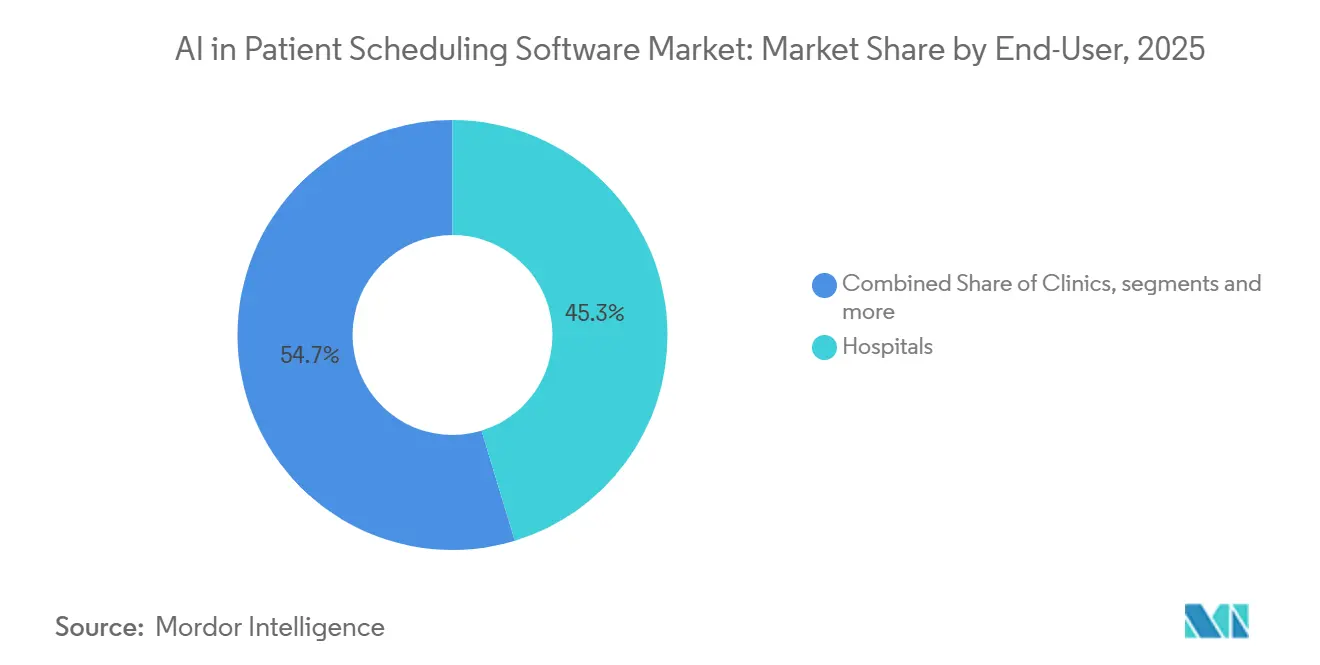

- By end-user, hospitals represented 45.29% of the AI in patient scheduling software market in 2025, while clinics are expected to expand at the fastest 26.68% CAGR over 2026-2031.

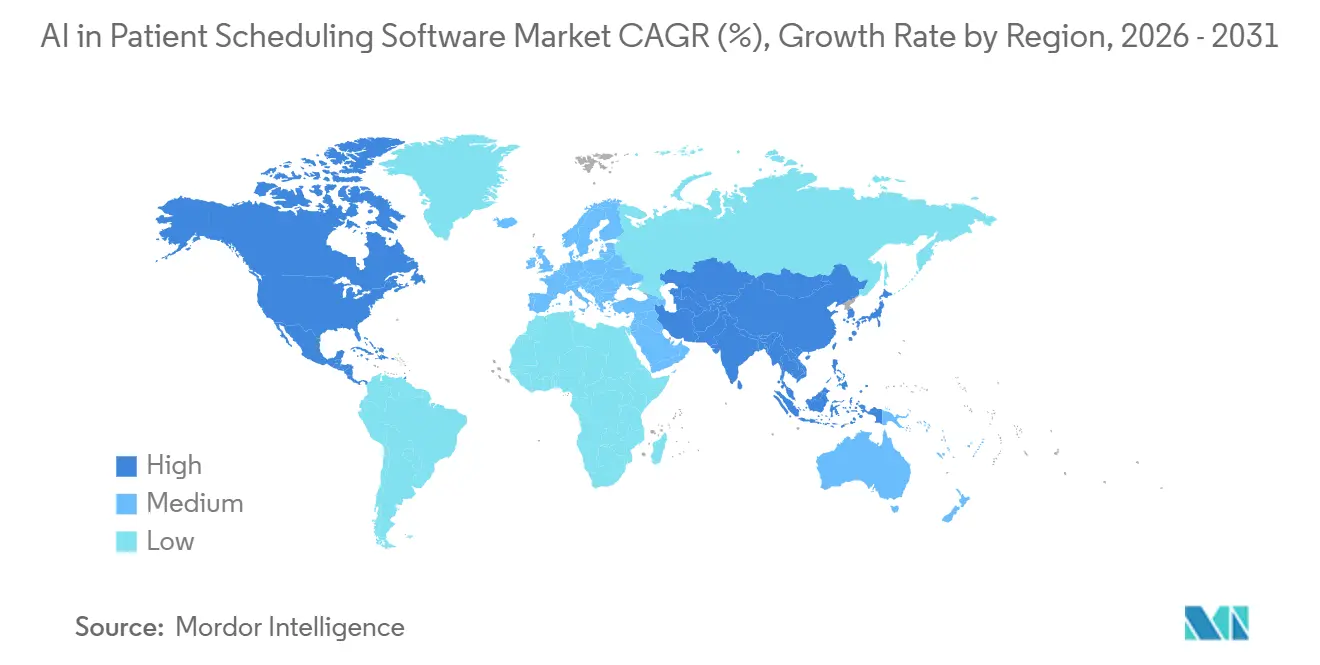

- By geography, North America led with 48.36% of the AI in patient scheduling software market in 2025, while Asia-Pacific is forecasted to record the highest 28.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Patient Scheduling Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need to Reduce Administrative Inefficiencies and Double Bookings | +4.5% | Global, with highest intensity in North America and Western Europe | Short term (≤ 2 years) |

| Rapid Healthcare Digital Front-Door Transformation | +4.0% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Rise of Telehealth and Hybrid Care Coordination | +3.2% | Global, APAC and North America leading adoption | Medium term (2-4 years) |

| Patient Self-Scheduling and Real-Time Rescheduling Expectations | +2.8% | North America and Europe, early gains in urban APAC centers | Short term (≤ 2 years) |

| Predictive No-Show Reduction and Slot Utilization Gains | +3.5% | Global, highest ROI concentration in North America and Northern Europe | Medium term (2-4 years) |

| Underused Appointment Capacity in Multi-Specialty and Multi-Site Networks | +2.2% | North America, early adoption in APAC multi-site hospital networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Need to Reduce Administrative Inefficiencies and Double Bookings

Administrative overhead remains one of the clearest spending targets for hospital finance teams, and that keeps the AI in patient scheduling software market closely tied to cost control. A 2025 systematic review covering 24 studies found that AI-assisted administrative tools reached efficiency gains of 40%, and it also noted that AI automation in hospital operations could support 5% to 10% savings in national health expenditure.[1]John Tayu Lee et al., “The Impact of Artificial Intelligence on the Health Economy, Workforce Productivity, and Administrative Efficiency: A Systematic Review,” medRxiv, medrxiv.org The cost problem is wider than a missed appointment because one double-booked slot can trigger billing errors, patient dissatisfaction, provider overtime, and delays across the rest of the day. Hyro said in 2025 that 41% of health systems adopted AI scheduling agents in part to address staffing shortages, and its deployments offloaded an average of 264 administrative hours each month.[2]Hyro, “Hyro Reveals Healthcare AI Agent Benchmarks Proving Deep EHR Integrations Are Key to Unlocking Over $1M in ROI,” PR Newswire, prnewswire.com That operating logic is widening from hospitals to ambulatory networks where front-desk teams still spend large parts of the day on rescheduling, confirmations, and waitlist calls. It also explains why the AI in patient scheduling software market is expanding in settings where reducing slot leakage produces a faster return than adding new clinical capacity.

Rapid Healthcare Digital Front-Door Transformation

The digital front door is compressing the role of standalone access tools, and that is changing how the AI in patient scheduling software market is being sold. Providers increasingly want patient communication, verification, documentation, and appointment management to work through one connected workflow rather than separate systems. Amazon Web Services launched Amazon Connect Health in 2026 as a purpose-built agentic AI solution that integrates with EHR systems for appointment management, patient verification, and clinical documentation. AWS also said its Netsmart partner integration led to a 275% increase in ambient documentation adoption, which shows that buyers are rewarding products that link front-office activity with the wider clinical workflow. As larger platform vendors and hyperscalers enter the stack, smaller vendors in the AI in patient scheduling software market need deeper specialty logic or stronger pricing discipline to keep their position. This is changing vendor positioning faster than topline growth rates alone would suggest.

Rise of Telehealth and Hybrid Care Coordination

Telehealth is now a routine part of care delivery, and that keeps the AI in patient scheduling software market tied to broader coordination needs rather than simple calendar management. A single episode of care may now involve an in-person visit, a virtual follow-up, a referral, and remote monitoring touchpoints that all need to be scheduled in the right sequence. That complexity is difficult to manage with manual workflows because staff must coordinate providers, modality rules, patient preference, and clinical urgency at the same time. It also creates more dependencies across systems because every hybrid encounter touches scheduling, communication, documentation, and coverage verification. This makes scheduling platforms more valuable when they can act as orchestration layers across multiple care settings. It also means that the AI in patient scheduling software market benefits from telehealth growth even when the actual appointment volume does not change, because the workflow burden per patient becomes heavier.

Patient Self-Scheduling and Real-Time Rescheduling Expectations

Consumer expectations are now a direct force in the AI in patient scheduling software market because patients increasingly judge healthcare access against digital experiences in other sectors. Zocdoc said in December 2025 that 1 in 4 Americans disliked calling a doctor’s office, and more than half of patients who could not reach a provider by phone delayed care. Kyruus Health expanded its Reach solution in July 2025 to Bing, Google Business Profiles, and 100 health plan websites, and said early adopters such as Intermountain Health saw appointments booked rise by 42% in the first 2 months. Real-time rescheduling now matters as much as first-time self-booking because a canceled visit is only recovered if the slot is filled quickly. Predictive no-show tools reinforce that shift because they let staff intervene before appointment leakage turns into lost revenue. The AI in patient scheduling software market is therefore moving toward platforms that combine search, matching, booking, reminders, and waitlist recovery inside one patient access flow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workflow Integration Complexity Across Clinical Departments | -1.8% | Global, acute in multi-site North American systems and European hospital groups | Medium term (2-4 years) |

| Data Privacy, Security, and AI Governance Burden | -2.0% | Global, most restrictive in EU and US | Long term (≥ 4 years) |

| Interoperability Gaps Across Legacy EHR and Practice Management Systems | -1.5% | Global, most severe in markets with heterogeneous EHR ecosystems, including South America, MEA, and parts of APAC | Long term (≥ 4 years) |

| Change Management Friction and Staff Adoption Lag | -1.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Workflow Integration Complexity Across Clinical Departments

The AI in patient scheduling software market still faces a practical limit because deployment is much harder than adding a self-service booking screen. A 2025 systematic review in Frontiers in Health Services found that semantic misalignment across HL7 FHIR and SNOMED CT standards, limited cross-system exchange, and weak engagement features in legacy EHR environments often extend implementation timelines beyond original plans.[3]Frontiers in Health Services, “Challenges and Strategies in Building a Foundational Digital Health Data Integration Ecosystem: A Systematic Review and Thematic Synthesis,” Frontiers in Health Services, frontiersin.org Clinical departments also work with different scheduling rules, provider preferences, equipment dependencies, and care pathways, so one generic scheduling logic rarely fits all of radiology, oncology, surgery, and primary care. The interoperability gap becomes sharper in multi-site systems that run mixed EHR and practice management stacks, because each added system increases the effort needed to normalize data and workflow logic. Staff adoption can lag as well when schedulers and clinic managers are asked to trust automated recommendations that change long-standing local routines. For that reason, the AI in patient scheduling software market often rewards vendors that bring integration depth and workflow configuration capacity rather than pure model performance alone.

Data Privacy, Security, and AI Governance Burden

Privacy and governance requirements continue to slow the AI in patient scheduling software market because scheduling data still contains protected health information and provider-specific workflow data. In the United States, HIPAA applies when systems access appointment type, contact data, and provider details, while European deployments must also address GDPR and local data residency requirements. France has been one of the clearer examples because hospital planning deployments increasingly need alignment with Health Data Hosting rules and procurement expectations around secure healthcare data environments. These requirements raise development cost for vendors and procurement complexity for providers, especially when public systems ask for auditability, explainability, and evidence of controlled data handling. They also favor suppliers that can document how model decisions are traced and reviewed after deployment. As a result, the AI in patient scheduling software market tends to move faster where governance has already been built into the product architecture rather than added later as a compliance layer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scheduling Type: Outpatient Volume Anchors Revenue, Inpatient AI Earns Premium

Outpatient scheduling held 43.17% of AI in patient scheduling software market share in 2025, which made it the largest revenue contributor within the segment mix. The volume of ambulatory visits, repeat encounters, and specialist follow-ups makes this part of the AI in patient scheduling software market the most direct fit for automation. Outpatient providers benefit first from no-show prediction, automated reminders, waitlist recovery, and provider-patient matching based on insurance, availability, and acuity.

Specialty care scheduling and emergency and urgent care scheduling serve narrower but clinically sensitive use cases in the AI in patient scheduling software industry. Those areas command attention because timing errors have higher downstream consequences for patient flow, care coordination, and resource use. Inpatient scheduling is anticipated to be the fastest-growing segment at 26.9% CAGR over 2026-2031, driven by bed management, surgical block planning, and care team coordination across multi-day stays. The revenue logic is clear because a canceled surgery or an idle intensive care bed creates an immediate and visible financial penalty. That is why the AI in patient scheduling software market continues to expand into inpatient environments even though these implementations usually require more workflow configuration than outpatient deployments.

By Deployment Mode: Cloud Dominates and Accelerates, On-Premises Holds Specific Niches

Cloud-based deployment represented 79.73% of the AI in patient scheduling software market size in 2025 and is also expected to advance at a 27.36% CAGR through 2031. That combination shows that cloud is not just replacing older infrastructure, but remains the preferred architecture for new deployments across the AI in patient scheduling software market. The main reason is that cloud-native platforms support real-time EHR synchronization, multi-site scheduling, model updates, and enterprise rollout without the same infrastructure burden faced by local deployments.

On-Premises deployment still matters for a narrower buyer group inside the AI in patient scheduling software industry. Government hospitals, highly integrated delivery networks, and health systems in jurisdictions with strict data residency rules still value direct control over infrastructure and data location. France remains a relevant example because hospital planning deployments have been shaped by HDS-aligned operating expectations and vendor partnerships built around compliant healthcare environments. Those conditions preserve a structural role for on-premises and sovereign-cloud models even as cloud economics improve. The result is that the AI in patient scheduling software market is cloud-led, but not cloud-exclusive, because procurement conditions vary sharply across provider types and national health systems.

By End-User: Hospitals Lead Adoption, Clinics Capture the Growth Premium

Hospitals accounted for 45.29% of the AI in patient scheduling software market in 2025, which reflects their position as the most complex scheduling environment in the care system. Hospitals need to coordinate specialists, diagnostics, surgical blocks, emergency intake, beds, and cross-department dependencies within a single operating structure. That complexity makes the AI in patient scheduling software market especially relevant in hospitals because scheduling errors affect both patient throughput and asset utilization. Ambulatory surgical centers and diagnostic and imaging centers remain smaller in revenue terms, but they are important because scheduling precision directly influences equipment use, chair allocation, and procedure volume.

Clinics are projected to be the fastest-growing end-user segment with a 26.68% CAGR over 2026-2031, largely because smaller provider organizations face staff shortages and heavy call volumes with fewer administrative resources. Other end-users, including home health agencies, behavioral health providers, and long-term care settings, remain a smaller base today. Still, the AI in patient scheduling software market is widening into these settings as vendors refine scheduling logic for care models outside acute and ambulatory hospitals.

Geography Analysis

North America held 48.36% of the AI in patient scheduling software market size in 2025, which kept the region in the lead on both installed base and vendor activity. The region benefits from dense EHR adoption, active digital health investment, and large multi-specialty systems that have enough scheduling complexity to justify enterprise deployment. Canada adds a public system angle through collaborative hospital planning and capacity tools, while Mexico remains earlier in adoption and is still led more by private hospital pilots than broad public deployment. That mix keeps North America central to the AI in patient scheduling software market because it combines technology readiness with strong financial pressure to recover labor hours and appointment capacity.

Europe remains a structurally important region in the AI in patient scheduling software market because it combines healthcare digitization with stricter compliance expectations. The United Kingdom, Germany, and France form the core demand base, while Scandinavia and the Benelux region show strong digital health spending and receptiveness to workflow automation. European growth is therefore steady, but vendor selection tends to be more sensitive to governance, integration, and procurement process than in faster commercial markets.

Asia-Pacific is projected to be the fastest-growing region in the AI in patient scheduling software market with a 28.31% CAGR through 2031. The region is being driven by hospital digitization programs in China, primary care infrastructure buildout in India, and growing pressure in Japan to manage aging populations with constrained clinical labor. These conditions create demand for cloud-based scheduling, centralized provider coordination, and front-office automation at scale. South Korea and Australia also support enterprise adoption through broader digital health programs, while the Middle East and Africa remain earlier in maturity but show targeted opportunity in GCC hospital expansion programs. South America is led by large private hospital groups in urban centers, but public adoption still moves more slowly because legacy IT systems and budget cycles constrain implementation. This regional split means the AI in patient scheduling software market is broadening globally, but the fastest gains are still concentrated where digitization mandates and provider capacity pressure are moving together.

Competitive Landscape

The AI in patient scheduling software market is moderately concentrated and has a competitive structure in which large EHR-linked vendors hold an advantage at the enterprise level, while specialists compete on workflow depth and operational outcomes. Epic Systems and Oracle Health benefit from bundled scheduling relationships, which lowers switching appetite among large health systems already committed to those ecosystems. At the same time, the AI in patient scheduling software market remains open enough for specialist vendors to grow because many providers still need stronger search, triage, rescheduling, and workflow automation than bundled tools provide. Luma Health, NexHealth, Phreesia, and Zocdoc compete more directly in patient engagement and self-scheduling, where differentiation rests on EHR integration, communication channels, and automation breadth.

A second competitive shift is coming from agentic AI, which is pushing the AI in patient scheduling software market beyond transaction handling and toward autonomous front-office execution. Qventus introduced its AI Solution Factory in September 2025 as a co-development model that allows health systems to build custom operational assistants with vendor engineering support. That move matters because large provider systems often need local workflow design that generic scheduling products cannot deliver. The AI in patient scheduling software market is therefore rewarding vendors that can combine platform scale with health-system-specific workflow design.

Recent product releases also show how fast the AI in patient scheduling software market is widening from booking into adjacent administrative tasks. Luma Health expanded its Operational AI capabilities in 2026 with automated no-show rescheduling, care gap closure support, and batch waitlist outreach, which pushed its platform further into routine access operations. Competitive intensity is moderate, but it is rising because new capital, faster release cycles, and broadening workflow scope are increasing pressure on both incumbents and specialists to deliver measurable operational value.

AI In Patient Scheduling Software Industry Leaders

Epic Systems Corporation

Veradigm LLC

Zocdoc

Relatient

Luma Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Luma Health released its Spring 2026 Operational AI update, introducing automated no-show rescheduling via its Navigator tool, intelligent care gap closure via Fax Transform, and batched waitlist outreach that fills open slots without staff intervention. The release built on platform workflows that had saved 2.5 million staff hours and completed 350,000+ care-related next steps, marking a substantive expansion of the operational AI perimeter for clinic and health system customers.

- March 2026: cibX GmbH announced the ORCHESTRA project in Hamburg, a next-generation real-time clinical process scheduling system using speech, motion, and location recognition to generate adaptive AI scheduling decisions in acute hospital settings, covering emergency intake through inpatient care to discharge coordination. The project represents a material advance in real-time AI-driven hospital operations in Europe.

- February 2026: Qventus announced Erlanger Health System's results since deploying its Surgical Growth Solution in June 2025, with the Tennessee-based multi-hospital system on track to deliver a 5x annualized ROI across 4 sites, demonstrating that AI surgical scheduling can generate measurable financial returns within 6 months of implementation.

- February 2026: Luma Health shared momentum from its Operational AI platform, highlighting that AI workflows had saved 2.5 million hours across health systems in 2025, and confirming continued platform expansion in 2026 across Epic, Oracle Health, MEDITECH, eClinicalWorks, and athenahealth ecosystems.

Global AI In Patient Scheduling Software Market Report Scope

According to the report’s scope, the AI in patient scheduling software market refers to the use of artificial intelligence technologies to automate, optimize, and manage patient appointment scheduling across healthcare settings. These solutions leverage machine learning, predictive analytics, and workflow automation to improve appointment allocation, reduce no-shows, optimize provider utilization, enhance patient access, and streamline administrative operations.

The AI in patient scheduling software market is segmented into scheduling type, deployment mode, end-user, and geography. By scheduling type, the market is segmented into outpatient scheduling, inpatient scheduling, specialty care scheduling, emergency and urgent care scheduling, and other scheduling types. By deployment mode, the market is segmented into cloud-based and on-premises. By end-user, the market is segmented into hospitals, clinics, diagnostic and imaging centers, ambulatory surgical centers, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Outpatient Scheduling |

| Inpatient Scheduling |

| Specialty Care Scheduling |

| Emergency and Urgent Care Scheduling |

| Other Scheduling Types |

| Cloud-Based |

| On-Premises |

| Hospitals |

| Clinics |

| Diagnostic and Imaging Centers |

| Ambulatory Surgical Centers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Scheduling Type | Outpatient Scheduling | |

| Inpatient Scheduling | ||

| Specialty Care Scheduling | ||

| Emergency and Urgent Care Scheduling | ||

| Other Scheduling Types | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By End-User | Hospitals | |

| Clinics | ||

| Diagnostic and Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of AI in patient scheduling software?

The market generated USD 79.80 million in 2025 and reached USD 99.02 million in 2026, it is forecasted to reach USD 311.22 million by 2031, at a 25.74% CAGR, which reflects strong expansion in provider demand for administrative automation.

Which scheduling type leads revenue today?

Outpatient scheduling leads with a 43.17% share in 2025 because high-volume ambulatory settings see a clear return from reducing no-shows and filling canceled slots faster.

Which deployment model is gaining the most traction?

Cloud-based deployment leads with 79.73% share in 2025 and is also the fastest-growing at 27.36% CAGR, showing that buyers prefer scalable, EHR-connected platforms.

Which region is expanding the fastest?

Asia-Pacific is expected to be the fastest-growing region at a 28.31% CAGR through 2031 as digitization mandates and hospital procurement programs accelerate across major healthcare systems.

Page last updated on: