Network Bandwidth Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

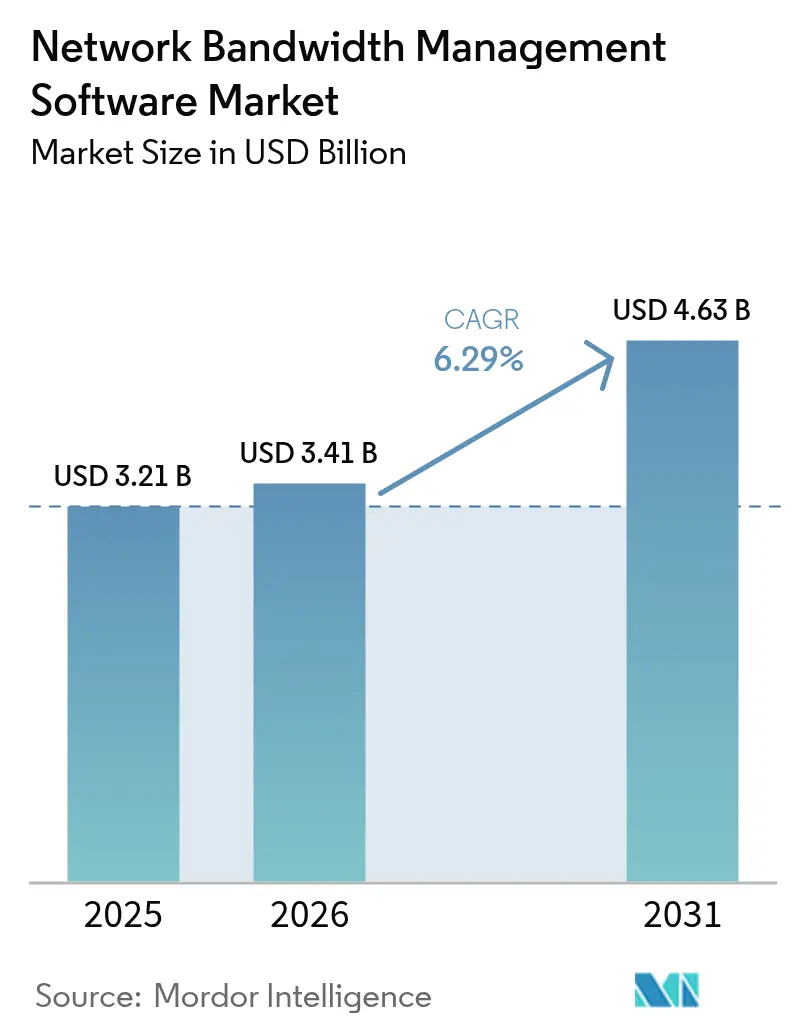

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.63 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

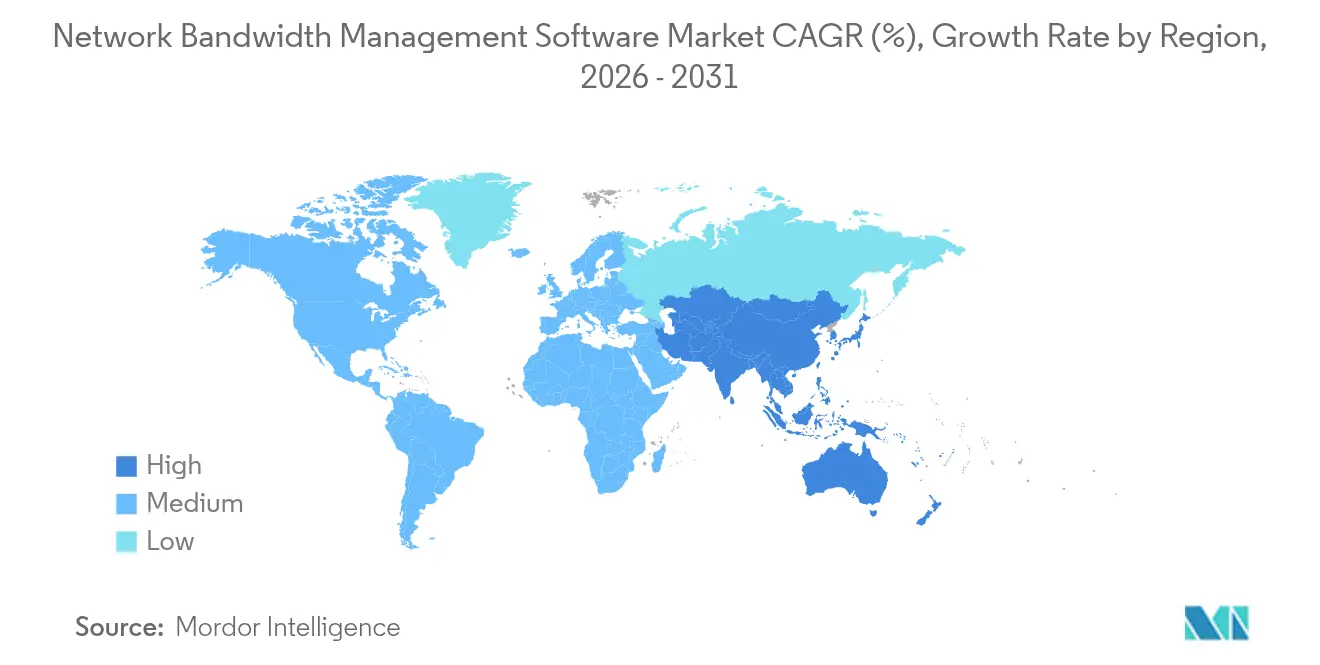

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Network Bandwidth Management Software Market Analysis by Mordor Intelligence

The Network Bandwidth Management Software market size is expected to grow from USD 3.21 billion in 2025 to USD 3.41 billion in 2026 and is forecast to reach USD 4.63 billion by 2031 at 6.29% CAGR over 2026-2031. The market’s expansion is underpinned by enterprises shifting from reactive monitoring to proactive, AI-enabled bandwidth orchestration that can manage soaring data flows from IoT devices, edge workloads, and latency-sensitive applications. Cloud deployment keeps momentum because centrally managed platforms align with hybrid work models, while SD-WAN integration continues to blur the boundaries between connectivity and security. Private 5G and Wi-Fi 7 upgrades spur demand for deterministic bandwidth allocation, and large-scale AI infrastructure investments ensure continued emphasis on traffic visibility, performance assurance, and compliance.

Key Report Takeaways

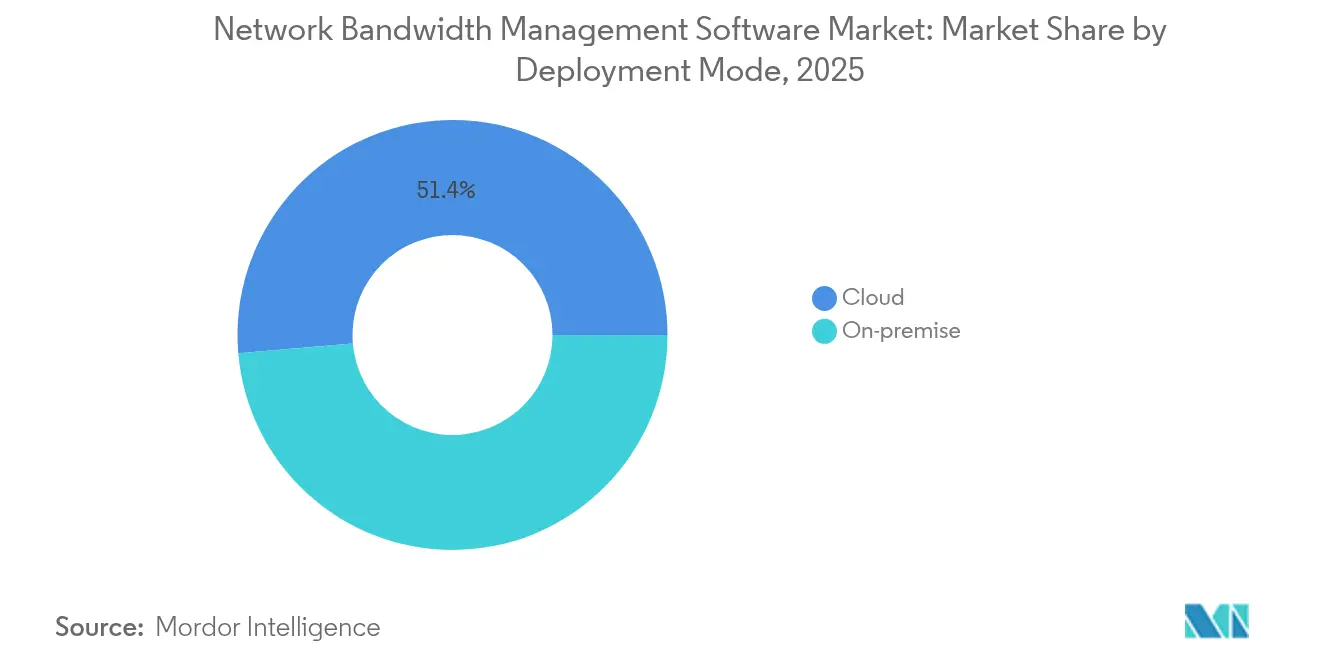

- By deployment model, cloud accounted for 51.35% of the Network Bandwidth Management Software market share in 2025, and cloud set to post a 8.14% CAGR

- By enterprise size, SMEs are set to post a 6.48% CAGR through 2031, eclipsing the growth of large enterprises. While large enterprises account for 63.05% in 2025

- By solution type, SD-WAN bandwidth management captured 26.42% of the Network Bandwidth Management Software market size in 2025 and set a CAGR of 6.22%.

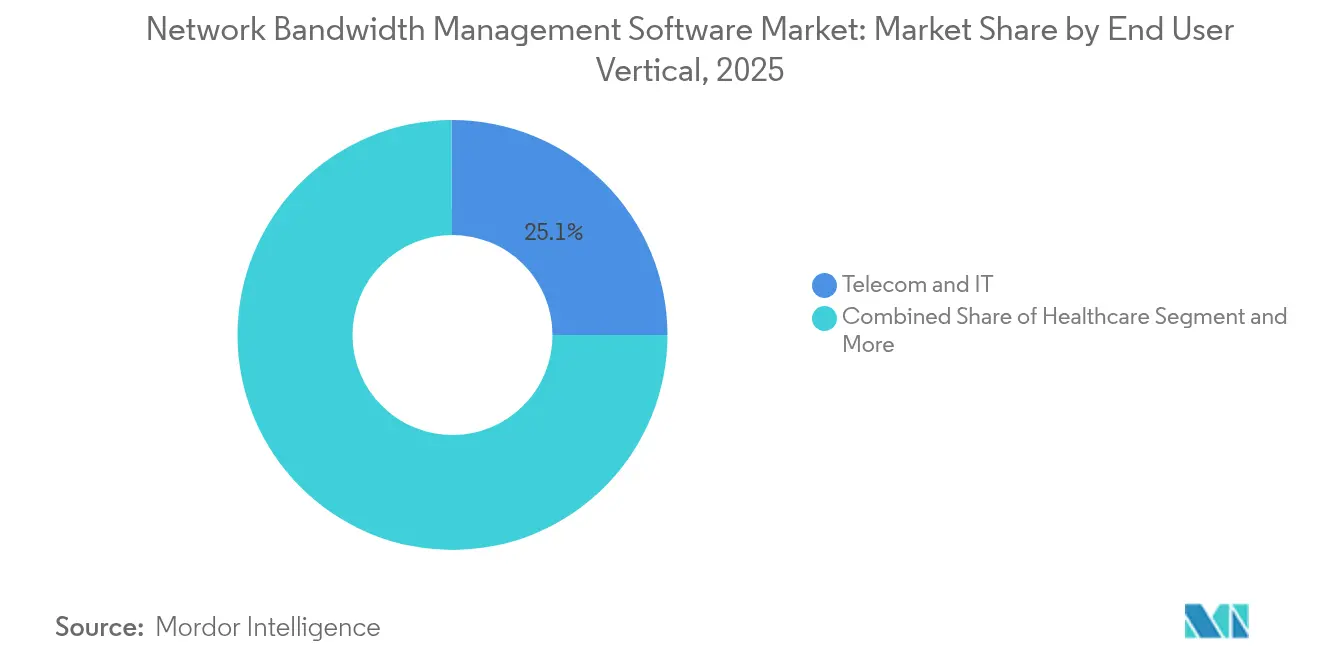

- By end user, Telecom and IT captured 25.08% of the Network Bandwidth Management Software market size in 2025, and Healthcare is expected to register a CAGR of 6.85%

- By network type, Wired captured 64.85 % of the Network Bandwidth Management Software market size in 2025, and wireless is expected to register a CAGR of 8.05%

- By geography, North America captured 34.05% of the Network Bandwidth Management Software market size in 2025, and Asia-Pacific is expected to register a CAGR of 7.05%

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Network Bandwidth Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of IoT endpoints and private 5G enterprise networks | +1.2% | Global, Asia-Pacific leading | Medium term (2-4 years) |

| High-speed internet demand and SD-WAN adoption | +0.8% | North America, Europe, growing Asia-Pacific | Short term (≤2 years) |

| Proliferation of data-rich applications | +0.6% | Global, developed markets | Medium term (2-4 years) |

| Edge AI workloads needing deterministic bandwidth | +0.4% | North America, Europe, select Asia-Pacific | Long term (≥4 years) |

| 5G network slicing for per-slice orchestration | +0.3% | Asia-Pacific, North America, parts of Europe | Long term (≥4 years) |

| Shift toward AIOps with embedded analytics | +0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosion of IoT Endpoints and Private 5G Enterprise Networks

Enterprise IoT rollouts add thousands of sensors across factories, offices, and logistics hubs, generating unpredictable traffic that legacy best-effort routing cannot handle. Private 5G further intensifies the challenge because ultra-low-latency applications require strict bandwidth guarantees. A live deployment supporting 40,000 first responders for specialized services illustrates how mission-critical users depend on granular bandwidth control. Enterprises, therefore, select AI-driven tools that classify traffic, forecast consumption, and reallocate resources across heterogeneous links in real time.

Growing Need for High-Speed Internet and SD-WAN Adoption

SD-WAN introduces application-aware routing that spans MPLS, broadband, and 5G, turning bandwidth management from a reporting task into a business value lever. Organizations adopting SD-WAN have recorded 70% lower hardware spend and 74% higher operational efficiency by unifying transport links under a single policy engine.[1]Zscaler ,"Bandwidth Control - 100% Cloud-delivered,"zscaler.com As a result, bandwidth software must optimize for user experience and business priority rather than raw throughput, embedding analytics to safeguard revenue-generating applications.

Proliferation of Data-Rich Apps (4K/8K Video, AR/VR, AI Analytics)

High-definition video and immersive reality place asymmetric loads on corporate backbones; 4K streaming alone consumes 25 Mbps per user while AR/VR requires low-latency stability. Hospitals now budget up to 1 Gbps to run electronic records, telehealth, and real-time monitoring simultaneously.[2]Elisity,"HIPAA Security Rule Changes 2025: New Network Segmentation Requirements and Implementation Guidelines," elisity.com AI model training generates traffic bursts during compute-intensive cycles, so administrators need predictive capacity planning to prevent bottlenecks.

Edge AI Workloads Requiring Deterministic Bandwidth

Manufacturing lines, autonomous vehicles, and site analytics increasingly execute inference at the edge, where every millisecond matters. Unlike cloud AI, these tasks tolerate neither jitter nor congestion. Multi-billion-dollar investments in distributed AI infrastructure amplify the need for bandwidth managers that synchronize network, compute, and storage while respecting latency budgets measured in microseconds.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Freemium/open-source traffic tools | -0.7% | Global, cost-sensitive markets | Short term (≤2 years) |

| Integration complexity with legacy infrastructure | -0.5% | North America, Europe | Medium term (2-4 years) |

| Privacy regulations limiting deep packet inspection | -0.3% | Europe, expanding globally | Long term (≥4 years) |

| Zero-trust focus diverting budgets | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Freemium/Open-Source Traffic Tools Lower Entry Barriers

Robust free tools such as Zabbix and LibreQoS give firms basic visibility without license fees, delaying conversions to commercial platforms. Vendors counter by offering starter tiers that include core sensors at no cost, pushing differentiation toward AI insights, policy automation, and premium support.[3]Adrem Software,"Bandwidth Monitoring with NetCrunch,"adremsoft.com This commoditizes monitoring while raising the bar for orchestration features.

Integration Complexity with Legacy On-Premise Infrastructure

Decades-old SNMP collectors, proprietary protocols, and customized workflows force lengthy professional-service engagements before full deployment. Regulated industries add compliance testing cycles that stretch projects from months to years, inflating total cost and discouraging upgrades until a critical refresh.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Adoption Outpaces Legacy Approaches

Cloud options commanded 51.35% of total spending in 2025, illustrating how organizations favor scalable control planes accessed from anywhere. The segment is forecast to grow at 8.14% CAGR to 2031, far faster than on-premise deployments. Enterprises cite 40% lower total ownership through the elimination of hardware refreshes and simplified patching schedules. On-premise systems remain in place where sovereignty or ultra-low-latency processing dictates local control. Hybrid architectures combine edge gateways for sensitive data with cloud analytics hubs for broad visibility.

Lower management overhead sits at the heart of migration economics. Administrators can roll out policy changes across hundreds of sites without traveling, while multi-tenant instances enable MSPs to serve SMEs lacking in-house expertise. The Network Bandwidth Management Software market, therefore, tilts steadily toward SaaS models, although vendors still offer appliance images for air-gapped environments. This dual delivery strategy protects existing revenue while paving a path to subscription growth.

By Enterprise Size: SMEs Narrow the Capability Gap

Large enterprises controlled 63.05% of 2025 revenue because complex topologies and compliance demands justified investment in advanced suites. Yet SMEs are on track for a 6.48% CAGR through 2031 as cloud-native pricing aligns with operating budgets. Managed services bundles allow smaller firms to outsource monitoring, reporting, and policy enforcement, accelerating adoption without adding headcount.

Volume growth among SMEs pushes vendors to streamline onboarding through auto-discovery, template-based policies, and guided remediation. At the same time, large enterprises continue to seek customizable modules that integrate with ITSM and SIEM stacks. This bifurcated roadmap anchors the Network Bandwidth Management Software market, giving suppliers multiple paths to expansion while maintaining clear account segmentation.

By Solution Type: SD-WAN Integration Sets the Pace

SD-WAN bandwidth management held a 26.42% share in 2025 as firms converged routing, optimization, and security. The sub-segment is projected to clock a 6.22% CAGR through 2031. QoS and shaping tools sustain relevance where voice or video quality remains paramount, while WAN optimization persists in branch scenarios with limited backhaul capacity.

Encrypted Traffic Intelligence capabilities emerge within policy-based modules to maintain application visibility amid pervasive TLS-encrypted flows. Bandwidth monitoring continues to underpin every deployment, acting as the telemetry feed for analytics engines. Collectively, these layers reinforce the Network Bandwidth Management Software market by providing both tactical metrics and strategic insights.

By End-User Vertical: Healthcare Surges on Telemedicine and IoT Devices

Telecommunications and IT service providers generated 25.08% of 2025 sales by managing massive multitenant backbones. Healthcare, however, is forecast to rise at 6.85% CAGR as hospitals expand telehealth portals, connect imaging centers, and deploy remote patient monitors that need deterministic throughput. BFSI, retail, education, and government use similar capabilities for branch rollouts, although growth curves are flatter due to earlier deployment waves.

Industry-specific regulations catalyze upgrades. Proposed HIPAA amendments require microsegmentation to isolate medical devices, pushing procurement of platforms that combine bandwidth analytics with policy enforcement. Comparable rules in finance and utilities further contribute to demand, ensuring the Network Bandwidth Management Software market remains diversified across verticals.

By Network Type: Wireless Gains Momentum but Wired Remains Backbone

Wired topologies retained 64.85% of spending in 2025 since data center fabrics and campus cores still anchor enterprise traffic. Wireless networks are projected to grow at 8.05% CAGR through 2031, propelled by Wi-Fi 7 access points and private 5G slices. The influx of mobile endpoints calls for unified bandwidth views covering both cabling and spectrum. Vendors that present wired and wireless metrics in a single dashboard appeal to organizations seeking operational simplicity.

As throughput ceilings climb beyond 40 Gbps on Wi-Fi 7, contention shifts from capacity to management. Intelligent scheduling, airtime fairness, and real-time interference mitigation become critical features. This evolution gives bandwidth software a new role in RF optimization, broadening addressable opportunities within the Network Bandwidth Management Software market.

Geography Analysis

North America generated 34.05% of 2025 revenue, buoyed by mature IT budgets, tight compliance regimes, and ongoing investment in AI-enabled data centers. Hyperscalers’ multibillion-dollar builds translate into sustained demand for traffic visibility, capacity planning, and SLA assurance. Regional healthcare and finance regulations add momentum because they mandate continuous monitoring and segmented architectures. Collectively, these forces cement North America as the largest slice of the Network Bandwidth Management Software market.

Asia–Pacific is poised for the fastest expansion with a 7.05% CAGR to 2031. Governments prioritize digital infrastructure, 5G rollouts advance quickly, and enterprises leapfrog legacy circuit models by adopting cloud and SD-WAN concurrently. Wide variance in network maturity encourages flexible licensing ranging from pay-as-you-grow SKUs for emerging economies to full-stack suites for advanced markets such as Japan and South Korea. Vendors that localize language support and compliance templates stand to capture outsized share.

Regulatory Landscape

The regulatory environment is reinforcing the move toward all-IP networks and higher-capacity connectivity, which increases the need for policy-based visibility and control. In the United States, the FCC advanced actions in 2026 to reduce barriers tied to legacy network transitions and to modernize requirements affecting network improvements and service changes, shaping how operators and large enterprises plan upgrades and manage service assurance across hybrid environments.

Standards and public-sector mandates are also influencing network architecture, and bandwidth management requirements by extension. China implemented GB/T 46464-2025 for IPv6 deployment requirements in national e-government networks in early 2026. International standards bodies such as ITU-T continued publishing recommendations relevant to orchestration and AI-enabled network optimization, including work on service function chaining and AI-driven quality auto-optimization. In Canada, the CRTC issued a 2026 decision framework allowing certain carrier-led blocking methods for cybersecurity measures, subject to accuracy and complaint-resolution requirements, which raises the bar for transparency and control mechanisms in traffic policies.

Competitive Landscape

The market remains moderately fragmented. Incumbents such as Cisco, IBM, and NetScout leverage long-standing channel ecosystems and full-stack offerings. Challenger brands focus on cloud-first architectures, usage-based billing, and API-centric integrations. The widening skills gap in enterprise IT operations further favors solutions that ship with AI-driven root-cause analysis and guided remediation.

Mergers and acquisitions accelerate scale and portfolio breadth. HPE closed a USD 14 billion deal for Juniper Networks in July 2025, combining edge compute with AI-powered switching to court enterprises standardizing on integrated infrastructure. Nokia’s planned USD 2.3 billion purchase of Infinera expands optical depth essential for AI data center interconnects. Arista added VeloCloud to enhance SD-WAN capabilities and secure incremental enterprise share. These moves underscore confidence that integrated networking plus AI analytics will dictate long-term leadership in the Network Bandwidth Management Software market.

Network Bandwidth Management Software Industry Leaders

-

Cisco Systems Inc.

-

IBM Corporation

-

NetScout Systems Inc.

-

SolarWinds Corporation

-

Broadcom Inc. (CA Technologies)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise operations are shifting from reactive monitoring toward autonomous, AI-driven NetOps, creating whitespace for bandwidth management that brings telemetry together with intent-based policy and automated remediation across SD-WAN, Wi-Fi, private 5G, and cloud interconnects. Recent product moves reinforce this direction. In May 2026, HPE announced self-driving network capabilities for HPE Mist and HPE Aruba Central. In June 2026, Cisco unveiled Cisco Cloud Control to unify management and defense of critical IT infrastructure. These launches raise the bar for embedded AIOps, cross-domain context, and workflow automation, pushing bandwidth management vendors to integrate more tightly with observability and security operations instead of focusing only on standalone reporting.

Operator and vertical-specific use cases are also expanding beyond traditional enterprise WAN monitoring. Vendor-agnostic optimization approaches are gaining attention among broadband providers seeking to extract more usable capacity from installed DOCSIS infrastructure, which supports demand for software that can quantify congestion, enforce QoE policies, and coordinate traffic engineering across multi-vendor networks. Specialized connectivity environments are becoming more software-orchestrated as well. ST Engineering iDirects launched Intuition Foresight for multi-vendor satellite networks with global bandwidth management features in March 2026, and NETGEAR released Insight 10.0 in June 2026, adding AI-driven management aimed at SMEs and MSPs, widening the addressable base for cloud-delivered bandwidth governance.

Recent Industry Developments

- July 2026: DriveNets expanded its AI networking portfolio with high-capacity AI fabric platforms (2600SL and 2601S) powered by Broadcom Tomahawk 6 (TH6) ASICs, targeting very large-scale bandwidth demands in AI clusters. The update underscores how higher-throughput fabrics are driving operators and enterprises to adopt tighter traffic visibility and control to prevent congestion and manage east-west traffic at scale.

- July 2025: HPE finalized its USD 14 billion acquisition of Juniper Networks, combining enterprise networking assets with AI-driven operations capabilities across edge-to-cloud portfolios. The deal strengthened integrated networking-plus-AIOps roadmaps that influence how bandwidth management features get bundled into broader network operations platforms.

- June 2024: SolarWinds enhanced its network monitoring portfolio with updates aimed at improving visibility and troubleshooting across hybrid environments. The release supported the ongoing shift toward consolidated dashboards that tie bandwidth utilization, application performance, and remediation workflows into a single operational view.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers software used to monitor, control, and optimize network traffic so available bandwidth is allocated to the right users and applications, and service quality stays consistent across wired and wireless networks.

Scope exclusions: Excludes pure connectivity services (internet access, carrier transport) and general network hardware when these are sold without a bandwidth management software license.

Segmentation Overview

-

By Deployment Model

- On-Premise

- Cloud

-

By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

-

By Solution Type

- Bandwidth Monitoring and Reporting

- Traffic Shaping / QoS Control

- WAN / Internet Link Optimization

- SD-WAN Bandwidth Management

- Others (Policy-based, DPI, etc.)

-

By End-User Vertical

- Telecommunication and IT

- BFSI

- Healthcare

- Retail and E-commerce

- Education

- Government and Defense

- Manufacturing

- Others

-

By Network Type

- Wired Networks

- Wireless and Wi-Fi Networks

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Netherlands

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Israel

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base and to avoid building the model on assumptions that cannot be checked. We reviewed public statistics and reference points relevant to enterprise networking demand, such as IT and telecom indicators from sources like the International Telecommunication Union (ITU), the US FCC, Eurostat, and the World Bank.

To anchor adoption logic, we also used sources such as NIST publications, IETF RFCs, and credible university and peer-reviewed networking research that explains traffic engineering patterns, QoS policy methods, and congestion behavior. Company filings, annual reports, and investor presentations were read to map product scope and revenue language, and a paid subscription for company financials and news was used to track corporate actions. These sources are not exhaustive, and many other public and paid references were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what desk research cannot fully confirm, especially how buyers define a bandwidth management tool versus adjacent network software, and how pricing moves with user counts, sites, and throughput. We spoke with a mix of suppliers, channel partners, and enterprise IT and network teams across APAC, EMEA, and the Americas so the final assumptions reflect different purchasing cycles and network maturity levels.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 44% |

| Mid tier: 47% | Functional/Unit leaders: 37% | EMEA: 37% |

| Smaller Players: 22% | Managers: 50% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the addressable demand pool is reconstructed using enterprise network spend signals and then filtered by where bandwidth control and traffic visibility are actively deployed. Inputs that help keep the logic grounded include growth in IP traffic, enterprise cloud migration intensity, the share of sites adopting SD-WAN, Wi-Fi upgrades (including Wi-Fi 6 and Wi-Fi 7 readiness), and the mix shift toward real-time traffic such as video collaboration and unified communications.

Those totals are then checked with selective bottom-up approximations, including sampled license pricing ranges, typical contract terms, and channel feedback on volumes by enterprise size, followed by adjustments when gaps show up. For forecasting, we used scenario analysis supported by expert views on how remote work steadiness, edge computing rollout, and security policy tightening affect adoption and renewal rates. Where direct volume proxies are thin, conservative penetration ranges are applied and later refined through follow-up discussions.

Data Validation & Update Cycle

Outputs are validated through multiple checks so individual assumptions do not quietly drive the whole number. We compare modeled revenue with independent signals like disclosed software revenue direction in filings, hiring and product activity trends, and regional IT spending indicators, and then outliers are reviewed before sign-off.

When a variance is material, we re-check definitions, re-contact respondents, and re-run currency and inflation handling so the series stays consistent year to year. Reports are refreshed annually, and interim updates are made when large events occur such as major acquisitions, pricing shifts, or regulation that changes network monitoring requirements. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Network Bandwidth Management Software Market Size Measured Against Other Published Estimates

Published market values for bandwidth management software can look different because each source draws the line around what counts as bandwidth management, which year is treated as the base, and how fast cloud deployment and pricing are assumed to shift.

Standalone network performance monitoring suites sit outside Mordor Intelligence's scope unless a clearly priced bandwidth control and traffic shaping capability is sold as part of the same product value that is being counted.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.21 B (2025) | |

| Global Consultancy A | USD 3.80 B (2026) | Uses a broader bucket that appears to fold in adjacent performance monitoring and optimization tools, and it anchors the starting point in 2026, which can lift the apparent size when adoption is rising. |

| Trade Publisher B | USD 4.37 B (2030) | Reports a later-year value and often blends aggressive cloud-led growth assumptions into the forward number, with less visibility on how on-premise renewals and price compression are treated. |

The table shows that timing and what is bundled into the software definition explain most of the spread. With a clearly stated inclusion test, year-consistent currency handling, and cross-checks against observable network adoption signals, the resulting value stays traceable to inputs that can be explained and repeated.

Key Questions Answered in the Report

What is the current value of the Network Bandwidth Management Software market?

The sector reached USD 3.41 billion in 2026 and is projected to grow to USD 4.63 billion by 2031 at a 6.29% CAGR.

Which deployment model is growing fastest?

Cloud deployments are expanding at 8.14% CAGR because centralized, subscription-based control planes cut hardware and maintenance overhead.

Why is healthcare the fastest-growing vertical?

Telemedicine adoption, IoT medical devices, and evolving HIPAA segmentation mandates are propelling healthcare spend at a 6.85% CAGR.

How are SMEs influencing the market?

SMEs gain enterprise-grade capabilities through cloud-native licensing and managed services, pushing the segment to a 6.48% CAGR.

Page last updated on: