AI In Network Traffic Analysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

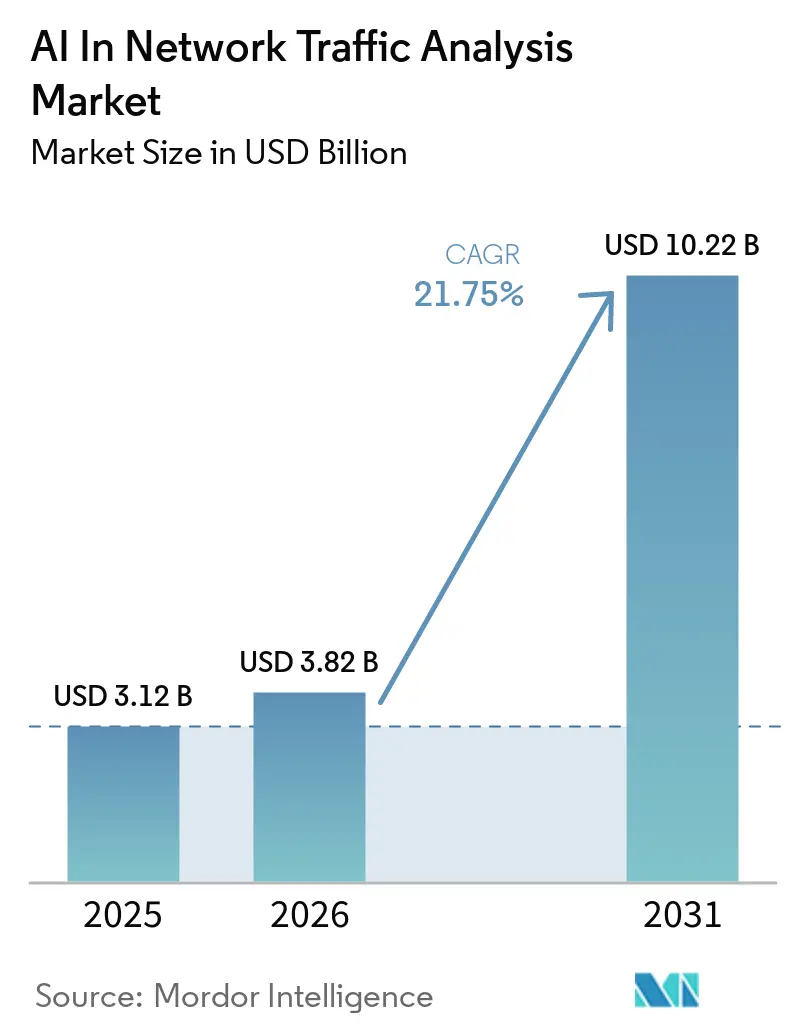

| Market Size (2026) | USD 3.82 Billion |

| Market Size (2031) | USD 10.22 Billion |

| Growth Rate (2026 - 2031) | 21.75% CAGR |

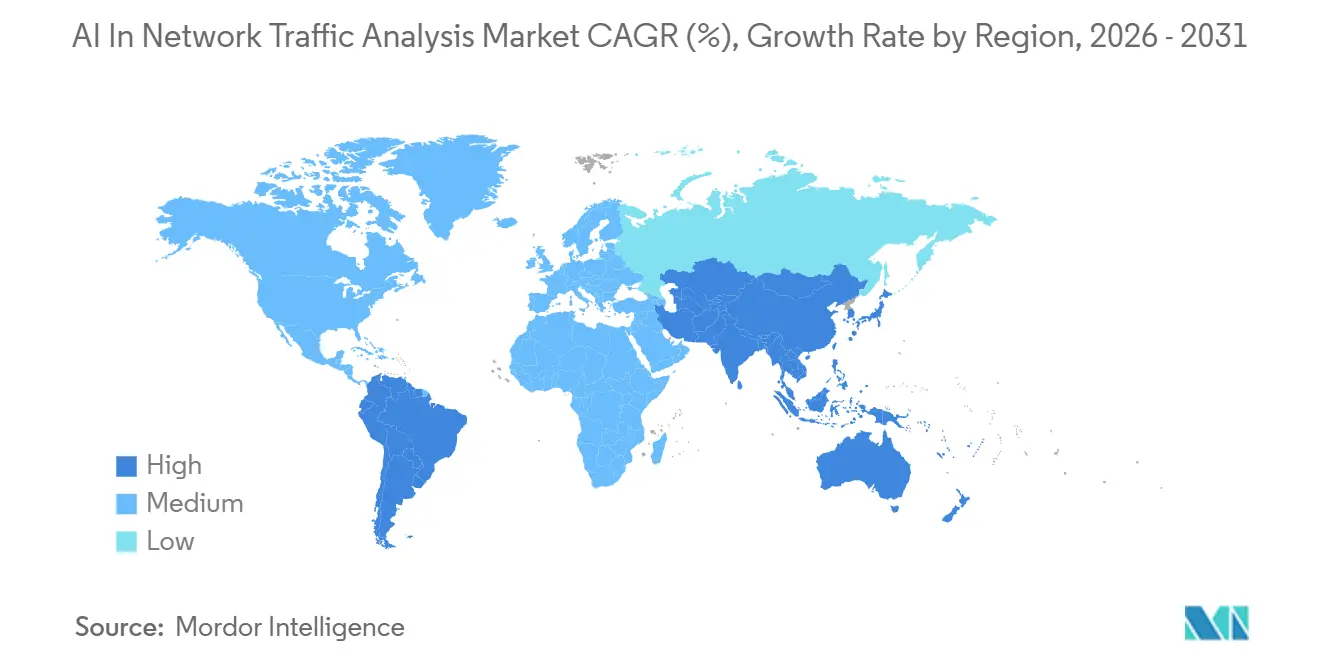

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

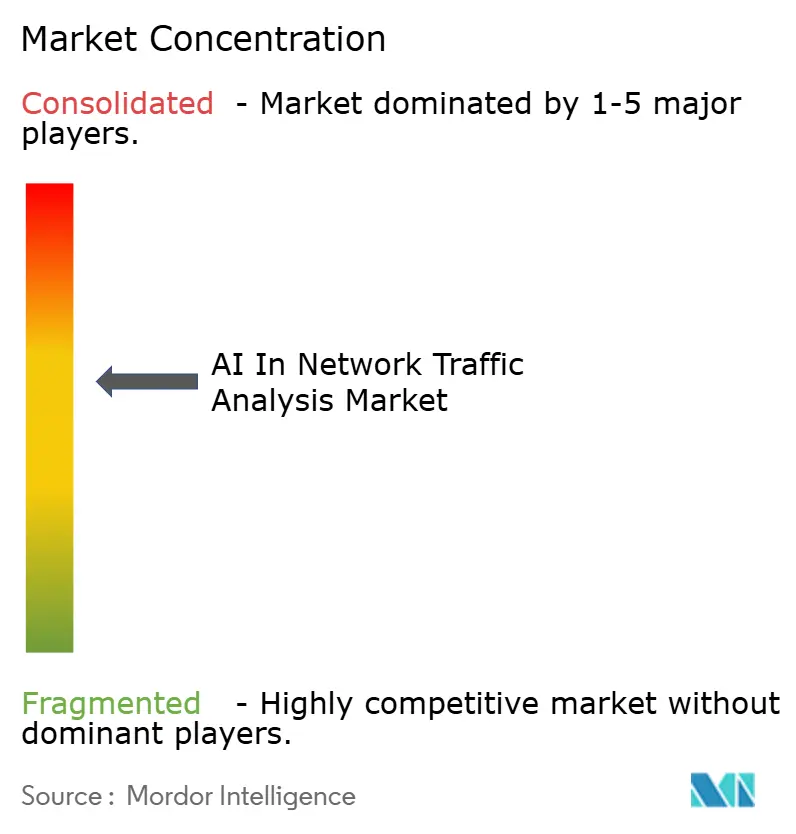

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Network Traffic Analysis Market Analysis by Mordor Intelligence

The AI in network traffic analysis market size is expected to grow from USD 3.12 billion in 2025 to USD 3.82 billion in 2026 and is forecast to reach USD 10.22 billion by 2031 at 21.75% CAGR over 2026-2031. Growth in the AI in network traffic analysis market is being supported by the need to inspect rising cloud traffic, encrypted sessions, and software agents that move through enterprise environments like normal users. Security teams are also buying platforms that can shorten response time when detection tools are spread across network, cloud, identity, and endpoint layers. Compliance pressure is reinforcing demand, especially as zero-trust programs, segmentation rules, and traffic-logging obligations now require more consistent monitoring. The vendor field is split between large security platforms that sell integrated controls and specialists that focus on behavioral models, observability, and network detection and response. This leaves room in the AI in network traffic analysis market for providers that can govern AI agent behavior, correlate telemetry across hybrid environments, and deliver managed outcomes for teams with limited security talent.

Key Report Takeaways

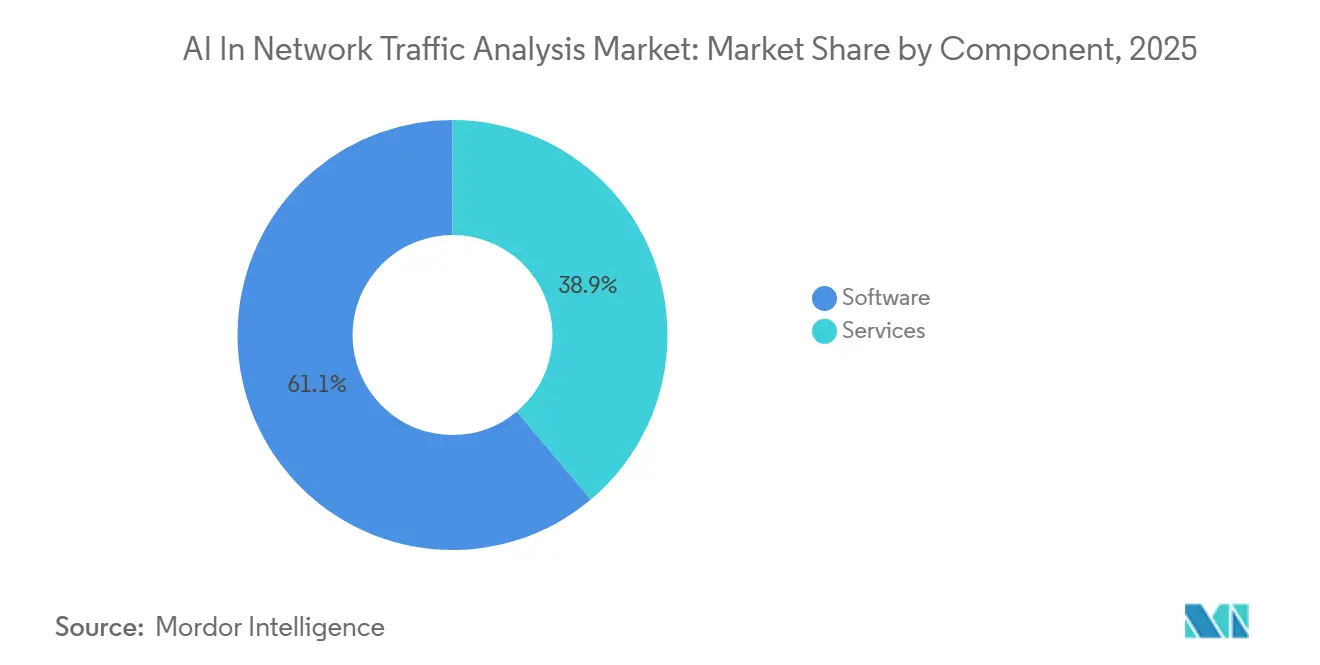

- By component, software remained the dominant delivery layer, with a 61.12% share of the AI in network traffic analysis market in 2025, while services are projected to expand at a 22.84% CAGR through 2031.

- By deployment, cloud held 54.08% share in 2025, while hybrid is expected to remain the fastest-growing deployment model through 2031.

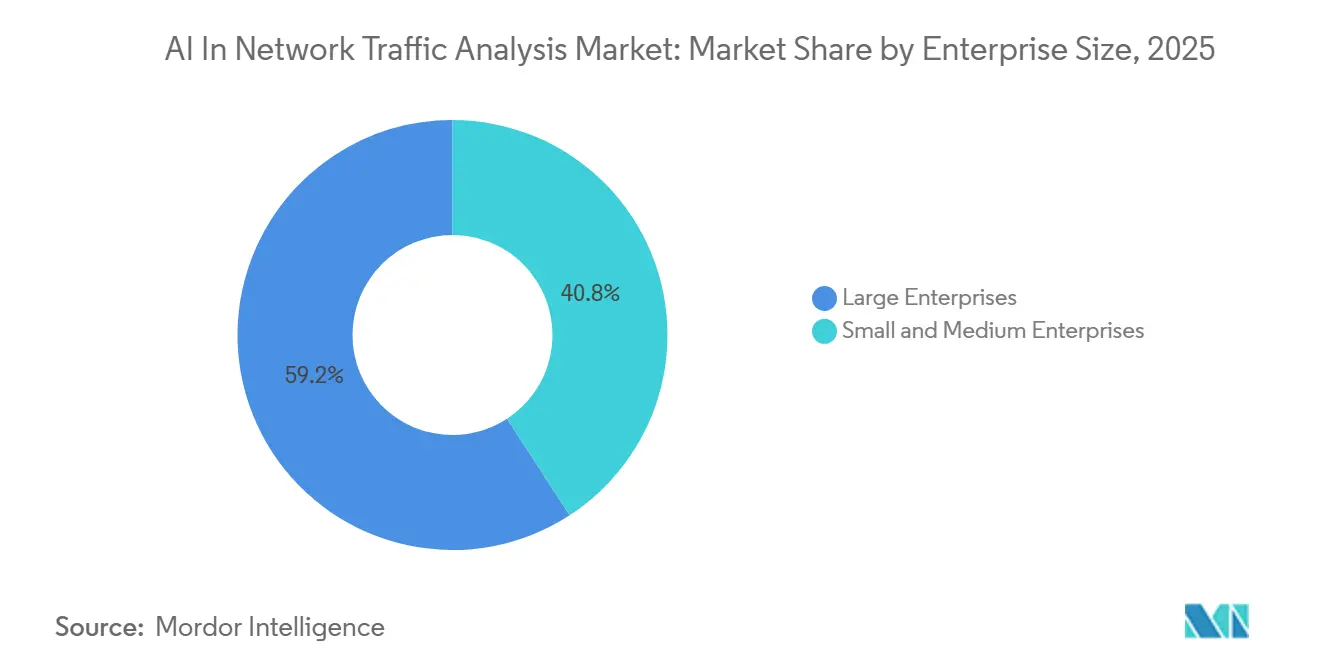

- By enterprise size, large enterprises held 59.17% share of AI in the network traffic analysis market in 2025, while SMEs are expected to post the fastest growth through 2031.

- By network type, enterprise networks remained the largest segment in 2025, while cloud networks are projected to grow at a 23.17% CAGR through 2031.

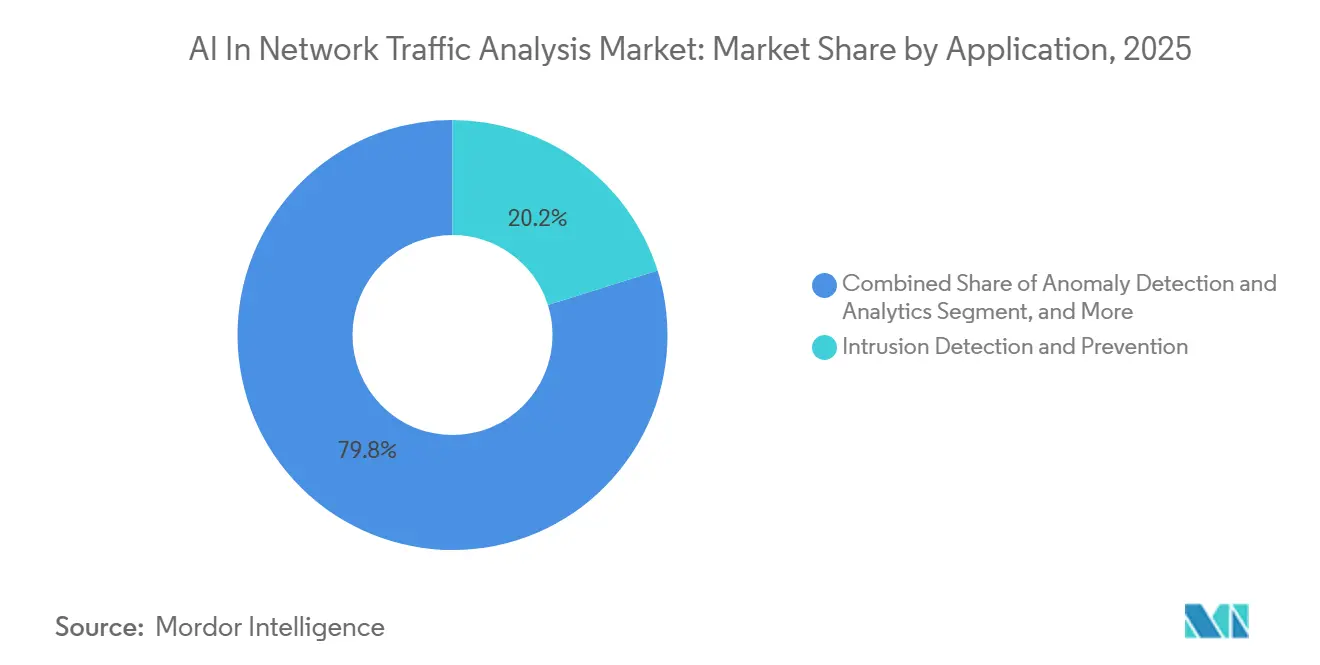

- By application, intrusion detection and prevention accounted for 20.16% share in 2025, while anomaly detection and behavioral analytics are expected to remain the fastest-growing applications through 2031.

- By end-user industry, BFSI remained the largest demand center in 2025, while healthcare and life sciences are projected to expand at a 23.39% CAGR through 2031.

- By geography, North America held 32.11% share in 2025, while the AI in network traffic analysis market in the Asia-Pacific is projected to grow at a 23.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Network Traffic Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Enterprise Demand for Real-Time Threat Detection | +3.2% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Increasing Hybrid and Multi-Cloud Network Complexity | +2.8% | Global, with particular intensity in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing Adoption of Zero Trust And XDR Architectures | +2.3% | North America and Europe, with federal mandate influence in the United States | Medium term (2-4 years) |

| Expansion of Encrypted Traffic Monitoring Requirements | +1.9% | Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Need for Automated Network Forensics and Root-Cause Analysis | +1.4% | Global, with early gains in North America and Asia-Pacific core markets | Long term (≥ 4 years) |

| AI Model Drift Management Demand in Security Operations | +0.9% | North America and Europe, with spillover into Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Demand for Real-Time Threat Detection

Real-time threat detection has become a near-term buying priority in the AI in network traffic analysis market because security teams cannot wait hours to validate suspicious traffic. ExtraHop reported in 2026 that 55% of respondents viewed AI tools as a top security risk, underscoring how quickly this need has moved into live security budgets.[1]ExtraHop, “Is Your AI Security Strategy Falling Short? Inside the 2026 Global Threat Landscape Report,” ExtraHop, extrahop.com The issue is sharper when autonomous software agents communicate across internal networks, because their behavior can blend into normal machine traffic until patterns are modeled continuously. ExtraHop launched AI Observability in March 2026 to discover AI infrastructure, map agent communication patterns, and detect unauthorized data movement in real time. These capabilities matter because they help analysts move from alert review to action before lateral movement spreads across connected systems. As a result, the AI in network traffic analysis market is shifting toward continuous behavioral inspection rather than periodic traffic review.[2]ExtraHop, “ExtraHop Delivers the Foundation for Secure AI Innovation Across the Agentic Enterprise,” ExtraHop Press Release, extrahop.com

Increasing Hybrid and Multi-Cloud Network Complexity

Hybrid and multi-cloud sprawl is widening blind spots in the AI in network traffic analysis market and raising the value of tools that can follow traffic across several environments. Gigamon's 2025 survey found that 91% of organizations made risky security compromises in hybrid cloud environments under pressure to adopt AI. The same survey found that 47% were already seeing more attacks targeting large language model deployments, tying network visibility gaps directly to new enterprise workloads. Thales reported in 2025 that 55% of respondents found cloud environments harder to secure than on-premises systems. Thales also reported that organizations use an average of 85 SaaS applications, which means traffic baselines must cover many distinct patterns. This is why the AI in network traffic analysis market is moving toward broader observability across east-west traffic, cloud services, and shared policy layers.

Growing Adoption f Zero Trust and XDR Architectures

Zero trust and XDR programs are expanding the telemetry burden inside the AI in network traffic analysis market. Under zero trust rules, security teams need constant visibility into who connects to which asset, how often, and under what conditions, which makes behavioral baselines more useful than static rules. The U.S. Department of Defense directed all components in July 2025 to implement Target Level Zero Trust across classified and unclassified systems, and the directive also called for XDR integration with operational technology environments.[3]U.S. Department of Defense, “DTM 25-003 Implementing the DoD Zero Trust Strategy,” DoD CIO, defense.gov That policy direction has pushed regulated buyers to place network telemetry closer to the center of security architecture. Vendors are responding by tying network analytics to identity, endpoint, cloud, and OT controls, enabling suspicious behavior to be validated more quickly. The AI in network traffic analysis market benefits because traffic analysis becomes a core sensor layer rather than a side tool.

Expansion of Encrypted Traffic Monitoring Requirements

Encrypted traffic monitoring is becoming more important in the AI in network traffic analysis market because payload inspection is no longer easy or always permitted. NIST noted that TLS 1.3 removed passive decryption methods that many legacy tools relied on, prompting security teams to analyze metadata, flow timing, and certificate behavior.[4]National Institute of Standards and Technology, “Addressing Visibility Challenges With TLS 1.3 Within the Enterprise,” National Institute of Standards and Technology, nist.gov Privacy rules are also shaping deployment choices, especially when sensitive health or financial communications require narrower inspection policies. The growing use of segmented environments in regulated sectors underscores the value of monitoring methods that can detect suspicious activity without relying on full packet capture. This is steering buyers toward selective inspection models that preserve detection value without relying on broad decryption practices. The AI in network traffic analysis market is therefore seeing higher demand for tools that can infer threat behavior from encrypted sessions with lower privacy risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High False Positive Sensitivity in Diverse Traffic Environments | -2.1% | Global, most acute in large enterprises with heterogeneous traffic | Short term (≤ 2 years) |

| Data Privacy And Packet Inspection Constraints | -1.7% | Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Skilled Analyst Shortage for AI Tuning And Validation | -1.3% | Global, most acute in emerging Asia-Pacific and Middle East and Africa markets | Long term (≥ 4 years) |

| Integration Friction With Legacy NDR, SIEM, and SOAR Stacks | -0.9% | North America and Europe, where legacy tool estates are largest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High False Positive Sensitivity in Diverse Traffic Environments

False positives remain a practical barrier in the AI in network traffic analysis market because noisy alerts consume limited analyst time and weaken trust in automated detection. A 2025 study in the International Journal of Advanced Research in Computer Science and Engineering found that AI-driven predictive analytics cut false positives by more than 40% compared with rule-based systems. That improvement is meaningful, but it does not remove the burden created by high-volume enterprise traffic and mixed device environments. When models are trained on past behavior, detection quality can weaken as new SaaS tools, container workloads, or IoT devices change network patterns. This is especially hard in environments that monitor IT, OT, and IoT traffic together, because a single baseline rarely fits all asset classes. Until vendors make tuning easier, some buyers will slow rollouts or keep human review tightly in the loop.

Data Privacy and Packet Inspection Constraints

Data privacy constraints and packet inspection rules are slowing certain parts of the AI in network traffic analysis market, even as demand for visibility is rising. NIST documented that TLS 1.3 reduces passive visibility within enterprise networks, making inspection decisions more complex for security teams that also need to honor privacy safeguards. Healthcare buyers face another layer of caution because segmented environments and sensitive records require tighter controls on what can be inspected and retained. These conditions do not prevent adoption, but they shift spending toward metadata-based analytics and encrypted traffic analysis rather than full packet capture. Global companies also need different inspection settings across regions, which increases rollout time and integration work. This keeps procurement cycles longer and favors vendors that can support flexible policy controls by geography and data type.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth is Changing Delivery Economics

Services are the fastest-growing component of the AI in network traffic analysis market, with a 22.84% CAGR during 2026-2031, positioning operating support close to the center of demand. That pace shows that many buyers now want ongoing monitoring, tuning, and response help instead of a one-time software purchase. Software remains the main delivery layer with a share of 61.12% because network detection and response platforms, behavioral analytics engines, and SIEM integrations are how most organizations deploy inspection at scale. The AI in network traffic analysis market is moving this way because many teams can buy a platform faster than they can build enough in-house expertise to operate it well. This makes service attachments more valuable in large rollouts where model tuning, policy setting, and investigation support all shape real-world performance.

Services in the AI in network traffic analysis market are projected to outpace headline growth through 2031, nudging vendors toward recurring delivery models. IBM launched ATOM in April 2025 to automate threat triage, investigation, and remediation, demonstrating how software vendors are packaging service-like outcomes within their platforms. Darktrace launched SECURE AI in February 2026 to extend behavioral oversight to generative AI tools and autonomous agents, thereby reducing the burden on internal teams that lack dedicated AI security specialists. As these models mature, customers will compare vendors less on feature lists and more on speed to value, depth of coverage, and day-to-day operational support. In the AI in network traffic analysis industry, providers that preconfigure traffic models for healthcare, finance, and industrial environments should retain an edge in services-led sales.

By Deployment: Cloud Leads While Hybrid Demand Broadens

Cloud deployment accounted for 54.08% of the AI in network traffic analysis market share in 2025, making it the largest delivery model among enterprise buyers. That lead reflects faster rollout, easier scaling, and broader sensor reach across distributed users, applications, and branch locations. The AI in network traffic analysis market is also favoring cloud delivery because software updates and detection improvements can be applied faster than appliance-based refresh cycles. Hybrid deployment is the fastest-growing model through 2031 because most large organizations still split sensitive systems, legacy workloads, and cloud analytics across multiple environments. That split keeps demand high for platforms that can correlate activity across both settings without leaving inspection gaps at the boundary.

Hybrid deployment is growing faster than the other models through 2031, while on-premises infrastructure continues to hold a necessary role in defense, government, and regulated finance. Cato Networks launched a GPU-powered SASE platform in March 2026, which showed that cloud-delivered inspection can now support more demanding inline analysis workloads. This matters because buyers no longer want to trade off performance against flexibility when they move network visibility into cloud-based control planes. The AI in network traffic analysis market should continue rewarding vendors that can apply consistent behavioral logic across private, public, and mixed environments. Vendors that support cloud, on-premises, and sovereign deployment models with the same policy quality are likely to remain stronger in complex accounts.

By Enterprise Size: Large Accounts Lead While SME Adoption Builds

Large enterprises held 59.17% of the AI in network traffic analysis market in 2025, which kept them at the center of vendor roadmaps and product design. Their lead reflects higher security budgets, more complex network estates, and stronger oversight across critical data, hybrid workloads, and regulated operations. The AI in network traffic analysis market still depends heavily on these customers because they generate large telemetry volumes and demand tighter integration across tools. At the same time, smaller organizations are becoming a more active source of new demand as SaaS delivery and managed services lower deployment barriers. This shift matters because many mid-sized teams want outcome-based coverage rather than a large in-house engineering build.

Small and medium enterprises are growing faster through 2031, even though large enterprises still dominate current spending and deployment depth in the AI in network traffic analysis market. ExtraHop launched an all-in-one NDR sensor in April 2025, reflecting a push toward simpler deployment, combined visibility, and easier operations for leaner teams. Easier packaging helps buyers who need detection, forensics, and performance visibility without having to maintain multiple tools or specialist staff. The AI in network traffic analysis market should continue to expand its customer base as pricing, onboarding, and managed response models become easier to adopt. In the AI in network traffic analysis industry, vendors that align with common SME traffic patterns in retail, healthcare, and local manufacturing can build stickier positions.

By Network Type: Cloud Traffic Is Expanding The Fastest

Cloud networks are projected to grow at a 23.17% CAGR during 2026-2031, making them the fastest-growing network type in the AI in network traffic analysis market. Enterprise networks still hold the largest share because they remain the main location for internal monitoring, compliance logging, and coordinated incident response. The AI in the network traffic analysis market continues to rely on enterprise networks because they carry identity activity, application flows, and lateral movement that teams must continuously validate. Data center environments keep a stable role because the same flow records support both security review and performance oversight. Industrial and OT networks are smaller today, but they are becoming more relevant as cyber risk moves closer to physical operations and production uptime.

Cloud networks are posting the strongest growth through 2031 because older perimeter tools often miss east-west movement inside containers, microservices, and serverless architectures. The U.S. Department of Defense required XDR integration with OT environments in its July 2025 zero-trust directive, which supports stronger monitoring beyond traditional IT networks. Vectra AI expanded unified cloud network observability across AWS, Azure, Google Cloud, and Oracle Cloud Infrastructure in June 2026, which showed where vendors are investing to close cross-cloud blind spots. These developments are prompting buyers to seek a single detection framework that covers enterprise, cloud, and OT environments without major policy fragmentation. The AI in network traffic analysis market is therefore moving toward network-type coverage that spans physical and virtual traffic within a single operating model.

By Application: Intrusion Detection Leads While Behavioral Analytics Gains Strength

Intrusion detection and prevention accounted for 20.16% of the AI in network traffic analysis market size in 2025, which made it the largest application segment. That lead reflects the continuing need to identify hostile activity early and support baseline compliance controls across enterprise environments. The AI in network traffic analysis market is also seeing faster expansion in anomaly detection and behavioral analytics, as static signatures struggle with zero-day attacks and AI-generated attack variants. This keeps the application mix broad, since buyers still need threat hunting, incident response, forensics, and performance monitoring around the same core telemetry. Capacity planning and traffic optimization remain smaller uses, but they add operational value beyond direct security tasks.

Anomaly detection and behavioral analytics are growing faster through 2031, while intrusion detection and prevention still anchors the largest current spend base in the AI in network traffic analysis market. A 2025 peer-reviewed Springer study reported an average cross-dataset accuracy of 96% for AI-driven intrusion detection across heterogeneous network environments. Fortinet advanced its security operations platform in March 2026 with agentic AI and deeper telemetry integration, which showed how detection, investigation, and response workflows are being simplified for analysts. That shift should help adoption move beyond highly specialized teams because the interface between alert review and action becomes clearer. Vendors that combine detection quality with simpler investigation flows should continue to gain share as usage expands across more security and network teams.

By End-User Industry: BFSI Anchors Current Demand While Healthcare Expands Faster

The healthcare and life sciences segment is projected to grow at a 23.39% CAGR during 2026-2031, making it the fastest-growing end-user segment in the AI in network traffic analysis market. The main driver is the push for stronger segmentation and closer monitoring of sensitive health data flows across distributed care environments. BFSI remained the largest end-user group because fraud exposure, critical transaction traffic, and strict oversight keep network visibility high on spending agendas. The AI in network traffic analysis market also remains relevant across IT and telecom, retail, manufacturing, and government because each sector has distinct traffic patterns and threat models. This means vendors need more than one generic anomaly threshold when they design deployments for different vertical environments.

Healthcare and life sciences are growing faster than the rest of the end-user base through 2031, while government and defense continue to influence buying standards in adjacent sectors. The DoD directive from July 2025 reinforced that direction by tying zero trust progress to XDR and OT integration requirements across both classified and unclassified systems. Government agencies are important reference buyers because their operating requirements often shape later enterprise expectations around visibility, validation, and segmentation. The AI in network traffic analysis market keeps broadening by vertical because each sector now has a clearer reason to map normal behavior and flag deviations earlier. In the AI in network traffic analysis industry, suppliers that package sector-specific use cases should see better adoption and renewal performance.

Geography Analysis

North America held 32.11% of the AI in network traffic analysis market share in 2025, maintaining its lead across regions. The region benefits from mature security budgets, high vendor concentration, and quicker adoption of new detection models across large enterprises. The U.S. Department of Defense directive issued in July 2025 raised the operational bar by requiring target-level zero trust and XDR integration across classified and unclassified systems, including OT environments. That kind of federal direction often shapes procurement standards far beyond direct government use. The AI in network traffic analysis market also gains regional support from vendor headquarters, channel depth, and a large installed base of enterprise security tools.

Europe remains an important demand center because enterprises need closer monitoring while balancing tighter privacy expectations around packet inspection. CERT-FR's 2025 cyber threat panorama highlighted the growing use of AI tools by threat actors, underscoring the need for stronger behavioral monitoring across European networks. This keeps interest high in metadata-based analysis, encrypted traffic monitoring, and region-specific policy controls. South America is still earlier in adoption, but Brazil is leading regional demand as digitization in finance and other regulated services raises the need for better network visibility.

Asia-Pacific is projected to expand at a 23.51% CAGR during 2026-2031, making it the fastest-growing regional segment of the AI in network traffic analysis market. Demand is being supported by cloud buildout, private 5G activity, and a wider push to secure distributed digital infrastructure. Vendors are expanding regional delivery capacity to offer cloud-based detection with lower latency and stronger local support. The Middle East and Africa are building from a smaller base, with Gulf countries leading enterprise cybersecurity spending while African adoption is more concentrated in financial services. As these regional patterns evolve, the AI in network traffic analysis market should continue to split into mature platform markets, compliance-led markets, and cloud-expansion markets.

Competitive Landscape

The AI in network traffic analysis market shows moderate consolidated at the platform level, but it remains open enough for specialists to win targeted use cases. Cisco Systems, Palo Alto Networks, Fortinet, and IBM compete mainly on integration depth, telemetry breadth, and the ability to bundle detection with managed outcomes. Cisco's June 2025 security announcements tied XDR, Splunk Security, and AI Defense into a more unified workflow, strengthening its position in network-centered security operations. IBM introduced Autonomous Security in April 2026 to analyze exposures, detect anomalies, and contain threats through multi-agent workflows, signaling a stronger move toward automated operating models. These moves show that scale vendors are trying to make traffic analysis a native part of a broader security platform.

Palo Alto Networks has also been broadening its Cortex platform to enable advanced AI reasoning to support detection, investigation, and response across multiple workflows. Fortinet advanced its security operations platform in March 2026 with unified SOC functions, agentic AI, and deeper telemetry integration, which made its network detection stack more central to multivendor monitoring. In the AI in network traffic analysis market, these platform strategies matter because many buyers want fewer tools and faster operational handoffs. They also raise switching costs, as telemetry, policy logic, and analyst workflows become increasingly intertwined over time.

Specialists are still gaining ground where large platforms have moved more slowly, especially in deep behavioral models, unified cloud observability, and AI traffic governance. ExtraHop launched AI Asset Inventory and AI Observability in March 2026 to discover agentic AI infrastructure and monitor related communication paths in real time. Vectra AI expanded unified cloud network observability across AWS, Azure, Google Cloud, and Oracle Cloud Infrastructure in June 2026, which sharpened its value in hybrid environments. Cato Networks introduced GPU-based inline inspection into its SASE platform in March 2026, demonstrating that performance-led specialization still has room to differentiate. This competitive mix means the AI in network traffic analysis market rewards both scale and focused technical depth, rather than pushing all demand toward one vendor model.

AI In Network Traffic Analysis Industry Leaders

Darktrace plc

Vectra AI, Inc.

ExtraHop Networks, Inc.

Gigamon Inc.

NETSCOUT Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: IBM joined the OpenAI Daybreak Cyber Partner Program and launched a new application security service using OpenAI's frontier AI models to identify and validate software vulnerabilities, extending machine-speed AI reasoning into network and application security operations workflows.

- June 2026: Palo Alto Networks announced native support for Anthropic Claude Sonnet 4.6, Claude Opus 4.8, and Google Gemini 3.5 Flash across the Cortex platform, embedding frontier AI reasoning across XSIAM, AgentiX, XDR, and Cloud for advanced network threat detection and investigation automation.

- May 2026: IBM and Red Hat launched Project Lightwell, a USD 5 billion commitment deploying more than 20,000 engineers to secure open source software at scale using frontier AI capabilities to identify and fix vulnerabilities across critical software infrastructure that underpins global network security deployments.

- April 2026: IBM introduced IBM Autonomous Security, a multi-agent-powered service designed to analyze software exposures, detect network anomalies, enforce security policies, and contain threats at machine speed, with insights feeding directly into governance and risk management systems.

Global AI In Network Traffic Analysis Market Report Scope

The AI in Network Traffic Analysis market refers to platforms and services that leverage artificial intelligence to monitor, analyze, and secure network traffic across enterprise, cloud, data center, and industrial environments. These solutions apply AI-driven analytics to detect intrusions, identify anomalies, optimize performance, and support incident response and forensic investigations, enabling organizations to gain deeper visibility into network behavior, proactively hunt threats, and automate capacity planning and traffic optimization. The market is driven by the exponential growth of digital connectivity, rising cyber threats, and the increasing complexity of hybrid and cloud-based networks, with industries such as BFSI, healthcare, IT, manufacturing, retail, and government adopting AI-powered traffic analysis to strengthen resilience, ensure compliance, and maintain secure and efficient operations. Its primary objective is to deliver adaptive, intelligence-driven monitoring and defense capabilities that minimize risk exposure, enhance operational efficiency, and safeguard digital infrastructures against evolving cyberattacks.

The AI in Network Traffic Analysis market report is segmented by Component (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Network Type (Enterprise Networks, Data Center Networks, Cloud Networks, Industrial and OT Networks), Application (Intrusion Detection and Prevention, Network Performance Monitoring, Anomaly Detection and Behavioral Analytics, Threat Hunting and Incident Response, Network Forensics and Root Cause Analysis, Capacity Planning and Traffic Optimization), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Enterprise Networks |

| Data Center Networks |

| Cloud Networks |

| Industrial and OT Networks |

| Intrusion Detection and Prevention |

| Network Performance Monitoring |

| Anomaly Detection and Behavioral Analytics |

| Threat Hunting and Incident Response |

| Network Forensics and Root Cause Analysis |

| Capacity Planning and Traffic Optimization |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Network Type | Enterprise Networks | ||

| Data Center Networks | |||

| Cloud Networks | |||

| Industrial and OT Networks | |||

| By Application | Intrusion Detection and Prevention | ||

| Network Performance Monitoring | |||

| Anomaly Detection and Behavioral Analytics | |||

| Threat Hunting and Incident Response | |||

| Network Forensics and Root Cause Analysis | |||

| Capacity Planning and Traffic Optimization | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Information Technology and Telecom | |||

| Retail and E-commerce | |||

| Industrial Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the AI in network traffic analysis market?

The AI in network traffic analysis market is valued at USD 3.82 billion in 2026 and is forecast to reach USD 10.22 billion by 2031.

What growth rate is expected through 2031 for AI in network traffic analysis?

The sector is forecast to grow at a 21.75% CAGR from 2026 to 2031, supported by cloud expansion, encrypted traffic monitoring, and zero trust adoption.

Which deployment model leads AI in network traffic analysis today?

Cloud deployment led in 2025 with a 54.08% share because it offers faster rollout, broader reach, and easier scale across distributed environments.

Which customer group is driving the fastest adoption?

Healthcare and life sciences is the fastest-growing end-user segment with a 23.39% CAGR, while SMEs are also becoming more active as managed delivery lowers barriers.

Why are cloud networks becoming more important in traffic analysis?

Cloud networks are projected to expand at a 23.17% CAGR because east-west traffic inside containers, microservices, and virtual environments is harder to monitor with older perimeter tools.

Who are the main competitors in this space?

Large platform vendors such as Cisco, Palo Alto Networks, Fortinet, and IBM lead broad enterprise accounts, while specialists such as ExtraHop, Vectra AI, Darktrace, and Cato Networks compete on focused capabilities.

Page last updated on: