Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Memory IC Market Report is Segmented by Memory Type (DRAM, Flash, and More), Application (Smartphones and Tablets, Servers and Data Centers, and More), Interface Standard (DDR4, DDR5, and More), End-User Industry (Consumer Electronics, Automotive, and More), and Geography (North America, Europe, South America, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

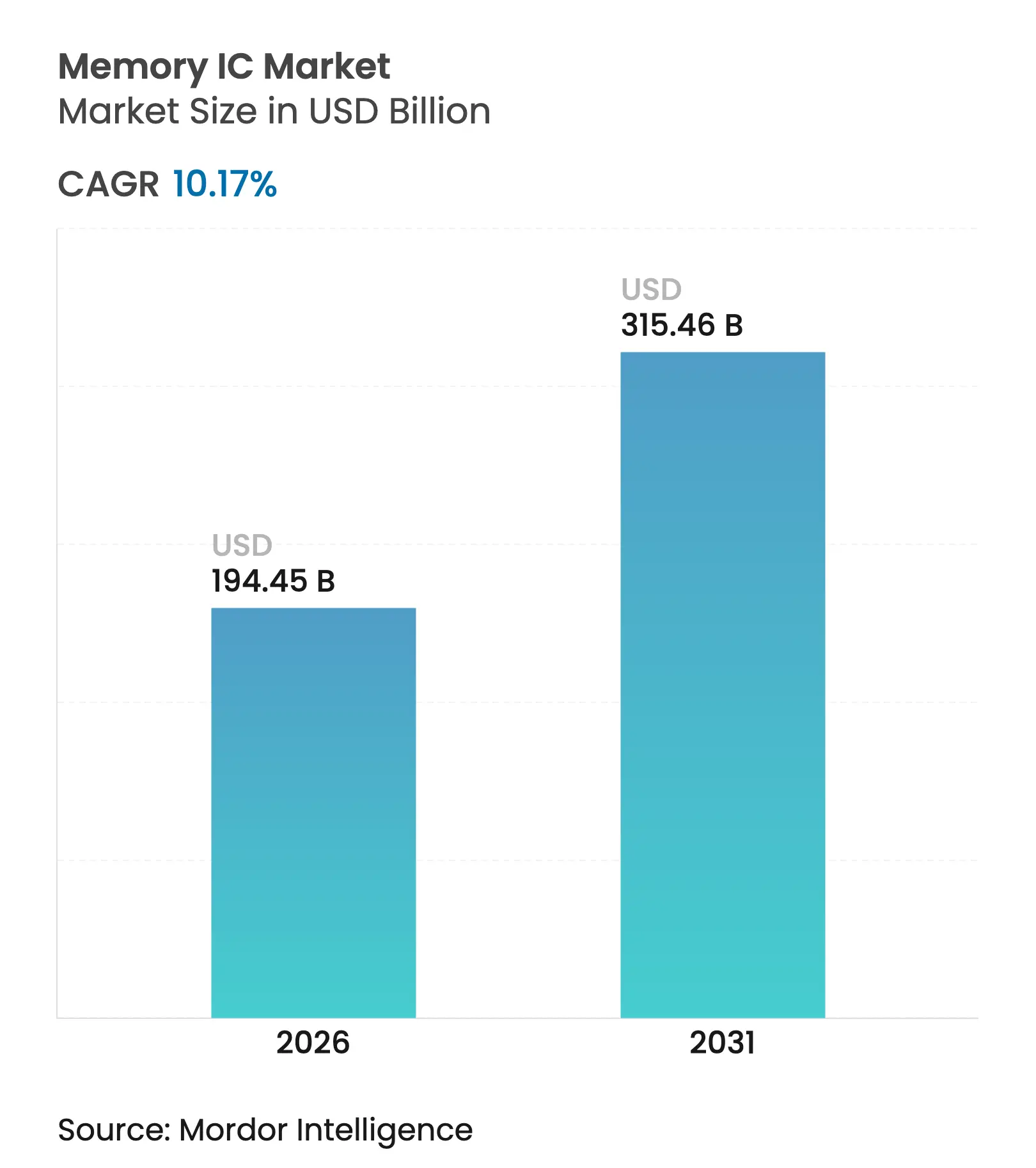

| Market Size (2026) | USD 194.45 Billion |

| Market Size (2031) | USD 315.46 Billion |

| Growth Rate (2026 - 2031) | 10.17 % CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Memory IC market size is expected to grow from USD 176.5 billion in 2025 to USD 194.45 billion in 2026 and is forecast to reach USD 315.46 billion by 2031 at 10.17% CAGR over 2026-2031. Intensifying AI adoption, rising vehicle electrification, and national fabrication incentives are reshaping demand patterns and encouraging geographic rebalancing within the Memory IC market. Discrete DRAM continues to underpin high-bandwidth processing for AI training, while NAND-flash density gains lower cost per bit and widens deployment in data-center and automotive storage. Specialized interface standards such as HBM3E and upcoming HBM4 allow accelerator vendors to place unprecedented bandwidth next to compute cores, reinforcing the Memory IC market’s pivot toward heterogeneous, workload-tuned architectures. Supply concentration among the three incumbent vendors remains high; however, sovereign technology programs exceeding USD 50 billion are catalyzing new entrants and expanding the Memory IC market’s regional footprint.[1]European Court of Auditors, “Special Report 12/2025 – The EU's Strategy for Microchips,” eca.europa.eu Cyclical pricing, tight HBM capacity, and elevated EUV-driven fab costs pose headwinds but also create openings for differentiated offerings such as MRAM and compute-in-memory devices that promise lower latency and power consumption.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Proliferation of Smartphones, Feature Phones and Tablets Rising Proliferation of Smartphones, Feature Phones and Tablets | +2.10% | Global, with APAC leading demand | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.10% | Geographic Relevance:Global, with APAC leading demand | Impact Timeline:Medium term (2-4 years) |

Growing Demand for Low-Power Memory in Portable Wireless Devices Growing Demand for Low-Power Memory in Portable Wireless Devices | +1.80% | Global, concentrated in mobile ecosystems | Short term (≤ 2 years) | |||

Increasing Demand for SSDs in Big-Data Storage Increasing Demand for SSDs in Big-Data Storage | +1.50% | North America and Europe data centers | Medium term (2-4 years) | |||

Rapid Adoption of High-Bandwidth Memory for AI Accelerators Rapid Adoption of High-Bandwidth Memory for AI Accelerators | +2.80% | Global, led by US and China AI infrastructure | Short term (≤ 2 years) | |||

Rising Memory Content per Vehicle in ADAS and EV Platforms Rising Memory Content per Vehicle in ADAS and EV Platforms | +1.40% | Global automotive markets, led by Europe and China | Long term (≥ 4 years) | |||

Government Incentives and CHIPS-style Programs Boosting Domestic Production Government Incentives and CHIPS-style Programs Boosting Domestic Production | +0.80% | US, EU, Japan, South Korea | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Proliferation of Smartphones, Feature Phones and Tablets

Form-factor innovation, such as Samsung’s 0.65 mm LPDDR5X package, allows OEMs to squeeze larger capacities into slim devices, elevating average DRAM content per flagship handset to 16–24 GB.[2]Samsung Electronics, “Samsung Electronics Begins Mass Production of Industry's Thinnest LPDDR5X DRAM,” news.samsung.com Generative-AI chat and on-device vision models intensify bandwidth needs, and JEDEC’s. LPDDR6 roadmap outlines 10.667–14.4 Gbps signaling to meet real-time inference requirements.[3]Zak Killian, “JEDEC Reveals Massive Speed Boosts for Next-Gen DDR6 and LPDDR6,” hothardware.com Feature-phone volumes in emerging markets add baseline shipments, while tablets regain traction from hybrid-work trends, collectively expanding the Memory IC market. Edge inference reduces cloud round-trips, translating to sustained demand for low-power, high-density mobile DRAM inside the Memory IC market.

Growing Demand for Low-Power Memory in Portable Wireless Devices

Wearables, AR glasses, and IoT gateways emphasize stringent power budgets, driving LPDDR and next-generation embedded memories that minimize refresh cycles. Suppliers optimize deep-sleep states, trimming idle currents to sub-50 µA and aligning with multi-day battery life targets. Such efficiency gains keep portable platforms competitive without sacrificing local compute capability, bolstering the Memory IC market.

Increasing Demand for SSDs in Big-Data Storage

Hyperscale operators expand NVMe flash arrays to accelerate data-lake access for AI analytics, shifting workload tiers away from hard disks. Layer-200 3D-NAND designs reduce USD per terabyte, allowing fleets to deploy multi-petabyte nodes that elevate the Memory IC market’s consumption of NAND wafers. Automotive over-the-air update strategies also fit SSD profiles, widening geographic uptake.

Rapid Adoption of High-Bandwidth Memory for AI Accelerators

HBM revenue already tops 30% of SK Hynix’s DRAM sales and is expected to reach 40% in Q4 2025 as accelerator demand outpaces supply.[4]Jin-Suk Choi, “Samsung Set to Triple HBM Output in 2024,” kedglobal.com HBM4 promises 5–6 TB/s per stack, quadrupling bandwidth over HBM3E and letting large language models converge faster. AMD’s MI350X pairs twelve-high HBM3E stacks totaling 288 GB near compute dies, illustrating tight memory-compute codesign in the Memory IC market. Suppliers remain sold out into 2026, giving them pricing power and funding for additional TSV capacity, which lifts the Memory IC market outlook.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Development and Fab Costs of Advanced Memory ICs High Development and Fab Costs of Advanced Memory ICs | -1.90% | Global, concentrated in leading-edge nodes | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.90% | Geographic Relevance:Global, concentrated in leading-edge nodes | Impact Timeline:Long term (≥ 4 years) |

DRAM/NAND Price Volatility and Cyclicality DRAM/NAND Price Volatility and Cyclicality | -1.60% | Global memory markets | Short term (≤ 2 years) | |||

Supply-Chain Disruptions and Critical-Material Shortages Supply-Chain Disruptions and Critical-Material Shortages | -1.20% | Global, with Asia-Pacific vulnerability | Medium term (2-4 years) | |||

Geopolitical Export Controls on Memory-Equipment Geopolitical Export Controls on Memory-Equipment | -0.80% | China, Russia, and restricted entities | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Development and Fab Costs of Advanced Memory ICs

Sub-10 nm DRAM lines demand USD 15–20 billion investments, with EUV scanners costing more than USD 160 million per tool. High-NA EUV adoption adds yet another capex layer, raising breakeven volumes, while HBM die-stacking consumes 2–3× more wafer starts than commodity DRAM.[5]Imec, “Imec Demonstrates Logic and DRAM Structures Using High NA EUV,” imec-int.com This capital burden narrows the field to deep-pocketed incumbents and slows node migration cycles inside the Memory IC market.

DRAM/NAND Price Volatility and Cyclicality

DDR4 spot prices surged 50% in May 2025 after makers curtailed legacy output to retool for DDR5 and HBM, lifting 8 GB modules from USD 1.75 to USD 2.73. Conversely, NAND ASPs slid 20% year-on-year amid new Chinese capacity, compressing margins and complicating inventory planning. Such swings deter predictable investment and can stall expansion within the Memory IC market during oversupply phases.

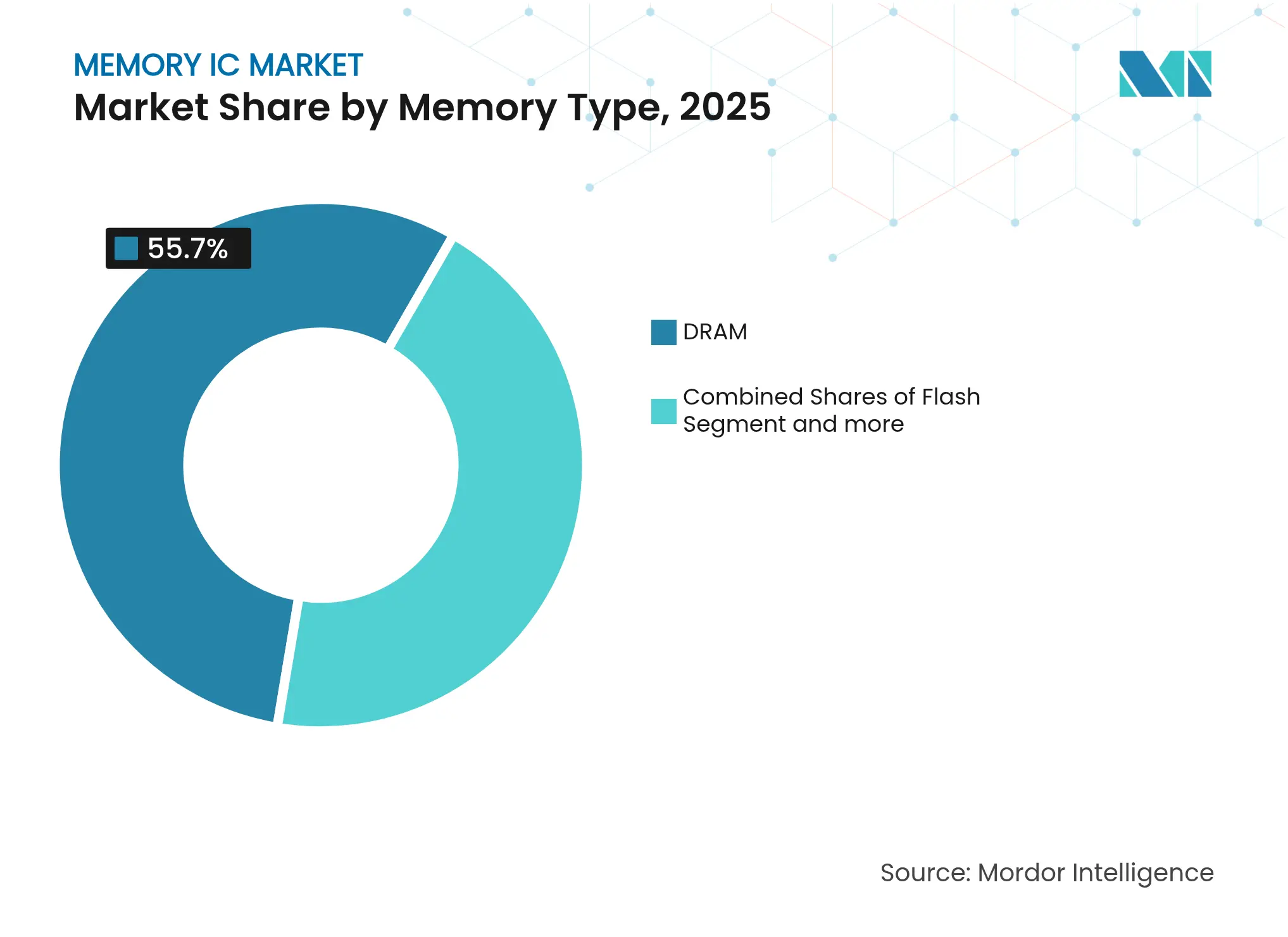

By Memory Type: DRAM Dominance Amid Flash Acceleration

DRAM supplied 55.70% of the Memory IC market share in 2025 and remains indispensable for AI training bandwidth. NAND flash, conversely, compounds at an 11.35% rate. 200-plus-layer 3D-NAND lowers cost per bit, expanding server boot drives and automotive storage footprints. NOR-flash sees renewed automotive traction, while MRAM secures design wins in industrial controllers where non-volatility and endurance matter.

Samsung’s stacked-DRAM roadmap signals 3D architectures that stretch conventional scaling. Emerging memories like ReRAM and 3D XPoint chase niche latency gaps, granting smaller vendors footholds in the wide-ranging Memory IC market. Application-specific optimization blurs the line between volatile and non-volatile categories, fostering hybrid hierarchies.

Note: Segment shares of all individual segments available upon report purchase

By Application: Mobile Foundation Shifts to Data-Center Growth

Smartphones and tablets led 2025 with 37.85% application share within the Memory IC market, yet servers and data centers rise at an 11.52% CAGR as AI workloads proliferate through 2031. Data-center nodes integrate 400 W accelerators sporting up to 288 GB HBM, magnifying per-socket memory spend.

Mobile devices counter by adopting LPDDR6, aligning handheld compute with on-device AI. Industrial IoT gateways and edge servers demand ruggedized components, while automotive ADAS combines DRAM, LPDDR, NOR, and SSDs in centralized vehicle computers.

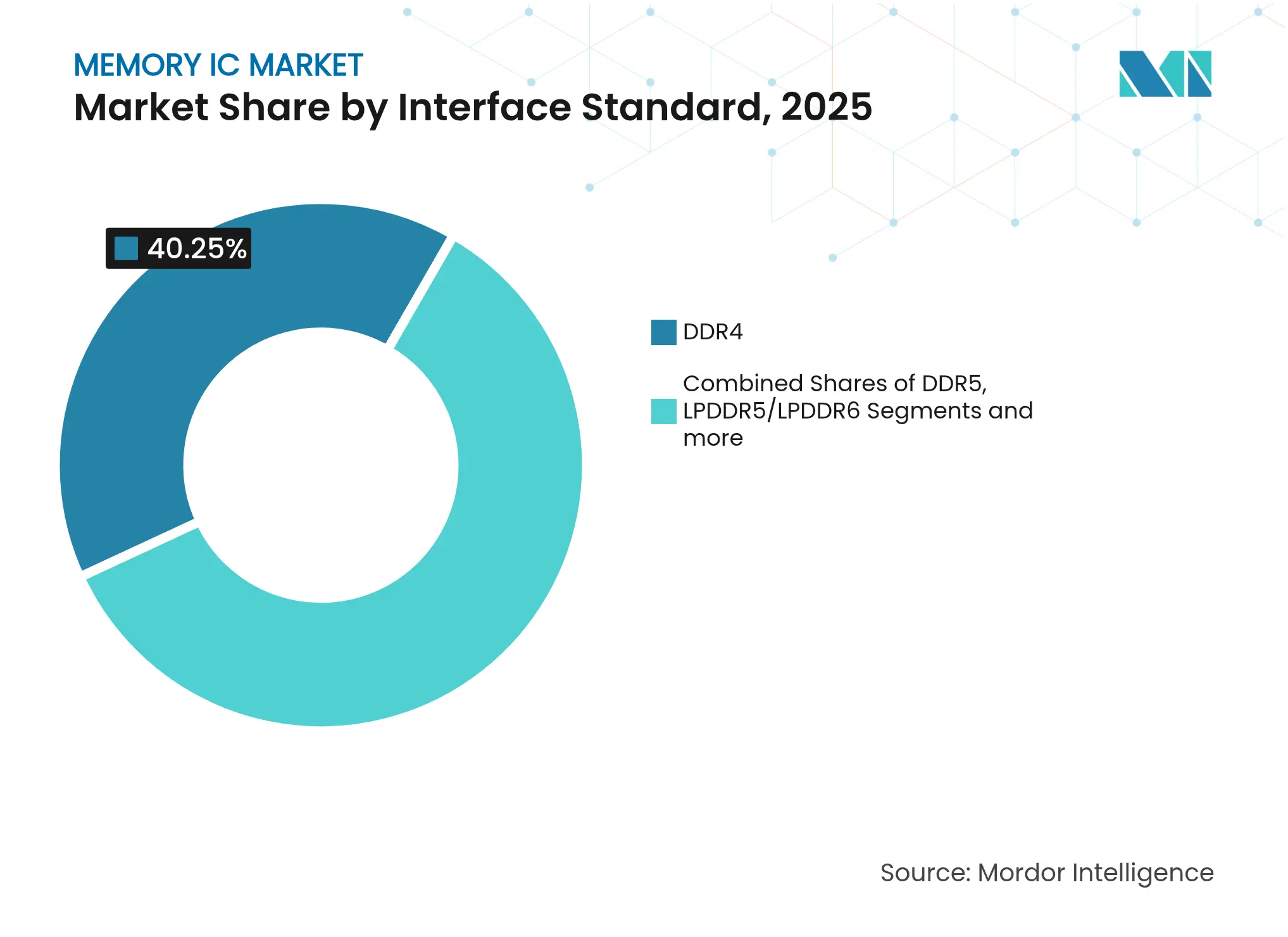

By Interface Standard: DDR4 Leadership Faces HBM Revolution

DDR4 still represented 40.25% of 2025 shipments inside the Memory IC market. However, DDR5 growth quickens, and HBM/HBM3/HBM3E races ahead at a 12.84% CAGR through 2031. JEDEC published DDR6 targets at 8.8–17.6 Gbps I/O for post-2027 adoption. LPDDR6 evolves to 24-bit channels at similar speeds, tailored for thermally constrained platforms.

PCIe 5.0 NVMe pushes SSD latencies down, while CXL disaggregates memory pools, enabling dynamic capacity allocation in hyperscale racks. Interface diversity underscores workload-centric engineering across the Memory IC market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Consumer Base Expands Through Automotive Innovation

Consumer electronics retained 45.90% of 2025 revenues, yet automotive’s 12.35% CAGR elevates its Memory IC market size contribution sharply through 2031. Vehicles are forecast to contain 278 GB of combined RAM and NAND by 2026, escalating toward multi-terabyte footprints by 2030. IT-telecom sectors reinforce edge and core networks with high-speed DRAM in 5G base stations.

Healthcare devices adopt fault-tolerant memories, and aerospace missions pilot radiation-hardened MRAM, validating spin-based storage before terrestrial rollouts. End-user variety diversifies revenue streams across the Memory IC market.

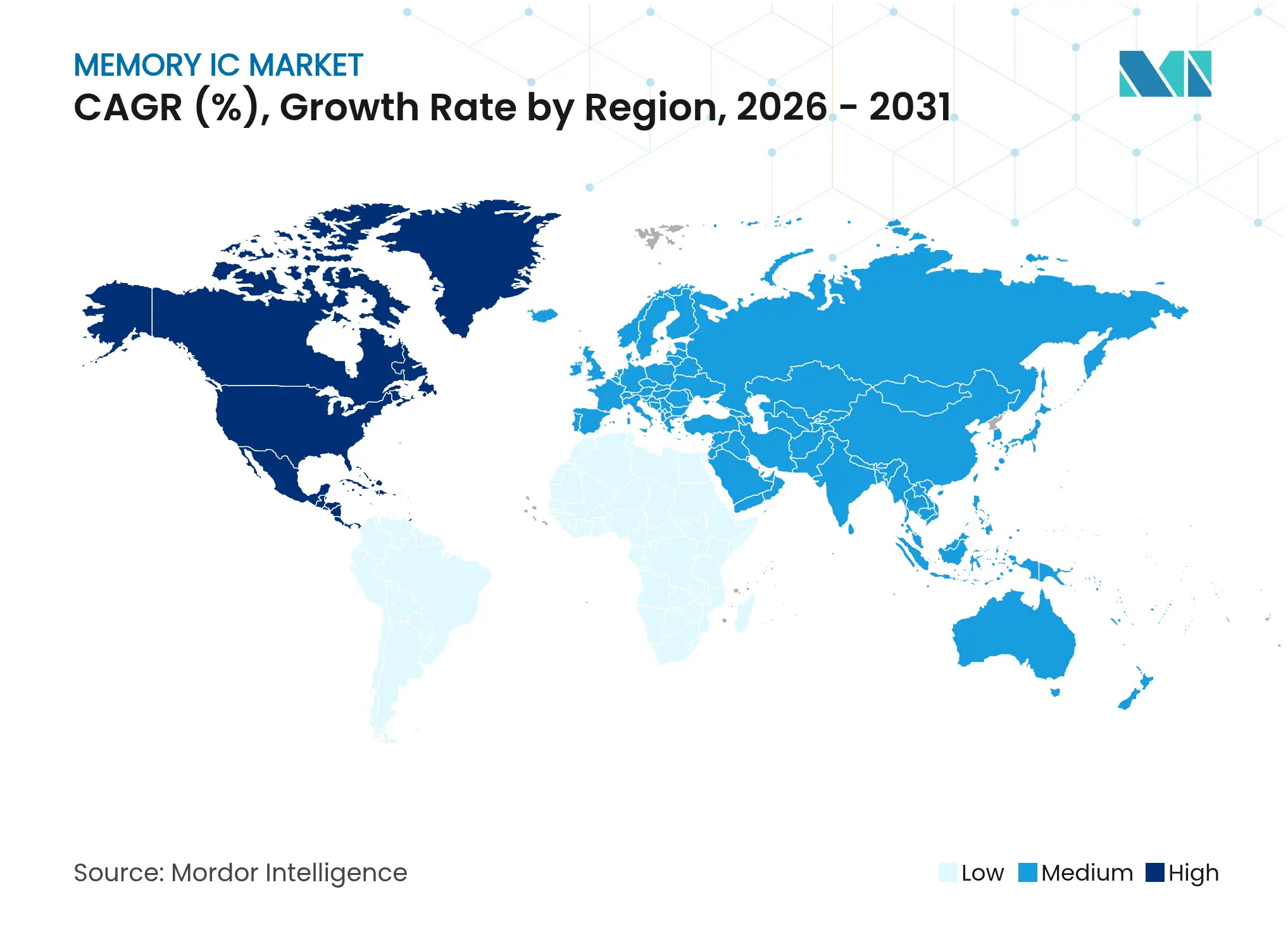

Asia-Pacific anchored 61.35% of 2025 shipments thanks to integrated supply chains spanning wafer fabrication to back-end assembly. Chinese vendor CXMT lifted DRAM share to 5%, while Samsung and SK Hynix reinvested more than USD 20 billion in R&D to preserve process leadership. Japan’s JPY 3.9 trillion (USD 25.7 billion) subsidy push and TSMC’s Kumamoto expansion widen regional manufacturing baselines. Export-control policies temper advanced tool shipments to China, potentially fragmenting technology nodes yet stimulating alternate capacity around the Memory IC market.

North America records the fastest 13.18% CAGR through 2031, propelled by the USD 52.7 billion CHIPS Act and Micron’s USD 125 billion investment plan that seeks 40% domestic DRAM output by 2030. Proximity to hyperscalers encourages co-development of leading-edge HBM and DDR6 products. Canada and Mexico supply chemicals and perform assembly, rounding out the regional ecosystem.

Europe leverages its automotive cluster, with Germany’s OEMs specifying ASIL-D certified LPDDR in next-gen ADAS stacks. The EU Chips Act’s EUR 43 billion (USD 49 billion) aims for 20% global capacity, but auditors forecast only 11.7% without further commitments. The region positions on specialty nodes such as embedded MRAM and security-certified memories inside the Memory IC market.

Middle East and Africa pursue digital-city and 5G rollouts, importing most components yet evaluating assembly lines tied to sovereign cloud projects. Latin America explores backend packaging to serve regional device makers. These nascent clusters contribute incremental volume to the Memory IC market, encouraged by supply-chain diversification.

Market Concentration

Samsung Electronics, SK Hynix, and Micron Technology retained a significant share of the 2024 DRAM supply, sustaining a high concentration in the Memory IC market. Samsung unveiled a 32 GB DDR5 part on 12 nm technology that doubles per-die capacity for AI servers. SK Hynix sampled 1c DDR5 and shipped early HBM4 modules to Nvidia, fortifying AI-centric positioning. Micron secured USD 6.165 billion CHIPS funding, expediting U.S. fab timelines and diversifying geopolitical exposure.

Challengers emerge: CXMT scales DRAM in China, Everspin expands MRAM lines targeting industrial controllers, and Marvell’s CXL accelerators tap pooled memory architectures. Partnerships gain prominence; SK Hynix collaborates with TSMC on advanced TSV stacking, while Intel and SoftBank form Saimemory to halve AI memory power draw within two years. Patent shields, packaging know-how, and fab incentives shape competition beyond simple bit-cost leadership in the Memory IC market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Memory integrated circuits are integrated circuits implemented in storage devices or used in digital devices to store data for computers. Both volatile and non-volatile memory for computer devices is created using memory-integrated circuits. They can be used in various digital and electronic devices, computers, and smartphones.

The Memory Integrated Circuit (IC) Market is segmented by Type (DRAM, Flash), End-user Industry (Consumer Electronics, Automotive, IT & Telecommunication, Healthcare), and Geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.