Scale-Up AI Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 28.64 Billion |

| Market Size (2031) | USD 82.43 Billion |

| Growth Rate (2026 - 2031) | 23.54% CAGR |

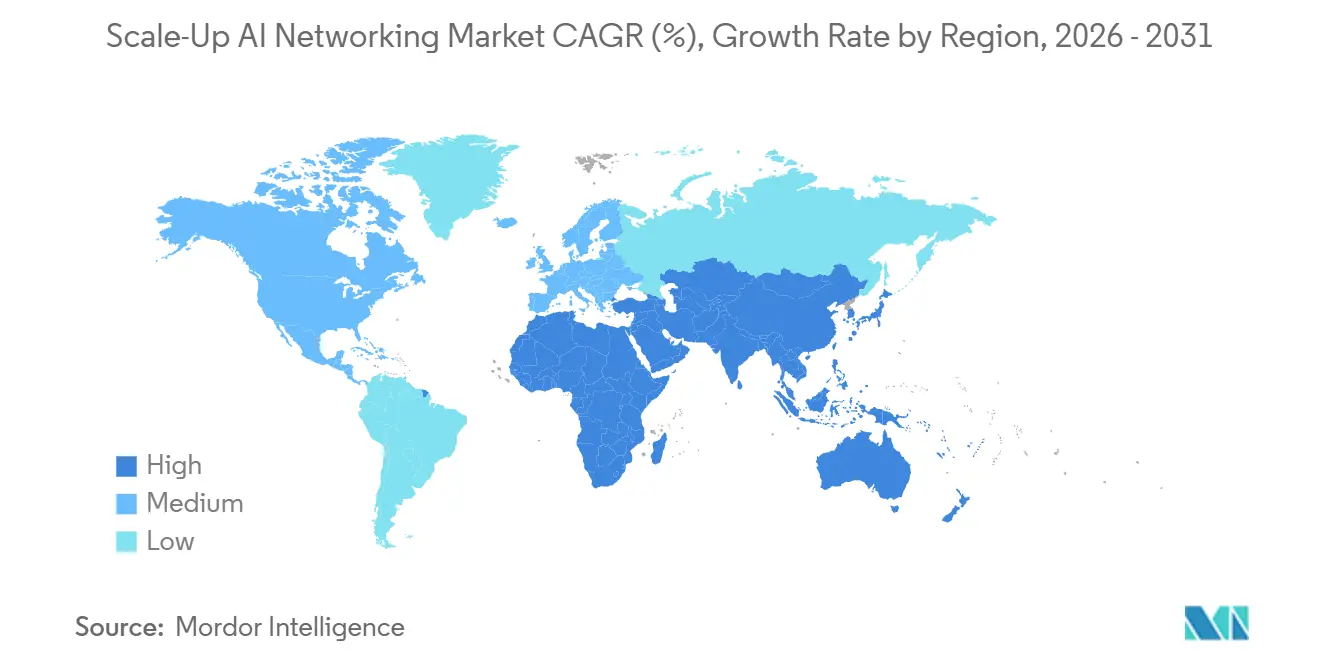

| Fastest Growing Market | Middle East |

| Largest Market | North America |

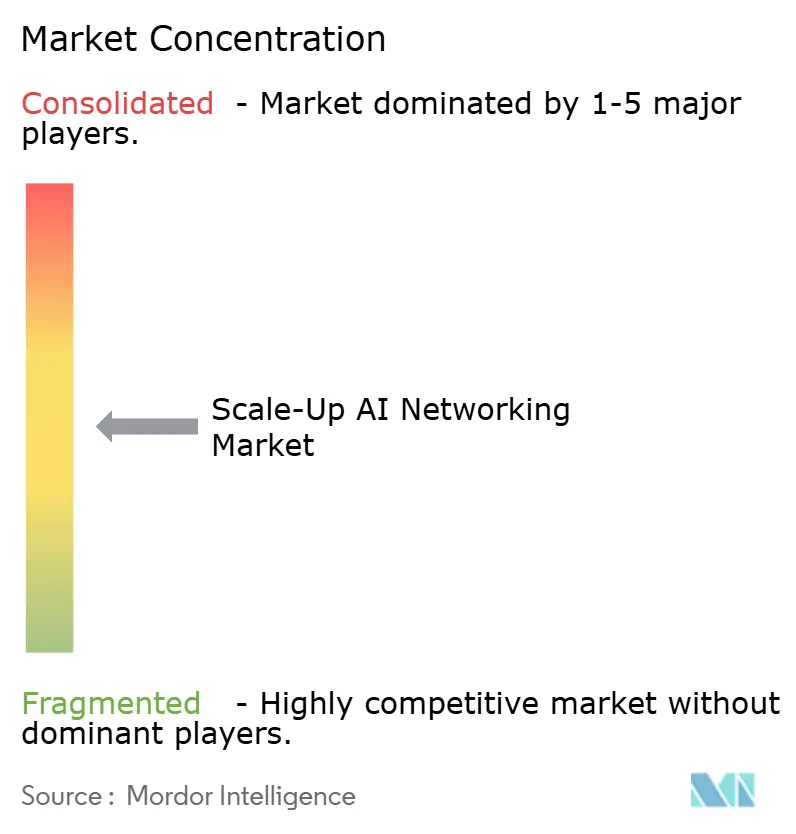

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scale-Up AI Networking Market Analysis by Mordor Intelligence

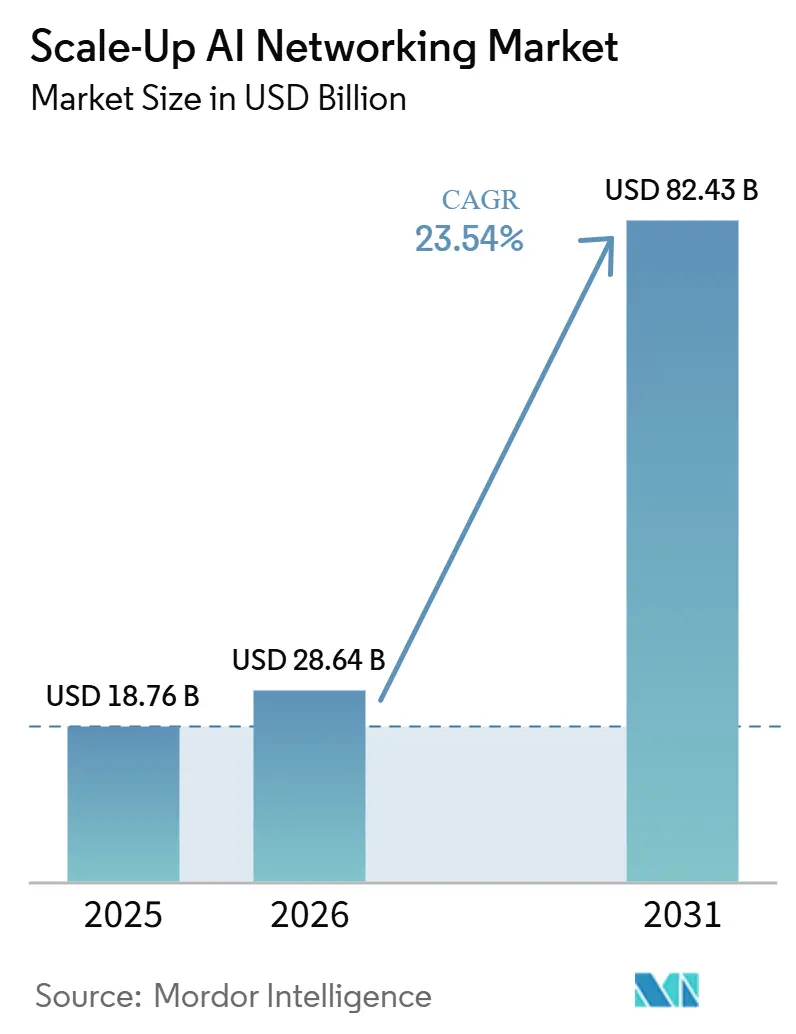

The scale-up AI networking market size was valued at USD 18.76 billion in 2025 and estimated to grow from USD 28.64 billion in 2026 to reach USD 82.43 billion by 2031, at a CAGR of 23.54% during the forecast period (2026-2031). The scale-up AI networking market is moving into a core layer of AI infrastructure because larger accelerator clusters now depend on reliable internal communication just as much as they depend on compute performance. The scale-up AI networking market is also benefiting from a broader shift toward open and multi-vendor fabric approaches, which is widening buyer choice and reducing dependence on one stack. Sovereign AI programs in the Middle East, Europe, and parts of Asia are adding a second stream of demand, which extends spending beyond traditional hyperscaler-led deployments. Vendors in the scale-up AI networking market are responding by pairing faster fabrics with stronger interoperability, automation, and rack-level efficiency rather than competing on bandwidth alone. Supply limits in optics and switch components, along with higher power and cooling needs, are not weakening demand in the scale-up AI networking market, but they are changing project timing and increasing the advantage of suppliers with stronger delivery access.

Key Report Takeaways

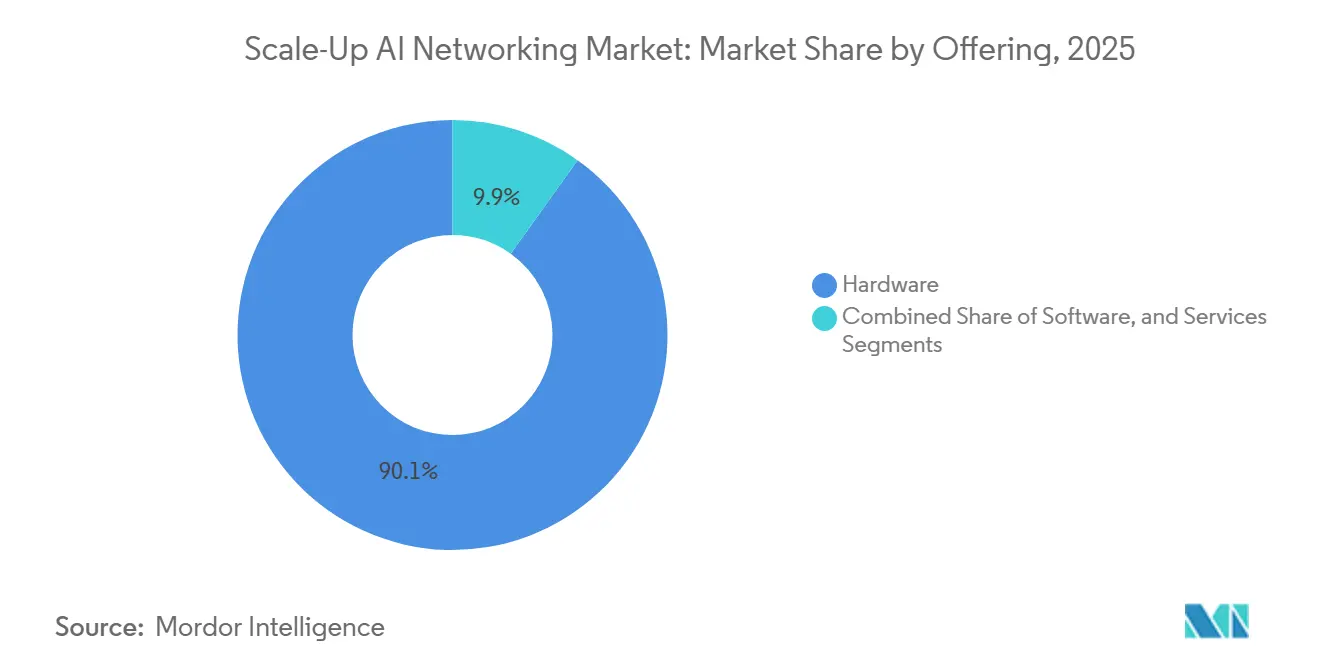

- By offering, hardware held 90.11% share of the scale-up AI networking market in 2025, while software is projected to expand at a 24.21% CAGR through 2031.

- By fabric technology, proprietary accelerator scale-up fabrics held 85.33% of revenue in 2025, while open scale-up fabrics are projected to grow at a 24.62% CAGR through 2031.

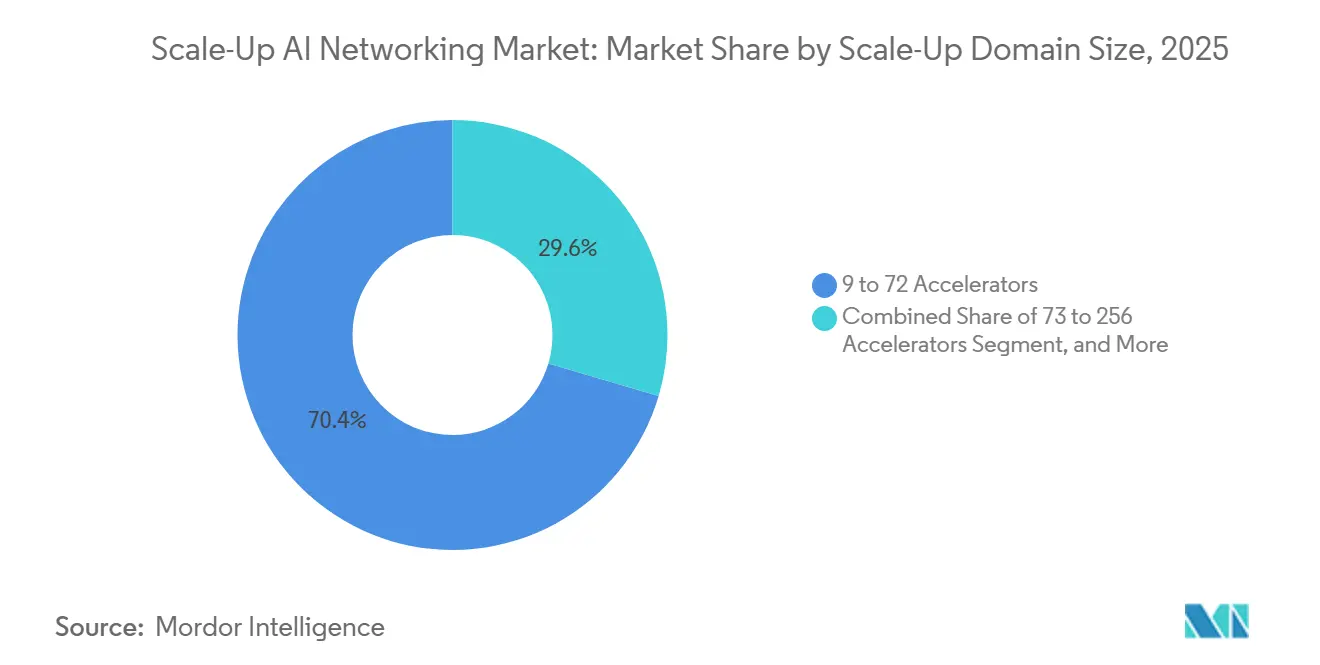

- By scale-up domain size, the 9-72 accelerators segment accounted for 70.42% of revenue in 2025, while the above 256 accelerators segment is projected to grow at a 24.53% CAGR through 2031.

- By workload, AI training held 58.12% of revenue in 2025, while AI inference is projected to expand at a 24.32% CAGR through 2031.

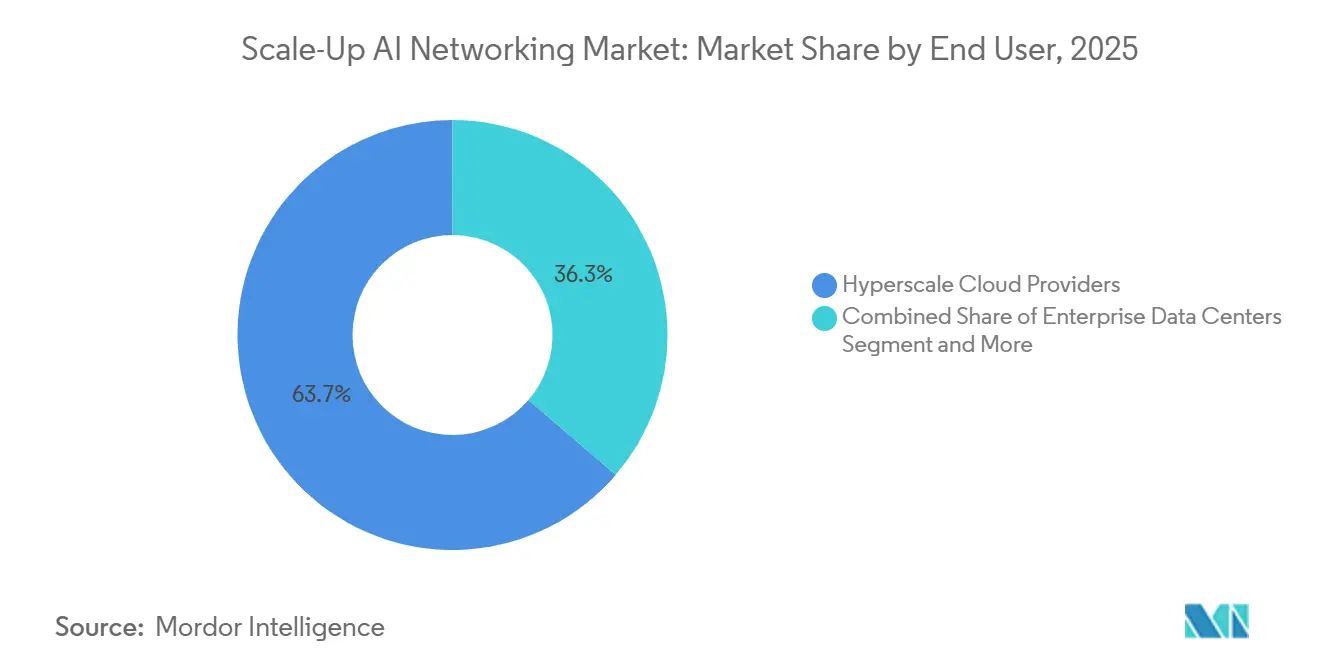

- By end user, hyperscale cloud providers held 63.73% of revenue in 2025, while AI cloud and GPU-as-a-service providers are projected to grow at a 24.44% CAGR through 2031.

- By geography, North America held 58.44% of the scale-up AI networking market share in 2025, while the Middle East and Africa is projected to expand at a 24.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Scale-Up AI Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of AI Training Clusters | +6.5% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Migration From Proprietary Links to Open Ethernet Fabrics | +4.8% | Global, Asia-Pacific and North America lead adoption | Short term (≤ 2 years) |

| Higher Rack-Level Bandwidth Density Requirements | +3.5% | Global, hyperscale-concentrated | Medium term (2-4 years) |

| Co-Packaged Optics and Silicon Photonics Adoption | +2.8% | North America and East Asia, early adopters | Medium term (2-4 years) |

| AI-Ready Network Automation and Telemetry Adoption | +1.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Sovereign AI Infrastructure Buildouts in Key Markets | +1.8% | Middle East and Africa, Europe, South and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of AI Training Clusters

The scale-up AI networking market is being pushed forward by the rapid increase in AI training cluster size, because larger synchronous workloads make network reliability a central design requirement rather than a secondary one. OpenAI said its Multipath Reliable Connection protocol was deployed across its largest NVIDIA GB200 supercomputers to address the network interruptions that had previously forced cluster-wide restarts during training.[1]OpenAI, “Supercomputer Networking to Accelerate Large Scale AI Training,” OpenAI Blog, openai.com The decision to contribute that protocol to the Open Compute Project shows that the scale-up AI networking market is moving toward shared methods for reliability as frontier training systems become more complex. This also changes vendor positioning, because suppliers that can support scale-up, scale-out, and operational software together are better placed when cluster architectures expand across racks, rows, and sites. As a result, the scale-up AI networking market is widening beyond a component sale and moving closer to a full-stack infrastructure decision.

Migration From Proprietary Links to Open Ethernet Fabrics

The scale-up AI networking market is also gaining support from the move toward open Ethernet fabrics, because buyers want broader interoperability across accelerators, switches, and control software. The Open Compute Project launched the ESUN initiative to define Ethernet for scale-up AI infrastructure as a standards-based community effort with participation from major silicon, cloud, and systems vendors. The Ultra Ethernet Consortium formalized an Ethernet-based communication stack for AI and HPC workloads, then updated it in 2026, which helped turn open Ethernet from a concept into a compliance-driven path. In the scale-up AI networking market, that matters because customers adopting AMD, custom silicon, or mixed environments need a fabric that is not tied to a single accelerator roadmap. It also means differentiation is shifting away from closed connectivity alone and toward integration quality, automation, and the ability to prove interoperability at scale.

Higher Rack-Level Bandwidth Density Requirements

Higher rack-level bandwidth density is becoming a direct growth factor for the scale-up AI networking market because each accelerator generation increases pressure on the switching layer, cable plant, and power envelope. NVIDIA said moving from pluggable optics to co-packaged optics in 1.6T networks cuts per-link power from 30W to 9W, which shows why efficiency now sits next to throughput in network design decisions.[2]NVIDIA, “NVIDIA Spectrum-X, the Open, AI-Native Ethernet Fabric, Sets the Standard for Gigascale AI, Now With MRC,” NVIDIA Blog, blogs.nvidia.com Arista's 7060XE7 Series, introduced in June 2026 with Broadcom Tomahawk 6 silicon, reflects that shift by framing the network as a tightly integrated AI supersystem instead of a standalone switch tier. In the scale-up AI networking market, these requirements shorten product cycles because operators cannot wait for long qualification windows when cluster layouts and bandwidth targets are rising so quickly. The result is faster refresh activity and stronger demand for suppliers that can deliver power-aware high-density platforms on a stable roadmap.

Co-Packaged Optics and Silicon Photonics Adoption

Co-packaged optics and silicon photonics are becoming more relevant to the scale-up AI networking market because they offer a clearer path to lower switching power and higher density at the rack level. Ayar Labs described co-packaged optics as moving into practical deployment attention, and Ciena introduced its Vesta 200 6.4T CPX as a pluggable CPO solution designed for AI data center connectivity.[3]Ciena, “Ciena Solidifies AI Networking Leadership, Unveils New Innovations for High-Speed Connectivity,” Ciena, ciena.gcs-web.com Ciena also tied that launch to IEEE 802.3dj-compliant optical interfaces, which is important because the scale-up AI networking market still needs interoperable building blocks before these designs can move broadly across vendor ecosystems. The commercial opening is clear, but deployment pace still depends on the supply chain's ability to support advanced optical components in volume. That keeps early advantage with vendors that can pair optical innovation with dependable manufacturing access and standards alignment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Power and Cooling Load at Scale-Up Layer | -1.8% | Global, most acute in mature markets with legacy data center stock | Short term (≤ 2 years) |

| Supply Chain Dependence for High-Speed Switch Silicon and Optics | -1.6% | Global, with particular exposure in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Interoperability Gaps Between Vendor Ecosystems | -1.2% | Global | Medium term (2-4 years) |

| Immature Standards Across Emerging Scale-Up Architectures | -1.0% | Global, impacts emerging markets adopting multi-vendor configurations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Power and Cooling Load at Scale-Up Layer

Power and cooling pressure is one of the clearest restraints on the scale-up AI networking market because network equipment now sits inside much denser AI infrastructure environments than conventional data halls were built for. Applied Thermal Engineering and IEEE ITherm both point to liquid cooling as a necessary direction, but they also note added complexity in plumbing, coolant compatibility, and long-term serviceability. Ciena said its pluggable CPO approach can reduce power consumption by up to 70%, which shows how strongly the scale-up AI networking market is now being shaped by power-performance tradeoffs rather than bandwidth alone. This favors greenfield campuses that can be designed around new thermal requirements, while retrofits in older facilities face longer readiness cycles and higher integration risk. It also means fabric decisions are becoming tied more closely to site engineering and deployment sequencing.

Supply Chain Dependence for High-Speed Switch Silicon and Optics

The scale-up AI networking market remains exposed to supply dependence in high-speed switch silicon and optics, because these components determine whether a planned cluster can move from order book to activation on schedule. Lumentum said optical components will define the next era of AI data centers, which underscores how central the photonics layer has become to network delivery rather than just to performance optimization. Celestica's move to make its DS6000-series 1.6TbE switches available for customer orders in 2026 illustrates how platform readiness in the scale-up AI networking market depends on synchronized availability across silicon, optics, and systems manufacturing. When those parts do not arrive in step, buyers can secure accelerators and still miss deployment windows because the fabric remains incomplete. This keeps pricing power and scheduling leverage with suppliers that can lock in strategic component access across the stack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Leads Revenue While Software Builds Strategic Weight

Hardware held 90.11% of revenue in 2025, which kept the physical layer as the main spending center of the scale-up AI networking market. That mix reflects the capital intensity of switches, ASICs, network interface cards, cables, and optical components required to stand up new AI clusters. It also shows that much of the scale-up AI networking market is still in a build phase where buyers first secure bandwidth, topology, and reliability at the physical layer before widening spend into orchestration. Software is the fastest-growing offering at a 24.21% CAGR through 2031, as operators add telemetry, congestion control, and automation tools around existing fabric deployments.

The software case is becoming stronger because the scale-up AI networking industry is moving toward more complex and distributed cluster operations. The Ultra Ethernet Consortium's specification provides a standards-driven software and transport framework for AI and HPC environments, which supports wider use of common operational methods across vendors. Google also showed through its Matryoshka network design system that model-driven management can support large data center estates over multiple years, which reinforces the long-run value of software layers in the scale-up AI networking market. Services remain smaller in revenue, but they rise with integration complexity because multi-site AI factory architectures need specialized design, commissioning, and ongoing support.

By Fabric Technology: Proprietary Leadership Faces a Broader Open Push

Proprietary accelerator scale-up fabrics held 85.33% of revenue in 2025, which reflected the installed base advantage of tightly integrated accelerator ecosystems in the scale-up AI networking market. That lead came from the technical and commercial strength of hardware-software co-design, especially where buyers wanted the shortest path to large training system deployment. Open scale-up fabrics are the fastest-growing segment at a 24.62% CAGR through 2031, which shows that customers are looking for alternatives as non-proprietary accelerator options gain traction. The scale-up AI networking market size for open scale-up fabrics is rising with demand for architectures that can work across broader silicon choices and longer procurement cycles.

AMD and Celestica said the Helios rack-scale AI platform will use Ultra Accelerator Link over Ethernet for scale-up connectivity, which gives the open fabric segment a clearer product path rather than just a standards narrative. NVIDIA responded with NVLink Fusion, which extends its ecosystem by allowing third-party custom XPUs to integrate through NVLink chiplets instead of leaving that adjacent space uncontested. Ethernet-based scale-up fabrics are also becoming more visible through ESUN and Arista's 7060XE7 platforms, while early optical I/O approaches such as Ayar Labs' optical chiplet work remain earlier in the development cycle. In the scale-up AI networking market, fabric competition is now defined less by raw connectivity alone and more by roadmap control, interoperability, and ecosystem depth.

By Scale-Up Domain Size: Mid-Range Pods Still Drive Volume

The 9-72 accelerators segment accounted for 70.42% of the scale-up AI networking market size in 2025, which confirms that most current commercial deployments still operate in mid-range cluster footprints. That segment remains the core demand base because many hyperscale, AI cloud, and enterprise projects deploy at a size that balances performance, cost, and operational simplicity. Above 256 accelerators is the fastest-growing segment at a 24.53% CAGR through 2031, which shows where the next wave of architectural change is being concentrated. The scale-up AI networking market is therefore being shaped by volume at one end and design complexity at the other.

Google's Virgo fabric showed what the upper end of this curve looks like, with a two-layer non-blocking topology capable of linking 134,000 chips and delivering up to 47 petabits per second of bi-sectional bandwidth. The 73-256 accelerators segment sits in the middle of the current design contest, because that is where buyers are actively weighing NVLink, UALink, and ESUN-aligned Ethernet options against their near-term cluster roadmaps. Up to 8 accelerators remains smaller in revenue, but it is useful as an entry point for enterprise and academic inference deployments that can later expand into larger programs. This mix means vendors in the scale-up AI networking market need different switch radix, cabling density, and thermal approaches across domain sizes rather than one universal design.

By Workload: Training Holds Revenue While Inference Gains Speed

AI training held 58.12% of revenue in 2025, which kept it as the largest workload in the scale-up AI networking market. That position reflects the bandwidth intensity of frontier model pretraining and the continued role of large synchronous clusters at hyperscalers and specialized AI cloud operators. AI inference is projected to grow at a 24.32% CAGR through 2031, which makes it the fastest-growing workload as production deployments increase. The scale-up AI networking market size for inference is rising because production systems need lower latency, burst tolerance, and efficient operation across more varied node populations than large training jobs do.

The UALink 2.0 specification introduced in-network compute capabilities and standardized management features, which shows that workload-specific optimization is moving into the standards layer as well. Fine-tuning and model adaptation are also becoming more relevant because enterprises want mid-scale AI infrastructure without committing to full pretraining environments. HPC and scientific computing remain a steady revenue contributor, since national labs and research programs are adopting many of the same networking building blocks. Other workloads, including analytics and recommendation pipelines, still account for less revenue today, but they broaden the long-run demand base of the scale-up AI networking market as AI-native applications spread.

By End User: Hyperscalers Lead Spend While AI Cloud Providers Expand Faster

Hyperscale cloud providers held 63.73% of revenue in 2025, which made them the dominant buyer group in the scale-up AI networking market. Their lead came from the size of their capital programs, their ability to co-design infrastructure with manufacturing partners, and their early demand for very large training clusters. AI cloud and GPU-as-a-service providers are projected to grow at a 24.44% CAGR through 2031, which makes them the fastest-growing end-user segment. The scale-up AI networking market share is still centered on hyperscalers, but the commercial pressure on AI cloud platforms is pushing them to compete more directly on fabric performance, availability, and latency.

IEEE Communications Society described how hyperscalers work with ODM partners on networking equipment design, which helps explain why this buyer group can move quickly on custom topologies and white-box systems. Enterprise data centers are growing as LLM fine-tuning and agentic AI projects expand, but many still prefer turnkey AI factory solutions instead of bespoke network engineering. Government, research, and HPC centers remain strategically important because they support national computing priorities and often adopt commercial AI networking standards into public infrastructure programs. Colocation providers are also building AI-ready pods to attract GPU cloud tenants, which turns the scale-up AI networking market into a service differentiator beyond the hyperscaler segment.

Geography Analysis

North America held 58.44% of the scale-up AI networking market share in 2025, which kept it as the largest regional contributor. The region remains the center of the scale-up AI networking market because it combines hyperscaler capital, accelerator ecosystem leadership, and strong participation in open standards efforts. The United States accounts for most of that demand, while Canada adds research-led activity and Mexico supports emerging colocation and nearshore infrastructure interest. North America also has an advantage in vendor proximity, because several of the companies and industry groups shaping Ethernet, UALink, and rack-scale AI systems are closely tied to the regional ecosystem.

Asia-Pacific is the second-largest geography in the scale-up AI networking market, with demand spread across China, Japan, South Korea, India, and Southeast Asia. Huawei's June 2026 launch of 10 AI-Optical Network products at MWC Shanghai showed that China is pushing actively into AI-centric optical and network infrastructure development. Japan remains technically important through sovereign computing priorities and optical interconnect work, while South Korea supports the broader ecosystem through its memory and semiconductor base. India and Southeast Asia are growing parts of the scale-up AI networking market because regional digital infrastructure buildouts are expanding alongside AI deployment ambitions.

Europe and the Middle East and Africa show different demand patterns within the scale-up AI networking market. Europe recorded solid momentum in 2025, with Germany standing out as a major data center location and as a recipient of federal support for at least one AI Gigafactory. The region's growth path is tied to sovereign compute priorities, compliance requirements, and longer public-private procurement cycles. The Middle East and Africa is the fastest-growing geography at a 24.42% CAGR through 2031, supported by sovereign AI investment and large campus-scale development plans. The Stargate UAE project, with total cost exceeding USD 30 billion and Phase 1 expected in Q3 2026, shows how quickly the region is moving from policy ambition to physical infrastructure commitment. South America remains earlier in development, with demand centered on colocation growth and domestic infrastructure programs that are still building scale.

Competitive Landscape

The scale-up AI networking market shows a moderately concentrated structure at the top, with a limited group of switch silicon vendors and system manufacturers holding outsized influence over revenue and roadmap direction. In Q3 2025, Celestica and NVIDIA together held close to 50% of Ethernet AI back-end switch revenue, which points to meaningful concentration even though the wider ecosystem still includes many optics, ODM, and software participants. The scale-up AI networking market is shaped by more than share alone, because NVIDIA competes across switch silicon, scale-up fabrics, and rack-scale system integration at the same time. Open initiatives such as ESUN and UALink are the clearest coordinated response, because they give competing vendors a common framework for interoperability and multi-vendor compliance.

The most attractive white space in the scale-up AI networking market sits where scale-up and scale-out requirements begin to overlap across multi-rack AI systems. NVIDIA's partnership with Marvell under NVLink Fusion, backed by a USD 2 billion equity investment, shows how component suppliers are trying to secure platform-level roles instead of competing only on standalone specifications. Celestica's DS6000-series launch and its Helios collaboration with AMD show that ODM-linked vendors are moving more aggressively into open 1.6T fabric infrastructure for next-generation clusters. At the same time, Ayar Labs is relevant because optical I/O has direct implications for rack-scale AI bandwidth and power efficiency, which places it closer to the core of this market than vendors whose portfolios remain centered on campus or general enterprise networking. That same logic makes component-focused players such as Astera Labs and AMD's Pensando more aligned with the scale-up AI networking market than companies without a disclosed AI cluster fabric role.

Competition in the scale-up AI networking market is increasingly decided by three things, interoperability, supply access, and deployment support. Vendors that can contribute to open standards while still extending proprietary advantages are in a stronger position than companies relying on a single layer of the stack. Buyers are also placing more weight on whether suppliers can support multi-site fabrics, power-aware switching, and timely delivery across optics and silicon. This leaves the scale-up AI networking market moderately concentrated at the top, but still open enough for specialized players to gain share where they solve integration or efficiency problems more directly than broad portfolio vendors.

Scale-Up AI Networking Industry Leaders

NVIDIA Corporation

Broadcom Inc.

Cisco Systems, Inc.

Arista Networks, Inc.

Marvell Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Huawei unveiled 10 new AI-Optical Network (AI-ON) products and solutions at MWC Shanghai 2026, targeting operators building AI-centric all-optical target networks. The announcement positions Huawei as an active participant in the next-generation AI fabric market, particularly for operators outside the US-centric hyperscaler ecosystem.

- June 2026: Arista Networks announced the 7060XE7 Series, a portfolio of 1.6T networking platforms engineered as a rack-scale AI supersystem leveraging Broadcom's Tomahawk 6 silicon. Air-cooled configurations are targeted for Q4 2026 shipment and liquid-cooled variants for Q1 2027, representing Arista's formal entry into the scale-up networking domain.

- June 2026: Cisco announced new Silicon One G300-based systems and Linear Pluggable Optics (LPO) offerings for AI data centers, with the LPO solution reducing optical module power consumption by 50% compared with retimed modules. Customers deploying the N9000 and 8000 series with LPO can reduce overall switch power by 30%.

- June 2026: HPE used its Discover 2026 conference to position Juniper-powered networking as the foundation of its AI infrastructure strategy, announcing the QFX5220 switch for large-scale AI training clusters and the QFX5140 for AI inference edge deployments, alongside the QFX5252 switch tray designed for AMD's Helios rack-scale platform.

Global Scale-Up AI Networking Market Report Scope

The Global Scale-Up AI Networking Market refers to the specialized industry segment that focuses on developing and deploying advanced networking solutions designed to support the scaling of artificial intelligence (AI) workloads across increasingly large and complex infrastructures.

The Scale-Up AI Networking Market Report is Segmented by Offering (Hardware, Software, and Services), Fabric Technology (Proprietary Accelerator Scale-Up Fabrics, Open Scale-Up Fabrics, Ethernet-Based Scale-Up Fabrics, and Other Emerging Scale-Up Fabrics), Domain Size (Up to 8 Accelerators, 9 to 72 Accelerators, 73 to 256 Accelerators, and Above 256 Accelerators), Workload (AI Training, AI Inference, Fine-Tuning and Model Adaptation, HPC and Scientific Computing, and Other Workloads), End User (Hyperscale Cloud Providers, AI Cloud and GPU-as-a-Service Providers, Enterprise Data Centers, Government, Research, and HPC Centers, and Colocation Data Centers), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Proprietary Accelerator Scale-Up Fabrics |

| Open Scale-Up Fabrics |

| Ethernet-Based Scale-Up Fabrics |

| Other Emerging Scale-Up Fabrics |

| Up to 8 Accelerators |

| 9 to 72 Accelerators |

| 73 to 256 Accelerators |

| Above 256 Accelerators |

| AI Training |

| AI Inference |

| Fine-Tuning and Model Adaptation |

| HPC and Scientific Computing |

| Other Workloads |

| Hyperscale Cloud Providers |

| AI Cloud and GPU-as-a-Service Providers |

| Enterprise Data Centers |

| Government, Research, and HPC Centers |

| Colocation Data Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Offering | Hardware | |

| Software | ||

| Services | ||

| By Fabric Technology | Proprietary Accelerator Scale-Up Fabrics | |

| Open Scale-Up Fabrics | ||

| Ethernet-Based Scale-Up Fabrics | ||

| Other Emerging Scale-Up Fabrics | ||

| By Scale-Up Domain Size | Up to 8 Accelerators | |

| 9 to 72 Accelerators | ||

| 73 to 256 Accelerators | ||

| Above 256 Accelerators | ||

| By Workload | AI Training | |

| AI Inference | ||

| Fine-Tuning and Model Adaptation | ||

| HPC and Scientific Computing | ||

| Other Workloads | ||

| By End User | Hyperscale Cloud Providers | |

| AI Cloud and GPU-as-a-Service Providers | ||

| Enterprise Data Centers | ||

| Government, Research, and HPC Centers | ||

| Colocation Data Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the scale-up AI networking market?

The scale-up AI networking market was valued at USD 18.76 billion in 2025, is estimated at USD 28.64 billion in 2026, and is forecast to reach USD 82.43 billion by 2031 at a 23.54% CAGR.

What is driving demand for scale-up AI networking?

The main demand drivers are larger AI training clusters, wider adoption of open Ethernet fabrics, and rising rack-level bandwidth density needs that make the network a core part of AI system design.

Which offering category leads revenue and which grows fastest?

Hardware led with 90.11% of revenue in 2025, while software is projected to grow fastest at a 24.21% CAGR through 2031 as automation and telemetry become more important.

Which fabric technology is expanding the fastest?

Open scale-up fabrics are projected to grow at a 24.62% CAGR through 2031, even though proprietary accelerator scale-up fabrics still held the largest 85.33% revenue share in 2025.

Which region leads spending and which region grows fastest?

North America led with a 58.44% share in 2025, while the Middle East and Africa is projected to expand fastest at a 24.42% CAGR through 2031.

What is the main constraint on deployment timelines?

Power and cooling readiness, along with dependence on high-speed optics and switch silicon, are the main factors that delay cluster commissioning even when compute demand remains strong.

Page last updated on: