Vietnam Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

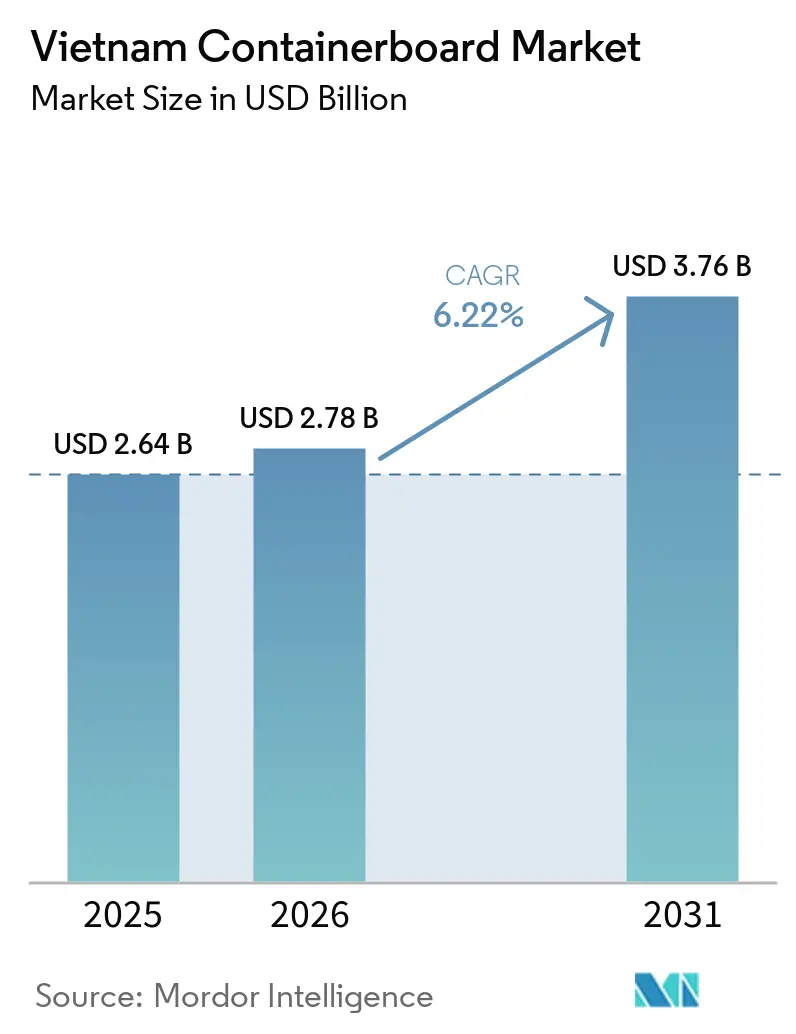

| Base Year Market Size (2025) | USD 2.64 Billion |

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 3.76 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

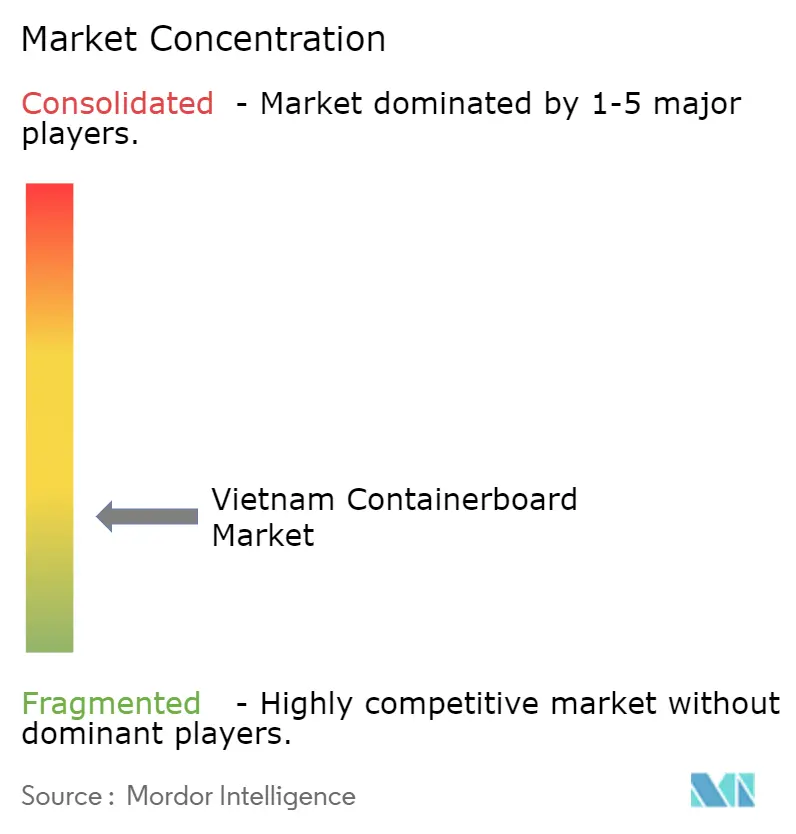

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Containerboard Market Analysis by Mordor Intelligence

The Vietnam containerboard market size was valued at USD 2.64 billion in 2025 and estimated to grow from USD 2.78 billion in 2026 to reach USD 3.76 billion by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). Vietnam’s packaging paper consumption reached 6.19 million tons in 2025, up 12.6% year over year, which shows that local demand is rising faster than the broader regional pace and that the country has become one of Southeast Asia’s strongest containerboard demand centers. In 2026, demand is supported by faster parcel movement, stronger export manufacturing output, and a regulatory shift increasingly favoring fiber packaging over single-use plastics. The northern industrial belt is driving strong demand for corrugated boxes from electronics and manufacturing projects, while the southern belt continues to anchor large corrugated box consumption for food processing, consumer goods, and export shipments. Food and Beverage remains the largest end-user base because retail and cold-chain networks are expanding deeper into the country, while Consumer Goods is growing fastest as incomes rise and export packaging volumes continue to increase. Competition remains strong among large, foreign-affiliated mills, but feedstock volatility in imported OCC and pulp remains the main downside risk for the Vietnam containerboard market.

Key Report Takeaways

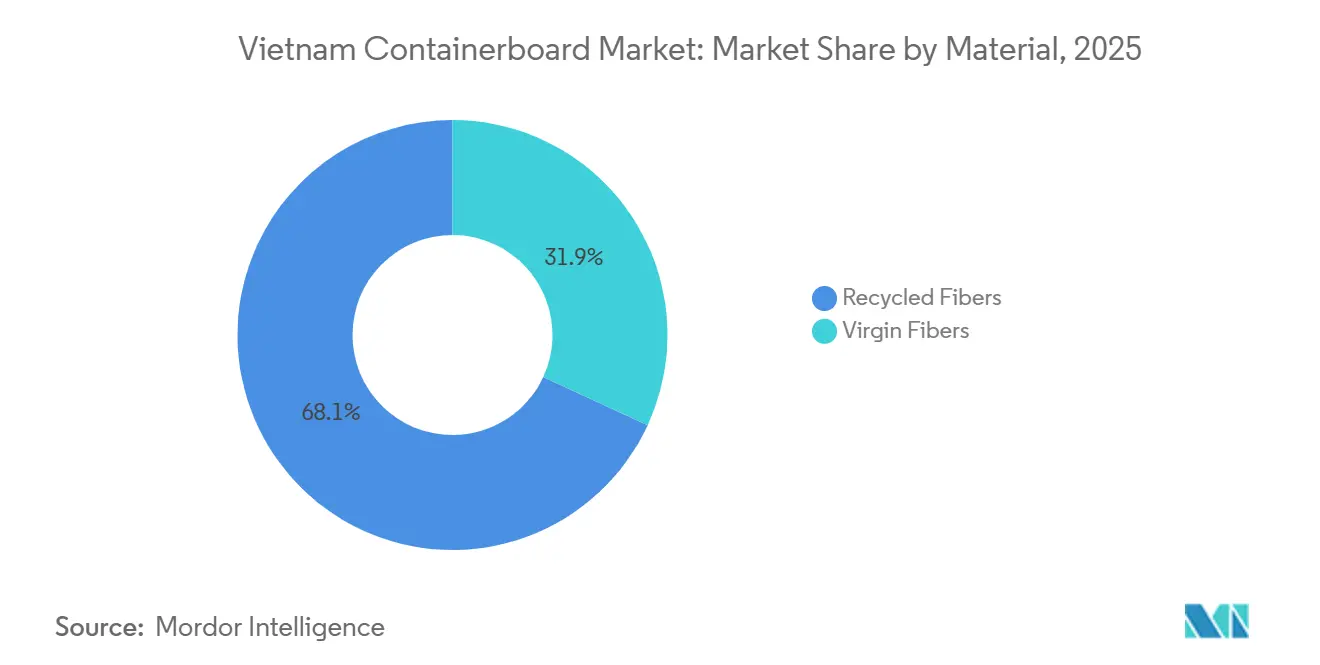

- By material, recycled fibers captured 68.11% of the Vietnam containerboard market share in 2025.

- By product type, the Vietnam containerboard market size for the kraftliners segment is forecast to advance at a 6.89% CAGR through 2031.

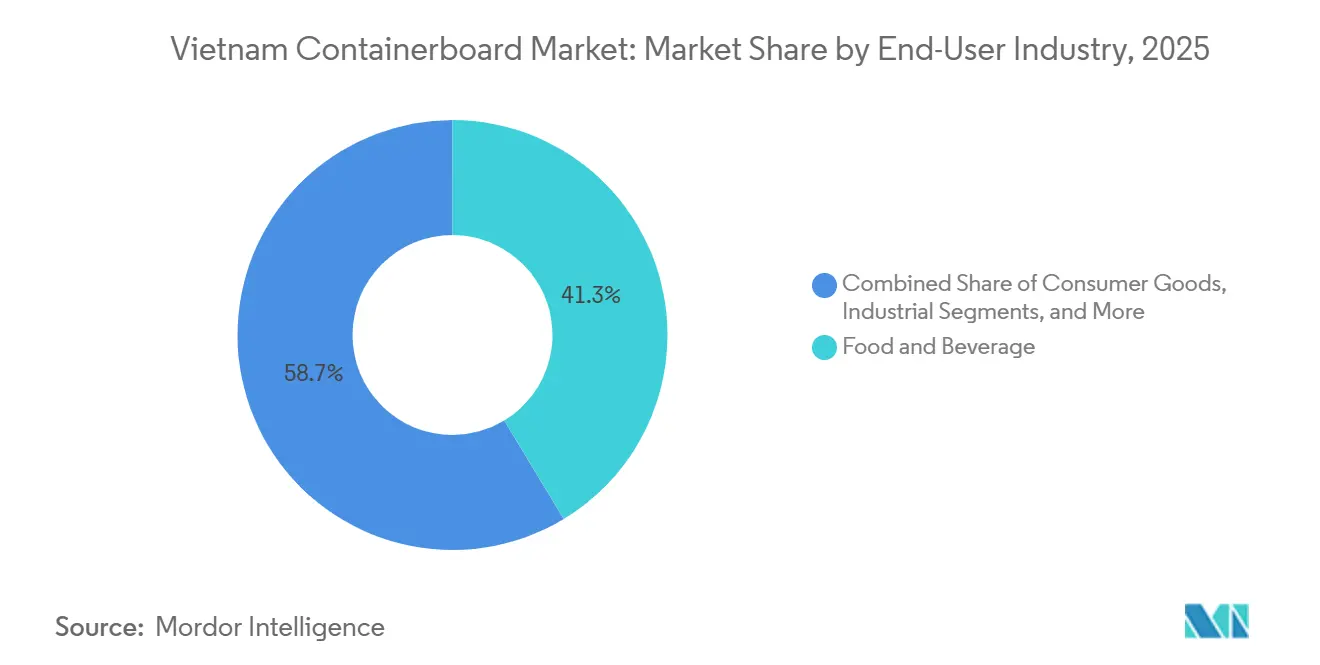

- By end-user industry, food and beverage captured 41.34% of the Vietnam containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel expansion and last-mile box intensity | +2.1% | National, with concentrated gains in Ho Chi Minh City, Hanoi, and Binh Duong logistics corridors | Short term (≤ 2 years) |

| Export manufacturing relocation boosting industrial carton demand | +1.6% | North Vietnam, including Thai Nguyen, Bac Ninh, and Hai Phong, and South Vietnam, including Binh Duong and Dong Nai | Medium term (2-4 years) |

| Food and beverage cold-chain and modern retail expansion | +1.1% | National, with spillover to second-tier and rural provinces | Medium term (2-4 years) |

| Plastic substitution and EPR compliance favoring fiber packaging | +0.8% | National, with early gains in Ho Chi Minh City and Hanoi under Decree 110/2026/ND-CP | Short term (≤ 2 years) |

| Scope 3 procurement rules favoring lightweight local recycled board | +0.3% | Export-linked industrial zones in North and South Vietnam | Long term (≥ 4 years) |

| AI-led box optimization improving yield for short-run orders | +0.2% | Ho Chi Minh City and Binh Duong, where FDI converter concentration is highest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel Expansion And Last-Mile Box Intensity

Vietnam’s leading e-commerce platforms generated VND 148.6 trillion (USD 5.7 billion) in gross merchandise value in Q1 2026, while sales volume reached 1.14 billion items, up 47% and 20% year over year, respectively.[1]Vietnam Chamber of Commerce and Industry, “Vietnam’s E-Commerce Sales Surge 47% to 5.64 Bln in Q1,” VCCI, en.vcci.com.vn Vietnam’s domestic e-commerce market reached USD 31 billion in 2025, placing the country among the world’s top 10 and ASEAN’s top 3 online retail markets. The important shift in the Vietnam containerboard market is that fulfillment is moving toward more individually boxed, better-protected shipments, which increases corrugated board usage per order even as item counts grow more slowly than sales value. This pattern is strongest in Ho Chi Minh City, Hanoi, and Binh Duong, where parcel density, warehousing, and last-mile activity are most concentrated. With the National E-commerce Development Master Plan for 2026-2030 targeting annual online retail growth of 15%-20%, the Vietnam containerboard market is set to receive a steady flow of shipment-driven demand over the next several years.[2]VietnamPlus, “Vietnam’s Q1 E-Commerce Revenue Jumps 47% to 5.7 Billion USD on Shopee, TikTok Shop, Lazada,” VietnamPlus, en.vietnamplus.vn

Export Manufacturing Relocation Boosting Industrial Carton Demand

Vietnam’s manufacturing sector grew 10.6% in 2025, the strongest industrial output growth in 7 years, while electronics and computers exceeded USD 100 billion in exports, and textiles reached USD 46 billion in exports. A survey of Japanese firms showed that 56.9% of respondents in Vietnam planned capacity expansion over the next 1-2 years, the highest expansion intent rate in ASEAN.[3]Voice of Vietnam, “Vietnam Set for Rise in Green FDI in 2026 as High-Tech Shift Accelerates,” VOV, english.vov.vn For the Vietnam containerboard market, this matters because each new factory adds several layers of packaging demand, including packaging for components, intermediate goods, and export master cartons. Electronics assembly also requires stronger corrugated formats, often using 3-layer and 5-layer box structures, which increases demand for higher-performance kraftliner and fluting grades. As more export-oriented production shifts to northern and southern industrial provinces, the Vietnam containerboard market continues to move toward a more industrial, specification-driven demand base.

Food And Beverage Cold-Chain And Modern Retail Expansion

Food distribution demand is expanding as modern trade networks continue to add store count and expand their logistics reach across Vietnam. Masan Group said WinCommerce is targeting nearly 6,100 stores by the end of 2026, with a longer-term goal of 13,000 outlets by 2030.[4]Vietnam.vn, “Masan Shareholders’ Meeting 2026, Opening a New Growth Cycle, Accelerating With Technology and AI,” Vietnam.vn, vietnam.vn Central Retail broke ground on the GO! Phổ Yên mall in Thai Nguyen Province in May 2026, with a VND 400 billion (USD 0.015 billion) investment and the 46th mall in Vietnam, reflects how provincial retail rollout is deepening outside the largest urban centers. CJ CheilJedang’s agreement with Bach Hoa XANH also included cold-chain logistics cooperation, which shows that branded food suppliers are investing in more structured chilled distribution. As the market shifts from wet-market selling toward pre-packed, labeled, and shipped food products, the Vietnam containerboard market benefits from higher use of corrugated trays, outer cases, and store-ready packaging. This is why food retail modernization remains one of the most durable demand supports for the Vietnam containerboard market.

Plastic Substitution And EPR Compliance Favoring Fiber Packaging

Vietnam finalized Decree 110/2026/ND-CP on April 1, 2026, and the regulation takes effect on May 25, 2026, setting a mandatory 20% recycling rate for paper and carton packaging under the country’s EPR framework. The cost structure under the decree strongly favors fiber formats because the recycling cost coefficient for paper and carton packaging is VND 1,938 (USD 0.073) per kilogram, while flexible plastics carry a much higher coefficient of VND 8,486-10,914 (USD 0.32-0.41) per kilogram. Large producers and importers must also file annual recycling declarations through Vietnam’s National EPR Information System, which makes paper-based packaging a simpler compliance route for many multinational consumer goods companies. In practical terms, this supports substitution from plastic trays, shrink-wrapped multipacks, and polybag-based shipping formats into fiber alternatives. The result is a policy-led uplift that strengthens the Vietnam containerboard market even when broader packaging demand is already expanding for commercial reasons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OCC and pulp cost volatility squeezing converter margins | -1.8% | Global, with highest exposure in Central and South Vietnam mills reliant on US and European OCC imports | Short term (≤ 2 years) |

| Import dependence for virgin fiber and premium kraftliner grades | -0.9% | National, with disproportionate impact on the North Vietnam electronics packaging supply chain | Medium term (2-4 years) |

| Monsoon humidity weakening compression strength in storage and transit | -0.4% | Mekong Delta, Central Highlands, and coastal provinces during the May-October wet season | Short term (≤ 2 years) |

| Export-market ESG traceability and carbon disclosure burden | -0.3% | Export-oriented mills supplying EU and US markets under evolving compliance frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OCC And Pulp Cost Volatility Squeezing Converter Margins

Vietnam-bound mills were paying USD 195-200 per ton for US double-sorted OCC in late 2024 before later price declines changed procurement economics across Southeast Asia. China’s recycled pulp import restrictions, introduced in October 2025, disrupted the regional OCC-to-pulp chain and altered buying patterns for imported recovered fiber. Large integrated mills can handle this pressure better because they have scale, broader inventories, and stronger pricing leverage than smaller mills and converters. Vietnam’s Pulp and Paper Association said domestic collection met only 56% of OCC demand in 2025, leaving the remaining 44% exposed to global recovered paper and freight swings. That exposure remains the biggest near-term brake on the Vietnam containerboard market because cost movements can pass through the supply chain faster than selling prices can be reset.

Import Dependence For Virgin Fiber And Premium Kraftliner Grades

Vietnam did not produce virgin kraft pulp at a commercial scale in 2025, and only 2 domestic facilities supplied pulp mainly for internal use, while total pulp imports rose 50% to 638,297 tons from 425,485 tons in 2024. Export-oriented sectors such as electronics and pharmaceuticals are asking for stronger kraftliner grades with performance thresholds that cannot always be met with fully recycled furnish. This is one reason virgin fibers are expected to expand faster than recycled fibers in the Vietnam containerboard market over 2026-2031. Short-fiber pulp averaged USD 540 per ton on a CIF basis in 2025 and increased to USD 568 per ton by early 2026, which keeps premium-grade economics exposed to imported input cycles. Until local premium-fiber capability broadens, the Vietnam containerboard market will remain vulnerable to external pulp pricing and supply conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominance Under Cost Pressure From Virgin-Grade Pull

Recycled fibers accounted for 68.11% of the Vietnam containerboard market share in 2025, keeping them firmly in the leading position, as OCC-based board remained the most economical option for standard corrugated grades. Over 80% of local production historically relied on recovered paper feedstock, so recycled furnish stayed central to mill economics and converter sourcing patterns. Vietnam’s domestic OCC recovery rate improved from 46% in 2021 to 58% in 2024, reducing but not eliminating import dependence for recycled fiber supply. Asia’s total OCC capacity is expected to grow by 4.5 million tons by 2028, with Vietnam contributing close to half of that expansion, strengthening the country’s role as a regional secondary fiber processor.

Virgin fibers accounted for 31.89% in 2025, and this segment of the Vietnam containerboard market is projected to grow at a 6.74% CAGR through 2031. Electronics and semiconductor assembly in provinces such as Thai Nguyen and Bac Ninh require packaging with more stable compression strength and lower moisture sensitivity, which supports demand for premium linerboard grades. Multinational buyers are also pushing local suppliers to increase recycled content because of Scope 3 reporting, but their packaging specifications still require performance standards that often favor virgin-furnish board. That conflict keeps a premium-grade supply gap in place and supports further investment interest in virgin-capable assets. The Vietnam containerboard industry is therefore moving toward a more mixed furnish structure, even though recycled board remains the largest base.

By Product Type: Testliner Leads Volume While Kraftliner Gains Strategic Weight

Testliners accounted for 44.57% of the Vietnam containerboard market in 2025, making them the leading product type by value. Their position reflects the economics of recycled-fiber production and the needs of Vietnam’s large base of converters serving the food, consumer goods, and standard export carton markets. Testliner fits a market where price sensitivity remains high and where many corrugated applications do not need premium strength performance. This is why the grade continues to carry the broadest volume base in the Vietnam containerboard market.

Kraftliners are projected to grow at 6.89% CAGR from 2026 to 2031, making them the fastest-growing product type. Vietnam’s export mix is shifting toward higher-value, more durable goods, which is driving demand for packaging with stronger puncture resistance and better stacking strength. The pressure is most visible in electronics and engineering-related shipments, where transport damage is costly, and packaging specifications are tighter. Fluting remains tied to total corrugated board output, but value per ton is gradually improving as more boxes shift toward higher-performance board combinations. The Vietnam containerboard industry is therefore seeing a slow but meaningful mix shift toward higher-margin grades while testliner still dominates mainstream box production.

By End-User Industry: Food And Beverage Holds The Base While Consumer Goods Accelerates

Food and Beverage accounted for 41.34% of the Vietnam containerboard market in 2025, making it the largest end-user segment. The category was supported by 11% growth in food processing output in 2025 and by wider chilled and ambient distribution networks across the country. WinCommerce’s plan to reach 6,100 stores by the end of 2026 is to expand packaged food distribution into provincial markets, which will drive recurring demand for trays, outers, and transit cartons. Premium food brands are also shifting toward recyclable, certified fiber packaging, which helps improve the value mix of board consumed in this segment.

Consumer Goods is forecast to grow at 6.96% CAGR through 2031, the fastest pace among end users in the Vietnam containerboard market. Rising incomes, stronger e-commerce activity in non-food categories, and export growth in apparel, footwear, and electronics are all increasing box demand per shipped unit. Vietnam exported USD 165 billion in electronics goods in 2025, and SCGP estimated that electronics already accounted for 20% of containerboard end-use in the country. Industrial and other end-user demand is also rising, driven by investment in chemicals, auto components, pharmaceuticals, and capital goods. The Vietnam containerboard industry is therefore balancing a stable food-led base with a faster-expanding consumer goods demand stream.

Geography Analysis

Southern Vietnam remained the largest production and consumption zone in the Vietnam containerboard market in 2025, led by Ho Chi Minh City, Binh Duong, and Dong Nai. This corridor hosts the densest concentration of corrugated converters, consumer goods factories, and export-oriented packaging activity. SCGP’s Vina Kraft Paper, Vina Corrugated Packaging, and Bien Hoa Packaging operations are concentrated in this southern belt, which links paper production to conversion and downstream delivery. The area also benefits from direct access to the Ho Chi Minh City port system, which keeps export container demand structurally high. Even as demand spreads to smaller provinces, the south still holds the scale advantage in raw material handling, labor access, and converter density.

Northern Vietnam is emerging as the fastest-growing consumption region in the Vietnam containerboard market, centered on Hanoi, Bac Ninh, Bac Giang, Hai Phong, and Thai Nguyen. The region’s electronics and semiconductor manufacturing cluster is driving increased demand for industrial cartons and higher-spec corrugated packaging. This northern demand is more specification-driven, as export-oriented assembly plants need stronger packaging performance and greater consistency. Vietnam’s paper and paper products industrial production index rose 10.4% in 2025, the strongest gain since 2019, while packaging demand growth in the north outpaced the local production base. That mismatch is already influencing how companies think about future mill placement and distribution strategy in the Vietnam containerboard market.

Central Vietnam, including Da Nang and the coastal provinces, remains a smaller consumption region in the Vietnam containerboard market. Demand in this corridor is mainly driven by seafood, agriculture, and light manufacturing shipments, which support a steady demand for food-grade corrugated packaging. The region also faces more frequent humidity and storage challenges during the wet season, which can raise packaging specification needs for compression strength and transit performance. Over time, provincial retail rollout and food-processing growth should gradually increase the central region’s role, even though the market remains anchored by the south and accelerated by the north.

Competitive Landscape

The Vietnam containerboard market is moderately consolidated at the production level but fragmented at the converter level. More than 334 companies were active in Vietnam’s packaging industry in 2025, yet the top 10 accounted for only around 30% of market revenue. This split gives large mills a clear scale advantage while keeping pricing pressure elevated across smaller converters and downstream box makers. SCG Packaging’s Vina Kraft Paper held an estimated 22% share of packaging paper sales volume in Vietnam in 2025. Its 500,000 MT per year packaging paper capacity and 52% integration rate between paperboard and fiber packaging give it a strong operating position in the Vietnam containerboard market.

SCGP also strengthened its local position in Q2 2025 by acquiring the remaining 30% stake in Duy Tan Plastics Manufacturing Corporation Joint Stock Company, bringing the business to full ownership and expanding its packaging platform in Vietnam. The company reported that favorable recovered paper costs and higher export volumes to China supported margin performance in its Vietnam integrated packaging operations during 2025. Another visible strategic move is the use of AI for production optimization, helping larger converters reduce material consumption and respond more effectively to short-run orders. These moves show that leadership in the Vietnam containerboard market is no longer defined only by tonnage. Integration, operating discipline, and service capability now matter just as much.

Other producers are targeting open space in premium kraftliner and other higher-spec grades, where local supply still trails demand from export packaging users. Dong Hai Ben Tre’s Giao Long 3 mill and Miza’s expansion plan reflect that push toward broader product capability and stronger linerboard positioning. Lee and Man also continues to treat Vietnam as a platform for wider regional reach, which keeps competitive pressure centered on efficiency and scale. As a result, the Vietnam containerboard market remains competitive even though a few large FDI-backed mills sit at the top of the supply chain.

Vietnam Containerboard Industry Leaders

Cheng Loong Binh Duong Paper Co., Ltd.

Vietnam Lee & Man Paper Manufacturing Limited

Nine Dragons Paper (Holdings) Limited

Kraft of Asia Paperboard & Packaging Co., Ltd.

Saigon Paper Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Central Retail broke ground on GO! Phổ Yên, a VND 400 billion (USD 15.4 million) hypermarket in Thai Nguyen Province, its 46th mall in Vietnam. The project, covering over 12,000 m², will open in October 2027 and is expected to deepen corrugated packaging demand in the northern provincial retail corridor as fresh produce, FMCG, and imported food categories expand distribution reach.

- April 2026: The Vietnamese Government issued Decree 110/2026/ND-CP, effective May 25, 2026, establishing mandatory recycling rates and compliance mechanisms for producers and importers under the Extended Producer Responsibility framework. Paper and carton packaging carries a 20% mandatory recycling rate, the same as aluminum, and the Fs cost coefficient of VND 1,938 (USD 0.07) per kilogram is the lowest among all packaging categories, structurally advantaging fiber-based packaging over plastics in cost-of-compliance calculations.

- December 2025: Dong Hai Ben Tre Joint Stock Company commenced construction of the Giao Long 3 paper mill in Ben Tre Province, a VND 2,250 billion (USD 87 million) investment targeting 390,000 MT per year of capacity with an expected commencement of commercial operations in Q3 2027. The facility will introduce kraftliner production capability to Dong Hai Ben Tre’s portfolio for the first time, diversifying the company’s product mix from its current testliner and corrugated medium focus.

- October 2025: China’s new recycled pulp import restrictions, requiring declaration of wet versus dry processing methods and allowing on-site cargo inspections, disrupted OCC and recycled pulp trade flows across Southeast Asia, causing dry-pulp processors in the region, including several Vietnam-based operations, to temporarily halt production. Vietnam-bound US double-sorted OCC prices, which had reached USD 208-210 per ton earlier in 2025 at China-affiliated mills, came under downward pressure following the policy announcement.

Vietnam Containerboard Market Report Scope

The Vietnam Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacturing of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Vietnam Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and projected size of the Vietnam containerboard market?

The Vietnam containerboard market stands at USD 2.78 billion in 2026 and is forecast to reach USD 3.76 billion by 2031, growing at a CAGR of 6.22%.

Which material type leads demand in Vietnam containerboard?

Recycled fibers lead the market with a 68.11% share in 2025 because they remain the most economical option for standard corrugated applications.

Which product type is growing fastest in Vietnam containerboard?

Kraftliners are projected to grow fastest at 6.89% CAGR through 2031 as export packaging needs shift toward stronger and higher-performance board.

Which end-user segment contributes the most to demand?

Food and Beverage is the largest end-user segment with a 41.34% share in 2025, supported by food processing growth and wider modern retail distribution.

What is driving growth in containerboard demand across Vietnam?

The main drivers are faster e-commerce parcel volumes, export manufacturing relocation, modern retail and cold-chain expansion, and regulation that favors recyclable fiber packaging.

What is the biggest risk facing containerboard producers in Vietnam?

The main risk is feedstock volatility, especially for imported OCC and pulp, because domestic collection met only 56% of OCC demand in 2025.

Page last updated on: