Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

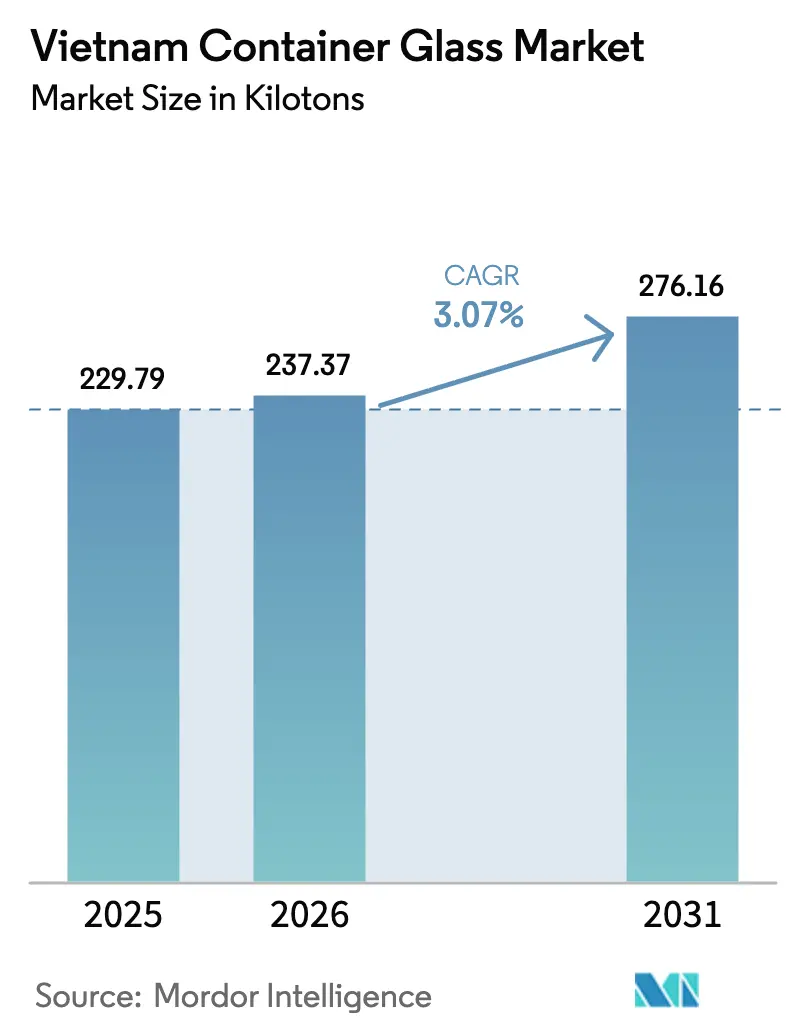

| Base Year Market Size (2025) | 229.79 kilotons |

| Market Volume (2026) | 237.37 kilotons |

| Market Volume (2031) | 276.16 kilotons |

| Growth Rate (2026 - 2031) | 3.07% CAGR |

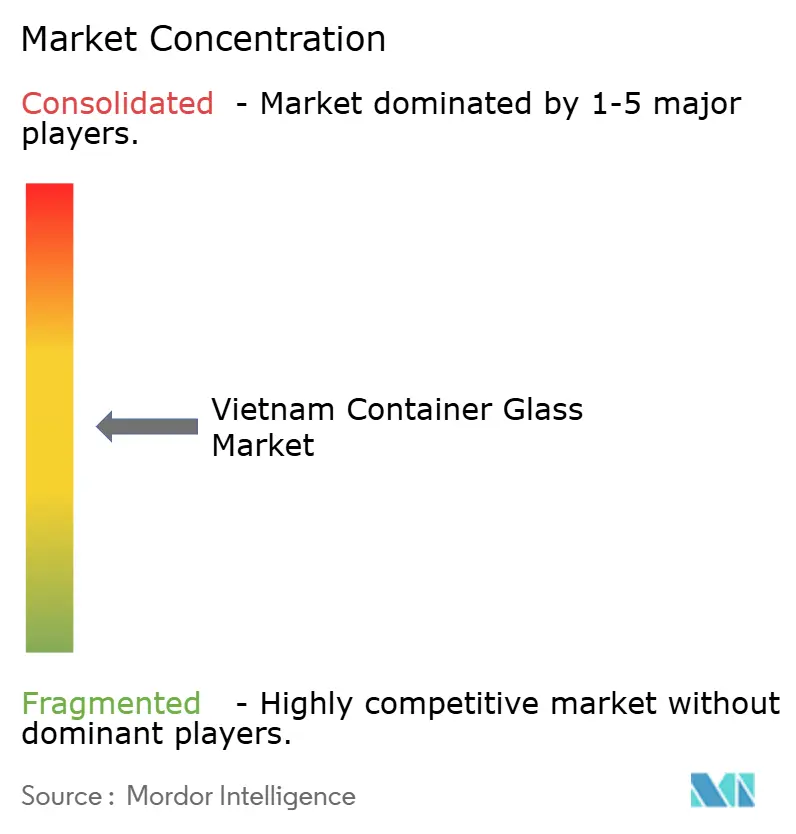

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Container Glass Market Analysis by Mordor Intelligence

The Vietnam container glass market size was valued at 229.79 kilotons in 2025 and estimated to grow from 237.37 kilotons in 2026 to reach 276.15 kilotons by 2031, at a CAGR of 3.07% during the forecast period (2026-2031). Strong demand from export-oriented food, beverage, pharmaceutical, and cosmetics clusters continues to underpin baseline growth even as single-use plastic restrictions accelerate substrate substitution toward glass. Foreign direct investment is supporting furnace upgrades that improve energy efficiency, reduce weight, and enhance decorative capabilities, allowing local suppliers to target higher-margin premium segments. At the same time, Extended Producer Responsibility rules are nudging brand owners to choose infinitely recyclable containers that lower scope 3 emissions. Capacity concentration among three domestic producers brings pricing discipline yet heightens the risk of supply disruption when energy prices spike or cullet access tightens.

Key Report Takeaways

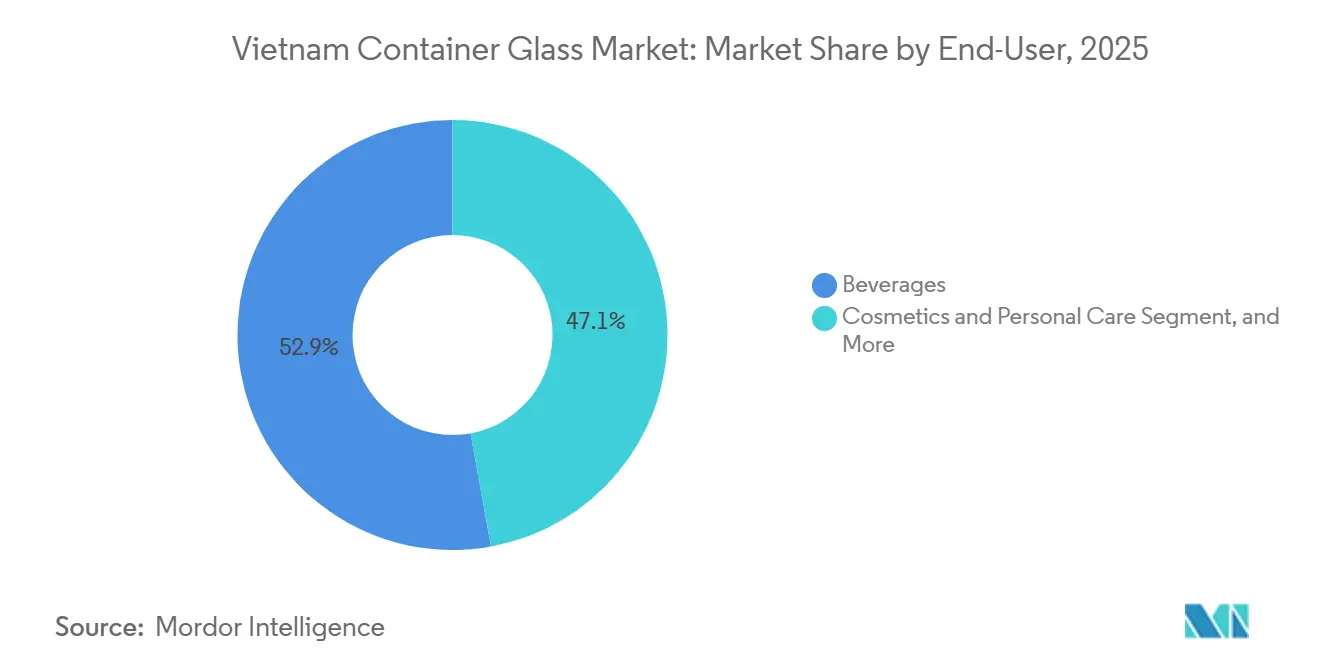

- By end-user, beverages commanded 52.87% of Vietnam’s container glass market share in 2025, while cosmetics and personal care is forecast to advance at a 4.09% CAGR through 2031.

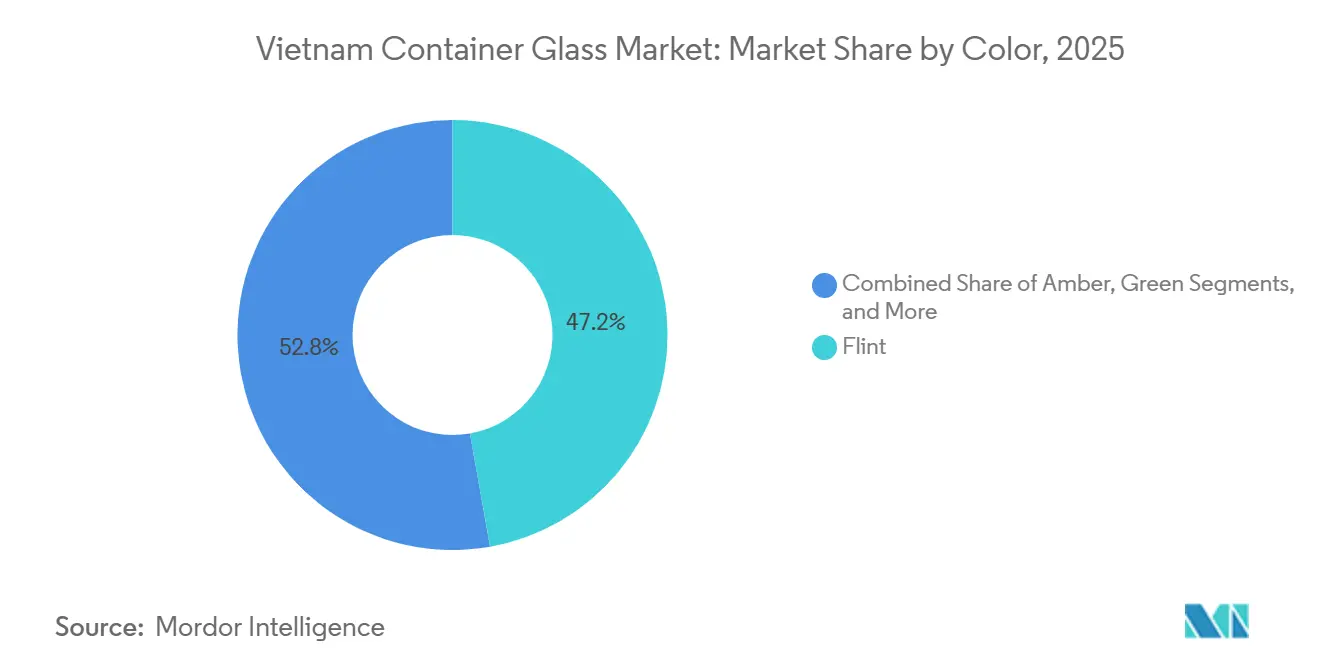

- By color, flint glass led with a 47.21% Vietnam container glass market share in 2025, whereas amber glass is projected to expand at a 3.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ESG-Driven Export Packaging Shift | +0.6% | Southern export processing zones and nationwide exporters | Medium term (2-4 years) |

| FDI-Driven Furnace Upgrades and Capacity Additions | +0.5% | Northern and Southern industrial clusters | Long term (≥ 4 years) |

| Government Push Against Single-Use Plastics | +0.5% | Coastal tourism zones, supermarkets, hotels | Short term (≤ 2 years) |

| Surging Alcoholic Beverage Output | +0.7% | Breweries concentrated in Southern provinces | Short term (≤ 2 years) |

| Pharmaceutical Manufacturing Expansion | +0.4% | Emerging pharma hubs in Binh Duong, HCMC, Thu Dau Mot, Hanoi, Phu Yen | Medium term (2-4 years) |

| Booming Cosmetics and Personal Care Sector | +0.3% | Major urban centers with strong e-commerce penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

ESG-Driven Export Packaging Shift

Export-focused processors are under mounting pressure from European and North American buyers to demonstrate packaging recyclability, as the EU’s Carbon Border Adjustment Mechanism signals future expansion to consumer sectors. Glass offers infinite recyclability, allows higher cullet content, and lowers scope 3 emissions compared with multilayer plastics. Vietnam’s portfolio of 17 free trade agreements strengthens the incentive, as preferential tariffs increasingly hinge on demonstrable environmental compliance. Exporters of premium sauces, organic foods, and craft beverages, therefore, specify glass to meet both regulatory and brand storytelling requirements. Demand is further reinforced by sustainability labeling in overseas retail channels, where a switch to glass can avoid costly repacking at destination markets. Collectively, these factors boost long-run volume visibility for domestic furnaces upgrading to narrow-neck press-and-blow lines to supply lightweight, high-clarity bottles.

FDI-Driven Furnace Upgrades and Capacity Additions

Manufacturing FDI surpassed USD 20 billion in 2024, bringing electronics, pharma, and food processors that expect just-in-time container supply. Vietnam Glass added a fourth line featuring narrow-neck press-and-blow technology to reduce weight by up to 10% and lower energy use. The government’s Investment Support Fund offsets 20-30% of R and D spending and 0.5% of fixed-asset cost for large projects, enabling domestic players to install modular furnaces that can run higher cullet ratios. New capacity aligns with regional clustering: Hai Phong for export seaports, Ba Ria-Vung Tau for brewery and food complexes, and Binh Duong for pharmaceuticals. These brown- and greenfield programs raise effective throughput and improve responsiveness to shorter product launch cycles in beverage and cosmetics categories.

Government Push Against Single-Use Plastics

Decree 08/2022/ND-CP bans thin non-degradable plastic bags from January 2026 and all single-use plastic items by December 2030, except those earning the Vietnam Green Label. Provinces must restrict single-use plastic sales in supermarkets and tourist zones starting in 2025, and field surveys show that plastic accounts for 62% of marine litter.[1]World Bank Group, “Toward a National Single-use Plastics Roadmap in Vietnam,” documents1.worldbank.org Replacement demand centers on reusable glass jars and bottles for sauces, condiments, hotel amenities, and refill stations. Operators that invest in deposit-return and in-house washing facilities gain first-mover access to institutional buyers keen to advertise circularity credentials. In parallel, the Extended Producer Responsibility framework enforces a 15% recycling rate for glass packaging beginning in 2024, escalating every three years, effectively making cullet infrastructure a competitive lever for large producers.

Surging Alcoholic Beverage Output

Beer consumption is forecast to grow from 4.23 billion liters in 2023 to 6.41 billion liters by 2028 at a 10.6% CAGR, cementing Vietnam as Asia’s fastest-expanding major beer market.[2] Agriculture and Agri-Food Canada, “Sector Trend Analysis – Wine, Beer, and Spirits in Vietnam,” agriculture.canada.ca Premium lager volume rose 10.9% annually between 2019 and 2023, and on-trade venues favor returnable glass for brand image and chilled-serve rituals. Heineken Vietnam and Carlsberg, which collectively supply about 90% of national beer output, maintain bottle pool logistics that reward consistent bottle shape and weight. Craft brewers scaling tap-room formats also choose amber glass to protect hop aromas, further lifting unit demand. Because breweries cluster near ports and industrial zones, they enable back-hauling of cullet, reducing inbound raw material costs for glass makers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| rPET Bottle Substitution Pressure | -0.5% | Mass-market beverages and low-margin food segments | Medium term (2-4 years) |

| Electricity Cost Inflation and Grid Instability | -0.4% | Entire grid, acute in Northern provinces during summer | Short term (≤ 2 years) |

| Weak Cullet Collection Infrastructure | -0.3% | Rural and peri-urban areas | Long term (≥ 4 years) |

| Logistics and Breakage Challenges | -0.2% | Mountainous North and Mekong Delta | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

rPET Bottle Substitution Pressure

Food-grade rPET capacity quadrupled in 2023 as global brands invested in domestic recycling plants and began shifting carbonated soft drinks and bottled water to lighter, cheaper bottles.[3]FiinGroup, “Vietnam PET Recycling,” fiingroup.vn A 500 milliliter PET bottle weighs roughly 25 grams versus 200-250 grams for the glass equivalent, slashing logistics costs by up to 80% and reducing breakage. Collection-for-recycling rates have reached 25% and are projected to keep climbing under Extended Producer Responsibility targets. As mainstream juices, teas, and soft drinks migrate, baseline glass volume loses momentum in high-velocity segments, compelling container producers to focus on premium beverages and proprietary shapes that deter competitors' bottle lightweighting.

Electricity Cost Inflation and Grid Instability

Furnace fuel spends can represent 20% of total cost, and recent Northern brownouts forced several float glass lines to pause for months, signaling similar vulnerability for container operations.[4]VnEconomy, “Ngăn chặn hàng kém chất lượng, gỡ khó cho sản xuất kính trong nước,” vneconomy.vn Power Development Plan 8 aims to diversify into renewables, yet interim reliance on coal and gas exposes glass makers to volatile tariffs and curtailment risk. Unplanned shutdowns shorten furnace campaign life and raise maintenance cost, while diesel backup raises marginal emissions, challenging ESG claims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Sustain Volume, Cosmetics Accelerate Margin

Beverages supplied 52.87% of the Vietnam container glass market in 2025, a lead reinforced by 4.23 billion liters of beer demand that is expanding at double-digit rates. The segment accounts for the largest share of Vietnam's container glass market and maintains high bottle-turn velocity under established deposit-return systems. Spirits and premium wines also drive demand for flint bottles, leveraging clarity for shelf appeal. Non-alcoholic drinks, however, are pivoting to rPET, capping glass gains in mass channels.

Cosmetics and personal care, though smaller in tonnage, is forecast to outpace headline growth with a 4.09% CAGR to 2031 as 23.2 million additional middle-income consumers join urban markets by 2030. Brands deploy heavy, intricately decorated bottles to convey luxury, raising average revenue per ton and offsetting lower shipment volume. Pharmaceuticals presently represent 12% of demand but are primed for share expansion once more domestic plants secure EU-GMP certification, requiring ISO 15378 vials and ampoules. Food and perfumery continue to provide diversified fill volumes that steady furnace utilization when beverage seasonality dips.

By Color: Flint Retains Lead, Amber Climbs

Flint glass held a 47.21% Vietnam container glass market share in 2025, since premium liquor, cosmetics, serums, and specialty foods prefer transparent packaging for ingredient visibility. Abundant high-purity silica sand along Vietnam’s central coast ensures cost-effective flint production. Amber glass, on the other hand, is projected to post the fastest growth at a 3.84% CAGR, driven by craft beer branding and pharmaceutical light-blocking requirements.

Green bottles maintain stable deployment in mainstream lagers and select wines, reinforcing returnable systems that dominate off-trade channels. Niche tints such as cobalt blue or frosted variants cater to limited-edition spirits and boutique skincare launches, adding decorative revenue streams. Color choice, therefore, balances functional requirements, raw material availability, and branding cues that help producers secure longer contracts and reduce price sensitivity.

Competitive Landscape

The Vietnam container glass market is moderately consolidated, with O-I BJC Vietnam Glass, San Miguel Yamamura Hai Phong Glass, and Go Vap Glass covering roughly 80% of volume. Scale affords bargaining power over soda ash suppliers and secures long-term contracts with brewers that jointly control 90% of beer output. Those anchor clients prize applied ceramic labeling and bottle-pool standardization, areas where O-I BJC’s investment in narrow-neck press-and-blow and ACL lines provides an edge.

San Miguel emphasizes amber lines tailored to craft beer and pharma, aligning with the fastest-growing color segments. Go Vap fills regional short runs and performs contract filling services for cosmetics start-ups, leveraging proximity to Ho Chi Minh City’s e-commerce merchants. Import competition from Thailand and China remains a volume buffer but is sensitive to freight rates and anti-dumping scrutiny.

Circularity is an emerging battleground. Pro Vietnam Packaging Recycling JSC collected 64,000 tonnes of packaging in 2024, while Duy Tan Recycling processes 200 tonnes daily, supplying cullet that lowers furnace energy demand by 2-3% per 10 percentage-point cullet addition. Producers engaged in such partnerships score better under multinational buyers’ ESG audits, locking in longer supply contracts even when spot prices swing.

Vietnam Container Glass Industry Leaders

O-I BJC Vietnam Glass Co.

San Miguel Yamamura Phu Tho Packaging Co., Ltd.

Saverglass SAS

Go Vap Glass

Ardagh Group S.A.

- *Disclaimer: Major Players sorted in no particular order

Geography Analysis

Production and consumption are concentrated in two industrial corridors. The Southern cluster, anchored by O-I BJC’s Ba Ria-Vung Tau plant and Go Vap Glass near Ho Chi Minh City, services export breweries, food processors, and cosmetics fillers located close to Cai Mep and Cat Lai deep-water ports. Efficient back-haul of cullet and soda-ash imports keeps landed cost competitive.

In the North, San Miguel Yamamura Hai Phong Glass operates near Hai Phong port, supplying demand in Hanoi’s metropolitan area and in Bac Ninh’s electronics and pharma hubs. Port efficiency ranks high on the World Bank CPPI, shortening transit for inbound colorants and outbound filled bottles. Northern electricity constraints, however, increase the risk of furnace downtime, prompting discussions of on-site solar plus storage options.

Central and Mekong Delta provinces are underpenetrated yet represent white-space. Planned expressways and a USD 14.1 billion seaport masterplan through 2030 will cut freight expense but route integrity challenges, especially in mountainous zones, sustain higher breakage ratios that favor producers able to supply lightweight, sturdier designs. As logistics improve, incremental demand from seafood processors and agri-exporters is likely to accrue to nearby furnaces, nudging regional diversification.

Recent Industry Developments

- January 2026: Vietnam’s Ministry of Natural Resources and Environment began enforcing QCVN 65:2024/BTNMT, capping non-glass contaminants in imported cullet at 2% and requiring pre-shipment conformity checks.

- August 2025: Tetra Pak doubled capacity at its Binh Duong aseptic carton plant with USD 110 million investment, intensifying substrate competition for liquid food packing.

- June 2025: New rules on imported glass scrap were released to secure higher-quality cullet for domestic furnaces.

- March 2025: Đạt Phương Group broke ground on an ultra-clear float glass facility in Hue, targeting PV and architecture glass with phase-one capacity of 400 tonnes per day.

Vietnam Container Glass Market Report Scope

The Vietnam Container Glass Market Report is Segmented by End-user (Beverages: Alcoholic (Beer, Wine, Spirits, Other Alcoholic Beverages) and Non-Alcoholic (Juices, Carbonated Drinks, Dairy Product Based Drinks, Other Non-Alcoholic Beverages); Food; Cosmetics and Personal Care; Pharmaceuticals; Perfumery) and Color (Green, Amber, Flint, Other Colors). The Market Forecasts are Provided in Terms of Volume (Kilotons).

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How quickly is Vietnam shifting away from single-use plastics?

Decree 08/2022/ND-CP bans thin non-degradable plastic bags from January 2026 and all single-use plastic products by December 2030, driving converters toward reusable glass.

Which sectors drive the strongest demand for glass bottles?

Beer remains dominant with 52.87% volume share in 2025, and craft beer plus premium cosmetics segments are generating the fastest incremental tonnage.

Why is amber glass gaining popularity?

Craft brewers and pharmaceutical fillers favor amber’s light-blocking properties, propelling its 3.84% CAGR through 2031.

What role does foreign investment play in capacity expansion?

More than USD 20 billion in manufacturing FDI in 2024 is funding furnace upgrades and new lines near industrial clusters, securing supply for export-oriented customers.

How does Extended Producer Responsibility affect glass makers?

A mandatory 15% recycling rate on glass bottles raises compliance costs but rewards producers building cullet collection networks that lower energy use and emissions.

Is the Vietnam container glass market at risk from rPET bottles?

RPET is eroding share in mass-market soft drinks, yet premium beverages, cosmetics, and pharma still rely on glass for brand image and product stability.

Page last updated on: