AI In Clinical Trial Patient Recruitment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.67 Billion |

| Market Size (2031) | USD 2.10 Billion |

| Growth Rate (2026 - 2031) | 25.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

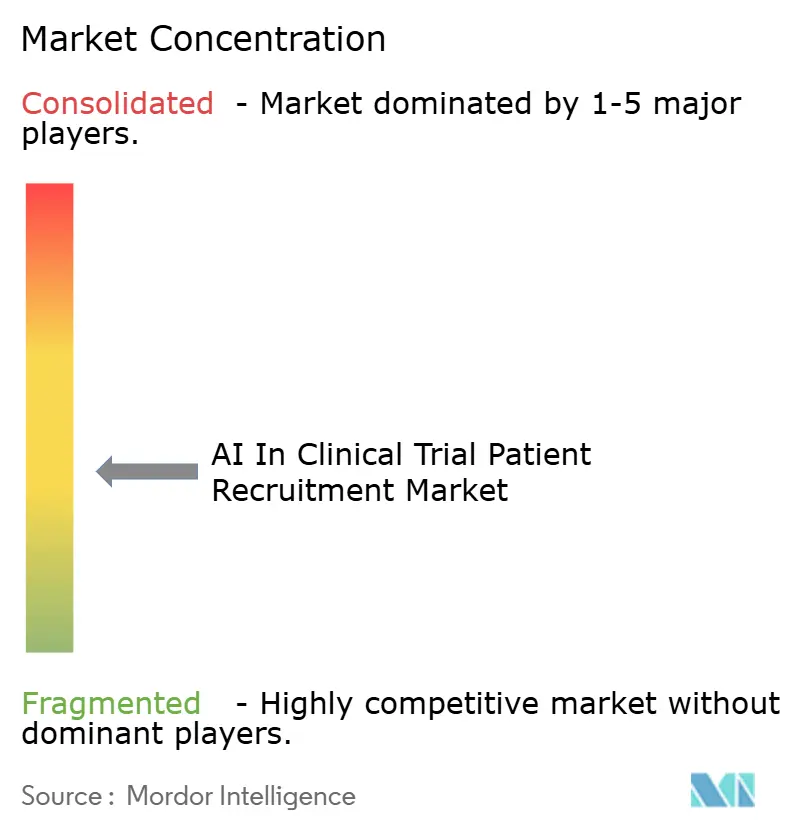

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Clinical Trial Patient Recruitment Market Analysis by Mordor Intelligence

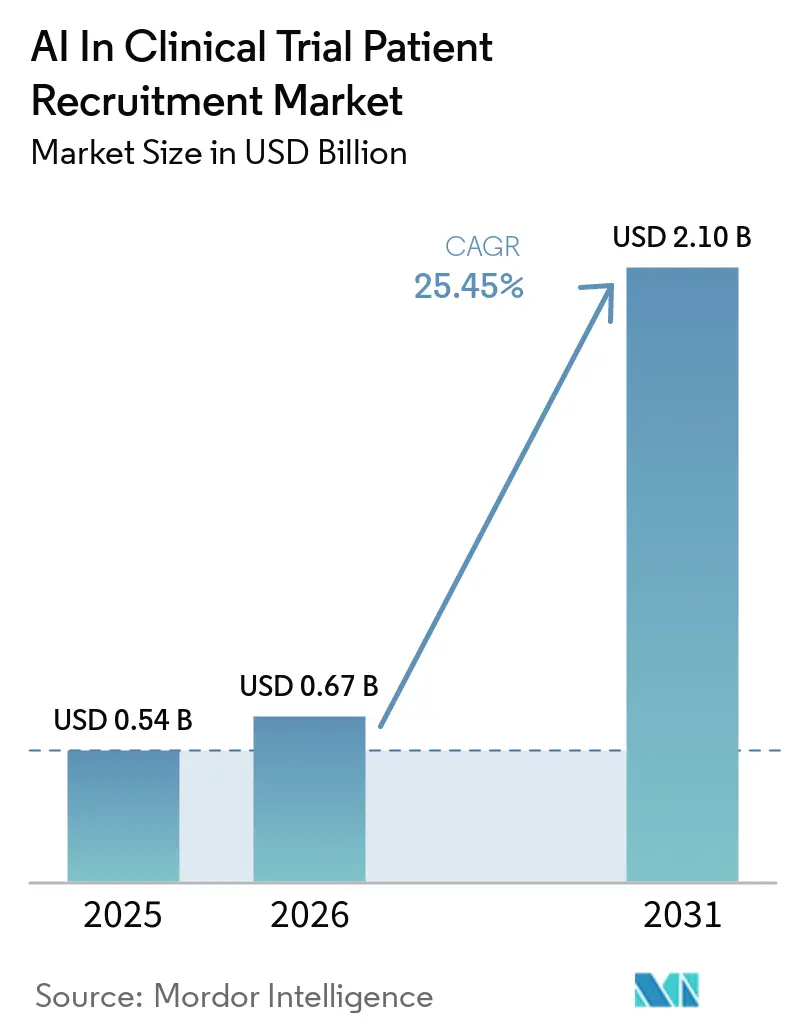

The AI In Clinical Trial Patient Recruitment Market size is expected to grow from USD 0.54 billion in 2025 to USD 0.67 billion in 2026 and is forecast to reach USD 2.10 billion by 2031 at 25.45% CAGR over 2026-2031.

As the pandemic revealed site-centric enrollment challenges, demand increased significantly, particularly as regulators began recognizing real-world evidence as a valuable complement to traditional case report forms. Large language models (LLMs) now process unstructured electronic health record (EHR) notes in under 30 seconds per patient. This advancement has streamlined site-activation cycles, reducing them to below the 15-day threshold set by sponsors. Additionally, machine-learning feasibility engines now predict site-patient density in advance, cutting USD 180,000 in overhead costs per site during a typical 24-month study. While oncology remains the primary area of spending, rare-disease sponsors are achieving the fastest growth by leveraging federated genomic matching algorithms. Cloud deployments are leading the market due to their ability to avoid significant capital expenditures. However, hybrid architectures are rapidly gaining momentum to comply with data-sovereignty regulations in regions such as the EU, China, and Japan.

Key Report Takeaways

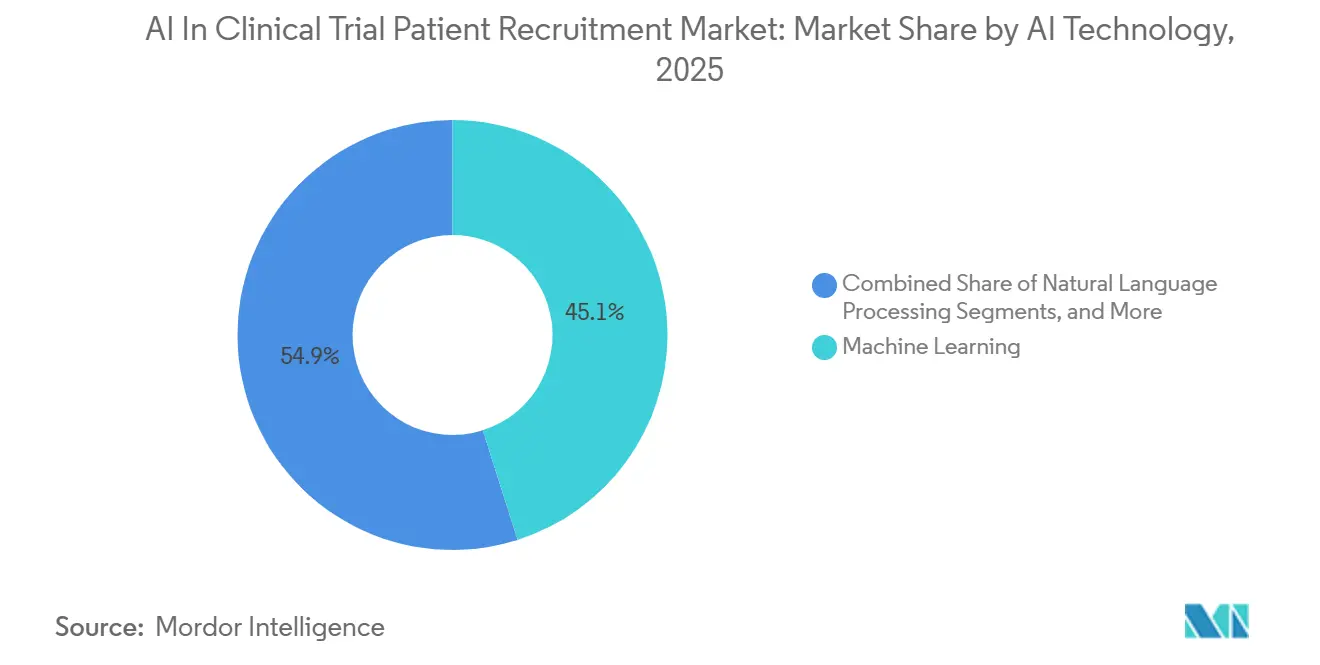

- By AI technology, machine learning captured 45.10% of the AI in clinical trial patient recruitment market share in 2025, while natural-language processing is forecasted to expand at a 26.25% CAGR through 2031.

- By deployment model, cloud infrastructure held 61.00% share of the AI in clinical trial patient recruitment market size in 2025, whereas hybrid architectures are projected to grow at a 26.86% CAGR through 2031.

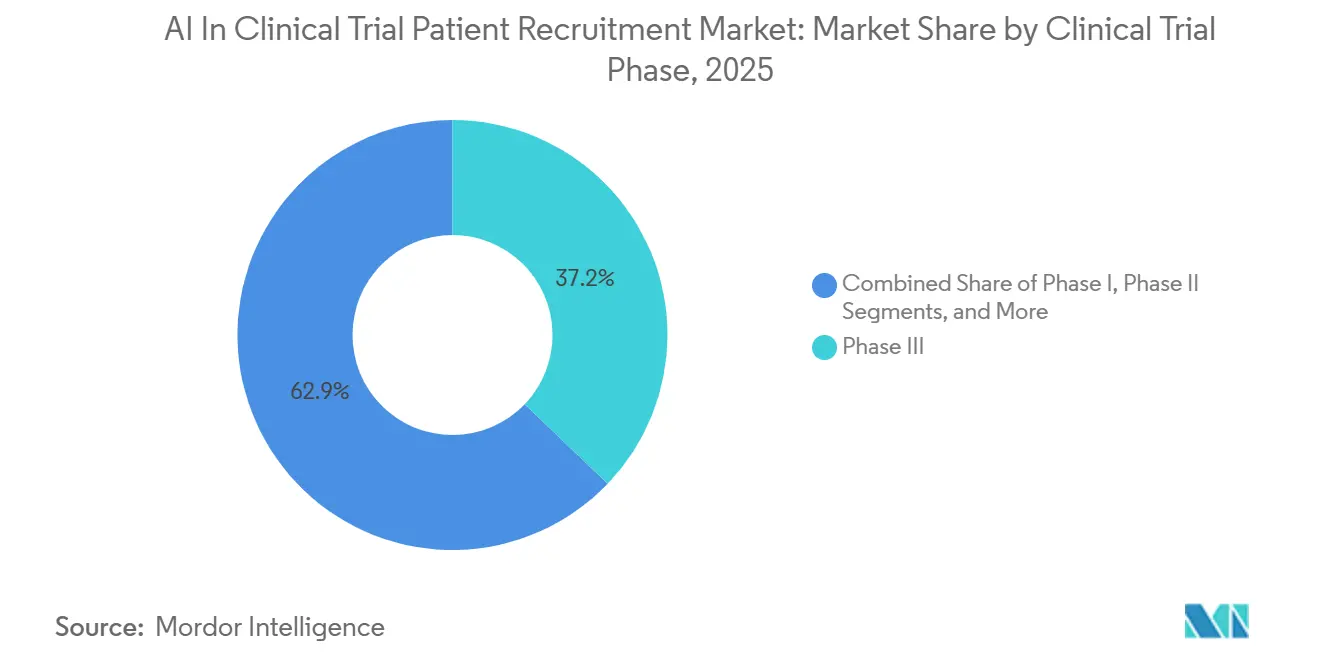

- By clinical-trial phase, Phase III enrollment accounted for 37.15% of the AI in clinical trial patient recruitment market size in 2025, and Phase I is expected to grow at a 27.45% CAGR through 2031.

- By therapeutic area, oncology led with 28.25% revenue share in 2025, and rare diseases are forecasted to rise at a 27.87% CAGR to 2031.

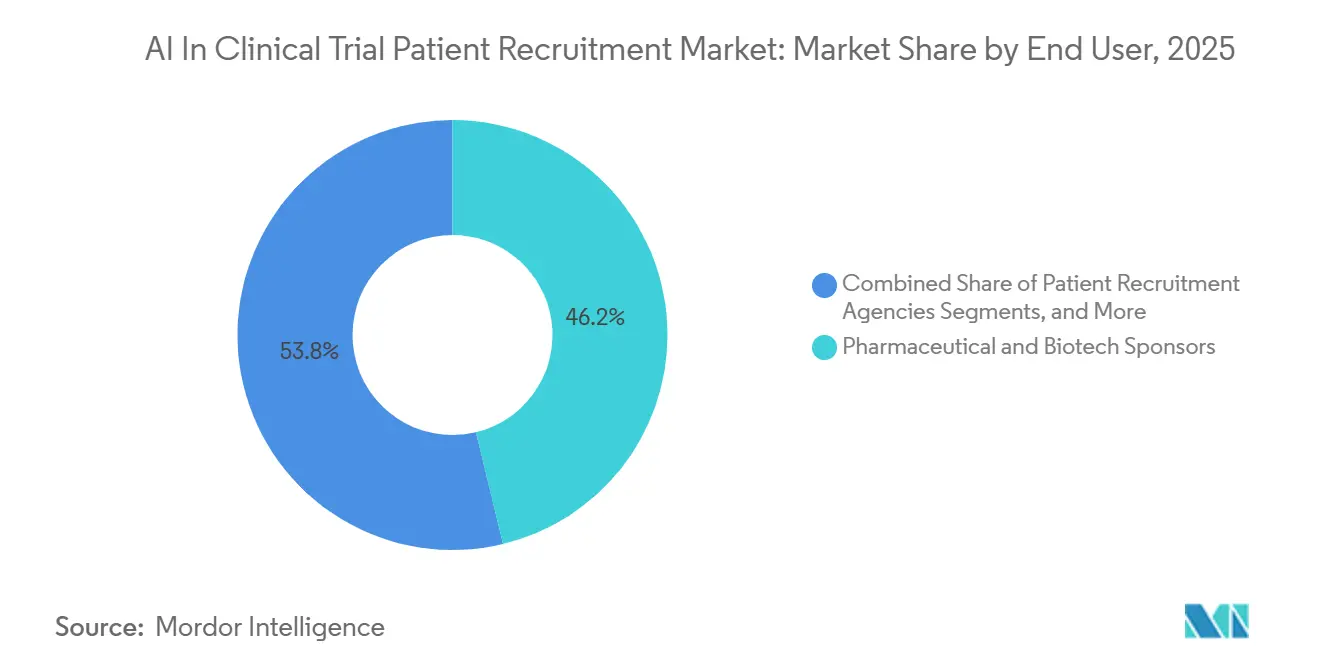

- By end user, pharmaceutical sponsors commanded 46.22% share of the AI in clinical trial patient recruitment market size in 2025, while patient-recruitment agencies record the highest projected CAGR at 26.96% through 2031.

- By data source, EHRs represented 52% share in 2025; wearables and digital biomarkers are expected to expand at a 27.00% CAGR through 2031.

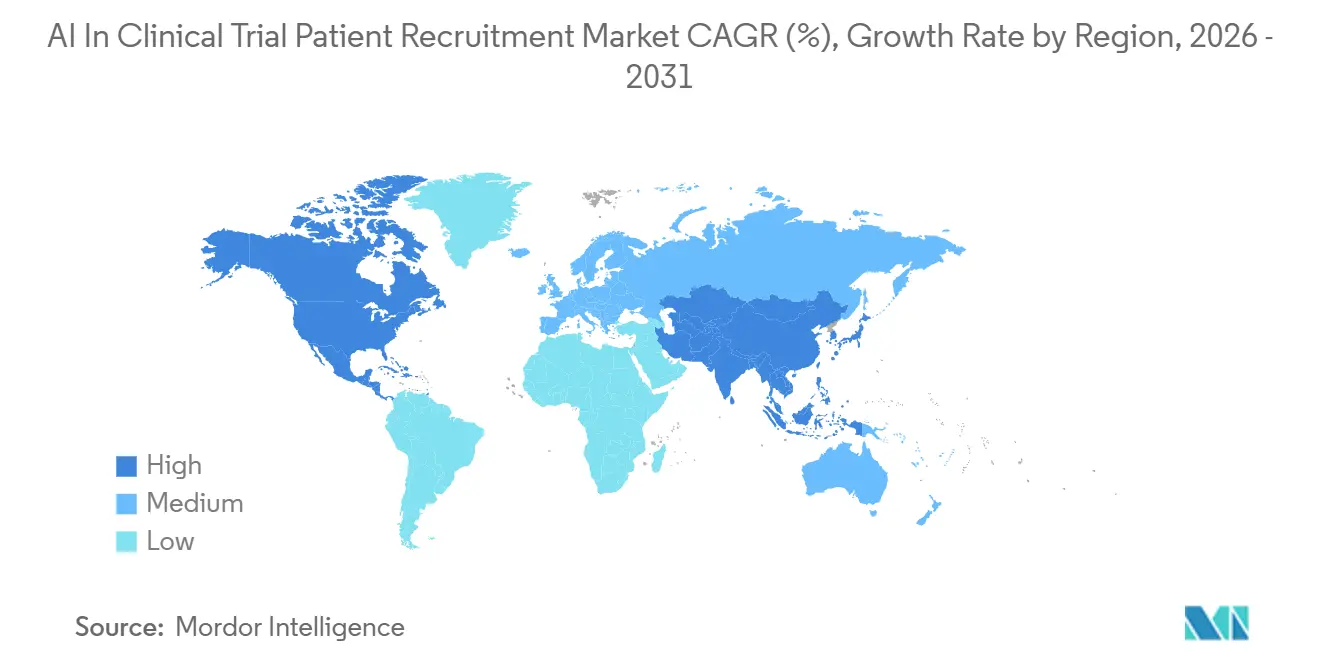

- By geography, North America held 49.45% of AI in the clinical trial patient recruitment market share in 2025, and Asia-Pacific is advancing at a 25.96% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Clinical Trial Patient Recruitment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing complexity and cost of patient enrollment | +7.2% | North America, EU | Medium term (2-4 years) |

| Pandemic-led rise of decentralized and hybrid trials | +6.8% | Global core, APAC & Latin America spillover | Short term (≤ 2 years) |

| Regulatory push for real-world data and AI validation pathways | +5.9% | North America, EU | Long term (≥ 4 years) |

| Growing EHR interoperability enabling scalable prescreening | +5.6% | North America, EU, advanced APAC | Medium term (2-4 years) |

| Multimodal Genomic-Phenotypic Matching Boosting Accuracy | +6.8% | Global core, APAC & Latin America spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Complexity and Cost of Patient Enrollment Propel AI Adoption

Manual chart reviews require an average of 44.7 hours per protocol, whereas AI systems can perform the same task in just 2.5 hours with a high accuracy rate of 96%. Enrollment delays remain a significant challenge, with 80% of trials failing to meet their timelines and 50% of sites unable to enroll any patients, underscoring the demand for clinical trial patient recruitment services. To address these inefficiencies, sponsors are increasingly implementing predictive enrollment engines. These advanced systems significantly reduce activation time from 39 days to 14 days and eliminate approximately USD 180,000 in unnecessary overhead costs per site, streamlining the enrollment process and improving overall trial efficiency.[1]IntuitionLabs, “Decentralized Trial Market Update,” intuitionlabs.ai

Pandemic-Led Rise of Decentralized and Hybrid Trials Accelerates Infrastructure Investment

Decentralized clinical trials have experienced substantial growth, with spending reaching USD 8.66 billion in 2025 and continuing to rise. AI-driven patient-matching technologies have become integral to these trials, enhancing the efficiency of participant selection.[2]Federal Register, “Electronic Submission of Real-World Data Using HL7 FHIR,” federalregister.gov The adoption of telemedicine consent and direct-to-patient drug shipping has expanded the geographic reach of trials, removing the previous 50-mile radius limitation tied to academic centers. Hybrid trials, which combine home-based monitoring with periodic in-person visits, address regulatory safety requirements while simultaneously providing continuous data streams to AI-powered dashboards. This approach ensures compliance with safety standards while leveraging technology to optimize trial operations.

Regulatory Push for Real-World Data and AI Validation Pathways Creates New Enrollment Opportunities

Regulatory bodies are increasingly supporting the use of real-world data and AI validation in clinical trials, creating new opportunities for patient enrollment. The FDA has endorsed the use of HL7 FHIR submissions, enabling the inclusion of electronic health record-derived evidence in regulatory filings. Similarly, the EMA has introduced draft guidelines requiring transparency in AI architecture, training data, and validation protocols. These measures provide multinational sponsors with a unified compliance framework, simplifying the regulatory process and encouraging the adoption of AI-driven solutions in clinical trials.

Growing EHR Interoperability Enables Scalable Prescreening

The widespread adoption of FHIR R4 in 2025 has significantly improved electronic health record interoperability, allowing sponsors to access patient demographics, diagnoses, and laboratory results without the need for custom interfaces. Vulcan’s accelerator has further streamlined this process by mapping LOINC and SNOMED CT codes into computable phenotypes, which automatically populate case-report forms and reduce transcription errors by 60%. Additionally, natural-language processing models have unlocked insights from unstructured text, increasing the pool of eligible patients by 3.5 times during feasibility studies. These advancements have made prescreening processes more scalable and efficient, ultimately enhancing the overall success of clinical trials.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Bias and cybersecurity concerns around patient data | -3.4% | Global, heightened in EU | Short term (≤ 2 years) |

| Under-representation of minority cohorts in training sets | -2.1% | North America, EU | Medium term (2-4 years) |

| Explainability & Validation Hurdles for AI Algorithms | -3.9% | Global, heightened in EU | Short term (≤ 2 years) |

| Site-Level Workflow Inertia & Change-Management Friction | -2.5% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bias and Cybersecurity Threats Constrain Adoption

Oncology prescreening models exhibit significant accuracy disparities, with up to a 12-percentage-point gap observed across racial subgroups. This has prompted regulatory bodies to emphasize the need for proactive bias assessments to address these discrepancies. Additionally, nearly a quarter of AI platforms lack comprehensive end-to-end encryption, leaving sensitive genomic data vulnerable to breaches. Such vulnerabilities not only compromise data security but also expose organizations to potential regulatory penalties under frameworks like HIPAA or GDPR.

Under-Representation of Minority Cohorts Limits Generalizability

Despite the implementation of FDA Diversity Action Plans, which stress the importance of outreach strategies, data sets from academic institutions remain predominantly composed of 70-80% White patients. This lack of diversity in data significantly limits the generalizability of findings. For instance, a study on hepatocellular carcinoma in China achieved an impressive specificity of 99.1%. However, its sensitivity was only 51.9%, highlighting the challenges in achieving accurate results when documentation from community hospitals is insufficient.[3]Samantha M. Subramaniam et al., “Manual vs AI-Assisted Prescreening,” JAMA Network, jamanetwork.com This under-representation underscores the need for more inclusive data collection practices to improve the applicability of research outcomes across diverse populations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By AI Technology: Machine Learning Leads, NLP Surges

In 2025, machine learning captured 45.10% of the AI market share in clinical trial patient recruitment, showcasing its capability to accurately rank site feasibility. Natural-language processing, driven by algorithms proficient in mining free-text notes containing up to 80% of eligibility data, is projected to grow at a robust 26.25% CAGR. The industry is also adopting predictive analytics, a method validated in real-time pilots with oncology sponsors. This approach enables mid-study patient reassignments based on Bayesian analyses.

Second-generation systems utilize synthetic data to strengthen rare-disease cohorts, enhancing model robustness while protecting identifiers. Compliance with AI/ML software guidance adds an estimated USD 800,000 per lifecycle, extending the time to market but significantly increasing trust among cautious pharmaceutical sponsors.

By Deployment Model: Cloud Dominates, Hybrid Rises

In 2025, cloud platforms accounted for 61.00% of the AI market in clinical trial patient recruitment, as sponsors avoided on-premise GPU expenditures. However, hybrid models are expanding at a 26.86% CAGR, driven by regulations that impose restrictions on cross-border data transfers. The market is witnessing hybrid workflows that retain identifiers on-site while transmitting anonymized eligibility summaries to global dashboards, balancing a 15% latency trade-off for compliance across multiple jurisdictions.

By Clinical Trial Phase: Phase III Rules, Phase I Accelerates

Phase III trials, with their large patient cohorts, accounted for 37.15% of the AI market in clinical trial patient recruitment in 2025, attracting AI providers seeking high-volume transactions. Meanwhile, Phase I studies are projected to grow at a 27.45% CAGR by 2031, as AI-driven dose optimization reduces participant counts and accelerates timelines. The industry benefits from adaptive designs that adjust cohorts based on real-time efficacy, reducing screen failures and the need for rescue sites.

By Therapeutic Area: Oncology Leads, Rare Diseases Grow Fastest

In 2025, oncology secured a 28.25% market share, with NLP efficiently extracting PD-L1 or BRCA statuses from pathology reports, aligning them with biomarker-driven protocols. Enrollment in rare diseases is expected to grow at a 27.87% CAGR, as federated genomic matching identifies mutation-positive patients across diverse EHRs without transferring raw identifiers. Additionally, cardiovascular trials are utilizing smartwatch ECG feeds, which demonstrate an 89.3% sensitivity in detecting atrial fibrillation, thereby expanding participant pools for stroke-prevention studies.

By End User: Sponsors Dominate, Agencies Scale Direct-to-Patient Models

In 2025, pharmaceutical and biotech sponsors held a 46.22% revenue share, reinforcing their role as primary budget controllers. Meanwhile, patient-recruitment agencies are projected to grow at a 26.96% CAGR by 2031, leveraging health-system APIs for large candidate prescreening and deploying multilingual AI coordinators to improve conversion rates. Hospital sites, claiming the remaining share, are adopting lightweight applications that integrate seamlessly into existing EHR workflows. These applications have notably reduced melanoma screening time from 427 minutes to just 2.5 minutes in pilot studies.

By Data Source: EHRs Lead, Wearables Close the Loop

EHRs dominated the 2025 data-source landscape, contributing 52% of the share due to the easily queryable structured fields like ICD-10, RxNorm, and LOINC. Wearables and digital biomarkers, advancing at a 27.00% CAGR, are critical in preemptive patient enrollment. For example, continuous signals can detect edema two weeks before decompensation, enabling timely interventions. Furthermore, patient registries, holding a 14.6% share, play a vital role in rare-disease recruitment by refining inclusion criteria through natural-history data.

Geography Analysis

North America contributes nearly half of global revenue, driven by 50,000 active investigator sites and extensive FHIR interoperability, which enables vendors to seamlessly integrate into health-system data lakes. The region also benefits from FDA pilots that demonstrate real-time oversight, providing assurance to risk-averse sponsors and accelerating procurement decisions. Additionally, state Medicaid claims engines enhance recruitment efforts by identifying disease events within 72 hours.

Asia-Pacific is the fastest-growing territory. Japan's effective use of generative-AI prescreeners and China's regulation requiring anonymized data to undergo security reviews before crossing borders encourage hybrid deployments. Australia, Singapore, and South Korea are adopting similar frameworks, supported by government grants focused on rare-disease diagnostics, which expand the AI in clinical trial patient recruitment market.

Europe follows, supported by GDPR-compliant architectures. EMA guidance on algorithmic transparency and the upcoming EU AI Act simplify filings across 27 states, reducing compliance costs and enabling mid-sized biotech firms to scale multi-country studies with confidence. Eastern European hospitals are increasingly implementing EHR systems compatible with HL7 FHIR standards, unlocking new patient pools for oncology and cardiology trials.

Competitive Landscape

In the fragmented AI market for clinical trial patient recruitment, the top five vendors are projected to capture less than 35% of the 2025 revenue. This highlights opportunities for new entrants, particularly those specializing in language localization, rare-disease data sets, or cybersecurity services. IQVIA has integrated Inteliquet’s natural language processing (NLP) capabilities with its monitoring contracts, providing sponsors with a comprehensive solution for feasibility, enrollment, and submission. This service has been validated using over 840,000 patient records from Kyoto University Hospital. Additionally, Medidata's partnership with Worldwide Clinical Trials in April 2026 has consolidated algorithmic screening, safety-signal detection, and protocol-deviation alerts into a unified platform.

The sector’s vibrancy is evident through strategic mergers and funding activities. In May 2026, Iterative Health raised USD 77 million to expand its AI network beyond gastroenterology into cardiology and obesity, reinforcing the competitive advantage of specialty-specific data. Brazil’s Fiocruz introduced Rebeca, the first generative-AI assistant for trial registration, which has reduced approval cycles to 48 hours and increased Latin America’s visibility in global studies. Vendors focusing on cybersecurity and bias-mitigation analytics are differentiating themselves as regulatory audit requirements become more stringent.

Contract Research Organizations (CROs) and tech startups are also exploring continuous-learning loops. These loops, approved under the FDA’s predetermined change-control plans, enable models to update weekly without requiring new 510(k) submissions. This capability is widening the gap between well-capitalized players and smaller niche providers that face challenges in managing compliance costs.

AI In Clinical Trial Patient Recruitment Industry Leaders

Antidote Technologies

Medidata Solutions

Syneos Health

IQVIA

Parexel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Iterative Health secured USD 77 million Series C funding to broaden its AI network across 100+ research sites on four continents.

- April 2026: FDA launched a real-time monitoring pilot with AstraZeneca and Amgen that streams AI-processed safety data, trimming review cycles by 20–40%.

- March 2026: Gainwell Technologies rolled out a Medicaid claims engine that flags new cardiovascular or diabetes events within 72 hours across 12 states.

- March 2026: IQVIA introduced IQVIA.ai, integrating 150 AI agents to cut Phase III enrollment timelines by up to 50%.

- January 2026: The FDA and EMA released joint principles for AI-enabled trials covering remote consent, telemedicine visits, and algorithmic matching provided validation protocols are filed.

Global AI In Clinical Trial Patient Recruitment Market Report Scope

As per the scope of the report, AI in clinical trial patient recruitment uses machine learning (ML), natural language processing (NLP), and predictive analytics to automate and accelerate finding eligible participants. It works by analyzing unstructured data (notes, EHRs) to match patient health profiles against trial criteria, reducing recruitment time, increasing diversity, and reducing human error.

The AI in clinical trial patient recruitment market is segmented by AI technology, deployment model, clinical trial phase, therapeutic area, end-user, and geography. By AI technology, the market includes machine learning, natural language processing, predictive analytics, and computer vision. By deployment model, the market is segmented into cloud-based, on-premise, and hybrid models. By clinical trial phase, the market is categorized into Phase I, Phase II, Phase III, and Phase IV (post-marketing). By therapeutic area, the market is segmented into oncology, cardiovascular, neurology, metabolic disorders, infectious diseases, rare diseases, and others. By end-user, the market is segmented into pharmaceutical & biotech sponsors, contract research organizations (CROs), academic medical centers, hospital sites & investigator groups, and patient recruitment agencies. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Machine Learning |

| Natural Language Processing |

| Predictive Analytics |

| Computer Vision |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Phase I |

| Phase II |

| Phase III |

| Phase IV (Post-Marketing) |

| Oncology |

| Cardiovascular |

| Neurology |

| Metabolic Disorders |

| Infectious Diseases |

| Rare Diseases |

| Others |

| Pharmaceutical & Biotech Sponsors |

| Contract Research Organizations (CROs) |

| Academic Medical Centers |

| Hospital Sites & Investigator Groups |

| Patient Recruitment Agencies |

| Electronic Health Records (EHR) |

| Genomic & Omics Datasets |

| Patient Registries |

| Insurance Claims |

| Wearables & Digital Biomarkers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By AI Technology | Machine Learning | |

| Natural Language Processing | ||

| Predictive Analytics | ||

| Computer Vision | ||

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Clinical Trial Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV (Post-Marketing) | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular | ||

| Neurology | ||

| Metabolic Disorders | ||

| Infectious Diseases | ||

| Rare Diseases | ||

| Others | ||

| By End User | Pharmaceutical & Biotech Sponsors | |

| Contract Research Organizations (CROs) | ||

| Academic Medical Centers | ||

| Hospital Sites & Investigator Groups | ||

| Patient Recruitment Agencies | ||

| By Data Source | Electronic Health Records (EHR) | |

| Genomic & Omics Datasets | ||

| Patient Registries | ||

| Insurance Claims | ||

| Wearables & Digital Biomarkers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI in clinical trial patient recruitment market today?

The AI in clinical trial patient recruitment market size is USD 0.67 billion in 2026 and is set to reach USD 2.10 billion by 2031.

What is the projected CAGR for AI-driven patient recruitment tools?

The market is forecast to grow at 25.45% CAGR between 2026 and 2031.

Which technology segment holds the largest share?

Machine learning leads with 45.10% share in 2025, driven by mature supervised models used for site feasibility scoring.

Which region is growing fastest in adopting AI for patient recruitment?

Asia-Pacific shows the highest growth, advancing at a 25.95% CAGR through 2031 thanks to national digital-health initiatives in Japan and China.

Why are hybrid deployment models gaining momentum?

Hybrid architectures balance the cost benefits of cloud with strict data-sovereignty rules in the EU, China, and Japan, driving a 26.86% CAGR to 2031.

Page last updated on: