AI Chipsets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

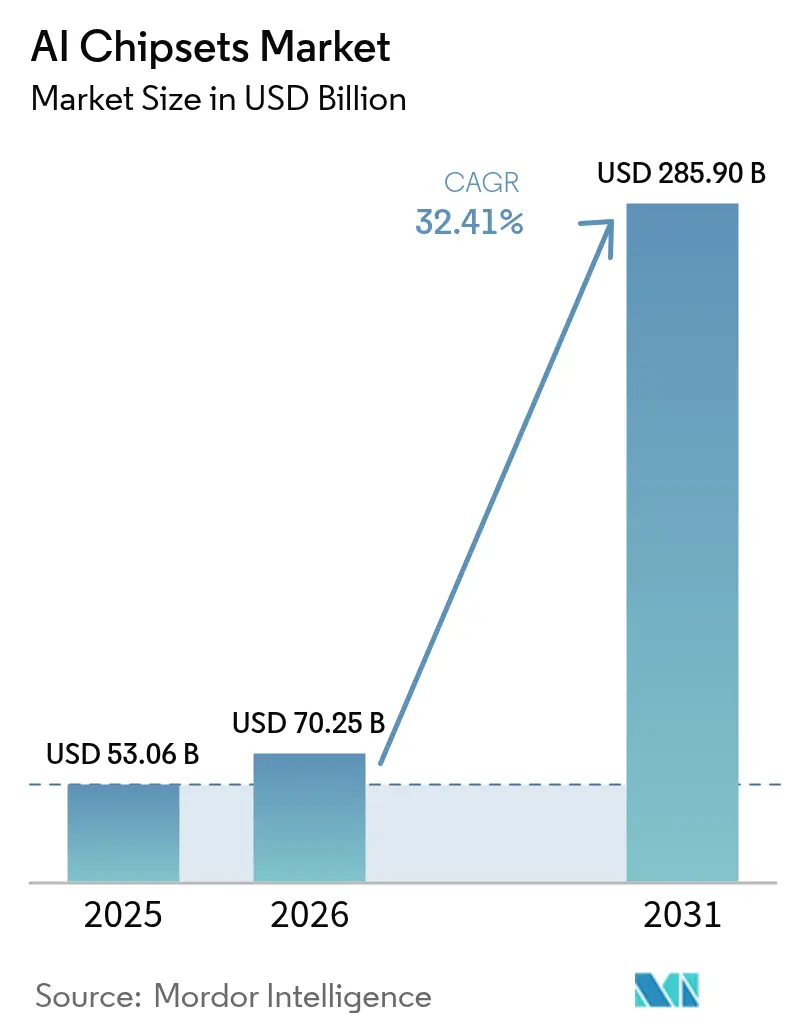

| Market Size (2026) | USD 70.25 Billion |

| Market Size (2031) | USD 285.9 Billion |

| Growth Rate (2026 - 2031) | 32.41% CAGR |

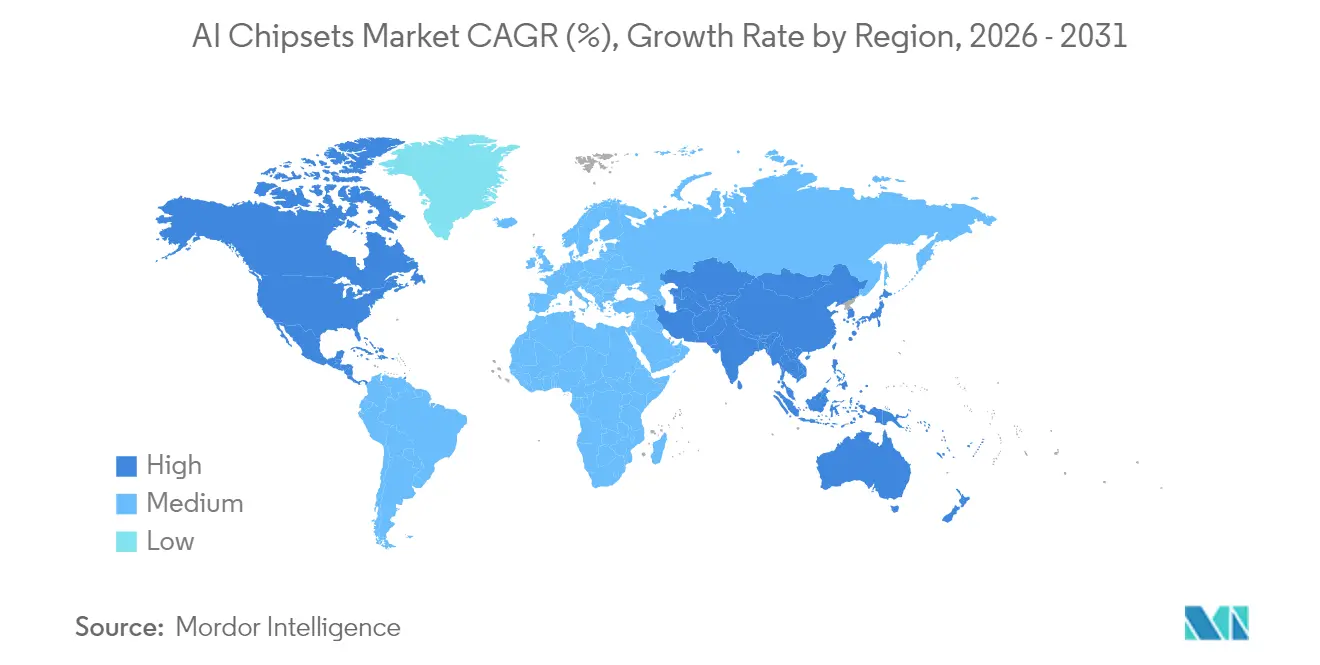

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Chipsets Market Analysis by Mordor Intelligence

AI Chipsets Market size in 2026 is estimated at USD 70.25 billion, growing from 2025 value of USD 53.06 billion with 2031 projections showing USD 285.9 billion, growing at 32.41% CAGR over 2026-2031.

Unprecedented demand for compute-intensive large language models, accelerating adoption of software-defined vehicles, and breakthroughs in ultra-low-power edge silicon are the three structural forces propelling this growth. Performance gains remain strongly tied to advanced packaging and high-bandwidth memory, yet supply constraints below the 3 nm node limit near-term output. Meanwhile, export-control ceilings, energy-efficiency mandates, and sustainability targets are reshaping sourcing decisions and favoring architectures that can deliver higher performance per watt. Market participants able to balance raw throughput with thermal efficiency and supply-chain resilience are securing long-term design wins in data-center, automotive, and edge deployments across every major region. Collectively, these dynamics position the AI chipsets market as a foundational enabler of generative AI, sovereign-cloud strategies, and on-device intelligence through 2030. [1]NVIDIA Corporation, “NVIDIA Reports Record Q1 FY2026 Results,” nvidia.com

Key Report Takeaways

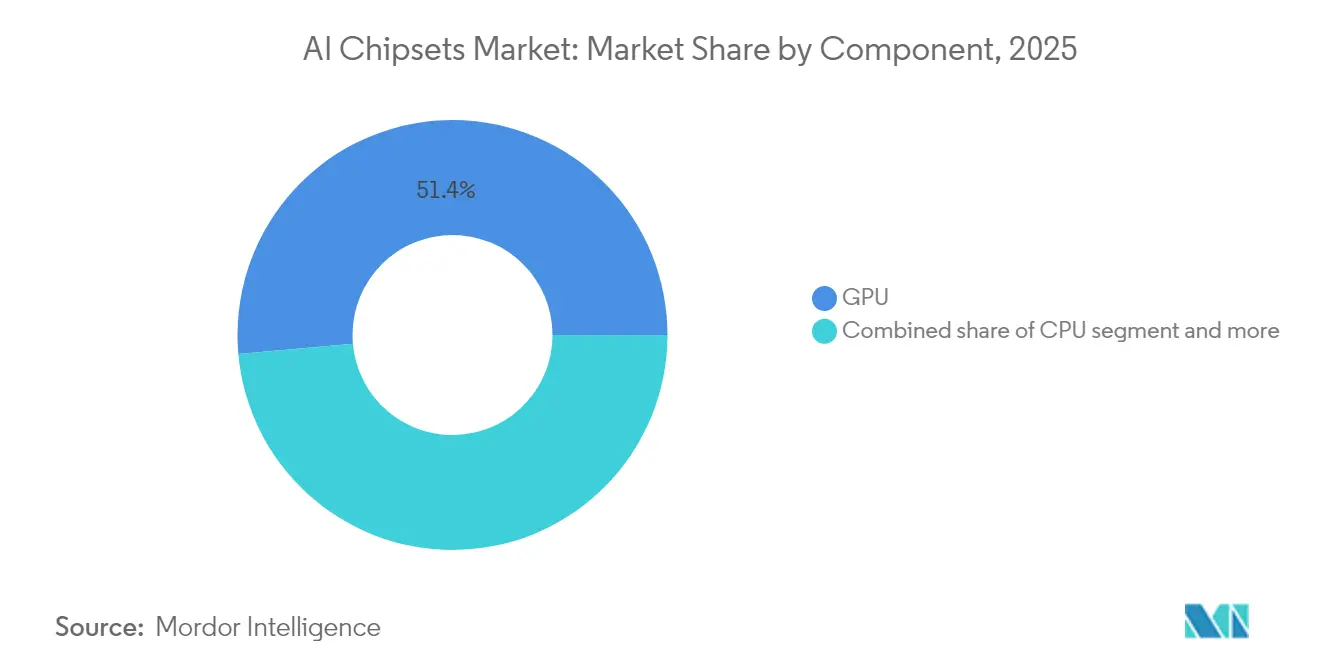

- By component, GPUs led with 51.40% of AI chipsets market share in 2025, while NPUs and ASICs are set to expand at a 44.2% CAGR through 2031.

- By processing type, training workloads commanded 60.30% share of the market size in 2025; inference is advancing at a 36.9% CAGR to 2031.

- By deployment location, cloud and hyperscale data centers held 63.10% share of the AI chipsets market size in 2025, whereas edge devices are projected to grow at a 39.2% CAGR through 2031.

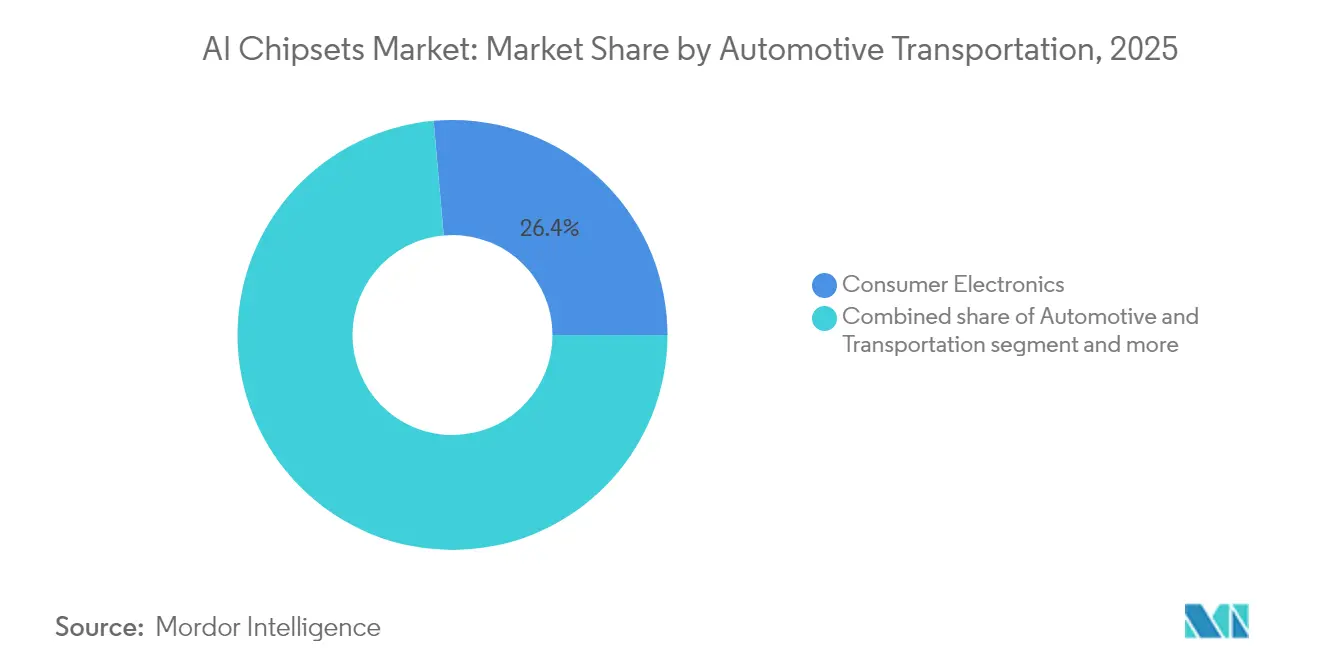

- By application, consumer electronics captured 26.40% share of the market size in 2025; automotive and transportation is forecast to post the fastest 42.6% CAGR to 2031.

- By geography, Asia-Pacific accounted for 41.10% of AI chipsets market share in 2025, while the Middle East and Africa region is expected to increase at a 34.1% CAGR through 2031.

- On the vendor front, NVIDIA, AMD, Intel, Google, and Amazon collectively controlled more than 80% of the training-accelerator market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI Chipsets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding training-compute demand from frontier-model developers | 12.50% | Global, concentrated in US, China, EU | Medium term (2-4 years) |

| Automotive "software-defined vehicle" silicon design wins | 8.20% | Global, led by Germany, US, China, Japan | Long term (≥ 4 years) |

| Ultra-low-power edge AI ASIC breakthroughs | 6.80% | Global, early adoption in Asia-Pacific, North America | Short term (≤ 2 years) |

| National AI infrastructure stimulus programs (US/China/EU) | 9.10% | US, China, EU, with spillover to allied nations | Medium term (2-4 years) |

| Open-source silicon (RISC-V) acceleration frameworks | 4.30% | Global, strongest in China, emerging in India, Europe | Long term (≥ 4 years) |

| High-bandwidth memory (HBM) technology advancements | 7.40% | Global, concentrated in South Korea, Taiwan, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Exploding Training-Compute Demand from Frontier-Model Developers

Annual compute needs for large-scale language models are increasing ten-foldev ery 18 months, driving sustained orders for multi-die GPUs and advanced packaging solutions. NVIDIA’s data-center revenue rose to USD 35.6 billion in Q4 2025 on the back of Blackwell supercomputer shipments, underscoring how hyperscale customers are accumulating vast AI-specific inventories. Multimodal model builders now require thousands of interconnected accelerators, pushing demand for CoWoS substrates and next-generation HBM stacks. As a result, leading AI companies are expected to control 15–20% of global AI-compute capacity by 2027, ensuring continuous procurement of 3 nm-class silicon. This volume concentration intensifies near-term shortages but establishes a multi-year revenue pipeline for suppliers that can execute at advanced nodes. Consequently, the AI chipsets market will benefit from a structurally higher baseline of training-oriented purchases through the forecast horizon.

Automotive "Software-Defined Vehicle" Silicon Design Wins

Automakers are consolidating scores of electronic control units into centralized AI-enabled compute domains. Industry analysts project that 80% of new vehicles will embed AI functionality by 2035, creating a large installed base for inference-class accelerators. NXP’s S32N processors built on 5 nm technology deliver 34 TOPS while meeting rigorous ASIL D requirements, signalling that automotive-grade safety and AI horsepower can coexist in a single device. With each design cycle spanning seven to ten years, silicon selected for today’s models generates annuity-like volume for their suppliers. Design wins now being awarded for Level 3 autonomy, sensor fusion, and over-the-air upgradability will therefore compound demand during the forecast period.

Ultra-Low-Power Edge AI ASIC Breakthroughs

Edge-native processors bring real-time inference to mobile, IoT, and industrial endpoints that cannot depend on cloud connectivity. Syntiant’s NDP250 delivers 30 GOPS within a milliwatt-class envelope, enabling always-on voice assistants and local LLM interactions. BrainChip’s neuromorphic coprocessor similarly harnesses event-driven processing to minimize power draw, unlocking AI in battery-powered sensors and wearables. These breakthroughs allow OEMs to embed intelligence without compromising form factor or battery life, accelerating design wins in healthcare diagnostics, predictive maintenance, and human-machine interfaces. The speed with which volume consumer products integrate such ASICs magnifies unit-shipment trajectories, adding yet another tailwind to the AI chipsets market.

National AI-Infrastructure Stimulus Programs

Sovereign AI agendas are rewriting semiconductor demand curves. The CHIPS and Science Act earmarks more than USD 50 billion for US foundry capacity and R&D, while China has committed USD 143 billion toward AI self-reliance. The UAE’s USD 200 billion AI infrastructure master plan—with NVIDIA chips at its core—propels fresh demand in the Middle East. Such fiscal programs subsidize fabs, data centers, and packaging facilities, anchoring local demand that is less sensitive to global macro cycles. The resulting procurement of AI accelerators, specialty memory, and interconnect silicon boosts addressable volumes for ecosystem players and sustains the market’s double-digit expansion into the medium term. [2]United States Congress, “CHIPS and Science Act of 2022,” congress.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain lithography bottlenecks below 3 nm | -5.20% | Global, concentrated impact on Taiwan, South Korea | Short term (≤ 2 years) |

| AI-model compression reducing silicon requirements | -3.80% | Global, led by research institutions and hyperscalers | Medium term (2-4 years) |

| Geopolitical export-control ceilings on advanced GPUs | -4.10% | China, Russia, with secondary effects globally | Medium term (2-4 years) |

| Escalating on-device thermal-design limits | -2.90% | Global, acute in data centers and mobile devices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Lithography Bottlenecks Below 3 nm

High-NA EUV machines required for 2 nm production cost more than USD 300 million each and remain limited in quantity. TSMC’s first 2 nm pilot line enters mass production in late 2025 but faces heavy pre-allocations from flagship customers. Capacity scarcity drives higher wafer pricing and lengthens delivery lead times for AI accelerators fabricated on these nodes. China’s exclusion from High-NA lithography further fragments global supply chains, raising the prospect of dual technology standards. The net effect lowers near-term unit availability and tempers the AI chipsets market growth rate until additional fabs come online after 2027.

AI-Model Compression Reducing Silicon Requirements

Pruning, quantization, and knowledge distillation techniques can cut inference compute demand by up to 70%, enabling smaller models to match original accuracy. If broadly adopted, these methods would lessen the need for high-end chips in certain workloads and moderate overall silicon volume growth. Consequently, compression innovation represents a structural counterforce to the market even as it enables wider AI deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Memory Integration Drives Silicon Evolution

GPUs retained 51.40% AI chipsets market share in 2025 by delivering unmatched parallelism for training, even as NPUs and ASICs are forecast to grow at a 44.2% CAGR by 2031. The market size allocated to GPU shipments will continue rising in absolute terms as frontier models swell compute budgets, yet the share shift toward domain-specific silicon is unmistakable. Memory and storage suppliers enjoy extraordinary tailwinds: HBM3E stacks from Samsung now reach 36 GB per die, meeting larger context window demands while raising average selling prices. A 500% increase in HBM pricing since 2024 confirms the market’s appetite for bandwidth over raw frequency. Heterogeneous designs based on chiplets are integrating CPUs, NPUs, and HBM on a common interposer to optimize power envelopes for edge inference. Vendors that master advanced 2.5D packaging, die-to-die interconnects, and memory co-location will capture premium margins within the evolving AI chipsets market.

The CPU segment adapts through on-die AI accelerators and new instruction sets, preserving relevance in traditional workloads that intermingle control logic and inference. FPGAs regain momentum where deterministic latency or in-field upgradability outweighs absolute throughput, especially inside industrial robots and telecom gateways. Architectural diversity ultimately raises the total addressable market because each workload maps to the most efficient silicon block. Suppliers capable of orchestrating multi-chiplet solutions are thus positioned for outsized share gains as system integrators demand turnkey subsystems rather than discrete parts.

By Processing Type: Inference Acceleration Reshapes Silicon Priorities

Training commanded 60.30% of AI chipsets market share in 2025, anchored by hyperscale data-center clusters running hundreds of petaflops per rack. The market size linked to training will keep growing because parameter counts in multimodal models expand geometrically; scenarios point to 100 million H100-class GPUs required by 2030. Still, inference shipments will scale at a 36.9% CAGR as enterprises roll out generative AI services across verticals and embed smaller models at the network edge. Cerebras Systems and Qualcomm jointly demonstrated 10× price-performance gains versus incumbent solutions, confirming that fresh architectures can disrupt historical cost curves.

Edge inference accelerators place energy efficiency above FLOPS, spurring chip vendors to adopt low-voltage SRAM, near-memory compute, and analog processing for kernels such as attention or convolution. This dichotomy creates two parallel product roadmaps: ultra-dense, liquid-cooled dies for training, and svelte, milliwatt-class ASICs for inference. Vendors that straddle both categories can cross-sell software toolchains, while specialists may seize niches around latency, security, or price-sensitive endpoints. The resulting competitive tension sustains innovation across the AI chipsets market.

By Deployment Location: Edge Computing Drives Architectural Innovation

Cloud facilities generated 63.10% of AI chipsets market size in 2025 as hyperscalers funnelled USD 500 billion into new data-center builds. Despite this dominance, edge deployments are forecast to increase at a 39.2% CAGR, reflecting demand for real-time analytics, reduced backhaul cost, and data-sovereignty compliance. Enterprises are also repatriating select AI workloads to on-premises clusters equipped with Intel’s Gaudi 3 accelerators, which provide 50% higher inference throughput than NVIDIA’s H100 at lower cost. These trends create a mosaic of deployment models, public cloud, private cloud, hybrid, and far-edge, that collectively diversify revenue streams for silicon suppliers.

On-device inference in vehicles, drones, and industrial controllers favours chiplets that pack domain-specific cores next to general-purpose logic. Thermal envelopes and ruggedization needs require innovations such as silicon carbide substrates, phase-change materials, and direct-inlet liquid coolers. Consequently, the market will fragment into form-factor sub-segments, each optimized for analogous environment and power constraints yet unified by common software runtimes.

By Application: Automotive Transformation Accelerates Silicon Demand

Consumer electronics accounted for 26.40% of the AI chipsets market size in 2025, a figure inflated by smartphone and PC refresh cycles integrating on-device generative AI. However, automotive and transportation are projected to grow at a 42.6% CAGR through 2031, overtaking consumer electronics by the decade’s close. Qualcomm estimates that software-defined vehicles could unlock a USD 650 billion annual semiconductor opportunity by 2030. Renesas’ R-Car V4H SoC delivers 34 TOPS at 16 TOPS/W, proving that high-grade functional safety and AI performance converge inside a single die, thus meeting OEM cost envelopes while future-proofing compute headroom.

Healthcare and life sciences apply high-throughput AI chipsets in imaging and genomics, whereas industrial and robotics segments demand deterministic latency and extended operating ranges. The enterprise IT and BFSI domain integrates accelerators into servers for fraud analytics and conversational agents. Each vertical’s distinct latency, power, and standards profile pushes vendors to customize silicon blocks, interactive compilers, and security modules. This heterogeneity ensures multipronged demand streams underpin the AI chipsets market.

Geography Analysis

Asia-Pacific maintained leadership with 41.10% AI chipsets market share in 2025. China’s USD 143 billion AI-self-reliance program, Taiwan’s >90% share in advanced AI manufacturing, and South Korea’s hegemony in HBM reinforce the region’s advantage. Japan’s Fugaku supercomputer upgrade further cements local demand for training-class accelerators. As a result, the market size tied to Asia-Pacific will expand steadily despite near-term export-control friction.

North America benefits from a deep R&D ecosystem, hyperscale capex, and government subsidies under the CHIPS and Science Act. NVIDIA’s platform dominance and Intel’s foundry reshore strategy tighten regional supply-chain control while preserving access to bleeding-edge capacity. These factors keep North America as the second-largest consumption base, especially for training clusters and custom accelerators for cloud providers.

The Middle East and Africa region, although smaller in absolute terms, is projected to post a 34.1% CAGR, making it the fastest-growing territory in the AI chipsets market. The UAE’s Stargate campus anchored by NVIDIA GPUs and Saudi Arabia’s Vision 2030 USD 40 billion AI fund draw direct investment from Western tech firms. Customizations for desert-climate thermals and Arabic-language LLMs broaden the application spectrum, underscoring how local conditions can trigger tailored silicon solutions. Europe remains focused on data sovereignty and energy efficiency, championing GAIA-X cloud standards that influence spec selection toward lower-power AI chipsets. South America is an emerging adopter, leveraging edge AI for agriculture and natural-resource monitoring, yet still trails on advanced-node access.

Value Chain Analysis

The AI chipsets value chain covers EDA/IP and architecture design (chip vendors and hyperscalers), wafer fabrication at advanced nodes, and advanced packaging and test. It also includes HBM and other memory supply, followed by system integration and distribution into cloud data centers, automotive platforms, and edge devices. In 2025-2026, the binding constraints have shifted from wafer availability alone to a combined gate of advanced packaging throughput (notably CoWoS-class 2.5D/3D integration) and HBM stacking capacity. This elevates the strategic role of memory suppliers such as SK hynix, Samsung, and Micron alongside leading foundry packaging operations. As a result, co-design across silicon, interconnect, packaging, and memory has become more central to meeting performance-per-watt and time-to-deployment targets.

Downstream, OEMs and AI infrastructure integrators are pulling the supply chain closer through multiyear technology and manufacturing partnerships, reflecting the need to lock in packaging and memory roadmaps early in the design cycle. For example, NVIDIA and SK hynix announced a multiyear partnership in June 2026 to advance next-generation memory for AI factories. Separately, Flex and Cerebras expanded manufacturing in California in July 2026 to scale CS-3 system production, while onshoring and multi-partner manufacturing collaborations have gained visibility. NVIDIA’s highlighted U.S. manufacturing activity with TSMC in Phoenix, along with collaborations with partners such as Foxconn and Wistron, points to tighter coupling between chip designers, foundry/OSAT ecosystems, and system builders to reduce lead-time risk and improve supply resilience.

Competitive Landscape

The AI chipsets market is characterized by high concentration. NVIDIA alone controls roughly 80% of training-accelerator revenue, buoyed by the comprehensive CUDA software stack and Blackwell-generation hardware that posted USD 11 billion in quarterly sales. AMD’s MI300 series has narrowed the gap, surpassing USD 1 billion in quarterly revenue and improving supply diversity. Hyperscalers now design custom silicon such as Google’s TPU v5e and Amazon’s Graviton4 to lower total cost of ownership and reduce vendor dependence, signifying a gradual vertical-integration shift.

Intel stakes its comeback on the Gaudi 3 accelerator, which claims 50% higher inference throughput than peer GPUs while positioning its foundry as an open manufacturing alternative. Start-ups like Cerebras Systems, Groq, and SiMa.ai are disrupting niches with wafer-scale engines, token-optimized pipelines, and multimodal edge ASICs. Meanwhile, memory vendors Samsung and SK Hynix expand HBM capacity through multibillion-dollar fabs, recognizing that memory bandwidth has become the new performance bottleneck. As the market approaches USD 226 billion by 2030, competitive dynamics will intensify around software ecosystems, heterogeneous integration, and total-system optimization rather than raw die size alone.

AI Chipsets Industry Leaders

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices Inc.

Alphabet Inc.

Huawei Technologies Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK hynix announced a multiyear technology partnership to co-develop next-generation memory for AI factories, targeting integration with NVIDIA platforms including Vera Rubin systems and Jetson Thor. The partnership tightens the coupling between accelerator roadmaps and HBM innovation, where bandwidth and packaging compatibility increasingly shape delivered performance and shipment timing.

- September 2025: NVIDIA and Intel announced a collaboration to develop AI infrastructure and personal computing products, including work to integrate NVIDIA NVLink with Intel x86 platforms. The agreement indicates deeper cross-vendor system-level engineering to broaden procurement options for data centers and accelerate deployment-ready reference designs across enterprise and cloud ecosystems.

- September 2024: Intel unveiled next-generation AI solutions with the launch of Xeon 6 and Gaudi 3. The product push reinforced Intel's position in AI servers by pairing general-purpose CPUs with dedicated accelerators, giving hyperscalers and enterprises an alternate stack for training and inference deployments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the artificial intelligence chipsets market covers revenue generated from chipsets and integrated circuits used to train and run AI models across devices and data centers. The market is measured in value terms in USD and reflects demand for AI-oriented processing hardware.

Scope exclusions: This sizing excludes AI software, cloud services revenue, and general IT services that are not part of chipset hardware spending.

Segmentation Overview

- By Component

- Central Processing Unit (CPU)

- Graphics Processing Unit (GPU)

- Neural Network Processor (NNP)

- Other Components

- By Application

- Consumer Electronics

- Automotive

- Healthcare

- Automation and Robotics

- Other Applications

- By Geography

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle-East

Data Sources, Market Sizing, and Validation

Desk Research

Desk research began by grounding the market definition around AI-oriented semiconductor hardware and then mapping where demand is showing up across data centers and edge devices. Public sources such as UN Comtrade (for electronics and semiconductor trade flows), the US Census Bureau and Bureau of Economic Analysis (for production and macro context), World Bank and OECD datasets (for ICT and investment indicators), and technical publications from bodies such as IEEE were referenced to shape assumptions that can be traced back to visible signals.

We also reviewed company filings, investor presentations, earnings call transcripts, product announcements, and reputed press coverage to understand capacity additions, shipment timing, and pricing direction. A paid subscription for company financials and news intelligence, plus patent databases, supported quick cross-checks on roadmap timing and compute design refreshes. The desk sources listed above are illustrative only, and additional public references were used for data collection, validation, and clarification during the analysis.

Primary Interviews and Surveys

Primary conversations helped validate what portion of AI compute spending converts into chipset revenue, and where demand is concentrated across training and inference deployments. Inputs were gathered from a mix of supply-side and demand-side stakeholders, including chipset and component participants, OEM and channel voices, data center focused buyers, and system integrators, with representation across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | APAC: 46% |

| Mid tier: 60% | Functional/Unit leaders: 30% | EMEA: 30% |

| Smaller Players: 14% | Managers: 58% | Americas: 24% |

Market-Sizing & Forecasting

The main model uses a top-down demand pool build-up by linking AI workload deployment to semiconductor spending, and then filtering that pool using evidence on where AI compute is installed (hyperscale training clusters, enterprise inference, and edge devices). The results are checked with selective bottom-up approximations, such as sampled ASP by chipset class multiplied by shipment ranges, followed by channel feedback on mix changes to correct the totals.

Key inputs used in the model included data center AI server build activity, the split between training and inference usage, accelerator attach rates in new deployments, leading-node versus mature-node supply availability, and observed ASP movement for high-performance compute parts. Each input was treated as a visible lever so that a new data point can be carried through the model without reworking every line.

For forecasting, scenario analysis was used and then anchored with a multivariate regression view that connected demand to drivers such as AI workload growth, hyperscale capex direction, semiconductor capacity additions, and regional electronics output. When public information was incomplete, bounded ranges were applied and then narrowed using interview feedback, and the midpoint was taken only after more than one signal aligned.

Data Validation & Update Cycle

Validation is completed in steps so the model stays consistent with real market signals. Outputs are compared against independent indicators such as semiconductor shipment direction, public signals on data center build-outs, and electronics trade movement, and then anomalies are reviewed to confirm whether they come from timing, currency treatment, or scope differences.

Before sign-off, a second analyst reviews the logic and reruns key calculations, and large variances trigger re-contact with selected participants to re-validate assumptions like ASP direction and workload mix. Reports are refreshed annually, with interim updates when material events occur such as capacity shifts, policy moves, or sharp pricing changes. Before delivery, a final pass is done so clients receive the most current view available at that time.

Mordor Intelligence's Artificial Intelligence Chipsets Market Size Versus Other Published Estimates

Published market sizes for AI chipsets can vary even when the topic name looks identical, because firms often count different product baskets and apply different timing assumptions. Gaps commonly come from whether the number covers only chipsets or a wider AI hardware set, how pricing is projected, and how frequently inputs are refreshed.

Data center build-out signals, the observed training versus inference mix, and checks against semiconductor shipment direction are used to keep the Mordor Intelligence 2026 value aligned to chipset revenue rather than wider system hardware. In other publications, the 2026 total can move up when broader compute hardware is included, or when ASP progression is extended from peak-cycle conditions without being re-tested against updated supply and deployment indicators.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 70.25 B (2026) | |

| Global Consultancy A | USD 125.15 B (2026) | Likely uses a broader definition that blends additional AI compute hardware beyond chipsets, and applies different ASP and volume ramp assumptions that lift the same-year total. |

| Industry Research Publisher B | USD 70.57 B (2024) | Uses a different base year and forecast window, and may classify chipset types and workload use differently, which makes cross-year comparisons sensitive to currency timing and assumed adoption pace. |

Across the three values, the main difference comes from how tightly chipset-only revenue is separated from adjacent AI hardware, and how pricing and adoption ramps are carried into the base year. By tying assumptions back to repeatable signals and re-checking outliers before sign-off, the final number stays transparent and easier to maintain through annual refresh cycles.

Key Questions Answered in the Report

What is the current size of the AI chipsets market?

The AI chipsets market stands at USD 70.25 billion in 2026 and is projected to reach USD 285.9 billion by 2031.

Which component leads the AI chipsets market?

GPUs hold 51.40% market share, largely due to entrenched software ecosystems that favour their parallel-processing strengths.

How fast is the automotive segment growing within the AI chipsets market?

Automotive and transportation applications are expected to expand at a 42.6% CAGR through 2031 as vehicles transition to centralized AI compute domains.

Why are high-bandwidth memory prices rising?

Demand from AI GPU clusters has outstripped supply, driving HBM prices up 500% and selling out capacity through 2025.

Which region shows the fastest growth in the AI chipsets market?

The Middle East and Africa region is forecast to grow at a 34.1% CAGR, backed by multibillion-dollar sovereign AI infrastructure plans.

What is the main restraint on near-term AI chipset supply?

Limited lithography capacity below the 3 nm node is constraining output, creating longer lead times and upward price pressure.

Page last updated on: