South Korea Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.63 Billion |

| Market Size (2026) | USD 4.79 Billion |

| Market Size (2031) | USD 5.69 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

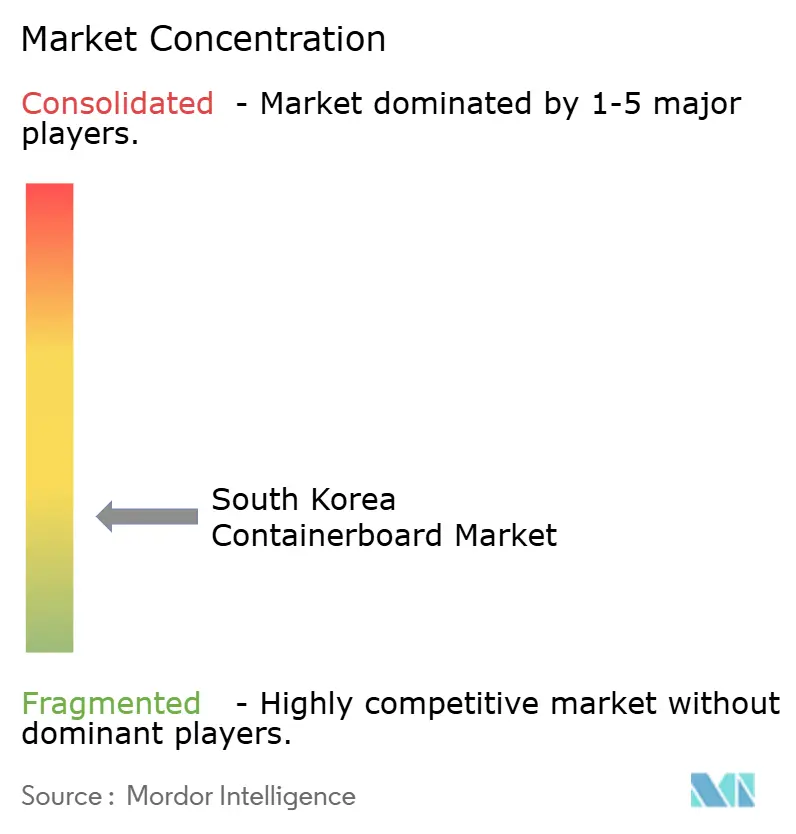

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Containerboard Market Analysis by Mordor Intelligence

The South Korea containerboard market size was valued at USD 4.63 billion in 2025 and estimated to grow from USD 4.79 billion in 2026 to reach USD 5.69 billion by 2031, at a CAGR of 3.52% during the forecast period (2026-2031). The South Korea containerboard market is being supported by 2 demand streams, online commerce and industrial exports, and those 2 streams do not weaken at the same time in most periods. Online retail continued to grow in 2025, while offline retail remained nearly flat, leading to a larger share of packaging demand shifting from shelf-ready formats to delivery-grade corrugated boxes. Export shipments also provided mills with a second utilization channel, helping protect production rates as domestic consumer spending remained soft and pricing conditions grew more challenging. The South Korea containerboard market also benefits from strong recycling systems and policy pressure that favor paper-based formats in delivery, food service, and branded retail packaging. Competitive conditions remain balanced between integrated mill operators and a fragmented converter base, while volatility in raw material and energy costs is pushing producers toward lighter, stronger, and more specialized grades.

Key Report Takeaways

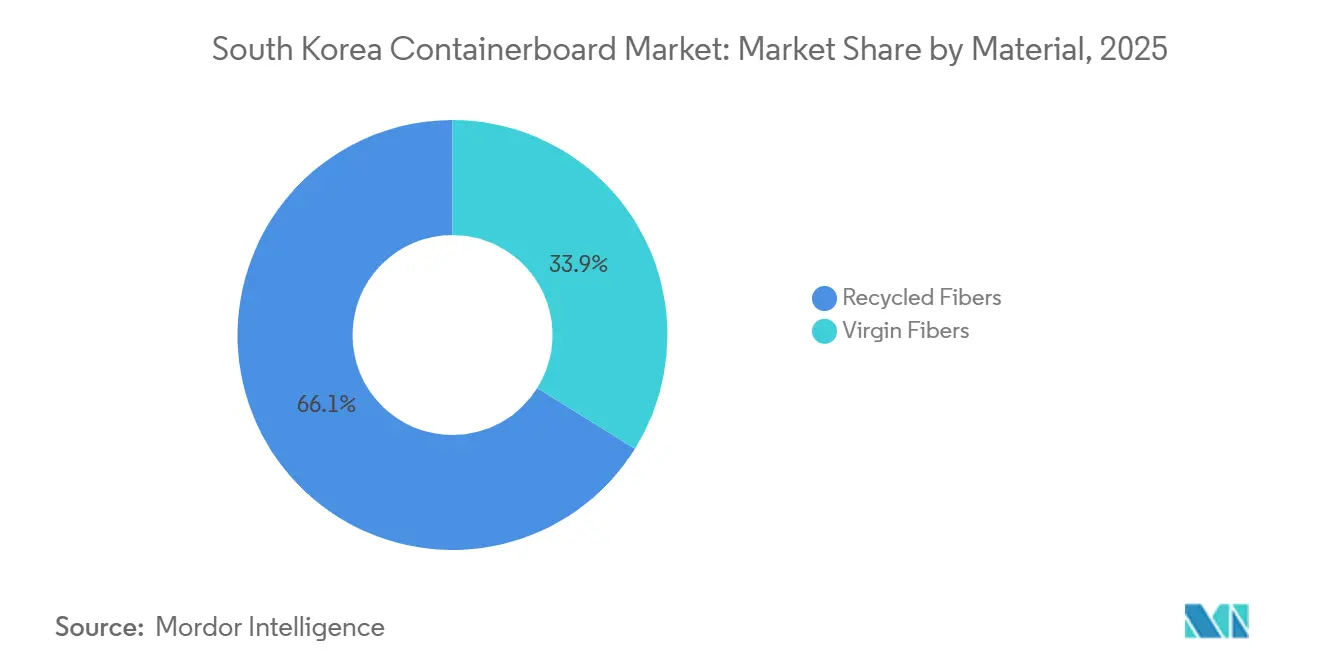

- By material, recycled fibers captured 66.12% of the South Korea containerboard market share in 2025.

- By product type, the South Korea containerboard market size for the kraftliners segment is forecast to advance at a 4.16% CAGR through 2031.

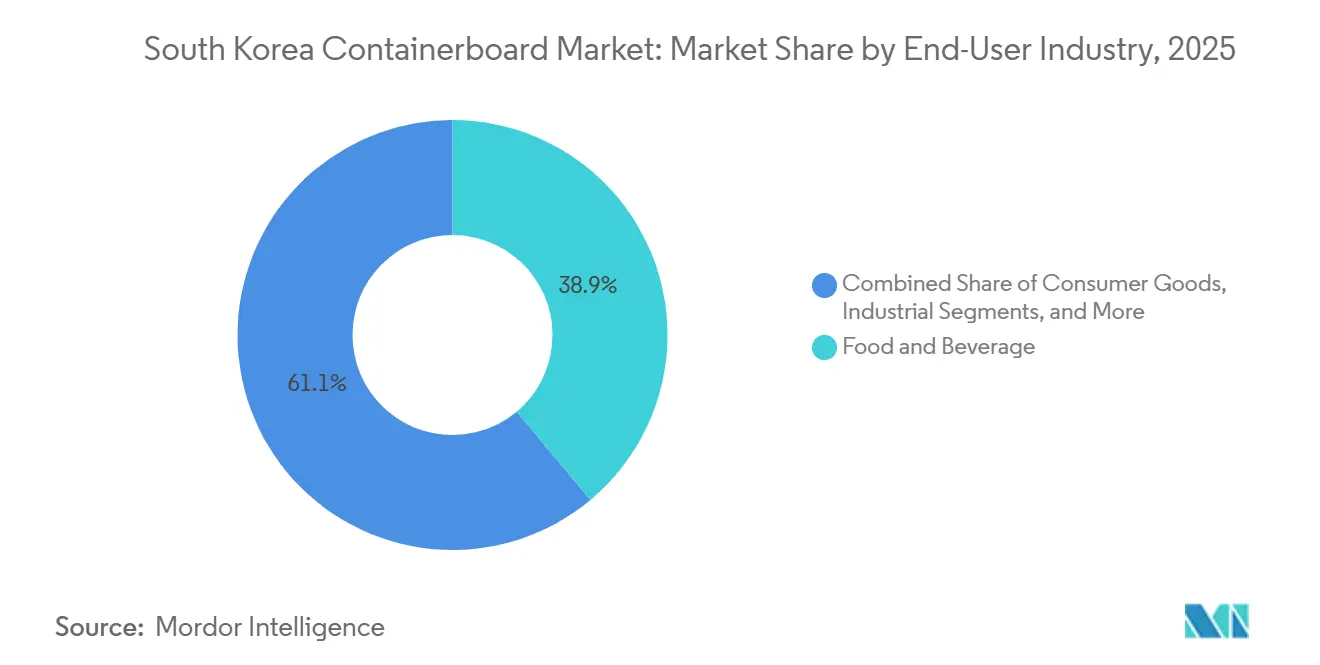

- By end-user industry, food and beverage captured 38.91% of the South Korea containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce Parcel Density | +1.2% | National, concentrated in Seoul-Incheon-Gyeonggi corridor fulfillment hubs | Short term (≤ 2 years) |

| Food And Grocery Fulfillment Growth | +0.8% | National, led by urban metros, Seoul, Busan, Daejeon, Incheon | Short term (≤ 2 years) |

| Export-Led Electronics And Auto Shipments | +0.6% | APAC export routes via Busan, Incheon, and Gwangyang ports | Medium term (2-4 years) |

| Shift Toward Recyclable Paper-Based Packaging | +0.5% | National, with fastest adoption in branded FMCG and e-commerce verticals | Medium term (2-4 years) |

| 2025 Mandatory Recycling Ratios For Packaging Materials | +0.3% | National, regulatory influence primarily from MCEE and KECO compliance frameworks | Long term (≥ 4 years) |

| Lightweight High-Strength Board Adoption | +0.2% | National, spill-over to Southeast Asian export markets requiring premium grades | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Parcel Density

Rising parcel density is increasing both the volume and the technical quality of corrugated packaging required across the South Korea containerboard market. Online retail sales in 2025 rose 11.8%, while offline retail expanded only 0.4%, shifting more packaging demand away from shelf-pack formats and toward transit-ready corrugated solutions designed for direct-delivery handling. This pattern matters because higher-order frequency and faster delivery schedules shorten parcel dwell time and place more stress on boxes during repeated handling cycles. As a result, strength-to-weight balance has become more valuable than simply using heavier paper, supporting micro-flute and lightweight, high-strength formats with better cube efficiency. That product shift also helps fulfillment operators reduce void space, lower transport inefficiency, and maintain automated packing line consistency across large order volumes. Revised courier packaging standards issued in March 2026 set a 50% ceiling on packaging space for companies with annual sales of KRW 50 billion (USD 0.035 billion) or more, providing a compliance rationale for wider adoption of right-sized corrugated packaging at scale.

Food And Grocery Fulfillment Growth

Food and grocery fulfillment is driving more intensive board use because perishable shipments require better protection, moisture management, and temperature control than many general merchandise orders. Online food and beverage transactions reached KRW 37.8 trillion (USD 0.026 trillion) in 2025, while online food service transactions reached KRW 41.4 trillion (USD 0.029 trillion) in the same year, extending high-frequency packaging demand across urban delivery networks. That growth carries extra value for the South Korean containerboard market because food parcels often use more protective packaging per unit of product value than standard non-food shipments. Seoul and 12 other major municipalities banned expanded polystyrene containers in 2024, and that policy direction widened the space for paper-based delivery packaging in quick-commerce and prepared-meal channels. Tailim Packaging's Teco Box, launched in 2024, maintained temperatures below 10°C for 21 hours, delivered 98% of the EPS box's thermal performance, and used only 50% of the warehouse footprint, demonstrating that corrugated solutions can replace rigid foam in more demanding cold-chain applications. These conditions are lifting both shipment volumes and packaging value intensity per order inside the South Korea containerboard market rather than simply swapping one low-value format for another.

Export-Led Electronics And Auto Shipments

Export manufacturing gives the South Korea containerboard market a second demand base that does not move in lockstep with domestic retail spending. Electronics, semiconductors, and automotive components require a board with consistent burst strength, a stable caliper, and lower moisture absorption along long, multi-stage logistics routes. Corrugated board exports from South Korea rose 34.7% in FY2025, with India, Vietnam, and Japan as the largest destination markets by volume, confirming that Korean mills can redirect output beyond local demand cycles.[1]Asia Paper Manufacturing Co., Ltd., “사 업 보 고 서 (제 70 기),” Korea Exchange, kind.krx.co.kr This export mix favors Kraft-top and other premium liner formats over fully recycled commodity grades, which helps explain why higher-value products are gaining momentum even as recycled fiber remains dominant. Busan, Incheon, and Gwangyang strengthen this utilization buffer by connecting mills and converters to regional trade lanes with lower outbound friction than many inland systems. That combination of export exposure and logistics reach makes the South Korea containerboard market less vulnerable to the full depth of domestic consumption slowdowns than several other mature regional markets.

Shift Toward Recyclable Paper-Based Packaging

The shift toward recyclable paper packaging is widening the addressable demand base for the South Korea containerboard market across retail, food service, and personal care applications. South Korea's EPR framework raised the national packaging recycling rate from 40.6% in 2002 to 72.9% by 2021, thereby strengthening the commercial case for corrugated board over harder-to-recycle, harder-to-certify materials. The 2026 Resource Circulation Roadmap introduced a Korean eco-design approach that asks companies to address environmental performance at the packaging design stage, which increases the importance of compliant paper solutions earlier in procurement planning. KECO's fee structure applies a 30% surcharge to difficult-to-recycle packaging, turning recyclable corrugated formats into a cost and compliance decision for brand owners and distributors. That matters because material conversion moves faster when it affects procurement budgets directly, rather than only sustainability targets or brand messaging. The policy mix is therefore pushing more substitution toward paper in delivery packaging, food service containers, and consumer-facing outer packaging, where recyclability now affects both operating cost and reporting requirements.[2]International Energy Agency, “Act on the Promotion of Saving and Recycling of Resources,” International Energy Agency, iea.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Paper, Pulp, And Energy Cost Volatility | -0.4% | National, export-exposed mills face additional USD-denominated pulp price risk | Short term (≤ 2 years) |

| Competition From Flexible Plastics And Alternative Formats | -0.3% | National, strongest substitution pressure in industrial and agricultural packaging segments | Medium term (2-4 years) |

| Weak Domestic Retail Spending And Poor Cost Pass-Through | -0.2% | National, most acute for small and medium-sized box plant operators | Short term (≤ 2 years) |

| Cross-Border E-Commerce Packaging Waste Escaping Domestic EPR Cost Recovery | -0.1% | National, regulatory blind spot concentrated in direct-to-consumer import channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Paper, Pulp, And Energy Cost Volatility

Input cost volatility remains the clearest pressure point for producers operating in the South Korea containerboard market. South Korea imports 85% of the virgin pulp it uses domestically, and raw materials account for 60% of paper production costs, which leaves mills highly exposed to both USD movements and commodity price swings.[3]Jino John, “Global Pulp Prices Rise for Sixth Consecutive Month, Increasing Pressure on Paper Producers,” Pulp and Paper Chronicle, pulpandpaperchronicle.com SBHK pulp prices rose from USD 630 per ton in August 2025 to USD 740 per ton in February 2026, a 17.5% swing that compressed margins before producers could renegotiate selling prices. Mills also attempted price increases of KRW 60,000 (USD 42.2) to 80,000 (USD 56.2) per tonne in August 2024, but converter resistance forced a reversal by October, showing that pass-through power remains limited when downstream demand is soft. Domestic OCC pricing can also move against mills, as inventory builds and price softness may occur at the same time as export demand from China weakens. Higher industrial electricity tariffs add another cost layer for continuous paper operations that cannot switch energy sources quickly or pause production without incurring efficiency losses.

Competition From Flexible Plastics And Alternative Formats

Flexible plastics and other alternative formats still hold a functional position in parts of food, industrial, and agricultural packaging, which limits full substitution in the South Korea containerboard market. Barrier pouches, liquid formats, and other technically demanding applications remain difficult for paper to replace without specification changes, equipment adjustments, or customer tolerance for higher conversion complexity. Some thermally sensitive delivery applications also continue to rely on foam or hybrid formats, while corrugated alternatives scale up and prove repeat performance in wider commercial use. In agricultural distribution, buyers still often link heavier boxes with better protection, which slows the move toward lighter, high-strength boards even when technical data supports the shift. Daehan Paper demonstrated that 46 g/m² low-grammage high-strength fluting can deliver stacking performance comparable to conventional 110 g/m² grades, but procurement habits change slowly across fragmented rural and wholesale channels. This keeps substitution pressure strongest where performance tradition and price sensitivity still outweigh sustainability preferences or freight-efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Leadership With A Rising Virgin Fiber Mix

Recycled fibers accounted for 66.12% of demand in 2025, making them the leading raw material base in the South Korean containerboard market. South Korea produced 11 million tonnes of paper in 2024, and 80% of that output came from recycled fiber, confirming that the country's mill structure is already built around secondary inputs rather than moving toward them only now. That installed base matters because it supports a reliable flow of testliner and other recycled-content grades that serve domestic FMCG, household goods, and broad-based shipping needs. It also reflects more than 2 decades of investment in collection systems, sorting routines, and recycled milling operations shaped by packaging recovery policy and producer responsibility rules.[4]International Energy Agency, “Act on the Promotion of Saving and Recycling of Resources,” International Energy Agency, iea.org The result is that recycled fiber remains the commercial backbone of the South Korea containerboard market even as producers look for selective quality upgrades.

Virgin fibers are forecast to expand at a 3.84% CAGR through 2031, and this segment of South Korea's containerboard market is being driven by export-grade specifications rather than large-scale domestic commodity demand. Electronics and automotive packaging often require more consistent burst strength, caliper control, and moisture resistance than fully OCC-based furnishes can deliver with the same repeatability across long export routes. Producers are therefore using selective virgin blending where performance stability matters most, especially for customers shipping higher-value goods across multi-modal international channels. This does not weaken the broader recycling base because the material shift is concentrated in premium applications where failure costs are much higher than fiber input savings. In practical terms, the South Korean containerboard industry is moving toward a better grade mix and a wider value ladder, rather than away from the circular systems that still define most local production.

By Product Type: Testliner Scale Holds While Kraftliner Gains Momentum

Testliners held 42.83% of the South Korean containerboard market share in 2025, keeping them in the lead because they fit the country's recycled-fiber base and the cost needs of domestic FMCG supply chains. Their position remains strong with converters serving food processors, household goods suppliers, and regional distributors that prioritize repeat specifications, reliable supply, and tight price control over appearance premiums. Testliner also aligns with the operating profile of many smaller box plants, as it supports fast-turn production for standard shippers used in local transport and retail replenishment. This volume role keeps Testliner central to the South Korean containerboard market, even as product requirements become increasingly segmented by customer type and route complexity. Fluting remains tied to this mass-market structure because the medium layer still determines much of the balance between stiffness, stacking performance, and paper consumption in standard box formats.

Kraftliners are projected to grow at the fastest 4.16% CAGR through 2031, and this slice of South Korea's containerboard market size is benefiting from export packaging needs and the stronger visual standards used by branded consumer goods sellers. Tailim Packaging's high-strength, lightweight box reduced paper use by up to 20% while increasing compression strength by over 20%, which is why customers are willing to pay for stronger, more efficient liner performance when shipping conditions are demanding. That same logic supports the move toward higher-grade linerboard for electronics, automotive components, and consumer-facing packs where appearance and protection both matter. The shift toward 46 g/m² precision-controlled high-strength fluting is also moving local performance closer to global lightweight benchmarks and lowering the penalty of using less paper in well-engineered structures. The South Korea containerboard industry is therefore developing a more differentiated product ladder, with testliner preserving scale while kraftliner captures the growth premium tied to export quality and premium presentation.

By End-User Industry: Food And Beverage Keeps Scale While Consumer Goods Raises Quality Demands

Food and beverage accounted for 38.91% of demand in 2025, which made it the single largest outlet for the South Korea containerboard market. That position reflects the corrugated intensity of chilled distribution, ambient food logistics, takeaway packaging, and short-cycle replenishment across stores, warehouses, and delivery networks. Online food and beverage transactions reached KRW 37.8 trillion (USD 0.026 trillion) in 2025, and online food service transactions reached KRW 41.4 trillion (USD 0.029 triilion), keeping packaging throughput high in urban fulfillment systems that handle frequent, smaller orders. Municipal restrictions on EPS packaging since 2024 created additional room for corrugated formats in food delivery and temperature-managed use cases, where paper solutions were less competitive a few years earlier. These factors keep food and beverage at the center of volume demand because the segment combines routine repeat orders with rising packaging requirements per shipment.

Consumer goods is projected to advance at a 4.02% CAGR through 2031 because personal care, cosmetics, home care, and lifestyle brands increasingly treat packaging as part of the delivered customer experience. Live shopping and social commerce formats reward better print quality, cleaner outer surfaces, and stronger box presentation during shipment, which supports demand for higher-value board specifications in this part of the South Korea containerboard market. Industrial buyers remain a mature demand base, but they continue moving toward lighter double-wall and single-wall formats to reduce logistics cost and improve pallet efficiency without giving up required protection standards. Other end-user groups, including electronics retail, agricultural produce, and pharmaceuticals, maintain steady corrugated use that moves more closely with export cycles and broader business spending patterns. Across these categories, KECO-linked recyclability rules keep corrugated board in a strong position because compliant paper grades remain easier to defend on both cost and environmental grounds.

Geography Analysis

The Seoul-Incheon-Gyeonggi corridor accounted for over 60% of national corrugated demand, making it the largest concentration point in the South Korean containerboard market. Seoul and Gyeonggi-do combine dense FMCG production, e-commerce fulfillment, and large parcel flows, so demand in this corridor spans both standard recycled grades and more specialized premium formats. Incheon International Airport adds a premium packaging layer because airfreight shipments of electronics and semiconductors require cleaner surfaces, tighter consistency, and better print quality than those in basic domestic distribution boxes. The same corridor also contains a large network of small and medium-sized food processors, cosmetics companies, and personal care brands that need fast converter turnaround and dependable packaging supply for online channels. South Korea's online shopping market reached KRW 272.3 trillion (USD 0.19 trillion) in 2025, and the Seoul metro area remained the main parcel hub driving that demand.

The Busan-Changwon-Ulsan belt forms the second major demand tier in the South Korea containerboard market because export manufacturing is concentrated there. Automotive assembly, marine engineering, electronics production, and chemical shipments in this corridor require a stronger board for longer and more complex logistics routes than many domestic consumer shipments. Gwangyang Bay adds a different layer of heavy industrial packaging demand, with a greater emphasis on double- and triple-wall applications for chemicals, metals, and petrochemical cargo. Corrugated board exports from South Korea increased 34.7% in FY2025, with India, Vietnam, and Japan as the main outbound destinations, which shows how coastal industrial zones help mills preserve utilization when local demand softens. The resource recycling law applies across all regions, but enforcement is strongest in major municipalities with mature collection and audit systems, which raises the compliance threshold for packaging suppliers serving large urban industrial customers.

The Chungcheong region, including Daejeon, Cheongju, and Sejong, is seeing increased industrial packaging demand as semiconductor and biopharmaceutical cluster development deepens inland manufacturing activity. Sejong's recyclable delivery packaging requirements, effective from 2025, also created a local reference point for other municipalities to follow as paper substitution moves further into delivery packaging systems. South Korea's corrugated packaging recycling rate reached 92% in 2023, which supports multinational sourcing interest in high-recyclability substrates and strengthens the environmental profile of domestic packaging supply chains. Jeju remains small in absolute volume, but it shows stronger per-unit demand for higher-quality packaging in export-oriented agricultural shipments and in tourism retail, adding another premium niche to the wider South Korea containerboard market.

Competitive Landscape

The South Korea containerboard market is moderately concentrated at the mill level and far more fragmented at the converter level, where more than 200 box plants compete on proximity, turnaround time, service flexibility, and customization. Large integrated producers hold structural advantages because they can coordinate recovered paper sourcing, paper production, and box conversion across the same operating chain. Standalone mills and independent converters still matter because they can respond faster to pricing, customer service, and localized production schedules for smaller accounts. The largest structural change now underway is Global Sae-A's sale process for Tailim Paper, Tailim Packaging, Jeonju Paper, and Jeonju Wonpower, a package with over 30% of corrugated base paper capacity and around 20% of the packaging materials market, valued at up to KRW 2 trillion (USD 1.4 billion). Once completed, that ownership transition is likely to reshape the upper tier of the South Korean containerboard market and influence future capacity, integration, and customer-allocation decisions.

Competitive strategy is increasingly dividing between scale-led efficiency and higher-value paper solutions targeted at compliance and product differentiation. Hansol Paper launched the Protego HS heat-sealable paper series in April 2026 to replace conventional plastic flexible packaging in food and confectionery applications, signaling a direct move toward adjacent packaging categories rather than merely defending core grades. Hansol Paper also used its April 2026 customer seminar to align domestic paperboard offerings with EU packaging rules for buyers such as CJ Logistics, Lotte Wellfood, GS Retail, and Ottogi, which tied product development more closely to customer compliance agendas. Asia Paper Manufacturing, Tailim Paper, and Korea Paper Mfg. filed an anti-dumping complaint against Japanese linerboard suppliers in late 2024, which showed that domestic producers are also willing to defend sensitive grade categories through trade mechanisms. Asia Paper Manufacturing also continued work on its KRW 195.1 billion (USD 140 million) corrugated board plant, with commercial completion still targeted for December 2026, which keeps capacity expansion on the table despite a tighter cost environment.

Tailim Packaging received the Ministry of Environment's recyclable resource usage product certification for its Sihwa factory in June 2025, strengthening its position with customers who increasingly screen suppliers based on compliance-related procurement criteria. The company also won a national packaging award in April 2025 for a high-strength lightweight corrugated box co-developed with Ottogi Ramen that cut paper use by up to 20% and increased compression strength by more than 20%. These moves show that competitive separation is increasingly built around recyclability, lightweighting, export performance, and customer-specific design rather than around commodity scale alone. The South Korean containerboard market, therefore, remains active and competitive, but it is not tightly consolidated, as concentrated mill assets still sit above a wide, service-driven converter base.

South Korea Containerboard Industry Leaders

Asia Paper MFG. Co., Ltd.

TAILIM PACKAGING Co., Ltd.

Daeyang Paper Mfg. Co., Ltd.

Sam Jung Pulp Co., Ltd.

Daelim Paper Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Hansol Paper reported Q1 2026 operating profit of KRW 11.2 billion, a 44.7% year-over-year decline, with consolidated revenue falling 2.7% to KRW 559.8 billion (USD 0.39 billion). Industrial paper, the segment encompassing containerboard-adjacent grades, recorded a 1.1% revenue decline to KRW 146.6 billion (USD 0.103 billion), driven by logistics and raw material cost volatility stemming from geopolitical risks in the Middle East and global trade uncertainty.

- April 2026: Hansol Paper launched the Protego HS (Heat Sealable) paper secondary packaging series, designed to replace conventional plastic flexible packaging in food and confectionery categories including chocolate, candy, powdered sauces, seaweed, and coffee. The product achieves Grade A recyclability under the EU Packaging and Packaging Waste Regulation and requires no customer equipment modification for adoption.

- April 2026: Hansol Paper held its "2026 Customer-Invited Paper Technology Seminar" at its Daejeon plant, presenting EU Packaging and Packaging Waste Regulation compliance strategies to 60 procurement officials from CJ Logistics, Lotte Wellfood, GS Retail, and Ottogi, directly aligning domestic paperboard solutions with multinational brand packaging decarbonization commitments.

- March 2026: Global Sae-A formally initiated the sale of Tailim Paper, Tailim Packaging, Jeonju Paper, and Jeonju Wonpower, with UBS as the sale arranger, dispatching teaser letters to over 20 strategic and financial investor candidates on March 17, 2026. The combined entity holds over 30% of corrugated base paper capacity and 20% of the packaging material market, with an estimated transaction value of up to KRW 2 trillion (USD 1.4 billion).

South Korea Containerboard Market Report Scope

The South Korea Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The South Korea Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the South Korea containerboard market size in 2026 and what will it reach by 2031?

The South Korea containerboard market stands at USD 4.79 billion in 2026 and is projected to reach USD 5.69 billion by 2031, growing at a 3.52% CAGR.

What is driving demand for containerboard in South Korea?

The main demand drivers are rising e-commerce parcel density, food and grocery fulfillment growth, export-led electronics and automotive shipments, and wider use of recyclable paper-based packaging.

Which material type leads demand in South Korea?

Recycled fibers led with a 66.12% share in 2025 because the country has a mature OCC collection and recycled milling system, while virgin fiber is growing faster in premium export packaging.

Which product type is growing the fastest?

Kraftliners are forecast to grow at a 4.16% CAGR through 2031, while testliners remained the largest product type in 2025 with a 42.83% share.

Which end-user group contributes the most demand?

Food and beverage was the largest end-user segment in 2025 with 38.91% of demand, supported by chilled distribution, food delivery, and high-frequency replenishment.

Which areas create the strongest regional demand in South Korea?

The Seoul-Incheon-Gyeonggi corridor is the main demand center because it concentrates e-commerce fulfillment and consumer goods production, while Busan, Ulsan, and Gwangyang support export-oriented industrial demand.

Page last updated on: