Network Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

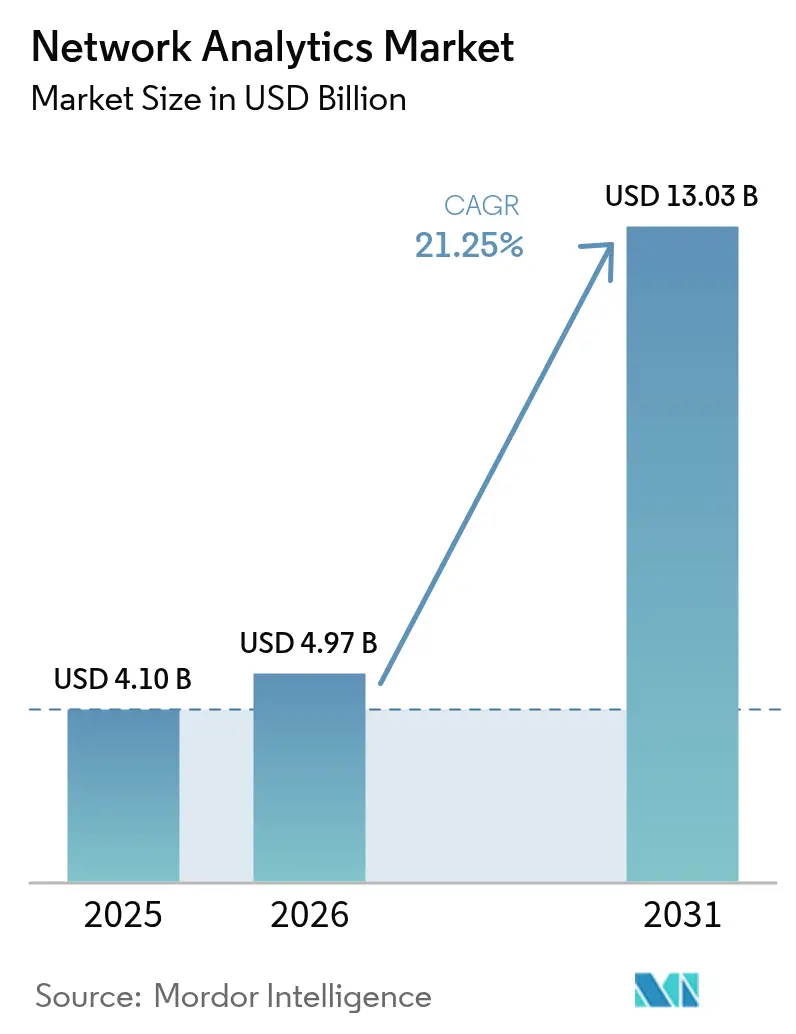

| Market Size (2026) | USD 4.97 Billion |

| Market Size (2031) | USD 13.03 Billion |

| Growth Rate (2026 - 2031) | 21.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Network Analytics Market Analysis by Mordor Intelligence

The network analytics market size was valued at USD 4.10 billion in 2025 and estimated to grow from USD 4.97 billion in 2026 to reach USD 13.03 billion by 2031, at a CAGR of 21.25% during the forecast period (2026-2031). Rapid data-traffic growth, 5G roll-outs, and the surge in connected devices have pushed network analytics from simple monitoring to a core element of digital infrastructure strategy. Enterprises view analytics as essential for predictive maintenance, capacity planning, and security, while service providers use it to monetize programmable networks. Artificial intelligence now underpins most leading platforms, with 60% of technology executives planning AI-enabled automation to streamline operations[1]Chuck Robbins, “The Role of Predictive Automation in Modern Networks,” Cisco, cisco.com. Consolidation among vendors, illustrated by IBM’s USD 6.4 billion acquisition of HashiCorp, signals demand for end-to-end stacks that blend analytics with broader IT management. Although high initial costs and specialized skill shortages still hinder adoption, cloud delivery models and managed services are easing entry barriers.

Key Report Takeaways

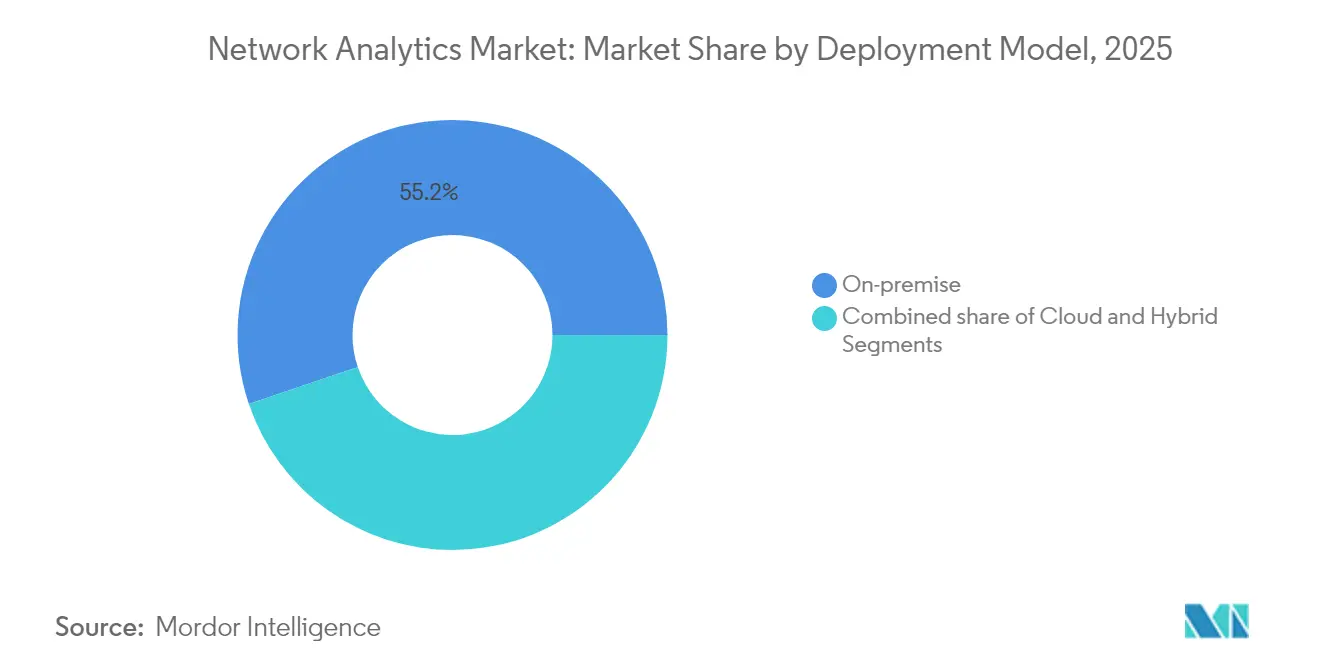

- By deployment model, on-premise installations led with 55.20% of the network analytics market share in 2025, while cloud deployments are set to advance at a 23.4% CAGR through 2031.

- By component, solutions captured 62.40% revenue share in 2025; services are forecast to grow the fastest at a 22.6% CAGR to 2031.

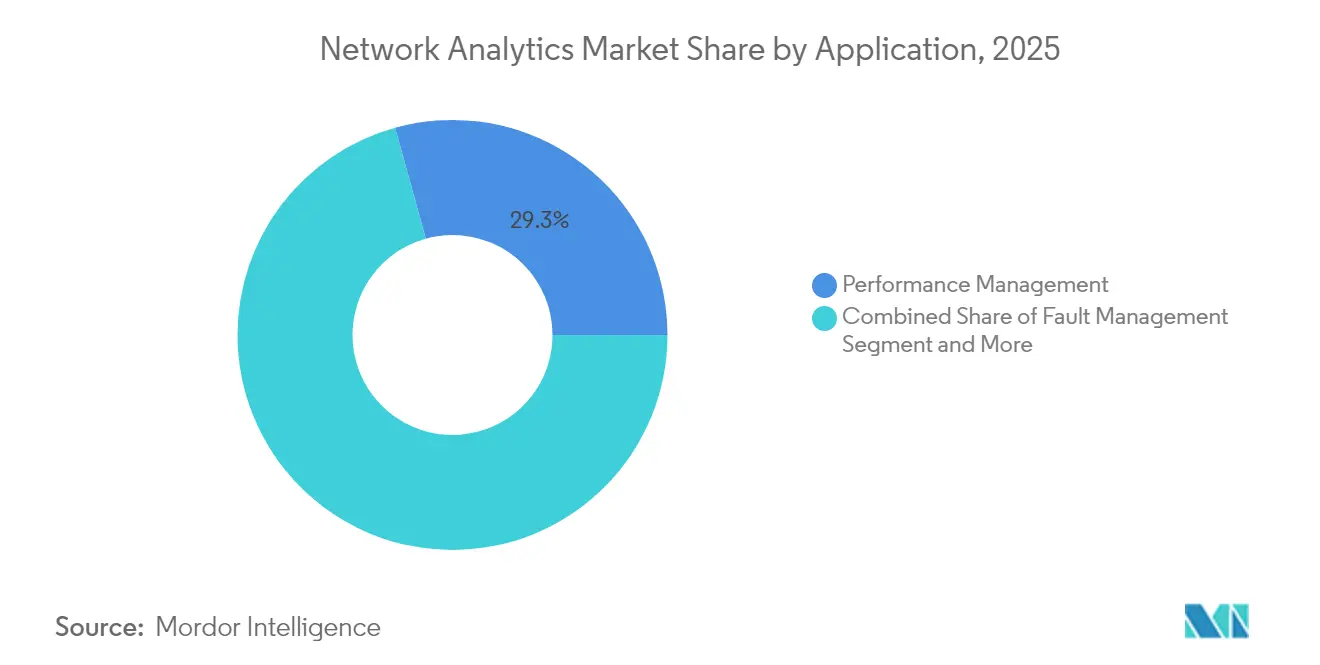

- By application, performance management held 29.30% of the network analytics market size in 2025, whereas security and anomaly detection are projected to expand at a 23.0% CAGR to 2031.

- By end user, communication service providers commanded 47.20% of the network analytics market size in 2025; cloud service providers exhibit the highest forecast CAGR of 22.3% through 2031.

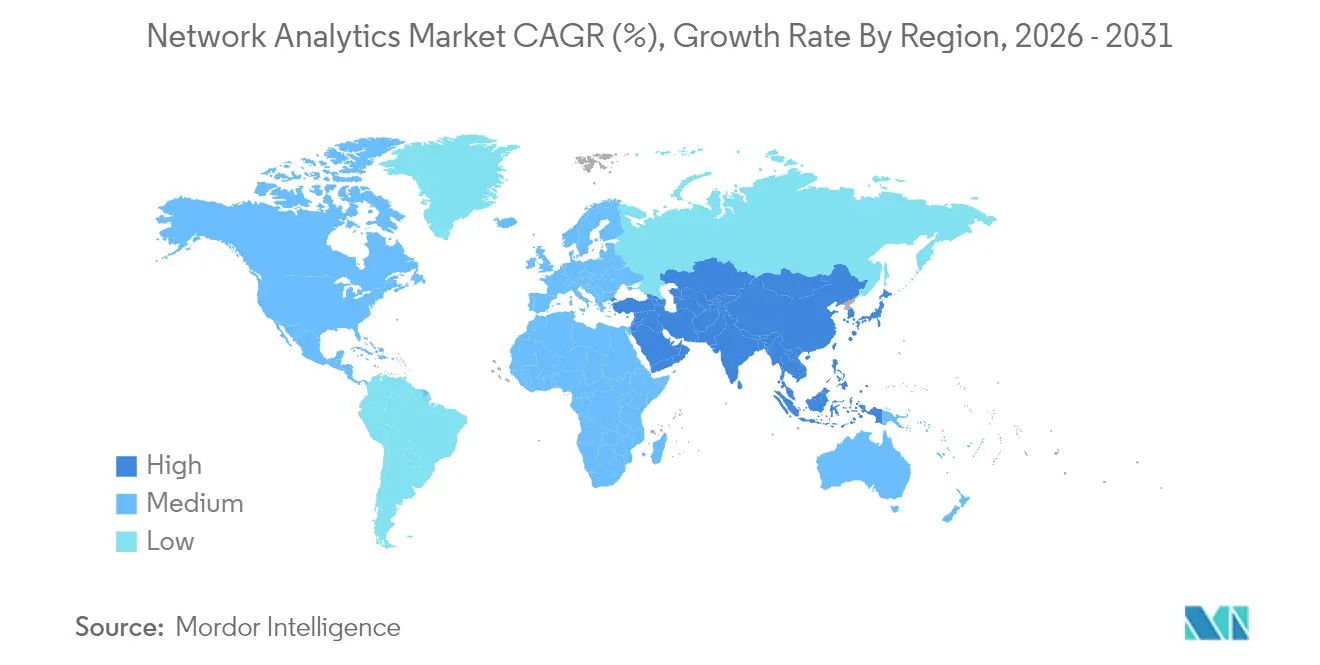

- By geography, North America maintained a 37.60% revenue share in 2025; Asia-Pacific is poised for a 22.7% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Network Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Autonomous and self-managing networks | +5.8% | North America, Europe | Medium term (2-4 years) |

| IoT and machine-to-machine expansion | +4.7% | Asia-Pacific, Global | Long term (≥ 4 years) |

| 5G roll-out and data-traffic surge | +4.3% | North America, Europe, Developed APAC | Medium term (2-4 years) |

| Closed-loop AI digital-twin optimisation | +3.2% | North America, Europe | Long term (≥ 4 years) |

| API-driven “network-as-code” monetisation | +2.1% | North America, Emerging Europe & APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Need for Autonomous and Self-Managing Networks

Escalating network complexity and the cost of downtime—USD 9,000 per minute for cloud-centric firms—have intensified demand for self-healing infrastructure. AI-infused analytics platforms now predict and remediate faults, enabling a shift from reactive troubleshooting to proactive optimisation. Industries running mission-critical workloads increasingly depend on AIOps, with 72% of IT leaders planning platform-based architectures that merge analytics, automation, and observability[2]Chuck Robbins, “The Role of Predictive Automation in Modern Networks,” Cisco, cisco.com. As a result, vendors are embedding real-time anomaly detection and policy-driven orchestration to cut mean-time-to-repair and protect service-level objectives.

Rise of IoT and Machine-to-Machine Communications

Network analytics platforms have added device-level visibility, protocol decoding, and behavioural baselining to manage heterogeneous traffic. In manufacturing, utilities, and smart-city roll-outs, real-time analytics supports predictive maintenance and energy optimisation, unlocking measurable cost savings and uptime improvements.

Exponential Data Traffic and 5G Roll-Out Pressure

5G promises speeds 100-times faster than 4G and latency under 1 millisecond, supporting up to 1 million devices per square kilometre. Such density amplifies traffic bursts and slicing complexity. Communication service providers rely on analytics to model network slices, forecast capacity, and maintain quality of experience during live events. Real-time correlation of radio, core, and transport metrics now underpins differentiated guarantees for enterprise customers.

Closed-Loop AI Digital-Twin Optimisation

Digital twins replicate live networks for scenario testing, capacity planning, and change-risk assessment. When fused with AI, they have delivered a 32% improvement in issue-resolution time for early adopters[3]Rob Thomas, “Hybrid Cloud Strategy After HashiCorp,” IBM, ibm.com. Large enterprises simulate upgrades in a sandbox, deploy configurations confidently, and feed post-deployment telemetry back into the model, creating a virtuous optimisation cycle across planning, implementation, and operations.

API-Based Network-as-Code Monetisation Needs Real-Time Analytics

Programmable interfaces allow service providers to expose bandwidth, latency, and security features as on-demand services. Real-time analytics validate service-level agreements, detect malicious use, and inform dynamic pricing. Telecom carriers moving beyond connectivity now embed usage telemetry in product catalogues, enabling rapid micro-service launches that expand average revenue per user.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial costs and uncertain RoI | -2.1% | Emerging Markets, Global | Short term (≤ 2 years) |

| Data-privacy and regulatory constraints | -1.8% | Europe, North America, APAC | Medium term (2-4 years) |

| AI/ML Ops skills gap | -1.5% | Emerging Markets, Global | Medium term (2-4 years) |

| Vendor lock-in through proprietary protocols | -1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Costs and Uncertain Return on Investment

Comprehensive deployments require software licences, telemetry-ready hardware, systems integration, and staff training. Quantifying financial returns linked to reduced outages or improved customer experience remains challenging, particularly for small and mid-sized organisations. Subscription-based cloud delivery eases capital burdens, yet budget pressures in emerging economies still slow adoption.

Data-Privacy and Regulatory Constraints

Frameworks such as GDPR impose strict rules on data usage, storage, and transfer. Networks carrying personal or sensitive information must anonymise or localise traffic records, which complicates global analytics architectures. Vendors are responding with fine-grained data-masking, role-based access, and in-region processing options, yet shifting regulatory requirements continue to add compliance overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Adoption Accelerates Transformation

Cloud deployments are set to expand at a 23.4% CAGR, outpacing the overall network analytics market. The move is driven by elastic scalability, pay-as-you-go economics, and easier access for distributed teams. Despite that momentum, on-premise installations retained 55.20% revenue in 2025 due to heightened security and sovereignty needs. Hybrid architectures have gained favour as organisations bridge legacy investments with future agility, a trend reinforced by financial institutions, where 91% have already begun their cloud modernisation journeys.

Hybrid operating patterns illustrate a pragmatic view: workloads with stringent data-control requirements remain on-premise, while bursty analytic tasks shift to public clouds. This duality supports cost optimisation without sacrificing governance. Analysts note that 30% of enterprise workloads now sit in public clouds, with analytics and DevOps leading migrations. Vendors have responded by delivering containerised collectors, SaaS dashboards, and unified policy engines that span private and public domains. Continuous integration pipelines further embed analytics into daily operations, compressing development cycles.

By Component: Services Drive Long-Term Value Creation

Solutions dominated 2025 revenue with 62.40%, yet services are forecast to grow 22.6% annually as organisations seek specialised expertise. Consulting and integration engagements align analytics architectures with business objectives, while managed services offload daily tuning and rule-maintenance. The services wave mirrors broader IT outsourcing patterns; the managed service provider segment is projected to reach USD 350 billion in 2024 and top USD 1 trillion by 2033.

Service partners increasingly deliver AI-driven advisory offerings that contextualise performance insights into business outcomes. Enterprises adopting such models have reported 20-30% cost savings and up to 25% productivity gains. To meet demand, vendors package runbooks, pre-trained models, and remote SOC capabilities, shortening time to value and mitigating the AI skills gap. This evolution cements services as a cornerstone of the network analytics market, unlocking recurring revenue and deeper client relationships.

By Application: Security Concerns Drive Analytics Adoption

Security and anomaly-detection platforms are projected to grow at a 23.0% CAGR, eclipsing performance management and fault management ambitions. The data-breach cost for professional-services firms is prompting boards to scrutinise protective controls. AI-powered analytics correlates trillions of packets, logs, and flow records to surface subtle attack patterns in near real time. Consequently, many organisations now deploy a unified analytics fabric that stitches together security, performance, and customer-experience insights.

Although performance management held 29.30% share in 2025, its role is evolving toward root-cause analysis that spans hybrid and multi-cloud estates. Smart-routing engines and traffic-optimisation algorithms use live telemetry to reroute flows away from congestion or malicious activity, preserving user experience while lowering bandwidth costs. Customer-experience analytics further ties technical metrics to sentiment, enabling proactive service credits and retention campaigns.

By End User: Cloud Providers Reshape Analytics Landscape

Communication service providers led with 47.20% of 2025 revenue, yet cloud providers form the fastest-growing cohort at a 22.3% CAGR. Hyperscalers apply analytics to balance compute loads, detect east-west threat vectors, and assure inter-region connectivity. Their innovation cadence is pressuring traditional telcos to adopt similar real-time intelligence or risk commoditisation. Enterprises in banking, healthcare, and retail also accelerate uptake, aligning network visibility with regulatory compliance and omnichannel experiences.

The Cloud Performance Report comparing AWS, Microsoft Azure, and Google Cloud underscores rising demand for vendor-neutral telemetry that benchmarks availability and latency across regions. Organisations integrate such comparative data with internal flows to determine workload placement and negotiate service-level objectives. As cloud providers mainstream network analytics, they also embed open APIs that foster an ecosystem of value-added partners.

Geography Analysis

North America retained 37.60% revenue share in 2025, supported by early adoption, sizeable IT budgets, and an advanced supplier ecosystem. United States financial-services and healthcare organisations deploy AI-infused analytics to satisfy stringent uptime and privacy mandates. Canadian carriers use analytics to optimise nationwide 5G roll-outs and manage rural-coverage obligations. Regulatory clarity and abundant talent expedite experimentation with predictive automation, keeping the region at the forefront of innovation.

Asia-Pacific is the fastest-growing region with a 22.7% CAGR to 2031. China and India fund large-scale 5G, smart-city, and industrial-IoT projects that demand granular visibility into multi-vendor environments. Japan and South Korea integrate AI with network monitoring to support autonomous-vehicle trials and factory automation, while Australia leverages analytics to protect critical infrastructure from cyber threats.

Europe advances amid stringent regulations and heightened security awareness. United Kingdom and Germany lead adoption in financial services and manufacturing, seeking GDPR-compliant insights across hybrid architectures. France and Italy augment telecom deployments to maintain customer satisfaction in competitive mobile markets. Energy and utilities operators in Northern and Eastern Europe deploy analytics to detect anomalies in smart-grid telemetry. Vendors thriving in the region emphasise data-sovereignty controls, granular user-access policies, and automated compliance reporting.

Regulatory Landscape

Network analytics deployments are increasingly shaped by cybersecurity and supply-chain rules that raise expectations for monitoring, logging, and reporting. In the European Union, the NIS2 Directive (Directive (EU) 2022/2555) increases incident-preparedness expectations for essential and important entities, and Commission Implementing Regulation (EU) 2024/2690 tightens technical requirements around logging of network traffic and authentication events. As a result, providers face higher pressure to run auditable telemetry pipelines with controlled access to analytics outputs.

In the United States, the Federal Communications Commission (FCC) has reinforced telecom supply-chain and cybersecurity requirements, including actions tied to the FCC Covered List. In May 2026, the FCC adopted a Notice of Proposed Rulemaking to restrict entities identified on the Covered List from providing domestic interstate telecommunications services, and it also adopted requirements for submarine cable network operators to implement cybersecurity risk management plans. These measures increase compliance scrutiny on network data handling, vendor provenance, and security controls embedded in analytics platforms used by carriers and critical infrastructure operators.

Value Chain Analysis

The network analytics value chain begins with telemetry generation across physical and virtual networks (RAN, core, transport, SD-WAN, SASE, and cloud networking), then moves into collection and normalization using agents, collectors, flow logs, packet capture, and APIs. Network intelligence platforms subsequently enrich and analyze the data through AI/ML correlation, anomaly detection, and root cause analysis, and feed results into execution layers such as orchestration, ticketing, and policy systems, with outputs delivered through dashboards, APIs, and closed-loop automation. Infrastructure vendors (for example, Cisco and Nokia) and platform vendors supply core software, while hyperscalers (AWS, Google Cloud) provide scalable compute and storage for cloud-delivered analytics.

Downstream, integration, operations, and lifecycle optimization drive a substantial services layer, with professional services and managed service providers (such as Accenture and Cognizant) packaging network observability, automation, and multi-cloud operations into ongoing engagements. Partnerships increasingly support domain expertise and automation, including Nokia launching Autonomous Network Fabric (June 2025) to apply telco-trained AI models across observability and remediation, and Mobileum and NOHOLD announcing a strategic AI alliance (September 2025) focused on AI-powered automation and telecom data monetization. Bottlenecks across the chain include security concerns in disaggregated environments, persistent skills gaps in AI/ML operations for network data pipelines, and capex/opex constraints that push buyers toward SaaS and managed models.

Competitive Landscape

The network analytics market shows moderate concentration. Cisco, IBM, and Juniper Networks combine broad portfolios with global support, reinforcing incumbent positions. Each has embedded machine-learning engines and intent-based orchestration to differentiate from commoditised packet capture tools. Specialised firms such as SAS Institute and Sandvine compete through depth in high-speed flow analytics or subscriber-aware use cases, pushing larger rivals to accelerate innovation.

Strategic acquisitions illustrate the race toward integrated stacks. IBM’s purchase of HashiCorp widens its hybrid-cloud reach, while Cisco’s addition of ThousandEyes extends visibility to the public internet. Hewlett Packard Enterprise bolstered its Aruba networking line with high-capacity switches for AI workloads[4]David Hughes, “Delivering AI-Ready Switching Fabric,” Hewlett Packard Enterprise, hpe.com. Vendor roadmaps emphasise ease of use, guided remediation, and cross-domain correlation to serve non-specialist operators.

White-space growth lies in quantum-safe encryption analytics, zero-trust policy validation, and vertical-specific solutions that embed domain ontologies. Vendors forging partnerships with cloud hyperscalers and security-information platforms gain early-mover advantage. Competitive intensity is likely to increase as open-source collectors and telemetry standards erode proprietary moats, propelling vendors toward value-added data science and outcome-based pricing.

Network Analytics Industry Leaders

Accenture PLC

Cisco Systems Inc.

Hewlett Packard Enterprise Company

IBM Corporation

Juniper Networks

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standardized interoperability in 5G analytics creates whitespace for vendors that can productize multi-vendor data collection and closed-loop assurance across RAN, core, and transport. In February 2026, 3GPP updated TS 129 552 (Release 19) with detailed procedures for network data analytics signaling flows and data collection across multiple 5G network functions, and in March 2026, 3GPP updated TS 129 575 (Release 17) to formalize the Analytics Data Repository Function (ADRF) for standardized real-time data injection, subscription-based collection, and batch retrieval. These specifications support commercial opportunities for analytics platforms that map to standardized interfaces while still differentiating via AI-driven correlation, policy validation, and domain-specific use cases for CSPs and large enterprises.

Operationalization is a key opportunity area. Many organizations already generate high-resolution telemetry, but gaps between analytics outputs and execution systems (controllers, orchestrators, and ITSM) limit autonomous actions in production networks. This drives demand for streaming data pipelines and near-real-time scoring architectures, including Kafka and Flink based stacks cited by industry practitioners in 2026, to reduce time-to-insight and integrate with network engineering workflows. Vendors and service partners that package data quality controls, explainable outputs, and pre-built integrations for hybrid and multi-cloud environments can target budgets that still stall at monitoring-only deployments, particularly in security and anomaly detection where cross-domain correlation across enterprise, internet, and cloud paths remains a common visibility gap.

Recent Industry Developments

- February 2026: Accenture acquired an advanced AI technology platform from Avanseus to enhance its cognitive network platform for telecommunications. The acquisition expands Accenture's ability to deliver agentic-AI assisted network operations programs that blend analytics with automation. It also increases competitive pressure on pure-play analytics vendors as system integrators embed proprietary AI capabilities into managed and professional services offerings.

- December 2025: Hewlett Packard Enterprise expanded its AI-native networking portfolio by integrating telemetry from HPE Aruba Networking and HPE Juniper Networking Apstra into a single hybrid command center through HPE OpsRamp. Unifying these data sources strengthens HPE's position in end-to-end observability and accelerates consolidation of analytics and operations tooling under one control plane. The move raises the bar for cross-domain correlation across campus, data center, and hybrid cloud networks.

- July 2025: Hewlett Packard Enterprise closed its all-cash acquisition of Juniper Networks, following a settlement with the U.S. Department of Justice that required divestiture of HPE's Instant On business. The transaction reshapes competitive dynamics by combining Aruba and Juniper portfolios across switching, routing, and AI-driven network operations. It also concentrates analytics and automation assets into a larger full-stack networking vendor, influencing procurement choices for CSP and enterprise network analytics deployments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the network analytics market covers software and related services that capture and analyze network data (such as flows, packets, and telemetry) to improve performance, plan capacity, and identify abnormal behavior across enterprise, telecom, and cloud networks.

Scope exclusions: We exclude custom in-house tools built only for internal use and stand-alone hardware probes when they are sold without an analytics software subscription.

Segmentation Overview

- By Deployment Model

- On-premise

- Cloud

- Hybrid

- By Component

- Solutions

- Network intelligence platforms

- Performance management

- Security analytics

- Root-cause and anomaly detection

- Traffic optimisation

- Services

- Professional services

- Managed services

- Solutions

- By Application

- Performance management

- Fault management

- Customer experience management

- Security and anomaly detection

- Smart routing and traffic optimisation

- By End User

- Communication service providers

- Telecom providers

- Internet service providers

- Satellite communication providers

- Cable network providers

- Cloud service providers

- Enterprises

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- Retail and e-commerce

- Manufacturing

- Government and public sector

- Communication service providers

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning definitions and the revenue boundary across software licenses, subscriptions, and managed services. We used public references such as FCC broadband and telecom datasets, ITU indicators, NIST cybersecurity guidance, ENISA threat reports, and OECD digital economy statistics to understand traffic growth, security pressure, and enterprise connectivity trends.

Next, we reviewed vendor filings and investor decks, product documentation, and reputable press to map typical buying patterns, including how analytics shifted from on-premise deployments to cloud-based offerings. Patent databases were checked to spot areas where investment is rising (for example, telemetry analytics and automation), and a news and financials subscription helped track major contracts, partnerships, and pricing signals. These examples are not exhaustive, and other public sources were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary inputs came from interviews and surveys with network operations leaders, security teams, managed service providers, and product owners who see budgets and deployment decisions. For a global market like this, coverage was spread across Americas, EMEA, and APAC to test differences in cloud maturity, telecom investment cycles, and the level of compliance pressure. Respondent input was used to refine average contract values, typical module adoption, and how buyers distinguish analytics from adjacent monitoring tools.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 39% |

| Mid tier: 58% | Functional/Unit leaders: 31% | EMEA: 35% |

| Smaller Players: 14% | Managers: 55% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up checks, where top-down demand pools were reconstructed from telecom and enterprise network spending signals and then filtered by the realistic share allocated to analytics software and related services. The totals were cross-checked using selective bottom-up approximations like sampled vendor revenue splits, channel checks with service providers, and ASP times volume logic for typical deployments.

Key inputs that shaped the model included enterprise and operator traffic growth, the rollout pace of 5G and fiber, cloud workload migration, the rate of telemetry adoption, and the frequency of network security incidents that trigger analytics upgrades. Where direct revenue splits were not consistently visible, gaps were handled through proxy ratios validated in interviews (for example, analytics attach rates to monitoring deployments) and then stress-tested across regions.

Forecasts were developed using scenario analysis supported by trend lines from the above indicators, and scenarios were refined after checking what practitioners expect for budget growth, cloud shift, and consolidation cycles over the next few years.

Data Validation & Update Cycle

Outputs were checked against independent signals such as regional IT spending direction, telecom capex cycles, and the expected pace of cloud adoption, and then the largest variances were investigated before sign-off. When a number looked off, the model was re-run with adjusted drivers, and the assumption was re-tested through follow-up expert calls.

Each report is refreshed annually, and interim updates are made when material events occur, such as major product launches, regulation shifts, or sharp changes in operator investment. Before delivery, a final analyst review is completed so clients receive an updated view aligned to the latest available information.

Mordor Intelligence's Network Analytics Market Estimate Compared With Other Published Estimates

Published market sizes for network analytics can vary even when they look like they cover the same topic, because the scope line is drawn differently and the same revenue is sometimes counted in more than one bucket. Differences also come from the base year chosen, how currency conversion timing is handled, and whether services are treated as part of the market or left out.

The main gap comes from whether stand-alone network monitoring and hardware-only probes are bundled into analytics totals, where Mordor Intelligence counts network analytics only when software and related services deliver packet, flow, or telemetry-based analysis rather than simple monitoring visibility.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.97 B (2026) | |

| Global Advisory A | USD 3.32 B (2025) | Uses a 2025 base and appears to apply a narrower monetization view, which can undercount services revenue and delay the recognition of cloud subscription expansion. |

| Industry Publisher B | USD 2.89 B (2022) | Anchors the model on an older base year and a longer forecast horizon, and the public summary does not clearly separate pure monitoring suites from analytics, which can shift the starting point materially. |

Taken together, the spread mainly reflects scope choices and timing, not just arithmetic. By tying the estimate to observable demand indicators like traffic growth, cloud migration, and telecom investment cycles, the market total stays traceable to repeatable steps that can be rechecked as conditions change.

Key Questions Answered in the Report

What is the current value of the network analytics market?

The market stands at USD 4.97 billion in 2026 and is projected to grow to USD 13.03 billion by 2031.

Which region leads revenue in network analytics solutions?

North America leads with 37.60% revenue share in 2025, propelled by early adoption and large-scale 5G investments.

Why are cloud service providers the fastest-growing end-user segment?

Their 22.3% CAGR reflects the need to optimise complex, distributed infrastructures and ensure high-performance service delivery.

How does AI improve network analytics outcomes?

AI enables predictive maintenance, automated remediation, and security anomaly detection, cutting resolution time by up to 32% in some deployments.

What deployment model is growing the fastest?

Cloud deployments are expanding at a 23.4% CAGR due to scalability, lower upfront costs, and rapid service roll-out.

Page last updated on: