Bangladesh Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 1.95 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Containerboard Market Analysis by Mordor Intelligence

The Bangladesh Containerboard Market size was valued at USD 1.42 billion in 2025 and is estimated to grow from USD 1.48 billion in 2026 to reach USD 1.95 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031).

The Bangladesh containerboard market is being lifted by a broader shift in packaging demand, as garment exports, processed food distribution, and organized fulfillment all require more reliable corrugated formats. Demand is no longer driven only by low-cost volume, because buyers are placing more value on board consistency, moisture control, and end-use performance. The supplier base is also changing, with financially stronger mills positioned to capture growth as weaker operators reduce output or exit. Policy support for paper-based substitutes in retail and institutional packaging is creating another layer of demand for the Bangladesh containerboard market. At the same time, imported raw material dependence, energy shortages, and financing pressure remain the main limits on how quickly local capacity can convert demand into profitable growth.

Key Report Takeaways

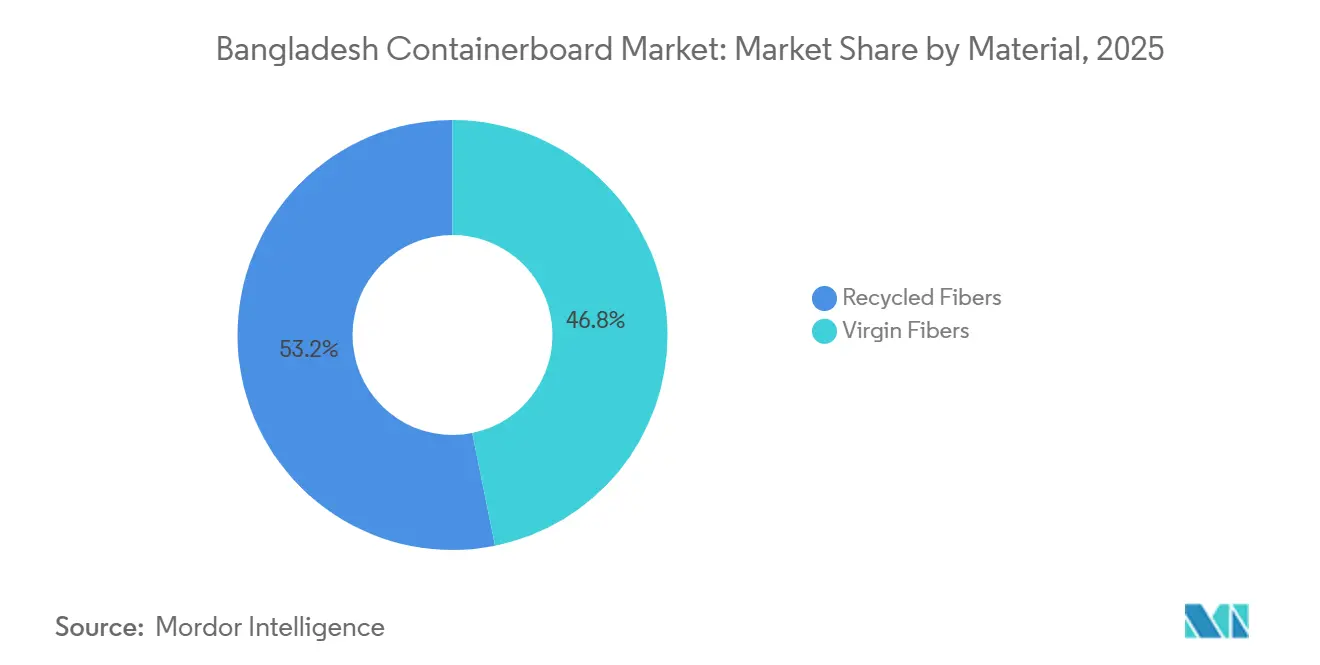

- By material, recycled fibers held 53.17% of the Bangladesh containerboard market share in 2025, while recycled fibers are also forecast to expand at a 6.21% CAGR through 2031.

- By product type, kraftliners accounted for 39.23% share of the Bangladesh containerboard market size in 2025, while flutings are forecast to grow at a 6.67% CAGR through 2031.

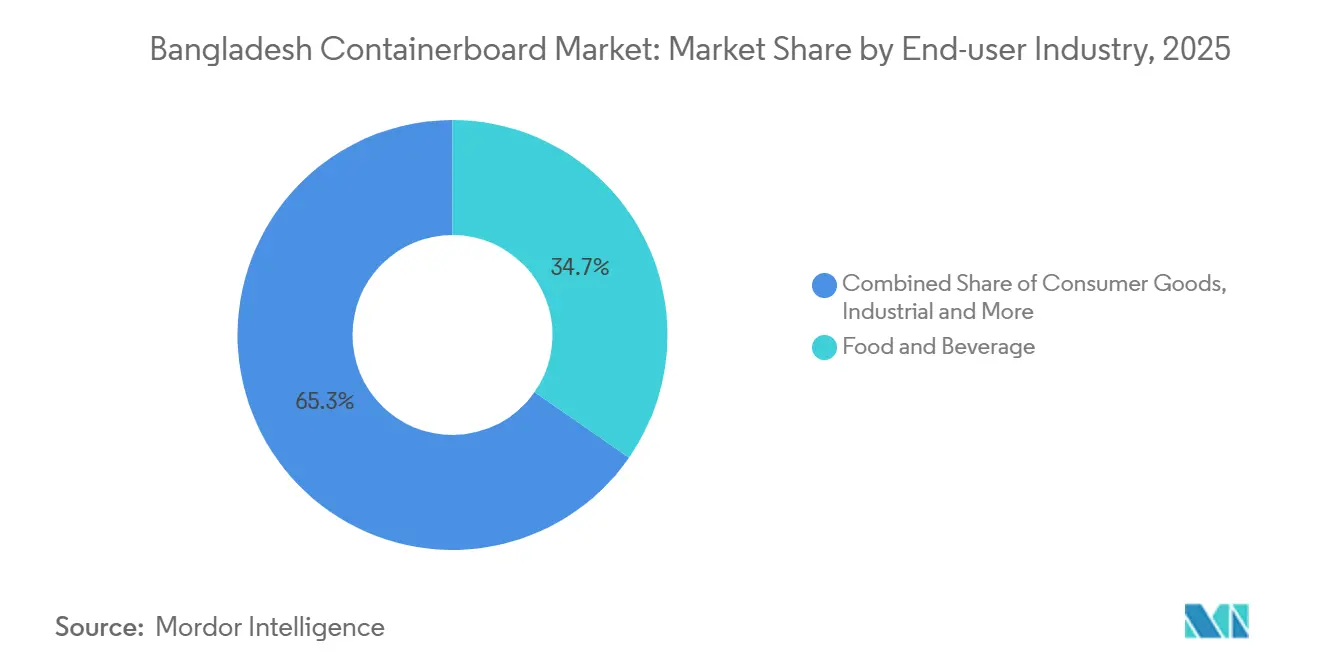

- By end-user industry, food and beverage held 34.67% of market value in 2025, while consumer goods is projected to record the highest CAGR at 6.38% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bangladesh Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Parcel Growth and Domestic Fulfillment Expansion | +1.2% | National, concentrated in Dhaka, Chattogram, with spill-over to Sylhet, Rajshahi, Khulna | Short term (≤ 2 years) |

| Food and Beverage Packaging Demand Expansion | +0.9% | National, with strongest concentration in Dhaka and Chattogram food-processing clusters | Medium term (2-4 years) |

| Export Packaging Demand From Garments and Accessories | +0.8% | Dhaka, Chattogram, and Chittagong EPZ manufacturing belts | Short term (≤ 2 years) |

| Plastic Substitution Push in Institutional and Consumer Packaging | +0.7% | National, with early gains in urban retail, hospitality, and coastal districts | Medium term (2-4 years) |

| Premium Testliner Localization Through Recycled-Fiber Upgrades | +0.5% | Narayanganj, Gazipur, Mirsarai economic zone | Long term (≥ 4 years) |

| Food-Contact Compliance Favoring Better-Quality Paperboard | +0.3% | National, with the heaviest compliance burden in the Dhaka food-processing hub | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel Growth Reshaping Linerboard Specifications

The Bangladesh containerboard market is gaining from faster online order fulfillment, because e-commerce represented 41.73% of CEP operator turnover in 2024 within the broader freight and logistics chain. This is pushing converters and fulfillment operators toward standardized single-wall corrugated formats that can move through repeated handling with less damage. The packaging mix is also shifting toward smaller and lighter boxes, which raises the need for E-flute and F-flute structures with tighter caliper control than many local recycled mills have consistently delivered. That change matters for the Bangladesh containerboard market, because thin-profile corrugated formats expose quality variation more quickly than bulk transport cartons. Mills that improve sheet formation, moisture management, and consistency are better placed to replace imports over the 2026-2031 period, and early technology upgrades at local facilities already point in that direction.

Food and Beverage Packaging Demand Underpinned by Structural Urbanization

Food and beverage was the largest end-user in the Bangladesh containerboard market in 2025 with a 34.67% value share. Demand is being supported by broader urban consumption patterns, because processed food, beverages, and organized retail formats all require shelf-ready cartons and transit packaging. This demand is less exposed to short-cycle export swings, which gives the Bangladesh containerboard market a steadier domestic base. The more demanding part of this shift comes from products that need moisture resistance and cleaner fiber control, especially when food-contact compliance standards become stricter. That is why integrated mills that can balance recycled fiber economics with stronger quality assurance should gain ground as buyers move away from purely commodity board.

Export Packaging Demand From Garments and Accessories

Garment exports remain a structural anchor for the Bangladesh containerboard market, with Bangladesh’s readymade garments sector generating USD 36.2 billion in FY2023-24 and USD 26.8 billion in the first 7 months of FY2024-25, up 10.7% year over year.[1]United States Department of Agriculture Foreign Agricultural Service, “Cotton and Products Annual, Bangladesh,” USDA Foreign Agricultural Service, usda.gov Corrugated master cartons remain essential for those shipments, which gives local kraftliner and testliner demand a large and recurring volume base. Bangladesh’s accessories and packaging segment also reached USD 7.45 billion in export earnings in the last fiscal year, showing that packaging is now a meaningful export-linked activity rather than a minor supporting function. Buyer requirements are also becoming stricter, because overseas retailers increasingly want recycled-content verification or traceable fiber sourcing on export cartons. That change should keep shifting demand in the Bangladesh containerboard market toward certified mills that can meet documentation needs at scale.

Plastic Substitution Creating Incremental Demand for Paper-Based Packaging

Bangladesh generated 87,000 tonnes of single-use plastics annually, much of which accumulated as unmanaged urban and waterway waste.[2]Ministry of Environment, Forest and Climate Change, Bangladesh, “Gazette Notification on Single-Use Plastic Phase-Out in 17 Sectors,” Government of Bangladesh, tbsnews.net The government issued a gazette notification on August 27, 2024 to phase out single-use plastics across 17 sectors, after earlier policy action in June 2024, and bans on polythene bags in superstores and kitchen markets took effect from October 1, 2024 and November 1, 2024. Enforcement was uneven in the early phase, but the stated target of reducing single-use plastic use by 90% by 2026 still sends a clear medium-term demand signal to institutional buyers. That matters for the Bangladesh containerboard market, because food retail, hospitality, and parts of pharmaceuticals are likely to turn first to paper-based cartons where cost-effective biodegradable substitutes are still limited. The effect may build gradually, but it creates a policy-backed floor for paper packaging adoption in channels that were previously dominated by plastic formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported OCC and Pulp Cost Volatility | -1.2% | National, amplified in mills dependent on US and European OCC imports through Chittagong port | Short term (≤ 2 years) |

| Gas, Power, and Financing Cost Pressure | -1.0% | Dhaka industrial belt, with severe impact in Chattogram | Short term (≤ 2 years) |

| Domestic Overcapacity and Distressed Pricing | -0.8% | National, concentrated among mid-size mills outside the Dhaka-Chattogram corridor | Medium term (2-4 years) |

| Duty-Free Leakage Distorting Local Paper Competition | -0.5% | National, with the highest leakage through the Chittagong bonded warehouse channel | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imported OCC and Pulp Cost Volatility Compressing Mill Margins

Bangladesh’s paper sector remained dependent on imported raw materials for nearly 70% of its input needs, including OCC, mixed office waste, and pulp chemicals. That leaves mills in the Bangladesh containerboard market as price takers in recovered fiber markets where they have limited bargaining power. US OCC prices averaged USD 91 per tonne in February 2024 and then shifted sharply again, with US double-sorted OCC at USD 147-150 per tonne in January 2025 after Southeast Asian restocking. The Bureau of International Recycling also noted that Bangladesh still plays only a minor role in import OCC markets compared with larger regional buyers, which limits its ability to anchor supply on favorable terms. A weaker taka and tighter letters of credit then added another layer of pressure, which is why margin recovery in the Bangladesh containerboard market depends as much on calmer input markets as it does on volume growth.

Gas, Power, and Financing Costs Structurally Elevated

Bangladesh’s industrial gas shortfall reached 312 mmcfd in mid-2025, when industrial demand stood at 1,306 mmcfd and actual supply was only 994 mmcfd. Gas prices had already risen 179% in 2023, and a further 33% increase for new industries followed in 2024, while captive power costs climbed from BDT 31.50 to BDT 42 per unit. Paper mills then faced production cost increases of 20-30%, and the Bangladesh Paper Mills Association said repeated gas pressure drops were damaging equipment and causing batch losses. When mills slow or interrupt runs under those conditions, caliper uniformity and basis weight consistency often become harder to maintain. That weakens converter performance and gives imported board more room to compete in the Bangladesh containerboard market, especially when bonded warehouse channels already distort pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominance With a Quality Ceiling Approaching

Recycled fibers held 53.17% of the Bangladesh containerboard market share in 2025, which reflects the basic economics of a fiber-scarce country with limited domestic pulp resources. The Bangladesh containerboard industry has therefore been built around waste paper collection, sorting, and reprocessing rather than around virgin pulp integration. A more advanced layer of that model appeared in October 2024, when ANDRITZ commissioned 2 recycled fiber lines at Lipy Paper Mills’ Kanchpur facility to process 150 tonnes per day of local OCC and mixed office waste into premium testliner. That project showed that the recycled base of the Bangladesh containerboard market is not static, because mills are now investing in quality upgrades rather than relying only on low-cost furnish.

Recycled fiber is also the fastest-growing material segment, with a 6.21% CAGR expected through 2026-2031. That outlook reflects a push to close the local fiber loop more effectively and reduce exposure to imported inputs where possible. Virgin fibers still matter in the Bangladesh containerboard industry, because export-grade kraftliner and some food-contact applications need strength, cleanliness, and migration performance that current recycled furnish does not always deliver. Bangladesh’s draft Food Contact Materials regulation adds more pressure in that direction, because it introduces migration limits and certification requirements for paper and board used in food applications. As these requirements move into practice, the Bangladesh containerboard market is likely to separate more clearly between certified recycled grades and lower-value commodity output.

By Product Type: Kraftliners Lead While Flutings Gain Speed

Kraftliners captured 39.23% share of the Bangladesh containerboard market size in 2025, which kept them as the leading product category by value. Their position reflects the needs of garment exports and other demanding corrugated applications where burst strength and box compression remain critical. Bashundhara Paper Mills’ packaging paper range includes brown wrapper, liner paper, and high-strength packaging board, which makes it a domestic reference point for export-oriented corrugated supply. The company’s BDT 4,000 crore (USD 333 million) investment in a 2,000 TPD kraft-liner complex in Mirsarai, with Valmet contracts finalized in February 2026, signals that large players still expect the Bangladesh containerboard market to reward scale and quality over the longer term.

Testliners remain the mid-tier product for domestic food and consumer goods cartons, where cost and acceptable performance still drive most buying decisions. Flutings are expanding faster, with a 6.67% CAGR forecast through 2026-2031, because e-commerce fulfillment and retail-ready corrugated displays use more corrugating medium relative to outer liners. MAQ Paper Industries has operated since 1992 as a dedicated corrugating medium producer and remains a useful reference point in domestic fluting supply with 55 TPD capacity. Papertech also continued to invest in packaging-grade paper, with an AFT order in May 2025 for a new 250 TPD stock preparation system and Valmet’s first automation package for the Bangladesh site delivered in Q4 2025 to improve quality control and raw material efficiency.

By End-User Industry: Food and Beverage Commands the Largest Share While Consumer Goods Accelerates

Food and beverage held 34.67% of the Bangladesh containerboard market in 2025, which made it the largest end-user industry. That position comes from packaged foods, bottled beverages, and export-linked seafood shipments that all require dependable corrugated formats. Consumer goods is projected to be the fastest-growing end-user segment at 6.38% CAGR through 2026-2031, supported by modern retail penetration, personal care products, and electronics packaging needs. This change matters because the Bangladesh containerboard industry is moving toward thinner flutes and better liner quality in categories where print quality, fit, and handling performance all matter more than bulk tonnage.

Industrial end users remain a stable but slower-growth base, serving electrical components, ceramics, and steel product shipments that often need double-wall or triple-wall corrugated protection. Other end-user industries, including pharmaceuticals and personal care, are drawing converter investment toward short-run printed boxes and more traceable packaging inputs. That changes the demand mix inside the Bangladesh containerboard market, because consistency and compliance start to matter alongside volume. As a result, the Bangladesh containerboard industry is beginning to see premium demand appear first in applications where branding, regulatory checks, and controlled handling are most visible.

Geography Analysis

Dhaka and Chattogram divisions held nearly 70% of Bangladesh containerboard market share in 2025, which makes geography the clearest concentration point in the market. Dhaka’s dominance comes from its dense garment and processed-food manufacturing base across Narayanganj, Gazipur, Savar, and Manikganj, where converters can supply cartons with short lead times. The Narayanganj belt is especially important because it combines integrated mills with a wider recycled-board ecosystem, which supports both industrial buyers and smaller packaging needs. Chattogram plays a different but equally important role, because it anchors seafood and vegetable export packaging while also handling imported OCC and virgin pulp flows through the port. Gas disruptions in FY25 and FY26 showed how exposed the Chattogram side of the Bangladesh containerboard market remains to infrastructure shocks that affect drying operations, captive power, and mill scheduling.

Sylhet, Rajshahi, and Khulna are emerging as the next layer of converter expansion in the Bangladesh containerboard market. These cities offer lower industrial land costs and better proximity to regional demand than many congested sites around Dhaka. Mirsarai Economic Zone in northern Chattogram is also becoming a distinct cluster because it offers planned gas, power, and terminal infrastructure for large industrial projects. Bashundhara’s kraftliner investment in Mirsarai suggests that future capacity additions may increasingly shift away from the crowded Dhaka-Narayanganj corridor toward purpose-built industrial zones.

Regional positioning adds another layer to the geography story, because India’s containerboard sector is far larger by volume and has periodically affected Bangladeshi pricing through imported testliner and fluting. The Bangladesh Paper Mills Association warned that grade misclassification under bonded warehouse channels has allowed cheaper imports to undercut local producers. Vietnam remains a useful comparison because it built export-capable testliner production through large technology-led investments in paper machinery and process systems. Similar technology choices by Lipy Paper Mills and Bashundhara suggest that Bangladesh’s route to higher-quality production is technically credible, even if energy and financing conditions have slowed execution.[3]ANDRITZ AG, “First ANDRITZ Recycled Fiber Lines Supplied to Bangladesh Start Up,” ANDRITZ Newsroom, andritz.com Over the forecast period, mills located in planned industrial zones should hold a stronger position than facilities that remain tied to unstable urban-edge infrastructure.

Competitive Landscape

The Bangladesh containerboard market remained moderately concentrated at the integrated mill level in 2026, with the top 3 producers holding roughly 40% of industrial-grade liner and fluting capacity. The rest of the market stayed fragmented across many smaller mills that differ widely in quality, efficiency, and financial strength. This created an uneven competitive pattern in the Bangladesh containerboard market, because stronger firms were gaining share partly by surviving a difficult operating cycle rather than by expanding production smoothly. The Bangladesh Paper Mills Association said that more than 70 of the country’s 100-plus private paper mills had shut by early 2025, and only 10-15 were operating at reduced capacity. That means competitive pressure is still real, but it is increasingly filtered through financial resilience and operating discipline rather than through simple price rivalry.

Large-scale strategic moves are defining the upper tier of the Bangladesh containerboard market. Bashundhara moved ahead with its BDT 4,000 crore (USD 333 million) Mirsarai kraft-liner project, which remains the largest single committed containerboard capacity addition by a Bangladeshi private player.[4]Bashundhara Paper Mills PLC, “Nine Months Ended March 31, 2026 Financial Statement,” Dhaka Stock Exchange Disclosure, tbsnews.netLipy Paper Mills moved on the quality side, where ANDRITZ started up 2 recycled fiber lines in October 2024 to convert local recovered paper into premium testliner furnish. Papertech pursued a similar upgrading path through automation and stock preparation investments from Valmet and AFT, showing that quality-focused capacity expansion is continuing even in a stressed market.

The clearest white space in the Bangladesh containerboard market is still in food-contact-certified recycled board and coated white-top linerboard for premium consumer goods packaging. Those needs are still served mainly by imports, which leaves room for domestic first movers that can achieve reliable certification and consistent quality. Bangladesh’s draft Food Contact Materials regulation is important here, because it raises the compliance bar for packaging used in sensitive applications. Converters that invest in digital printing and short-run packaging formats are also changing what they ask from mills, because they need smoother surfaces, better traceability, and more predictable board behavior. As a result, competition in the Bangladesh containerboard market is moving gradually away from a pure price-per-tonne model and toward a narrower contest built around certification, reliability, and performance consistency.

Bangladesh Containerboard Industry Leaders

Bashundhara Paper Mills PLC

Meghna Group of Industries

AkijBashir Group

MAQ Paper Industries Limited

Papertech Industries Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bashundhara Paper Mills PLC finalized Valmet contracts for a BDT 4,000 crore (USD 333 million) kraft-liner complex in the Mirsarai Special Economic Zone, targeting a 2,000 TPD design capacity with full-line completion scheduled for late 2027. The project is the largest single committed containerboard investment by a Bangladeshi private entity and positions the company for export-oriented liner supply once operational.

- December 2025: Valmet delivered its first automation package to Papertech Industries Co., Ltd.'s Bangladesh production site, ordered in Q2 2025, designed to reduce quality variability, optimize raw material usage, and improve operational efficiency through advanced process control. The deployment marked Valmet's inaugural automation technology installation in the Bangladesh paper sector.

- May 2025: Aikawa Fiber Technologies (AFT) received an order from Papertech Industries Co., Ltd. for a complete stock preparation system for a new 250 TPD production line at Papertech's Bangladesh mill, covering full scope from pulper to approach flow and incorporating energy-efficient refining and screening. Startup is targeted for 2026 and is expected to expand Papertech's capacity to serve growing domestic demand for packaging-grade paper.

Bangladesh Containerboard Market Report Scope

The Bangladesh Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Bangladesh Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Bangladesh containerboard market size in 2026 and what is the growth outlook?

The Bangladesh containerboard market was valued at USD 1.48 billion in 2026 and is projected to reach USD 1.95 billion by 2031, growing at a 5.67% CAGR over 2026-2031.

Which material segment leads demand in Bangladesh containerboard?

Recycled fibers led demand with a 53.17% share in 2025, reflecting Bangladesh’s strong dependence on collected waste paper and limited domestic pulp resources.

Which product type is growing the fastest in containerboard demand?

Flutings are forecast to grow the fastest at a 6.67% CAGR through 2031, supported by e-commerce packaging, retail-ready displays, and greater use of corrugating medium.

Which end-user group contributes the most to demand for containerboard in Bangladesh?

Food and beverage was the largest end-user segment with a 34.67% share in 2025, supported by processed foods, beverage cartons, and moisture-resistant export packaging needs.

What are the main risks affecting paper mills and converters in Bangladesh?

The key risks are imported OCC and pulp cost volatility, gas and power shortages, financing pressure, and price distortion from bonded warehouse leakage.

Which company strategies are shaping competition in Bangladesh containerboard?

The main competitive moves include Bashundhara’s large kraft-liner expansion in Mirsarai, Lipy Paper Mills’ recycled fiber upgrade with ANDRITZ, and Papertech’s automation and stock preparation investments with Valmet and AFT.

Page last updated on: