Medical Scheduling Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

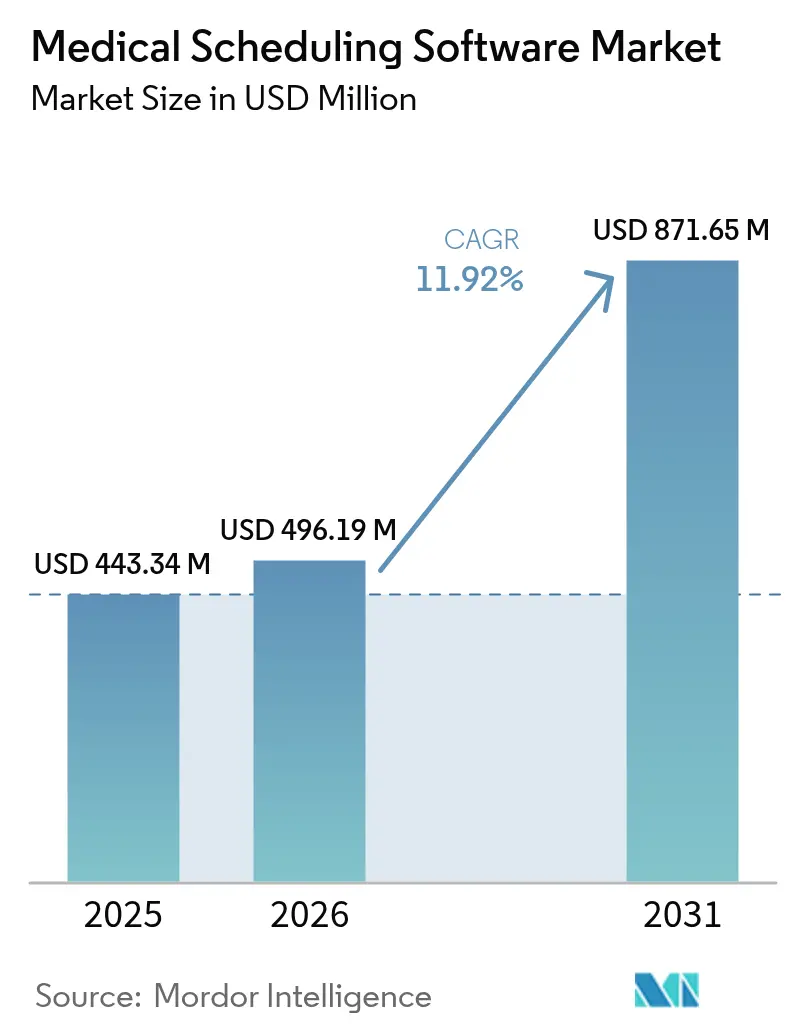

| Market Size (2026) | USD 496.19 Million |

| Market Size (2031) | USD 871.65 Million |

| Growth Rate (2026 - 2031) | 11.92% CAGR |

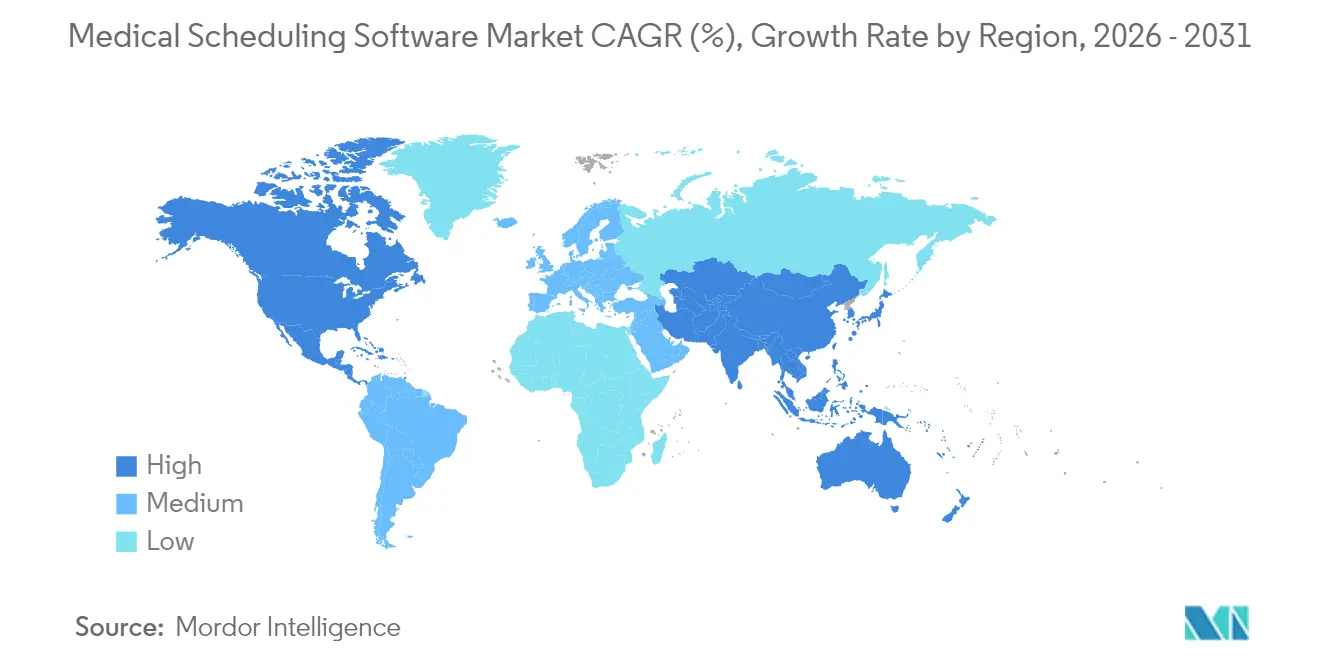

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

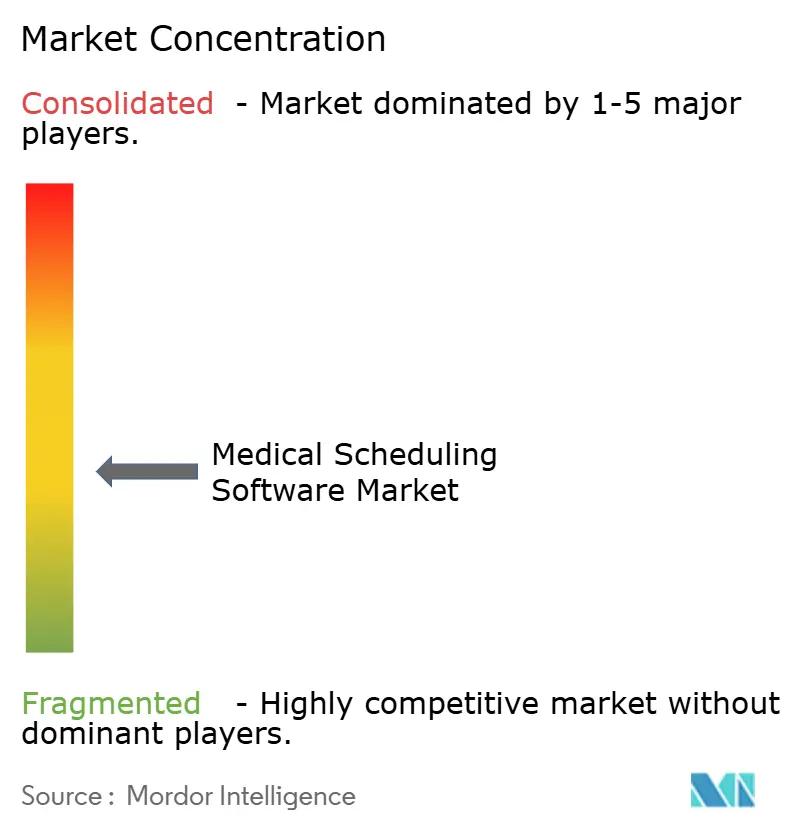

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Scheduling Software Market Analysis by Mordor Intelligence

The medical scheduling software market size in 2026 is estimated at USD 496.19 million, growing from 2025 value of USD 443.34 million with 2031 projections showing USD 871.65 million, growing at 11.92% CAGR over 2026-2031. The expansion of the medical scheduling software market is fueled by health-system digitization mandates, intensifying labor shortages, and higher scrutiny on operating margins. Hospitals are replacing fragmented calendars with unified platforms that cut appointment bottlenecks, trim overtime, and lower patient no-show rates [1]Office of the National Coordinator for Health Information Technology, “Health Data, Technology, and Interoperability: Certification Program Updates,” healthit.gov . Vendor consolidation, heightened regulatory pressure for interoperability, and growing consumer insistence on anytime, anywhere booking continue to reshape competitive strategies within the medical scheduling software market.

Key Report Takeaways

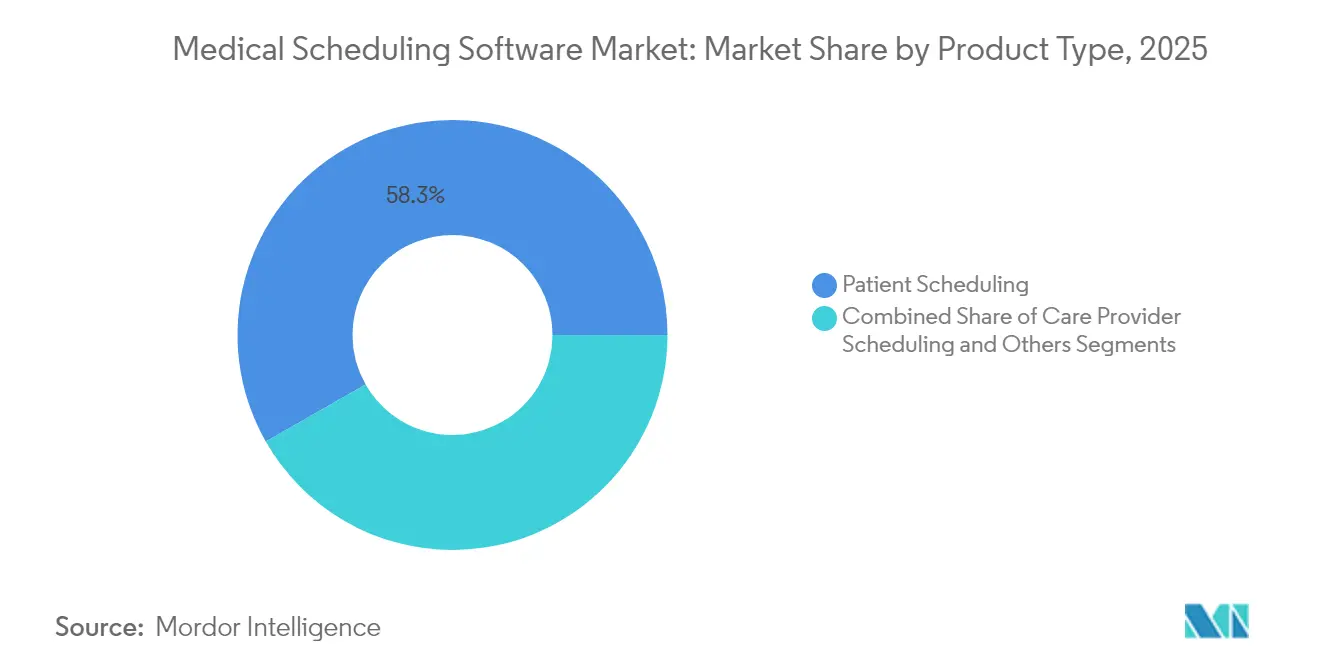

- By product type, patient scheduling software held 58.25% of the medical scheduling software market share in 2025, while care-provider scheduling is projected to post the fastest 12.64% CAGR through 2031.

- By deployment model, cloud deployment captured 69.10% of the medical scheduling software market size in 2025; hybrid deployment is forecast to advance at a 12.70% CAGR between 2026 and 2031.

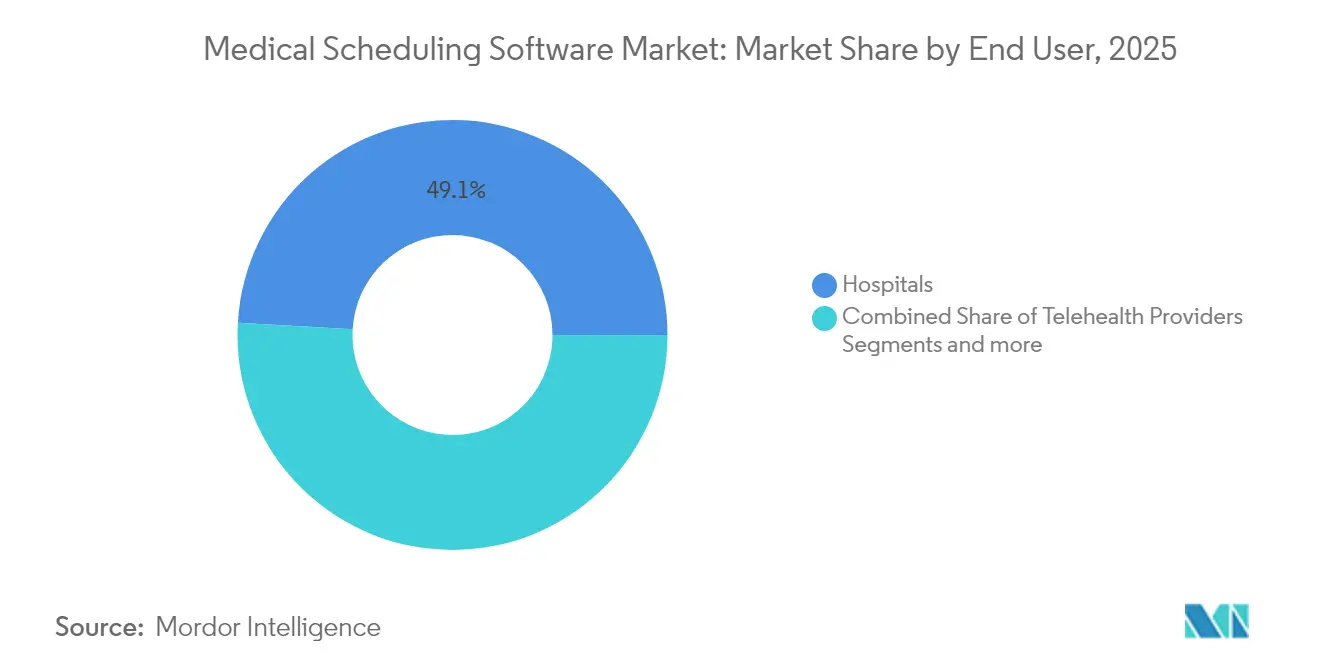

- By end user, hospitals accounted for 49.10% of end-user demand in 2025, whereas telehealth providers are expected to record a 12.78% CAGR to 2031.

- By specialty, primary care represented 61.50% of the medical scheduling software market size in 2025; behavioral and mental health scheduling is anticipated to grow at 12.95% CAGR through 2031.

- By geography, North America led with 42.10% revenue share in 2025, and Asia-Pacific is poised for the highest 13.02% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Scheduling Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficient workflow optimisation | +2.8% | North America & Europe lead | Medium term (2-4 years) |

| Patient-centric care adoption | +2.1% | Global, led by North America | Long term (≥ 4 years) |

| Cloud-native IT migration | +1.9% | Global | Short term (≤ 2 years) |

| Telehealth expansion | +1.7% | APAC & MEA surge | Medium term (2-4 years) |

| AI-driven capacity management | +1.4% | North America & Europe | Long term (≥ 4 years) |

| Real-time insurance verification | +1.2% | Mainly North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand to Efficiently Manage & Optimize Workflow

Manual appointment coordination consumes up to half a day of administrative time per month in the average ambulatory facility, driving leaders to automate template creation, wait-list handling, and resource balancing. A Florida-based health system saved USD 2 million in contract labor by shrinking the shift-planning cycle from three business days to less than four hours. Predictive scheduling has also dropped labor costs 8% at large academic centers, while simultaneously lifting provider satisfaction scores. Executives increasingly view streamlined scheduling as a lever to bolster net operating margins, curb staff burnout, and improve patient throughput [2]America's Essential Hospitals, "Unlocking Efficiency: How Predictive Scheduling Technology Sustainably Optimizes Staffing and Lowers Labor Costs," essentialhospitals.org.

Rising Adoption of Patient-Centric Care Models

Eight in ten U.S. consumers prefer to set appointments online, and more than half of self-service bookings originate from new patients. Digital convenience lowers missed-visit risk by 17% and enlarges clinics’ new-patient funnel by over one-third. Millennials remain the most prolific users, yet nearly 40% of bookings placed through self-scheduling portals come from patients aged >40 years. Providers that embed real-time slot visibility and automated reminders into websites and mobile apps are therefore outpacing peers on both acquisition and retention metrics.

Accelerated Shift Toward Cloud-Native Healthcare IT Stacks

Seventy percent of health-IT leaders already host at least one clinical application in the public cloud, and another 20% plan migrations by 2027. Early movers report USD 2 million in two-year savings versus on-premise systems, alongside 94% higher satisfaction with upgrade velocity. Cloud platforms simplify compliance reporting, enable instantaneous software rollouts, and support elastic scaling for consumer-facing booking volumes. As cost controls tighten, CFOs increasingly greenlight cloud-first scheduling deployments that can be activated in weeks instead of quarters.

Expansion of Telehealth & Remote Consultations

Virtual visits now account for roughly 1 in 4 outpatient encounters across large U.S. systems, requiring appointment workflows distinct from in-person care. Nearly 70% of bookings are placed on mobile devices and 43% occur outside standard office hours, forcing vendors to maintain always-on scheduling environments [3]Waseem Jerjes, "Telemedicine in the post-COVID era: balancing accessibility, equity, and sustainability in primary healthcare," Frontiers in Digital Health, frontiersin.org. Video consultations require pre-visit tech checks, automatic link distribution, and configurable visit lengths. Behavioral health presents additional complexity, holding the highest no-show probability even in virtual formats. Solutions that unify hybrid (in-clinic + virtual) templates and auto-route appointments by modality are therefore gaining rapid adoption.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security breaches | –1.8% | North America & Europe | Short term (≤ 2 years) |

| Shortage of health-IT talent | –1.5% | Global | Long term (≥ 4 years) |

| Fragmented interoperability | –1.2% | North America & Europe | Medium term (2-4 years) |

| Freemium price pressure | –0.9% | North America & Europe; spreading to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Risk of Data Security Breaches & Cyber-Attacks

Health records remain the most valuable data category on the dark web, and breaches rose for a third consecutive year. Security fears deter 60% of non-migrated providers from moving scheduling to the cloud. HIPAA, GDPR, and emerging U.S. state privacy laws demand multi-layer encryption, role-based access, and audit trails. Breach remediation can cost USD 9.5 million per incident, diverting budgets away from new deployments. Vendors that maintain SOC 2 and HITRUST certifications are consequently gaining a competitive edge.

Shortage of Skilled Health-IT Professionals

Two-thirds of hospital CIOs cite open headcount for certified EHR and scheduling-system engineers, up from 59% in 2020. Sub-4% unemployment among IT specialists inflates wage bills, pushing smaller facilities toward managed-service contracts that inflate total ownership cost by up to 40%. Project timelines lengthen and customization depth suffers, delaying productivity gains expected from advanced scheduling modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Patient Access Drives Market Leadership

The patient-scheduling segment generated 58.25% revenue in 2025—the highest within the medical scheduling software market size—as hospitals prioritized frictionless consumer access. Platforms now embed AI suggestions to propose optimal physician-patient matches, boosting completed-visit ratios by 9%. Care-provider scheduling, the fastest-expanding niche at 12.64% CAGR, benefits from modules that map acuity scores against staffing skillsets to reduce understaffing penalties.

Integrators increasingly combine both modules so a vacant provider slot automatically surfaces to patients, uniting demand and capacity management. Advanced provider-scheduling suites supervise duty-hour compliance, fatigue indices, and licensure alerts, further tightening quality control. Vendors that bundle these capabilities are differentiating in request-for-proposal (RFP) cycles, especially among IDNs operating across multiple time zones.

By Deployment Model: Cloud Dominance Meets Hybrid Innovation

Public-cloud rollouts contributed 69.10% of 2025 revenue, reinforcing cloud as the default backbone of the medical scheduling software market. Multitenant architectures accelerate quarterly feature drops, keep version skew low, and provide API toolkits for omnichannel patient engagement. Nonetheless, hybrid models will climb at 12.70% CAGR as providers isolate sensitive clinician payroll data on-premise while steering consumer-facing workflows toward hyperscale data centers.

Edge-compute nodes inside hospital data rooms handle latency-sensitive image uploads or real-time surgery updates, while bulk analytics and AI training run in the cloud. This split mitigates bandwidth constraints and supports national-data-residency statutes now active in 65+ jurisdictions worldwide. Vendors able to orchestrate workload placement seamlessly are seeing longer contract tenures and higher net-promoter scores.

By End User: Hospital Leadership Faces Telehealth Disruption

Hospitals retained 49.10% share of 2025 spend due to multispecialty complexity, union scheduling rules, and back-office integration demands. Enterprise solutions integrate tightly with command centers that oversee bed capacity, operating-room turnover, and ancillary staff call-outs. Telehealth operators represent the 12.78% CAGR growth engine as care shifts outside physical walls. Their software wish list includes pre-visit device triage, secure link generation, and automatic fallback to voice when bandwidth dips.

Independent ambulatory clinics value speed: plug-and-play templates, self-registration kiosks, and instant credit-card vaulting compress check-in times by up to 40%. Retail health and home-care agencies comprise an “other” category focused on route optimization and mobile workforce dispatch, underscoring the expanding functional perimeter of scheduling platforms.

By Specialty: Primary Care Stability vs Mental Health Dynamism

Primary care visits supply 61.50% of 2025 scheduling transactions, sustaining steady seat-fill demand for annual exams, vaccinations, and chronic-disease reviews. Standardized 15- and 30-minute blocks simplify slot management and allow quick deployment of reminder bots connecting through SMS and patient portals. Behavioral and mental health leads specialty growth at 12.95% CAGR, driven by an uptick in therapy utilization and tele-psych options.

Mental-health workflows require longitudinal recurrence, session-length variability, and confidentiality rules that cap group-view visibility. Matching algorithms now gauge therapist availability, patient preferences, and insurance authorizations before confirming dates, reducing administrative phone loops. Specialty-neutral vendors are adding modular toolkits to address these nuanced requirements without rewrites.

Geography Analysis

North America commanded 42.10% of global revenue in 2025 on the strength of mature EHR penetration, payer reimbursement mandates favoring electronic workflows, and a consolidated hospital network eager to scale AI pilots into production. Epic Systems added 176 facilities to its Cadence install base, while Oracle Health lost ground, illustrating momentum shifts based on scheduling-module performance. Yet saturation among tier-one health systems is slowing incremental license expansion, opening space for cost-conscious regional hospitals to experiment with lighter SaaS entrants.

Europe posts stable single-digit growth underpinned by coordinated e-health regulations and investments targeting cross-border interoperability. Country-level privacy statutes necessitate configurable consent tracking and in-language patient-facing screens. National Health Service trusts in the United Kingdom recently mandated open-Booking APIs, elevating vendor scoring criteria focused on standards adherence. Eastern European clinics, retooling post-pandemic, increasingly adopt subscription models bundled with outcome-based contracting.

Asia-Pacific, forecast at 13.02% CAGR, remains the prime acceleration zone. Public-private funding blends in India and Indonesia subsidize cloud scheduling for mid-size hospitals lacking robust IT teams. China’s smart-hospital plan Phase III earmarks budget for AI triage and real-time scheduling dashboards in provincial centers. Local data-residency laws drive partnerships with domestic cloud providers, requiring multinational vendors to refactor code for onshore hosting.

The Middle East shows emergent momentum as Gulf Cooperation Council hospitals surpass 75% EHR adoption, paving the way for enterprise scheduling tie-ins. Africa and South America remain nascent but feature innovation sandboxes—mobile-first booking apps bundled with appointment-linked ride services—that could leapfrog legacy desktop systems once connectivity improves.

Competitive Landscape

The medical scheduling software market remains moderately fragmented yet is tilting toward consolidation. Hearst acquired QGenda and Francisco Partners paid USD 1.125 billion for AdvancedMD, reflecting private-equity conviction that scheduling engines are mission-critical digital infrastructure. Integrated EHR vendors—Epic, Oracle, MEDITECH—retain an installation moat inside large U.S. health systems, leveraging unified data models to cross-sell capacity-planning modules.

Standalone specialists answer with deep workflow flexibility and verticalized AI. QGenda automates anesthesiology call schedules factoring fatigue and credentialing, while UK-based Patchwork Health targets gig-style clinician shifts within National Health Service trusts. Freemium disruptors such as Calendly captured mainstream mindshare, compelling enterprise vendors to articulate premium value tied to HIPAA compliance and claims integration.

AI differentiation is intensifying: algorithms that forecast no-shows, re-sequence provider templates in real time, and pull insurance eligibility straight from clearinghouses are now table stakes. Vendors unable to supply RESTful APIs that surface availability to consumer-facing apps risk exclusion from health-system digital-front-door strategies. Compliance posture is equally decisive; platforms audited for SOC 2 Type II and HITRUST win procurement points as HTI-2 drives mandatory USCDI v4 adoption by 2026. Vendors that balance relentless feature velocity with airtight security thus emerge as front-runners.

Medical Scheduling Software Industry Leaders

-

American Medical Software

-

Kyruus

-

Caspio

-

AdvancedMD, Inc.

-

Q-nomy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Net Health completed the acquisition of Limber Health, extending its rehabilitation and therapy scheduling portfolio.

- April 2025: Promptly acquired MDprospects and Patient Spectrum Suite to broaden patient-engagement and omni-channel booking assets.

- October 2024: Francisco Partners agreed to purchase AdvancedMD for USD 1.125 billion, aiming to accelerate R&D in integrated scheduling and practice-management.

- July 2024: Commure and Athelas announced plans to acquire Augmedix, projecting AI assistance across 3 million annual physician appointments.

Global Medical Scheduling Software Market Report Scope

As per the scope of the report, the medical scheduling software aids the medical practitioners in managing and automating patient scheduling and care provider practices. The market is segmented by segmented Product Type (Patient Scheduling, Care Provider Scheduling, and Others), Deployment Type (Cloud-based and Installed), End User (Hospitals, Clinics, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report offers the value (USD million) for the above segments.

| Patient Scheduling |

| Care Provider Scheduling |

| Others |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Hospitals |

| Clinics |

| Ambulatory Surgical Centers |

| Telehealth Providers |

| Others |

| Primary Care |

| Dentistry |

| Behavioral and Mental Health |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Patient Scheduling | |

| Care Provider Scheduling | ||

| Others | ||

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User | Hospitals | |

| Clinics | ||

| Ambulatory Surgical Centers | ||

| Telehealth Providers | ||

| Others | ||

| By Specialty | Primary Care | |

| Dentistry | ||

| Behavioral and Mental Health | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medical scheduling software market?

The market is valued at USD 496.19 million in 2026 and is projected to reach USD 871.65 million by 2031.

How fast is the medical scheduling software market expected to grow?

It is forecast to expand at a 11.92% CAGR between 2026 and 2031.

Which deployment model is most popular for medical scheduling platforms?

Cloud-based solutions account for 69.10% of current implementations, with hybrid models gaining ground.

Why are hospitals investing heavily in scheduling software?

Hospitals seek to cut overtime, reduce no-shows, and streamline multi-specialty workflows while integrating with existing EHRs.

How does telehealth influence scheduling software demand?

The rise of virtual visits drives demand for systems that can handle device checks, secure links, and after-hours booking.

What is the top security concern limiting new deployments?

Fear of data breaches and compliance obligations remains the primary barrier, especially among providers yet to migrate to the cloud.

Page last updated on: