AI In Medication Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 4.11 Billion |

| Growth Rate (2026 - 2031) | 11.41% CAGR |

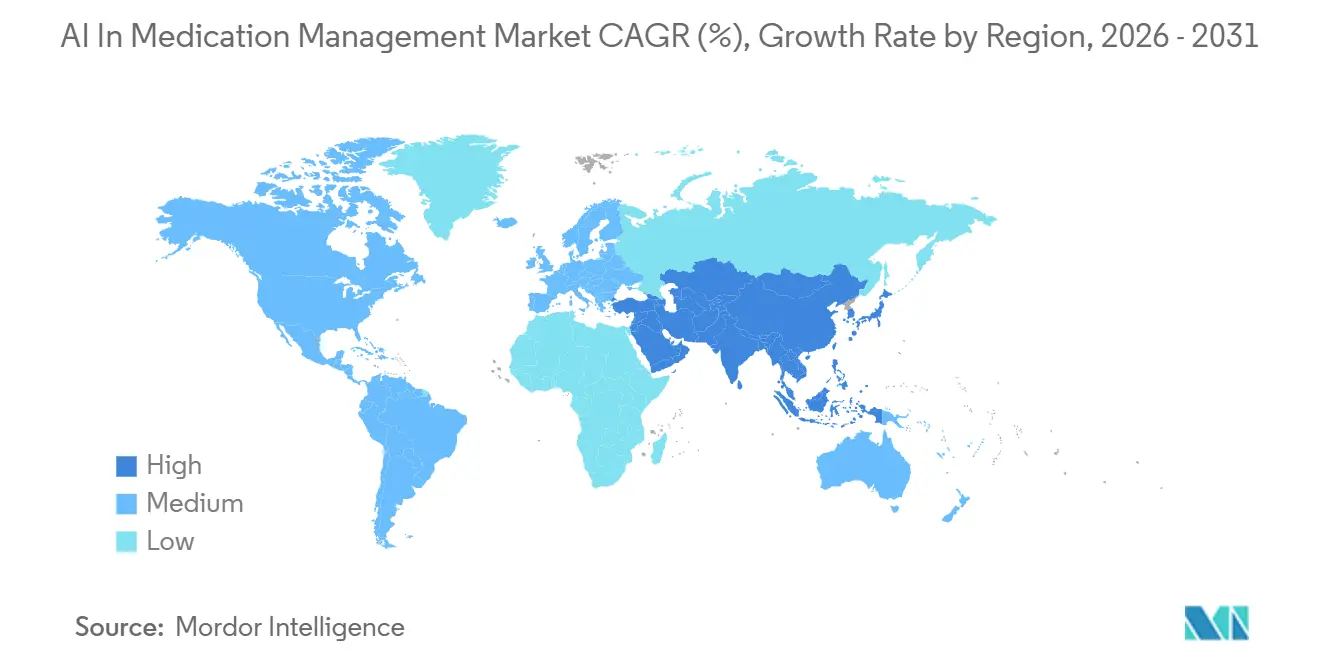

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

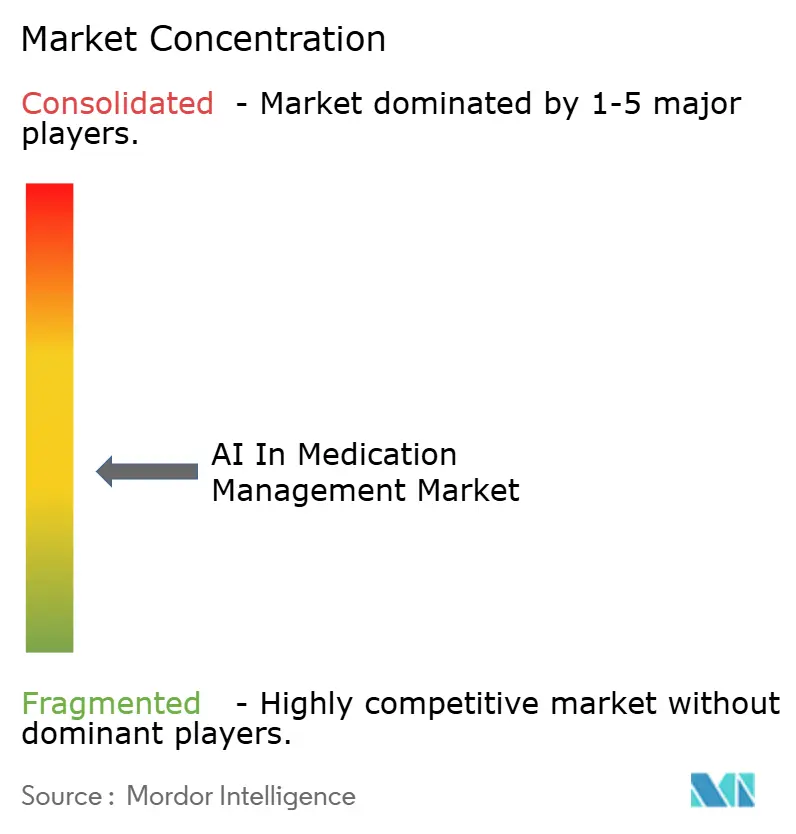

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Medication Management Market Analysis by Mordor Intelligence

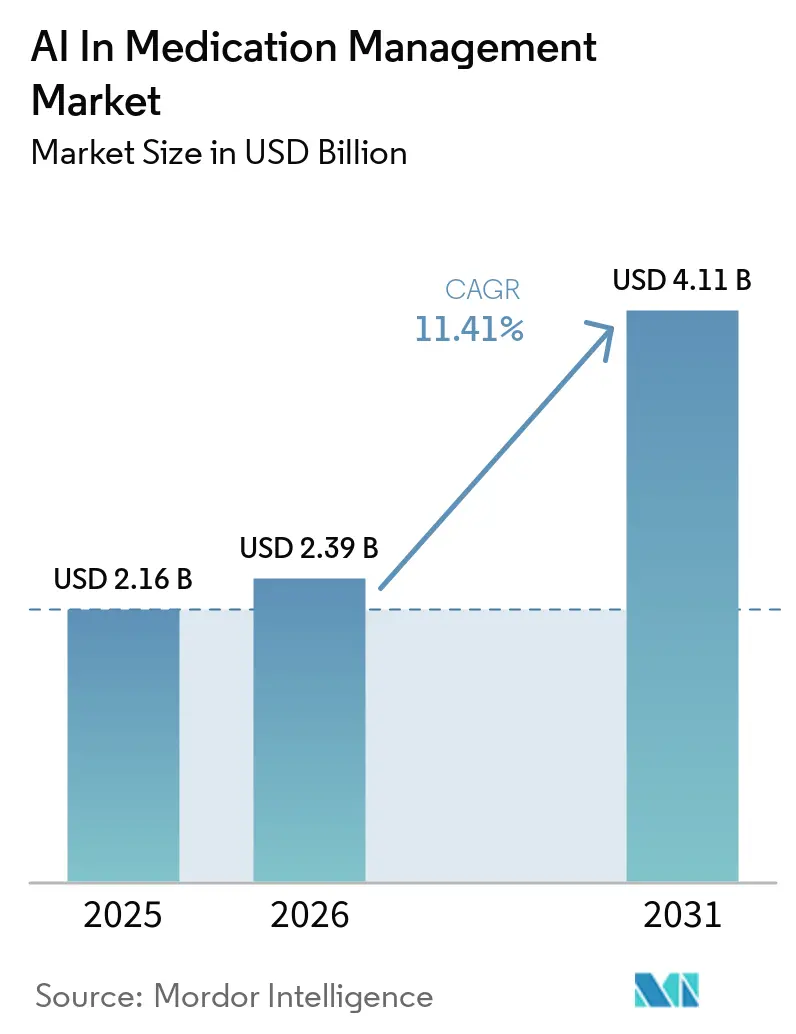

The AI In Medication Management Market size is expected to grow from USD 2.16 billion in 2025 to USD 2.39 billion in 2026 and is forecast to reach USD 4.11 billion by 2031 at 11.41% CAGR over 2026-2031.

The AI in medication management market is being supported by the persistent burden of adverse drug events, which continue to raise treatment costs and clinical risk across hospital settings. It is also benefiting from rising polypharmacy among older adults, where medication review, interaction checking, and deprescribing support are becoming harder to manage through manual workflows alone. Cloud-connected pharmacy systems and AI-enabled adherence programs are widening the addressable use case base, especially where providers and payers can connect medication performance to operational savings and quality-linked revenue. The AI in medication management market is therefore moving beyond isolated pilots and toward embedded workflow deployment, although validation requirements, interoperability gaps, and clinician trust issues still slow full production rollouts. Competitive activity reflects that shift, with large platform vendors deepening EHR, dispensing, and cloud integration while focused specialists expand around adherence, precision dosing, prior authorization, and pharmacovigilance use cases.

Key Report Takeaways

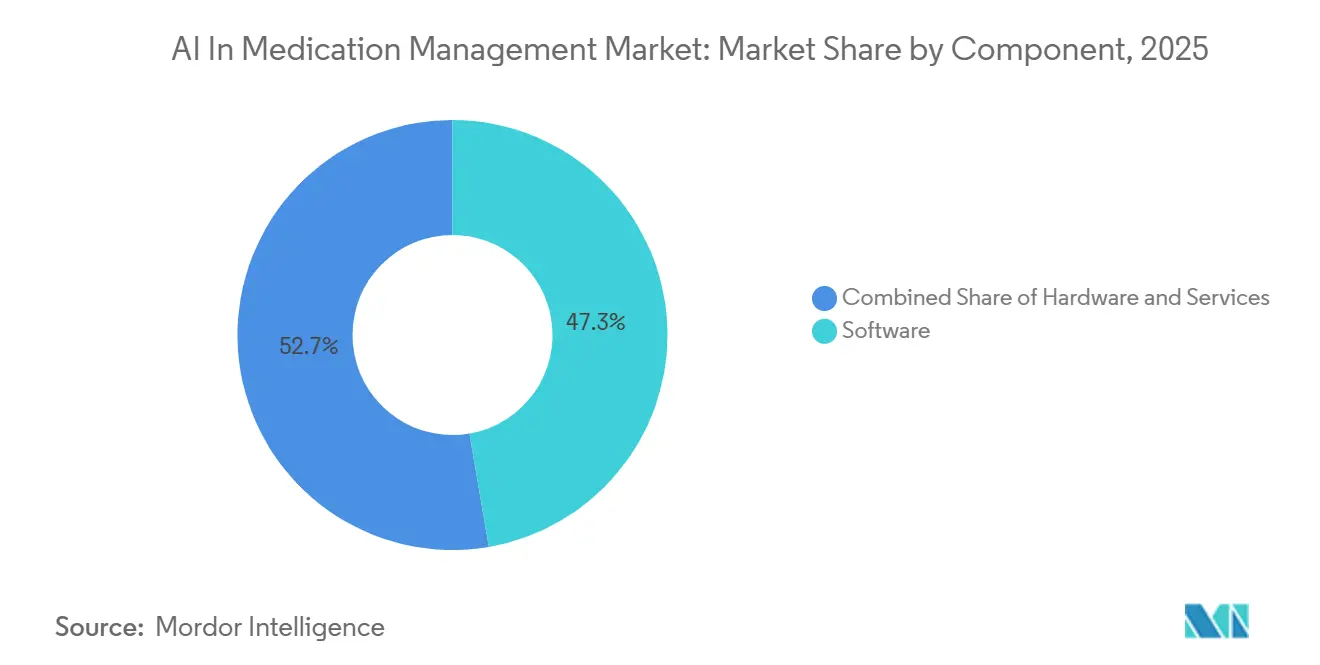

- By component, software led with 47.32% revenue share in 2025, while services are forecast to expand at 11.73% CAGR through 2031.

- By deployment mode, cloud-based systems held 64.73% of the market in 2025, while on-premises deployment recorded the highest projected CAGR at 11.32% through 2031.

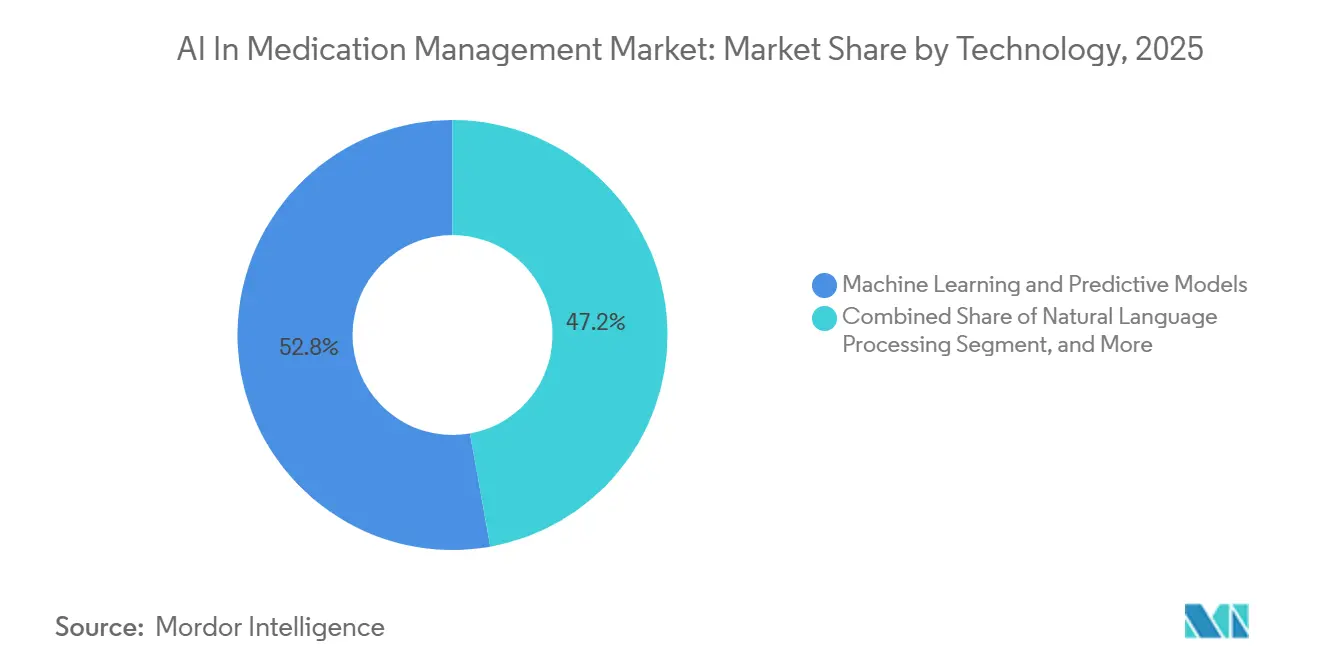

- By technology, machine learning and predictive models accounted for 52.81% share in 2025, while natural language processing is advancing at 12.62% CAGR through 2031.

- By application, medication adherence and engagement held 38.08% share in 2025, while medication decision support and interaction checking are projected to grow at 14.29% CAGR through 2031.

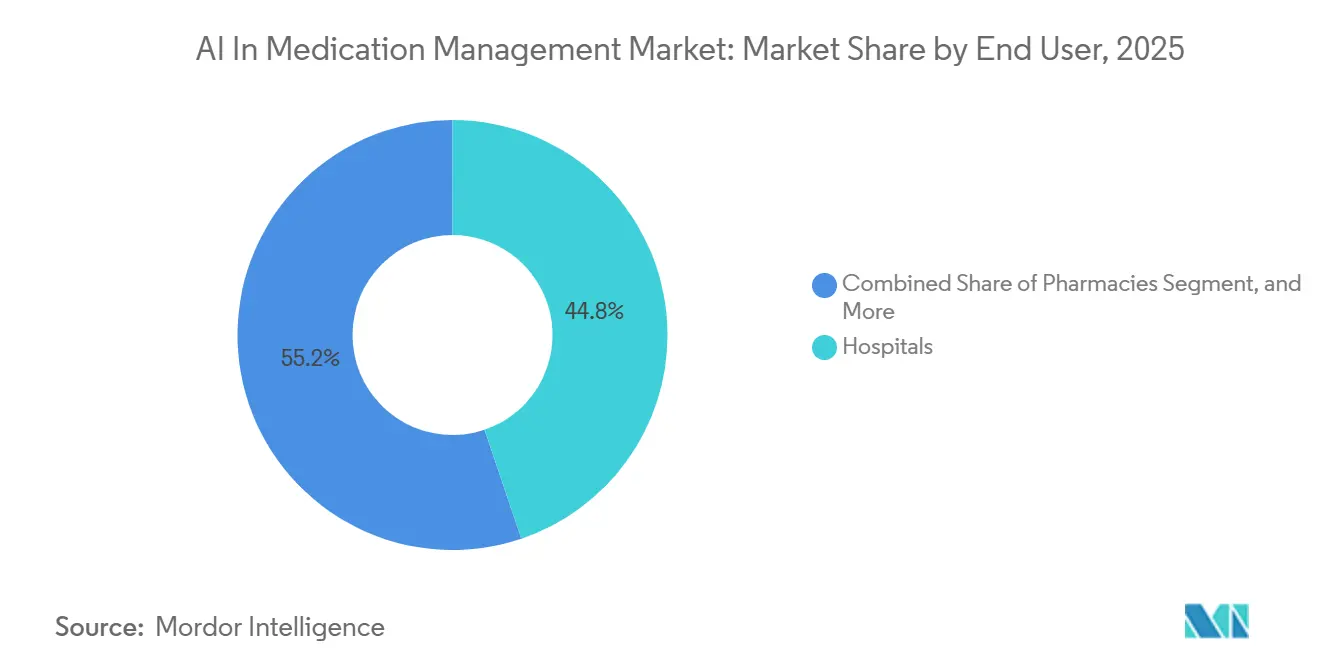

- By end user, hospitals held 44.83% share in 2025, while pharmacies are forecast to expand at 12.58% CAGR through 2031.

- By geography, North America held 38.43% of revenue in 2025, while Asia-Pacific is expected to record the fastest growth at 13.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Medication Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Medication Error and ADE Burden | +2.4% | Global | Short term (≤ 2 years) |

| Polypharmacy and Complex Regimen Complexity | +1.8% | Global, with highest intensity in North America & Europe | Medium term (2-4 years) |

| Expansion of Cloud Connected Medication Workflows | +2.1% | North America & APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Growth of AI Enabled Medication Adherence Programs | +1.6% | Global | Medium term (2-4 years) |

| Drug Shortage Orchestration and Substitution Intelligence | +1.0% | North America & Europe | Medium term (2-4 years) |

| Value Based Pharmacy Economics and Quality Incentives | +0.8% | North America, with early gains in UK and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Medication-Error and ADE Burden

The AI in medication management market continues to gain support from the high clinical and financial burden tied to medication errors and adverse drug events. A November 2025 evaluation in Frontiers in Pharmacology reported 1.8 million adverse drug events annually among hospitalized patients in the United States, with 9,000 associated deaths and more than USD 40 billion in related costs.[1]Aaron Chase, Amoreena Most, Shaochen Xu, et al., “Large Language Models Management of Complex Medication Regimens, A Case-Based Evaluation,” Frontiers in Pharmacology, frontiersin.org Separate evidence in BMC Medical Informatics and Decision Making showed that unintended ADEs affected 5% of the more than 36 million hospitalized patients in the United States each year, while annual treatment costs exceeded USD 1.5 billion. This burden is pushing providers toward AI systems that can review prescriptions and monitor risk signals continuously, because manual review becomes less reliable as medication volumes rise and care teams face higher alert loads. A 2025 systematic review in Digital Health found that 85% of AI-generated alerts were clinically valid and 43% led to order revisions, which helps explain why hospitals are treating AI review layers as a practical response to persistent medication safety failures.[2]Saad S. Alqahtani, Santhosh Joseph Menachery, et al., “Artificial Intelligence in Clinical Pharmacy, A Systematic Review of Current Scenario and Future Perspectives,” Digital Health, pmc.ncbi.nlm.nih.gov

Polypharmacy and Complex-Regimen Complexity

The AI in medication management market is also being lifted by the growing complexity of regimens used by older adults and patients with multiple chronic conditions. A 2024 review in Healthcare reported polypharmacy prevalence at 30.2% among community-dwelling individuals and 61.7% among hospitalized patients, showing how widely complex medication use is now embedded in care deliver. The same body of evidence showed that each additional medication raised adverse-event risk by 12% to 18%, which increases the value of AI tools that can surface interaction risk and identify candidates for deprescribing. The ABiMed study published in 2025 estimated savings of EUR 273 (USD 298) per patient-year through reduced emergency department visits, which turns medication review from a clinical necessity into a measurable efficiency lever. A 2025 scoping review in Cureus found that AI tools were effective in detecting potentially inappropriate medications and recurring multimorbidity patterns in adults aged 50 and older, which supports steady platform demand as these patient cohorts expand.

Expansion of Cloud-Connected Medication Workflows

The AI in medication management market is moving forward as hospitals and pharmacies connect medication workflows to cloud-based data layers that support enterprise visibility and remote decision-making.[3]NYC Health + Hospitals, “NYC Health + Hospitals Upgrades to State-of-the-Art Medication Management Technology,” NYC Health + Hospitals, nychealthandhospitals.org NYC Health + Hospitals migrated to centralized cloud-based medication management in 2024 across a network that dispenses more than 22 million doses annually, which reduced manual nursing tasks and enabled remote order management with real-time inventory tracking. Amazon Pharmacy stated that AWS Bedrock and Comprehend Medical help automate prescription processing and provide upfront pricing estimates on 99% of prescriptions, while AI-based labor planning improved forecasting accuracy by 50% against the industry-standard MAPE target. Dedalus MedChart's deployment at MidCentral in New Zealand saved 16 to 27 minutes per inpatient on medication management and cut initial pharmacy review time by as much as 110 minutes per patient, showing that workflow value is becoming visible at the unit level instead of only at enterprise scale. At the same time, the AI in medication management market is not moving toward a cloud-only structure, because hospitals with strict sovereignty requirements are expanding hybrid and local inference models rather than abandoning connected architectures altogether.

Growth of AI-Enabled Medication Adherence Programs

The AI in medication management market is seeing sustained demand from adherence programs because long-term medication use still breaks down at scale across chronic care pathways. A 2025 narrative review in Frontiers in Pharmacology stated that 50% of patients with long-term treatments worldwide do not take medicines as prescribed, which leaves a large base of avoidable deterioration and cost in place. A focused review in Frontiers in Digital Health found that AI-based adherence tools improved medication compliance by 6.7% to 32.7% against controls and existing practice, which supports broader adoption across payer and provider settings. The REINFORCE trial published in npj Digital Medicine reported a 13.6 percentage-point gain in pill-bottle adherence versus control, while predictive accuracy improved over the course of the 6-month study, showing that these systems can adapt to individual patient response patterns. Arine reported that its AI platform covered more than 30 million members and delivered more than USD 1,500 in annual savings per engaged Medicaid member together with a greater than 40% reduction in inpatient admissions, which explains why payer contracts are moving beyond small pilots.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and AI Validation Burden | -1.5% | Global | Medium term (2-4 years) |

| EHR and Pharmacy System Interoperability Gaps | -1.2% | Global | Short term (≤ 2 years) |

| Alert Fatigue and Low Clinician Trust in AI Outputs | -1.0% | Global | Medium term (2-4 years) |

| Liability and Auditability Constraints in High Risk Workflows | -0.7% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and AI Validation Burden

The AI in medication management market still faces a meaningful adoption barrier from data privacy controls, internal governance reviews, and model validation requirements. Regulatory expectations moved higher as the FDA had authorized more than 1,451 AI-enabled medical devices by December 2025, including 295 new authorizations in 2025, while the Predetermined Change Control Plan framework required manufacturers to define future algorithm modifications in advance and monitor model drift after deployment. A national survey of 941 academic physicians published in JMIR AI found that 62% cited bias from unrepresentative training data as a core concern, and 78.9% worried about clinical errors attributable to AI systems. The FDA's January 2026 guidance for certain transparent clinical decision support tools lowered the burden for some categories, but health systems still maintain stricter internal review processes for prescribing and pharmacovigilance use cases where patient risk is higher. This means the AI in medication management market is expanding under tighter compliance discipline, not under a light-touch regulatory setting.

EHR and Pharmacy-System Interoperability Gaps

The AI in medication management market is also constrained by the uneven ability of EHR and pharmacy systems to exchange and reconcile data across settings. Although more than 96% of U.S. non-federal acute care hospitals used certified EHR systems, only 70% performed all 4 key interoperability functions as recently as 2023, which shows that digitization has not yet produced full medication data continuity. Research in JMIR Medical Informatics found that 22.2% of pediatric patients with new psychotropic prescriptions did not fill them within 30 days, and that kind of mismatch between prescribing records and dispensing records can distort adherence models when the systems are not linked. A 2025 scoping review on medication reconciliation found that only 16% of reviewed AI models had reached deployed status, with interoperability repeatedly identified as the main hurdle between algorithm development and clinical use. The AI in medication management market will keep advancing, but deployment speed will remain uneven until health systems can connect order, dispensing, refill, and medication history data with less friction across care settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Infrastructure Anchors Platform Value

Software accounted for 47.32% of the AI in medication management market size in 2025, which made it the largest component within the AI in medication management market. That position reflects the recurring revenue profile of SaaS-based clinical decision support, adherence, and pharmacovigilance tools, which can be updated continuously without waiting for hardware replacement cycles. Epic's direct embedding of AI within medication workflows supports this pattern, because more than 85% of its customer base used at least 1 AI tool and Summit Health reduced prior authorization submission time by 42% through Epic's Penny AI agent. In the AI in medication management industry, that level of workflow embedding matters more than standalone feature breadth, because medication teams are adopting tools that reduce clicks and review time inside systems they already use.

Services are projected to grow at 11.73% CAGR through 2031, which shows that deployment support is expanding alongside software sales instead of being displaced by plug-and-play claims. Health systems are increasingly outsourcing validation, integration engineering, and staff change management because internal clinical AI expertise remains scarce relative to implementation ambition. Hardware remains structurally important because smart dispensing devices, connected adherence sensors, and robotic systems are still the physical control points where medication workflows become executable and measurable. Omnicell's Titan XT and cloud-linked OmniSphere architecture show that hardware value is increasingly tied to data generation and inventory intelligence, not only to cabinet replacement demand.

By Deployment Mode: Cloud Leads While On-Premises Rebounds in Sensitive Settings

Cloud-based deployment held 64.73% share in 2025, giving it the leading position in the AI in medication management market. This lead comes from enterprise-wide visibility, lower upfront capital needs, and the ability to centralize medication operations across hospitals, pharmacies, and distribution nodes. BD stated that its AWS-hosted Incada Connected Care Platform processes more than 9.8 million daily medication dispensing transactions from the installed Pyxis base, which shows the data throughput now supporting real-time AI inference at the point of care. Within the AI in medication management market, cloud scale is therefore tied to both workflow unification and data density rather than to hosting preference alone.

On-premises deployment is expected to expand at 11.32% CAGR through 2031, which makes it the fastest-growing mode despite cloud leadership. Hospitals in sovereignty-sensitive jurisdictions are choosing local inference and local data processing for high-risk clinical use cases, especially where encryption, auditability, and national security standards remain strict. Jingzhou Central Hospital's August 2025 AI digital pharmacist deployment used locally deployed databases covering more than 100,000 drug types with medical-grade encrypted data, which shows why on-premises demand is rising in parts of Asia. Hybrid models are therefore gaining ground as a practical middle path, especially where systems want cloud analytics but cannot move full clinical datasets outside local environments.

By Technology: Machine Learning Leads, but NLP Closes the Clinical Text Gap

Machine learning and predictive models held 52.81% of the AI in medication management market size in 2025, which kept them in the leading technology position. Their lead is rooted in long-running use cases such as adverse drug event surveillance, interaction scoring, medication review, and inventory risk forecasting, where once-deployed models are rarely replaced quickly. A 2025 systematic review in Digital Health reported 97.93% accuracy for a CC+CatBoost ensemble detecting potentially inappropriate medications across 18,338 older adults in 8 Chinese cities, which illustrates the precision achievable with large institution-linked datasets. In the AI in medication management industry, the established model-based approach gives machine learning an installed advantage, even as newer AI approaches attract more attention.

Natural language processing is forecast to grow at 12.62% CAGR through 2031, making it the fastest-growing technology segment in the AI in medication management market. That momentum reflects expanding access to structured and semi-structured medication data as FHIR-based APIs scale and ambient clinical documentation tools become more common. FDB's March 2026 MedProof MCP launch is an example of this shift, because it allows AI agents to query structured medication intelligence directly and reduces integration burden for developers building agentic medication workflows. Generative AI and computer vision are also expanding, but current evidence still supports a human-in-the-loop role for high-acuity medication decisions rather than full autonomous substitution.

By Application: Adherence Anchors Volume, Decision Support Leads Forecast Growth

Medication adherence and engagement held 38.08% share in 2025, making it the largest application area in the AI in medication management market. This lead reflects the scale of nonadherence in chronic care and the fact that adherence gains can be linked to measurable savings, reduced admissions, and quality-linked payer performance. Arine reported more than USD 4,300 in per-member savings for Medicaid behavioral health populations and a 50% reduction in behavioral health polypharmacy, which shows why adherence tools have become financially visible to payers and PBMs. The AI in medication management market therefore, still draws much of its current volume from engagement, refill, and medication therapy management workflows rather than from fully autonomous prescribing support.

Medication decision support and interaction checking are projected to expand at 14.29% CAGR through 2031, which makes it the fastest-growing application area. That growth reflects the rise of ambient documentation and NLP pipelines that can convert clinical conversation into order suggestions, interaction screening, and more structured review before orders are finalized. Oracle Health stated in February 2026 that its Clinical AI Agent had already saved U.S. doctors more than 200,000 hours of documentation time, which indicates how quickly workflow capture tools are becoming part of routine prescribing environments. Prescription verification, medication reconciliation, shortage optimization, precision dosing, and pharmacovigilance continue to expand as adjacent use cases, but decision support is where documentation automation and medication intelligence are currently converging most directly.

By End User: Hospitals Command Share While Pharmacies Drive Future Growth

Hospitals held 44.83% of the AI in medication management market share in 2025, which kept them as the largest end-user group. Their position comes from the concentration of high-acuity medication tasks, the scale of integrated dispensing infrastructure, and the fact that hospital systems can spread AI tools across inpatient order verification, inventory management, prior authorization, and transitions of care. Mount Sinai Health System's pharmacy AI strategy spans inpatient verification, prior authorization, inventory optimization, and ambulatory transitions integrated with Epic, which shows the breadth of deployment that large health systems can support. In the AI in medication management industry, hospitals also remain the most important proving ground for vendors that need large workflow volumes and complex clinical environments to validate product performance.

Pharmacies are forecast to grow at 12.58% CAGR through 2031, making them the fastest-growing end-user segment in the AI in medication management market. That growth is linked to value-based pharmacy models, prior authorization automation, and direct-to-patient fulfillment workflows where AI can shorten turnaround times and improve intervention targeting. At Ochsner Health, Latent Health's AI reduced specialty prior authorization review time to an average of 4 minutes and increased monthly throughput by 96% after full-network scaling in 2025, which explains why specialty and retail channels are increasing AI investment. Home care, virtual care, payers, PBMs, and life sciences companies remain smaller in current share terms, but they continue to expand as medication management shifts toward decentralized monitoring and post-market safety analytics.

Geography Analysis

North America held 38.43% of the AI in medication management market share in 2025, which kept it as the largest regional contributor. The region benefits from high EHR penetration, mature value-based reimbursement, and a provider base that is already integrating AI into prescribing, documentation, dispensing, and specialty pharmacy workflows. Utah's January 2026 state-backed autonomous refill program is especially important because it allows AI to participate legally in prescription renewals for 190 chronic-condition medications and tracks refill timeliness, patient safety, adherence outcomes, and cost effects. Oracle's Clinical AI Agent expansion and large-scale distribution and dispensing automation by companies such as McKesson, BD, and Omnicell show that North America is moving from pilots toward embedded operational infrastructure. The region still faces alert fatigue, bias concerns, and governance friction, but it remains the most active commercial environment for scaling the AI in medication management market.

Europe is the second-largest regional market in the AI in medication management market, supported by hospital digitalization programs and a regulatory push toward safer medication data use. Germany's Krankenhauszukunftsgesetz allocated EUR 4.3 billion (USD 4.7 billion) to hospital digitalization, which created a clear demand base for medication workflow modernization across hospital systems. BD's March 2026 partnership with Sinteco added advanced unit-dose robotics and drug traceability capabilities for European hospitals, reflecting continued investment in the connection between automation hardware and medication data visibility. The region's regulatory structure is raising compliance costs, but it also favors vendors that can document validation, traceability, and workflow safety at scale.

Asia-Pacific is forecast to grow at 13.09% CAGR through 2031, making it the fastest-growing regional segment in the AI in medication management market. Japan's pharmacy digitalization programs have created a strong operating base, and by May 2025, Nihon Chouzai had deployed its AI medication history creation service across all 763 pharmacies, cutting daily manual documentation time and giving pharmacists more time for patient interaction. China is also showing measurable clinical use, with Shandong Provincial Second People's Hospital reporting a 99.7% medication error interception rate and a 70% increase in patient pharmaceutical monitoring coverage during 2025 trial operations. South Korea and India are expanding digital health infrastructure that can support pharmacy AI deployment, while Middle East and Africa and South America remain earlier-stage opportunity pools led by healthcare digitalization and specialty pharmacy demand in selected countries. Infrastructure and interoperability constraints still limit near-term penetration outside the most advanced systems, but the regional growth profile keeps Asia-Pacific central to the long-term expansion path of the AI in medication management market.

Competitive Landscape

The AI in medication management market is moderately fragmented, with large platform vendors competing alongside specialized companies that focus on narrower but high-value workflow problems. Becton, Dickinson and Company, Omnicell, Oracle Health, and Epic Systems hold an institutional advantage because they can connect AI functionality to established hardware footprints, EHR environments, and distribution-scale data networks. The AI in medication management market therefore rewards vendors that can shorten deployment time inside existing workflows rather than vendors that offer isolated tools with limited integration paths. That structure keeps entry possible for specialists, but it raises the commercial value of interoperability, installed base reach, and regulatory discipline.

BD has been using its Pyxis footprint and new Incada Connected Care Platform to turn connected dispensing infrastructure into a high-volume medication data layer that supports analytics and AI-driven visibility across care settings. Omnicell has followed a similar path through OmniSphere and Titan XT, where the strategic goal is to connect robotics and dispensing systems to a common cloud workflow engine and improve stock risk prediction and enterprise inventory control. Oracle Health is taking the EHR-layer route by embedding ambient listening and automated order creation into the clinical workflow, which makes medication AI part of documentation and ordering rather than a separate procurement decision. Epic is also widening the competitive field through its Agent Factory and custom model strategy, which gives health systems more freedom to build AI agents inside Epic workflows while still remaining within the EHR environment. These moves show that leading companies are not only adding features, but they are also trying to control the operating layer where medication data, clinical context, and AI orchestration meet.

Specialists still have room to win contracts where outcomes are easier to quantify, and workflow pain is highly concentrated. Arine has positioned itself around payer-side medication optimization, while Latent Health showed strong traction in specialty pharmacy prior authorization at Ochsner Health. FDB's MedProof MCP also points to a new line of competition around open agent interoperability and structured medication intelligence, where standards can become a differentiator instead of only product features. The AI in medication management market is unlikely to consolidate into a winner-take-all structure in the near term, because hospitals, pharmacies, and payers continue to buy a mix of integrated platforms and targeted point solutions based on workflow need and deployment readiness.

AI In Medication Management Industry Leaders

Omnicell

Becton, Dickinson and Company

Epic Systems Corporation

McKesson Corporation

Oracle Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BD and Sinteco signed a European technological partnership to deploy advanced unit-dose medication packaging robotics across hospitals, enabling full drug traceability from manufacturer bulk supplies to individual patient doses and integration with hospital information systems.

- February 2026: Oracle Health expanded its Clinical AI Agent to include automated order creation using ambient listening during clinical appointments, covering laboratory, imaging, and prescription orders. The agent has reportedly saved US doctors over 200,000 hours of documentation time since its initial launch.

- October 2025: BD launched the BD Incada Connected Care Platform alongside the next-generation BD Pyxis Pro Automated Medication Dispensing Solution, built on AWS with AI-powered natural language analytics across data from nearly 3 million smart connected BD devices, providing enterprise-wide medication inventory visibility.

- September 2025: BD and Henry Ford Health signed the first-of-its-kind US pharmacy automation partnership to develop the "health system pharmacy of the future," deploying the BD Rowa Vmax robotic storage system for 24/7 patient prescription pickup at Southeast and Central Michigan hospital-based community pharmacies.

Global AI In Medication Management Market Report Scope

The AI in Medication Management Market refers to the industry segment focused on software, platforms, and devices that use artificial intelligence (machine learning, natural language processing, and predictive analytics) to optimize how drugs are prescribed, dispensed, tracked, and consumed to improve patient safety and treatment outcomes.

The AI in Medication Management Market Report is Segmented by Component (Software, Services, Hardware), Deployment Mode (Cloud-Based, Hybrid, On-Premises), Technology (Machine Learning and Predictive Models, Natural Language Processing, Computer Vision, Generative AI Assistants, Other Technologies), Application (Medication Decision Support and Interaction Checking, Medication Adherence and Engagement, Prescription and Order Verification, Medication Reconciliation, Inventory and Shortage Optimization, Precision Dosing and Therapy Optimization, ADE Surveillance and Pharmacovigilance), End User (Hospitals, Pharmacies, Payers and PBMs, Pharmaceutical and Life Sciences Companies, Home Care and Virtual Care Providers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | |

| Hardware | Smart Dispensing and Verification Devices |

| Connected Adherence Sensors and Devices | |

| Robotic Dispensing and Packaging Systems |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Machine Learning and Predictive Models |

| Natural Language Processing |

| Computer Vision |

| Generative AI Assistants |

| Other Technologies (Graph and Rules-Augmented Reasoning, etc.) |

| Medication Decision Support and Interaction Checking |

| Medication Adherence and Engagement |

| Prescription and Order Verification |

| Medication Reconciliation |

| Inventory and Shortage Optimization |

| Precision Dosing and Therapy Optimization |

| ADE Surveillance and Pharmacovigilance |

| Hospitals |

| Pharmacies |

| Payers and PBMs |

| Pharmaceutical and Life Sciences Companies |

| Home Care and Virtual Care Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware | Smart Dispensing and Verification Devices | |

| Connected Adherence Sensors and Devices | ||

| Robotic Dispensing and Packaging Systems | ||

| By Deployment Mode | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Technology | Machine Learning and Predictive Models | |

| Natural Language Processing | ||

| Computer Vision | ||

| Generative AI Assistants | ||

| Other Technologies (Graph and Rules-Augmented Reasoning, etc.) | ||

| By Application | Medication Decision Support and Interaction Checking | |

| Medication Adherence and Engagement | ||

| Prescription and Order Verification | ||

| Medication Reconciliation | ||

| Inventory and Shortage Optimization | ||

| Precision Dosing and Therapy Optimization | ||

| ADE Surveillance and Pharmacovigilance | ||

| By End User | Hospitals | |

| Pharmacies | ||

| Payers and PBMs | ||

| Pharmaceutical and Life Sciences Companies | ||

| Home Care and Virtual Care Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the AI in medication management market?

The AI in medication management market was valued at USD 2.16 billion in 2025 and reached USD 2.39 billion in 2026, with forecasts pointing to USD 4.1 billion by 2031 at 11.41% CAGR.

Which application area is growing the fastest in this space?

Medication decision support and interaction checking is the fastest-growing application, with a projected 14.29% CAGR through 2031 as ambient documentation and NLP workflows expand.

Why are hospitals still the largest end users?

Hospitals held 44.83% share in 2025 because they manage the highest-acuity medication workflows and can deploy AI across verification, inventory, prior authorization, and care transitions.

Why are pharmacies expected to grow faster than hospitals?

Pharmacies are projected to grow at 12.58% CAGR through 2031 because prior authorization, specialty dispensing, adherence support, and direct-to-patient fulfillment are becoming more AI-enabled.

Which region leads adoption and which region is growing fastest?

North America led with 38.43% share in 2025, while Asia-Pacific is expected to grow the fastest at 13.09% CAGR through 2031.

Page last updated on: