ADAS Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.05 Billion |

| Market Size (2031) | USD 7.54 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

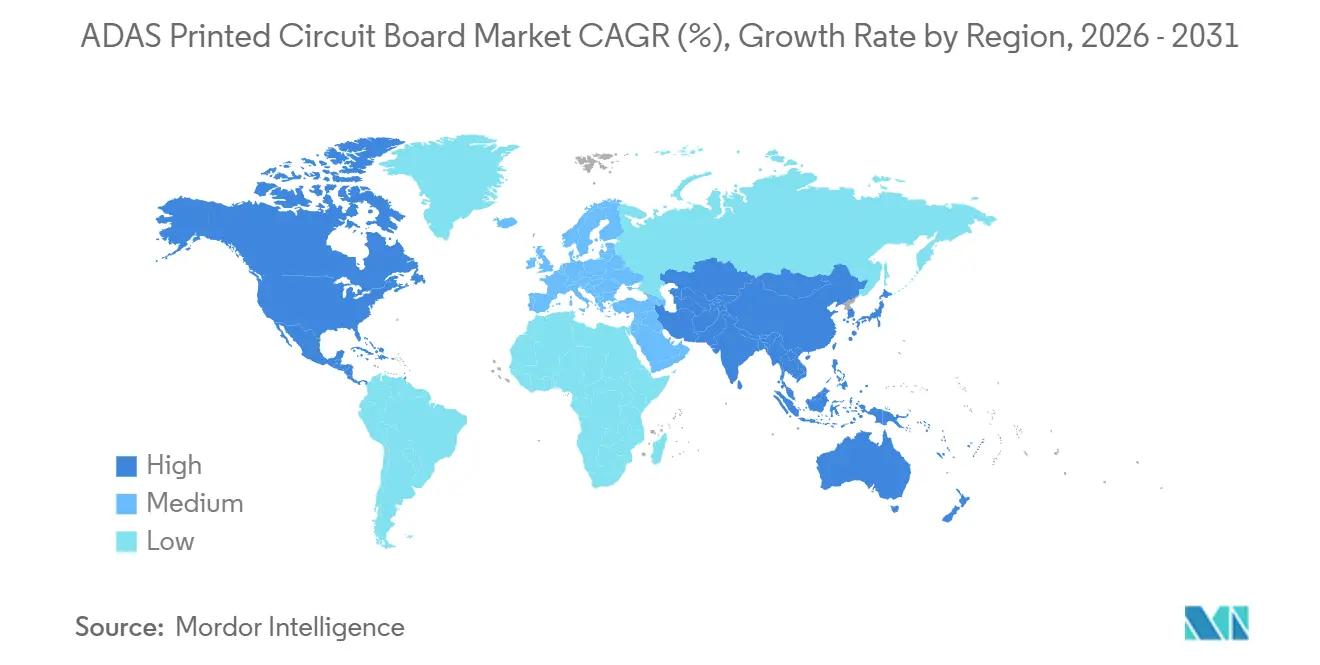

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

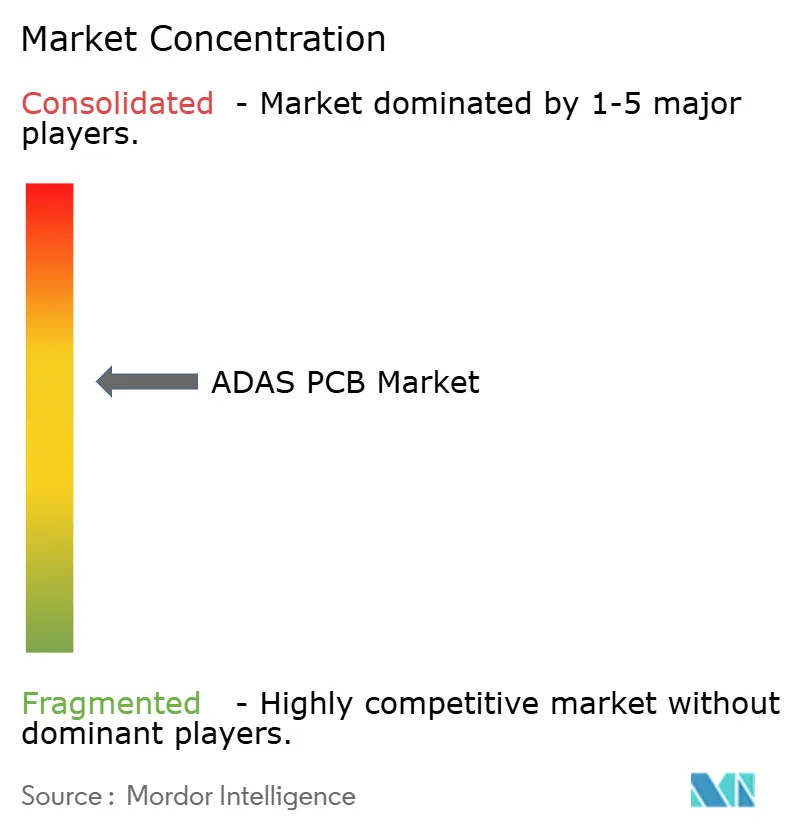

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ADAS Printed Circuit Board Market Analysis by Mordor Intelligence

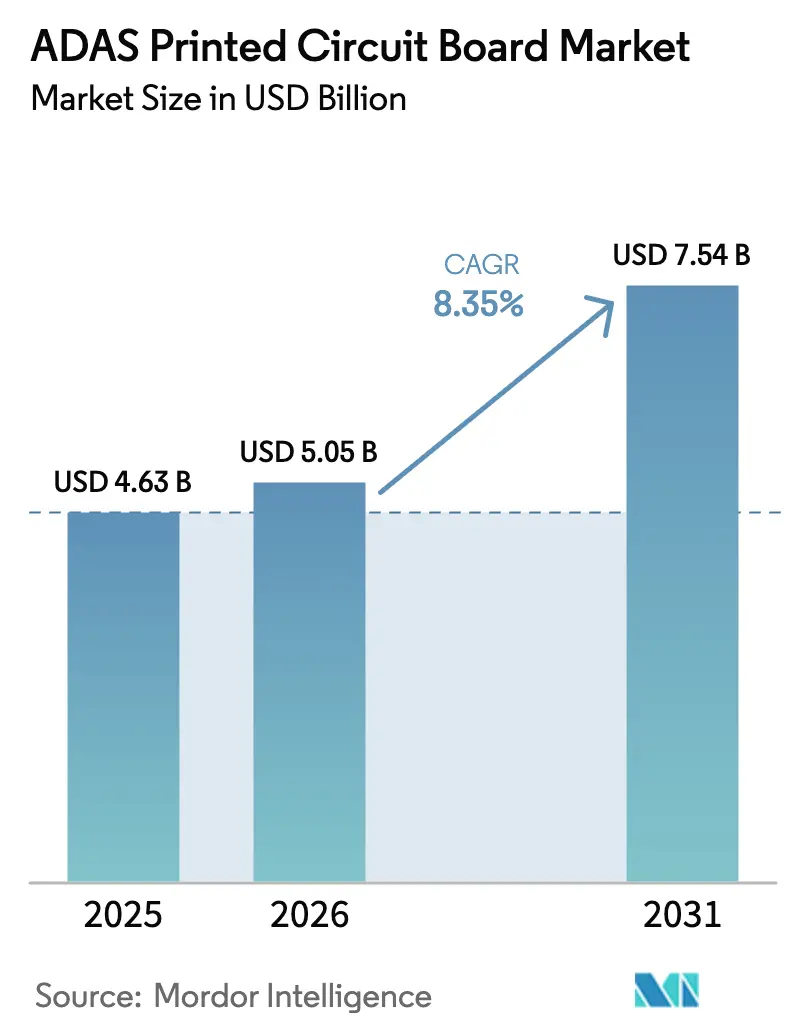

The ADAS Printed Circuit Board Market size is expected to increase from USD 4.63 billion in 2025 to USD 5.05 billion in 2026 and reach USD 7.54 billion by 2031, growing at a CAGR of 8.35% over 2026-2031.

Robust regulatory pressure in the European Union, China and the United States, combined with a steep decline in radar sensor pricing, is lifting multilayer board content in every passenger-car segment. Fabricators able to supply 16-layer high-density interconnect (HDI) boards with via-in-pad technology have benefited from larger average selling prices even as total PCB count per vehicle falls. Concurrently, battery-electric platforms and the transition to domain and zonal electronic-architecture designs are creating sustained demand for rigid-flex substrates that can withstand vibration, temperature cycling and 28 Gbps Ethernet signal integrity requirements. Near-shoring by North American and European original equipment manufacturers (OEMs) has started to rebalance global production footprints, yet Asia-Pacific retains undisputed fabrication leadership thanks to its mature supply chain and capital-efficient capacity additions.

Key Report Takeaways

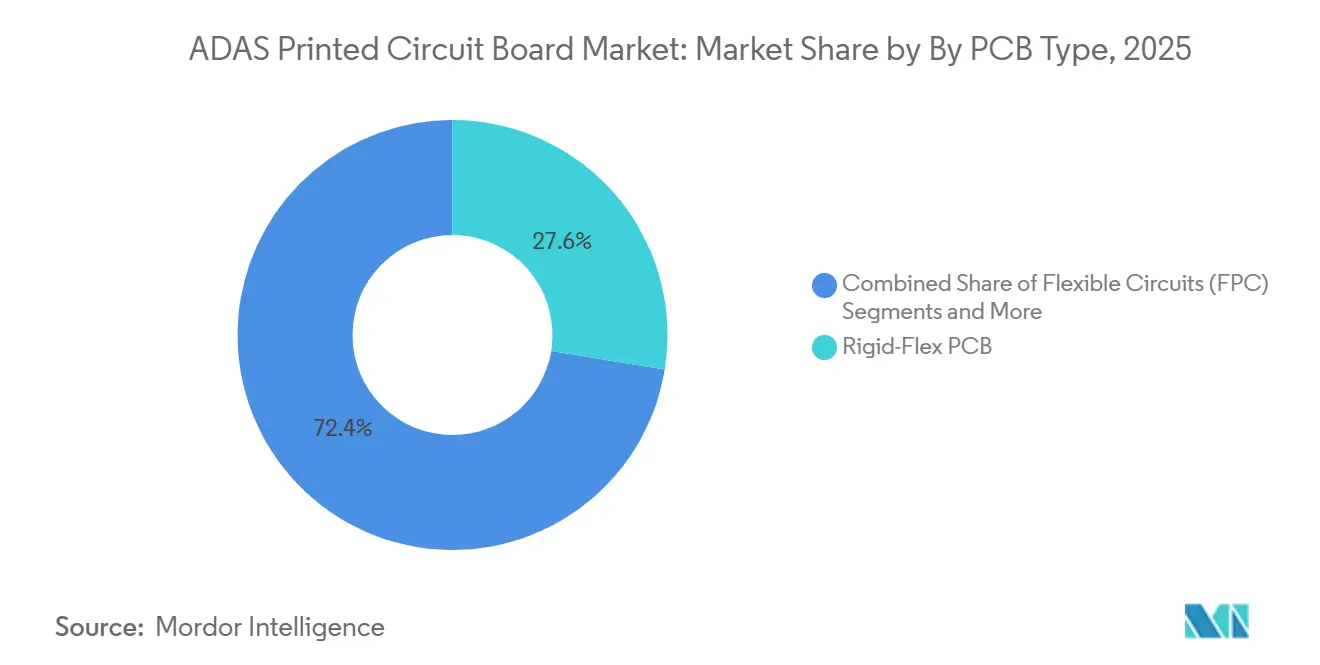

- By PCB type, rigid-flex captured 27.56% revenue share in 2025, while flexible circuits are advancing at an 8.39% CAGR through 2031.

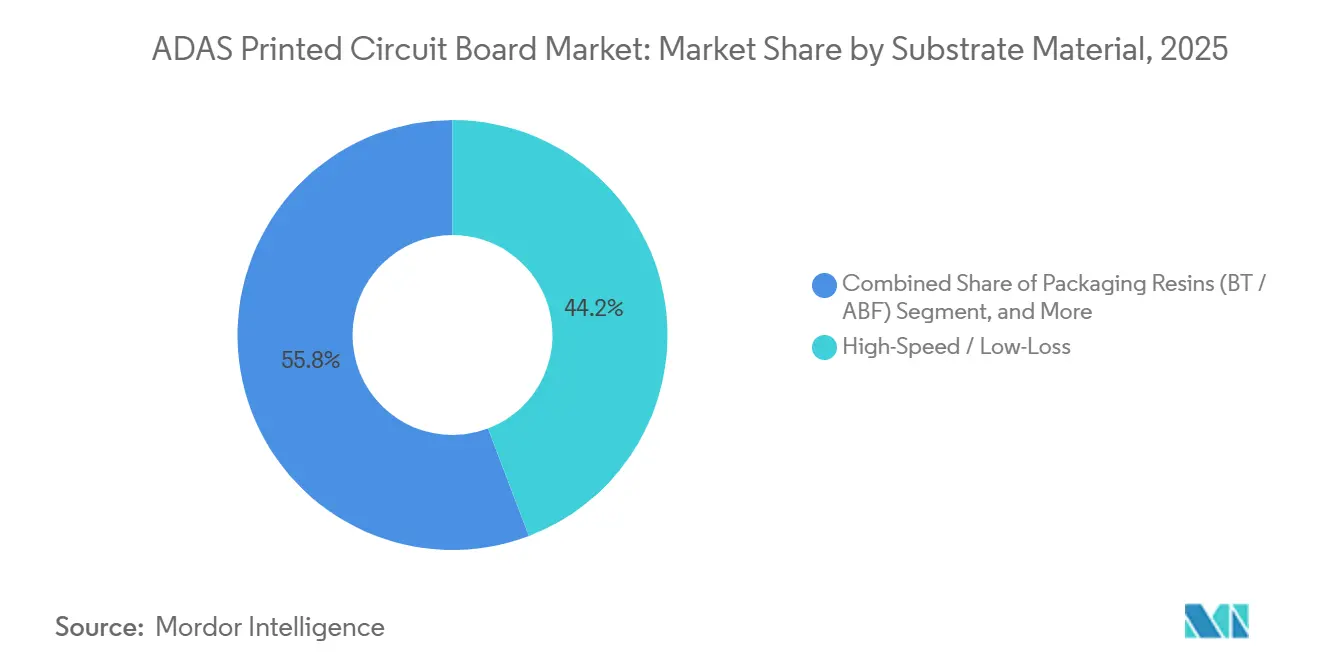

- By substrate material, high-speed and low-loss laminates led with 44.21% of ADAS Printed Circuit Board (PCB) market share in 2025; polyimide is the fastest growing at a 10.11% CAGR to 2031.

- By PCB materials, copper clad laminate accounted for 62.56% of the ADAS Printed Circuit Board (PCB) market size in 2025; high-density packaging substrates are tracking an 8.37% CAGR.

- By geography, Asia-Pacific held an 86.10% share of the ADAS Printed Circuit Board (PCB) market in 2025, and the region is forecast to expand at an 8.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ADAS Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates driving ADAS adoption | +2.1% | Global, strongest in EU and China | Short term (≤ 2 years) |

| Electrification boosting high-layer PCB content per vehicle | +1.8% | Global, concentrated in China, EU, North America | Medium term (2-4 years) |

| Radar sensor cost declines enabling mass-market penetration | +1.3% | Asia-Pacific core, spill-over to South America and Middle East | Medium term (2-4 years) |

| Shift to domain and zonal E/E architectures requiring HDI boards | +1.6% | North America and EU lead, Asia-Pacific following | Long term (≥ 4 years) |

| OEM near-shoring of PCB sourcing after 2025 tariffs | +0.9% | North America and Mexico, secondary in EU | Short term (≤ 2 years) |

| Polyimide material breakthroughs improving flexible-circuit yields | +0.7% | Asia-Pacific manufacturing hubs, Japan, Taiwan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates Driving ADAS Adoption

Global safety legislation is compressing the timeline for moving lane-keeping, autonomous emergency braking and speed-assistance functions from premium trims to entry-level models. EU rules effective July 2024 triggered a step-change in sensor count, vaulting radar usage to three units and cameras to two units per passenger car. China’s 2024 C-NCAP protocol requires radar–camera fusion that in turn needs 8-layer to 12-layer HDI boards capable of 1.2 Gbps throughput. In the United States, a proposed National Highway Traffic Safety Administration rule targeting the 2029 model year embeds 77 GHz corner radars in roughly 17 million vehicles annually. These mandates are lifting PCB value per sub-USD 30,000 vehicle by 18%–22% as OEMs redesign 4-layer boards into 6-layer configurations that expose additional sensor interfaces.

Electrification Boosting High-Layer PCB Content Per Vehicle

Battery-electric architectures concentrate multiple functions into a single domain controller, raising layer counts beyond those of internal combustion equivalents. A typical 400 V electric platform in 2025 relied on 14-layer to 18-layer boards to route high-speed Ethernet, CAN-FD and power-over-coax signals while satisfying 60-ohm differential impedance. Tesla’s Hardware 4.0 design used a 20-layer rigid-flex substrate, shaving 2.3 kg of wiring harness from Model 3 and Model Y builds. BYD standardized 12-layer HDI boards in its Dynasty and Ocean series to hold per-board pricing below USD 18. Higher 800 V systems adopted by Hyundai and General Motors demand thicker copper and specialized dielectrics to prevent arcing, further boosting premium laminate consumption.

Shift To Domain And Zonal E/E Architectures Requiring HDI Boards

Consolidation from dozens of electronic control units to a handful of domain controllers increases per-board value even as unit counts fall. Volkswagen’s E3 2.0 architecture cut ECU count from 70 to 5 but required 16-layer to 20-layer HDI boards with via-in-pad structures to meet 0.4 mm ball-grid-array pitch limits. Stellantis’ STLA Brain integrates 12 cameras, 5 radars and 12 ultrasonic sensors on a 22-layer rigid-flex board engineered for 28 Gbps Ethernet. Suppliers with in-house signal-integrity modeling capacity are winning the majority of these high-value contracts.

Polyimide Material Breakthroughs Improving Flexible-Circuit Yields

Advances in film chemistry and laser drilling have reduced defect rates, allowing flexible circuits to move beyond luxury radar and camera modules. DuPont’s Pyralux AP Plus achieves a coefficient of thermal expansion below 12 ppm/°C, minimizing delamination under −40 °C to +125 °C duty cycles[1]Source: DuPont, “Pyralux AP Plus Technical Bulletin,” dupont.com. Nippon Mektron reported a 35% yield jump after adopting CO₂ laser micro-via drilling that reduced heat-affected zones to ±15 µm[2]Source: Nippon Mektron, “Annual Report 2025,” nippom.com. Taiwan’s Zhen Ding invested USD 120 million to capitalize on rising European demand for ISO 26262-compliant polyimide rigid-flex assemblies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced laminate cost inflation post-COVID | -1.2% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Automotive functional-safety validation bottlenecks | -0.9% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Radar-LiDAR sensor fusion increasing EMC failure rates | -0.6% | Asia-Pacific and North America | Medium term (2-4 years) |

| Skilled-labor shortage in ≥ 8-layer rigid-flex fabrication | -0.5% | North America and EU, emerging in Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Laminate Cost Inflation Post-COVID

Spot prices for low-loss Megtron 6 and similar materials jumped 28% year-over-year in 2025, compressing fabricator margins by up to 220 basis points. Energy costs remain elevated, with German natural-gas prices averaging EUR 45 per MWh (USD 50 per MWh) in 2025, roughly double pre-pandemic norms. HDI builds of 12 layers or more, where laminate share of material cost climbs to 40%, face the harshest impact. North American suppliers negotiated annual price pass-through mechanisms, yet contracts trail spot moves by up to nine months, producing interim gross-margin volatility.

Automotive Functional-Safety Validation Bottlenecks

ISO 26262 ASIL-D certification obliges fabricators to demonstrate random hardware failure rates below 10 failures per billion hours, extending verification cycles. AT&S noted that functional-safety validation consumed 18%-22% of total development time for automotive HDI boards in 2025. Independent labs such as TÜV SÜD and Intertek carried 12-month backlogs, delaying platform launches and steering tier-1 suppliers toward entrenched PCB manufacturers with in-house test chambers and reliability expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Rigid-Flex Boards Hold Lead While Flexible Circuits Accelerate

Rigid-flex substrates captured 27.56% of 2025 revenue, underscoring their dominance in ADAS camera modules and domain controllers where a three-dimensional stackup delivers vibration resistance with a 40%-60% price premium. Flexible circuits recorded the fastest trajectory, advancing at an 8.39% CAGR through 2031 as wrap-around radar housing and slim lidar units reject rigid form factors. HDI technology, critical for NVIDIA Orin and Qualcomm Snapdragon Ride processors, is increasingly standardized in centralized compute platforms, replacing conventional multilayer boards in mid-range vehicles. Standard multilayer rigid boards persist in ultrasonic sensors, yet their share continues to shrink as OEMs consolidate suppliers to simplify procurement. IC substrates provide the bridge between ADAS system-on-chips and controller boards, benefitting from finer line-and-space geometries below 10 µm that underpin 5 nm and 3 nm semiconductor nodes. Metal-core and ceramic variants fill thermal or dielectric niches, notably in 4D radar and lidar power stages.

Samsung Electro-Mechanics ramped FC-BGA capacity by 35% in 2025, enabling a 22% package footprint reduction for Qualcomm’s Snapdragon Ride Flex processor. Yield gains from next-generation polyimide films are lowering flexible-circuit scrap rates, unlocking high-volume adoption beyond premium segments. Consequently, the ADAS Printed Circuit Board market is poised for a steady pivot from rigid multilayer dominance toward a mixed landscape in which flexible and rigid-flex formats coexist with HDI builds tailored to domain-controller performance envelopes.

By Substrate Material: High-Speed Laminates Dominate, Polyimide Gains Momentum

High-speed, low-loss materials owned 44.21% of 2025 revenue because 77 GHz radar and 10 Gbps Ethernet links demand dissipation factors below 0.004 at 10 GHz. Polyimide substrates are on a 10.11% CAGR path through 2031, favored for under-hood radar locations where 150 °C continuous operating temperatures and aggressive thermal cycling challenge conventional FR-4. Glass epoxy serves entry-level cameras and ultrasonic sensors yet cedes share as automakers prioritize impedance control. Build-up films and bismaleimide-triazine resins dominate the IC-substrate space, supporting via densities above 10,000 vias/cm² for advanced system-on-chips.

Rogers RO4000 and Panasonic Megtron 6 lead the high-frequency bracket, enabling 28 Gbps differential signaling over 200 mm trace runs without exceeding a 1 dB insertion-loss budget[3]Source: Rogers Corporation, “RO4000 Series Laminates Datasheet,” rogerscorp.com. AT&S reported that radar board material cost mix shifted from 38% to 52% high-frequency laminate between 2023 and 2025. Polyimide adoption is further stimulated by DuPont’s Pyralux AP Plus, whose 12 ppm/°C thermal-expansion coefficient shrinks die-pad mis-registration during reflow, providing a cost-effective entry point for mass-market flexible circuits.

Geography Analysis

Asia-Pacific commanded 86.10% of 2025 revenue, cementing its status as the fabrication nucleus for the ADAS Printed Circuit Board market. China alone shipped 38 million m² of automotive boards, buoyed by 9.8 million domestic battery-electric vehicle sales and government subsidies favoring ADAS-equipped models. Shennan Circuits and Kinwong added 1.6 million m² of HDI capacity to serve Huawei and Desay SV Automotive. Taiwan’s exports climbed 19% as Unimicron, Zhen Ding and Tripod Technology dispatched 18 million m² of HDI and rigid-flex boards to Europe and North America. South Korea concentrated on high-density package substrates, with Samsung Electro-Mechanics capturing 22% of global automotive IC-substrate revenue. Japan slipped 3% as Toyota and Honda localized sourcing, yet Meiko Electronics continues to dominate ultra-low defect lidar applications.

North America held 9.2% in 2025 but is forecast to rise to 11.5% by 2031. TTM Technologies inaugurated a USD 95 million HDI line in Juarez, Mexico, shaving four to six weeks off OEM lead times. The United States−Mexico corridor benefits from tariff relief, government incentives and proximity to Stellantis and General Motors assembly plants.

Europe maintained 4.7% share under the weight of elevated energy costs; AT&S and Schweizer Electronic emphasize low-volume, high-mix programs such as luxury-segment lidar substrates. Southeast Asia, notably Thailand and Vietnam, is gaining final-assembly work but still imports most HDI boards from China and Taiwan.

Competitive Landscape

The ADAS printed circuit board market exhibits moderate concentration: the top five suppliers, TTM Technologies, Unimicron, AT&S, Samsung Electro-Mechanics and Meiko Electronics, controlled roughly 38% of 2025 revenue. Capital intensity for a single 16-layer HDI production line exceeds USD 80 million, and ISO 26262 ASIL-D certification imposes multi-year investment and process-audit cycles that deter new entrants.

Technology leadership revolves around via-in-pad HDI construction enabling 0.4 mm BGA pitch and any-layer interstitial via structures that trim layer count by up to 30% while safeguarding 28 Gbps signal margins. AT&S filed 14 embedded-component PCB patents in 2025, demonstrating a 1.2 l reduction in domain-controller enclosure volume. Ceramic substrates for solid-state lidar and metal-core boards for high-power 4D radar represent attractive niches where thermal conductivity rather than cost dictates material choice.

Regional challengers hold meaningful positions. Shennan Circuits doubled ASIL-C-qualified volume, leveraging proximity to BYD and SAIC Motor. Schweizer Electronic introduced copper-invar-copper metal-core boards reaching 120 W/m-K thermal conductivity, expanding addressable share in 4D radar power-amplifier modules. Emerging fabricators such as China’s DSBJ and India’s AT&S India aim to undercut incumbents by 25%-30% on mid-tier ADAS programs, though their lack of ASIL-D-graded lines currently caps upside.

ADAS Printed Circuit Board Industry Leaders

TTM Technologies Inc.

Unimicron Technology Corp.

AT&S AG

Samsung Electro-Mechanics Co., Ltd.

Meiko Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Samsung Electro-Mechanics committed KRW 280 billion (USD 210 million) to lift Busan package-substrate output by 40%, targeting ultra-fine-pitch ADAS system-on-chips.

- December 2025: Unimicron finalized a USD 180 million acquisition of a Kunshan HDI plant, earmarking 12-layer to 18-layer automotive production for 2Q 2026.

- November 2025: AT&S secured a seven-year, EUR 420 million (USD 470 million) rigid-flex supply deal with Stellantis for STLA Brain controllers.

- October 2025: TTM Technologies opened a USD 95 million 20-layer HDI line in Juarez, Mexico, dedicated to General Motors and Stellantis ADAS boards.

Global ADAS Printed Circuit Board Market Report Scope

The ADAS Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, HDI, Flexible Circuits, IC Substrates, and Rigid-Flex), Substrate Material (Glass Epoxy, High-Speed/Low-Loss, Polyimide, and Packaging Resins), PCB Materials (Copper Clad Laminate, and High-Density Packaging Substrate), and Geography (North America, Europe, Asia-Pacific, South America). Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) Rigid |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types (Metal-core, Ceramic, Heavy Copper) |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Materials (Metal-core, Ceramic, CEM) |

| North America | United States |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By PCB Type | Standard Multilayer (non-HDI) Rigid | |

| Rigid 1-2 Sided | ||

| High-Density Interconnect (HDI) | ||

| Flexible Circuits (FPC) | ||

| IC Substrates (Package Substrates) | ||

| Rigid-Flex | ||

| Other PCB Types (Metal-core, Ceramic, Heavy Copper) | ||

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT / ABF) | ||

| Other Materials (Metal-core, Ceramic, CEM) | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

How large is the ADAS Printed Circuit Board market today?

The ADAS PCB market size stood at USD 5.05 billion in 2026 and is projected to reach USD 7.54 billion by 2031.

What is the expected growth rate for ADAS Printed Circuit Boards?

The market is forecast to post an 8.35% CAGR between 2026 and 2031.

Which PCB type dominates automotive ADAS applications?

Rigid-flex boards lead with 27.56% revenue share because their three-dimensional structure withstands vibration in camera and controller modules.

Why are high-speed laminates important for ADAS?

77 GHz radar and 10 Gbps Ethernet links require low-loss laminates with dissipation factors below 0.004 to ensure signal integrity.

Page last updated on: