AI Accelerator Memory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

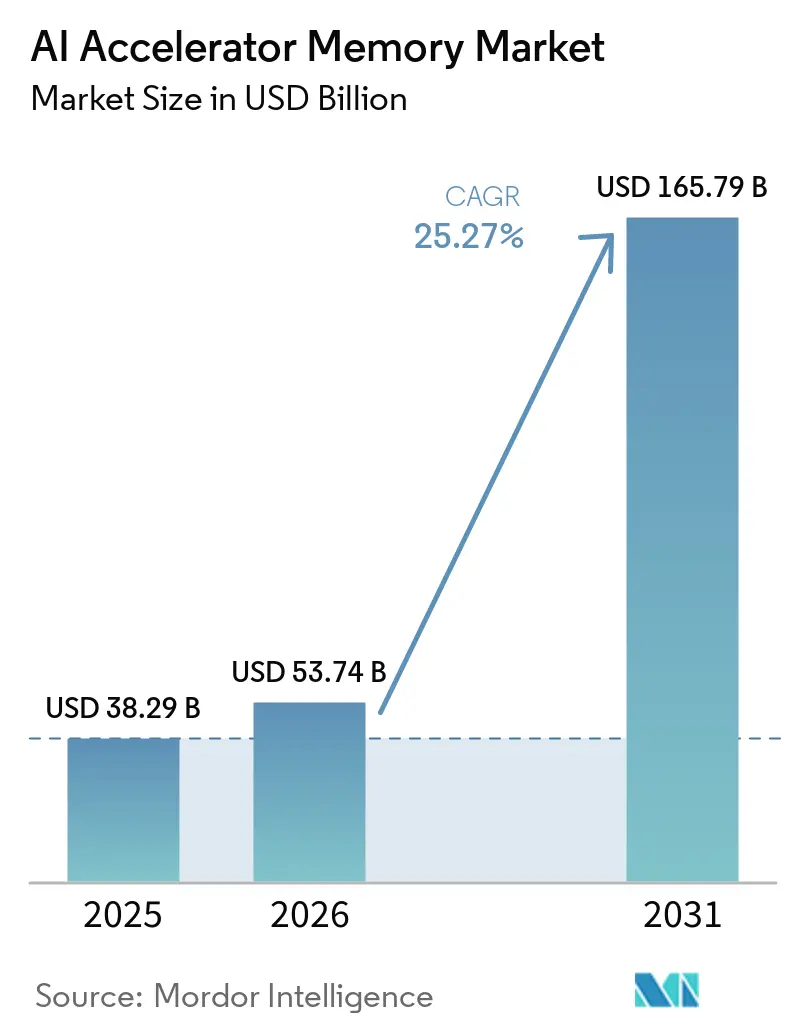

| Market Size (2026) | USD 53.74 Billion |

| Market Size (2031) | USD 165.79 Billion |

| Growth Rate (2026 - 2031) | 25.27% CAGR |

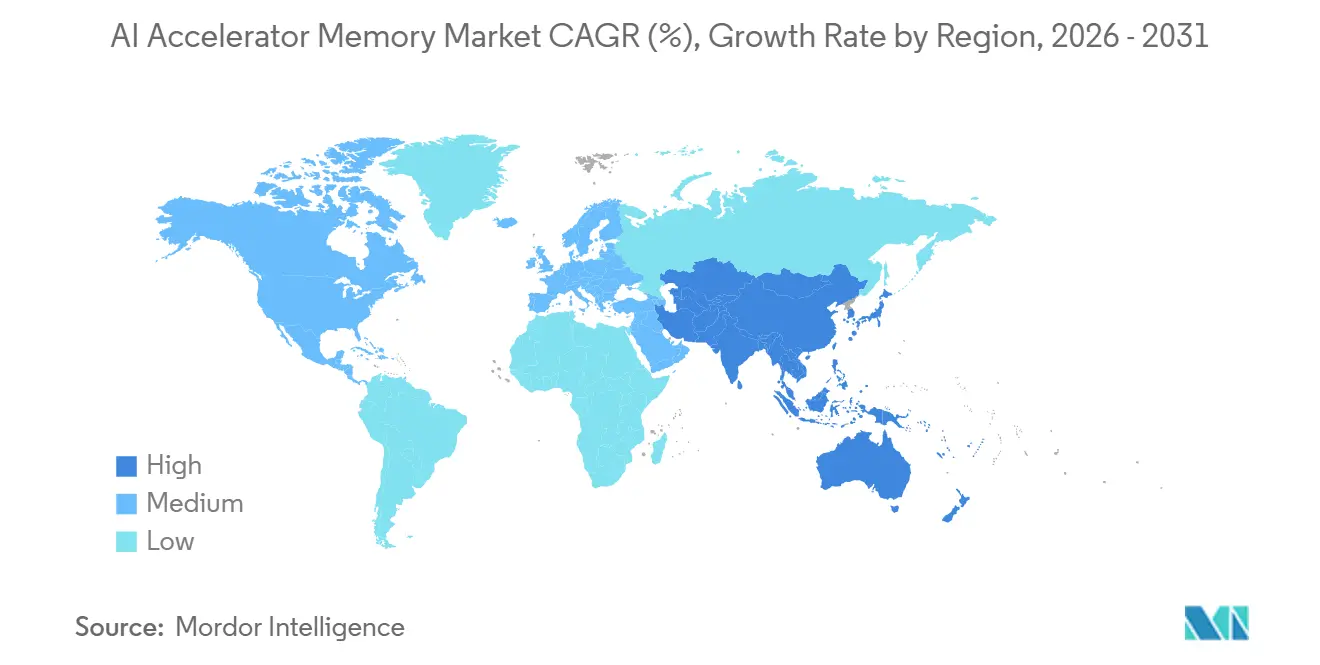

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

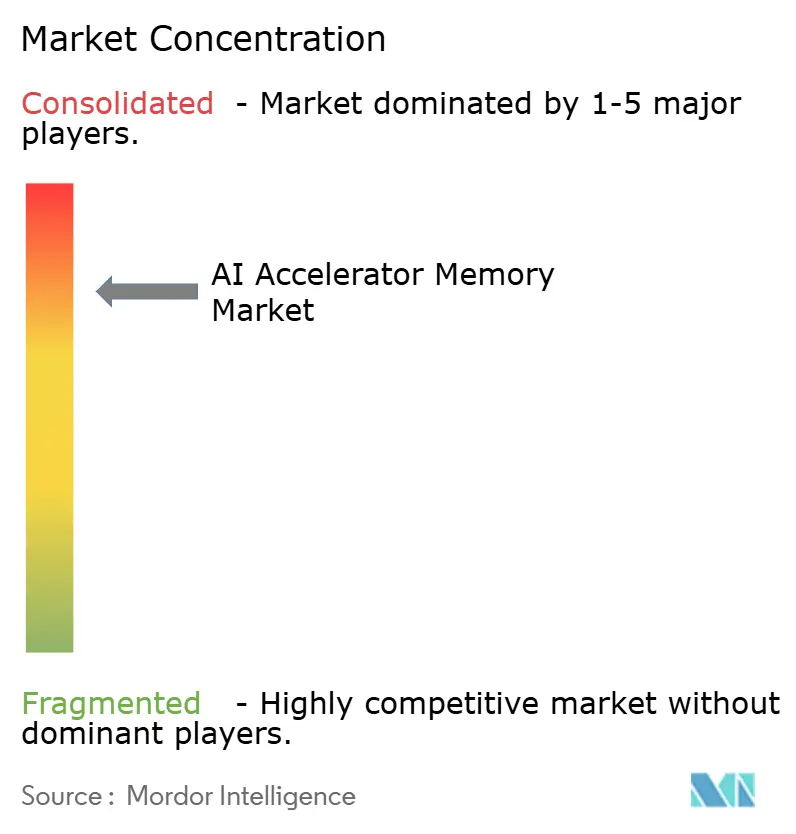

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Accelerator Memory Market Analysis by Mordor Intelligence

The AI accelerator memory market size is expected to grow from USD 38.29 billion in 2025 to USD 53.74 billion in 2026 and is forecast to reach USD 165.79 billion by 2031 at 25.27% CAGR over 2026-2031. The AI accelerator memory market is being shaped by the lock-in of high-bandwidth memory across leading training and inference accelerators, which has made memory architecture a core design constraint rather than a supporting component. The AI accelerator memory market is also being lifted by hyperscale spending that continues to favor large AI server fleets, custom silicon programs, and dense rack-scale systems with high memory content per accelerator. Supply discipline is equally important because the three leading DRAM suppliers have shifted capital, engineering effort, and product mix toward HBM products with better margins and stronger long-term demand visibility. That shift has made the AI accelerator memory market more concentrated on both the supply and demand sides, as a small set of memory vendors and hyperscale buyers now shape most allocation decisions. The strongest near-term opportunities are tied to newer HBM generations, higher stack heights, and edge inference platforms, while the main risk remains the pace at which packaging, thermal control, and qualification capacity can keep up with demand.

Key Report Takeaways

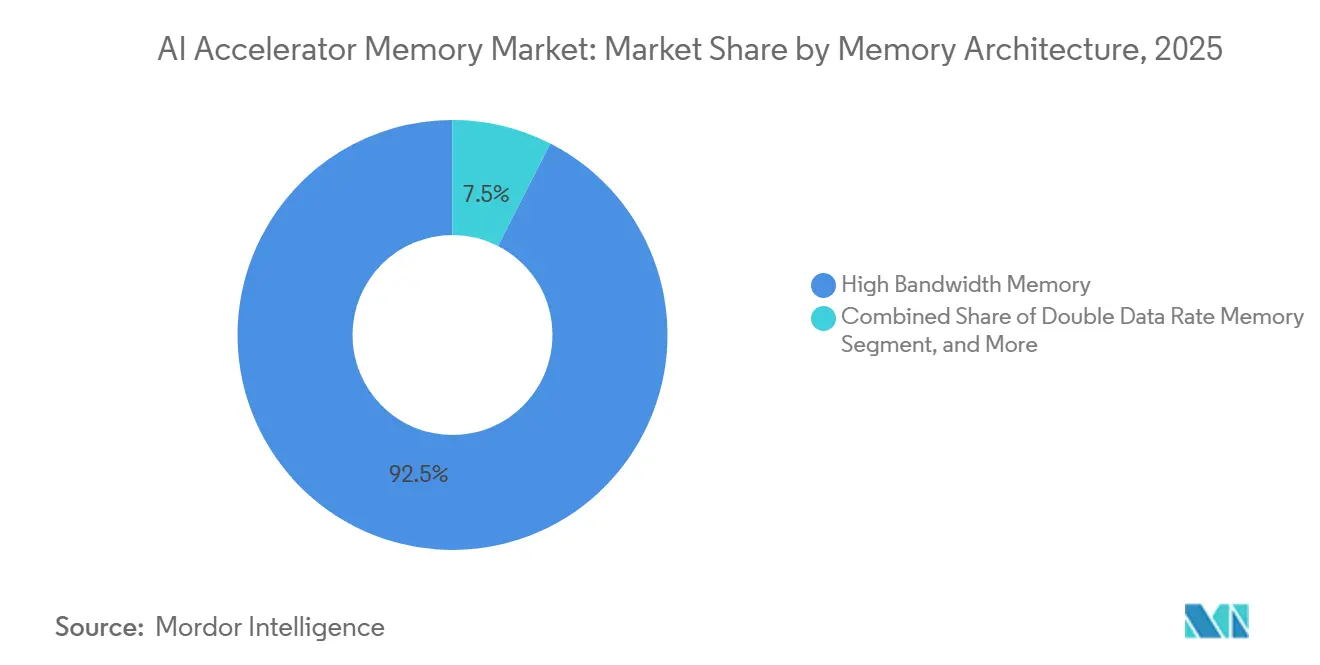

- By memory architecture, High Bandwidth Memory led with 92.48% share in 2025 of the AI accelerator memory market, while Low-Power Double Data Rate memory is projected to expand at a 26.27% CAGR through 2031.

- By accelerator platform, Data Center GPU Accelerators held 73.58% share of the AI accelerator memory market in 2025, while Custom AI ASICs and XPUs are projected to record the fastest CAGR at 26.46% through 2031.

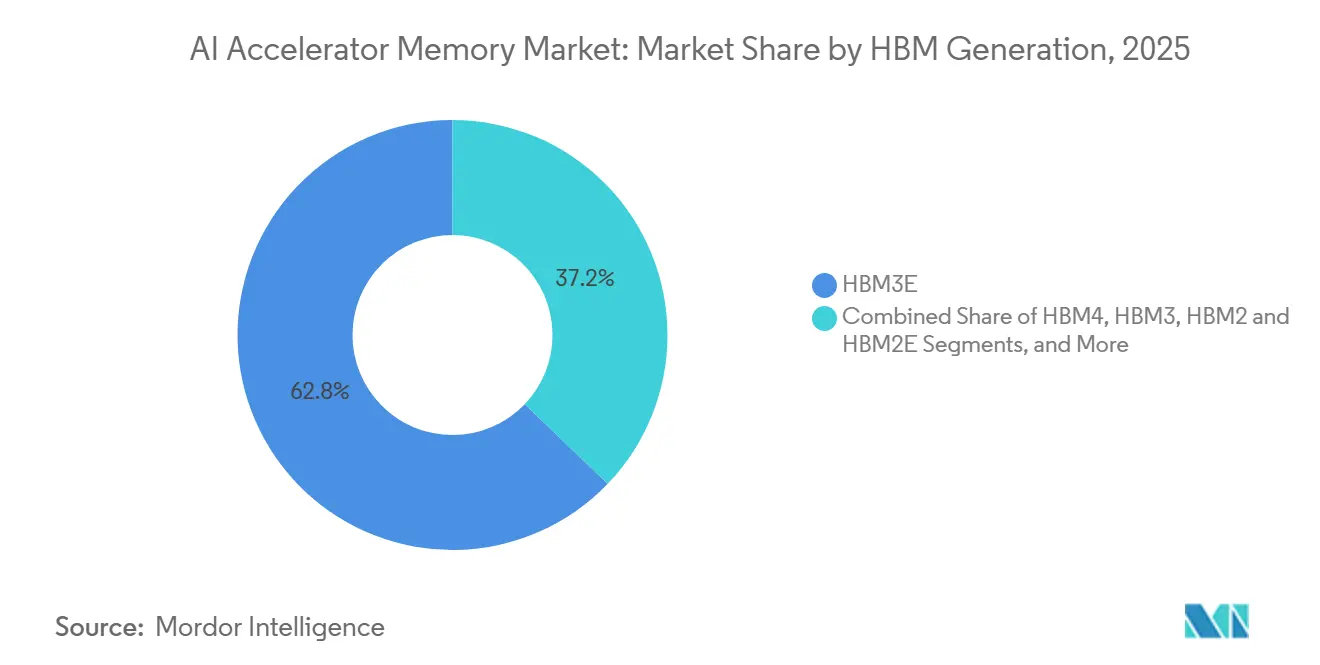

- By HBM generation, HBM3E accounted for 62.84% share in 2025, while HBM4E and Next-Generation HBM are projected to advance at a 26.18% CAGR through 2031.

- By HBM stack height, 8-High commanded 61.32% share in 2025 for the artificial intelligence (AI) accelerator memory market, while 16-High is projected to expand at a 26.13% CAGR through 2031.

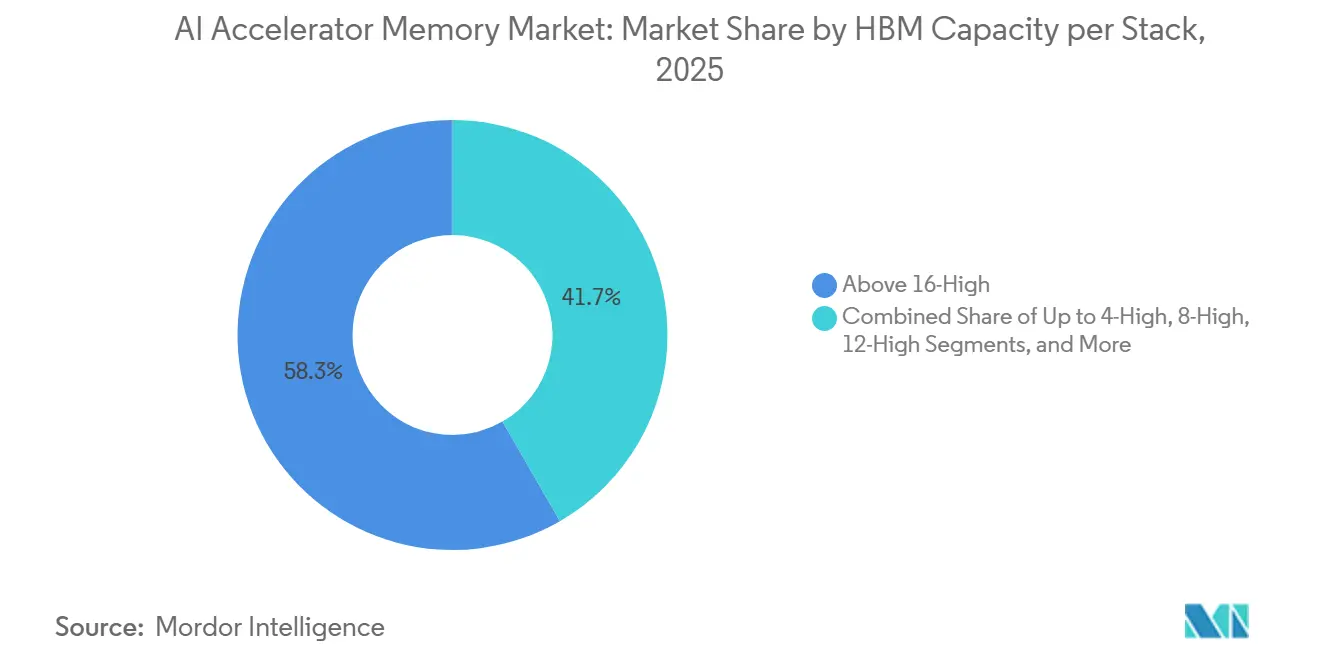

- By HBM capacity per stack, the Above 16 GB to 24 GB tier held 58.33% share of the AI accelerator memory market in 2025, while the Above 36 GB tier is projected to grow at a 26.28% CAGR through 2031.

- By deployment platform, Hyperscale Cloud and AI Factories captured 73.87% share in 2025, while Edge AI and Industrial Systems are projected to post the fastest CAGR at 26.54% through 2031.

- By geography, North America held 48.12% share of the AI accelerator memory market in 2025, while the Asia-Pacific is projected to expand at a 26.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Accelerator Memory Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of HBM3E and HBM4 in AI Accelerators | +6.2% | Global, most concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising AI Training and Inference Compute Density | +5.1% | Global | Medium term (2-4 years) |

| Expansion of Hyperscale Data Center AI Fleets | +4.3% | North America and Europe | Short term (≤ 2 years) |

| Higher Bandwidth Demand per Watt in Advanced GPUs and ASICs | +3.0% | Global | Medium term (2-4 years) |

| Supply Reallocation Toward High-Margin AI Memory SKUs | +1.5% | Asia-Pacific core, South Korea and Japan, spillover to North America | Short term (≤ 2 years) |

| Rising Adoption of Chiplet-Based AI Architectures | +1.1% | Global, early gains in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of HBM3E and HBM4 in AI Accelerators

The AI accelerator memory market is benefiting from each HBM generation upgrade because higher performance now comes with greater process complexity and higher selling prices. SK hynix stated that its HBM3E reached up to 9.6 Gbps per pin and more than 1.23 TB/s of bandwidth, underscoring why current AI accelerators continue to move toward denser, faster memory configurations. Samsung said in February 2026 that it had begun mass production of HBM4 using a 1c DRAM process and a 4 nm logic base die, signaling that the market had already begun shifting to the next qualification cycle. NVIDIA confirmed in June 2026 that Samsung, SK hynix, and Micron had all qualified and entered production for its Vera Rubin platform, reducing uncertainty around vendor readiness and widening the supply base for the next accelerator ramp. The AI accelerator memory market, therefore, moves higher not only because unit demand is rising, but also because each transition to HBM4 and HBM4E ties revenue growth to a more demanding and more expensive manufacturing path.

Rising AI Training and Inference Compute Density

The AI accelerator memory market is also being pushed by the steady rise in memory capacity and bandwidth required per chip for both training and inference. Google introduced TPU 8i in April 2026 with 288 GB of HBM and 8,601 GB/s per chip, while also tripling on-chip SRAM to 384 MB, demonstrating how memory intensity has risen in one product cycle.[1]Google Cloud Blog, “TPU 8t and TPU 8i Technical Deep Dive,” Google Cloud Blog, cloud.google.com NVIDIA's Vera Rubin platform extended that direction with a 576 GB HBM4 configuration per accelerator, indicating that long-context models and larger working sets are still pushing minimum memory requirements upward. JEDEC's LPDDR6 roadmap also showed that even edge systems are moving toward richer memory functions, including processing-in-memory support, which reflects broader pressure to reduce data movement and improve local inference efficiency. In the AI accelerator memory market, this means memory content per accelerator is rising even when model efficiency improves, because longer context windows and more complex inference pipelines continue to consume additional bandwidth and capacity.

Expansion of Hyperscale Data Center AI Fleets

The AI accelerator memory market remains closely tied to hyperscale infrastructure growth, as large cloud operators continue to account for the largest memory-intensive accelerator deployments. Amazon announced in February 2026 that it would invest USD 12 billion in Louisiana for cloud and AI infrastructure, which reflects the size of individual projects now being committed at the data center level. Google expanded its TPU roadmap in 2026, and NVIDIA deepened its multiyear memory partnership with SK hynix, which shows that compute platform roadmaps and memory supply planning are now being aligned several cycles ahead. Rack-scale system designs also intensify demand because each deployment adds much more HBM content than a conventional server refresh. This keeps the AI accelerator memory market exposed to a small number of very large buyers whose spending plans can absorb available supply before smaller enterprise customers gain access.

Higher Bandwidth Demand Per Watt in Advanced GPUs and ASICs

The AI accelerator memory market is no longer driven solely by peak bandwidth, as thermal and power limits now shape which memory configurations can be used in real deployments. Marvell announced in December 2024 that its custom HBM compute architecture could reduce memory interface power by 70%, support 33% more HBM stacks, and increase compute area by 25%, underscoring that power efficiency has become central to accelerator design. Samsung's LPDDR6 program and JEDEC's LPDDR6 roadmap both point to the same design priority at the edge, on-device AI needs higher memory performance without large power penalties. Micron's edge AI white paper also linked memory bandwidth directly to token-generation speed during decode, reinforcing why bandwidth per watt matters across both large and small AI systems. As accelerator packages approach higher thermal loads and larger stack counts, suppliers that manage power and heat more effectively will keep a pricing and qualification advantage in the AI accelerator memory market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Package-Level Thermal and Yield Constraints | -3.8% | Global, most acute at Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Limited Qualified Supply Base for Advanced HBM | -2.6% | Global | Medium term (2-4 years) |

| Heavy Dependence on Advanced Packaging Capacity | -2.0% | Asia-Pacific core, Taiwan, spillover to North America | Medium term (2-4 years) |

| Export Controls and Supply Chain Localization Friction | -1.0% | North America and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Package-Level Thermal and Yield Constraints

The AI accelerator memory market faces a significant technical constraint; thermal management becomes more difficult as layer counts rise and logic dies are integrated into the base structure. Samsung's HBM4 ramp and the industry's move to higher stack heights show that memory vendors are trying to increase density while staying within qualification and reliability limits.[2]Samsung Semiconductor Global Newsroom, “Samsung Begins Mass Production of Industry’s First 12-Layer HBM3E DRAM,” Samsung Semiconductor Global Newsroom, news.samsungsemiconductor.com JEDEC standards remain important because commercialization depends on meeting defined thermal and performance thresholds across successive generations. Micron and Marvell both highlighted memory architecture changes aimed at reducing data movement and interface power, confirming that the issue is not limited to raw supply volume but extends to package-level feasibility. This keeps the artificial intelligence (AI) accelerator memory market vulnerable to slower-than-expected ramps whenever new stack heights or new logic-process combinations push yields below commercial targets.

Limited Qualified Supply Base for Advanced HBM

The AI accelerator memory market is also constrained by the fact that advanced HBM supply is still concentrated among a very small group of qualified vendors. NVIDIA's June 2026 confirmation that Samsung, SK hynix, and Micron had all entered production for Vera Rubin also underscored that the qualified supply base is only now broadening within a narrow field of existing leaders. SK hynix's February 2026 approval of KRW 21.61 trillion (approximately USD 16 billion) for further Yongin cluster phases shows how large and how slow new capacity commitments are at the manufacturing level. Micron's exit from consumer memory in December 2025 reinforced the same point by redirecting resources toward AI-oriented enterprise memory rather than spreading capacity across broader end markets. In practical terms, the AI accelerator memory market can remain supply-constrained even when demand visibility is strong, since qualification lead times and capacity expansion schedules move much more slowly than accelerator order cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Architecture: HBM Dominates As LPDDR Accelerates At The Edge

HBM held 92.48% of the AI accelerator memory market share by memory architecture in 2025, which confirms that leading AI accelerators still depend on very high bandwidth and dense on-package memory. Google's Ironwood TPU deployed 8 stacks of HBM3E at 7,370 GB/s per chip, and the later TPU 8i lifted performance to 8,601 GB/s with 288 GB per chip, which shows why HBM stayed the default design choice for frontier systems. GDDR kept a role in lower-cost inference GPUs and workstation cards, where system designers still balance performance against integration cost. DDR also remained relevant for CPU-attached functions in hybrid AI servers, especially when accelerators are deployed alongside broader enterprise compute infrastructure. In the AI accelerator memory market, this wide gap between HBM and the rest of the architecture mix reflects how strongly current data center AI depends on bandwidth-intensive accelerator packages.

LPDDR is the fastest-growing sub-segment, with a 26.27% CAGR from 2026 to 2031, indicating that the next wave of demand is broadening beyond the largest data center deployments. JEDEC said its LPDDR6 roadmap adds processing-in-memory support and extends LPDDR into data centers and edge use cases, suggesting a wider role for low-power memory in AI systems that need local inference and lower energy draw. Samsung's LPDDR6 program targets AI edge systems, AI PCs, data centers, and automotive platforms, confirming that suppliers are treating LPDDR as an AI memory growth area rather than just a mobile component. Micron also linked LPDDR bandwidth directly to token-generation speed in edge AI, making memory throughput a direct performance lever outside the hyperscale cloud. The AI accelerator memory market is therefore splitting into a data center HBM core and a fast-growing edge LPDDR layer, with each architecture serving a distinct deployment model.

By Accelerator Platform: GPU Platforms Anchor Spend As Custom Silicon Accelerates

Data Center GPU Accelerators captured 73.58% of the AI accelerator memory market size in 2025, reflecting the installed base and allocation strength of mainstream training and inference GPU platforms. NVIDIA's H100, H200, and Blackwell families kept GPU platforms at the center of large-scale AI deployments, while AMD remained a meaningful secondary customer route for HBM supply through platforms such as MI455X in the next cycle. AI SoCs, NPUs, and APUs continued to serve mobile, automotive, and embedded AI, but their memory value per unit remained lower than that of large data center accelerators. FPGA-based accelerators still mattered in latency-sensitive workloads where adaptability and deterministic response times remained important. This left the AI accelerator memory market anchored by GPU-led infrastructure, even as other platform types widened the demand base.

Custom AI ASICs and XPUs are projected to grow at 26.46% CAGR through 2031, making them the fastest-growing platform segment in the AI accelerator memory market. Broadcom said in February 2026 that it began shipping the first 2 nm custom compute SoC on its 3.5D XDSiP architecture, with support for multiple HBM stacks, demonstrating how custom silicon is moving into advanced heterogeneous packaging earlier and faster.[3]Broadcom Inc., “Broadcom Ships 3.5D Face-to-Face Compute SoC Powering AI Revolution,” Broadcom Investor Relations, investors.broadcom.com AWS Trainium, Google TPU 8, and Meta MTIA 500 indicate that hyperscalers are increasingly designing their memory needs around workload-specific bandwidth and latency targets rather than accepting a standard GPU template. Marvell's custom HBM compute architecture also supports more HBM stacks per XPU with lower interface power, which makes tailored memory interfaces a competitive design feature for custom accelerators. As that shift continues, the AI accelerator memory market will see a broader mix of qualification paths and product-specific HBM configurations than it did in the prior GPU-dominated cycle.

By HBM Generation: HBM3E Leads Current Deployments As HBM4E Defines The Next Architecture

HBM3E accounted for 62.84% of the AI accelerator memory market in 2025, which reflects its role in the current wave of installed accelerator platforms. It was deployed across NVIDIA Blackwell GPUs, Google Ironwood TPU, and AMD MI300 and MI350 series products, making it the commercial center of present HBM demand. SK hynix said its HBM3E delivers more than 1.23 TB/s, while Micron's 24 GB 8-High HBM3E also exceeded 1.2 TB/s in NVIDIA H200 systems, which explains why HBM3E remained the dominant bridge between today's infrastructure and tomorrow's platforms. HBM2 and HBM2E continued to decline as newer deployments increasingly require higher bandwidth, greater capacity, and stronger power efficiency. The AI accelerator memory market, therefore, continued to rely on HBM3E as the leading commercial generation while buyers and suppliers prepared for the next handoff.

HBM4E and Next-Generation HBM are projected to grow at a 26.18% CAGR through 2031, making them the fastest-rising generational layers in the AI accelerator memory market. SK hynix shipped 12-layer HBM4E samples with 48 GB capacity in June 2026 and reported more than a 20% power-efficiency improvement over HBM4, signaling that suppliers are already positioning for post-Vera Rubin accelerator needs. Samsung also moved HBM4 into mass production and accelerated early HBM4E sampling, suggesting that the next cycle will be defined by how quickly suppliers convert technology readiness into stable volume output. The doubling of I/O count and the use of logic-process base dies raise the value of each stack, but they also raise the burden on qualification and packaging. For that reason, the AI accelerator memory market will likely see HBM4E shape the premium end of demand well before capacity becomes easy.

By HBM Stack Height: 8-High Commands Majority Share As 16-High Gains Momentum

The 8-High configuration held a 61.32% share in 2025, making it the largest stack-height category in the AI accelerator memory market. This reflected maturity, yield stability, and the installed base of HBM3E deployments in current AI server fleets. Most H200 and Blackwell B200 generation systems were aligned with 8-High stacks at 24 GB capacity, which kept the format commercially dominant across active rollouts. The 12-High format expanded through products such as Micron's 36 GB 12-layer HBM3E, which already showed that buyers were willing to move higher when the added capacity supported clear workload gains. Up to 4-High stacks remained relevant only in lower-performance or legacy inference cards where cost efficiency mattered more than memory density.

The 16-High segment is projected to grow at a 26.13% CAGR through 2031, making it the fastest-growing stack-height tier in the AI accelerator memory market. NVIDIA's Vera Rubin platform specifies HBM4 in a 16-High configuration with 576 GB of total capacity per accelerator, creating a direct pull for this format as next-cycle deployments scale. SK hynix's HBM4E sampling and future HBM5 work also show that suppliers are pushing toward even greater stack density, but each step raises thinning, bonding, and thermal challenges. That means commercial growth at the high end will depend not only on accelerator demand, but also on how quickly process stability improves at advanced stack heights. The artificial intelligence (AI) accelerator memory market is therefore likely to keep its largest installed base in mature formats, while its fastest revenue growth shifts to taller stacks.

By HBM Capacity Per Stack: Mid-Tier 24 GB Leads As Ultra-High Capacity Targets Next Platforms

The Above 16 GB to 24 GB tier led with a 58.33% share in 2025, placing it at the center of the AI accelerator memory market for current-generation systems. This tier matched the cost-performance profile of mainstream AI server deployments, especially where 8-High HBM3E remained the practical standard. Micron's 24 GB 8-High HBM3E used in NVIDIA H200 systems illustrates why this tier has become the commercial sweet spot for active infrastructure buildouts. The 8 GB to 16 GB range remained useful for mid-range inference and FPGA settings, but it no longer met the minimum capacity requirements of leading production AI workloads. Up to 8 GB continued to lose relevance as training and long-context inference raised the capacity floor materially.

The Above 36 GB tier is projected to grow at 26.28% CAGR through 2031, making it the fastest-growing capacity band in the AI accelerator memory market. SK hynix shipped 48 GB HBM4E samples in June 2026, and Samsung's HBM4E efforts also centered on 48 GB capacity, indicating that suppliers now view this capacity as a core target for next-generation accelerator programs. Rising context lengths, richer agent behavior, and larger multimodal workloads are all increasing the need for larger KV caches and larger per-stack memory budgets. That pressure supports a shift toward ultra-high-capacity HBM even before it becomes the broad market standard. As a result, the AI accelerator memory market is expected to maintain its current revenue base in mid-tier capacity as future platform designs continue to pull demand upward.

By Deployment Platform: Hyperscale Anchors Volume As Edge AI Diversifies Demand

Hyperscale Cloud and AI Factories held 73.87% of the AI accelerator memory market share in 2025, which made them the dominant deployment setting by a wide margin. A single NVIDIA GB200 NVL72 rack integrates more than 19 TB of HBM3E across 72 Blackwell GPUs, showing how rack-scale system design multiplies memory demand far beyond a traditional server format. Enterprise and on-premise data centers formed the next layer of demand as organizations built inference clusters to meet data-residency and control requirements. High-performance computing and research systems remained important for scientific AI and defense-related use cases that still depend on dense accelerator clusters. Networking and telecommunications infrastructure also expanded its memory needs as AI workloads moved closer to the network edge.

Edge AI and Industrial Systems are projected to grow at a 26.54% CAGR through 2031, making them the fastest-growing deployment segment in the AI accelerator memory market. Micron's edge AI white paper showed that memory bandwidth directly affects inference latency and token generation speed in smaller language models, which helps explain why memory design matters so much outside the cloud. Samsung's LPDDR6 positioning for AI PCs, automotive, and edge systems points to the same demand pattern, where local inference needs stronger memory performance without the cost and power profile of full HBM integration. Automotive AI also adds qualification requirements that lengthen design cycles and make memory selection more strategic than in mainstream consumer devices. This means the AI accelerator memory market will remain hyperscale-led in terms of value, but its fastest diversification will come from edge systems that need more local processing and stricter deployment controls.

Geography Analysis

North America held 48.12% of the AI accelerator memory market in 2025, maintaining its position as the leading regional demand center. The region's lead came from the concentration of hyperscale buyers, custom silicon programs, and large AI server deployments rather than from memory manufacturing capacity alone. Amazon's February 2026 decision to invest USD 12 billion in Louisiana showed the scale of single-project commitments that continue to shape regional hardware demand. Google also expanded its TPU roadmap in 2026, reinforcing North America's role as the primary early-deployment zone for memory-intensive accelerators. Canada supported regional growth through favorable power conditions for data centers, while Mexico gained attention as a nearshore infrastructure corridor for future AI buildouts.

Asia-Pacific is projected to grow at 26.19% CAGR through 2031, making it the fastest-growing region in the AI accelerator memory market. The region plays a dual role as both the manufacturing base for advanced HBM and a rising center of demand for AI infrastructure. South Korea remained central through the fab networks of SK hynix and Samsung, while Micron's Hiroshima site added an important production node in the broader Pacific supply chain. SK hynix's KRW 21.61 trillion (approximately USD 16 billion) Yongin cluster approval in February 2026 showed how heavily the region is investing in future memory output. Japan contributed advanced packaging capabilities, and India and Southeast Asia continued to build demand through AI cloud expansion, AI PC adoption, and local inference deployments.

Europe, South America, the Middle East, and Africa remained smaller in current share, but each added strategic demand for the artificial intelligence (AI) accelerator memory market. Germany and the United Kingdom led European AI server deployments, while public initiatives such as France 2030 continued supporting domestic compute capacity. The EU AI Act also encouraged more local infrastructure planning because compliance and data control now influence where enterprise AI workloads are hosted. The Middle East and Africa gained importance through sovereign AI cluster procurement in Saudi Arabia and the UAE, supported by export frameworks and cross-border technology agreements. South America remained earlier in its cycle, but Brazil and Chile continued laying the groundwork for future regional AI infrastructure expansion.

Competitive Landscape

The AI accelerator memory market operated with a highly concentrated supply structure in 2026 because advanced HBM production remained concentrated among SK hynix, Samsung Electronics, and Micron Technology. Demand was also concentrated because NVIDIA, AMD, and large hyperscalers shaped which memory suppliers received qualification and allocation for the biggest accelerator programs. NVIDIA and SK hynix announced a multiyear technology partnership in June 2026 to advance memory for AI factories, which showed how closely memory roadmaps are now tied to platform roadmaps.[4]NVIDIA Investor Relations, “NVIDIA and SK hynix Announce Multiyear Technology Partnership to Advance Memory for AI Factories,” NVIDIA Investor Relations, investor.nvidia.com Samsung pursued a different path by pushing HBM4 mass production with a logic-based die and a more integrated manufacturing model, aiming to improve its position in the next qualification cycle. Micron strengthened its focus by exiting consumer memory in December 2025 and redirecting resources toward AI-oriented enterprise memory, thereby aligning its portfolio more closely with the AI accelerator memory market.

Custom silicon designers have formed a second competitive layer, increasingly influencing interface design, stack count, and qualification requirements in the AI accelerator memory market. Broadcom began shipping a 2 nm custom compute SoC on its 3.5D XDSiP platform in February 2026, demonstrating that custom accelerators are moving rapidly toward advanced HBM integration. Marvell's December 2024 custom HBM compute architecture gave hyperscalers a way to support more HBM stacks with lower interface power, shifting the competitive discussion from supply volume to interface efficiency. Google, AWS, and Meta continued to expand this custom design layer through TPU, Trainium, and MTIA programs that leverage memory tailored to workload-specific bandwidth needs. This means suppliers that can support product-specific HBM configurations and faster qualification cycles will hold an advantage beyond simple wafer output.

A third layer of competition lies in packaging and system integration, as the AI accelerator memory market depends on more than DRAM fabrication alone. Advanced packaging partners and foundry-linked assembly capacity matter because high-density HBM products cannot scale without reliable bonding and package throughput. That is why supplier strategy now includes co-engineering across memory, logic, packaging, and platform design rather than only negotiating component supply. The competitive field is still narrow, but it is becoming increasingly technical as memory vendors, accelerator designers, and packaging partners vie to secure a position in the next HBM transition.

AI Accelerator Memory Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA Corporation and SK hynix Inc. announced a multiyear technology partnership to advance next-generation memory for the global AI factory buildout, covering HBM4 and future generations. The agreement builds on co-engineering across the Blackwell and Vera Rubin GPU platforms and supports supply alignment for NVIDIA's accelerator roadmap through SK hynix's Yongin cluster capacity ramp.

- June 2026: SK hynix Inc. shipped 12-layer HBM4E samples, 48 GB capacity, up to 16 Gbps per pin, with more than 20% power efficiency improvement over HBM4, to multiple customers, advancing its originally planned H2 2026 schedule. The company targets HBM4E mass production in 2027 for post-Vera Rubin AI accelerator platforms.

- April 2026: Google LLC unveiled the 8th-generation TPU family, TPU 8t and TPU 8i, at Google Cloud Next 2026. The TPU 8i carries 288 GB of HBM at 8,601 GB/s per chip and 384 MB of on-chip SRAM, triple the prior generation. These are the first Google accelerators hosted entirely on a custom Axion ARM CPU host.

- February 2026: SK hynix Inc.'s board approved KRW 21.61 trillion (approximately USD 16 billion) in new facility investment for Phases 2 through 6 of the Yongin semiconductor cluster, running through December 2030, targeting a doubling of DRAM wafer capacity to approximately 1 million wafers per month by 2030.

Global AI Accelerator Memory Market Report Scope

The AI Accelerator Memory Market comprises memory technologies, architectures, and subsystems specifically designed to support artificial intelligence (AI), machine learning, high-performance computing (HPC), and accelerated data processing workloads. AI accelerator memory solutions provide the bandwidth, capacity, latency, and power-efficiency characteristics required to feed increasingly powerful AI accelerators with large volumes of data, enabling efficient training, inference, analytics, simulation, and generative AI operations across data center, enterprise, edge, and embedded computing environments.

The AI Accelerator Memory Market Report is Segmented by Memory Architecture (HBM, Graphics Double Data Rate Memory, Low-Power Double Data Rate Memory, Double Data Rate Memory, and Other Specialized Accelerator Memory), Accelerator Platform (Data Center GPU Accelerators, Custom AI ASICs and XPUs, AI SoCs, NPUs, and APUs, FPGA-Based Accelerators, Data Processing Units, SmartNICs, and Networking Accelerators, and Other Accelerator Platforms), HBM Generation (HBM2 and HBM2E, HBM3, HBM3E, HBM4, and HBM4E and Next-Generation HBM), HBM Stack Height (Up to 4-High, 8-High, 12-High, 16-High, and Above 16-High), HBM Capacity per Stack (Up to 8 GB, 8 GB to 16 GB, 16 GB to 24 GB, 24 GB to 36 GB, and Above 36 GB), Deployment Platform (Hyperscale Cloud and AI Factories, Enterprise and On-Premise Data Centers, High-Performance Computing and Research Systems, Networking and Telecommunications Infrastructure, Edge AI and Industrial Systems, AI Workstations and AI PCs, and Automotive AI and Autonomous Systems), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| High Bandwidth Memory (HBM) |

| Graphics Double Data Rate Memory |

| Low-Power Double Data Rate Memory |

| Double Data Rate Memory |

| Other Specialized Accelerator Memory |

| Data Center GPU Accelerators |

| Custom AI ASICs and XPUs |

| AI SoCs, NPUs, and APUs |

| FPGA-Based Accelerators |

| Data Processing Units, SmartNICs, and Networking Accelerators |

| Other Accelerator Platforms |

| HBM2 and HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| HBM4E and Next-Generation HBM |

| Up to 4-High |

| 8-High |

| 12-High |

| 16-High |

| Above 16-High |

| Up to 8 GB |

| 8 GB to 16 GB |

| 16 GB to 24 GB |

| 24 GB to 36 GB |

| Above 36 GB |

| Hyperscale Cloud and AI Factories |

| Enterprise and On-Premise Data Centers |

| High-Performance Computing and Research Systems |

| Networking and Telecommunications Infrastructure |

| Edge AI and Industrial Systems |

| AI Workstations and AI PCs |

| Automotive AI and Autonomous Systems |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Architecture | High Bandwidth Memory (HBM) | |

| Graphics Double Data Rate Memory | ||

| Low-Power Double Data Rate Memory | ||

| Double Data Rate Memory | ||

| Other Specialized Accelerator Memory | ||

| By Accelerator Platform | Data Center GPU Accelerators | |

| Custom AI ASICs and XPUs | ||

| AI SoCs, NPUs, and APUs | ||

| FPGA-Based Accelerators | ||

| Data Processing Units, SmartNICs, and Networking Accelerators | ||

| Other Accelerator Platforms | ||

| By HBM Generation | HBM2 and HBM2E | |

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| HBM4E and Next-Generation HBM | ||

| By HBM Stack Height | Up to 4-High | |

| 8-High | ||

| 12-High | ||

| 16-High | ||

| Above 16-High | ||

| By HBM Capacity per Stack | Up to 8 GB | |

| 8 GB to 16 GB | ||

| 16 GB to 24 GB | ||

| 24 GB to 36 GB | ||

| Above 36 GB | ||

| By Deployment Platform | Hyperscale Cloud and AI Factories | |

| Enterprise and On-Premise Data Centers | ||

| High-Performance Computing and Research Systems | ||

| Networking and Telecommunications Infrastructure | ||

| Edge AI and Industrial Systems | ||

| AI Workstations and AI PCs | ||

| Automotive AI and Autonomous Systems | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the AI accelerator memory space?

The AI accelerator memory market stood at USD 53.74 billion in 2026 and is forecast to reach USD 165.79 billion by 2031, growing at a 25.27% CAGR over 2026-2031.

Which memory architecture leads AI accelerator deployments today?

High Bandwidth Memory led with 92.48% share in 2025 because leading training and inference accelerators still require very high on-package bandwidth and dense memory integration.

Which accelerator platform is growing the fastest through 2031?

Custom AI ASICs and XPUs are projected to expand at a 26.46% CAGR through 2031 as hyperscalers keep designing silicon for workload-specific memory and bandwidth needs.

Why is edge deployment becoming more important for memory demand?

Edge AI and Industrial Systems are projected to grow at a 26.54% CAGR because local inference needs lower latency, stronger data control, and memory-efficient performance outside the cloud.

Which region leads demand and which region is expanding the fastest?

North America led with 48.12% share in 2025, while Asia-Pacific is projected to grow the fastest at a 26.19% CAGR through 2031 because it combines production strength with rising regional AI deployment.

What is the main constraint on near-term growth?

The main constraint is the slow ramp of advanced HBM capacity due to thermal limits, yield pressure, qualification timelines, and the narrow base of suppliers able to produce at scale.

Page last updated on: