CXL Memory Expansion For AI Workloads Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 2.79 Billion |

| Growth Rate (2026 - 2031) | 30.16% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CXL Memory Expansion For AI Workloads Market Analysis by Mordor Intelligence

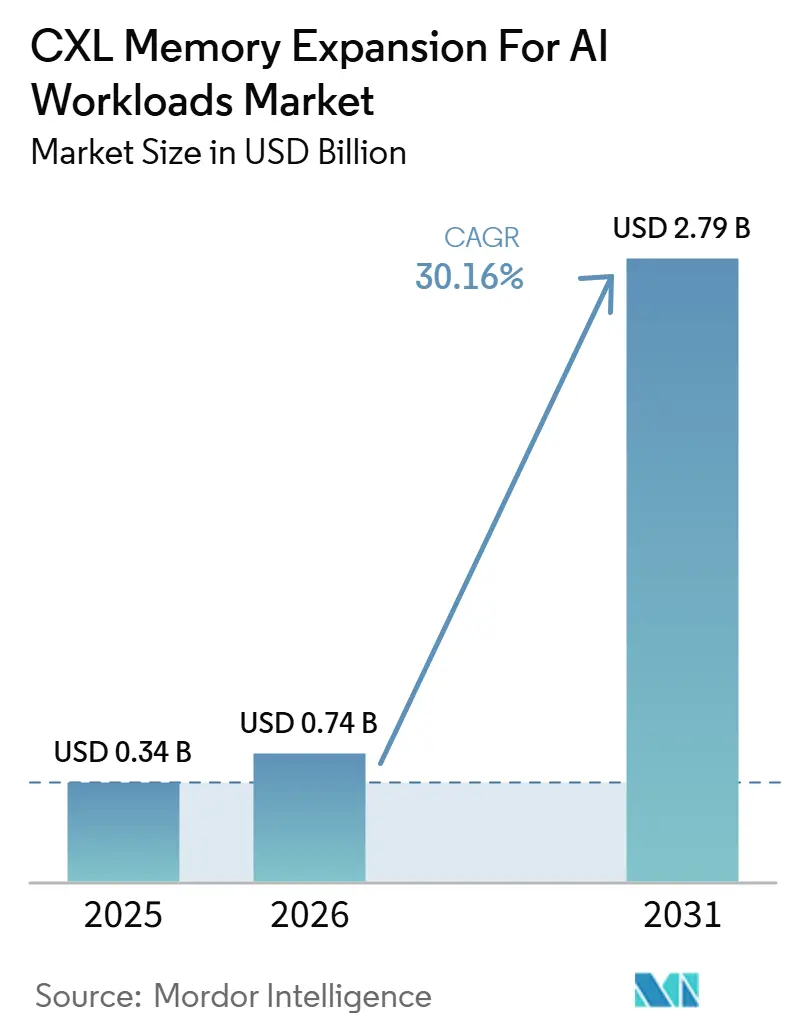

The CXL memory expansion for AI workloads market size is projected to be USD 0.34 billion in 2025, USD 0.74 billion in 2026, and reach USD 2.79 billion by 2031, growing at a CAGR of 30.16% from 2026 to 2031. The market is entering a new phase because AI infrastructure buyers now face a memory bottleneck that cannot be solved solely by adding more accelerator compute. The pressure comes from the widening gap between model scale, context length, and the physical limits of on-socket DRAM and on-package HBM, which keeps memory capacity central to deployment economics. The CXL memory expansion for the AI workloads market is also benefiting from broader platform readiness, as CPU, controller, and memory suppliers have moved from isolated testing to qualified product combinations. Large cloud operators continue to shape the pace of adoption because their validation cycles, custom architecture programs, and spending power influence commercial design priorities across the supply chain. At the same time, supply qualification, interoperability effort, and software orchestration maturity still determine how fast the CXL memory expansion for AI workloads market can convert technical promise into scaled production deployment.

Key Report Takeaways

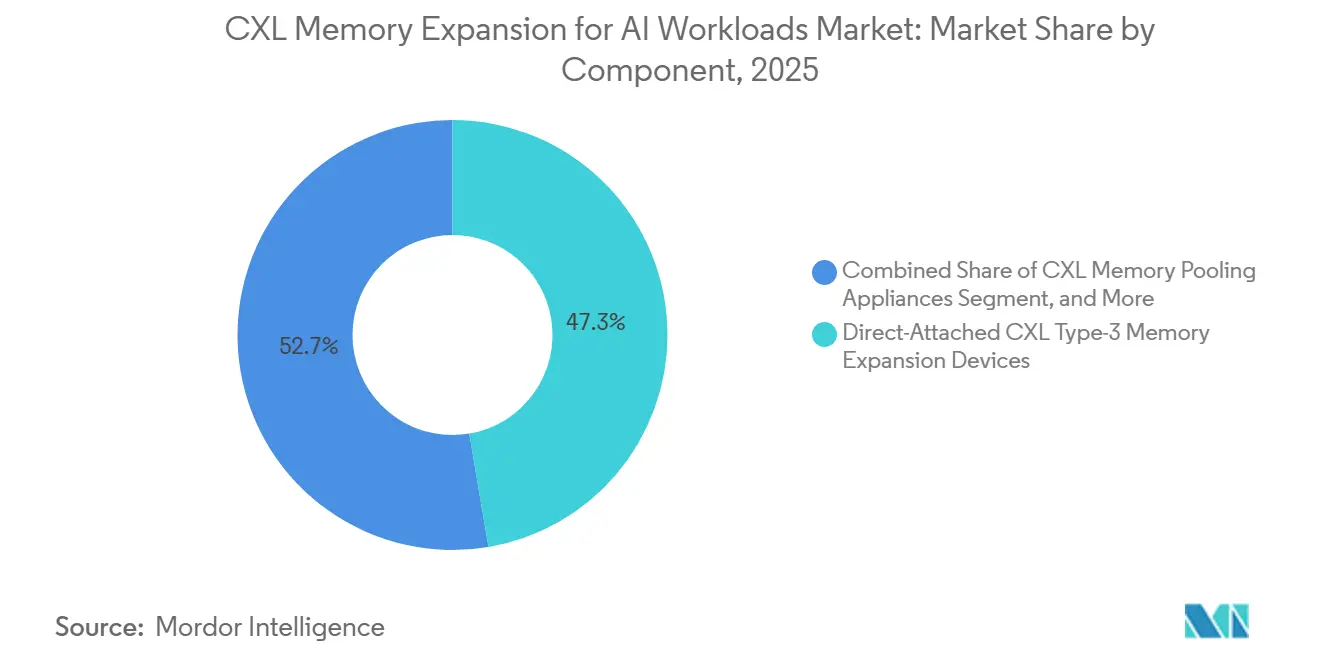

- By component, direct-attached CXL Type-3 memory expansion devices held 47.32% share of the CXL memory expansion for AI workloads market in 2025, while CXL memory fabric and rack-scale systems are projected to expand at a 30.96% CAGR through 2031.

- By physical form factor, EDSFF/E3.S CXL memory modules held 49.84% share in 2025, while PCIe add-in cards are projected to expand at a 30.92% CAGR through 2031.

- By application, AI inference and model serving accounted for 43.39% share of the CXL memory expansion for AI workloads market size in 2025, while AI data preparation, vector databases, and retrieval-augmented generation are projected to expand at a 31.14% CAGR through 2031.

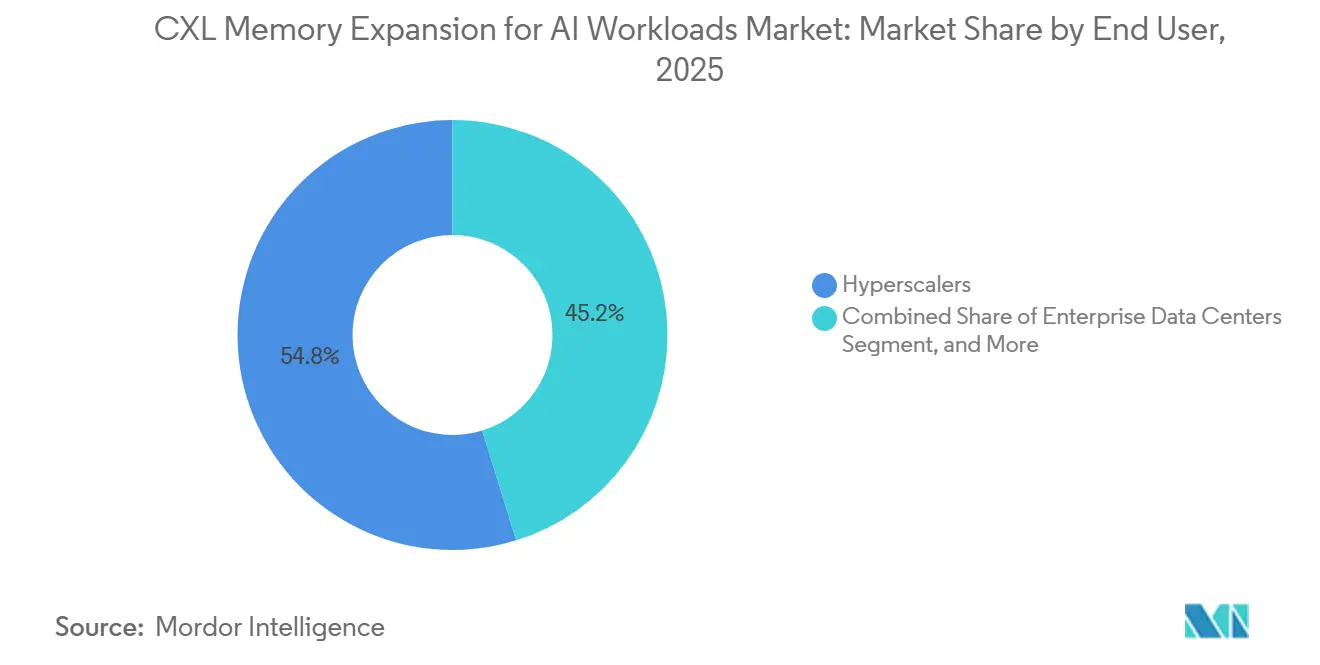

- By end user, hyperscalers held 54.79% share in 2025, while AI cloud, GPU cloud, and neo-cloud providers are projected to expand at a 31.28% CAGR through 2031.

- By CXL specification, CXL 2.0 held 79.63% share in 2025, while CXL 4.0 is projected to expand at a 30.87% CAGR through 2031.

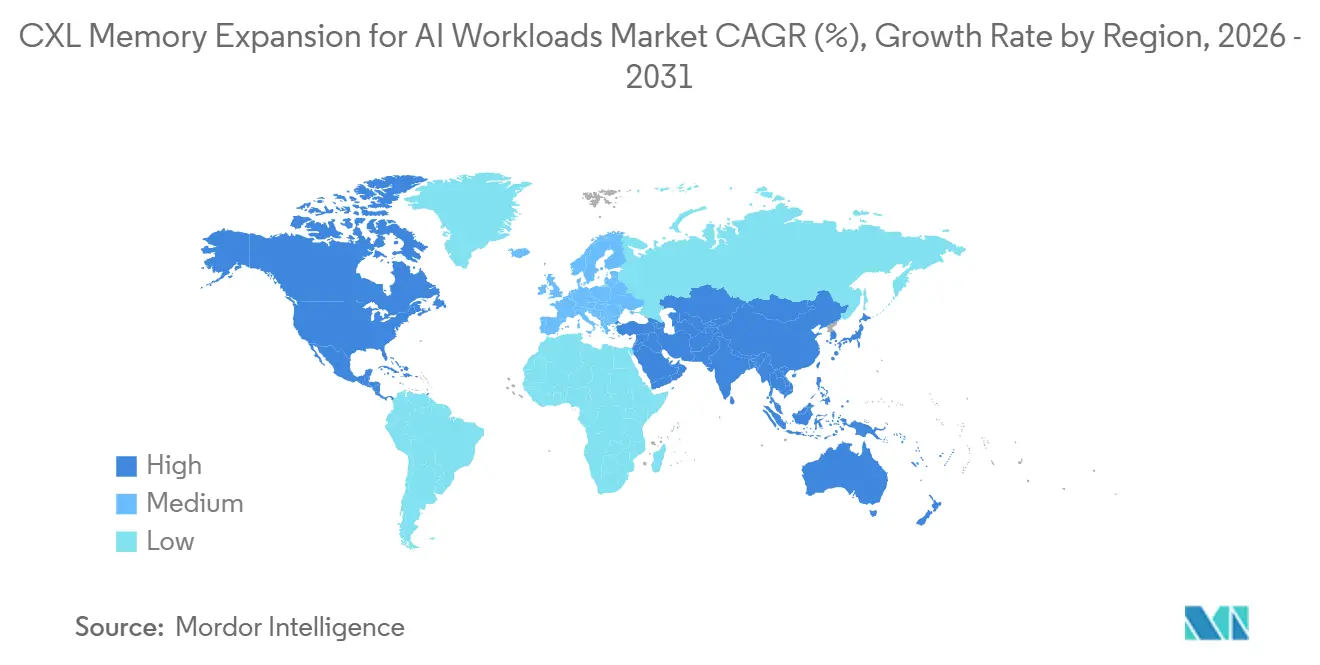

- By geography, North America held 61.44% share of the CXL memory expansion for AI workloads market in 2025, while Asia-Pacific is projected to expand at a 31.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CXL Memory Expansion For AI Workloads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Model Parameter Growth Outpacing HBM and DIMM Capacity | +7.5% | Global | Short term (≤ 2 years) |

| Hyperscaler Shift Toward Memory Disaggregation To Improve Utilization | +6.2% | North America and Asia-Pacific Core | Short term (≤ 2 years) |

| CXL 2.0 and CXL 3.x Ecosystem Maturity | +5.1% | Global | Short term (≤ 2 years) |

| PCIe Gen 5 and Gen 6 Platform Rollout | +3.8% | North America and Europe | Medium term (2-4 years) |

| Multi-Tenant AI Infrastructure Needs for Dynamic Memory Allocation | +2.7% | North America and Asia-Pacific | Medium term (2-4 years) |

| AI Inference Cost Pressure Driving Lower TCO Memory Pooling | +2.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI Model Parameter Growth Outpacing HBM and DIMM Capacity

The CXL memory expansion for AI workloads market is being accelerated by a problem that lies above raw accelerator throughput, because many AI workloads run into memory limits before compute limits. A 70-billion-parameter model trained in BF16 precision requires close to 140 GB of memory for weights alone, and long-context inference pushes practical memory needs much higher once KV cache growth is added. The same research path also shows that 1-million-token contexts can drive KV cache needs to nearly 330 GB for a 70-billion-parameter model, which is beyond the HBM capacity available on any current GPU. This keeps the CXL memory expansion for AI workloads market closely tied to inference economics, because adding coherent external memory can extend usable model contexts without redesigning the accelerator package or the host socket. Penguin Solutions stated in 2026 that inference workloads are heavily shaped by memory pressure rather than pure compute pressure, which supports the view that idle GPU time has become a direct cost problem in production clusters. As a result, the CXL memory expansion for the AI workloads market is gaining support not only as a hardware category, but also as a way to recover utilization from expensive deployed accelerators.

Hyperscaler Shift Toward Memory Disaggregation to Improve Utilization

The CXL memory expansion for AI workloads market is also advancing because hyperscalers are no longer treating memory disaggregation as a lab exercise. Microsoft Research published its Octopus architecture to demonstrate that sparse CXL pod topologies can connect large memory domains without requiring an expensive full-mesh switching model, thereby lowering the cost barrier to scaled pooling.[1]Microsoft Research, “Octopus: Enhancing CXL Memory Pods via Sparse Topology,” Microsoft Research, microsoft.com That matters because the commercial path for the CXL memory expansion for AI workloads market depends on whether memory pooling can grow without forcing proportional switch cost at every expansion step. Astera Labs announced in November 2025 that its Leo controllers were enabled on Microsoft Azure M-series virtual machines, which marked the first publicly announced commercial cloud deployment of CXL-attached memory. This public deployment created a usable reference point for enterprise buyers and smaller cloud operators that had been waiting for evidence beyond internal hyperscaler projects. The commercial implication is that vendors in the CXL memory expansion for AI workloads market now need to support both merchant deployments and custom cloud-architecture paths simultaneously.

CXL 2.0 and CXL 3.x Ecosystem Maturity

The CXL memory expansion for AI workloads market benefited in 2025 and 2026 from broader improvements in ecosystem credibility, as more parts of the stack achieved validated interoperability simultaneously. Marvell stated in September 2025 that its Structera memory expansion controllers had achieved interoperability with DDR4 and DDR5 products from Samsung Electronics, SK hynix, and Micron Technology, as well as with AMD EPYC and 5th-generation Intel Xeon platforms. SK hynix separately completed customer validation of its 96 GB CMM-DDR5 CXL 2.0 module in April 2025 and confirmed work on a 128 GB version, indicating that qualified supply is broadening, even if it remains limited. The CXL Consortium also stated in its 2024 white paper that using CXL add-in cards for memory expansion can reduce the memory cost per GB by close to 56% compared with HBM-only configurations, providing procurement teams with a direct economic argument for broader evaluation. The CXL memory expansion for AI workloads market is therefore moving beyond a specification story and into a qualified product story, which is a much stronger signal for commercial adoption. That shift matters because system buyers usually commit only after controller, module, and host combinations have cleared repeatable multi-vendor validation.

PCIe Gen 5 and Gen 6 Platform Rollout

The CXL memory expansion for AI workloads market remains tied to the server platform cycle, because deployment speed depends on how quickly CXL-capable CPU generations move into volume systems. Intel stated in 2026 that the Xeon 6+ Clearwater Forest provides 96 PCIe Gen 5 lanes, including 64 lanes with CXL 2.0 support, expanding practical attachment options for memory devices and fabrics. Intel also signaled that Diamond Rapids is expected in 2027, with PCIe Gen 6 support and higher socket bandwidth, which will create the platform base for later CXL 3.x and CXL 4.0 rollouts. AMD EPYC Turin support for CXL memory expansion is equally important because the AI workloads market would be far more exposed if one CPU roadmap were the only viable host path. Marvell announced in March 2026 that its Structera S 30260 switch would sample in Q3 2026, with PCIe Gen 6 support and up to 4 TB/s aggregate bandwidth, linking future switching capability to the next phase of rack-scale pooling. This means platform availability is no longer only about host compatibility, because it now shapes how quickly fabric-level architectures can move from product demos into deployable systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Production-Qualified CXL Type 3 Supply Base | -3.6% | Global | Short term (≤ 2 years) |

| Platform Interoperability and Validation Complexity | -2.8% | Global | Medium term (2-4 years) |

| Software Stack Immaturity for Memory Orchestration | -1.9% | Global | Medium term (2-4 years) |

| High Initial Platform Re-Qualification Cost for AI Data Centers | -1.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Production-Qualified CXL Type 3 Supply Base

The CXL memory expansion for AI workloads market still faces a supply ceiling because the pool of production-qualified Type-3 memory vendors remains narrow. The qualified supplier base is centered on Samsung Electronics, SK hynix, and Micron Technology, yet the range of tested densities, form factors, and specification combinations is still much smaller than data center buyers want for broad deployment. SK hynix confirmed customer validation of its 96 GB CMM-DDR5 CXL 2.0 module in 2025 and noted a 128 GB variant in parallel validation, which shows progress but not full breadth across deployment options. This matters because the CXL memory expansion for the AI workloads market competes for the same underlying memory manufacturing capacity that also serves standard DDR5 and HBM demand. When HBM volumes rise, internal allocation can shift away from emerging CXL products even if customer interest remains strong. The result is that the CXL memory expansion for AI workloads market can see demand faster than shippable volume, which slows real deployment even when the technology case is already accepted.

Platform Interoperability and Validation Complexity

The CXL memory expansion for AI workloads market is also constrained by the validation work required across modules, controllers, switches, and host platforms. An IEEE Transactions on Computers study published in 2026 found that first-generation deployment behavior is heavily influenced by CPU and DRAM internals, and that standard interoperability testing may not capture all real-world failure modes. Research presented at ASPLOS 2025 also showed that the CXL specification does not fully guarantee safe interoperability across hosts with different cache coherence behaviors, which creates a deeper semantic challenge for heterogeneous environments. A separate 2026 arXiv study on multi-tenant memory tiering showed that the absence of container-level controls can lead to performance degradation of up to 65% when tenants compete for CXL-attached memory. This keeps enterprise and tier-2 buyers dependent on pre-validated solutions from OEM partners, because the cost of independent qualification remains high relative to the scale of early deployment. Until more of this process becomes automated, the CXL memory expansion for AI workloads market will expand through validated system paths rather than fully open-ended plug-and-play adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Rack-Scale Pooling Architectures Accelerate Beyond Single-Host Expansion

Direct-attached CXL Type-3 memory expansion devices held a 47.32% share of the CXL memory expansion for AI workloads market in 2025, indicating that early demand favored simple single-host deployments over more complex pooled designs. This position reflected near-term buying behavior because initial inference deployments required additional memory capacity without forcing a full change in rack architecture. In the CXL memory expansion for AI workloads industry, direct-attached devices were easier to validate on Intel Xeon 6 and AMD EPYC Turin platforms, which reduced deployment friction for first-wave buyers. Mid-layer products, such as memory pooling appliances and enclosures, served customers who needed more flexibility than single-host cards could offer, but were not ready for full fabric implementations. Memory management and orchestration software held a smaller share, yet it remained central to commercial usefulness because pooled memory has limited value unless it can be assigned dynamically across changing workloads. MemVerge positions this layer around transparent memory tiering and GPU cluster efficiency, which helps explain why the software stack is strategically important even when it is not yet the largest revenue contributor.

CXL memory fabric and rack-scale systems are projected to grow at a 30.96% CAGR through 2031, which makes them the fastest-expanding component segment in the CXL memory expansion for AI workloads market. Their momentum comes from the ability to let multiple compute hosts draw from a shared memory pool, which changes how GPU-to-memory ratios can be set at the rack level. XConn Technologies and MemVerge demonstrated a 100 TB commercial CXL pool in October 2025 and reported more than 5x performance improvement over SSD-based KV cache offload for AI inference workloads. Marvell then announced in March 2026 that the Structera S 30260 switch would support up to 48 TB of shared memory across 16 to 32 hosts at 4 TB/s aggregate bandwidth, providing a clearer commercial roadmap for rack-scale pooling.[2]Marvell Technology, “Marvell Launches Next-Generation CXL Switch, Enabling Memory Pooling to Break Through the AI Memory Wall,” Marvell Newsroom, marvell.com The shift from device-level expansion to shared-fabric architectures matters because it allows capacity to more closely follow workload demand across the cluster. That is why the CXL memory expansion for the AI workloads market is likely to see value move gradually from simple attachment products toward higher-level pooling systems over the forecast period.

By Physical Form Factor: EDSFF/E3.S Modules Anchor Near-Term Deployments While PCIe Add-In Cards Scale Inference Infrastructure

EDSFF/E3.S CXL memory modules held 49.84% share in 2025, which made them the leading physical form factor within the CXL memory expansion for AI workloads market. Their lead came from compatibility with standard server NVMe bays, a lower thermal footprint, and closer alignment with mainstream server integration paths. Intel demonstrated the use of Xeon 6 6900P processors with multiple CXL E3.S modules for AI and HPC workloads, which reinforced this form factor as a practical fit for OEM server configurations. In the CXL memory expansion for AI workloads industry, this gave EDSFF/E3.S modules an advantage in enterprise and OEM qualification pipelines where mechanical fit and platform familiarity matter. Proprietary integrated formats still have a role, especially in custom cloud systems where vendors can optimize board design and latency paths more tightly than commodity server formats allow.

PCIe add-in cards are projected to grow at a 30.92% CAGR from 2026 to 2031, which places them just behind the leading growth tiers in the overall CXL memory expansion for AI workloads market. Penguin Solutions launched its MemoryAI KV cache server in March 2026 with up to 8 x 1 TB CXL add-in cards and a total of 11 TB of CXL-based memory in a 4U chassis, which made the AIC role in inference infrastructure very clear. This points to a split in adoption paths, AICs fit purpose-built inference appliances, while EDSFF/E3.S modules fit mainstream server refresh cycles. The CXL memory expansion for AI workloads market, therefore, is not moving toward a single universal physical format. It is moving toward a dual-track model where enterprise servers and custom inference systems favor different packaging choices. That form factor split is likely to persist because thermal, serviceability, and deployment model needs differ sharply between standard data center fleets and AI-specialized racks.

By Application: Inference Demand Dominates While Retrieval Workloads Gain Momentum

AI inference and model serving accounted for 43.39% of the CXL memory expansion market share for AI workloads in 2025, making it the largest application segment. This lead reflected the fact that continuous inference generates persistent KV cache pressure, which is harder to manage with static memory configurations. Astera Labs stated that each Leo CXL Smart Memory Controller can provide up to 2 TB of attached memory and enable total server memory scaling of more than 1.5x, which supports inference, in-memory databases, and KV cache expansion. That capability matters for the CXL memory expansion market for AI workloads because inference performance is shaped by usable memory depth as much as by raw accelerator count. AI training and model development still consume significant memory, but they are less prone to the same token-by-token memory behavior that makes inference the near-term anchor workload. AI-enabled HPC and large in-memory analytics also support demand, as those workloads often exceed standard DRAM ceilings, even when they can tolerate higher latency than inference traffic.

AI data preparation, vector databases, and retrieval-augmented generation are projected to grow at a 31.14% CAGR through 2031, which makes them the fastest-growing application group in the CXL memory expansion for AI workloads market. Their growth comes from enterprise retrieval architectures in which embedding stores and data indexes can reach multi-terabyte scale and exceed standard server memory footprints. A 2026 arXiv study showed that pooling engram conditional memory with CXL can deliver near-DRAM end-to-end performance for LLM inference, which supports the case for memory-rich retrieval workflows. That research matters because retrieval workloads involve frequent low-latency access patterns that need more than simple bulk storage offload. The CXL memory expansion for AI workloads market is therefore expanding across both real-time serving and data-access-heavy model support tasks. This broadens the commercial opportunity because vendors can address enterprise knowledge systems, vector search platforms, and retrieval pipelines in addition to pure model serving environments.

By End User: Hyperscalers Set The Qualification Standard While Neo-Cloud Providers Drive Growth

Hyperscalers held 54.79% share of the CXL memory expansion for AI workloads market in 2025, making them the largest end-user group by a wide margin. Their lead came from capital strength, deep validation teams, and the ability to absorb the qualification overhead tied to a new memory architecture. The CXL memory expansion for the AI workloads market has effectively used hyperscaler adoption as a commercial proof point, because other buyers often wait for large cloud operators to validate system behavior at scale. Custom architecture programs inside leading cloud providers also shape product requirements, even when merchant silicon vendors supply the broader ecosystem. Tier-2 cloud operators and managed service providers are entering through OEM-integrated systems because that route reduces the need for independent testing. Enterprise data centers remain earlier in the curve, and many are starting with in-memory database use cases before extending deployments toward AI inference as the software stack matures.

AI cloud, GPU cloud, and neo-cloud providers are projected to grow at a 31.28% CAGR through 2031, which makes them the fastest-growing end-user segment in the CXL memory expansion for AI workloads market. These providers run multi-thousand-GPU clusters where fixed HBM per GPU can either leave memory underused or limit context length for customers. Their demand profile is different from hyperscalers, because they need flexible multi-tenant memory allocation as part of a commercial service model rather than only for internal workloads. The 2026 arXiv study on fairness in CXL memory tiering found that missing per-container controls can reduce workload performance by up to 65% in contested environments, underscoring why orchestration quality is central to this group. Telecom, network, and edge cloud operators remain a smaller but meaningful part of the CXL memory expansion for AI workloads market, because constrained edge footprints can still benefit from tiered memory behavior. Research institutions and national laboratories also matter at the frontier, since they are more willing to evaluate early multi-host and fabric-attached memory designs before those designs become mainstream. Taken together, these end-user patterns show that the market is widening beyond hyperscale ownership even though hyperscalers still set the qualification standard.

By CXL Specification: CXL 2.0 Leads Current Revenue While CXL 4.0 Defines Future Direction

CXL 2.0 accounted for 79.63% of the market share in 2025, making it the clear revenue leader in the CXL memory expansion for AI workloads market. Its lead came from a simple fact, because it was the first version backed by production silicon, host support, and broader interoperability work. Intel stated in 2026 that Xeon 6+ Clearwater Forest includes 64 CXL 2.0 lanes per socket, while AMD EPYC Turin also supports CXL memory expansion, which kept CXL 2.0 aligned with live platform deployment. Earlier versions remained present only in residual legacy or pilot environments, because they did not offer the same pooling and scaling path needed for modern multi-tenant AI use cases. This means the CXL memory expansion for the AI workloads market is still being monetized around the version buyers can deploy now. It also means current revenue is being shaped more by qualification depth than by the newest published specification.

CXL 4.0 is projected to grow at a 30.87% CAGR through 2031, which makes it the fastest-growing specification segment despite the lack of commercial silicon in 2026. The CXL Consortium released the CXL 4.0 specification on November 18, 2025, and stated that it doubles bandwidth to 128 GT/s through PCIe 7.0 alignment while adding support for multi-headed and fabric-attached devices. The forecast path reflects future product cycles rather than current shipments, because the next host and controller generations are expected to align with later commercial rollouts. Montage Technology introduced its CXL 3.1 Memory eXpander Controller to customers in August 2025, indicating that the bridge between today's deployed base and later CXL 4.0 systems is already forming. The CXL memory expansion for AI workloads market is therefore likely to move through a staged transition, where CXL 2.0 drives current sales, CXL 3.x expands switching and pooling capabilities, and CXL 4.0 sets the longer-term architectural horizon. That sequence matters because buyers need continuity between deployed infrastructure and future upgrade paths, not isolated specification leaps.

Geography Analysis

North America held a 61.44% share in 2025 and remained the largest regional contributor to the CXL memory expansion for AI workloads market, as the region hosts hyperscale cloud operators, advanced validation capacity, and early production deployments. Microsoft Azure's November 2025 enablement of Astera Labs' Leo controllers on M-series virtual machines marked the region's first publicly announced commercial cloud deployment of CXL-attached memory.[3]Astera Labs, “Astera Labs' Leo CXL Smart Memory Controllers on Microsoft Azure M-series Virtual Machines Overcome the Memory Wall,” Astera Labs Newsroom, asteralabs.com The United States leads regional demand because major cloud operators and system partners can justify both bespoke designs and long validation cycles. Intel's 2026 Xeon 6+ platform rollout also reinforced North America's position by increasing live host support for CXL-based deployments across AI and scale-out infrastructure.

Asia-Pacific is projected to grow at a 31.08% CAGR through 2031, which makes it the fastest-growing regional block in the CXL memory expansion for AI workloads market. South Korea sits at the center of regional supply because SK hynix and Samsung Electronics are central to the availability of qualified memory, and that supply role increasingly overlaps with local demand growth. SK hynix completed customer validation of its 96 GB CMM-DDR5 CXL 2.0 module in 2025, which supports the region's efforts to move qualified memory into deployable configurations. Japan and India support regional momentum through sovereign AI infrastructure programs and broader data center expansion priorities described in the input. China adds a different layer to the regional picture because domestic controller activity is forming alongside demand for local AI infrastructure. Montage Technology's CXL 3.1 controller entered customer sampling in 2025, which shows that Asia-Pacific is not only a memory manufacturing base but also a growing source of controller innovation.

Europe remains an established but more cautious part of the CXL memory expansion for AI workloads market, with early use cases centered on enterprise data centers running large in-memory database environments before wider AI inference adoption. This creates a practical entry point for CXL memory expansion, as buyers can first justify adoption by addressing database and analytics workloads that already strain standard DRAM limits. The region also has a structural interest in improving memory utilization because energy-efficiency rules and sustainability reporting favor architectures that reduce overprovisioned dedicated memory. The United Kingdom, Germany, and France remain the most important country markets in Europe, while South America, the Middle East, and Africa are still earlier in adoption and are likely to follow the pace of broader AI data center build-out. The overall geographic picture shows that CXL memory expansion for AI workloads market is scaling first, where compute density, validation capacity, and memory supply access are already in place.

Competitive Landscape

The CXL memory expansion for AI workloads market remains moderately concentrated across product categories because no single vendor controls memory devices, controllers, switches, software, or systems. The strongest integrated position today belongs to Marvell following its January 2026 acquisition of XConn Technologies for USD 540 million, which combined controller, retimer, and switch capabilities into a single portfolio. Samsung Electronics, SK hynix, and Micron Technology hold a different kind of leverage, because a qualified memory supply remains narrow and gives the memory layer unusual influence over the downstream deployment pace. Software specialists such as MemVerge fill an important gap in CXL memory expansion for the AI workloads market, because hardware alone does not address allocation, orchestration, and transparent tiering challenges.

A clear strategic pattern in the CXL memory expansion for AI workloads market is that vendors are racing to prove interoperability first, because qualification is the shortest path into hyperscale and OEM design cycles. Marvell used this route by validating Structera across major memory suppliers and across AMD and Intel host platforms, which raised its credibility beyond a single-product controller story.[4]Marvell Technology, “Marvell Extends CXL Ecosystem Leadership with Structera Interoperability Across All Major Memory and CPU Platforms,” Marvell Newsroom, marvell.com Another pattern is software alignment with real deployment bottlenecks, as seen in Penguin Solutions' March 2026 launch of a production-ready CXL KV cache server that targeted inference memory behavior directly. A third pattern is commercial validation through live cloud reference points, which Astera Labs secured through its November 2025 Azure M-series enablement. These moves matter because the CXL memory expansion for AI workloads market rewards vendors that reduce buyers' risk, not only those that publish the newest technical capabilities.

The next area of competition is likely to lie between hardware and workload control, because the market still lacks a widely deployed orchestration layer that can manage HBM, attached CXL memory, and multi-tenant scheduling within a single production stack. The 2026 arXiv paper on fairness in CXL memory tiering shows why this gap matters, as contested environments can lose significant performance without deeper allocation controls. At the same time, the 2026 IEEE study on deployment lessons suggests that practical system behavior still depends on far more than nominal protocol support, which favors vendors with deeper validation resources. As a result, the CXL memory expansion for AI workloads market is likely to remain fragmented, with limited product offerings, while becoming more concentrated among vendors that can combine silicon, software compatibility, and deployment proof.

CXL Memory Expansion For AI Workloads Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Intel Corporation

Astera Labs, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Penguin Solutions launched the industry's first production-ready CXL-based KV cache server, the MemoryAI, delivering up to 11 TB of CXL-based memory per 4U chassis (3 TB DDR5 plus up to 8 x 1 TB CXL Add-in Cards). The product is compatible with NVIDIA Dynamo inference orchestration and targets enterprise-scale agentic AI inference, representing the first commercially available CXL memory appliance designed specifically for the KV cache challenge.

- March 2026: Marvell Technology announced the Structera S 30260, a 260-lane CXL 3.0 switch supporting up to 48 TB of shared memory across 16 to 32 hosts at 4 TB/s aggregate bandwidth. The device, showcased in a live demonstration at OFC 2026 and expected to begin sampling to customers in Q3 2026, is positioned as the first purpose-built CXL switching solution for rack-scale AI memory pooling.

- January 2026: Marvell Technology completed its acquisition of XConn Technologies for USD 540 million, combining Marvell's Structera CXL memory-expansion controllers and retimers with XConn's Apollo CXL/PCIe switch portfolio. The combined entity now offers the market's only end-to-end CXL fabric architecture spanning device-level memory access through multi-host rack-scale pooling.

- November 2025: The CXL Consortium released the CXL 4.0 specification on November 18, 2025, doubling bandwidth to 128 GT/s via PCIe 7.0 integration and introducing multi-headed and fabric-attached device support. The specification also doubles and halves latency compared to CXL 3.0 and adds enhanced memory RAS features for production AI infrastructure, with no silicon implementation available in 2026 but foundational silicon designs underway.

Global CXL Memory Expansion For AI Workloads Market Report Scope

The CXL Memory Expansion for AI Workloads market comprises hardware and software solutions that leverage the Compute Express Link (CXL) standard to expand, pool, share, and dynamically manage memory resources for artificial intelligence (AI) workloads across servers and accelerator-based computing environments. These solutions address the growing memory capacity, bandwidth, and utilization requirements of AI training, inference, vector databases, retrieval-augmented generation (RAG), high-performance computing (HPC), and other memory-intensive applications by enabling coherent memory expansion beyond traditional direct-attached DRAM architectures. The market includes CXL Type-3 memory expansion devices, memory pooling appliances, CXL memory fabrics and rack-scale systems, and memory management and orchestration software deployed in hyperscale, cloud, enterprise, telecom, and research data centers. The analysis covers solutions across multiple physical form factors, including EDSFF/E3.S modules, PCIe add-in cards, proprietary and server-integrated designs, and other emerging implementations, while evaluating adoption across CXL specification generations from CXL 1.1 through CXL 4.0.

The CXL Memory Expansion for AI Workloads Market Report is Segmented by Component (Direct-Attached CXL Type-3 Memory Expansion Devices, CXL Memory Pooling Appliances, CXL Memory Fabric and Rack-Scale Systems, and CXL Memory Management and Orchestration Software), Physical Form Factor (EDSFF / E3.S CXL Memory Modules, PCIe Add-In Cards, Proprietary or Server-Integrated Form Factors, and Other Form Factors), Application (AI Training and Model Development, AI Inference and Model Serving, AI Data Preparation, Vector Databases, and RAG, AI-Enabled HPC and Scientific Computing, and Large-Scale In-Memory Databases and Analytics), End User (Hyperscalers, AI Cloud, GPU Cloud, and Neo-Cloud Providers, Tier-2 Cloud and Managed Service Provider, Enterprise Data Centers, Telecom, Network, and Edge Cloud Operators, and Research Institutions, National Laboratories, and Academic HPC Centers), CXL Specification (CXL 1.1 and Earlier, CXL 2.0, CXL 3.x, CXL 4.0), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Direct-Attached CXL Type-3 Memory Expansion Devices |

| CXL Memory Pooling Appliances |

| CXL Memory Fabric and Rack-Scale Systems |

| CXL Memory Management and Orchestration Software |

| EDSFF / E3.S CXL Memory Modules |

| PCIe Add-In Cards |

| Proprietary or Server-Integrated Form Factors |

| Other Form Factors |

| AI Training and Model Development |

| AI Inference and Model Serving |

| AI Data Preparation, Vector Databases, and RAG |

| AI-Enabled HPC and Scientific Computing |

| Large-Scale In-Memory Databases and Analytics |

| Hyperscalers |

| AI Cloud, GPU Cloud, and Neo-Cloud Providers |

| Tier-2 Cloud and Managed Service Providers |

| Enterprise Data Centers |

| Telecom, Network, and Edge Cloud Operators |

| Research Institutions, National Laboratories, and Academic HPC Centers |

| CXL 1.1 and Earlier |

| CXL 2.0 |

| CXL 3.x |

| CXL 4.0 |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Direct-Attached CXL Type-3 Memory Expansion Devices | |

| CXL Memory Pooling Appliances | ||

| CXL Memory Fabric and Rack-Scale Systems | ||

| CXL Memory Management and Orchestration Software | ||

| By Physical Form Factor | EDSFF / E3.S CXL Memory Modules | |

| PCIe Add-In Cards | ||

| Proprietary or Server-Integrated Form Factors | ||

| Other Form Factors | ||

| By Application | AI Training and Model Development | |

| AI Inference and Model Serving | ||

| AI Data Preparation, Vector Databases, and RAG | ||

| AI-Enabled HPC and Scientific Computing | ||

| Large-Scale In-Memory Databases and Analytics | ||

| By End User | Hyperscalers | |

| AI Cloud, GPU Cloud, and Neo-Cloud Providers | ||

| Tier-2 Cloud and Managed Service Providers | ||

| Enterprise Data Centers | ||

| Telecom, Network, and Edge Cloud Operators | ||

| Research Institutions, National Laboratories, and Academic HPC Centers | ||

| By CXL Specification | CXL 1.1 and Earlier | |

| CXL 2.0 | ||

| CXL 3.x | ||

| CXL 4.0 | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of CXL memory expansion for AI workloads?

The CXL memory expansion for AI workloads market was projected at USD 0.34 billion in 2025, valued at USD 0.74 billion in 2026, and is forecast to reach USD 2.79 billion by 2031 at a 30.16% CAGR.

Why is memory becoming a bigger constraint than compute in AI infrastructure?

Large models need far more memory for weights and KV cache, especially in long-context inference, so many production deployments hit memory ceilings before they exhaust accelerator compute.

Which workload currently leads demand for CXL-based memory expansion?

AI inference and model serving led with 43.39% share in 2025 because continuous serving creates persistent KV cache pressure and unpredictable memory growth across GPU clusters.

Which application area is growing the fastest through 2031?

AI data preparation, vector databases, and retrieval-augmented generation are projected to expand at a 31.14% CAGR because enterprise retrieval systems often require multi-terabyte memory footprints.

Which end users are shaping product qualification and buying behavior?

Hyperscalers held 54.79% share in 2025 and still set the qualification benchmark, while AI cloud, GPU cloud, and neo-cloud providers are projected to post the fastest growth at 31.28% CAGR.

Which region is leading adoption and which region is expanding the fastest?

North America led with 61.44% share in 2025 due to hyperscaler concentration and early commercial deployment, while Asia-Pacific is projected to grow fastest at a 31.08% CAGR through 2031.

Page last updated on: