Automotive AI Accelerator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.85 Billion |

| Market Size (2031) | USD 63.21 Billion |

| Growth Rate (2026 - 2031) | 33.60% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive AI Accelerator Market Analysis by Mordor Intelligence

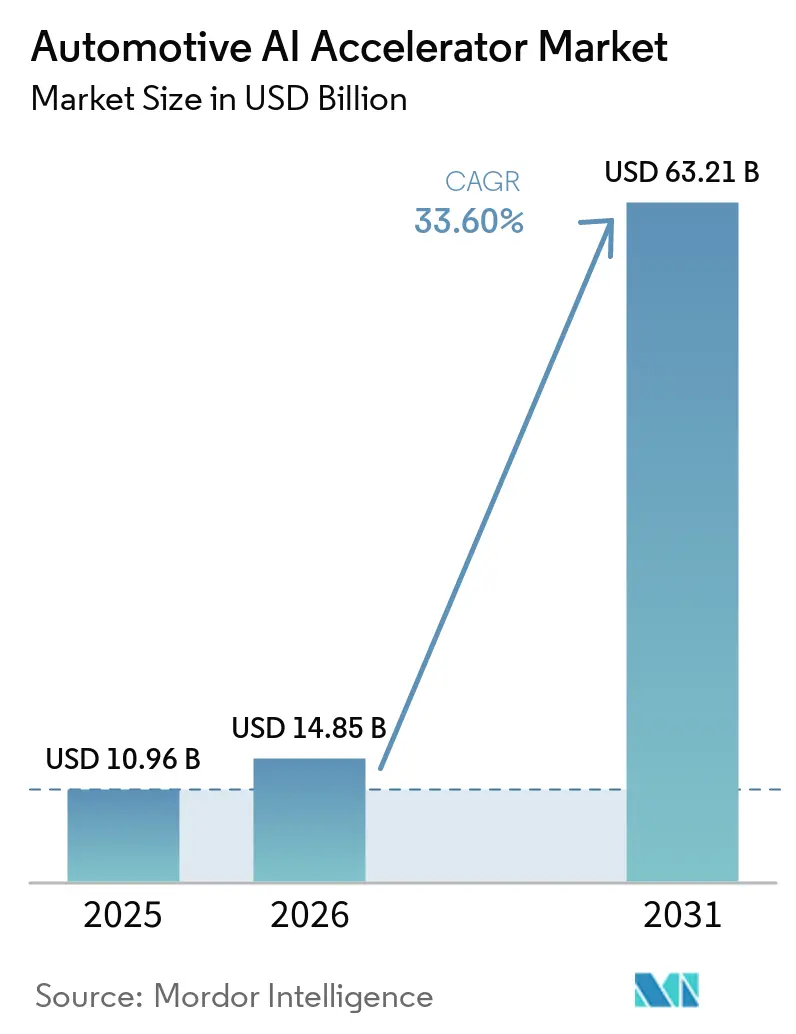

The automotive AI accelerator market size is expected to grow from USD 10.96 billion in 2025 to USD 14.85 billion in 2026 and is forecast to reach USD 63.21 billion by 2031 at 33.60% CAGR over 2026-2031. The 2026 base shows that the automotive AI accelerator market is already scaling well before full Level 3 and Level 4 rollout becomes common across global vehicle fleets. Demand is clustering around high-compute functions, where software-defined vehicle programs are replacing distributed ECU layouts with centralized compute platforms that can support perception, planning, cockpit, and update-driven feature expansion. Regulatory changes in safety and cybersecurity are also raising the minimum compute requirement for new vehicle programs, which keeps procurement activity strong even when vehicle production cycles remain uneven. Competition in the automotive AI accelerator market is now shaped by performance per watt, software lock-in, and the ability to support multi-domain workloads on one platform. Even with thermal and validation costs still acting as real constraints, the automotive AI accelerator market continues to attract sustained OEM and Tier-1 spending because AI compute is becoming part of the core vehicle architecture rather than an optional feature layer.

Key Report Takeaways

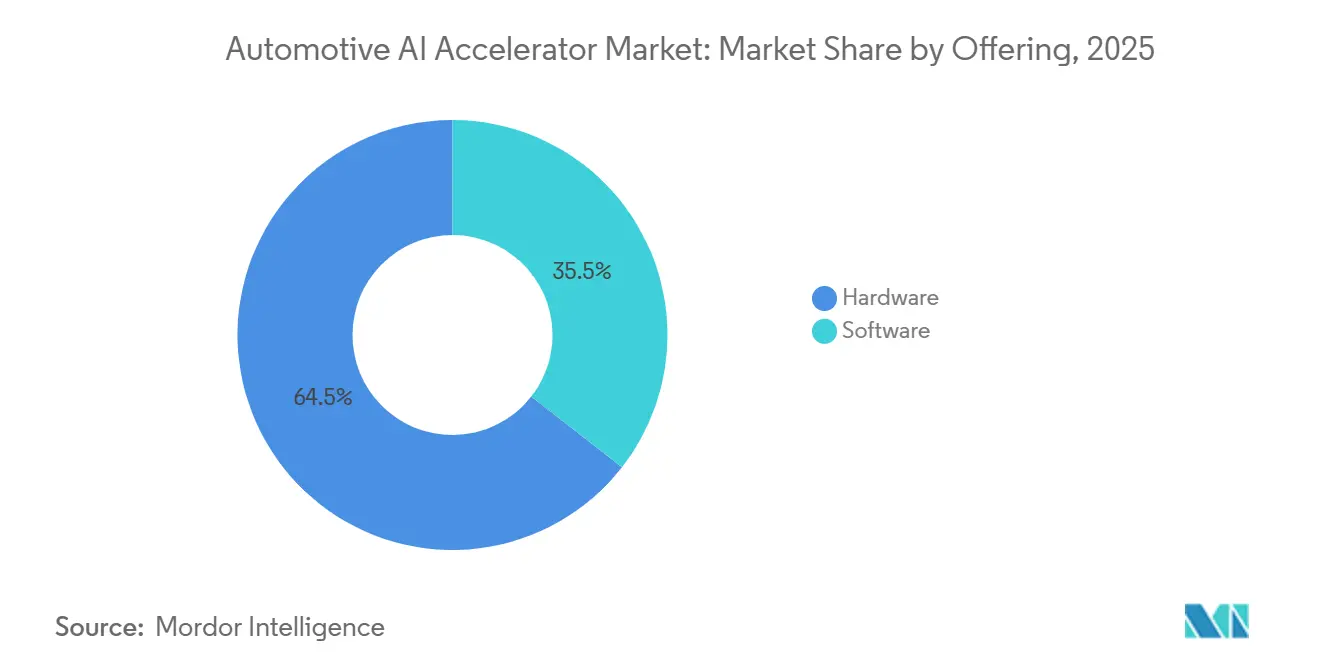

- By offering, hardware held 64.46% of revenue of the automotive AI accelerator market in 2025, while software is projected to expand at a 33.88% CAGR through 2031.

- By processor type, GPU-based accelerators accounted for 37.22% of revenue of the automotive AI accelerator market in 2025, while NPU and AI ASIC platforms are expected to record the fastest growth at 34.09% through 2031.

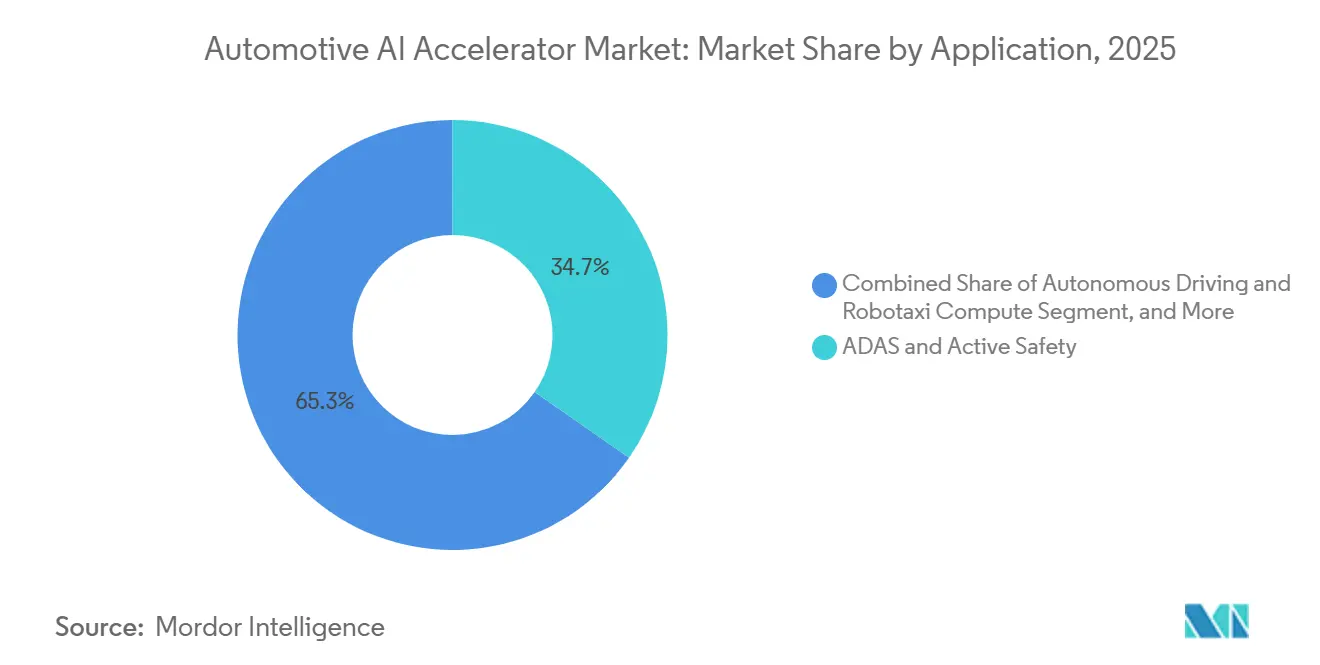

- By application, ADAS and active safety accounted for 34.66% of revenue in 2025, while autonomous driving and robotaxi compute are projected to grow at a 34.11% CAGR through 2031.

- By vehicle type, passenger vehicles held 68.78% of the automotive AI accelerator market share in 2025, while commercial vehicles are expected to grow at a 34.24% CAGR through 2031.

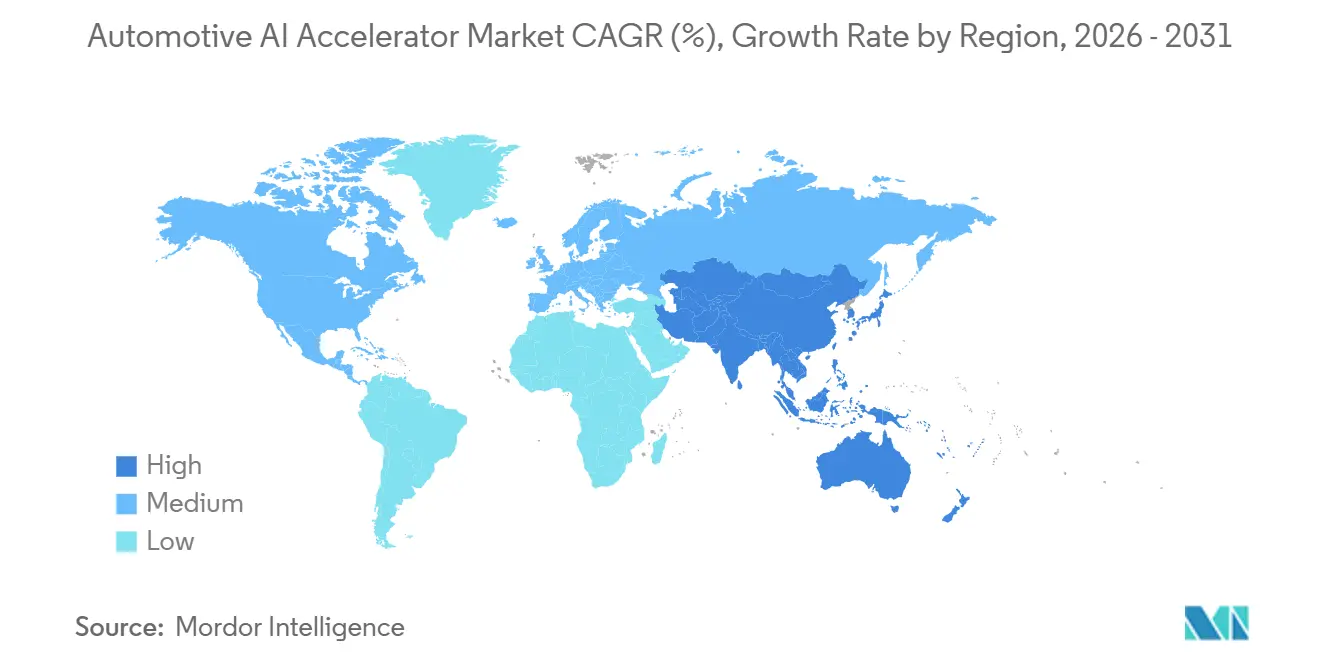

- By geography, Asia-Pacific accounted for 38.18% of the automotive AI accelerator market size in 2025, while the Middle East and Africa are projected to expand at a 34.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive AI Accelerator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of ADAS And Active Safety Functions | +9.5% | Global, with intensity in Europe, China, and North America | Short term (≤ 2 years) |

| Growing Demand For On-Vehicle Real-Time Inference | +7.2% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Software-Defined Vehicle Architectures Increasing Centralized Compute Demand | +5.8% | Global, led by Europe and China | Medium term (2-4 years) |

| Expansion Of Level 2 Plus And Level 3 Automation Programs | +4.1% | North America, Europe, China, South Korea | Medium term (2-4 years) |

| Increasing AI Content In Intelligent Cockpits And Driver Monitoring | +3.2% | Global, early gains in China and Europe | Medium term (2-4 years) |

| Automaker And Semiconductor Co-Development Of Automotive Edge AI Platforms | +2.5% | Global, concentrated in China, the United States, the European Union, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption Of ADAS And Active Safety Functions

Euro NCAP’s 2026 revision changed how new vehicles are assessed and introduced a 100-point Safe Driving category, which raised the practical compute threshold for mainstream safety programs in Europe.[1]Euro NCAP, “Euro NCAP Announces 2026 Protocol Changes to Tackle Modern Driving Risks,” Euro NCAP, euroncap.com This has pushed the automotive AI accelerator market toward larger ADAS procurement programs because features such as braking support, lane assistance, and driver monitoring now carry greater approval weight in volume vehicles. Mobileye said in January 2026 that its 8-year revenue pipeline reached USD 24.5 billion at the end of 2025, showing how design wins have expanded across large OEM programs.[2]Mobileye Global Inc., “Mobileye Releases Fourth-Quarter and Full-Year 2025 Results and Provides Business Overview,” Mobileye Investor Relations, ir.mobileye.com It also announced future delivery of more than 19 million EyeQ6H-based Surround ADAS systems across 2 top-10 automaker programs, which shows that AI-enabled safety hardware is moving into very large production runs. As these functions shift from premium trims into broader lineups, the automotive AI accelerator market gains volume, while suppliers face pressure to bundle more functions on each compute platform to protect margins.

Growing Demand For On-Vehicle Real-Time Inference

The automotive AI accelerator market is seeing stronger demand for on-vehicle inference because safety, responsiveness, and feature reliability depend on local processing rather than delayed remote execution. Horizon Robotics said its Journey 6 series was being deployed across more than 100 vehicle models in 2025 and was tracking toward 10 million cumulative units, which signals that production programs are favoring local AI execution at scale. Qualcomm and Leapmotor presented a central computer in January 2026 that combines Snapdragon Cockpit Elite and Ride Elite on one architecture, which reflects a clear move toward real-time multi-domain processing inside the vehicle.[3]Qualcomm Technologies, Inc., “Leapmotor and Qualcomm Debuts World’s First Automotive Central Computer Powered by Snapdragon Cockpit Elite and Snapdragon Ride Elite Platforms,” Qualcomm News Releases, qualcomm.com This shift matters for the automotive AI accelerator market because local inference does not just add compute demand, it changes the kind of compute demand, favoring platforms that can sustain AI tasks within tight automotive power, packaging, and safety limits. It also raises the value of processors that can handle cockpit, sensing, and active safety workloads together, since OEMs gain lower latency and simpler software coordination from that setup.

Software-Defined Vehicle Architectures Increasing Centralized Compute Demand

The automotive AI accelerator market is also benefiting from the move away from large distributed ECU fleets and toward centralized vehicle computing. Qualcomm’s Ride Flex platform was positioned for mixed-criticality workloads, allowing cockpit and ADAS functions to run on the same SoC, which matches the architectural direction of software-defined vehicles. Leapmotor and Qualcomm’s joint central computer announcement in January 2026 showed that this design has already moved from concept to production-oriented deployment. In the automotive AI accelerator market, that shift increases compute density at the remaining central nodes, even if the number of separate control units per vehicle declines. Once an OEM builds its software stack, toolchain, and validation work around a specific compute family, supplier replacement becomes slower and more expensive, which strengthens long-cycle revenue opportunities for incumbent chip and platform vendors.

Expansion Of Level 2 Plus And Level 3 Automation Programs

The expansion of Level 2 Plus and Level 3 programs is giving the automotive AI accelerator market a wider production base for high-performance compute. NVIDIA said in March 2026 that BYD, Geely, Isuzu, and Nissan were adopting DRIVE Hyperion for Level 4-ready vehicles, which shows that current sourcing decisions are being made on platforms with headroom beyond today’s immediate feature set. In the same month, Hyundai Motor, Kia, and NVIDIA expanded their partnership for next-generation autonomous driving technology, which pointed to a platform-level commitment rather than a single-model program. Qualcomm and BMW also introduced a jointly developed Snapdragon Ride Pilot system for the BMW iX3 Neue Klasse, and the company said the system had been validated in more than 60 countries. For the automotive AI accelerator market, this means the same silicon platform can support current L2 Plus deployment and later software-led upgrades, which helps OEMs spread qualification cost across a longer product cycle.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Thermal Design And Power Efficiency Constraints | -3.8% | Global, accentuated in EV-heavy markets such as China, Europe, and South Korea | Short term (≤ 2 years) |

| Functional Safety And Validation Complexity | -3.2% | Global, most acute where ISO 26262 and ISO PAS 8800 compliance is mandatory | Medium term (2-4 years) |

| Long Qualification Cycles And Automotive Grade Supply Risk | -2.1% | Global, with supply concentration risk in TSMC-dependent programs | Long term (≥ 4 years) |

| Cybersecurity Exposure In Multi-Domain AI Architectures | -1.8% | Global, with the highest regulatory burden in UNECE WP.29 contracting states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Thermal Design And Power Efficiency Constraints

Thermal design remains a real restraint for the automotive AI accelerator market because higher compute density adds cooling, packaging, and energy management burdens inside the vehicle. The issue is more visible in EV programs, where added compute draw can work directly against range and thermal stability targets, especially when several AI functions run at the same time. STMicroelectronics introduced Stellar P3E in February 2026 as the first automotive microcontroller with an integrated Neural-ART accelerator, and the product was positioned for edge AI use cases that need a lower thermal footprint than larger central processors. That product direction shows why the automotive AI accelerator market is not only rewarding raw TOPS growth, it is also rewarding better efficiency and more task-specific silicon. Vendors that cannot balance performance with automotive power budgets risk losing share in volume programs, even when their compute capability remains technically strong.

Functional Safety And Validation Complexity

Functional safety rules keep slowing deployment in the automotive AI accelerator market because AI systems must prove safe behavior across a wide operating range before production approval. ISO PAS 8800:2024 set out a dedicated safety framework for artificial intelligence in road vehicles, which added structure to AI validation but also increased documentation and traceability expectations. UNECE Regulation No. 155 also remains mandatory for type approvals across a wide group of contracting states, which means cybersecurity management must now be built into the validation burden for multi-domain AI platforms. SAE research published in 2026 showed that AI-enhanced predictive fault management can improve diagnostic coverage while remaining within ASIL-D expectations, but the same work also underscored the continued need for engineering rigor. The result is that OEMs and Tier-1 suppliers often stay with incumbent compute suppliers longer than they would in a less regulated electronics category, because requalification takes time and consumes engineering capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Anchors Revenue While Software Deepens Value Capture

Hardware accounted for 64.46% of revenue in 2025, which shows that the automotive AI accelerator market still depends first on silicon, memory access, packaging, and board-level integration before software monetization can scale. This mix fits the current stage of the market because OEMs must first secure the compute base required for ADAS, cockpit, and future autonomy programs. The hardware layer also remains the part of the stack with the largest upfront cost, since automotive-grade qualification, long product life requirements, and vehicle integration all push spending toward proven semiconductor platforms. In the automotive AI accelerator market, this keeps hardware spending elevated even when software becomes a larger source of future margin. The segment’s position also reflects the fact that compute capability must be installed before update-led business models can generate recurring value.

Software is still the fastest-growing offering segment, with a 33.88% CAGR expected through 2031, and that direction says the value pool is gradually broadening beyond one-time chip sales. The automotive AI accelerator industry is shifting toward systems where features can be activated, refined, or extended through software updates once the underlying compute has already been placed in the vehicle. Qualcomm’s mixed-domain central compute approach and STMicroelectronics’ edge AI controller launch both point to platforms where multiple software workloads can share the same silicon foundation. That means software growth is not replacing hardware growth inside the automotive AI accelerator market, it is building on top of it by making each installed compute platform economically useful for longer. As vehicle architectures centralize, software also becomes harder to separate from hardware choice, which raises switching costs and makes platform ecosystems more important.

By Processor/Accelerator Type: NPU And AI ASIC Designs Gain Ground Against GPU Leadership

GPU-based accelerators held 37.22% of revenue in 2025, which shows that the automotive AI accelerator market still leans on established high-compute platforms and their mature software environments. GPUs entered the category with a clear advantage in autonomous driving development because they supported large neural workloads, broad tool access, and easier scaling from research into production. That installed base still matters because many OEM and robotaxi programs have already built perception and planning stacks around GPU-compatible environments. In the automotive AI accelerator market, this gives GPU suppliers an advantage in high-end domain controllers and complex autonomy programs where software continuity matters as much as raw performance. It also explains why leadership at the top end can remain durable even as other processor types expand faster.

NPU and AI ASIC platforms are projected to grow at a 34.09% CAGR through 2031, which shows that the next phase of the automotive AI accelerator market is likely to reward inference efficiency more directly. Horizon Robotics said its Journey 6 family was being deployed across more than 100 models, which shows how purpose-built AI compute can move beyond pilot programs into broad production ADAS volumes. STMicroelectronics also positioned its Stellar P3E for edge intelligence tasks that benefit from integrated AI acceleration with a smaller thermal and system burden than larger multi-chip setups. Heterogeneous SoCs will still matter because many programs need CPU, graphics, signal, and AI resources together, but the automotive AI accelerator industry is clearly moving toward more specialized inference blocks within those broader designs. As thermal limits, power budgets, and cost pressure become tighter, the fastest gains are likely to come from processor types that can deliver more useful local AI per watt rather than the highest theoretical performance.

By Application: ADAS Provides The Broadest Volume Base While Robotaxi Programs Lift Performance Needs

ADAS and active safety accounted for 34.66% of revenue in 2025, giving this application group the largest production footprint in the automotive AI accelerator market. That lead reflects the simple fact that camera perception, braking support, lane assistance, and related functions already reach far more vehicles than full autonomy programs. The automotive AI accelerator market therefore still gets much of its installed volume from systems that improve conventional driving safety rather than from vehicles built mainly around driverless operation. Euro NCAP’s 2026 scoring changes further support this pattern because they increase the practical value of AI-enabled safety functions in mainstream vehicle approvals. Even when the most visible product launches focus on advanced autonomy, the largest day-to-day hardware flow still comes from ADAS deployments across broader vehicle portfolios.

Autonomous driving and robotaxi compute is projected to grow at a 34.11% CAGR through 2031, which makes it the fastest-moving application layer in the automotive AI accelerator market. NVIDIA expanded DRIVE Hyperion partnerships in 2026 and added more vehicle and manufacturing partners, which shows how supplier roadmaps are being shaped by platforms that can support L4-ready compute needs. Dubai’s Roads and Transport Authority also launched commercial autonomous taxi operations in March 2026, which gave the segment a visible operating example rather than a trial-only reference point. At the same time, intelligent cockpit and driver monitoring functions are widening the application base, with Mobileye securing a major U.S. driver monitoring production program in March 2026. That mix means the automotive AI accelerator market is being shaped by two related currents, broad ADAS volume at one end and high-performance autonomy roadmaps at the other.

By Vehicle Type: Passenger Vehicles Lead Today While Commercial Fleets Set The Faster Growth Pace

Passenger vehicles held 68.78% of 2025 revenue and therefore represented the largest base of demand in the automotive AI accelerator market. This lead reflects both higher unit volumes and stronger feature spread across passenger cars, where ADAS, infotainment, cabin sensing, and software-defined functions are reaching more trim levels. The automotive AI accelerator market size in passenger vehicles also benefits from the fact that safety and convenience features can be rolled out across broad model families with less operational specialization than in heavy freight fleets. OEMs in this segment are also under direct pressure from consumer expectations, safety ratings, and update-led differentiation, all of which support continued AI compute integration. As a result, passenger vehicles remain the anchor segment for current revenue even as other vehicle groups become strategically important.

Commercial vehicles are projected to expand at a 34.24% CAGR through 2031, making them the fastest-growing vehicle type in the automotive AI accelerator market. NVIDIA’s March 2026 announcements and the broader DRIVE Hyperion ecosystem expansion showed continued momentum behind heavy-duty autonomous and high-compute fleet programs. Applied Intuition and TRATON said in 2026 that TRATON ONE OS was being developed for global truck fleets, which points to a more centralized and software-led computing path in commercial vehicles as well. The commercial story is different from the passenger story because operators buy compute as part of uptime, route automation, and driver replacement logic, not only as a feature upgrade. That creates a higher functional floor for platform capability, which can keep revenue per unit attractive in the automotive AI accelerator market even when fleet volumes remain smaller than passenger car volumes.

Geography Analysis

Asia-Pacific accounted for 38.18% of revenue in 2025, giving the region the leading position in the automotive AI accelerator market. China remains central to that lead because the region combines strong EV production, active ADAS rollout, and growing interest in closer chip and automaker coordination. Horizon Robotics said its Journey 6 series was being deployed across more than 100 vehicle models, which highlights how local AI compute platforms are gaining broad production relevance in the region. Japan also remains important through established semiconductor and vehicle electronics capability, and Renesas continues to position the R-Car V4H for Level 2 Plus and Level 3 use cases with NCAP-focused functionality. South Korea adds strength through automotive-grade memory supply, while India is becoming a more visible destination for future programs after Mobileye reported a major Mahindra design win covering at least 6 vehicle models.

The Middle East and Africa are expected to grow at a 34.32% CAGR through 2031, making it the fastest-growing regional block in the automotive AI accelerator market. This growth does not rest on broad domestic vehicle manufacturing, but on fast-moving smart mobility deployment, public backing for autonomous transport, and a willingness to commercialize advanced services early. Dubai’s Roads and Transport Authority launched commercial autonomous taxi operations through Uber and Apollo Go in March 2026, and WeRide also began fully driverless commercial robotaxi operations in Dubai with Uber. Those moves matter because they create live demand for compute platforms that can support production-grade autonomy in real operating conditions. In the automotive AI accelerator market, this makes the region a smaller revenue base today, but an important signal market for future deployment models.

Europe and North America form the next major regional cluster in the automotive AI accelerator market, though their strengths are different. Europe is being pushed by tighter safety frameworks and faster ADAS content expansion, which supports higher compute needs in mainstream production programs. Qualcomm’s jointly developed system with BMW and NVIDIA’s work with Mercedes-Benz show how Europe remains important for premium vehicle programs and globally deployable software-hardware stacks. North America remains highly relevant in autonomous trucking and advanced compute deployment, while South America is still an early-stage market where AI content mainly enters through imported vehicles that already meet stricter safety expectations elsewhere.

Competitive Landscape

The automotive AI accelerator market remains moderately concentrated at the platform level, even though the wider supplier base is still broad. NVIDIA, Qualcomm, and Mobileye remain the most visible leaders in large-scale design wins, while specialized chipmakers, software providers, and edge AI firms continue to compete for narrower roles around them. This structure means the automotive AI accelerator market is not dominated by a single supplier, but it is increasingly shaped by a small group of firms that control the reference architectures, software environments, and validation pathways that OEMs rely on. Once those elements are in place, the cost of switching suppliers rises because a compute platform affects operating systems, safety workflows, feature roadmaps, and the pace of later software updates. That gives leading vendors a durable advantage without making the field fully closed to challengers.

NVIDIA’s strategy in the automotive AI accelerator market centers on full-stack integration. The company has tied DRIVE AGX compute, DriveOS, and the broader DRIVE Hyperion framework into a unified development path, and its 2026 partner expansion with BYD, Geely, Isuzu, Nissan, Hyundai Motor, and Kia showed how that ecosystem approach scales across different OEM relationships. Qualcomm is taking a different route by pushing mixed-domain platforms that fuse cockpit and ADAS tasks on one chip, and its work with Leapmotor and BMW shows that this argument is resonating with OEMs that want lower hardware sprawl and easier software coordination. Mobileye remains a major force where scalable ADAS, driver monitoring, and production volume matter most, supported by its USD 24.5 billion pipeline and expanding EyeQ6 deployments.

The most open competitive space in the automotive AI accelerator market sits below the top end of autonomy. Hailo’s 10H edge AI accelerator, which the company positioned for 2026 production use, reflects demand for low-power compute that can handle cockpit and monitoring workloads without the thermal burden of larger data-center-derived designs. STMicroelectronics is also aiming at this gap with the Stellar P3E, which brings integrated AI acceleration into an automotive microcontroller class rather than only into large centralized processors. These moves matter because many mid-range programs need enough AI for L2 Plus, cabin sensing, or predictive maintenance, but do not need the cost and power profile of the most advanced autonomy platforms. Cybersecurity readiness is also becoming a competitive differentiator, since UNECE Regulation No. 155 requires vehicle programs to embed cyber management into approval workflows, which favors vendors that can support compliance as part of the platform rather than only selling silicon. That is why competition in the automotive AI accelerator market is increasingly moving from pure chip performance toward broader platform credibility, validation support, and the ability to carry several AI functions on one architecture.

Automotive AI Accelerator Industry Leaders

NVIDIA Corporation

Qualcomm Technologies, Inc.

NXP Semiconductors N.V.

Intel Corporation

Mobileye Global Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA announces a major expansion of the DRIVE Hyperion robotaxi-ready platform ecosystem at GTC Taipei, adding Foxconn as a strategic manufacturing partner for Level 4-ready electric vehicle fleets, with initial deployment targeting Kaohsiung and broader Asia rollout planned.

- May 2026: Stellantis and Qualcomm Technologies expand their multi-year partnership to power next-generation Stellantis vehicles with Snapdragon Digital Chassis SoCs, including the Snapdragon Ride Pilot ADAS platform enabling active safety through Level 2-plus hands-free autonomy across millions of vehicles.

- March 2026: NVIDIA announces that BYD, Geely, Isuzu, and Nissan are building Level 4-ready vehicles on the NVIDIA DRIVE Hyperion platform, and that Hyundai Motor and Kia have expanded their NVIDIA collaboration to develop a scalable autonomous driving stack from L2 to L4.

- March 2026: Mobileye secures a major DMS production program with a leading US automaker, integrating the Mobileye Driver Monitoring System on EyeQ6L SoCs across millions of vehicles with start of production targeted for 2027, expanding consolidated ADAS and in-cabin sensing scope.

Global Automotive AI Accelerator Market Report Scope

The Automotive AI Accelerator Market refers to the market for specialized hardware and software used to run AI workloads inside vehicles, such as ADAS, autonomous driving, in-cabin sensing, and voice or vision-based features. It includes AI processors, GPUs, NPUs, and related compute platforms that enable real-time perception, decision-making, and sensor fusion in cars.

The Automotive AI Accelerator Market Report is Segmented by Offering (Hardware, and Software), Processor Type (GPU-Based Accelerators, NPU / AI ASIC Accelerators, FPGA-Based Accelerators, DSP / Vision Processing Accelerators, and Heterogeneous AI SoCs), Application (ADAS and Active Safety, Autonomous Driving and Robotaxi Compute, Intelligent Cockpit and In-Cabin AI, Telematics and Connected Vehicle Services, and Predictive Maintenance and Fleet Intelligence), Vehicle Type (Passenger Vehicles, and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| GPU-Based Accelerators |

| NPU / AI ASIC Accelerators |

| FPGA-Based Accelerators |

| DSP / Vision Processing Accelerators |

| Heterogeneous AI SoCs |

| ADAS and Active Safety |

| Autonomous Driving and Robotaxi Compute |

| Intelligent Cockpit and In-Cabin AI |

| Telematics and Connected Vehicle Services |

| Predictive Maintenance and Fleet Intelligence |

| Passenger Vehicles |

| Commercial Vehicles |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Offering | Hardware | |

| Software | ||

| By Processor / Accelerator Type | GPU-Based Accelerators | |

| NPU / AI ASIC Accelerators | ||

| FPGA-Based Accelerators | ||

| DSP / Vision Processing Accelerators | ||

| Heterogeneous AI SoCs | ||

| By Application | ADAS and Active Safety | |

| Autonomous Driving and Robotaxi Compute | ||

| Intelligent Cockpit and In-Cabin AI | ||

| Telematics and Connected Vehicle Services | ||

| Predictive Maintenance and Fleet Intelligence | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the automotive AI accelerator market?

The automotive AI accelerator market was at USD 10.96 billion in 2025, reached USD 14.85 billion in 2026, and is forecast to reach USD 63.21 billion by 2031 at a 33.60% CAGR.

Which application area leads demand for automotive AI accelerators?

ADAS and active safety led demand with 34.66% of revenue in 2025 because these functions already ship across a far larger vehicle base than full autonomy programs.

Which processor type is growing the fastest in vehicle AI compute?

NPU and AI ASIC platforms are projected to grow the fastest at 34.09% through 2031 as automakers look for stronger inference efficiency and lower thermal burden.

Why is Asia-Pacific leading this space?

Asia-Pacific held 38.18% of revenue in 2025 because the region combines high vehicle output, strong EV activity, local chip programs, and a deep automotive electronics base.

What is pushing commercial vehicles to adopt more AI compute?

Commercial vehicles are expected to grow at 34.24% through 2031 as autonomous trucking, uptime management, and centralized fleet software raise the need for higher-capability onboard compute.

What are the main barriers slowing wider adoption?

Thermal limits, power efficiency pressure, functional safety validation, cybersecurity compliance, and long qualification cycles continue to slow platform changes and extend development timelines.

Page last updated on: