AI Memory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.93 Billion |

| Market Size (2031) | USD 98.28 Billion |

| Growth Rate (2026 - 2031) | 28.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

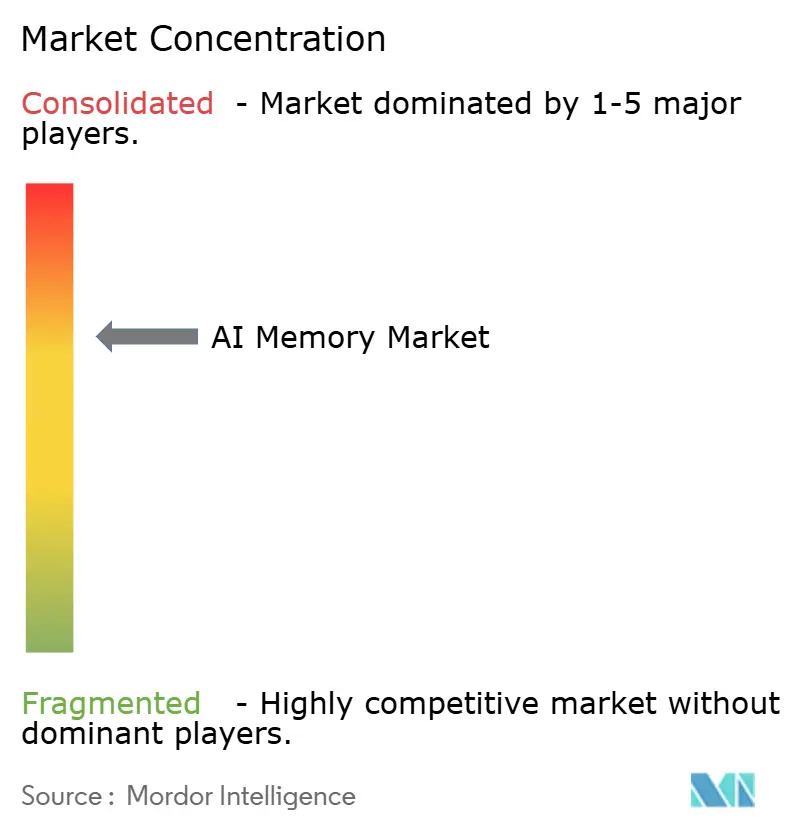

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Memory Market Analysis by Mordor Intelligence

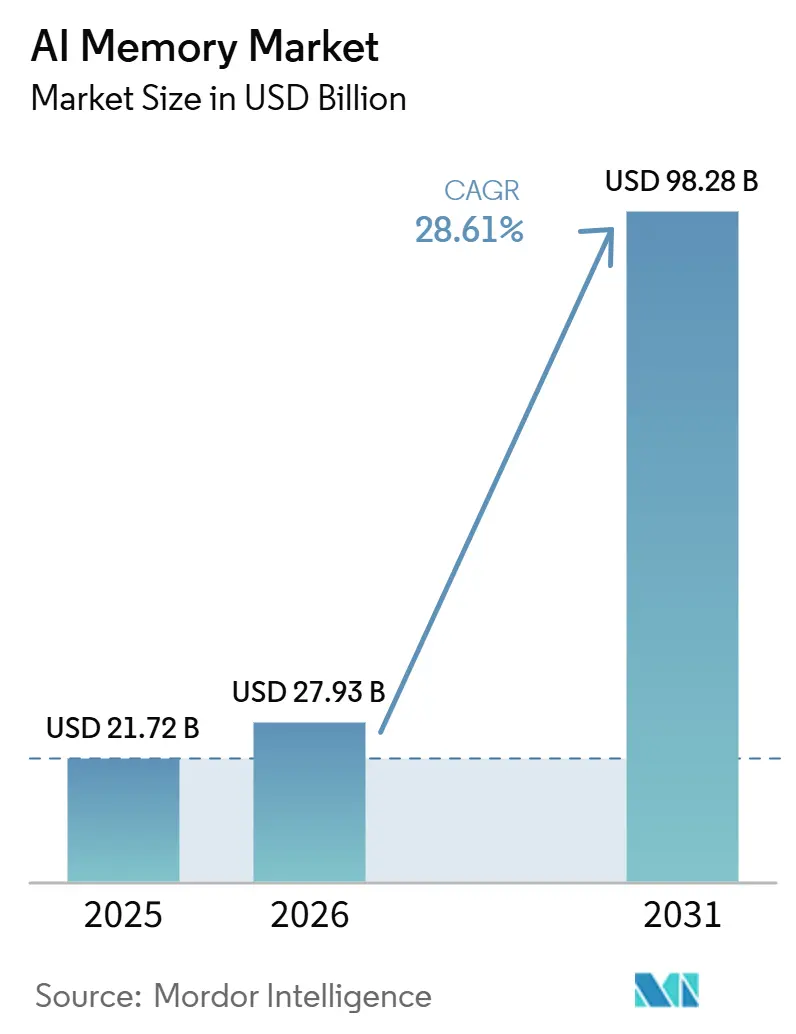

The AI memory market size is expected to grow from USD 21.72 billion in 2025 to USD 27.93 billion in 2026 and is forecast to reach USD 98.28 billion by 2031 at 28.61% CAGR over 2026-2031. This pace reflects how memory has moved to the center of AI system design as model training, inference serving, and context storage all depend on higher bandwidth and larger active memory pools. The AI memory market is also expanding because hyperscale buyers are planning larger AI server fleets, while edge systems in automotive, robotics, and industrial settings are creating a second wave of demand outside the data center. Product roadmaps are now being shaped by qualification speed, packaging readiness, and the ability to support multiple memory tiers in one platform. That is making supplier strategy more focused on long-term platform alignment, production planning, and ecosystem partnerships. It is also opening room for newer memory layers such as CXL-based expansion and AI-native storage memory, which widen the commercial scope of the AI memory market.

Key Report Takeaways

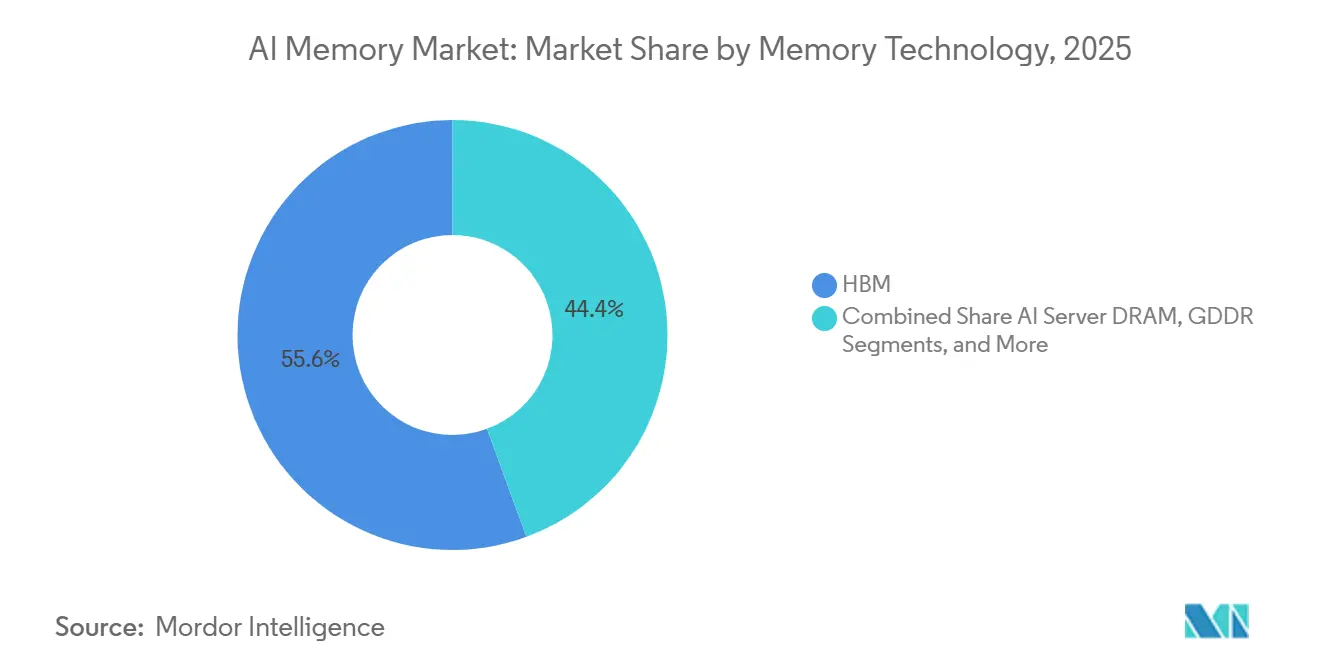

- By memory technology, HBM held 55.60% revenue share of the AI memory market in 2025, while GDDR is projected to expand at a 29.44% CAGR through 2031.

- By AI application, AI Training and Model Development accounted for 45.50% of revenue in 2025, while AI Inference is expected to record the highest CAGR at 29.57% through 2031.

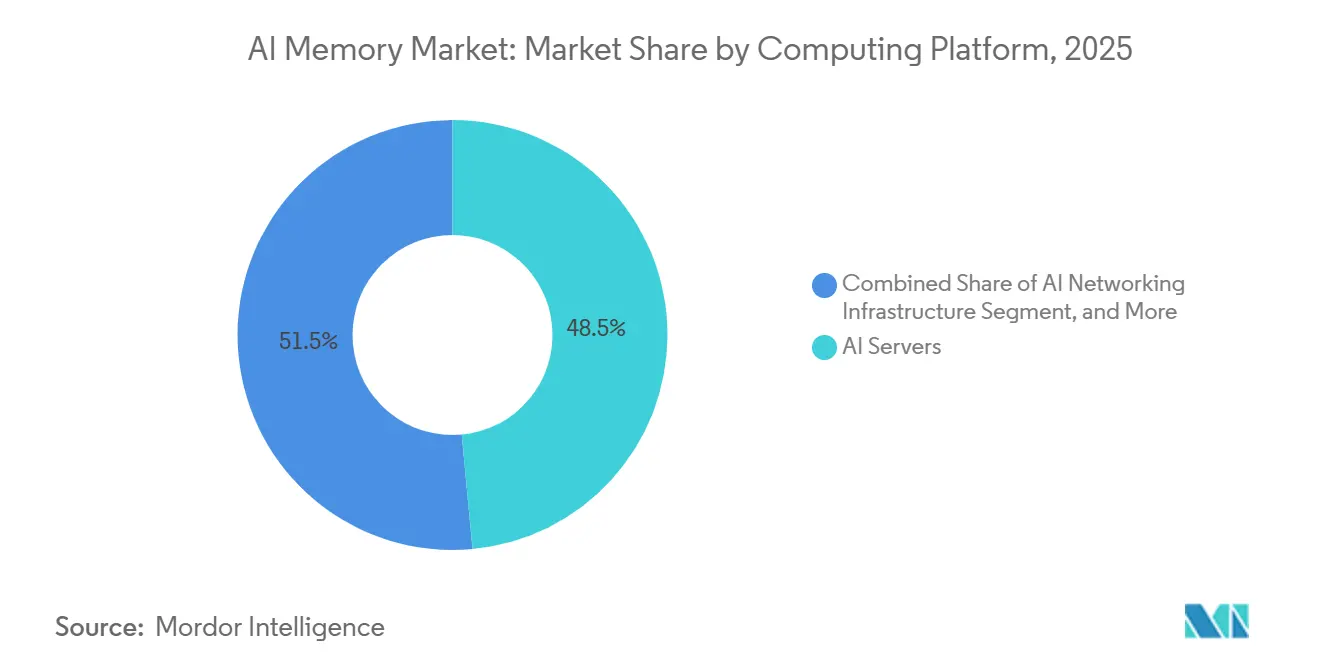

- By computing platform, AI Servers held 48.52% share of the AI memory market in 2025, while Edge AI Systems are projected to grow at a 29.62% CAGR through 2031.

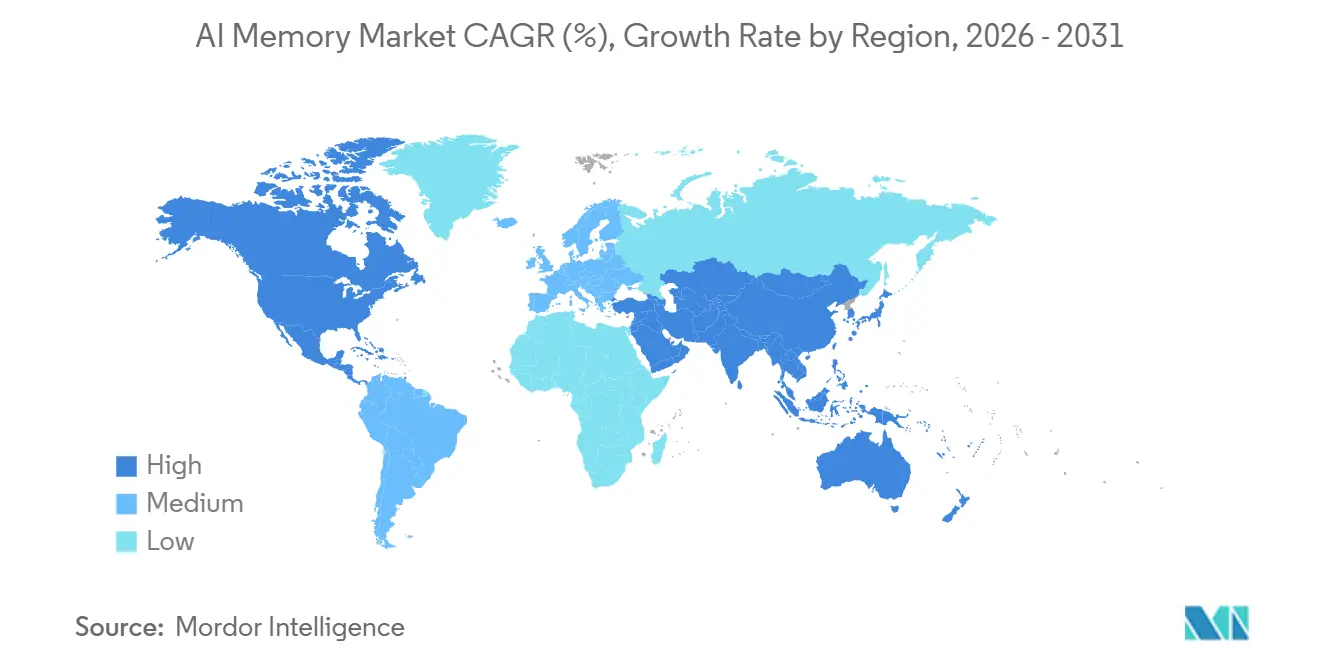

- By geography, North America held 38.41% share in 2025, while Asia-Pacific is projected to expand at a 29.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Memory Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of HBM3E And HBM4 in AI Accelerators | +8.5% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Hyperscale AI Server Fleets | +7.0% | Global, strongest in North America with spillover to Europe and Asia-Pacific | Short term (≤ 2 years) |

| Rising AI Training and Inference Compute Density | +5.5% | Global, led by North America | Medium term (2-4 years) |

| Memory Content Inflation in AI Servers and Racks | +4.0% | Global, strongest in North America, Europe, and core Asia-Pacific markets | Short term (≤ 2 years) |

| Higher Bandwidth Demand Per Watt in Advanced GPUs And ASICs | +3.5% | Global, early concentration in North America and South Korea | Medium term (2-4 years) |

| Persistent KV Cache Growth in Long-Context Agentic AI Workloads | +2.5% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of HBM3E And HBM4 in AI Accelerators

The move from HBM3E to HBM4 is progressing quickly as accelerator vendors push for more bandwidth and better power efficiency in each new platform generation. NVIDIA stated in May 2026 that the Vera Rubin platform was ramping into full production, which confirms that next-generation memory demand is now tied directly to production deployments rather than early sampling activity.[1]NVIDIA Corporation, “NVIDIA Vera Rubin Ramps Into Full Production to Power Agentic AI Factories Worldwide,” NVIDIA Investor Relations, investor.nvidia.com This matters because HBM is no longer a premium option inside leading AI systems and has become a required part of the compute stack. As buyers align hardware roadmaps with more capable accelerators, memory planning starts earlier and stays locked in for longer periods. That shifts procurement from short-cycle component buying toward platform-level commitment. For the AI memory market, this keeps HBM at the center of revenue growth and strategic supplier positioning.

Expansion of Hyperscale AI Server Fleets

Large AI server programs are moving from staged pilots to committed deployment cycles across cloud infrastructure. AMD and Meta Platforms announced in February 2026 an expanded partnership to deploy 6 gigawatts of AMD GPU infrastructure, with shipments for the first-gigawatt phase beginning in the second half of 2026.[2]Advanced Micro Devices, “AMD and Meta Announce Expanded Strategic Partnership to Deploy 6 Gigawatts of AMD GPUs,” AMD Newsroom, amd.com Each rollout of that scale pulls in HBM, server DRAM, storage memory, and networking memory at the same time. That means growth is not confined to a single memory type and instead spreads across the full stack that supports AI clusters. It also favors suppliers that can offer dependable qualification, stable output, and roadmap continuity. The AI memory market is therefore benefiting from both larger fleet counts and higher memory content inside each deployed system.

Rising AI Training and Inference Compute Density

Training clusters and inference clusters are both carrying larger model state in active memory than earlier AI systems did. NVIDIA launched the BlueField-4 STX modular storage architecture in March 2026 with CMX context memory storage, which shows that memory is now being designed into inference infrastructure as a dedicated layer rather than treated as a secondary component.[3]NVIDIA Corporation, “NVIDIA Vera Rubin Ramps Into Full Production to Power Agentic AI Factories Worldwide,” NVIDIA Investor Relations, investor.nvidia.com Penguin Solutions introduced a production-ready CXL-based KV cache server in the same month with up to 11TB of CXL memory for enterprise-scale inference, reinforcing the same architecture shift. These launches show that adding compute alone does not remove throughput limits when long context windows and persistent session state have to stay close to the processor. As model usage becomes more interactive and continuous, memory bandwidth and capacity both rise in importance. That keeps the AI memory market tied closely to the way AI inference systems are being built.

Memory Content Inflation in AI Servers and Racks

New AI racks now carry more memory across the accelerator layer, the server layer, and the storage layer. NVIDIA said the Vera Rubin platform integrates HBM4 with a context memory storage architecture, which points to a broader system design that carries a larger memory footprint than earlier platforms. Penguin Solutions responded to the same pressure with a CXL-based server design that combines DDR5 and CXL add-in cards to expand available memory for inference deployments. These moves show that buyers are no longer sizing memory as a support component that can be adjusted late in the purchase cycle. Memory now shapes system cost, architecture choice, and procurement timing together. That creates a wider revenue base across HBM, server DRAM, LPDDR, and expansion memory inside the AI memory market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Package-Level Thermal and Yield Constraints | -2.5% | Global, with strongest effect in South Korea and Taiwan | Short term (≤ 2 years) |

| Limited Qualified Supply Base for Advanced HBM | -2.0% | Global, with direct downstream impact on North America | Short term (≤ 2 years) |

| Heavy Dependence on Advanced Packaging Capacity | -1.5% | Global, with primary pressure in Taiwan and South Korea | Medium term (2-4 years) |

| Rapid Obsolescence Risk Across HBM Generations | -1.0% | Global, with strategic risk concentrated in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Package-Level Thermal and Yield Constraints

Advanced stacked memory is harder to scale than conventional memory because more layers have to perform together inside a tighter thermal envelope. This is especially important in HBM, where finished output depends on packaging quality as much as wafer supply. If packaging performance slips, accelerator deliveries can slow even when end demand stays firm. Validation also takes time because each generation has to clear thermal, reliability, and platform-level requirements before volume shipment. That can narrow the usable ramp window for a new product generation. The AI memory market therefore stays exposed to package-level execution risk even when demand conditions remain strong.

Limited Qualified Supply Base for Advanced HBM

Only a small number of suppliers can support top AI accelerator programs with advanced HBM. Qualification takes time because the memory has to match the controller, package design, thermal profile, and performance targets of each platform. Buyers therefore depend on a narrow supply base when they plan large deployment cycles. That concentration gives qualified vendors more control over allocation and timing. It also raises the cost of a delayed product cycle for both suppliers and customers. The AI memory market will keep carrying this constraint until the qualified supplier base broadens in future HBM generations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Technology: HBM Anchors Revenue While GDDR Scales Across Broader AI Deployments

HBM held 55.60% of AI memory market share in 2025, which shows how strongly hyperscale training infrastructure shaped revenue during the year. Its lead came from the fact that leading AI accelerators depend on very high bandwidth memory and cannot sustain expected throughput without it. NVIDIA said in May 2026 that Vera Rubin was ramping into full production, which supports continued HBM demand as next-generation systems move into active deployment. AI Server DRAM remained the second-largest technology layer because large AI systems still need substantial main memory around the accelerator complex.

GDDR is projected to record the fastest AI memory market size growth at 29.44% CAGR through 2031, supported by the commercial rollout of GDDR7. Rambus noted that GDDR7 was standardized by JEDEC in March 2024 and brought a higher-performance path for graphics and accelerator applications. Within the AI memory industry, that gives GDDR a stronger position in GPUs and edge accelerators that need higher bandwidth but do not always require HBM-class packaging. AI Edge Memory LPDDR is also set to expand as inference systems and edge devices need better bandwidth per watt under tight thermal limits. Other memory technology, including CXL-based expansion, adds a longer runway because Penguin Solutions introduced a production-ready CXL-based KV cache server with up to 11TB of memory for enterprise inference in March 2026.

By AI Application: Training Leads Current Revenue While Inference Reshapes the Memory Stack

AI Training and Model Development held 45.50% of revenue in 2025, which kept it as the largest application area in the AI memory market. That position reflected the heavy memory needs of frontier model development, where thousands of accelerators operate together and require large active memory pools. AI Inference is forecast to grow at the fastest pace with a 29.57% CAGR through 2031 as AI services move from periodic training events to constant user-facing workloads. This shift matters because inference runs continuously and scales with every prompt, retrieval cycle, and context update.

Penguin Solutions stated in March 2026 that inference workloads are 30% compute-driven and 70% memory-driven, which underscores why memory bandwidth and accessible capacity are becoming the main design variables in deployment planning. NVIDIA also introduced CMX context memory storage for agentic AI inference, which reflects the growing need to keep KV cache and related model state close to the active workload. In the AI memory industry, this makes inference more than a demand add-on because it changes the memory hierarchy inside the deployed system. HPC and Scientific AI remains the third application block and provides a steadier demand base through national labs, climate modeling, and drug discovery workloads that often rely more on broader server memory balance than on the top HBM tier.

By Computing Platform: AI Servers Dominate Today While Edge AI Systems Expand the Demand Base

AI Servers accounted for 48.52% of revenue in 2025, giving them the largest share among computing platforms in the AI memory market. Their lead came from the fact that rack-scale AI systems absorb HBM, server DRAM, storage memory, and networking memory in the same deployment cycle. AI Compute Accelerators also matter because they define the memory interface requirements that shape demand for each new HBM and DRAM generation. As a result, platform competition in AI hardware directly feeds into memory roadmaps and production planning.

Edge AI Systems are projected to expand at the fastest pace with a 29.62% CAGR through 2031, which widens the reach of the AI memory market beyond centralized data centers. These systems need sustained bandwidth within stricter power and thermal limits, which supports demand for LPDDR and selected GDDR configurations. Across the AI memory industry, that makes the platform mix more diverse because demand now comes from both large AI server clusters and distributed intelligent devices. AMD and Meta announced in February 2026 a plan to deploy 6 gigawatts of AMD GPU infrastructure, which illustrates how single platform commitments can pull forward large memory requirements over the following production cycle. AI Networking Infrastructure and Other Computing Platform categories also gain relevance as larger clusters need memory-aware switching, storage, and context-serving layers to keep inference performance stable.

Geography Analysis

North America held 38.41% of AI memory market share in 2025, which made it the largest regional demand center. Its lead came from hyperscaler AI infrastructure buildouts that turned memory into a strategic procurement item instead of a routine server component. The region also benefits from the concentration of major cloud and accelerator platform buyers, which gives it strong pull on qualified supply. This keeps North America central to both near-term allocation decisions and longer-term platform planning in the AI memory market.

Asia-Pacific is projected to grow at a 29.48% CAGR through 2031, making it the fastest-growing region in the AI memory market. The region matters on both the demand side and the production side because it houses the main HBM manufacturing base and much of the supporting packaging ecosystem. South Korea remains the core production center for advanced AI memory, while Japan is strengthening its role as an additional manufacturing node through new investment in HBM capacity. China adds another layer of demand through rising domestic AI model development, even as technology restrictions shape the type of memory infrastructure that can be deployed. India is emerging more as a consumption market during the forecast period, supported by cloud expansion and a growing AI startup base.

Europe and the remaining regions represented a smaller share of the AI memory market in 2025, but their demand pattern is strategically distinct. In Europe, demand is centered on industrial AI, financial services, life sciences, and sovereign computing programs that place a premium on traceability and energy efficiency. South America, the Middle East, and Africa remain earlier-stage markets, yet they are developing additional AI inference demand through sovereign cloud programs and wider regional data center investment. This means the global footprint of the AI memory market is broadening even though revenue concentration remains highest in North America and production concentration remains strongest in Asia-Pacific.

Competitive Landscape

The AI memory market is highly consolidated at the manufacturing tier, especially in HBM, which represented 55.60% of revenue in 2025. The supply of advanced HBM remains limited to a very small group of qualified vendors, which gives that part of the market a much tighter structure than the broader memory category. Competition is therefore shaped less by headline product launches alone and more by qualification speed, packaging readiness, and the ability to stay aligned with leading accelerator roadmaps. Those conditions make scale and execution more important than price-only competition.

Several strategic moves in 2026 showed how vendors are positioning for the next phase of the AI memory market. Micron broke ground on an HBM plant expansion in Hiroshima in July 2026, which supports its long-term place in advanced AI memory supply. Applied Materials and TSMC announced an innovation partnership in May 2026 to accelerate materials engineering and process integration for next-generation AI semiconductor devices. NVIDIA launched BlueField-4 STX and CMX context memory storage in March 2026, which widened the commercial role of memory beyond the accelerator package itself. Penguin Solutions also introduced a production-ready CXL-based KV cache server in March 2026, showing that new entrants can still find room in adjacent memory tiers even when core HBM supply stays concentrated.

The main white space in the AI memory market sits in advanced packaging support, CXL expansion memory, and AI-native storage layers rather than in direct HBM substitution. Standards and interface ecosystems also reinforce incumbent strength because they raise the qualification burden for any new entrant. Rambus remains relevant here because controller IP and memory interface support help determine how quickly new standards move into deployable products. The result is a market where the core manufacturing tier is narrow, while the surrounding ecosystem offers selective entry points for specialized suppliers.

AI Memory Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Micron Technology broke ground on a USD 9.3 billion HBM plant expansion in Hiroshima, Japan, supported by up to 500 billion yen from Japan's Ministry of Economy, Trade and Industry, with mass production targeted from summer 2028. The facility is dedicated to HBM4 production for AI accelerator platforms and is part of Micron's broader USD 200 billion U.S. and international manufacturing expansion commitment.

- June 2026: NVIDIA CEO Jensen Huang confirmed at GTC Taipei that Samsung Electronics, SK hynix, and Micron Technology had all qualified as HBM4 suppliers for the Vera Rubin platform, the first instance of concurrent triple-vendor qualification for a single AI accelerator generation.

- May 2026: NVIDIA announced that the Vera Rubin platform was ramping into full production at GTC Taipei on May 31, 2026, with production shipments scheduled to begin from the third quarter of 2026. The platform delivers 10x agent throughput at scale compared with the prior Grace Blackwell generation and integrates HBM4 across its accelerator and CMX context memory storage architecture.

- May 2026: Applied Materials and TSMC announced an innovation partnership at Applied Materials' EPIC Center in Silicon Valley, targeting co-development of materials engineering and process integration technologies for next-generation AI semiconductor devices spanning data center and edge applications.

Global AI Memory Market Report Scope

The AI Memory Market refers to the industry segment dedicated to the design, development, and deployment of advanced memory technologies optimized for artificial intelligence (AI) workloads, enabling faster data access, higher bandwidth, and improved energy efficiency in training and inference processes.

The AI Memory Market Report is Segmented by Memory Technology (HBM, AI Server DRAM, GDDR, AI Edge Memory LPDDR, and Other Memory Technology (CXL Memory and Other Emerging Memory Types)), AI Application (AI Training and Model Development, AI Inference, and AI Inference, and HPC and Scientific AI), Computing Platform (AI Servers, AI Compute Accelerators, AI Networking Infrastructure, Edge AI Systems, and Other Computing Platform (Specialized AI Computing Platforms and AI Workstations)), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM |

| AI Server DRAM |

| GDDR |

| AI Edge Memory LPDDR |

| Other Memory Technologies (CXL Memory and Other Emerging Memory Types) |

| AI Training and Model Development |

| AI Inference |

| HPC and Scientific AI |

| AI Servers |

| AI Compute Accelerators |

| AI Networking Infrastructure |

| Edge AI Systems |

| Other Computing Platforms (Specialized AI Computing Platforms and AI Workstations) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Technology | HBM | |

| AI Server DRAM | ||

| GDDR | ||

| AI Edge Memory LPDDR | ||

| Other Memory Technologies (CXL Memory and Other Emerging Memory Types) | ||

| By AI Application | AI Training and Model Development | |

| AI Inference | ||

| HPC and Scientific AI | ||

| By Computing Platform | AI Servers | |

| AI Compute Accelerators | ||

| AI Networking Infrastructure | ||

| Edge AI Systems | ||

| Other Computing Platforms (Specialized AI Computing Platforms and AI Workstations) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the AI memory market?

The AI memory market size stood at USD 21.72 billion in 2025, is expected to reach USD 27.93 billion in 2026, and is forecast to grow to USD 98.28 billion by 2031 at a 28.61% CAGR.

Which memory technology leads revenue in AI memory?

HBM led the market with 55.60% revenue share in 2025 because leading AI accelerators and training systems depend on very high bandwidth memory.

Which application is growing fastest in AI memory demand?

AI Inference is the fastest-growing application with a 29.57% CAGR through 2031 as AI services move toward continuous, memory-intensive deployment models.

Which computing platform generates the most demand for AI memory?

AI Servers held the largest share at 48.52% in 2025 because they combine HBM, server DRAM, networking memory, and storage memory in the same deployment cycle.

Which region leads the AI memory market and which region grows fastest?

North America led with 38.41% share in 2025, while Asia-Pacific is projected to grow the fastest at a 29.48% CAGR through 2031 due to its strong production base and rising AI demand.

What is changing competition in AI memory?

Competition is being shaped by HBM qualification, packaging capacity, and ecosystem partnerships, while CXL memory and AI-native storage are creating new openings beside the core HBM supplier group.

Page last updated on: