Turkey Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.24 Billion |

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 2.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Containerboard Market Analysis by Mordor Intelligence

The Turkey Containerboard Market size is projected to be USD 1.24 billion in 2025, USD 1.27 billion in 2026, and reach USD 1.45 billion by 2031, growing at a CAGR of 2.69% from 2026 to 2031.

The Turkey containerboard market in 2026 is supported by steady demand from e-commerce logistics, food processing, and consumer goods distribution. Turkey also benefits from its role as both a major producer and a net exporter to the Middle East and North Africa, which gives the market more resilience than domestic demand alone would suggest. The current phase is more selective because new mill capacity is rising faster than near-term end-user demand, which keeps pricing under pressure even as long-run supply strength improves. Large integrated producers are using scale, product mix, and logistics reach to strengthen their position, while smaller participants face a tighter margin environment. The baseline outlook remains steady because e-commerce growth, food packaging demand, and paper-based substitution continue to support the Turkey containerboard market, while manufacturing caution and input cost volatility keep expansion measured.

Key Report Takeaways

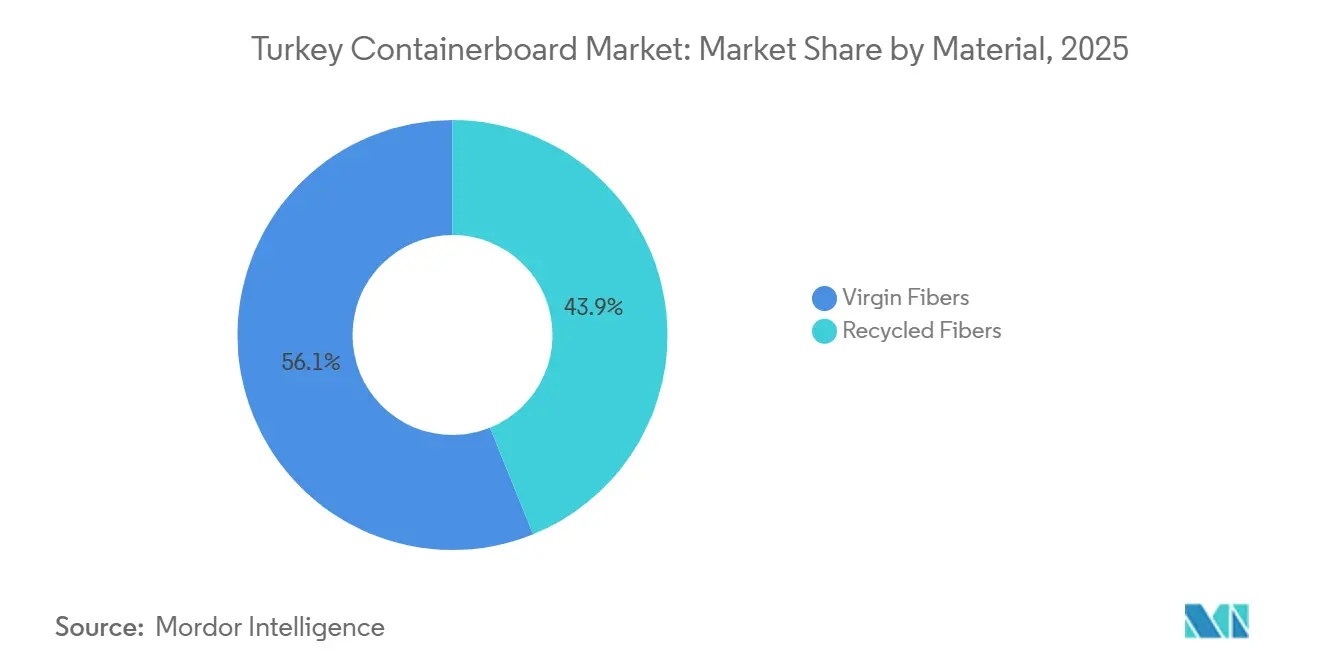

- By material, virgin fibers held 56.12% of the Turkey containerboard market in 2025, while recycled fibers are projected to expand at a 2.92% CAGR through 2031.

- By product type, testliners accounted for 43.23% share of the Turkey containerboard market in 2025, while kraftliners are forecast to grow at a 3.41% CAGR through 2031.

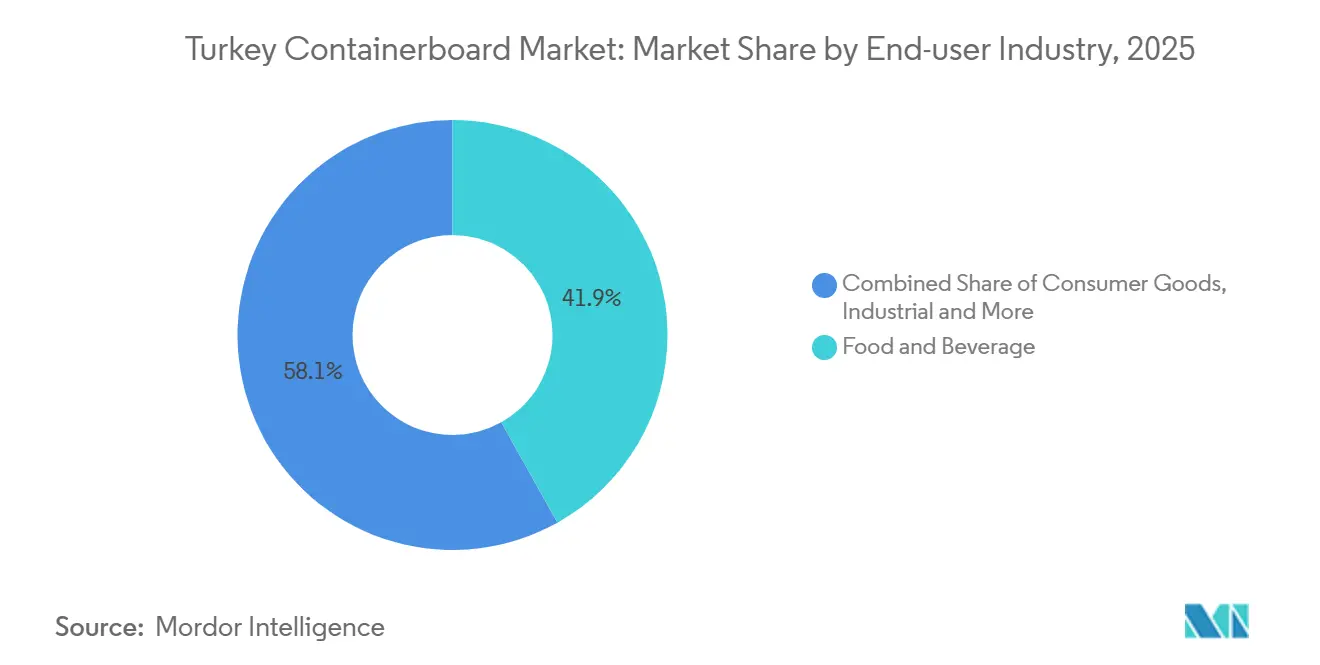

- By end-user industry, food and beverage held 41.89% of the Turkey containerboard market in 2025, while consumer goods is projected to advance at a 3.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Turkey Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth In E-Commerce And Quick Commerce Box Throughput | +0.80% | National, with concentration in Istanbul, Izmir, and Ankara metropolitan corridors | Short term (≤ 2 years) |

| Food And Beverage Packaging Demand Resilience | +0.55% | National, with highest intensity in Marmara, Aegean, and Central Anatolia agri-processing hubs | Medium term (2-4 years) |

| Paper-Based Packaging Substitution In Transit Applications | +0.45% | National, with early gains driven by e-commerce fulfillment centers near Istanbul and Izmir | Medium term (2-4 years) |

| Domestic Capacity Additions Improving Local Availability | +0.35% | National, Zonguldak, Söke, Konya, and Çorlu production corridors | Long term (≥ 4 years) |

| Higher Recovered Fiber Collection Under Zero Waste | +0.25% | National, with deposit return system presently operational across 53 provinces | Long term (≥ 4 years) |

| Safeguard Measures Supporting Local Sourcing | +0.20% | National, with strongest commercial impact in regions dependent on European and Asian CCM imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth In E-Commerce And Quick Commerce Box Throughput

Turkey's parcel economy has moved to a scale where box usage is a structural driver for the Turkey containerboard market. E-commerce volume reached TRY 4.57 trillion, USD 115.43 billion, in 2025, up 52.2% year over year, with 5.94 billion transactions recorded.[1]Ministry of Trade of the Republic of Türkiye, “Outlook of E-Commerce in Türkiye: 2025 Report,” WORLDEF, worldef.com Quick commerce reached TRY 388.7 billion in 2025, up 55.6% from 2024, and food accounted for 69.5% of that volume. Each direct-to-consumer order uses a dedicated shipping pack, which raises packaging intensity versus store replenishment. Delivery windows also fell to 42.2 hours in 2025 from 46.2 hours 2 years earlier, which pushed fulfillment centers toward more standardized box formats and higher board use per shipment.

Food And Beverage Packaging Demand Resilience

The food and beverage base gives the Turkey containerboard market its most stable demand floor. The segment held 41.89% share in 2025, and demand is supported by poultry, dairy, grocery, and beverage supply chains that need regular secondary packaging. Corrugated trays and wraps are also used more often in temperature-controlled transport, which keeps containerboard demand tied to essential goods movement. Turkey's August 2025 roadmap on single-use plastics identified food packaging and beverage containers as priority areas for restriction, which makes paper-based secondary formats the easier compliance route for brands. That policy direction matters because it turns paper substitution from a brand choice into a packaging decision with a clearer time path.

Paper-Based Packaging Substitution In Transit Applications

The shift from plastic transit fillers toward corrugated and kraft-based protection is widening the addressable base for the Turkey containerboard market. The change is moving faster in e-commerce because branded paper packs serve both protection and presentation needs. Turkey's August 2025 plastics roadmap encouraged a move away from selected single-use plastic food and beverage formats and toward reusable or paper alternatives. That creates a wider opening for corrugated inserts, paper cushioning, and lighter transit formats across retail and food service chains. Mondi Turkey also showed that custom corrugated redesign can lower logistics costs by 10% for industrial shipments, which supports paper-based transit packaging beyond consumer parcels.

Domestic Capacity Additions Improving Local Availability

Capacity additions changed the supply balance of the Turkey containerboard market during 2025 and carried their largest effects into 2026. Modern Karton's PM6 at Zonguldak added 640,000 metric tons of recycled containerboard capacity after an investment of EUR 540 million, USD 583.2 million, and lifted the company's total capacity to close to 2 million metric tons per year. Barem Ambalaj's new Konya mill started shipping commercial output on December 31, 2025, and it reached 60% utilization by March 2026, with recycled testliner and fluting capacity estimated at 260,000 to 300,000 metric tons per year after spending more than EUR 100 million, USD 108 million. Kipaş Kağıt's PM3 at Söke added another 650,000 metric tons of annual capacity and widened domestic availability across kraftliner, white-top testliner, testliner, and fluting grades. The effect is not immediate volume growth alone, because it also improves local grade availability, delivery flexibility, and supply depth across the Turkey containerboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak Industrial Orders And Tight Credit Conditions | -0.55% | National, most acute in export-oriented industrial clusters in Bursa, Kayseri, and Gaziantep | Short term (≤ 2 years) |

| Manufacturing Cost Inflation And Margin Compression | -0.45% | National, energy-intensive paper mills in Zonguldak, Çorlu, and Söke face highest exposure | Medium term (2-4 years) |

| Imported Grade Access Tightened By Safeguards And Quotas | -0.30% | National, most significant for converters in Istanbul and Izmir reliant on premium imported board | Short term (≤ 2 years) |

| Recycled-Heavy Supply Mix Limiting Premium Grade Flexibility | -0.20% | National, with spillover into export markets requiring virgin-fiber performance boards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak Industrial Orders And Tight Credit Conditions

Weak factory orders remain a near-term brake on the Turkey containerboard market. Turkish manufacturing stayed below the 50 PMI threshold for 22 straight months through early 2026, with readings such as 47.3 in April 2025 and 49.3 in February 2026. Lower factory output cuts both inbound packaging for components and outbound boxes for finished goods. Credit conditions also stayed tight, with weighted average commercial loan rates near 46%-47% through late 2025, which limited working capital and equipment plans for mid-sized box converters. That pressure falls hardest on the converter tier that usually adds new SKUs and niche volumes faster than large integrated mills.

Manufacturing Cost Inflation And Margin Compression

Cost inflation remains a major restraint on the Turkey containerboard market because paper mills carry high energy exposure. EMRA raised industrial electricity prices by 10% in April 2025, and BOTAŞ raised industrial natural gas prices by 20% from April 4, 2025. The same period also saw annual producer price inflation at 23.13% in May 2025 and a manufacturing sector price index that rose 30.6% year over year in April 2025. When mills cannot pass those increases through quickly, margins tighten and smaller producers delay maintenance, upgrades, and product development. The result is a Turkey containerboard market that leans more heavily toward larger integrated players with stronger financing and energy management options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Gains Ground While Virgin Fiber Keeps The Lead

Virgin fibers held 56.12% of the Turkey containerboard market share in 2025, which kept them in the lead across the material mix. That position came from the long-standing use of virgin-fiber grades in export corrugated and in food packaging that needs dependable strength and print quality. In Turkey, this preference is tied less to simple cost and more to performance because exporters to the European Union and Gulf markets face tighter specifications. Those requirements are harder to meet consistently with recycled-content board, especially in lighter grammages below 120 g/m².

Recycled fibers are still the fastest-growing material segment, with the Turkey containerboard market size for recycled fibers projected to advance at a 2.92% CAGR through 2031. Turkey's Zero Waste Project lifted the national recovery rate from 13% in 2017 to 37.53% in 2025, and 36.1 million tons of paper and cardboard had been recovered since launch.[2]Ministry of Environment, Urbanization and Climate Change, “Zero Waste Project Recovery Rate Reaches 37.53% in 2025,” Daily Sabah, dailysabah.com The Deposit Management System was active across 53 provinces in 2025, which improved post-consumer fiber collection and increased the quality and volume of available feedstock. Modern Karton's fully recycled PM6 shows how large-scale capacity and green-linked financing are narrowing the quality gap, even though virgin fibers still hold the structural lead in the Turkey containerboard market.

By Product Type: Testliners Lead Volumes While Kraftliners Grow Faster

Testliners accounted for 43.23% of the Turkey containerboard market size in 2025, which made them the volume backbone of domestic corrugated output. Their lead reflects broad use across appliances, textiles, and processed foods where cost control matters more than premium surface finish. Turkish converters also rely on testliners for domestic distribution because burst strength needs are moderate in many standard shipping cases. This keeps recycled-content grades at the center of day-to-day box production even as premium demand grows at the top end.

Kraftliners are the fastest-growing product type in the Turkey containerboard market, with a 3.41% CAGR through 2031. Their growth is tied to exporters that need stronger box performance and better printability for cross-border shipments to European Union and Gulf destinations. Kipaş Kağıt's Söke PM3 was built around that opportunity because the machine can produce kraftliner, white-top testliner, fluting, and recycled grades across a broad grammage range. Fluting remains essential to every corrugated structure, but its growth is more limited because lighter box designs are reducing board weight without removing the need for structural strength.

By End-User Industry: Food And Beverage Stays Largest While Consumer Goods Expands Faster

Food and beverage held 41.89% of the Turkey containerboard market share in 2025, which kept it as the largest end-user base. The segment stays steady because refrigerated proteins, dairy, beverages, and ambient grocery all need dependable secondary corrugated packaging through the year. Those product flows are less exposed to economic swings than durable goods, so they give the Turkey containerboard market a consistent shipment floor. The market also benefits because food producers moving into export channels often need higher packaging consistency and better compliance records.

Consumer goods is the fastest-growing end-user segment, with the Turkey containerboard market size for this group projected to rise at a 3.12% CAGR through 2031. E-commerce has increased secondary packaging demand across FMCG, personal care, household products, and small appliances, where pick-and-pack activity uses more boxes per unit sold. Pressure to replace plastic-based secondary formats should reinforce this shift as retail and brand owners adjust packaging choices under the policy direction introduced in 2025. Industrial demand remains under pressure from weak manufacturing output, while agriculture and pharmaceuticals still offer room for coated kraftliners and cold-chain applications that are not yet fully developed in Turkey.

Geography Analysis

Turkey's containerboard production remained concentrated in a small set of industrial corridors, even as new mills broadened the map in 2025 and 2026. The Marmara and Thrace corridor, anchored by Çorlu and linked to Zonguldak on the Black Sea coast, held the largest installed production base in the Turkey containerboard market because of Modern Karton's scale. Modern Karton's PM6 in Zonguldak lifted site-linked capacity close to 2 million metric tons per year after the 2025 startup. The Black Sea location also benefits from port access for recovered fiber and proximity to power generation assets, which matters in an energy-intensive business. Aquakraft's Ferizli mill in Sakarya added another node near Istanbul after first commercial output in September 2025 and a later rebuild plan targeting a 60% capacity increase by Q4 2027.[3]Voith GmbH and Co. KGaA, “Voith to Deliver Comprehensive Rebuild of Paper Machine and Stock Preparation for Aquakraft's PM 2 Containerboard Mill in Turkey,” PulpaPaperNews, pulpapernews.com

The Aegean cluster around Söke became another major supply point in the Turkey containerboard market after Kipaş Kağıt expanded combined PM2 and PM3 capacity to nearly 1.4 million metric tons per year. That position supports both domestic converters and export flows into North Africa and the Levant because western Turkey offers efficient outbound logistics. Central Anatolia also moved up the map when Barem Ambalaj started its Konya Ereğli mill, which reduced the freight disadvantage inland food manufacturers once faced when sourcing from coastal mills. The wider rollout of the Deposit Management System across 53 provinces should gradually balance recovered fiber collection beyond coastal and Marmara-heavy networks.

Demand consumption follows a different pattern because Istanbul and its wider metro area absorb the largest share of converted containerboard through logistics, retail, and converting activity in the Turkey containerboard market. Postal and cargo data showed that inter-city movements remained heavily concentrated in this corridor during H2 2025, which supported sustained box throughput around the country's largest delivery hub. Izmir, Ankara, Bursa, and Gaziantep form the next tier of demand, with mixes that range from export food and textiles to consumer goods, chemicals, and industrial packaging. Turkey's regional export role also shapes domestic pricing because safeguard duties on imported corrugated case material and the January 2026 safeguard investigation show that policy is being used to protect mill utilization while port cargo volumes remain high enough to support export shipments.

Competitive Landscape

The Turkey containerboard market was moderately concentrated at the production level in 2026, but it stayed fragmented in converting and distribution. Modern Karton and Kipaş Kağıt held the strongest position in domestic recycled containerboard supply after the 2024 and 2025 expansion cycle. Their scale stands in contrast to a converter base made up of many small and mid-sized corrugated box companies that compete mostly on lead time, geography, and customer ties. This structure gives integrated mills more leverage when demand is firm, but it also gives local converters room to negotiate when supply is long. That balance is especially important now because the Turkey containerboard market entered 2026 with capacity additions that exceed near-term demand growth.

Modern Karton reset the regional scale benchmark when it commissioned the 640,000-metric-ton PM6 line in Zonguldak, which pushed total capacity close to 2 million metric tons per year. Kipaş Kağıt reinforced its position through the 650,000-metric-ton PM3 at Söke, which widened its reach across premium and mainstream grades. Barem Ambalaj added a new inland production platform in Konya, which gave it a different freight profile and direct access to Central Anatolia customers. Aquakraft then followed with a commercial start in 2025 and a 2026 rebuild contract that targets higher output and a broader mix of corrugating medium, testliner, high performance testliner, and white top liner.

International producers also keep a place in the Turkey containerboard market because premium-grade positions are less exposed to recycled testliner oversupply. Hamburger Containerboard announced a EUR 100 per ton price increase for brown recycled containerboard from February 1, 2026, which shows how mills are still trying to recover energy and fiber cost pressure.[4]W. Hamburger GmbH, “Hamburger Containerboard Announces Price Increase for Corrugated Base Paper,” Paper World, paper-world.com Mondi Turkey has competed through packaging design and value engineering, including a case where custom corrugated redesign cut logistics costs by 10% for Argesim Teknoloji. If Hamburger's Kütahya greenfield plan moves ahead, premium-grade competition would rise further in a Turkey containerboard market that is already well supplied.

Turkey Containerboard Industry Leaders

Modern Karton Sanayi ve Ticaret A.Ş.

Kipaş Kağıt Sanayi İşletmeleri A.Ş.

Hamburger Containerboard (Turkey)

KÜTAHYA ENTEGRE KAĞIT SAN. VE TİCARET A.Ş.

Parteks Kağıt Endüstrisi A.Ş.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Aquakraft Kağıt ve Ambalaj and Voith signed a contract for a comprehensive rebuild of PM2 at the Ferizli mill (Sakarya, Turkey), targeting a 60% capacity increase and a broader grade portfolio encompassing Corrugating Medium, Testliner, High Performance Testliner, and White Top Liner in grammages of 80 to 200 g/m² at speeds up to 1,200 m/min. Startup is scheduled for Q4 2027, making this the most significant forward capacity commitment currently visible in the Turkish containerboard sector.

- March 2026: Barem Ambalaj's new containerboard mill in the Konya Ereğli Organized Industrial Zone reached approximately 60% capacity utilization, with output progressively expanding across different formats and quality specifications. Built at a cost exceeding EUR 100 million and designed for recycled testliner and fluting grades, the facility's ramp-up adds an estimated 260,000-300,000 metric tons per year to Turkey's domestic recycled containerboard supply.

- January 2026: Hamburger Containerboard (part of the Prinzhorn Group) announced a EUR 100 per ton price increase for brown recycled containerboard, effective February 1, 2026, reflecting persistent cost pressure from energy, fiber, and currency exposure that had compressed operating margins across the European and Turkish recycled containerboard supply chain.

Turkey Containerboard Market Report Scope

The Turkey Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Turkey Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Turkey containerboard market and where is it headed by 2031?

The Turkey containerboard market was valued at USD 1.24 billion in 2025, reached USD 1.27 billion in 2026, and is projected to reach USD 1.45 billion by 2031 at a 2.69% CAGR.

What is driving box demand in Turkey the most?

E-commerce and quick commerce are major demand drivers, with 2025 e-commerce volume at USD 115.43 billion and 5.94 billion transactions, which increased shipping pack usage.

Which material category is growing fastest in Turkey containerboard?

Recycled fibers are the fastest-growing material segment, with a forecast CAGR of 2.92% through 2031, supported by wider fiber collection under the Zero Waste framework.

Which product type leads the market and which one is growing fastest?

Testliners led with 43.23% share in 2025, while kraftliners are forecast to grow the fastest at a 3.41% CAGR because export shipments need better strength and printability.

Which end-user segment remains the most important for demand stability?

Food and beverage remains the largest end-user segment with 41.89% share in 2025, giving demand a steady base through grocery, dairy, protein, and beverage supply chains.

Why is pricing pressure still a concern even though demand is rising?

New capacity from Modern Karton, Kipaş Kağıt, and Barem Ambalaj has increased supply faster than near-term demand, while energy and fiber costs continue to pressure margins.

Page last updated on: