Laptop GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.33 Billion |

| Market Size (2031) | USD 43.86 Billion |

| Growth Rate (2026 - 2031) | 12.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

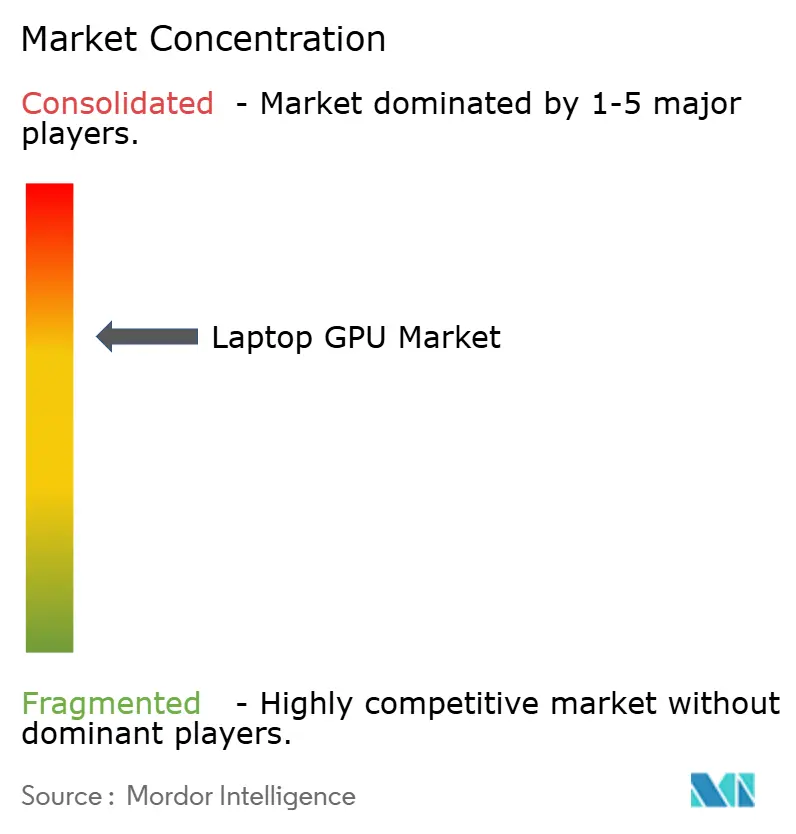

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laptop GPU Market Analysis by Mordor Intelligence

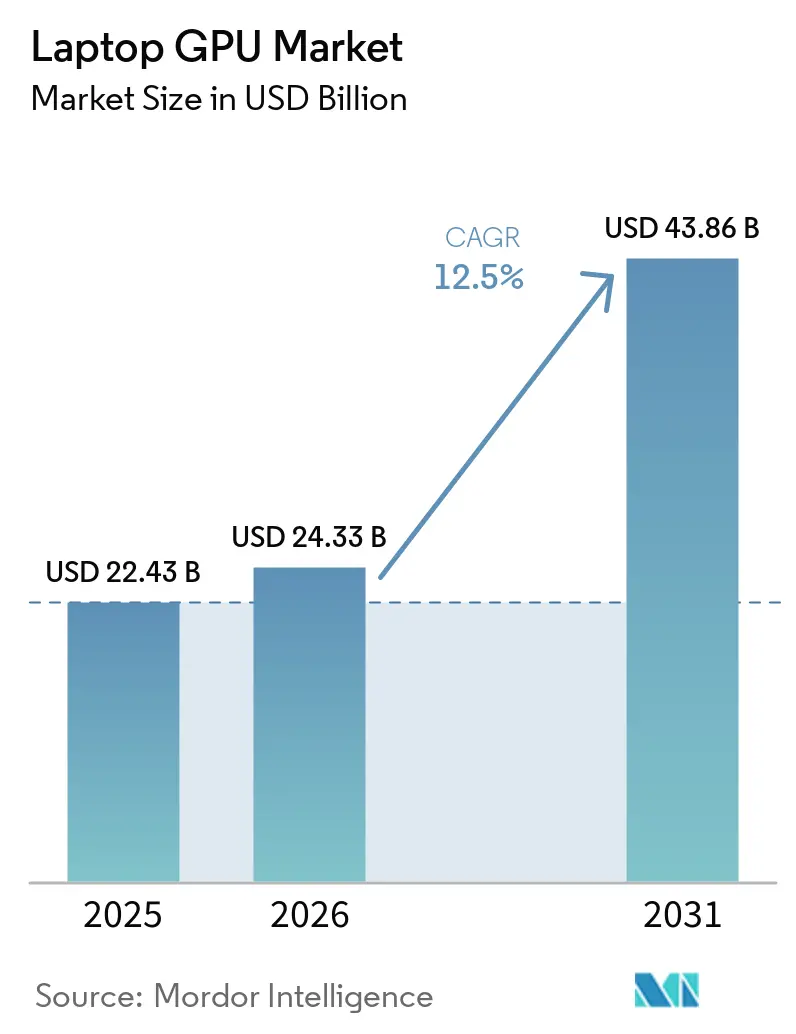

The laptop GPU market size is expected to increase from USD 22.43 billion in 2025 to USD 24.33 billion in 2026 and reach USD 43.86 billion by 2031, growing at a CAGR of 12.50% over 2026-2031. The laptop GPU market is moving through a broader demand cycle than earlier notebook graphics upgrades because spending now comes from gaming users, professional creators, enterprise AI buyers, and premium consumer notebooks at the same time. This pattern is changing product planning across the value chain, since vendors now have to balance graphics performance, battery life, thermal control, AI capability, and system cost within one device category rather than treating them as separate priorities. The laptop GPU market is also seeing stronger pricing power at the upper end because premium gaming, creator, and workstation systems carry richer graphics configurations and more advanced memory, cooling, and display components. Competition is becoming more uneven because NVIDIA has strengthened its lead in discrete mobile graphics, Intel continues to defend mainstream integrated volume, AMD remains important in integrated and x86 platforms, and Apple is changing expectations for performance per watt in premium notebooks. Opportunity in the laptop GPU market is therefore widening in AI-ready enterprise fleets, gaming systems, thin-and-light creator devices, and premium Windows and macOS laptops, even as supply and thermal limits continue to shape how fast vendors can convert demand into shipments.

Key Report Takeaways

- By GPU integration type, integrated GPUs accounted for 62.11% of the 2025 base, while discrete GPUs are projected to expand at a 13.24% CAGR through 2031.

- By laptop class, standard laptops held 46.33% share of the 2025 laptop GPU market size, while gaming laptops are expected to record the fastest CAGR at 13.55% through 2031.

- By processor architecture, x86 captured 75.42% of the 2025 base, while Apple Silicon is forecast to grow at a 13.46% CAGR through 2031.

- By end user, consumer buyers held 48.12% share of the laptop GPU market in 2025, while enterprise buyers are projected to post the fastest CAGR at 13.43% through 2031.

- By geography, Asia-Pacific represented 38.44% of the 2025 base and is expected to remain the fastest-growing regional pocket with a 13.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laptop GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for AI-Enabled and Copilot-Class Notebooks | +3.8% | Global, with early concentration in North America and China | Short term (≤ 2 years) |

| Growth in High-Frame-Rate Gaming and Creative Workloads | +2.9% | Global, Asia-Pacific gaming core, North America and Europe creative | Short term (≤ 2 years) |

| Expansion of Thin-and-Light Gaming and Creator Laptops | +2.0% | Global, fastest in Asia-Pacific and Europe | Medium term (2-4 years) |

| OEM Transition to Hybrid CPU-GPU-NPU Architectures | +1.4% | Global, led by North America and East Asia OEMs | Medium term (2-4 years) |

| Thermal Design Improvements Enabling Higher Sustained Laptop GPU Performance | +0.9% | Global, concentrated in premium segments in North America and Europe | Medium term (2-4 years) |

| Rising Adoption of Mobile Workstations for On-Device AI and 3D Workflows | +0.7% | North America and Western Europe, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for AI-Enabled and Copilot-Class Notebooks

The laptop GPU market is benefiting from a new client computing cycle where AI features are no longer treated as a separate software layer, but are becoming part of how notebooks are specified, marketed, and refreshed across both consumer and enterprise accounts. Microsoft’s Copilot+ PC framework pushed hardware buyers to focus more closely on local AI capability in 2024 and 2026, which raised the importance of acceleration hardware inside notebooks even when the original buyer intent was productivity rather than gaming.[1]Microsoft Corporation, “Copilot+ PCs Developer Guide,” Microsoft Learn, microsoft.com That shift matters because enterprise buyers increasingly want local inference for privacy, latency, and cost reasons, and that keeps GPU-equipped systems relevant even when cloud AI remains available for larger workloads. The result is that the laptop GPU market is drawing demand from users who previously would have stayed with conventional notebook refreshes, especially when AI tasks, graphics tasks, and daily productivity now sit inside the same purchase decision. It also raises the value of vendors that can position their products as AI-ready without giving up battery life, system responsiveness, or the software compatibility that enterprise procurement teams still expect. Over time, this widens the addressable base for premium notebooks and shortens replacement cycles for users who see AI capability as a practical feature rather than an experimental add-on.

Growth In High-Frame-Rate Gaming and Creative Workloads

The laptop GPU market continues to draw strong momentum from gaming systems because high-refresh displays are now common enough that they influence graphics requirements in mid-range and premium notebooks, not only in enthusiast devices. NVIDIA’s Blackwell-based GeForce RTX 50 Series added DLSS 4 and Multi Frame Generation, which strengthens the case for buying more capable mobile graphics hardware in systems designed for high-frame-rate gaming and visually complex applications. The same hardware direction also benefits creator workloads because the tensor and graphics resources used for advanced gaming effects are increasingly useful in denoising, upscaling, rendering, and editing workflows that run on portable systems. That overlap is important because it reduces the old separation between gaming laptops and creator laptops, which means one device category can now absorb demand from multiple user groups without a major change in platform design. ASUS’s published 2025 power specifications also show how aggressively OEMs are tuning these systems around higher mobile GPU ceilings across gaming lines, which supports broader premiumization inside the laptop GPU market.[2]ASUSTeK Computer Inc., “The Complete List of GeForce GPU Power Specifications for 2025 ROG and TUF Gaming Laptops,” ASUS ROG, rog.asus.com As this convergence continues, buyers are less likely to see a high-end mobile GPU as a niche gaming component and more likely to see it as a general performance asset across entertainment, creation, and AI-assisted software.

Expansion Of Thin-And-Light Gaming and Creator Laptops

The laptop GPU market is gaining from the fact that discrete graphics are moving into slimmer notebook designs that previously had little room for meaningful thermal headroom or sustained graphics power. NVIDIA’s Max-Q positioning for the Blackwell laptop generation focused directly on better battery life and thinner chassis support, which helps discrete GPUs reach buyer groups that historically defaulted to integrated graphics because of size and mobility priorities. ASUS’s 2025 ROG and TUF lineup showed how far this shift has progressed, with the same GPU family appearing across very different chassis and power envelopes, which means industrial design and cooling execution now shape real performance more than the graphics brand alone. This matters for the laptop GPU market because it opens price bands and form factors that were once difficult for discrete graphics to enter, especially in premium notebooks aimed at users who travel frequently but still need strong visual or AI performance. It also changes how OEMs differentiate products, since the value now sits not just in the GPU chip but in how well each vendor packages power delivery, vapor chambers, fan curves, and display quality into a portable design. As thin-and-light gaming and creator laptops become more credible, the market ceiling for discrete mobile graphics rises without requiring buyers to move into bulky workstation-style machines.

OEM Transition to Hybrid CPU-GPU-NPU Architectures

The laptop GPU market is also being shaped by platform design changes as OEMs treat CPU, GPU, and NPU resources as a combined performance stack instead of isolated processing blocks. That approach matters because local AI inference, graphics rendering, productivity tasks, and background acceleration no longer need to compete for one processor path when workload routing is planned more carefully at the system level. Dell’s Pro Max 16 Plus is one example of how vendors are already framing portable AI systems around multiple acceleration engines, pairing discrete AI hardware and professional graphics resources inside one mobile workstation platform.[3]Dell Technologies Inc., “Reimagining AI: Discrete NPU Power with Dell Pro Max,” Dell Blog, dell.com In practical terms, this can improve effective system efficiency because low-power AI tasks can be moved away from graphics resources that are better reserved for rendering, simulation, or visually intensive creation workloads. The laptop GPU market benefits when this division of labor improves user experience, since buyers are more willing to pay for higher-end configurations if they feel the hardware is being used intelligently rather than simply being advertised with bigger specifications. Europe’s evolving compliance environment around AI, privacy, and device design also strengthens the appeal of more capable local computing stacks, particularly in enterprise notebooks where on-device processing has security and control advantages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Bill of Materials Pressure in Premium and AI-Ready Notebooks | -2.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Power and Thermal Constraints in Thin Chassis | -1.9% | Global, most pronounced in the thin-and-light and ultrabook segments | Medium term (2-4 years) |

| Short Upgrade Cycles in Mainstream Consumer Laptops | -1.3% | Global, most acute in North America and China | Medium term (2-4 years) |

| Supply Chain Dependence on Advanced Packaging and Memory Availability | -0.9% | Global, disproportionate impact on TSMC-dependent GPU vendors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Bill of Materials Pressure in Premium And AI-Ready Notebooks

The laptop GPU market faces a real volume constraint because the same notebook classes that carry the strongest graphics content also absorb higher memory, display, cooling, and power subsystem costs at the same time. NVIDIA’s move to GDDR7 across newer mobile graphics products raises performance potential, but it also contributes to a richer bill of materials that can restrict how widely premium GPU configurations spread into mainstream price bands. JEITA’s April 2026 PC market data from Japan showed how sharply memory and system costs can affect notebook pricing, with domestic average unit prices climbing materially in a short period under supply pressure. This matters because higher selling prices can lift revenue in the laptop GPU market even when shipment growth slows in entry and value segments, which creates a gap between market value expansion and unit accessibility. It also puts more pressure on OEMs to defend margins through premium positioning, which can narrow the reachable buyer pool if macro conditions weaken. Until component costs ease more clearly, the market will keep facing a trade-off between better graphics capability and the affordability needed for wider adoption.

Power and Thermal Constraints in Thin Chassis

The laptop GPU market also remains limited by the fact that a mobile graphics chip only delivers its intended value when the notebook can sustain the power and thermal load attached to it over real workloads. ASUS’s published 2025 configuration data showed large differences in total graphics power across systems that use the same GPU family, which illustrates how much real output still depends on chassis design rather than on model branding alone. That gap becomes more important when notebooks are expected to handle both AI inference and graphics tasks, because simultaneous CPU and GPU stress can expose thermal weaknesses that are less visible in short gaming demonstrations. The risk for the laptop GPU market is that buyers may pay for a premium graphics nameplate but receive inconsistent sustained performance, which can weaken repeat purchase intent in enterprise and creator segments that depend on predictable output. Thermal engineering therefore matters not only for differentiation, but also for trust, since informed buyers and procurement teams increasingly evaluate cooling credibility before approving higher-cost graphics configurations. If vendors do not solve this problem cleanly in thinner designs, some of the addressable demand created by AI and premium mobility will remain harder to convert into long-run market volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Integration Type: Discrete GPU Demand Rising On AI And Gaming Convergence

Integrated GPUs held 62.11% of the global laptop GPU market in 2025, which kept them firmly in the lead because mainstream notebooks still prioritize cost efficiency, battery life, and adequate daily performance over specialized graphics throughput. This large installed base reflects the volume weight of education systems, commercial fleets, and value consumer notebooks where integrated graphics remain sufficient for office productivity, browsing, video playback, and light content creation. Intel Xe integrated graphics and AMD’s integrated RDNA-based solutions continue to matter in this part of the laptop GPU market because they serve the broadest shipment layers and fit the economics of sub-USD 700 notebooks. That position is not likely to reverse quickly because mainstream buyers still respond strongly to total system price, long battery runtime, and software compatibility rather than to headline graphics specifications. Even so, the integrated segment is no longer insulated from premiumization because AI expectations and richer media workloads are lifting the performance floor even in conventional notebook categories.

Discrete GPUs are projected to record the fastest growth in this segmentation at a 13.24% CAGR from 2026 to 2031, which reflects rising demand from gaming, creator, and AI-capable notebook buyers. Integrated GPUs represented 62.11% of the laptop GPU market share in 2025, but the faster expansion of discrete configurations shows that incremental value is increasingly being created higher in the performance stack. NVIDIA’s Blackwell laptop graphics launch strengthened that shift by widening feature differentiation in ray tracing, AI acceleration, and frame generation across mobile systems. AMD remained important to the broader laptop GPU industry, but its 2025 RDNA4 emphasis on desktop products left NVIDIA with more room to shape pricing and feature expectations in discrete mobile gaming graphics. The net effect is that the laptop GPU market is still led by integrated volume, while growth leadership has moved more clearly toward discrete systems that can justify higher pricing through gaming quality, creator speed, and local AI capability.

By Laptop Class: Gaming Laptops Outpace All Other Categories

Standard laptops held 46.33% of the laptop GPU market in 2025, and that share shows how much the laptop GPU market still depends on broad commercial, education, and general consumer demand rather than on specialized performance systems alone. Most of these notebooks continue to ship with integrated graphics because their primary use cases are document work, communications, learning, streaming, and basic multitasking, all of which can be handled without a discrete GPU premium. The size of this class also means that even small specification changes at the mainstream level can influence the whole market’s direction, especially if AI features gradually push buyers toward stronger integrated solutions or selective entry discrete options. At present, however, system cost remains the main boundary, and that keeps standard laptops anchored to integrated graphics for much of the forecast period. The category therefore provides scale and stability to the laptop GPU market even if it does not produce the strongest growth rates.

Gaming laptops are forecast to expand at a 13.55% CAGR through 2031, which makes them the clearest high-growth class in the current notebook graphics cycle. This segment commands a meaningful share of the laptop GPU market size because buyers in gaming systems accept higher prices for better refresh rates, stronger thermals, richer displays, and more advanced mobile graphics. NVIDIA’s RTX 50 Series supports that momentum by giving OEMs a stronger premium story around AI-enhanced graphics performance, frame generation, and higher-end mobile gaming experiences. ASUS’s 2025 published power envelopes across ROG and TUF systems also show how gaming notebooks have become the main proving ground for chassis, cooling, and graphics differentiation in the mobile space. Workstations, ultrabooks, and thin-and-light creator systems remain important adjacent classes, but gaming laptops are setting the pace because they combine strong buyer enthusiasm, visible product differentiation, and the clearest path to higher graphics content per device.

By Processor Architecture: Apple Silicon Reshaping the Premium Tier

The x86 architecture accounted for 75.42% of the 2025 base, which confirms that the laptop GPU market still rests primarily on Windows-based software environments, enterprise workflows, and compatibility requirements that favor Intel and AMD platforms. This dominance remains important because business fleets, education deployments, and commercial applications still depend heavily on established x86 ecosystems and related certification processes. The laptop GPU market therefore continues to derive most of its unit volume from x86 notebooks, even when premium attention often shifts toward more specialized product launches. That installed base gives Intel and AMD a durable position in procurement-led segments where stability, support, and continuity matter more than architectural novelty. It also means that changes in x86 integrated graphics quality and AI readiness can still influence the wider market more than many premium headlines suggest.

Apple Silicon is projected to grow at a 13.46% CAGR through 2031, and that growth is notable because it reflects rising acceptance of a very different performance model in the premium notebook tier. Apple’s M4 Pro and M4 Max launch highlighted stronger GPU capability and improved performance per watt, which tightened the gap between advanced integrated graphics and mid-tier discrete laptop graphics in a range of creator and productivity tasks. This pressure matters to the laptop GPU market because it compresses the value proposition of some discrete configurations in workflows where mobility, acoustics, and battery life are more important than raw peak graphics throughput. It also changes competitive expectations, since Windows notebook vendors now have to defend the benefits of separate graphics hardware more clearly when premium buyers compare total system efficiency rather than only top-end benchmarks. Other architectures remain a live variable, but the immediate architectural challenge inside the laptop GPU market is less about replacing x86 volume and more about how Apple is redefining what premium notebook graphics performance should feel like at lower power levels.

By End User: Enterprise Segment Drives Premium GPU Revenue

Consumer buyers held 48.12% of the 2025 base, which made them the largest end-user group in the laptop GPU market by revenue share. This weight comes from gaming, entertainment, general productivity, and content creation demand, all of which support a wide span of notebook price points and graphics levels. Consumer demand also remains more price sensitive than enterprise demand, so it reacts faster when graphics-rich notebooks move too far above mainstream affordability. That sensitivity matters because premium gaming and creator systems can lift revenue, while a softer value segment can still reduce overall unit velocity in the broader market. The consumer segment therefore remains essential to scale, visibility, and product innovation in the laptop GPU market, even when its spending pattern is less predictable than professional procurement.

Enterprise is forecast to post the fastest CAGR in this segmentation at 13.43% through 2031, and that pace shows how quickly professional demand is moving toward portable systems with stronger local compute. Enterprise buyers are a growing source of laptop GPU market size because mobile workstations and AI-ready commercial notebooks now support data-sensitive tasks that organizations prefer to keep on-device. Dell’s Pro Max 16 Plus is a clear example of this shift, with a design that combines professional graphics and dedicated AI hardware for developers and advanced technical users who need portable local inference capability. HP’s ZBook Fury line also shows how established workstation vendors are targeting high-value professional users who need certified, portable graphics performance for engineering, design, and compute-heavy tasks. Education and government remain smaller by revenue, but they continue to add meaningful unit support in selected markets, while enterprise is becoming the segment that most directly ties the laptop GPU market to AI, security, and professional workflow spending.

Geography Analysis

Asia-Pacific held 38.44% of the laptop GPU market size in 2025 and is expected to record the fastest regional CAGR at 13.57% through 2031. This leadership reflects a region with both scale and momentum, since China contributes a large notebook volume base while India and Southeast Asia are adding demand through premiumization, gaming interest, and broader notebook adoption. The laptop GPU market in Asia-Pacific also benefits from a wide spread of buyer groups, ranging from entry consumer notebooks and school deployments to premium gaming systems and creator laptops. China remains the main anchor for regional scale because premium notebook demand has strengthened along with AI PC interest, which lifts the value mix toward better graphics configurations. India is becoming a more visible growth market as gaming notebook adoption rises from a lower base and more buyers move toward higher-spec portable systems. Japan adds another important layer because replacement activity and institutional programs supported a strong PC cycle through FY2025, even if some correction is expected afterward. Taken together, these dynamics make Asia-Pacific the broadest opportunity set in the laptop GPU market, with both mainstream and premium demand contributing to growth.

North America remains the strongest revenue region on a per-unit basis because enterprise workstation demand and premium gaming notebooks carry higher average selling prices than most global regions. The laptop GPU market in North America benefits from mature buyer awareness, strong channel support for premium devices, and a corporate base that is willing to invest in mobile graphics for AI development, CAD, simulation, and advanced content work. NVIDIA’s premium mobile graphics push and HP’s workstation positioning both align well with this demand structure, which keeps higher-value graphics configurations visible across commercial and enthusiast channels. Europe also remains important because engineering, design, and media use cases support workstation and creator notebook demand, while AI and privacy considerations strengthen the case for local processing in regulated environments. The region’s generally higher replacement budgets in Western and Northern Europe help sustain premium graphics attach rates, which makes Europe a meaningful contributor to value in the laptop GPU market even when its notebook unit base is smaller than Asia-Pacific’s.

South America, the Middle East and Africa hold smaller shares of the current laptop GPU market, but they remain meaningful long-run growth spaces because notebook adoption and digital capability are still deepening across several buyer groups. South America benefits from a strong gaming culture in key markets such as Brazil and Argentina, which supports selective demand for discrete GPU notebooks above the regional mainstream. The Middle East and Africa are seeing more technology modernization activity in government and enterprise settings, which gradually expands interest in higher-performance portable systems rather than purely entry-level consumer notebooks. In these regions, the laptop GPU market is still weighted toward entry and mid-range demand today, but improving digital infrastructure, education spending, and interest in AI-enabled computing should widen the path for stronger mobile graphics adoption over the forecast period.

Competitive Landscape

The laptop GPU market is concentrated at the graphics design layer, even though notebook brands and system integrators remain far more fragmented. NVIDIA, Intel, AMD, and Apple account for the large majority of notebook GPU intellectual property shipping into the market, which means most competitive leverage still sits in silicon design, platform integration, software ecosystems, and supplier relationships rather than in the final laptop badge alone. NVIDIA strengthened its position in the discrete part of the laptop GPU market with the January 2025 Blackwell GeForce RTX 50 Series launch, which extended its feature lead in AI-assisted graphics, ray tracing, and frame generation. AMD remained a key player across x86 notebooks and graphics, but its 2025 RDNA4 launch focused first on desktop products, which left mobile discrete competition more open for NVIDIA during an important cycle. Intel continued defending mainstream notebook volume through integrated graphics in the broad commercial and value consumer layers, while Apple used tight hardware and software integration to build a closed premium position that competes on efficiency as much as on raw capability.

Strategic moves in the laptop GPU market have become more varied because suppliers are no longer competing only on frame rates or core counts. NVIDIA pushed further down the price ladder with its June 2026 GeForce RTX 5050 Laptop GPU, which widened Blackwell access to more mainstream discrete systems without giving up the company’s AI and ray-tracing story. Dell took a different route by introducing the Pro Max 16 Plus with separate AI acceleration and professional graphics capability, which suggests that some enterprise buyers may value a more specialized portable compute stack rather than relying on one processor type for every heavy task. Apple’s M4 generation created another form of pressure by raising expectations for graphics performance per watt in premium notebooks, which can pull some professional users away from mid-tier discrete Windows systems if their workload balance favors efficiency and battery life. These moves show that leadership in the laptop GPU market now depends on a mix of performance, AI readiness, thermal execution, system integration, and software compatibility rather than on a single specification race.

White space in the laptop GPU market remains visible in lower-priced AI-capable discrete notebooks and in portable professional systems for regulated or data-sensitive workloads. Vendors that can lower system cost without weakening thermal credibility or graphics consistency will have a clearer route into the upper mainstream market, where many buyers want more capability but still resist premium workstation pricing. Compliance and lifecycle support are also becoming more important because enterprise buyers increasingly expect documented updates, stronger support frameworks, and clearer platform road maps before committing to expensive mobile compute fleets. This means the next competitive gains are likely to come not only from faster chips, but also from better execution across supply, software support, mobility, and trust.

Laptop GPU Industry Leaders

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Apple Inc.

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA confirmed the GeForce RTX 5050 Laptop GPU with 8 GB of GDDR7 VRAM, a 128-bit memory bus (33% wider than the RTX 4050's 96-bit bus), and a TDP range of 35-100 W with Dynamic Boost. Entry-level laptops with the RTX 5050 are available from USD 999, extending Blackwell-generation AI and ray-tracing capabilities to the mainstream discrete GPU segment for the first time.

- May 2026: MSI unveiled its 2026 gaming laptop lineup, led by the Raider 16 Max with Intel Core Ultra 200HX Plus processors and NVIDIA GeForce RTX 5090, rated for up to 300 W combined CPU and GPU power, the highest sustained TDP specification in a production gaming laptop to date. The Crosshair 16 Max targets a thinner chassis at up to 200 W combined power.

- May 2026: Lenovo launched the ThinkStation P4 mobile workstation with AMD Ryzen PRO 9000 Series processors and NVIDIA RTX PRO 6000 Blackwell Workstation Edition GPU, targeting local AI inference and advanced visualization for engineering and data-science professionals.

- April 2026: NVIDIA completed one year for shipping GeForce RTX 5090, RTX 5080, and RTX 5070 Ti Laptop GPUs through OEM partners including Acer, ASUS, Dell, Gigabyte, HP, Lenovo, MSI, and Razer, the most widespread simultaneous GPU launch across laptop OEMs to date, introducing DLSS 4 Multi Frame Generation and FP4 AI precision to portable computing.

Global Laptop GPU Market Report Scope

The Global Laptop GPU Market refers to the worldwide industry encompassing the design, production, and distribution of graphics processing units (GPUs) specifically engineered for laptops, serving applications ranging from gaming and content creation to artificial intelligence, machine learning, and professional visualization.

The laptop GPU market Report is segmented by GPU Integration Type (Integrated GPU and Discrete GPU), Laptop Class (Standard Laptops, Gaming Laptops, Workstation Laptops, and Ultrabooks and Thin-and-Light Laptops), Processor Architecture (x86 Architecture, Apple Silicon Architecture, and Other Architectures), End User (Consumer, Enterprise, Education, and Government), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPU |

| Discrete GPU |

| Standard Laptops |

| Gaming Laptops |

| Workstation Laptops |

| Ultrabooks and Thin-and-Light Laptops |

| x86 Architecture |

| Apple Silicon Architecture |

| Other Architectures |

| Consumer |

| Enterprise |

| Education |

| Government |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By GPU Integration Type | Integrated GPU | |

| Discrete GPU | ||

| By Laptop Class | Standard Laptops | |

| Gaming Laptops | ||

| Workstation Laptops | ||

| Ultrabooks and Thin-and-Light Laptops | ||

| By Processor Architecture | x86 Architecture | |

| Apple Silicon Architecture | ||

| Other Architectures | ||

| By End User | Consumer | |

| Enterprise | ||

| Education | ||

| Government | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the laptop GPU market?

The laptop GPU market reached USD 22.43 billion in 2025, stands at USD 24.33 billion in 2026, and is forecast to reach USD 43.86 billion by 2031 at a 12.50% CAGR.

Which GPU integration type leads notebook graphics demand?

Integrated GPUs led the 2025 base with 62.11% share because mainstream commercial, education, and value consumer notebooks still rely on lower-cost graphics configurations.

Which laptop class is expanding the fastest through 2031?

Gaming laptops are projected to grow the fastest at a 13.55% CAGR as high-refresh displays, premium performance, and creator use cases continue to overlap.

Why are enterprise buyers becoming more important for notebook graphics vendors?

Enterprise buyers are projected to grow at a 13.43% CAGR because they increasingly want mobile systems that can support local AI inference, workstation tasks, and secure on-device computing.

Which region offers the strongest near-term opportunity?

Asia-Pacific is the largest regional pocket at 38.44% of the 2025 base and is also the fastest-growing region at a 13.57% CAGR through 2031.

How is Apple affecting competition in premium notebooks?

Apple Silicon is forecast to grow at a 13.46% CAGR, and the M4 generation is raising expectations for graphics performance per watt, which puts pressure on some mid-tier discrete Windows notebook configurations.

Page last updated on: