IT Hardware Refresh Cycle Optimization Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 3.18 Billion |

| Growth Rate (2026 - 2031) | 17.33% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IT Hardware Refresh Cycle Optimization Software Market Analysis by Mordor Intelligence

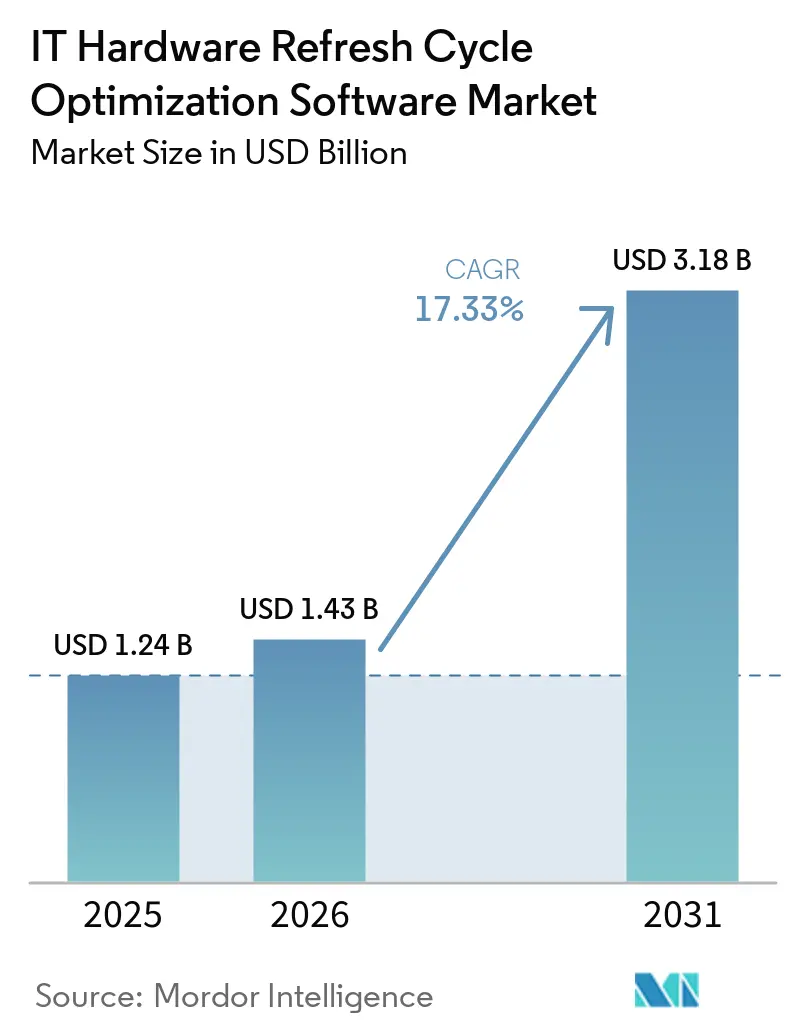

The IT Hardware Refresh Cycle Optimization Software Market size is projected to expand from USD 1.24 billion in 2025 and USD 1.43 billion in 2026 to USD 3.18 billion by 2031, registering a CAGR of 17.33% between 2026 and 2031. The IT Hardware Refresh Cycle Optimization Software Market is moving on the back of delayed device replacement across 2022 to 2024, which left many enterprises with aging fleets and weak asset records. The end of Windows 10 support in 2025 pushed many organizations to review endpoint readiness and exposed the limits of spreadsheet-led tracking, which lifted demand for software built around lifecycle planning and replacement governance. Compliance pressure has also moved hardware disposition and refresh planning into formal operating processes, especially in organizations that need a clear asset trail and better audit readiness. In the IT Hardware Refresh Cycle Optimization Software Market, vendors are expanding their offerings through acquisitions, workflow integration, and stronger discovery features, while smaller vendors are finding a foothold in mid-market accounts and in industries where legacy tools still leave gaps. The IT Hardware Refresh Cycle Optimization Software Market also faces short-term friction from budget deferrals and system integration issues, yet the gap between manual practice and policy-led lifecycle management continues to support demand through 2031.

Key Report Takeaways

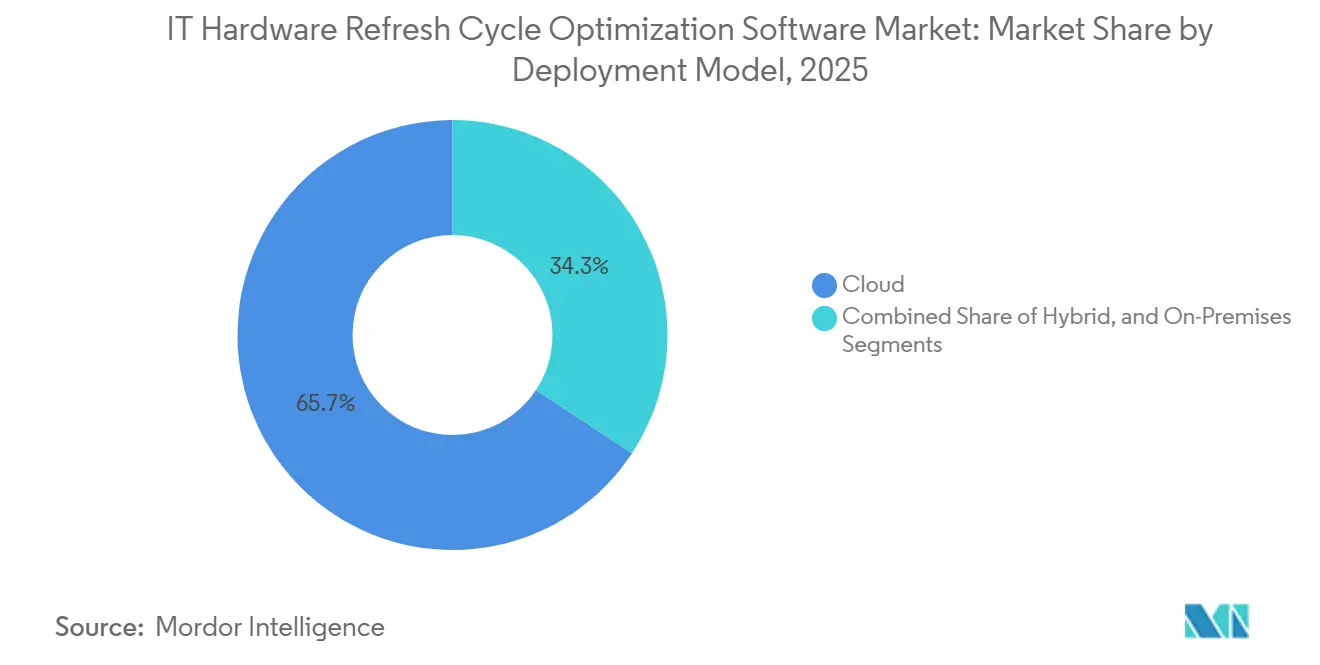

- By deployment model, cloud-based platforms led with 65.74% revenue share of the IT Hardware Refresh Cycle Optimization Software Market in 2025, while hybrid deployment is projected to expand at an 18.05% CAGR through 2031.

- By enterprise size, large enterprises held 64.12% of the IT Hardware Refresh Cycle Optimization Software Market share in 2025, while small and medium enterprises recorded the highest projected CAGR at 18.21% through 2031.

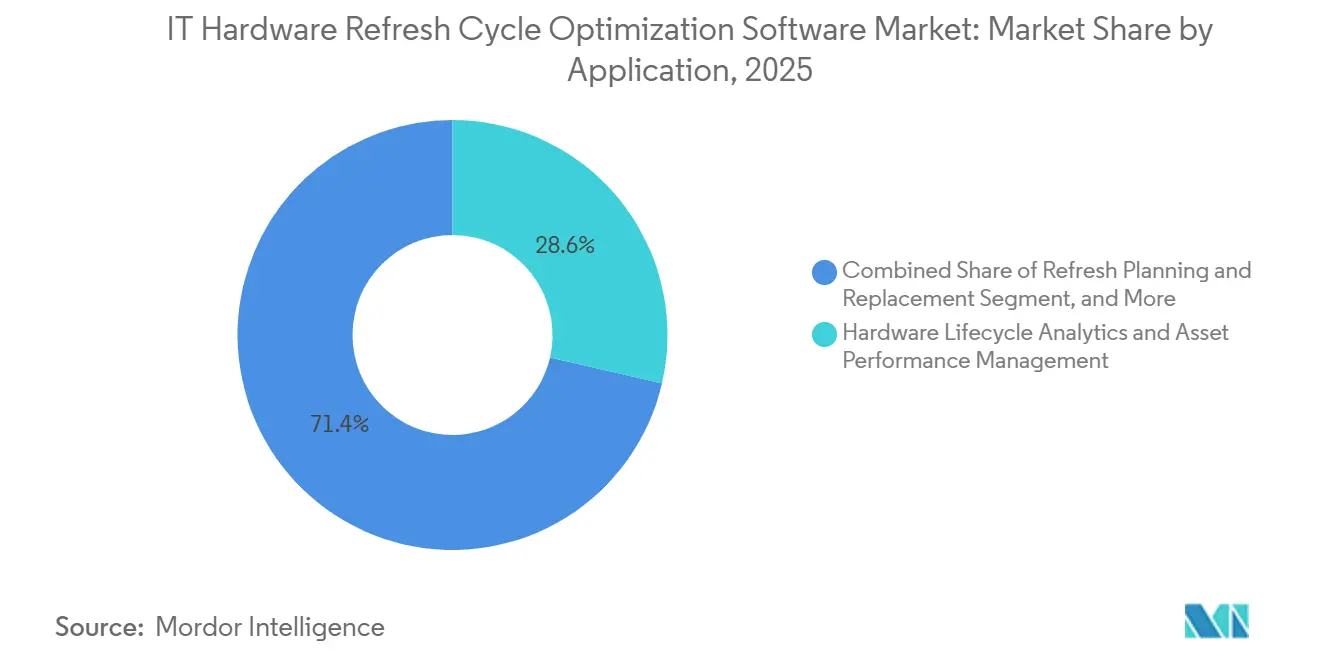

- By application, hardware lifecycle analytics and asset performance management accounted for 28.63% of the market share in 2025, while refresh planning and replacement optimization are expected to grow at a 18.45% CAGR through 2031.

- By end user, IT and telecom accounted for 27.41% of revenue in 2025, while retail and e-commerce are projected to expand at a 17.92% CAGR through 2031.

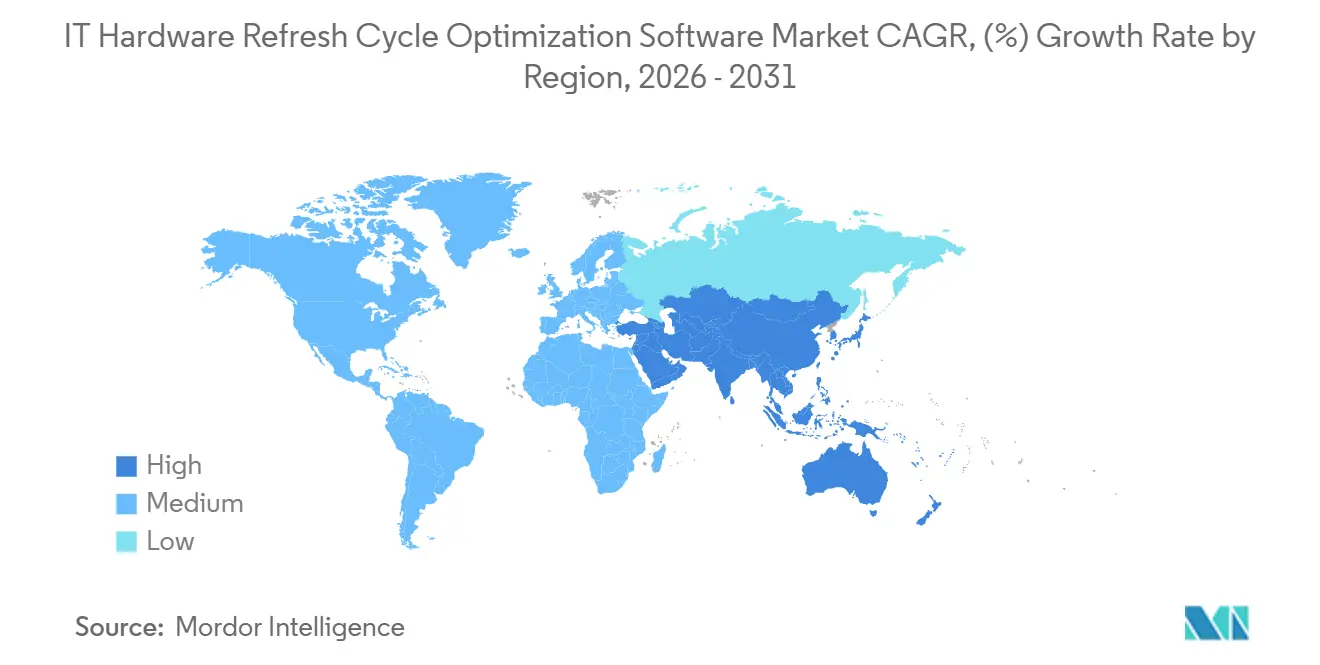

- By geography, Europe led with 34.56% revenue share of the IT Hardware Refresh Cycle Optimization Software Market in 2025, while Asia-Pacific recorded the highest projected CAGR at 18.34% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IT Hardware Refresh Cycle Optimization Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Hardware Refresh Backlogs | +3.8% | Global, with strong pressure in North America and Europe | Short term (≤ 2 years) |

| Windows and Endpoint Operating System End-Of-Support Waves | +3.2% | Global, led by North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Shift To Predictive Lifecycle Optimization | +2.9% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Audit Pressure From Compliance Gaps | +2.4% | North America and Europe | Medium term (2-4 years) |

| AI-Based Failure Prediction And Replacement Timing | +1.8% | Global, with early uptake in North America and Asia-Pacific | Medium term (2-4 years) |

| Sustainability-Linked Asset Renewal And E-Waste Reduction Goals | +1.2% | Europe, with wider global spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Enterprise Hardware Refresh Backlogs

Deferred hardware spending from 2022 to 2024 left many enterprises with a larger-than-usual set of devices nearing the end of life, creating a durable demand pool for the IT Hardware Refresh Cycle Optimization Software Market.[1]Microsoft Support, “Windows 10 Support Has Ended on October 14, 2025,” Microsoft, support.microsoft.com The issue is not only the age of devices; delayed replacements also weakened asset records and made it harder for IT teams to know what was still active, repairable, or ready for redeployment. In the IT Hardware Refresh Cycle Optimization Software Market, this has raised interest in software that can clean discovery data, classify device condition, and support replacement timing with clearer rules. The result is a shift away from occasional refresh projects toward continuous lifecycle oversight, which gives vendors more room to sell broader platforms rather than narrow tools. That pattern keeps the IT Hardware Refresh Cycle Optimization Software Market tied to operating discipline as much as to hardware demand.

Windows and Endpoint Operating System End-Of-Support Waves

Microsoft ended support for Windows 10 on October 14, 2025, prompting many organizations to review their large endpoint estates in a more structured way. In the IT Hardware Refresh Cycle Optimization Software Market, the operating system deadline mattered because it forced companies to identify devices that could move to Windows 11 and those that needed replacement. That audit process often uncovered missing serial numbers, stale records, and unmanaged devices, thereby increasing the value of discovery, lifecycle scoring, and replacement planning functions within the IT Hardware Refresh Cycle Optimization Software Market. Microsoft also set out a paid Extended Security Updates path, which made the cost of delaying change easier for buyers to compare against refresh planning tools and device upgrades. With Microsoft Office 2021 and LTSC 2021 support due to expire in October 2026, the IT Hardware Refresh Cycle Optimization Software Market continues to benefit from a follow-on compliance cycle already in motion.

Shift From Reactive Inventory to Predictive Lifecycle Optimization

The IT Hardware Refresh Cycle Optimization Software Market is also being shaped by a clear shift away from time-based replacement rules toward condition-led decision-making. ISO/IEC TS 19770-10:2025 provided organizations with updated guidance for implementing IT asset management in complex environments, supporting more disciplined, repeatable lifecycle practices.[2]SO, “ISO/IEC TS 19770-10:2025, Information Technology, IT Asset Management, Part 10, Guidance for Implementing ITAM,” ISO, iso.org As enterprises improve discovery and record accuracy, the IT Hardware Refresh Cycle Optimization Software Market becomes more relevant, as procurement and support teams can act on usage, health, and dependency data rather than fixed replacement intervals. This creates room for platforms that combine asset intelligence with workflow steps around approvals, redeployment, and retirement. The move is gradual, but it gives the IT Hardware Refresh Cycle Optimization Software Market a stronger role in daily operations rather than only during yearly budget cycles.

Audit Pressure From Software And Hardware Compliance Gaps

Compliance gaps remain a direct driver of demand in the IT Hardware Refresh Cycle Optimization Software Market, as many enterprises still lack reliable asset and location inventory. The lack of integration with legacy systems remains a major hurdle for IT asset management programs, making audit preparation more difficult in mixed environments.[3]Linh Hoang et al., “Optimizing IT Asset Management With ServiceNow, A Data-Driven Approach to HAM and SAM,” World Journal of Advanced Engineering Technology and Sciences, wjaets.com When companies begin formal reviews of hardware, software, and related controls, they often find duplicate records, undocumented endpoints, and weak links between service management and procurement. That turns the IT Hardware Refresh Cycle Optimization Software Market into a practical way to improve record quality, support policy enforcement, and maintain a clearer chain of custody across refresh and disposition workflows. The same pressure is likely to persist as organizations treat hardware governance less as a back-office task and more as a documented control process.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity Across ITSM, EAM, And Procurement Stacks | -2.1% | Global, strongest in large enterprises with legacy stacks | Medium term (2-4 years) |

| Data Quality Gaps In Asset Discovery And Utilization Records | -1.6% | Global, with greater effect in mid-market and distributed environments | Short term (≤ 2 years) |

| Budget Deferral In Mid-Market And Public Sector Buyers | -1.2% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Resistance To Policy-Driven Replacement Decisions | -0.8% | Global, strongest where asset lives are extended for longer periods | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across ITSM, EAM, and Procurement Stacks

The IT Hardware Refresh Cycle Optimization Software Market still faces a significant barrier: complex system environments that combine legacy service tools, procurement modules, and separate asset databases. Seventy percent of organizations cite interoperability with legacy ITSM systems as the main implementation barrier, underscoring how common this issue remains. In practice, that means even buyers who want better refresh planning may move slowly if discovery data, contract data, and service records do not align. The IT Hardware Refresh Cycle Optimization Software Market, therefore, favors vendors that can offer strong connectors and a cleaner path into mixed environments. Until those connections become easier to deploy, implementation effort will continue to slow some purchases in large accounts.

Data Quality Gaps In Asset Discovery And Utilization Records

Data quality is another barrier to adoption in the IT Hardware Refresh Cycle Optimization Software Market, as poor asset records undermine trust in automated recommendations. Ghost assets, inactive devices, and missing utilization fields can make an otherwise capable platform look unreliable if the source data is incomplete. That issue is most visible in distributed organizations where devices move often, and local record-keeping is inconsistent. In the IT Hardware Refresh Cycle Optimization Software Market, vendors that can remediate records during onboarding are better placed than vendors that expect clean data from the start. Better baseline discovery remains important because the value of lifecycle planning depends on the quality of the information it relies on.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Leads, Hybrid Gains In Complex Environments

Cloud-based deployment accounted for 65.74% of revenue in 2025, keeping this model at the center of the IT Hardware Refresh Cycle Optimization Software Market. That lead came from an easier rollout, lower upfront infrastructure costs, and the ability to monitor device estates across dispersed workforces from a single environment. In the IT Hardware Refresh Cycle Optimization Software Market, cloud delivery also helped buyers move faster when spreadsheet tracking or isolated tools no longer gave enough visibility. The segment remained especially relevant for organizations that had expanded hybrid work and needed a single view of assets across multiple locations.

Hybrid deployment is projected to grow at a 18.05% CAGR through 2031, making it the faster-moving option where legacy infrastructure still matters. ISO/IEC TS 19770-10:2025 supports structured ITAM implementation across mixed environments, and that aligns with the appeal of hybrid architectures that combine cloud analytics with local discovery and control. Many large buyers want cloud-side planning tools while keeping some discovery or record systems on premises for control, security, or residency needs. That makes hybrid a practical middle ground in the IT Hardware Refresh Cycle Optimization Software Market, especially where full migration would add unnecessary disruption.

By Enterprise Size: Large Enterprises Hold Scale, SMEs Expand Faster

Large enterprises captured 64.12% of the IT Hardware Refresh Cycle Optimization Software market share in 2025, reflecting the depth of their asset estates and the greater need for multi-region governance. These buyers usually have more mature service management environments, which have historically made them early adopters of lifecycle optimization software. In the IT Hardware Refresh Cycle Optimization Software Market, large accounts also tend to prefer integrated platforms that connect discovery, service records, and approval workflows. Their scale gives vendors larger contract values, but it also raises expectations around integration depth and process fit.

Small and medium enterprises are forecast to grow at a 18.21% CAGR through 2031, indicating that access barriers are starting to come down in the IT Hardware Refresh Cycle Optimization Software Market. SaaS delivery and simplified onboarding have made it easier for smaller firms to adopt structured refresh planning without building a large internal ITAM team. Freshworks has also expanded Freshservice with embedded discovery and dependency mapping, which supports the kind of simpler, broader visibility that smaller organizations often need first. As a result, the IT Hardware Refresh Cycle Optimization Software industry is opening to buyers that once relied on manual lists, local spreadsheets, or ad hoc replacement decisions.[4]Freshworks Inc., “Stop Flying Blind, Freshservice IT Asset Management,” Freshworks, freshworks.com

By Application: Analytics Leads, Replacement Planning Grows Fastest

Hardware lifecycle analytics and asset performance management accounted for 28.63% of the market share in 2025, making this the largest application area in the IT Hardware Refresh Cycle Optimization Software Market. The segment led because most later decisions depend on having a usable view of health, age, support status, and total cost of ownership across active devices. In the IT Hardware Refresh Cycle Optimization Software Market, analytics serves as the foundation for refresh timing, redeployment, warranty management, and audit readiness. Without that record foundation, other modules are harder to use with confidence.

Refresh planning and replacement optimization is expected to grow at an 18.45% CAGR through 2031, showing that buyers increasingly want software that turns discovery data into action. Microsoft’s Windows 10 support deadline and the related update cycle have kept replacement readiness in the spotlight for endpoint-heavy organizations. At the same time, the Basel Convention’s e-waste amendments, effective from January 1, 2025, strengthened the need for clearer end-of-life handling and cross-border disposition controls. That mix of replacement timing and disposition discipline keeps this application area moving faster inside the IT Hardware Refresh Cycle Optimization Software Market.

By End User: IT And Telecom Sets The Pace, Retail And E-Commerce Picks Up

IT and telecom held 27.41% revenue share in 2025, giving the segment the largest position in the IT Hardware Refresh Cycle Optimization Software Market. This sector typically manages large endpoint, network, and server estates, so it usually implements formal lifecycle governance earlier than most other end users. The IT Hardware Refresh Cycle Optimization Software Market has therefore treated IT and telecom as a reference segment where integration depth and asset visibility are already more developed. BFSI also remains important because firms in that segment often move quickly when asset governance becomes part of wider control requirements.

Retail and e-commerce are projected to expand at a 17.92% CAGR through 2031, supported by wider store networks, greater adoption of point-of-sale devices, and ongoing modernization of operating systems and infrastructure. The need to manage a large number of distributed assets gives the IT Hardware Refresh Cycle Optimization Software Market a stronger role as retailers connect central teams with store-level hardware decisions. Continued investment in ITAM and service operations, including the move to a unified asset and incident experience, shows why simpler workflow-led tools can appeal to fast-moving commercial users. Over time, this should help close part of the maturity gap between retail and the more established user groups inside the IT Hardware Refresh Cycle Optimization Software Market.

Geography Analysis

Europe held a 34.56% share in 2025, making it the largest region in the IT Hardware Refresh Cycle Optimization Software Market. The region’s demand base is supported by organizations that need a documented view of assets, repair options, and disposition steps across regulated operating environments. The European Union’s Right to Repair Directive requires member states to adopt the rules into national law by July 31, 2026, thereby extending the relevance of repair-versus-replace decisions within hardware programs. The Basel Convention’s e-waste amendments, effective from January 1, 2025, add further weight to controlled end-of-life handling and clearer movement of used equipment across borders. In the IT Hardware Refresh Cycle Optimization Software Market, these policy conditions help keep Europe at the forefront, as hardware refresh is increasingly linked to documentation quality and asset management discipline.

North America remained the second-largest region in the IT Hardware Refresh Cycle Optimization Software Market because many large enterprises there already run mature service and asset management programs. The Windows 10 end-of-support deadline had a clear effect on large endpoint estates, making structured inventory review and replacement planning more urgent for many buyers. The region also benefits from the presence of major platform vendors that sell broader service, security, and asset workflows into established enterprise accounts. That combination keeps North America closely tied to the product direction and revenue base of the IT Hardware Refresh Cycle Optimization Software Market.

Asia-Pacific is set to grow at an 18.34% CAGR through 2031, making it the fastest-growing regional block in the IT Hardware Refresh Cycle Optimization Software Market. Growth in the region is supported by ongoing digitization, data-center build-out, and new enterprise investment linked to manufacturing shifts and local infrastructure programs. The IT Hardware Refresh Cycle Optimization Software market in Asia-Pacific is growing as new device estates require structured tracking earlier in their life cycles, not only after assets become hard to manage. South America, the Middle East, and Africa remain at an earlier stage, though multinational operating standards are helping create demand in selected countries. Over time, those regions should see wider adoption as lifecycle governance becomes more formal and less reliant on manual recordkeeping.

Competitive Landscape

The IT Hardware Refresh Cycle Optimization Software Market is moderately consolidated, with a small group of platform vendors holding strong positions through installed enterprise bases and broad workflow coverage. Two models shape competition, one focused on large suites that combine service management, security, and asset visibility, and another centered on specialist tools with strong discovery or lifecycle depth. In the IT Hardware Refresh Cycle Optimization Software Market, this split matters because buyers often choose between platform convenience and specialist fit. The market is not fully closed, because white space remains in mid-market accounts and in sectors where operational technology assets require a different treatment from standard endpoint fleets. That leaves room for both broad vendors and focused vendors to grow.

ServiceNow strengthened its position after completing the Armis acquisition in May 2026, which extended asset visibility across IT, OT, IoT, medical devices, and physical AI environments. It also closed the Veza acquisition in March 2026, adding identity security and giving the broader platform a tighter link between assets, access, and governance. Freshworks expanded Freshservice with a reworked IT asset management experience that embedded Device42 discovery and dependency mapping, improving visibility across cloud, on-premises, and hybrid environments. These moves show how the IT Hardware Refresh Cycle Optimization Software Market is shifting toward platforms that connect asset intelligence with service and governance workflows.

Specialists remain relevant in the IT Hardware Refresh Cycle Optimization Software Market because many buyers want faster deployment and a clearer fit for specific asset problems. Lansweeper’s July 2025 acquisition of Redjack expanded its visibility into unmanaged and transient assets, enabling more complete intelligence in asset-heavy environments. Ivanti also introduced new AI-driven capabilities across the Neurons Platform in 2026, including stronger discovery visibility and unified risk context, which keeps asset data closer to daily IT operations. Flexera continued to expand contract ingestion, cloud inventory control, and monitoring features across its 2026 ITAM releases, supporting organizations seeking tighter governance across mixed estates. Taken together, these moves suggest the IT Hardware Refresh Cycle Optimization Software Market will continue to balance consolidation at the top with practical opportunities for vendors that reduce deployment effort or solve a narrower problem well.

IT Hardware Refresh Cycle Optimization Software Industry Leaders

ServiceNow, Inc.

Flexera Software LLC

Ivanti, Inc.

BMC Software, Inc.

USU Software AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ServiceNow completed its acquisition of Armis for approximately USD 7.75 billion in cash, integrating Armis's AI-powered cyber exposure management across IT, OT, IoT, medical devices, and physical AI into its security and asset management platform; the transaction represented ServiceNow's largest acquisition to date and extended hardware asset intelligence into operational and industrial device environments.

- April 2026: Ivanti unveiled agentic AI capabilities and autonomous endpoint management (AEM) across its Neurons Platform, including next-generation asset visibility in Ivanti Neurons for Discovery with embedded license management and unified risk insights; the Q2 2026 release also introduced agentic AI capabilities to Ivanti Neurons for ITSM, advancing autonomous incident handling into commercial deployment.

- March 2026: Freshworks expanded Freshservice with a reimagined IT asset management experience on March 31, 2026, natively embedding Device42's continuous infrastructure discovery and application dependency mapping into the platform; the launch provided continuously updated visibility across cloud, on-premise, and hybrid environments and was made immediately available to all new Freshservice customers, with phased transition for existing customers through 2026 and early 2027.

- March 2026: ServiceNow completed its acquisition of Veza on March 2, 2026, extending identity security into its security and risk portfolios and enabling end-to-end asset governance grounded in least-privilege principles; the acquisition was initially announced in December 2025 and positions ServiceNow to govern AI agent identities alongside hardware and software assets.

Global IT Hardware Refresh Cycle Optimization Software Market Report Scope

The IT Hardware Refresh Cycle Optimization Software market refers to platforms and services that help organizations strategically manage and optimize the lifecycle of IT hardware assets. These solutions provide capabilities such as hardware lifecycle analytics, asset performance monitoring, refresh planning and replacement optimization, procurement and redeployment management, warranty and support contract optimization, and compliance governance. By embedding intelligence into refresh cycle planning, these platforms enable enterprises to reduce costs, extend hardware lifespans, minimize downtime, and align IT operations with sustainability and governance requirements.

The IT Hardware Refresh Cycle Optimization Software market report is segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Hardware Lifecycle Analytics and Asset Performance Management, Refresh Planning and Replacement Optimization, Procurement, Redeployment and Reallocation Optimization, Warranty and Support Contract Optimization, Audit, Compliance and Asset Governance), End User (IT and Telecom, BFSI, Industrial Manufacturing, Energy and Utilities, Oil and Gas, Retail and E-Commerce, Construction and Infrastructure, Government and Public Sector, and Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Hardware Lifecycle Analytics and Asset Performance Management |

| Refresh Planning and Replacement Optimization |

| Procurement, Redeployment and Reallocation Optimization |

| Warranty and Support Contract Optimization |

| Audit, Compliance and Asset Governance |

| IT and Telecom |

| BFSI |

| Industrial Manufacturing |

| Energy and Utilities |

| Oil and Gas |

| Retail and E-Commerce |

| Construction and Infrastructure |

| Government and Public Sector |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Application | Hardware Lifecycle Analytics and Asset Performance Management | ||

| Refresh Planning and Replacement Optimization | |||

| Procurement, Redeployment and Reallocation Optimization | |||

| Warranty and Support Contract Optimization | |||

| Audit, Compliance and Asset Governance | |||

| By End User | IT and Telecom | ||

| BFSI | |||

| Industrial Manufacturing | |||

| Energy and Utilities | |||

| Oil and Gas | |||

| Retail and E-Commerce | |||

| Construction and Infrastructure | |||

| Government and Public Sector | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast size of the IT Hardware Refresh Cycle Optimization Software Market?

The IT Hardware Refresh Cycle Optimization Software Market was valued at USD 1.24 billion in 2025, reached USD 1.43 billion in 2026, and is forecast to reach USD 3.18 billion by 2031 at a CAGR of 17.33%.

What is driving demand for IT hardware refresh cycle optimization software?

Key demand factors include delayed device replacement from 2022 to 2024, the Windows 10 support deadline, tighter audit expectations, and the need to move from spreadsheet tracking to structured lifecycle planning.

Which deployment model leads in this software category?

Cloud-based deployment led with 65.74% revenue share in 2025 because it offers easier rollout, lower upfront infrastructure needs, and better visibility across dispersed device estates.

Which enterprise size segment is expanding the fastest?

Small and medium enterprises are projected to record the fastest growth at an 18.21% CAGR through 2031 as SaaS delivery and simpler onboarding lower adoption barriers.

Which application area is growing the fastest in IT hardware refresh cycle optimization software?

Refresh planning and replacement optimization is forecast to grow at an 18.45% CAGR through 2031 as more organizations try to turn inventory data into replacement roadmaps and budget decisions.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific is expected to post the fastest growth at an 18.34% CAGR through 2031, supported by ongoing digitization, data-center investment, and expanding enterprise IT estates.

Page last updated on: