Mobile GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 42.68 Billion |

| Market Size (2031) | USD 77.93 Billion |

| Growth Rate (2026 - 2031) | 12.80% CAGR |

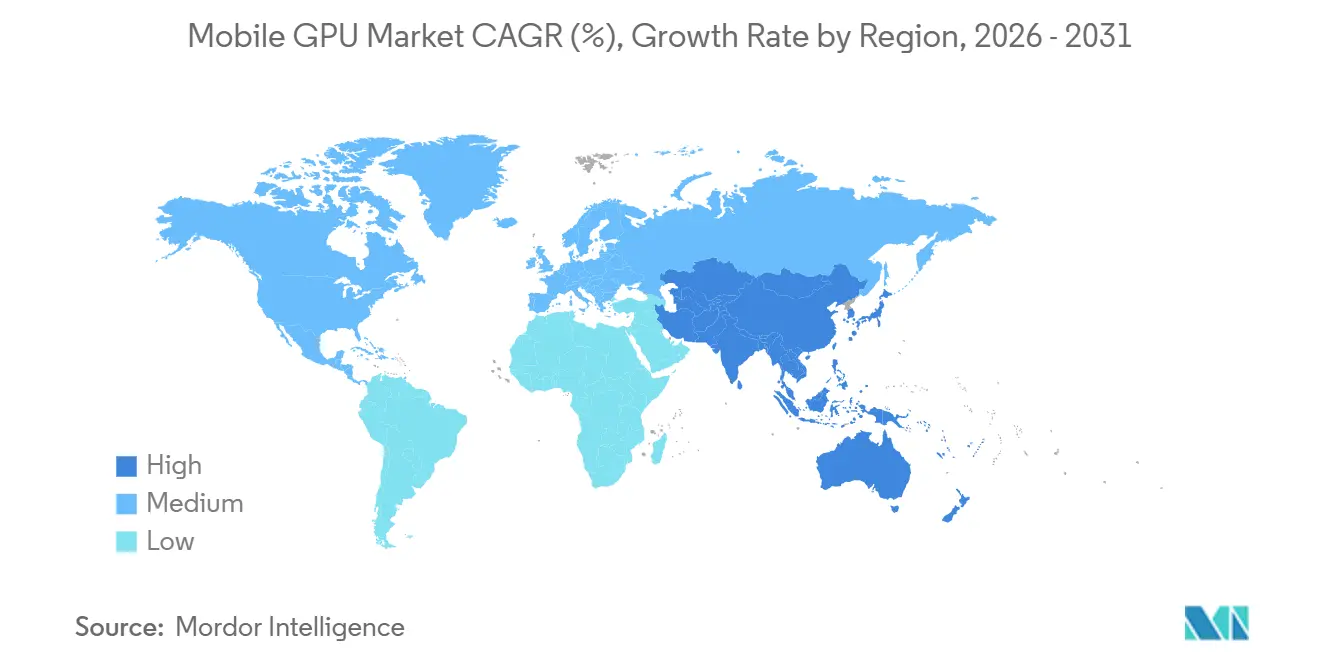

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

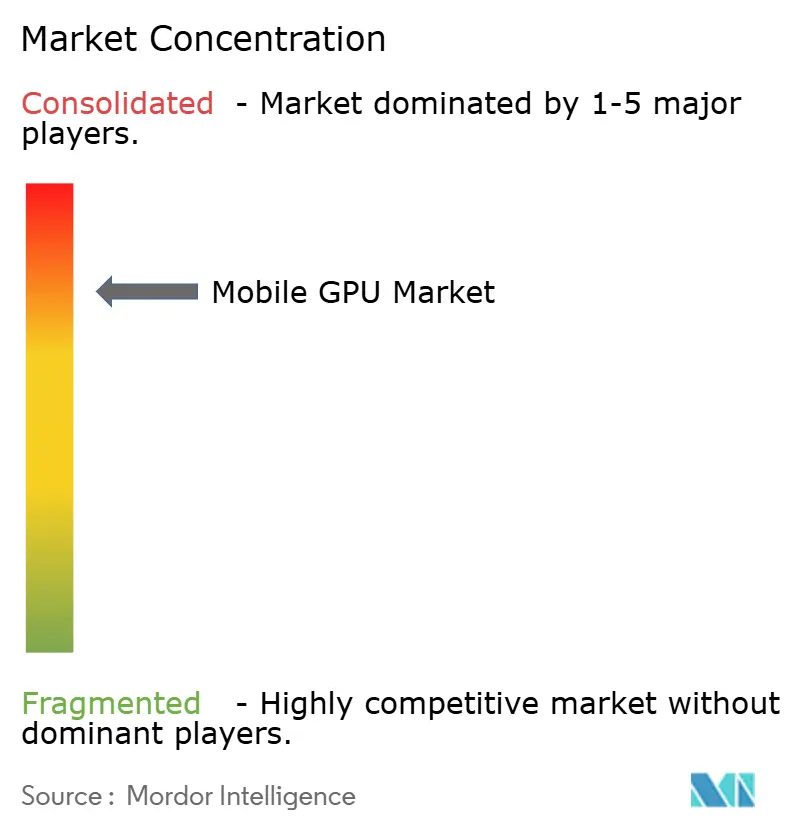

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile GPU Market Analysis by Mordor Intelligence

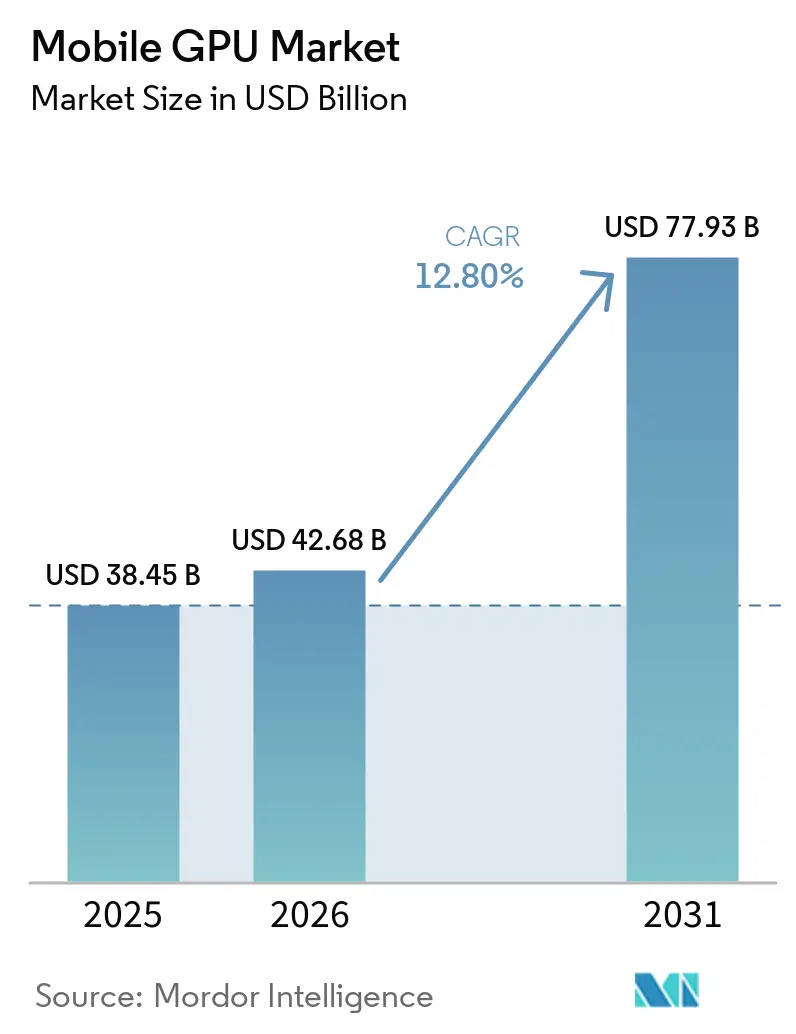

The Mobile GPU market size is projected to expand from USD 38.45 billion in 2025 and USD 42.68 billion in 2026 to USD 77.93 billion by 2031, registering a CAGR of 12.8% between 2026 and 2031. A confluence of on-device artificial intelligence acceleration, mobile gaming monetization, and the continued shift from discrete graphics toward integrated system-on-chip (SoC) architectures is lifting demand for energy-efficient yet compute-dense mobile GPUs. Asia-Pacific dominates shipments because smartphones remain the primary computing device for more than half of the region’s residents, and 5G coverage has improved game-streaming quality. Foundry transitions to 3 nm and 2 nm nodes are unlocking higher transistor budgets for ray tracing and tensor cores without breaching handset thermal envelopes, while game studios are standardizing on Vulkan and Metal to reach both Android and iOS audiences, lowering porting costs for richer titles. Meanwhile, hardware-accelerated upscaling, such as Qualcomm’s Adreno HPM and Samsung’s ENSS, is helping mid-range phones deliver console-grade visuals within their tighter power budgets.

Key Report Takeaways

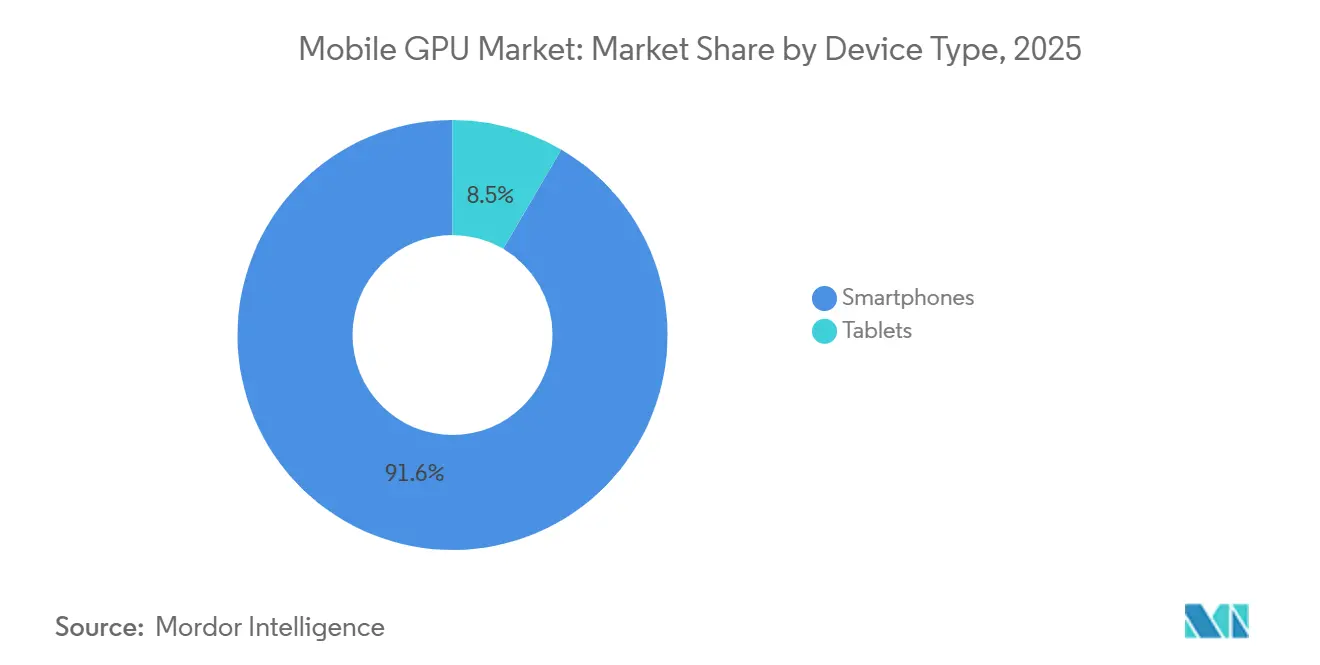

- By device type, smartphones led the mobile GPU market with 91.55% share in 2025, and tablets are forecast to grow at a 13.47% CAGR through 2031.

- By price tier, devices above USD 600 expanded at a 13.88% CAGR from 2026 to 2031.

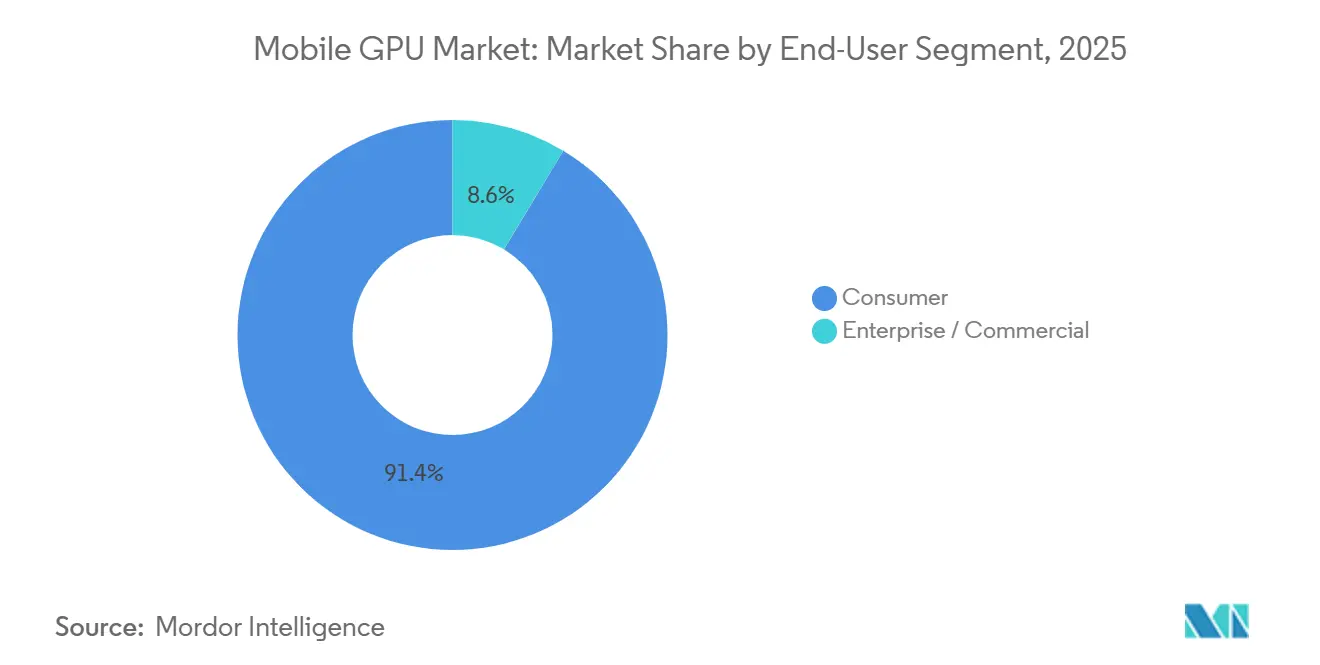

- By end-user segment, enterprise and commercial deployments recorded the fastest 13.83% CAGR over 2026-2031.

- By geography, the Asia Pacific led the mobile GPU market with a 68.33% share in 2025 and is forecast to grow at a 13.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing Demand for Mobile Gaming Graphics Performance | +3.2% | Global, strongest in China, India, Indonesia, Philippines | Medium term (2-4 years) |

| Adoption of AI Accelerators Within Mobile GPUs | +2.8% | North America and premium-tier Asia-Pacific | Long term (≥ 4 years) |

| Rollout of 5G Enabling High-Bandwidth Graphics Streaming | +2.1% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Growth of Foldable Devices Requiring Enhanced GPU Efficiency | +1.5% | China, South Korea, United States | Medium term (2-4 years) |

| Mainstream Integration of Ray Tracing Capabilities | +1.4% | Global, premium and mid-range tiers | Medium term (2-4 years) |

| Rising Developer Adoption of Vulkan and Metal APIs | +0.9% | Global, with higher penetration in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Mobile Gaming Graphics Performance

Mobile gaming revenue increased in 2024, and rising session times are pressuring handset makers to deliver sustained 60 frames-per-second play without thermal throttling. MediaTek’s Dimensity 9500, released in September 2025, employs the Mali-G1 Ultra GPU to boost ray-tracing throughput by 119%, allowing real-time global illumination in titles such as Genshin Impact.[1]MediaTek, “Dimensity 9500 Launch Presentation,” mediatek.com Strategy and role-playing install growth was in the double digits, and these genres rely on complex shader pipelines, which in turn persuade original equipment manufacturers to allocate more die area to graphics blocks. As publishers shift from hyper-casual toward hybrid-casual designs with 5-to-30-minute sessions, demand for mid-range devices that can stay within temperature limits is accelerating.

Adoption of AI Accelerators Within Mobile GPUs

SoCs now integrate neural processing units capable of 40-48 tera-operations per second, enabling night-mode photography, live translation, and generative AI effects entirely on the device. Qualcomm’s Snapdragon 8 Elite Gen 5 pairs the Adreno 840 GPU with a 45-TOPS Hexagon NPU to quadruple dynamic range in imaging pipelines. Microsoft’s Surface Pro 11th Edition leverages the same silicon to drive two external 4K monitors while running on-device summarization features for hybrid workforces.[2]Microsoft, “Surface Pro 11th Edition Technical Specs,” microsoft.com As designers co-locate tensor engines within GPU clusters, shared caches reduce memory contention and allow simultaneous graphics rendering and AI inference.

Rollout of 5G Enabling High-Bandwidth Graphics Streaming

Standalone 5G networks have lowered round-trip latency below 20 milliseconds, making cloud-rendered lighting viable for first-person shooters. NVIDIA inserted Blackwell-based GPUs into GeForce NOW edge nodes, and test sessions over Verizon’s 5G Edge showed 15 ms input lag, letting mid-tier phones stream console-level visuals while the local GPU handles compositing.[3]NVIDIA, “GeForce NOW and Verizon 5G Edge Performance Test,” nvidia.com Qualcomm’s X80 modem supports satellite fallback, maintaining stable throughput during cell hand-offs, a critical factor for competitive esports. Hybrid rendering reduces on-device power draw by up to 40%, lengthening battery life in thin flagships.

Growth of Foldable Devices Requiring Enhanced GPU Efficiency

Foldables demand double-panel rendering and therefore higher sustained graphics clocks, yet their hinged form factors concentrate heat. Samsung’s Exynos 2600 integrates an AMD RDNA 4-based Xclipse 960 GPU plus hybrid pixel-binning thermal controls that keep the chip at 985 MHz without throttling. HONOR’s Magic V6 employs a binned seven-core Adreno to stay below 42 °C surface temperature while gaming.[4]HONOR, “Magic V6 Foldable Thermal Design White Paper,” honor.com Foundry moves to gate-all-around 2 nm nodes, providing the efficiency needed to balance graphics throughput with battery runtime in USD 1,200-plus devices.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Thermal Constraints in Ultra-Slim Smartphone Designs | -1.8% | Global, most acute in premium ultra-thin models | Short term (≤ 2 years) |

| Rising Smartphone ASP Pressure Limiting GPU BOM Cost | -1.5% | Global, pronounced in mid-range tiers | Medium term (2-4 years) |

| Export Controls on Advanced Semiconductor IP | -0.9% | China, secondary effects in Russia | Long term (≥ 4 years) |

| Patent Litigation Risks Among IP Licensors | -0.6% | United States and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Thermal Constraints in Ultra-Slim Smartphone Designs

Flagship handsets are now 7-8 mm thick, so vendors sometimes disable one GPU compute unit or lower frequencies to avoid exceeding 43 °C. Samsung’s hybrid pixel-binning control adds cost to the power-management integrated circuit, but without it, frame rates would collapse during ten-minute gaming sessions.[5]Samsung, “Hybrid Pixel-Binning PMIC Datasheet,” samsung.com Qualcomm created a seven-core Adreno variant for foldables, cutting power draw by roughly 12%. Vapor-chamber cooling adds USD 3-5 per device, squeezing margins in price-sensitive segments.

Rising Smartphone ASP Pressure Limiting GPU BOM Cost

Average selling prices are forecast to rise by 2029, leaving limited headroom for larger die sizes. Qualcomm’s Snapdragon 8 Gen 5, announced in April 2026, drops custom Oryon CPUs in favor of stock Cortex cores to meet OEM budget targets while still boosting graphics by 11%. UNISOC’s 6 nm T8300 offers Mali graphics comparable to two-year-old Snapdragon 700-series chips, enabling sub-USD 150 handsets for growth markets. These cost constraints force tier-two suppliers to trim L2 caches or omit ray-tracing hardware in mid-range launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Smartphones Anchor Volume, Tablets Accelerate in Enterprise

Smartphones held 91.55% of the Mobile GPU market in 2025, confirming their role as the primary screen for more than 5 billion users. Multiple refresh cadences, annual for flagships, biennial for mid-tiers, sustain a steady need for incremental graphics gains that power 120 Hz OLED panels and real-time ray tracing. Tablets represent the fastest-growing slice, posting a 13.47% CAGR between 2026 and 2031 as enterprises favor 2-in-1 devices with multi-monitor support. Microsoft’s Surface Pro 11th Edition couples an Adreno GPU with a 45-TOPS NPU, enabling AI captioning across two external 4K displays, evidence that tablets are graduating from consumption to workstation roles.

The smartphone sub-segment will continue to account for the bulk of the Mobile GPU market, as Qualcomm, MediaTek, and Apple shipped more than 1.2 billion SoCs in 2025. Yet commercial tablets equipped with Snapdragon X Elite are closing the performance gap with thin laptops, bringing workstation-class graphics to field technicians and creative freelancers. Apple’s iPad Air with the M4 chip integrates a nine-core GPU that renders 3D scenes four times faster than the M1, underscoring the convergence of handheld and notebook compute.

By Device Price Tier: Mid-Range Dominates Share, Premium Leads Growth

Mid-range handsets priced USD 200-600 accounted for 43.73% of the Mobile GPU market share in 2025. Qualcomm’s Snapdragon 7-series and MediaTek’s Dimensity 8000-series deliver sustained 60 fps performance at 1080p. Premium devices above USD 600 are forecast to grow at 13.88% CAGR through 2031 as OEMs layer in ray tracing, 40-plus TOPS NPUs, and hardware upscaling to justify higher bills of materials. Samsung’s Exynos 2600, fabricated on a 2 nm gate-all-around node, elevates ray tracing by 50% and introduces ENSS upscaling, demonstrating how leading-edge lithography benefits the upper tier.

Entry-level phones remain dependent on UNISOC’s Mali-based SoCs, which deliver around 50 fps in mainstream titles yet fall short for advanced effects. Nonetheless, longer handset replacement cycles and incremental ASP growth mean mid-range volumes will continue to anchor the Mobile GPU market, even as premium models capture the margins and spotlight for new graphics capabilities.

By End-User Segment: Consumer Applications Drive Volume, Enterprise Accelerates

Consumer apps represented 91.38% of demand in 2025, reflecting the ubiquity of gaming and social media. Adjust’s 2026 Gaming App Insights Report recorded a 45% jump in paid user acquisition across Asia-Pacific, a sign that publishers are investing in immersive titles that push mobile GPUs harder.

Enterprise and commercial uptake is expanding at a 13.83% CAGR as organizations deploy rugged tablets with Snapdragon X Plus and Intel Core Ultra Series 2 processors. These devices pair GPU rendering with onboard AI for live transcription and zero-trust security, answering frontline worker needs. UNISOC’s T8300 powers digital signage and kiosks, highlighting the breadth of industrial graphics use cases beyond traditional smartphones.

Geography Analysis

Asia-Pacific accounted for 68.33% of the Mobile GPU market in 2025 and is set to grow at a 13.79% CAGR over 2026-2031. India’s online gaming revenue is projected to climb by 2028, helped by 87 million additional smartphone users and nationwide 5G rollouts. China remains the largest market by installed base, though regulatory constraints are moderating its growth. Chinese chipmaker UNISOC has seized share in Africa and Southeast Asia with Mali-equipped SoCs that fit ultra-budget phones, broadening the addressable Mobile GPU market.

North America and Europe are driven by premium handsets that integrate ray tracing and 40-plus TOPS NPUs. Microsoft’s enterprise push with Snapdragon X Elite laptops illustrates regional appetite for productivity-class GPUs. U.S. Bureau of Industry and Security export controls have restricted Chinese access to leading-edge GPU IP, reinforcing a bifurcated supply chain where Western consumers receive the latest architectures while Chinese brands fall back on earlier Mali cores.

South America, the Middle East, and Africa are seeing growth. Brazil’s fast-growing Pix payment rails and affordable 4G handsets are helping South America’s gaming revenue rise toward USD 7 billion by 2028. Gulf Cooperation Council countries are investing in esports arenas, boosting demand for high-end handsets. Nonetheless, mid-range silicon will remain dominant in these regions because purchasing power lags the global average.

Competitive Landscape

Qualcomm, Apple, ARM, and MediaTek dominate mobile GPU shipments, reflecting high barriers to entry for low-power graphics design. Qualcomm’s September 2025 court victory over ARM preserved its ability to pair Adreno GPUs with custom Oryon CPUs, a differentiator that competitors on stock cores cannot easily match. Samsung’s co-development with AMD on RDNA-based mobile GPUs and MediaTek’s aggressive 3 nm road map show that partnerships with desktop GPU houses are accelerating feature migration into phones.

Imagination Technologies and UNISOC address cost-sensitive niches: PowerVR cores appear in select Chinese handsets, while UNISOC’s 6 nm SoCs have gained significant traction in global smartphone shipments. AMD re-entered the mobile field in Q1 2026 with the Ryzen AI 400 Series and Radeon 800M GPUs that leverage FSR Redstone upscaling, challenging Qualcomm in handheld gaming devices.

Intel’s 18A Panther Lake platform delivers 77% more gaming performance than Lunar Lake, targeting foldable PCs where x86 software compatibility remains crucial. Across suppliers, the trajectory points toward heterogeneous compute: GPUs, NPUs, and image signal processors now share on-die caches, minimizing latency for hybrid workloads.

Mobile GPU Industry Leaders

Qualcomm Technologies, Inc.

Apple Inc.

Arm Ltd.

Samsung Electronics Co., Ltd.

MediaTek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Qualcomm introduced Snapdragon 8 Gen 5 for the premium mid-range, delivering an 11% graphics uplift at a lower bill of materials versus its Elite sibling.

- March 2026: Apple rolled out the iPad Air powered by the M4 chip and a nine-core GPU, which quadruples 3D rendering performance compared with the M1.

- December 2025: Samsung announced Exynos 2600, featuring the Xclipse 960 GPU on a 2 nm gate-all-around process, boosting ray tracing by 50%.

- September 2025: MediaTek launched Dimensity 9500 with Mali-G1 Ultra, raising graphics performance by 33%.

Global Mobile GPU Market Report Scope

The Mobile GPU Market Report is Segmented by Device Type (Smartphones and Tablets), Device Price Tier (Entry-Level Devices less than USD 200, Mid-Range Devices USD 200 to USD 600, and Premium Devices greater than USD 600), End-User Segment (Consumer, and Enterprise and Commercial), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smartphones |

| Tablets |

| Entry-Level Devices (Less Than USD 200) |

| Mid-Range Devices (USD 200-USD 600) |

| Premium Devices (Greater Than USD 600) |

| Consumer |

| Enterprise / Commercial |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Device Type | Smartphones | |

| Tablets | ||

| By Device Price Tier | Entry-Level Devices (Less Than USD 200) | |

| Mid-Range Devices (USD 200-USD 600) | ||

| Premium Devices (Greater Than USD 600) | ||

| By End-User Segment | Consumer | |

| Enterprise / Commercial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the mobile GPU space today, and where is it headed?

The Mobile GPU market size stood at USD 38.45 billion in 2025 and is projected to reach USD 77.93 billion by 2031, expanding at a 12.8% CAGR over 2026-2031.

Which device category drives most shipments for mobile GPUs?

Smartphones accounted for 91.55% of global shipments in 2025, firmly anchoring volume demand, while tablets posted faster growth on the enterprise side.

What role do AI accelerators play in next-generation mobile GPUs?

Integrated neural processing units now deliver 40-48 TOPS on flagship SoCs, enabling on-device tasks such as real-time translation, enhanced night photography, and generative content without cloud latency.

Which geographic region shows the strongest uptake of advanced mobile graphics?

Asia-Pacific holds 68.33% share thanks to rapid smartphone adoption in China, India, and Southeast Asia, and is forecast to grow at 13.79% CAGR between 2026 and 2031.

What is the biggest near-term challenge for handset makers integrating powerful GPUs?

Managing heat in 7-8 mm-thin flagships: vendors often underclock or bin GPU cores and add vapor-chamber cooling, which raises bill-of-materials costs yet remains essential to avoid surpassing 43 °C surface temperatures during extended gaming sessions.

Page last updated on: