Edge AI Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.25 Billion |

| Market Size (2031) | USD 6.82 Billion |

| Growth Rate (2026 - 2031) | 24.83% CAGR |

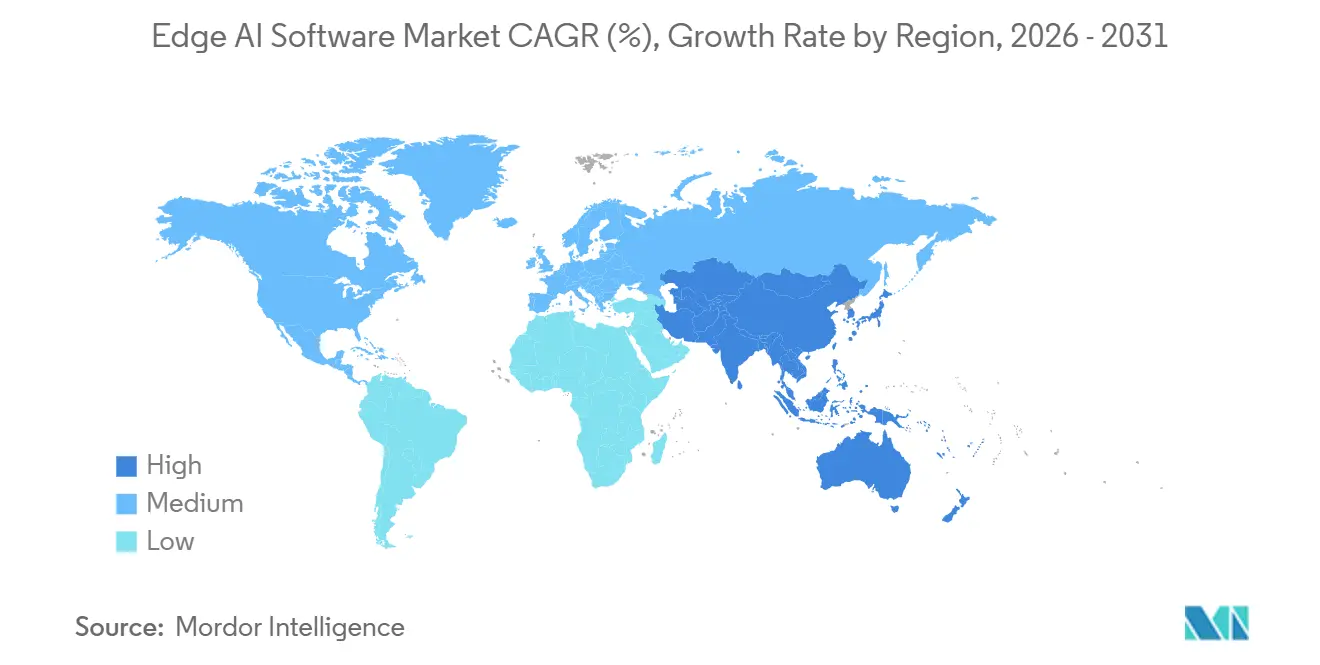

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

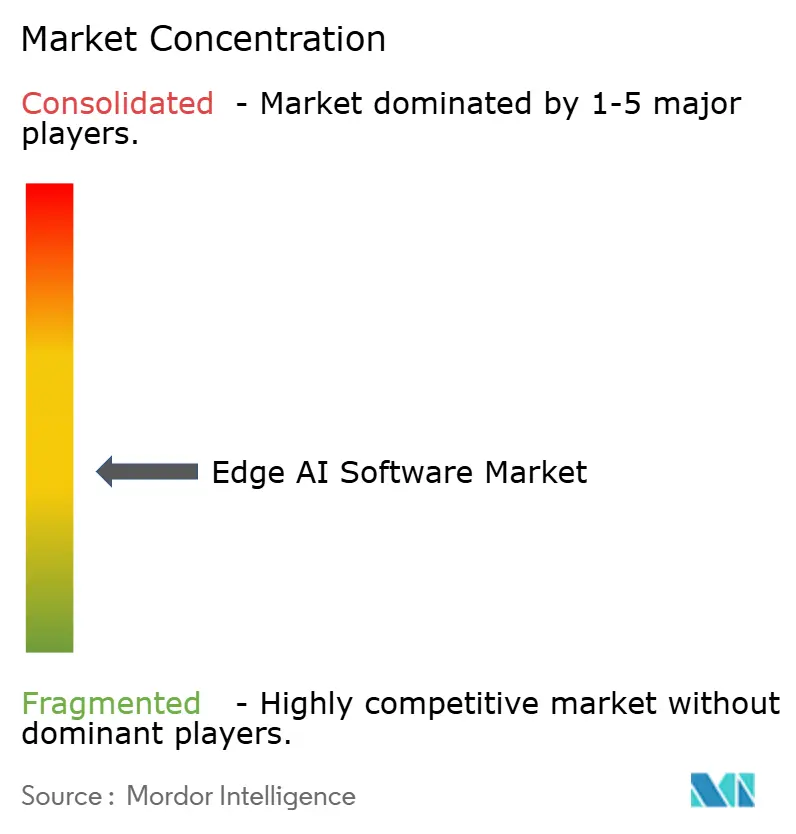

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edge AI Software Market Analysis by Mordor Intelligence

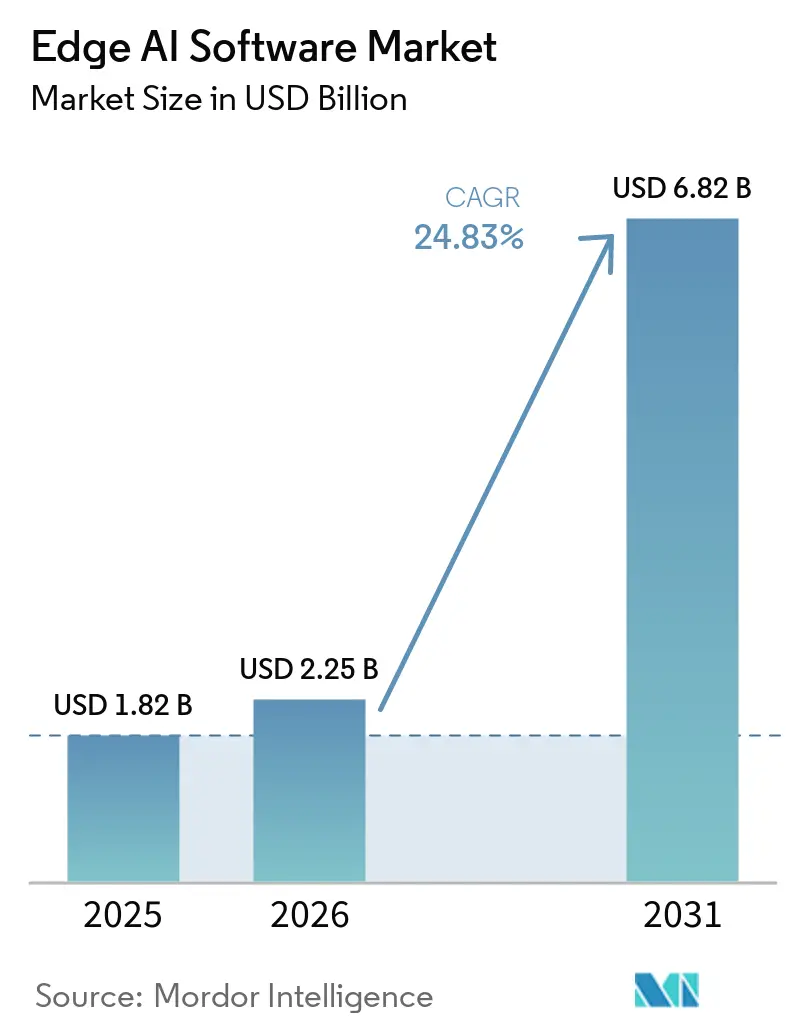

The edge AI software market size is projected to be USD 1.82 billion in 2025, USD 2.25 billion in 2026, and reach USD 6.82 billion by 2031, growing at a CAGR of 24.83% from 2026 to 2031. The edge AI software market is expanding because AI inference is moving away from centralized cloud environments and closer to the point where data is created. This shift is being driven by latency requirements, rising data-transfer costs, and the growing burden of moving large industrial sensor streams into remote infrastructure. As enterprise AI workloads move from pilot use into daily operations, the cloud-only variable cost model becomes harder to sustain across distributed environments. The edge AI software market is also benefiting from broader enterprise demand for hybrid orchestration, sovereign AI control, and platform designs that reduce dependence on constant connectivity. Competitive pressure is rising because semiconductor vendors, hyperscalers, and industrial software providers are all trying to control a larger portion of the deployment stack, which is narrowing room for software vendors that cannot prove interoperability across mixed hardware fleets.

Key Report Takeaways

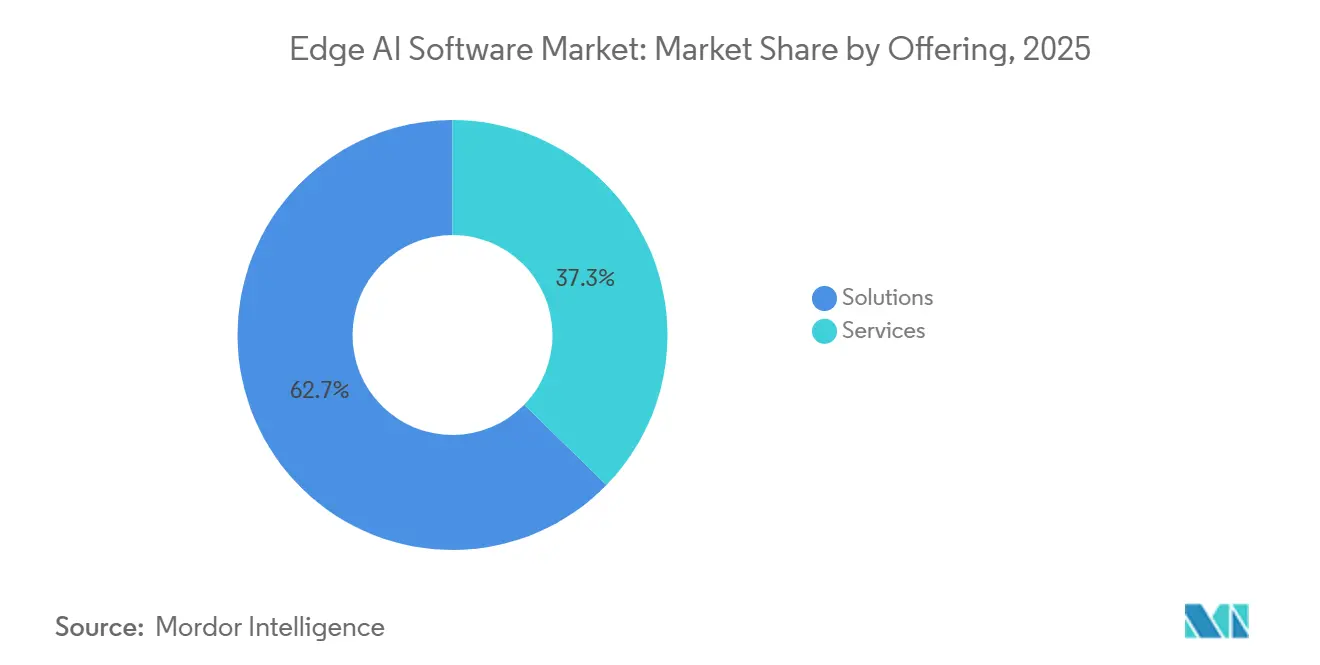

- By offering, solutions segment, held 62.72% of the edge AI software market share in 2025, while services are projected to expand at a 25.64% CAGR through 2031.

- By data modality, visual data led with a 29.98% revenue share of the edge AI software market in 2025, while auditory data is projected to grow at a 26.88% CAGR through 2031.

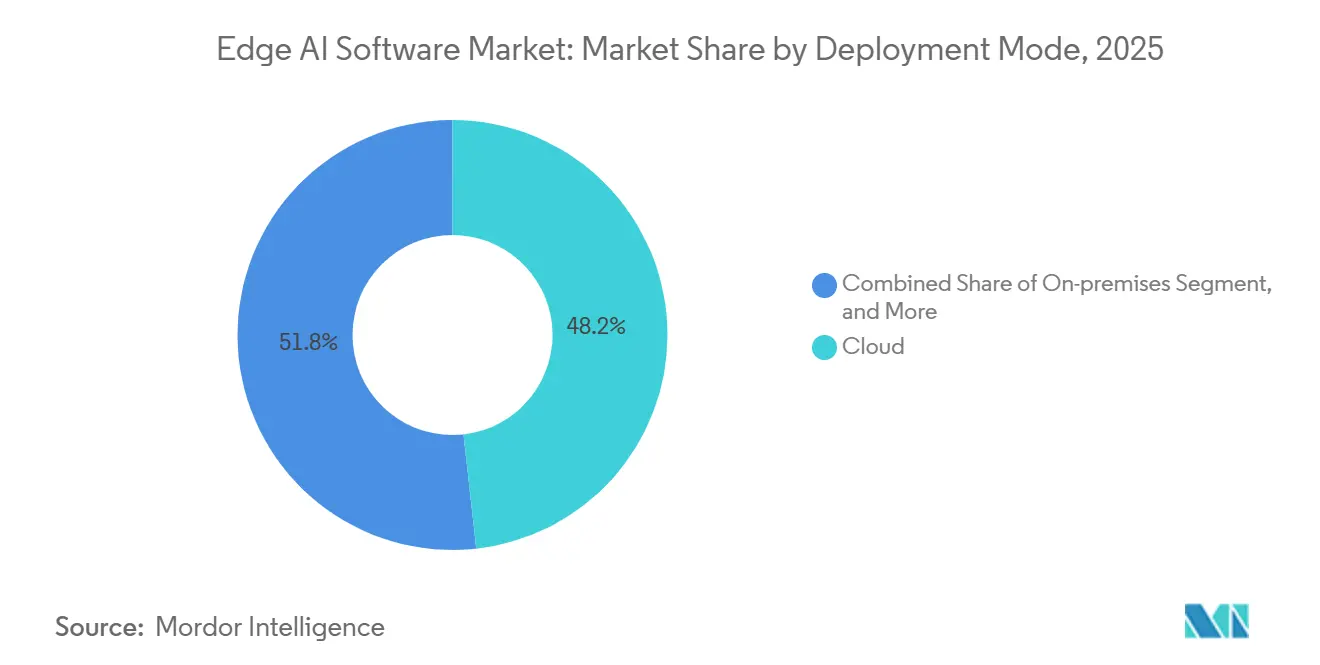

- By deployment mode, cloud accounted for 48.24% of the edge AI software market size in 2025, while on-premises deployment is expected to advance at a 25.73% CAGR through 2031.

- By end-user industry, manufacturing captured 20.99% of the edge AI software market size in 2025, while automotive and transportation is projected to expand at a 27.12% CAGR through 2031.

- By geography, North America held 34.78% share of the edge AI software market in 2025, while Asia-Pacific is projected to record the highest regional CAGR at 26.71% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Edge AI Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation Of Internet Of Things Endpoint Data | +6.5% | Global, with APAC core, China, Japan, South Korea, and North America as primary generators | Short term (≤ 2 years) |

| Demand For Low-Latency Decisioning At The Edge | +5.5% | Global, strongest in North America, Europe, and APAC industrial corridors | Short term (≤ 2 years) |

| Need For Privacy-Preserving On-Device Inference | +4.0% | Europe, North America, with spillover to APAC data-localization markets | Medium term (2-4 years) |

| 5G-Enabled Distributed Application Architectures | +3.2% | North America and APAC, China, Japan, South Korea, with spillover to Europe and Middle East and Africa | Medium term (2-4 years) |

| Fleet-Scale Edge Model Operations And Orchestration | +2.5% | North America and Europe industrial zones, APAC manufacturing hubs | Medium term (2-4 years) |

| Certification-Ready Stacks For Safety-Critical Deployments | +1.8% | North America and Europe, automotive, aerospace, medical device sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Internet Of Things Endpoint Data

The edge AI software market is gaining momentum because the amount of machine-generated data at industrial and enterprise endpoints has become too large for cloud-relay architectures to handle efficiently. Research on the ELARA framework, published in Discover Computing in May 2026, showed end-to-end latency of 39-52 milliseconds, bandwidth savings of up to 48%, and task completion rates of 93-98% across large-scale IoT networks, which directly supports local processing for time-sensitive workloads. That result matters because industrial systems can emit sensor streams at 1 Hz or higher across thousands of nodes, and the cost of transmitting raw telemetry into centralized infrastructure rises quickly as deployments scale. Cisco’s State of Wireless Report 2026 also found that IoT growth ranked as the top driver of enterprise wireless investment, ahead of user mobility and high-bandwidth application adoption, which shows that network spending is now being shaped by endpoint intelligence rather than simple connectivity expansion.[1]Cisco, “State of Wireless Report 2026,” Cisco, cisco.com. In this setting, the edge AI software market benefits because enterprises need software that can filter, contextualize, and act on data locally before deciding what should move upstream, and raw network capacity alone does not solve that requirement.

Demand For Low-Latency Decisioning At The Edge

The edge AI software market is also being pushed forward by use cases that require decisions in real time across manufacturing, autonomous systems, utilities, and public safety environments. Once latency budgets fall below 50 milliseconds, or site telemetry rises to 1 terabyte per day, local inference becomes a practical requirement rather than a design preference. NVIDIA and T-Mobile announced in March 2026 that they were integrating physical AI applications over distributed 5G edge networks with the NVIDIA Metropolis platform, including smart city operations, automated utility inspection, and industrial safety workloads where response speed is operationally critical.[2]NVIDIA, “NVIDIA, T-Mobile and Partners Integrate Physical AI Applications on AI-RAN-Ready Infrastructure,” NVIDIA Newsroom, nvidianews.nvidia.com. Hewlett Packard Enterprise also launched HPE AI Grid in March 2026 to deliver predictable low-latency performance across distributed inference sites, and Comcast began field trials for real-time edge inferencing on its network using small language models.[3]Hewlett Packard Enterprise, “HPE Transforms Distributed AI Factories into Intelligent AI Grid Powered by NVIDIA,” Hewlett Packard Enterprise, hpe.com. The edge AI software market is therefore shifting toward platforms that can hold inference performance steady under constrained compute conditions, because average throughput on benchmark hardware matters less than deterministic behavior at the point of use.

Need For Privacy-Preserving On-Device Inference

Privacy rules are turning on-device AI execution into a purchasing requirement for many deployments, and that is giving the edge AI software market a strong medium-term tailwind. NIST Special Publication 800-226, finalized in 2025, pushed the sector toward a stricter interpretation of privacy-preserving AI by tying deployment claims to defined threat models, quantified privacy loss, and explicit utility tradeoffs.[4]National Institute of Standards and Technology, “NIST SP 800-226: Guidelines for Evaluating Differential Privacy Guarantees,” National Institute of Standards and Technology, nist.gov. That guidance raises the standard for vendors because privacy is no longer a broad positioning statement, and it must now be engineered into the software stack in measurable ways. IBM responded in May 2026 by making IBM Sovereign Core generally available, combining governance, compliance, and AI execution in a single deployment model for enterprises and governments that want tighter control over their workloads. The edge AI software market is benefiting most in healthcare, banking, defense, and public administration, where local inference helps organizations meet approval requirements that would be harder to satisfy in shared cloud environments.

5G-Enabled Distributed Application Architectures

The spread of 5G is changing where AI workloads can run, and that is widening the addressable footprint of the edge AI software market. Intel, Nokia, and Dell presented a far-edge User Plane Function device at Mobile World Congress 2026 that offered a 30% performance boost for 5G core UPF deployments while reducing latency and improving local service enablement, which supports inference closer to cell sites and other network edge locations. NVIDIA and T-Mobile’s March 2026 collaboration followed the same architecture, using T-Mobile’s 5G standalone network for coverage and quality of service while NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs handled distributed inference at the cell site layer. Research published in the Journal of Computer Science and Technology in 2026 described edge-native system design as a core enabler of next-generation autonomous and robotic systems, which reinforces the view that 5G is supporting a new class of distributed AI applications rather than only faster connectivity. For the edge AI software market, this matters because software placement, orchestration, and service delivery now have to span enterprise premises, telecom nodes, and distributed field locations within the same operating model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heterogeneous Edge Environment Integration Complexity | -2.6% | Global, most acute in multi-vendor APAC manufacturing and Middle East and Africa infrastructure deployments | Short term (≤ 2 years) |

| Model Optimization Limits On Constrained Devices | -1.9% | Global, especially in APAC IoT device-heavy markets and Middle East and Africa resource-limited deployments | Medium term (2-4 years) |

| Certification Gaps For Regulated Deployments | -1.4% | North America and Europe, automotive, aerospace, medical device sectors | Long term (≥ 4 years) |

| Immature Benchmarking For Heterogeneous Software Stacks | -0.8% | Global, with enterprise procurement implications in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heterogeneous Edge Environment Integration Complexity

The edge AI software market still faces a major operational barrier because most enterprise deployments span different processor types, operating systems, and connectivity conditions. Research published in Sensors in 2026 on the MIGS architecture found that heterogeneous device integration requires protocol-agnostic middleware that can work across Modbus, OPC UA, and MQTT at the same time, which shows how difficult interoperability remains in real industrial settings. ZEDEDA’s 2026 survey results also pointed to the same problem, with 41% of enterprises identifying distributed workload management as a primary challenge and 47% reporting the use of hybrid cloud-edge architectures that demand consistent governance across different hardware environments. This creates a split in the edge AI software market because large enterprises with standardized fleets can scale faster, while buyers with legacy operational technology face longer deployment cycles and higher integration costs. Until the sector develops a more universal hardware abstraction layer, interoperability will remain a structural drag on rollout speed and software standardization.

Model Optimization Limits On Constrained Devices

Model optimization remains another clear restraint because the smallest edge devices still place hard limits on what software can run in production. Research published on arXiv in April 2026 showed that running advanced language models on devices with sub-4-gigabyte memory budgets depends on multi-stream decoding, dynamic speculative decoding, and sub-4-bit quantization, and those techniques still rely heavily on specific silicon-software pairings. Work presented at the AAAI Conference on Artificial Intelligence in 2026 also found that latency prediction across heterogeneous edge devices requires device-specific execution profiling instead of generic black-box regression, which means vendors still struggle to promise consistent behavior across mixed fleets. That limitation raises engineering costs in the edge AI software market because vendors often need separate optimization pipelines for each hardware target. It also slows deployment in the long tail of IoT endpoints, where buyers want software portability but the available optimization methods remain closely tied to individual chip families.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Anchor Revenue As Services Scale Rapidly

Solutions held 62.72% of the edge AI software market share in 2025, which kept them in the leading position as enterprises favored integrated platforms over modular contracting models. That pattern reflects a practical buying preference because manufacturers, telecom operators, and other large users want validated packages that combine inference runtimes, compression tools, and deployment orchestration in one product. Buyers have generally preferred this route because it reduces interoperability uncertainty at the edge and lowers the burden of stitching together tools from different vendors. In the edge AI software market, that preference has given platform providers an early revenue advantage because they can sell a complete operating layer rather than only a narrow point capability. The same trend also shows that the edge AI software market has moved beyond trial deployments, since procurement teams usually standardize on bundled solutions only after internal teams see a clear path toward long-term operations.

Services are projected to expand at a 25.64% CAGR through 2031, and that pace is faster than the overall edge AI software market. That spread signals a change in how deployments are being managed after the initial software stack is installed. Enterprises are increasingly outsourcing edge MLOps, model optimization, lifecycle management, and fleet-wide observability because many do not have the internal engineering teams needed to manage model drift across distributed assets. Siemens made that transition more concrete in April 2026 when it announced broader availability for its Industrial AI Suite on Siemens Industrial Edge, covering model training, deployment, retraining, and AI model management across multiple factory sites. Google’s expansion of LiteRT-LM support across iOS Swift, JavaScript, and Android APIs in 2026 showed a similar direction in mobile environments, where the runtime increasingly behaves like an embedded managed layer rather than a stand-alone software purchase.

The edge AI software market is therefore seeing a gradual blending of product and service economics, even if the two categories are still reported separately. Integrated solutions remain the first purchase for many enterprises, but service layers become more important once deployments move from pilots into full operations. That is especially visible among mid-market industrial users that installed edge hardware in 2023 and 2024 but still lack internal AI staffing depth. As a result, the edge AI software industry is developing toward lifecycle platforms that combine packaged software with ongoing operational support, rather than simple license-based software delivery.

By Data Modality: Visual Intelligence Anchors The Market As Auditory Demand Surges

Visual data accounted for 29.98% of revenue in 2025, making it the largest modality in the edge AI software market. That lead was built on years of computer vision deployment across factory inspection, security surveillance, and automotive perception systems. The installed global camera base continues to create a large demand reservoir because many endpoints still collect video that is not analyzed in real time. NVIDIA noted in 2026 that more than 1.5 billion cameras were installed globally and that less than 1% was being meaningfully analyzed in real time, which points to a large remaining opportunity for local visual inference frameworks. For the edge AI software market, this means visual workloads still anchor current revenue because they connect directly to established enterprise spending categories such as quality control, safety monitoring, and automated inspection.

Other data modalities are also expanding because end users are broadening the kinds of information they want to process locally. Text and language data support human-machine interfaces and local conversational functions, while environmental and location data are tied to monitoring, routing, and infrastructure use cases. Multimodal AI has become strategically important because enterprises increasingly want a single stack that can interpret several inputs at once without relying on separate models for each data stream. NVIDIA’s Nemotron 3 Nano Omni model, released in May 2026, combined vision, language, and audio perception in one compact model designed for agentic edge workloads, which reflected this shift toward more unified inference architectures. The edge AI software market is gaining from this because multimodal models can simplify operational complexity when customers need richer local context but cannot support multiple full software stacks on constrained devices.

Auditory data is projected to grow at a 26.88% CAGR through 2031, which makes it the fastest-growing modality in the edge AI software market. The strongest demand is coming from audio anomaly detection in rotating machinery, voice-command interfaces in warehouse robotics, and conversational systems that need local responsiveness in healthcare and banking settings. Audio workloads also carry a cost advantage because the models are often smaller than comparable visual systems and can therefore run on more modest hardware footprints. That lowers deployment barriers for industrial original equipment manufacturers that already have installed MCU-class devices across large endpoint fleets. Over time, the edge AI software industry is likely to see auditory and multimodal use cases become more important because they offer practical performance gains without requiring the larger compute budgets that visual inference often demands.

By Deployment Mode: Cloud Orchestration Leads As On-Premises Urgency Grows

Cloud deployment led with 48.24% of the edge AI software market size in 2025, although that leadership mainly reflects where orchestration and governance are managed rather than where inference actually happens. In most production settings, the cloud functions as the control plane for model versioning, rollout governance, and telemetry aggregation across distributed nodes. That arrangement fits the current state of the edge AI software market because enterprises still want centralized observability even when the actual AI task runs locally on a device or gateway. Hybrid architectures have therefore become common, with local inference at the edge and retraining, validation, or analytics running in cloud or data center environments. ZEDEDA reported in 2026 that 47% of enterprises had adopted hybrid cloud-edge architectures, which aligns with the broader pattern of data gravity keeping inference close to the source while management remains more centralized.

On-premises deployment is projected to expand at a 25.73% CAGR through 2031, making it the fastest-growing mode in the edge AI software market. That growth is being driven by sovereign data requirements, air-gapped operations in defense and critical infrastructure, and the economics of high-volume inference workloads that become expensive under recurring cloud usage. IBM’s May 2026 launch of IBM Sovereign Core directly addressed this need by embedding AI execution in sovereign on-premises environments with governance and compliance controls built into the platform. Regulatory expectations are making that model more attractive because organizations can document, control, and audit workloads more easily inside controlled infrastructure than in shared multi-tenant environments. For the edge AI software market, this creates a clear pattern where cloud-led orchestration remains important, but on-premises stacks are gaining urgency whenever data residency, security, or operational independence becomes part of the approval process.

The edge AI software market is therefore not moving toward a single deployment architecture. Instead, the market is settling into a mixed model where cloud, hybrid, and on-premises choices serve different operational needs. Cloud still leads because centralized fleet management remains useful across widely distributed assets. Hybrid remains common because it balances local responsiveness with centralized control. The edge AI software industry is likely to keep this mixed structure over the forecast period because no single deployment mode resolves latency, cost, governance, and sovereignty requirements equally well across all end users.

By End-User Industry: Manufacturing Anchors Volume As Automotive Leads Growth

Manufacturing accounted for 20.99% of the edge AI software market size in 2025, which made it the largest end-user vertical. That position reflects years of investment in Industry 4.0 programs, machine vision inspection, predictive maintenance, and real-time process control across large factory networks. The edge AI software market has found a natural fit in manufacturing because plants often generate continuous data streams that need immediate interpretation close to the production line. Cognex provided a visible example in May 2026 when it stated that its OneVision platform had gained more than 100 customers globally since beta launch, with several customers moving from single-line pilots to multi-site rollouts. That pattern shows that the edge AI software market is no longer driven only by proof-of-concept activity in factories, and it is increasingly tied to broader operational scaling decisions.

The remaining demand is spread across information technology and telecommunications, healthcare and life sciences, retail and consumer goods, energy and utilities, smart cities and public infrastructure, and banking, financial services, and insurance. Each of those sectors uses local AI for a distinct reason, including network anomaly detection, wearable diagnostics, in-store responsiveness, grid monitoring, traffic management, and fraud checks at branch or kiosk level. This creates a broad customer base for the edge AI software market, but the operational logic differs by vertical, so vendors still need domain-specific functionality. In practice, that favors providers that can support both common AI lifecycle tools and industry-specific deployment conditions. It also helps explain why the edge AI software market remains moderately fragmented, since no single software design fits every regulated or distributed use case equally well.

Automotive and transportation is projected to grow at a 27.12% CAGR through 2031, making it the fastest-growing end-user segment in the edge AI software market. That pace reflects the commercial rise of software-defined vehicles, where advanced driver-assistance, cabin intelligence, and local decisioning depend on on-vehicle inference stacks. Visteon launched an edge-to-cloud AI arbitration architecture in March 2026 with NVIDIA, designed to distribute workloads between on-device hardware and cloud infrastructure based on latency, privacy, and connectivity conditions. STMicroelectronics also introduced Stellar P3E in 2026 as an automotive microcontroller with dedicated AI acceleration supported by the ST Edge AI Suite, showing how software tooling is being embedded directly into automotive-grade silicon platforms. Safety requirements are also becoming more formal, and ISO/PAS 8800 is giving software vendors a clearer path to automotive AI certification, which matters for access to original equipment manufacturer supply chains.

Geography Analysis

North America held 34.78% of the edge AI software market share in 2025, which kept it as the largest regional contributor. The region benefits from a dense concentration of hyperscaler platforms and industrial technology vendors, and that gives enterprise buyers earlier access to full-stack deployment options than most other regions. The edge AI software market also gains in North America from mature enterprise software procurement cycles, where large organizations are more willing to fund multi-site deployments after pilot validation. HPE’s AI Grid launch in March 2026 and Comcast’s field trials for distributed edge inferencing show that deployment activity is spreading beyond factories and into communications infrastructure and consumer service delivery networks. IBM’s May 2026 launch of Sovereign Core also reflects a procurement environment where digital sovereignty and operational control are influencing both government and regulated enterprise demand.

Asia-Pacific is projected to expand at a 26.71% CAGR through 2031, which makes it the fastest-growing regional segment in the edge AI software market. That momentum is being supported by China’s manufacturing scale, Japan’s robotics and automotive programs, India’s engineering base, and South Korea’s semiconductor ecosystem. Nikkei reported in March 2026, citing Fuji Chimera Sogo Kenkyusho research, that AI agents and edge-based physical AI inference were expected to push market expansion in Japan from 2026 onward, with the edge environment gaining importance for both privacy protection and AI agent commercialization. This growth profile matters because the edge AI software market in Asia-Pacific is tied both to large industrial deployment volumes and to local design ecosystems that can embed AI functions closer to the device layer. It also means regional vendors and global suppliers are competing in a setting where cost efficiency, localization, and hardware alignment matter as much as software features.

Europe continues to hold a meaningful share of the edge AI software market because the region combines a strong industrial base with a regulatory environment that pushes buyers toward more controlled AI deployment models. Deutsche Telekom’s European Edge Continuum moved into live lab and pre-production status in 2025 and continued toward commercial rollout in 2026, which supports Europe’s digital sovereignty agenda through a federated and interoperable edge infrastructure layer. Cisco also highlighted Audi’s Edge Cloud 4 Production deployment with Siemens at the Böllinger Höfe factory in March 2025, bringing virtualized software-defined automation and AI-driven process control into European automotive manufacturing. These examples show why the edge AI software market in Europe remains tied to industrial modernization, data control, and sovereign infrastructure priorities. South America, the Middle East and Africa, and Turkey are smaller in current scale, but they still matter because investment in agriculture, financial inclusion, smart cities, logistics, and energy control is creating selective demand for local AI execution. In those regions, adoption is often shaped by mobile-first connectivity and national digital infrastructure programs rather than by broad enterprise standardization.

Competitive Landscape

The edge AI software market shows a moderately fragmented competitive structure, with hyperscalers such as AWS, Google, and Microsoft competing alongside industrial software providers, hardware-linked platform vendors, and a smaller group of pure-play specialists. No single vendor controls the full market because buyers value different combinations of orchestration, interoperability, domain expertise, and hardware alignment. NVIDIA holds a strong cross-stack position because it packages software frameworks such as Metropolis and TensorRT Edge-LLM with its silicon portfolio, which lets it influence both deployment tooling and hardware selection at the same time. That approach narrows the room for stand-alone software vendors that cannot offer similar performance integration or ecosystem reach. In the edge AI software market, this has intensified competition around stack ownership rather than only around individual software features.

Qualcomm’s March 2025 agreement to acquire Edge Impulse is a clear example of that direction because it linked an end-to-end edge AI software platform with Qualcomm’s processor and AI Hub ecosystem. NXP’s February 2025 agreement to acquire Kinara followed a related pattern by pairing discrete neural processing capabilities with its industrial and automotive processor portfolio in order to build a more vertically integrated edge inference platform. ZEDEDA took the opposite route in March 2026 by launching its Edge Intelligence Platform as a hardware-agnostic control plane designed to create, secure, and operate edge and physical AI across large fleets. The edge AI software market therefore contains both vertically integrated challengers and neutral orchestration providers, and that division is likely to remain central to competitive positioning.

White space remains strongest in certifiable stacks for safety-critical deployments, hardware-agnostic MLOps across mixed fleets, and non-visual sensor-fusion software where the installed base is large but commercial tooling is still limited. Ferrous Systems’ December 2025 IEC 61508 SIL 2 certification for the Ferrocene Rust toolchain showed continued movement toward certifiable software foundations for industrial, automotive, and medical environments that require formal safety pathways. Latent AI has focused on that kind of constrained and regulated deployment environment, and its February 2026 work with Sigma Defense and Abaco Systems highlighted interoperable defense edge AI built around modular open systems requirements. ClearBlade remains relevant in industrial IoT settings because multi-protocol bridging is still important where legacy operational technology must connect with modern inference pipelines, even though the largest players tend to prioritize their own ecosystems. The edge AI software market is therefore competitive, but not fully consolidated, because buyers still need specialized software for domains that large platform vendors do not yet address with sufficient depth.

Edge AI Software Industry Leaders

Amazon Web Services, Inc.

Google LLC

Microsoft Corporation

International Business Machines Corporation

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IBM announced the general availability of Red Hat AI Inference on IBM Cloud and IBM Sovereign Core, a software platform embedding AI execution within sovereign on-premises environments with built-in governance, compliance, and AI lifecycle controls, targeting governments and regulated enterprises requiring operational independence from shared cloud infrastructure.

- May 2026: BrainChip entered an IP distribution license agreement with ASICLAND, granting a non-exclusive worldwide license to incorporate Akida neuromorphic AI IP into custom system-on-chip designs across edge AI, industrial, automotive, consumer, and IoT market segments.

- April 2026: Siemens announced major expansions to its Industrial Edge ecosystem at Hannover Messe 2026, including the general availability of the Industrial AI Suite covering the full AI lifecycle, expanded Industrial Edge Management v2.0 with OpenShift and Hyper-V hypervisor support, and IEC 62443-4-2-certified security functions targeted for H2 2026, collectively positioning Siemens Industrial Edge as a primary platform for IT and OT convergence in manufacturing.

- March 2026: ZEDEDA unveiled its Edge Intelligence Platform at NVIDIA GTC 2026, described as the first solution capable of creating, deploying, securing, and operating edge AI at scale in a single control plane, built on an orchestration foundation managing tens of thousands of edge nodes globally, with Edge Inference Services reducing model deployment from weeks to minutes.

Global Edge AI Software Market Report Scope

The Edge AI Software Market refers to software platforms, frameworks, and services that enable AI models to run on edge devices close to where data is generated, instead of depending only on centralized cloud systems. The market is driven by the rapid spread of IoT endpoints, industrial automation, smart manufacturing, autonomous systems, and privacy-sensitive workloads that benefit from local decision-making.

The Edge AI Software Market Report is Segmented by Offering (Solutions and Services), Data Modality (Visual Data, Auditory Data, Text and Language Data, Environmental and Location Data, and Multimodal Data), Deployment Mode (Cloud, On-premises, and More), End-User Industry (Manufacturing, Information Technology and Telecommunications, Healthcare and Life Sciences, Automotive and Transportation, Retail and Consumer Goods, Energy and Utilities, Smart Cities and Public Infrastructure, and Banking, Financial Services, and Insurance), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Visual Data |

| Auditory Data |

| Text and Language Data |

| Environmental and Location Data |

| Multimodal Data |

| Cloud |

| On-premises |

| Hybrid |

| Manufacturing |

| Information Technology and Telecommunications |

| Healthcare and Life Sciences |

| Automotive and Transportation |

| Retail and Consumer Goods |

| Energy and Utilities |

| Smart Cities and Public Infrastructure |

| Banking, Financial Services, and Insurance |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Offering | Solutions | |

| Services | ||

| By Data Modality | Visual Data | |

| Auditory Data | ||

| Text and Language Data | ||

| Environmental and Location Data | ||

| Multimodal Data | ||

| By Deployment Mode | Cloud | |

| On-premises | ||

| Hybrid | ||

| By End-user Industry | Manufacturing | |

| Information Technology and Telecommunications | ||

| Healthcare and Life Sciences | ||

| Automotive and Transportation | ||

| Retail and Consumer Goods | ||

| Energy and Utilities | ||

| Smart Cities and Public Infrastructure | ||

| Banking, Financial Services, and Insurance | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the edge AI software market?

The edge AI software market was valued at USD 1.82 billion in 2025, stands at USD 2.25 billion in 2026, and is forecast to reach USD 6.82 billion by 2031 at a 24.83% CAGR.

What is driving demand for edge AI software solutions?

Demand is being driven by rising IoT endpoint data volumes, the need for low-latency decisioning, stronger privacy requirements, and wider use of distributed 5G architectures.

Which region leads edge AI software adoption today?

North America led in 2025 with a 34.78% share, supported by strong enterprise procurement, a dense vendor base, and sovereign AI demand in regulated environments.

Which region is growing fastest through 2031?

Asia-Pacific is projected to grow the fastest at a 26.71% CAGR, supported by manufacturing scale in China, robotics and automotive programs in Japan, engineering depth in India, and semiconductor strength in South Korea.

Which end-user segment is the largest in edge AI software?

Manufacturing was the largest end-user segment in 2025 with a 20.99% revenue share, reflecting strong use of AI vision, predictive maintenance, and real-time process control on factory floors.

Which deployment model is expanding the fastest?

On-premises deployment is projected to grow at a 25.73% CAGR through 2031 as sovereign data rules, air-gapped operations, and cloud cost concerns push more inference workloads into controlled local environments.

Page last updated on: