AI In Healthcare Workflow Optimization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 33.40 Billion |

| Market Size (2031) | USD 82.90 Billion |

| Growth Rate (2026 - 2031) | 29.95% CAGR |

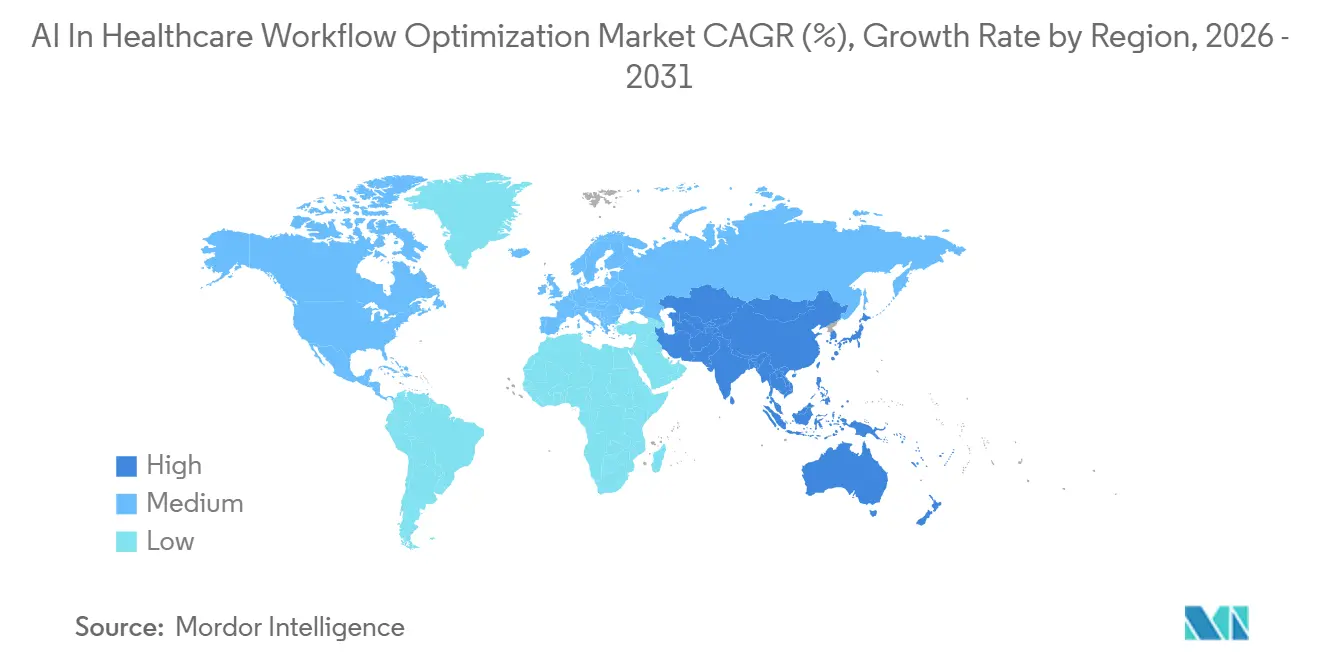

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

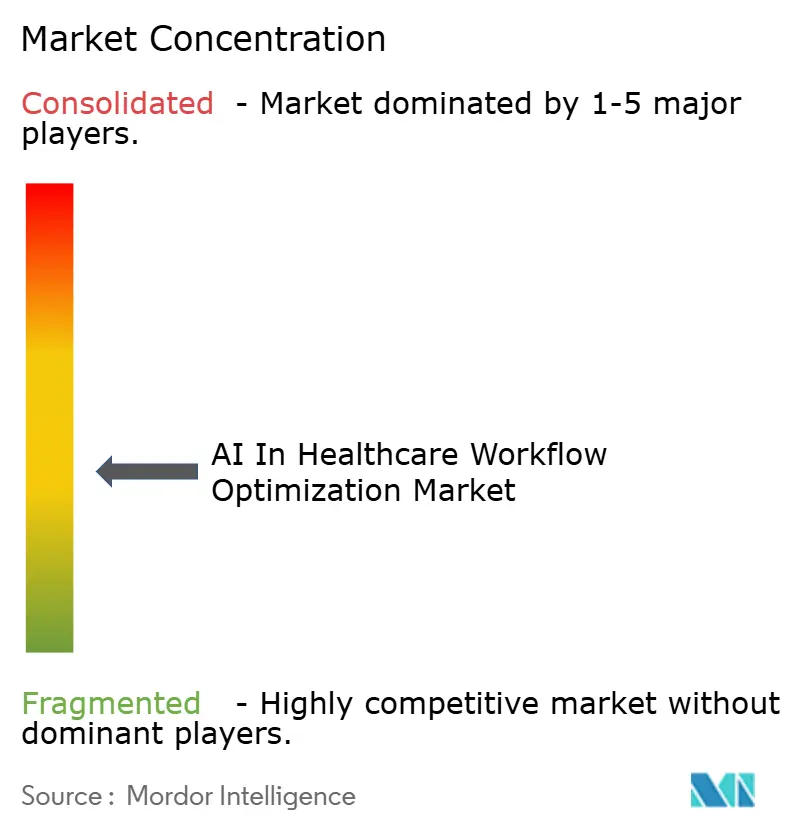

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Healthcare Workflow Optimization Market Analysis by Mordor Intelligence

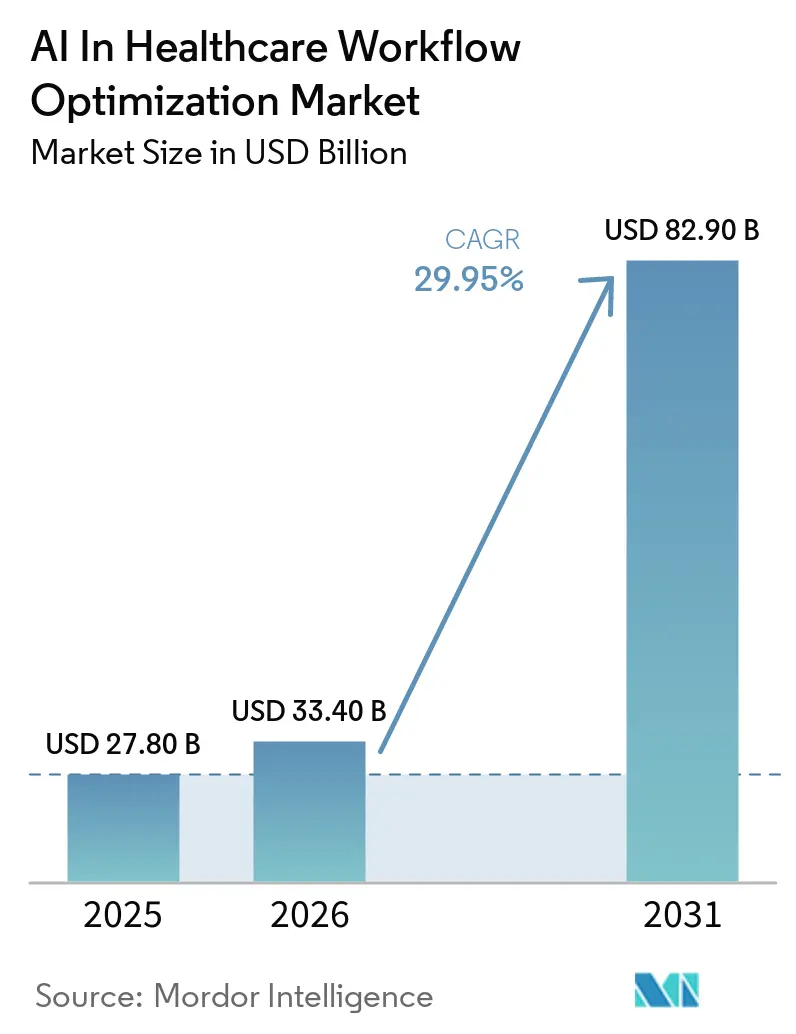

The AI In Healthcare Workflow Optimization Market size is projected to expand from USD 27.80 billion in 2025 and USD 33.40 billion in 2026 to USD 82.90 billion by 2031, registering a CAGR of 29.95% between 2026 to 2031.

The AI-driven healthcare workflow optimization market is experiencing significant growth, driven by a shift toward integrated automation. This transformation reduces documentation time, accelerates approvals, and enhances capacity utilization across inpatient and outpatient settings. Regulatory deadlines for payer-facing prior-authorization APIs, combined with API-focused platforms from EHR vendors, are minimizing integration challenges and enabling faster deployment of tools for ambient scribing, triage, and orchestration. Health systems are prioritizing solutions that improve clinician efficiency and increase throughput without requiring capital expansion, fueling strong momentum in documentation automation and perioperative optimization. Additionally, hospitals are adopting both cloud-native and hybrid models to balance the flexibility of SaaS with the limitations of legacy imaging and revenue-cycle systems that cannot transition immediately.

Key Report Takeaways

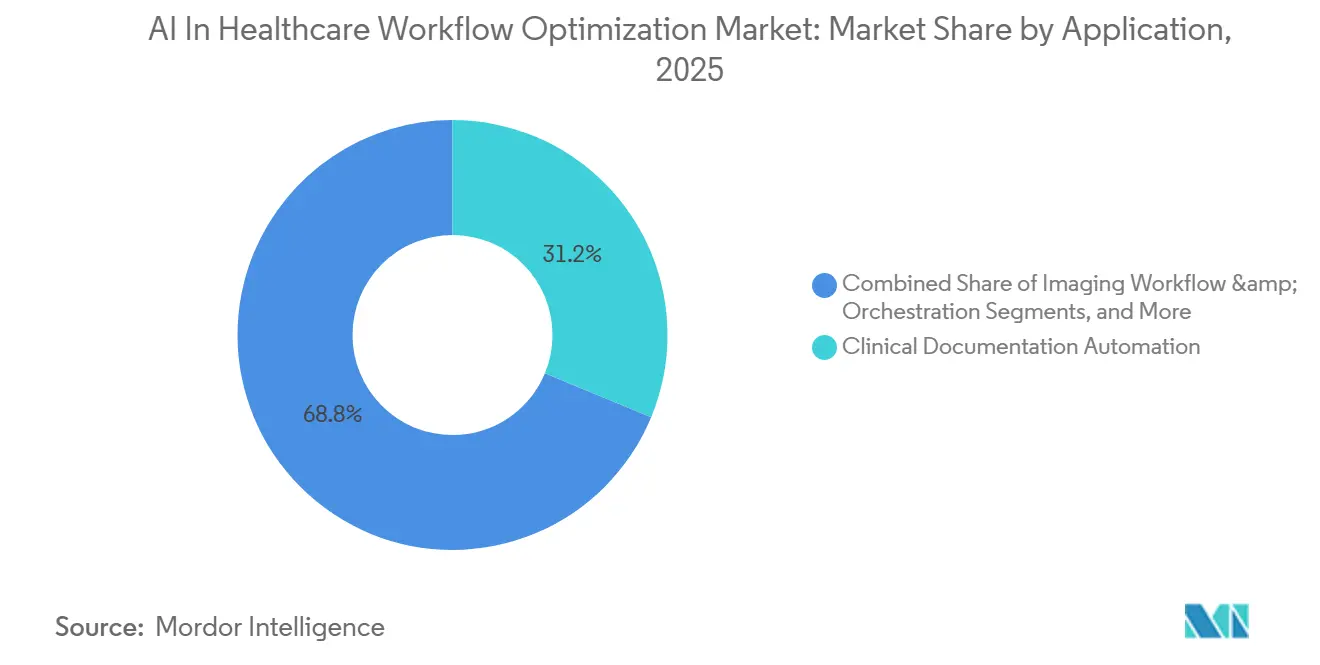

- By application, clinical documentation automation led with 31.24% revenue share in 2025, while inpatient capacity and patient flow tools are projected to grow at a 23.17% CAGR through 2031.

- By end user, hospitals and health systems held 47.68% of 2025 spending, while ambulatory and outpatient clinics are projected to grow at a 22.43% CAGR through 2031.

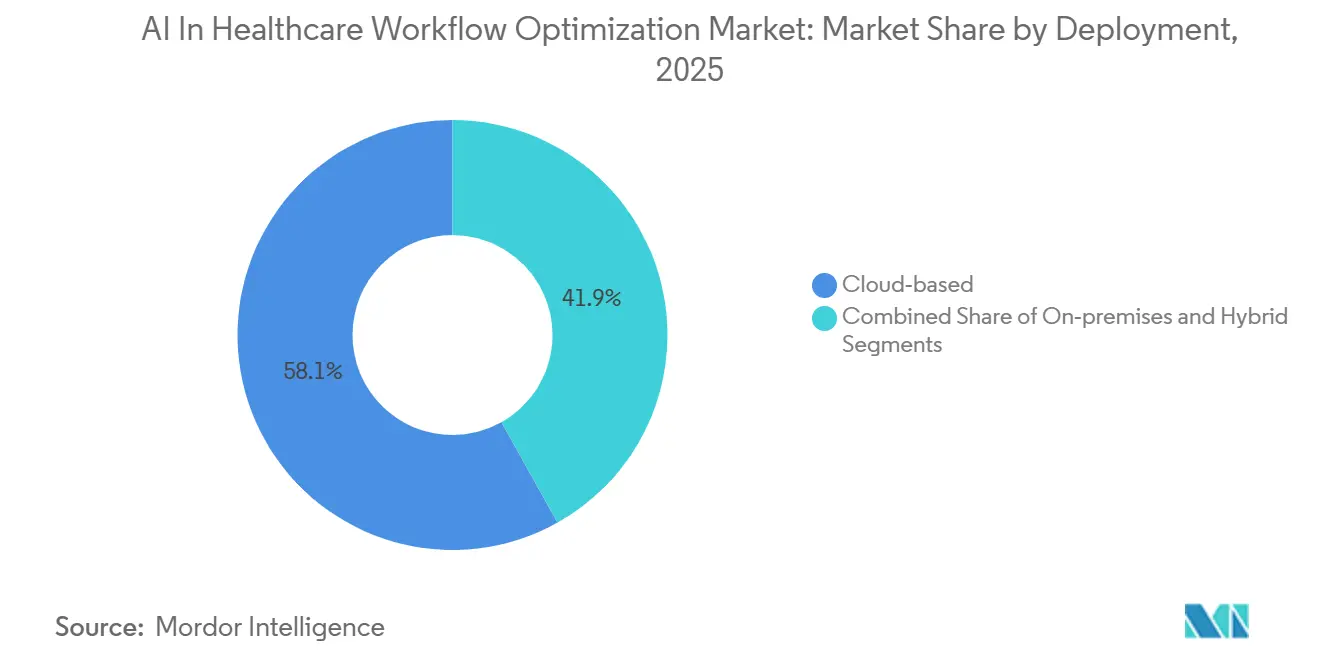

- By deployment, cloud-based models commanded 58.13% of 2025 revenue, and hybrid architectures are projected to grow at a 24.11% CAGR through 2031.

- By technology, natural language processing and large language models accounted for 36.18% of 2025 revenue, while optimization and simulation engines are projected to expand at a 25.16% CAGR through 2031.

- By geography, North America represented 42.16% of 2025 revenue, while Asia-Pacific is projected to grow at a 24.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Healthcare Workflow Optimization Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Clinician documentation burden reduction via ambient AI and NLP | 4.8% | North America & Europe, expanding to urban APAC | Short term (≤ 2 years) |

| Throughput, capacity, and perioperative optimization priorities | 5.2% | Global, concentrated in North America & Western Europe | Medium term (2-4 years) |

| Imaging workflow orchestration and acute care coordination | 3.9% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Cloud–EHR integration enabling embedded AI in workflows | 4.6% | Global, led by North America & cloud-mature APAC markets | Long term (≥ 4 years) |

| CMS prior authorization APIs and interoperability deadlines (2026–2027) | 5.5% | Global, concentrated in North America & Western Europe | Medium term (2-4 years) |

| ONC HTI-1 DSI transparency driving AI governance inside certified EHRs | 3.7% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ambient AI and NLP Alleviate Clinician Documentation Burden

Ambient AI scribes, designed to capture clinician-patient interactions and generate structured notes, have reduced documentation time by 33% to 40% in large-scale, multi-site trials. This advancement has allowed clinicians to reclaim 2 to 3 hours per shift while significantly reducing after-hours charting. By mid-2025, 62.6% of U.S. hospitals connected to Epic had implemented these ambient documentation tools, reflecting their rapid adoption in mainstream healthcare.[1]Centers for Medicare & Medicaid Services, “Prior Authorization API Requirements,” CMS, cms.gov Vendor participation in these deployments, including Microsoft DAX Copilot, Abridge, and Ambience Healthcare, highlights a competitive market driving faster innovation cycles. The January 2027 CMS deadline for the Prior Authorization API further emphasizes the importance of ambient notes, as structured summaries can streamline requests, reduce manual data entry, and expedite approval processes. Additionally, ONC’s HTI-1 rule mandated transparency through provenance and confidence indicators for AI-generated content in decision support, enhancing trust while increasing development requirements for vendors and IT teams.

Hospitals Optimize Throughput and Capacity Amid Rising Demand

Hospitals are leveraging AI to address rising inpatient demand without expanding physical capacity, achieving significant improvements in operating room and bed utilization. These gains range from high single to low double digits. Case studies demonstrate success, such as an 8-percentage-point increase in operating room utilization at Gundersen Health System and a 46% fill rate for last-minute openings at Inova Health System, converting idle blocks into revenue-generating cases. At Allina Health, automated sequencing and block-release tools delivered an 11-times return on investment within 18 months, aligning with CFO expectations for an 18 to 24-month payback period. These platforms are evolving into semi-autonomous systems capable of reallocating staff and expediting pre-operative tasks under governance protocols, transitioning from analytics tools to essential operational infrastructure. Large community and academic medical centers are scaling these solutions to boost daily case volumes, protect financial margins, and reduce overtime expenses.

AI Enhances Imaging Workflow and Acute Care Coordination

AI-powered imaging triage is transforming care delivery by accelerating treatment timelines for critical conditions such as strokes and pulmonary embolisms. By prioritizing urgent findings and notifying care teams promptly, these tools significantly reduce time-to-treatment. A multimodal platform, deployed in 2,000 U.S. hospitals by 2025, achieved a 73% reduction in CTA-to-team notification time for suspected large-vessel occlusions, expediting thrombectomy decisions.[2] Foundation models integrated into PACS systems can detect multiple pathologies in a single inference, with sensitivity and specificity rates of 97% and 98%, respectively, in large health system implementations.

Cloud-EHR Integration Paves the Way for AI-Enhanced Workflows

Cloud-native EHR systems, equipped with FHIR and modern REST APIs, are replacing outdated custom interfaces and middleware, which previously extended deployment timelines by 6 to 12 months and incurred substantial integration costs. Oracle Health’s Clinical AI Agent, certified by ONC in late 2025, has demonstrated its ability to reduce clinician workloads and documentation hours when integrated into daily workflows. Epic's marketplace strategy, featuring prebuilt connectors, facilitates the rapid deployment of ambient scribing, clinical risk alerts, and revenue-cycle automation while minimizing IT overhead. The CMS requirement for real-time data exchange between payers and providers strengthens the business case for embedded AI, which can compile requests and monitor approvals without manual portal interactions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| EHR integration complexity and platform gatekeeping risks | -1.8% | North America & Europe with high Epic/Oracle penetration | Medium term (2-4 years) |

| Capital constraints and cautious procurement cycles at providers | -1.3% | Global, acute in mid-tier U.S. health systems & emerging APAC | Short term (≤ 2 years) |

| FDA PCCP and lifecycle governance increasing compliance workload | -1.7% | North America & Europe with high Epic/Oracle penetration | Medium term (2-4 years) |

| Change management and clinician adoption hurdles | -1.4% | Global, acute in mid-tier U.S. health systems & emerging APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EHR Platform Owners Leverage Features, Tightening Market Dynamics

EHR platform owners are strategically integrating features like ambient documentation and clinical decision support into their core systems. This approach enhances their offerings while exerting pressure on third-party pricing and distribution routes. By 2025, Epic embedded native ambient scribes into its platform, effectively narrowing the market for independent documentation vendors and shifting the competitive landscape towards multi-EHR interoperability.[3] Office of the National Coordinator for Health Information Technology, “HTI-1: Decision Support Intervention Transparency,” ONC, healthit.gov Oracle Health's integration of the former Cerner stack into its AI roadmap has increased the need for clear data-access agreements, particularly for imaging and capacity tools reliant on EHR integration.

Providers Tighten Budgets Amidst Shrinking Margins in 2024

In 2024, many providers faced tightened operating margins, leading to stricter procurement standards with an emphasis on an 18 to 24-month payback period. Budgets increasingly focused on tools that deliver measurable throughput or labor savings. Mid-tier systems deferred larger IT investments, prioritizing essential upgrades and cybersecurity measures over discretionary pilots that lacked a clear return on investment. Buyers demanded multi-site pilots and independent outcome validations, which extended procurement cycles but improved confidence in scaling decisions. The most compelling cases, particularly those tied to additional daily operating room cases or reduced patient stay durations, secured support from clinical and finance leaders due to their direct impact on contribution margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Documentation Automation Leads Revenue, Capacity Tools Surge

Clinical documentation automation accounted for 31.24% of the 2025 revenue in the AI-driven healthcare workflow optimization market. This growth is primarily driven by the widespread adoption of ambient scribes, which have demonstrated the ability to reduce documentation time by 33% to 40% in large-scale implementations. These advanced tools automatically generate structured notes within Electronic Health Records (EHR), significantly reducing after-hours charting. This not only enhances work-life balance but also allows more time for direct patient care. Health systems that adopted documentation automation early have reported faster scaling, particularly when EHR vendors bundle native functionality. Such bundling eliminates additional licensing costs and streamlines procurement processes. Inpatient capacity and patient flow tools, while generating smaller absolute revenues, are experiencing strong annual growth of 23.17% through 2031. Hospitals are increasingly focusing on improving utilization rates, reducing patient stays, and minimizing canceled cases.

By End User: Hospitals Lead Spending, Ambulatory Clinics on the Rise

Hospitals and health systems accounted for 47.68% of spending in 2025. This level of expenditure aligns with acute labor shortages, high contribution margins from surgical lines, and governance mandates embedded within EHRs under ONC’s HTI-1 rule. These institutions are standardizing on ambient scribing, perioperative optimization, and imaging triage. Such measures not only enhance throughput but also recover clinician time, safeguarding revenue and reducing burnout. Vendor partnerships and marketplaces within leading EHRs are further accelerating these deployments by simplifying connections, which significantly reduce time-to-value. Imaging centers and service lines that adopt unified triage platforms differentiate themselves by delivering faster care, which helps reduce overtime and improve efficiency in reading rooms. Ambulatory and outpatient clinics are projected to grow at an annual rate of 22.43% through 2031. This growth is driven by the shift of risk to smaller practices under value-based contracts, which increasingly reward automation in scheduling and prior authorizations.

By Deployment: Cloud Dominates with API Agility, Hybrid Rises for Legacy Integration

Cloud-based models captured 58.13% of the 2025 revenue in the AI-driven healthcare workflow optimization market. This dominance is attributed to API-first EHRs and payer API mandates that incentivize real-time data exchanges. For instance, prebuilt connectors and embedded agents offered by leading platforms have significantly reduced deployment timelines by eliminating the need for custom integration work. These efficiencies enable quicker onboarding of tools like documentation automation, capacity forecasting, and revenue-cycle management, reducing timelines from months to weeks. Hybrid architectures are expanding at a CAGR of 24.11% through 2031. This growth is primarily due to the challenges associated with migrating imaging archives, revenue-cycle platforms, and clinical data stores simultaneously.

By Technology: NLP Leads, Optimization Engines Rise Amid Throughput Demands

Natural language processing (NLP) and large language models constituted 36.18% of the 2025 revenue in the AI-driven healthcare workflow optimization market. This strong performance is supported by successful ambient scribing trials involving thousands of physicians. These NLP tools streamline documentation time and alleviate after-hours workloads. Additionally, chatbot interfaces play a critical role in triage and summarizing care plans, expediting the flow of information. Optimization and simulation engines are expected to grow at a CAGR of 25.16% through 2031. This growth is driven by advancements in reinforcement learning, which enhance operating room scheduling, bed assignments, and staff allocations.

Geography Analysis

In 2025, North America accounted for 42.16% of the revenue share in the AI-driven healthcare workflow optimization market. This growth was driven by extensive EHR adoption, the scaling of ambient scribing, and the upcoming 2027 deadline for prior-authorization APIs. By mid-2025, 62.6% of U.S. hospital clients using a leading EHR provider had implemented ambient documentation tools, indicating widespread adoption in major health systems. The implementation of decision support intervention mandates in August 2026 is accelerating investments in provenance, confidence labeling, and AI content exportability. These developments are expediting the deployment of ambient documentation, perioperative optimization, and triage orchestration within the AI healthcare workflow optimization market as governance structures continue to evolve.

Asia-Pacific is projected to grow at a strong CAGR of 24.78% through 2031, supported by regional AI triage mandates in parts of China and the expansion of interoperable health records in India. Health authorities in China are promoting the adoption of AI triage in hospitals outside tier-1 cities, driving increased use of imaging orchestration and acute care coordination. In India, the Ayushman Bharat Digital Mission is scaling patient-linked health records across a wide network of facilities, enhancing the utility of AI in documentation and scheduling. Additionally, corporate hospital groups in India are deploying radiology AI to address specialist shortages, strengthening the triage value proposition in high-volume centers. In Japan, while regulators have approved AI-enabled tools for endoscopy and ophthalmology through expedited pathways, adoption remains concentrated in academic institutions due to reimbursement challenges and IT infrastructure limitations.

Competitive Landscape

The AI in healthcare workflow optimization market remains moderately fragmented due to its diverse use cases, spanning documentation, imaging, capacity, perioperative, revenue cycle, and more. Each domain demands distinct data, workflows, and integrations. Ambient documentation providers have expanded their deployments as EHR vendors integrate native scribes, placing greater emphasis on accuracy, specialty coverage, and alignment with governance standards. Imaging workflow leaders have incorporated foundational models within PACS, aiming to unify detection across various pathologies while delivering high performance and broad coverage. Vendors focusing on perioperative optimization have shifted from traditional dashboards to workflow-executing teammates capable of real-time tasks, such as releasing blocks and resequencing cases.

EHR platform strategies are shaping the competitive landscape. Marketplaces and embedded agents are simplifying integration efforts, accelerating clinical adoption. Oracle Health’s Clinical AI Agent, certified by ONC in 2025, has demonstrated significant reductions in documentation hours and overall workload. By 2025, Epic’s App Orchard featured hundreds of AI-enabled applications, ready for rapid deployment through prebuilt connectors. These strategic advancements are driving buyer preference for solutions that seamlessly integrate with existing EHR workflows while meeting HTI-1 transparency standards.

AI In Healthcare Workflow Optimization Industry Leaders

Epic Systems

GE HealthCare

Oracle Health

Siemens Healthineers AG

Microsoft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Medisolv, Inc., a national leader in healthcare quality data management, announced the acquisition of Health Elements AI, whose technology helps capture and structure clinical data from medical records for quality reporting and clinical registries.

- April 2026: Ambience Healthcare unveiled a multiyear platform roadmap designed to fundamentally reshape how health systems deliver, coordinate, and improve care using AI.

- October 2025: Viz.ai expanded its multimodal Viz Assist platform to 2,000 U.S. hospitals, integrating stroke, pulmonary embolism, and aortic dissection triage into a unified inference engine that reduced CTA-to-team notification time by 73%.

- September 2025: LeanTaaS reported that Inova Health System filled 46% of last-minute released operating-room time slots using predictive algorithms that forecast case durations and text surgeons when upstream delays create openings.

Global AI In Healthcare Workflow Optimization Market Report Scope

As per the scope of the report, AI in healthcare workflow optimization refers to the application of artificial intelligence (AI), machine learning, and natural language processing (NLP) to automate, streamline, and enhance clinical and administrative processes. It involves analyzing data to reduce manual effort, eliminate bottlenecks, and improve efficiency, such as automating scheduling, documenting patient visits, or prioritizing radiology worklists.

The AI in healthcare workflow optimization market is segmented by application, end-user, deployment, technology/AI modality, and geography. By application, the market includes clinical documentation automation, imaging workflow & orchestration, inpatient capacity & patient flow, operating room scheduling & perioperative optimization, revenue cycle & prior authorization automation, and others. By end-user, the market is segmented into hospitals & health systems, ambulatory & outpatient clinics, imaging centers, ambulatory surgery centers, payers, and others. By deployment, the market is categorized into cloud-based, on-premises, and hybrid. By technology/AI modality, the market is segmented into NLP/LLMs, computer vision, optimization & simulation, predictive analytics, and RPA/intelligent process automation. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Clinical Documentation Automation |

| Imaging Workflow & Orchestration |

| Inpatient Capacity & Patient Flow |

| Operating Room Scheduling & Perioperative Optimization |

| Revenue Cycle & Prior Authorization Automation |

| Others |

| Hospitals & Health Systems |

| Ambulatory & Outpatient Clinics |

| Imaging Centers |

| Ambulatory Surgery Centers |

| Payers |

| Others |

| Cloud-based |

| On-premises |

| Hybrid |

| NLP / LLMs |

| Computer Vision |

| Optimization & Simulation |

| Predictive Analytics |

| RPA / Intelligent Process Automation |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Clinical Documentation Automation | |

| Imaging Workflow & Orchestration | ||

| Inpatient Capacity & Patient Flow | ||

| Operating Room Scheduling & Perioperative Optimization | ||

| Revenue Cycle & Prior Authorization Automation | ||

| Others | ||

| By End User | Hospitals & Health Systems | |

| Ambulatory & Outpatient Clinics | ||

| Imaging Centers | ||

| Ambulatory Surgery Centers | ||

| Payers | ||

| Others | ||

| By Deployment | Cloud-based | |

| On-premises | ||

| Hybrid | ||

| By Technology / AI Modality | NLP / LLMs | |

| Computer Vision | ||

| Optimization & Simulation | ||

| Predictive Analytics | ||

| RPA / Intelligent Process Automation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the AI in healthcare workflow optimization market by 2031?

The AI in healthcare workflow optimization market is projected to reach USD 82.9 billion by 2031, growing at a 19.95% CAGR from USD 33.4 billion in 2026.

Which applications are scaling fastest within AI in healthcare workflow optimization?

Inpatient capacity and patient flow tools are the fastest growing, advancing at a 23.17% CAGR through 2031 as hospitals focus on higher utilization and shorter wait times.

Who spends the most on AI in healthcare workflow optimization and which buyer group is growing faster?

Hospitals and health systems accounted for 47.68% of 2025 spending, while ambulatory and outpatient clinics are growing faster at a 22.43% CAGR through 2031.

What deployment model is most common for AI in healthcare workflow optimization?

Cloud-based deployments held 58.13% of 2025 revenue, while hybrid models are growing rapidly at a 24.11% CAGR due to legacy imaging and revenue-cycle anchors.

Which technologies lead adoption in AI in healthcare workflow optimization?

Natural language processing and large language models led with 36.18% of 2025 revenue, while optimization and simulation engines are expanding at a 25.16% CAGR as providers seek throughput gains.

Which region leads and which region is growing fastest in AI in healthcare workflow optimization?

North America led with 42.16% of 2025 revenue, while Asia-Pacific is growing fastest at a 24.78% CAGR through 2031 due to policy support and digital health infrastructure scale-up.

Page last updated on: