Vietnam Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

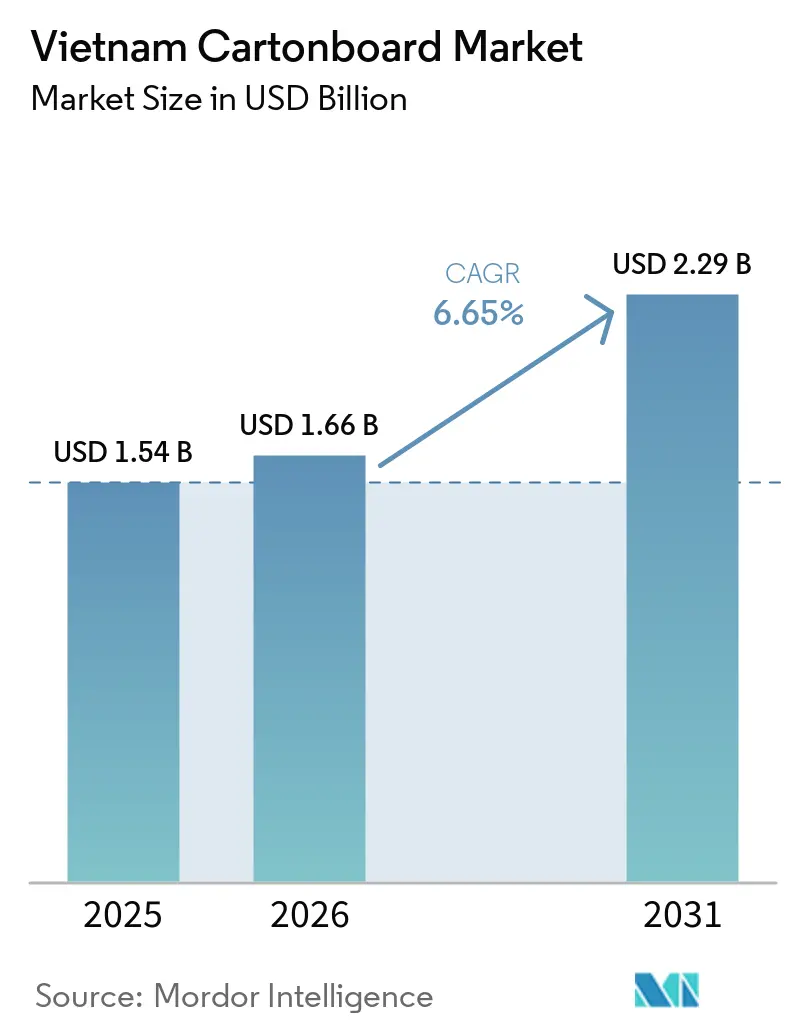

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Cartonboard Market Analysis by Mordor Intelligence

The Vietnam cartonboard market size was valued at USD 1.54 billion in 2025 and estimated to grow from USD 1.66 billion in 2026 to reach USD 2.29 billion by 2031, at a CAGR of 6.65% during the forecast period (2026-2031). The Vietnam cartonboard market is supported by stronger packaged food consumption, wider use of shelf-ready retail packs, and steady investment in converting and liquid carton capacity nationwide. Demand is also moving beyond standard white-lined chipboard as buyers in healthcare, premium food, and export supply chains seek better printability, tighter quality control, and packaging formats that meet stricter product-handling requirements. The Vietnam cartonboard market is also seeing a clearer split between commodity converters that compete mainly on price and specialty players that protect margins through compliance, process reliability, and closer customer integration. E-commerce growth is boosting demand for printed folding cartons that serve both transit and display needs, improving the mix for converters with stronger finishing and short-run printing capabilities. Over the forecast period, the best opportunities are likely to remain in liquid packaging, pharmaceutical secondary cartons, and higher-value folding formats linked to organized retail, food service, and export-oriented manufacturing.

Key Report Takeaways

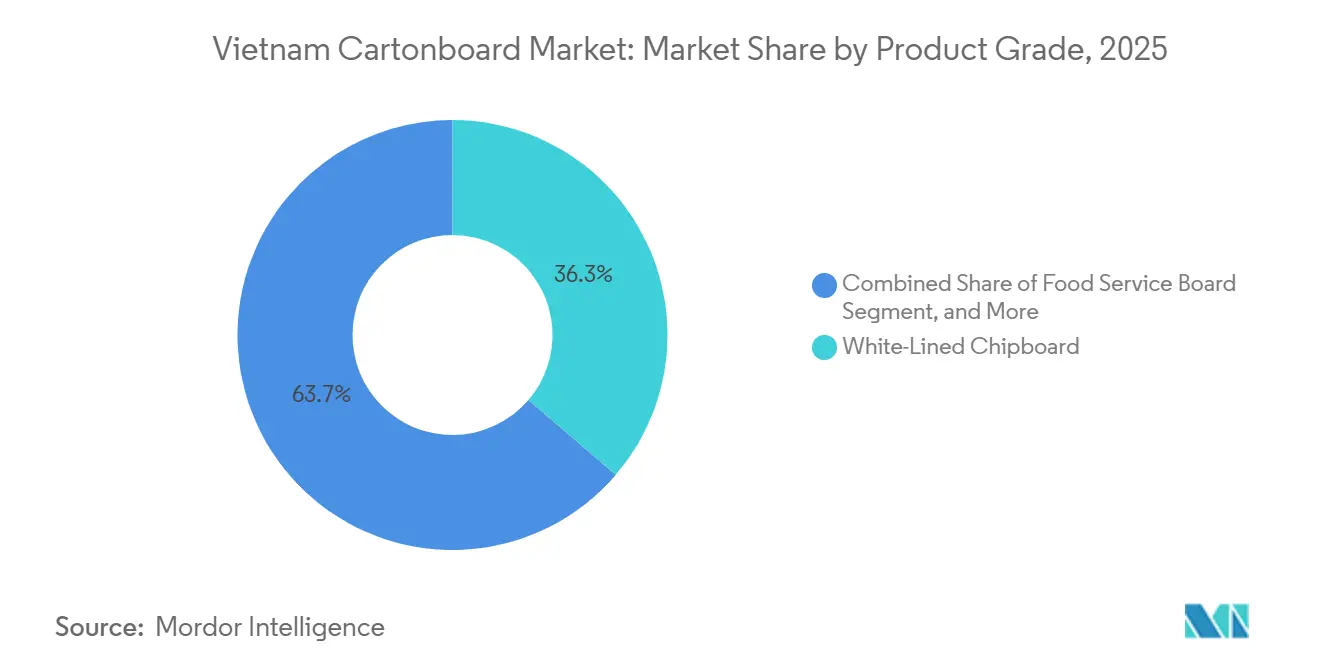

- By product grade, white-lined chipboard captured 36.27% of the Vietnam cartonboard market share in 2025.

- By packaging format, the Vietnam cartonboard market size for the liquid packaging segment is forecast to advance at a 7.15% CAGR through 2031.

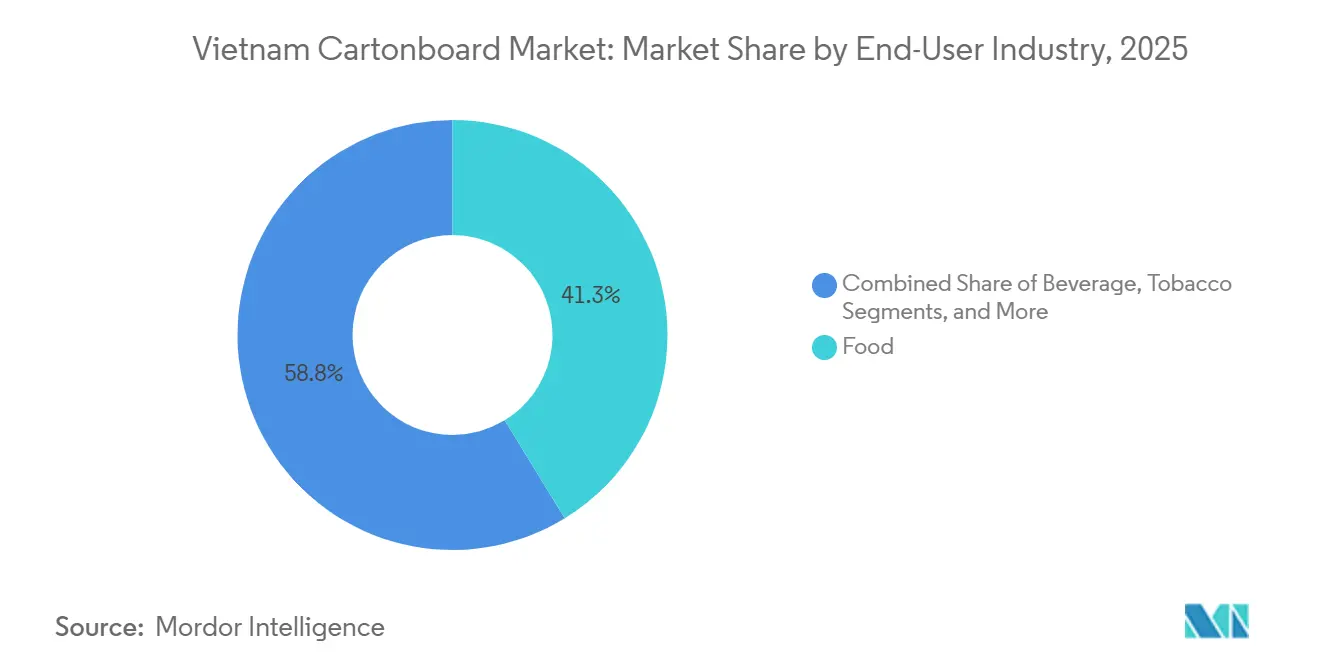

- By end-user industry, food captured 41.25% of the Vietnam cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Processed Food and Beverage Consumption | +2.0% | National, with concentrated demand in HCMC, Hanoi, and Binh Duong | Short term (≤ 2 years) |

| E-commerce and Retail-Ready Packaging Expansion | +1.6% | National, strongest in southern belt, HCMC and Binh Duong, and Hanoi metropolitan area | Short term (≤ 2 years) |

| Plastic Substitution and EPR-Led Paper Packaging Shift | +1.1% | National, accelerated by EPR compliance pressure in FMCG and retail sectors | Medium term (2-4 years) |

| Pharmaceutical Localization and Compliance Packaging Demand | +0.8% | National, with early gains in pharma manufacturing clusters in Hanoi, Binh Duong, and Dong Nai | Medium term (2-4 years) |

| Tetra Pak Capacity Expansion Supporting Liquid Carton Adoption | +0.5% | Southern Vietnam, centered on Binh Duong, with spillover to regional ASEAN markets | Medium term (2-4 years) |

| Export-Buyer Traceability and FSC Requirements Reshaping Converter Selection | +0.4% | National, strongest among export-facing converters in HCMC, Binh Duong, and Bac Ninh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Processed Food And Beverage Consumption

Vietnam's food and beverage sector generated VND 726.5 trillion (USD 27.94 billion) in 2025 and is projected to reach VND 760 trillion (USD 29.23 billion) in 2026, which keeps a broad demand base in place for milk cartons, dry food cartons, frozen food packs, and other secondary paperboard formats.[1]iPOS.vn and Nestlé Professional, “Vietnam Food and Beverage Market Report 2025,” Vietstock, en.vietstock.vn That spending matters to the Vietnam cartonboard market because it supports demand across multiple board grades simultaneously, rather than relying on a single end-use pocket. As household purchases move further toward packaged and branded food, converters benefit from repeat demand driven by labeling, transport protection, and visual shelf presentation in modern retail and foodservice channels. The demand profile also favors suppliers that can handle mixed jobs across beverages, dairy, frozen products, and dry grocery lines without long lead times or inconsistent print quality. The result is a steadier order book for folding cartons, foodservice packs, and liquid board applications, helping the Vietnam cartonboard market maintain growth even as lower-value commodity formats remain under pricing pressure.

E-Commerce And Retail-Ready Packaging Expansion

Vietnam's e-commerce market recorded GMV of VND 458.16 trillion (USD 16.58 billion) in 2025, and revenue in the first quarter of 2026 rose 32.74% year on year to VND 134.6 trillion (USD 5.19 billion).[2]Vietnam E-commerce and Digital Economy Agency, “Vietnam's E-commerce Set for Safer, More Sustainable Growth Under New Law,” Vietnam Trade Office in Canada, vntradetoca.org The Ministry of Industry and Trade's digital economy platform also stated that Vietnam's e-commerce market is targeting USD 37 billion in 2026, which points to continued expansion in direct-to-consumer shipments and branded packaging demand.[3]Vietnam.vn, “Vietnam's E-commerce Market Aims for a Size of USD 37 Billion,” Vietnam.vn, vietnam.vn This shift supports the Vietnam cartonboard market because packaging is increasingly expected to protect goods in transit and still perform as a display-ready unit when it reaches the buyer or retailer. That change improves the position of converters with digital and UV offset capabilities, since shorter runs, greater artwork variation, and faster product refresh cycles are becoming more common. It also shifts the value mix away from plain transit packs and toward litho-laminated and better-finished folding cartons, giving the Vietnam cartonboard market a stronger revenue profile than pure volume growth would suggest.

Plastic Substitution And EPR-Led Paper Packaging Shift

Vietnam's packaging EPR system now sets mandatory recycling rates of 15% to 22% for packaging materials, raising the cost and compliance burden associated with plastic-heavy packaging formats.[4]Springer Nature, “Current Status and Compliance Management of EPR Regulations for Packaging Waste in Vietnam,” Circular Economy and Sustainability, springer.com That policy direction supports the Vietnam cartonboard market because brand owners can improve the economics of compliance by shifting selected packaging applications toward paper-based structures where performance and recovery pathways are easier to defend. The change is especially relevant in FMCG, retail, and food service, where packaging decisions are made at scale and compliance costs are repeated across large product portfolios. It also changes how brands present themselves in modern trade channels, as a move into paper cartons can support regulatory alignment and a clearer sustainability message on the shelf. Over time, this should help better-positioned converters win more work in secondary packs, food-service containers, and retail-ready paper formats as packaging specifications are redesigned to align with EPR obligations.

Pharmaceutical Localization And Compliance Packaging Demand

Vietnam's pharmaceutical market was estimated at USD 8.58 billion in 2025 and is expected to reach USD 10 billion in 2026, while the national industrial development program approved in February 2025 targets 20% domestic self-sufficiency in pharmaceutical raw materials by 2030. This matters to the Vietnam cartonboard market because each increase in domestic drug production expands the need for compliant secondary cartons that can support labeling, traceability, transport protection, and plant-level quality systems. The regulatory environment is also tightening, with pharmaceutical packaging standards consolidated under the Ministry of Health framework in 2024, raising the bar for converters serving drug manufacturers. This helps suppliers that already operate with stronger documentation, controlled production processes, and more stable board quality, while making it harder for low-cost commodity players to compete only on price. As a result, pharmaceutical demand provides the Vietnamese cartonboard market with a recurring stream of higher-value work that is less exposed to day-to-day price pressure than standard FMCG cartons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Fiber Price Volatility and Import Dependence | -0.8% | National, concentrated in WLC-producing mills dependent on imported OCC | Short term (≤ 2 years) |

| Fragmented Converter Base and Persistent Price Competition | -0.6% | National, most acute in Southern Vietnam's dense converter cluster | Medium term (2-4 years) |

| PolyAl Beverage Carton Recycling Bottlenecks | -0.3% | National, with critical infrastructure gaps in HCMC and major urban centers | Long term (≥ 4 years) |

| Imported Barrier and Liquid Board Dependence | -0.3% | National, affecting liquid packaging-focused converters in Southern Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recovered Fiber Price Volatility And Import Dependence

Vietnam banned imports of mixed paper and left old corrugated containers as the dominant imported recovered fiber grade, which keeps domestic mills exposed to international trade flows and pricing changes in recycled fiber. US wastepaper unit prices rose from USD 167 per tonne in 2020 to USD 204 per tonne in 2024, which shows how input cost swings can move quickly across the supply chain before easing again. This is a direct issue for the Vietnam cartonboard market because white-lined chipboard remains the largest product-grade segment and depends on recycled fiber layers in its cost structure. When fiber costs move sharply, mills and converters cannot always pass those changes through to customers on fixed or price-sensitive contracts, especially in food and FMCG work. The result is a recurring margin squeeze that slows value growth, weakens planning visibility, and keeps commodity-focused suppliers more vulnerable than specialty-grade operators with tighter customer relationships.

Fragmented Converter Base And Persistent Price Competition

Vietnam's paper packaging sector included 334 companies in 2025, with more than 100 FDI companies and over 200 domestic players, while the top 10 firms together accounted for only 30% of sector revenue. This fragmented structure limits pricing discipline in the Vietnamese cartonboard market, particularly in standard folding carton applications, where many small- and mid-sized converters compete for similar jobs. A large part of the pressure falls on white-lined chipboard-based food trays and secondary FMCG cartons, where customers can switch suppliers quickly and technical differentiation is limited. It also slows investment in digital printing, quality certification, automation, and shared collection infrastructure because many smaller firms lack the capital to fund those upgrades on their own. Over time, that keeps a wide productivity gap in place between international or well-capitalized players and local firms that still rely on price-led competition to protect volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: White-Lined Chipboard Anchors Volume, Food Service Board Accelerates

White-lined chipboard held 36.27% of the Vietnam cartonboard market share in 2025, maintaining its lead by balancing acceptable print quality with cost efficiency across food, beverage, and everyday FMCG packaging applications. The grade remains central to the Vietnam cartonboard market, where domestic buyers still closely weigh substrate cost in large-volume secondary cartons and multipack applications. Solid bleached board and folding boxboard continue to serve more demanding packaging lines in pharmaceuticals, cosmetics, and premium food, where surface finish, branding quality, and cleaner board appearance support better pricing and more controlled procurement standards. Liquid packaging board also retained an important role because dairy and ready-to-drink categories depend on aseptic formats that require a different performance profile than standard folding carton jobs.

The food service board is projected to grow at a 7.57% CAGR during 2026-2031, making it the fastest-expanding grade, as quick-service restaurants, delivery platforms, and single-serve consumption continue to drive demand for cups, containers, and takeaway packs. Vietnam's total food and beverage outlet count was estimated at 329,500 in 2025 and is projected to reach 333,600 by the end of 2026, supporting a broader adoption of disposable paperboard formats across urban centers. Within the Vietnam cartonboard industry, this creates a clearer split between large-volume white-lined chipboard demand and faster-value growth in food service and liquid applications. It also means suppliers that invest in barrier performance, consistent forming behavior, and food-contact quality control are likely to capture a larger share of the premium mix than converters that focus only on standard recycled-board grades.

By Packaging Format: Folding Cartons Dominate, Liquid Packaging Gains Ground

Folding cartons captured 57.44% share of the Vietnam cartonboard market size in 2025, reflecting their wide use across frozen food, pharmaceutical secondary packs, cosmetics, tobacco, and other branded consumer goods. The format sits at the center of the Vietnamese cartonboard market because it can serve both retail presentation and product protection without the added complexity of multilayer liquid formats. It has also benefited from the growth of organized retail and e-commerce, where outer appearance, print quality, and unboxing performance increasingly shape packaging decisions beyond pure transport needs. Vietnam's online retail expansion is reinforcing that trend because more product categories now move through display-ready cartons rather than plain secondary packs.

Liquid packaging is expected to grow at a 7.15% CAGR during 2026-2031, supported by both new converting investment and stronger demand from dairy and beverage applications. Tetra Pak's expanded Binh Duong facility lifted annual capacity to more than 30 billion aseptic packs in July 2025, and Oji Holdings announced a USD 104 million liquid packaging carton plant in Dong Nai, scheduled to start operations in 2028. Within the Vietnam cartonboard industry, that investment signals a longer-term shift toward higher-value packaging formats that depend on process control, specialized materials, and deeper customer integration. Sleeves, trays, cups, and foodservice containers are also gaining relevance, but liquid formats remain the clearest example of how capital spending and end-use demand are reshaping the Vietnam cartonboard market.

By End-User Industry: Food Leads, Pharmaceutical And Healthcare Gain Pace

Food accounted for 41.25% of the Vietnamese cartonboard market in 2025, making it the largest end-user group, as it meets several packaging needs at once, including dairy packs, frozen food cartons, cereal boxes, condiment cartons, and other branded grocery formats. That base keeps the Vietnam cartonboard market closely tied to everyday consumer spending, giving the sector broad, repeat demand rather than a narrow reliance on a few industrial applications. The value of Vietnam's food and beverage sector reached VND 726.5 trillion (USD 27.94 billion) in 2025 and is projected to rise again in 2026, which supports continued packaging demand across supermarkets, food service, and convenience channels. VN Beverage demand also remains important because aseptic packaging helps brand owners reach areas with uneven cold-chain coverage, thereby strengthening the role of liquid board and related specialty carton formats.

Pharmaceutical and healthcare are projected to expand at a 7.36% CAGR during 2026-2031, making it the fastest-growing end-user segment as domestic drug output, compliance needs, and packaging documentation requirements continue to rise. Vietnam's pharmaceutical market is expected to reach USD 10 billion in 2026, and the government's February 2025 industrial development program is guiding increased local production of pharmaceutical inputs and related products. That creates recurring demand for converters that can meet tighter quality systems, consistent board performance, and better traceability for secondary cartons. Cosmetics and toiletries also add value at the premium end of the market because higher-finish cartons with embossing, foiling, and specialty coatings can lift unit pricing even when volumes are modest. Other end uses, such as household goods, toys, apparel, and electrical products, continue to support baseline demand, but the strongest value shift within the Vietnam cartonboard market is coming from healthcare and premium consumer packaging rather than from commodity applications alone.

Geography Analysis

Southern Vietnam remained the main demand and converting center in the Vietnam cartonboard market because Ho Chi Minh City, Binh Duong, Dong Nai, and Ba Ria-Vung Tau combine large FMCG, beverage, and pharmaceutical production bases with established packaging supply chains. Binh Duong alone had attracted 4,400 FDI projects with USD 42.5 billion in registered capital by December 31, 2024, which shows why the province remains central to packaging demand linked to manufacturing and consumer goods output. Tetra Pak's expanded Binh Duong facility, commissioned in July 2025, now produces more than 30 billion aseptic packs per year and sends over 55% of output to the Vietnamese market, reinforcing the South's role in liquid carton supply. Oji Holdings' planned USD 104 million plant in Dong Nai adds another long-cycle investment that will strengthen the region's role in liquid packaging once commercial operations begin in 2028. The region also benefits from a mature converter base and port access that support both imported board supply and export-oriented carton converting.

Northern Vietnam is emerging as a more technically distinct part of the Vietnam cartonboard market because electronics, pharmaceuticals, and food processing are creating demand for cleaner, higher-specification carton formats. The region's industrial structure supports packaging jobs that require stronger print control, moisture handling, and brand consistency than the more price-led segments common in standard commodity cartons. Ngoc Diep Joint Stock Company, which operates the largest carton packaging factory in Northern Vietnam at Quang Minh Industrial Zone in Hanoi, reflects the scale that specialized northern converters are building around demand for pharmaceutical, food, and industrial packaging. As industrial activity continues to shift northward, the Hanoi-Hai Phong corridor is likely to remain an important market for premium folding boxboard and solid bleached board.

Central Vietnam and the Mekong Delta remained smaller parts of the Vietnamese cartonboard market, but both regions are adding incremental demand as manufacturing and export processing expand beyond the main northern and southern belts. Central provinces are attracting more mid-sized food processors and apparel exporters, creating a steady demand for secondary cartons and branded retail packs in categories that previously relied more on basic transport packaging. In the Mekong Delta, seafood and fresh produce exporters are facing stronger traceability and brand presentation requirements from overseas buyers, which is driving a gradual shift toward more retail-ready paperboard formats for selected value-added products. These regions are still well behind the South and North in scale, but they should continue to contribute to volume growth as Vietnam spreads industrial investment more evenly across its logistics and manufacturing network.

Competitive Landscape

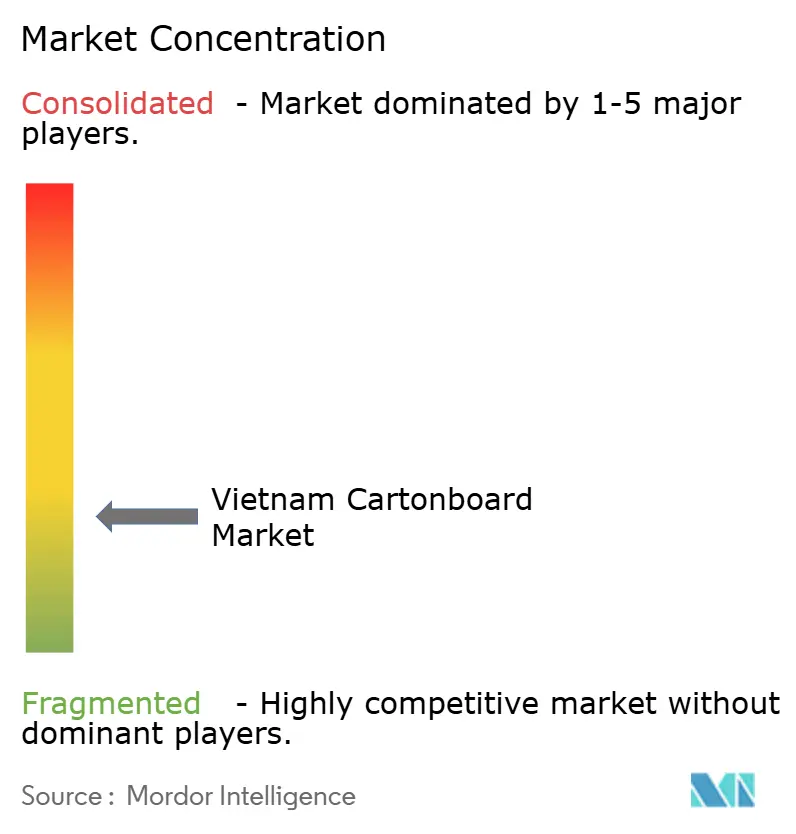

The Vietnam cartonboard market remains fragmented, and no domestic converter holds a double-digit share, while the top 10 players together account for only 30% of broader paper packaging revenue. That structure means competition is still divided between multinational specialists with stronger capital and process systems, and domestic converters that compete through flexibility, customer responsiveness, and shorter production runs. In the Vietnamese cartonboard market, multinational players are strongest in premium liquid packaging and specialty folding cartons, where board sourcing, certification, and operating discipline matter more than price alone. Domestic firms remain relevant because many Vietnamese brand owners still value local account management, quicker artwork revisions, and smaller batch support for frequent product changes. The result is a market where scale helps, but specialization and execution still determine who captures the most profitable contracts.

Recent corporate moves show how competition is shifting toward capacity depth, technology, and application-specific positioning rather than simple expansion in standard carton output. Tetra Pak increased annual production capacity at Binh Duong from 12 billion to more than 30 billion packs per year in July 2025, which raised the competitive bar in liquid carton supply for Vietnam and nearby export markets. Oji Holdings also committed USD 104 million to a new liquid packaging carton plant in Dong Nai and linked the project to a future regional collection and recycling system for used cartons, which shows a broader strategic push beyond simple manufacturing capacity. SCG Packaging added another competitive signal by approving a VND 604 billion (USD 23.3 million) first-phase investment to expand fiber packaging converting capacity in Ho Chi Minh City, with commercial operations expected in September 2027.

Technology is also reshaping competitive positions in the Vietnam cartonboard market, as customers increasingly expect shorter runs, better print quality, and packaging that supports traceability or premium brand presentation. Digital UV offset capability is becoming increasingly valuable in pharmaceutical and personal care work, where product portfolios can change quickly, and many launches do not justify long conventional print runs. Compliance-sensitive procurement is creating another divide, as converters with stronger quality systems are better positioned to win work from multinational FMCG firms and drug manufacturers. That leaves the market open to consolidation pressure over time, but it also preserves room for specialized domestic suppliers that can prove reliability in healthcare, export-facing food, and higher-finish folding carton applications.

Vietnam Cartonboard Industry Leaders

Tetra Pak International S.A.

Oji Interpack Vietnam Co., Ltd.

SONG LAM Trading & Packaging Production CO., Ltd.

Khang Thanh Manufacturing JSC

Starprint Vietnam Joint Stock Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SIG, a global provider of aseptic carton packaging solutions, has extended its "Recycle for Good" initiative to Vietnam. This expansion involves a partnership with the Bac Ninh Province Department of Education and Training and Lagom waste management. The program focuses on collecting and recycling used milk cartons from preschools and primary schools in Bac Ninh Province. The separated PolyAl material is processed at Lagom's facility into products such as clothing hangers, flowerpots, and building panels. This initiative marks the establishment of Vietnam's first structured school-based liquid carton recycling program and enhances SIG's compliance with the country's stricter Extended Producer Responsibility (EPR) framework.

- January 2026: Mainetti, an Italian flexible packaging manufacturer, has opened a new 5,000 m² facility at Minh Quang Industrial Park in Hung Yen Province. The facility aims to produce up to 3,000 metric tonnes of polypropylene bags annually, primarily using recycled materials. These bags are intended for apparel supply chain clients such as Gap, Columbia Sportswear, Lululemon, and Amazon. This investment highlights the increasing focus on sustainable secondary packaging within Vietnam's export manufacturing corridors.

- July 2025: Tetra Pak International S.A. inaugurated the second phase of its aseptic packaging material production line at its Binh Duong, Vietnam facility, following an additional investment of EUR 97 million (USD 104.2 million), bringing total site investment to EUR 217 million (USD 233 million) and increasing annual production capacity from 12 billion to over 30 billion packs per year with 15 new packaging formats, the expanded LEED Version 4 Gold Certified plant serves Vietnam, Thailand, Malaysia, Indonesia, Singapore, the Philippines, Australia, and New Zealand, with over 55% of output destined for the Vietnamese domestic market.

- July 2025: Tetra Pak International S.A. and Dong Giao Foodstuff Export JSC (Doveco) launched Vietnam's first Tetra Recart paper-based food packaging line, with a capacity of 6,000 cartons per hour, enabling shelf-stable retort packaging for sweetcorn, pineapple juice, and assorted beans, the launch establishes Vietnam as Southeast Asia's first market for commercial-scale Tetra Recart deployment and broadens the range of applications for aseptic liquid packaging board.

Vietnam Cartonboard Market Report Scope

The Vietnam Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include solid bleached board, solid unbleached board, folding boxboard, white-lined chipboard, liquid packaging board, and food service board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Vietnam Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

How large is the Vietnam cartonboard market?

The Vietnam cartonboard market was valued at USD 1.54 billion in 2025, is estimated at USD 1.66 billion in 2026, and is forecast to reach USD 2.29 billion by 2031 at a 6.65% CAGR.

Which product grade leads cartonboard demand in Vietnam?

White-lined chipboard led demand with a 36.27% share in 2025 because it remains cost efficient for food, beverage, and general FMCG secondary packaging.

Which packaging format is growing the fastest in Vietnam?

Liquid packaging is the fastest-growing format, with a projected 7.15% CAGR through 2031, supported by rising aseptic pack demand and major capacity additions by Tetra Pak and Oji.

Which end-user segment offers the strongest growth potential?

Pharmaceutical and healthcare is expected to record the fastest growth at a 7.36% CAGR through 2031 because local drug production and compliance requirements are raising demand for higher-specification secondary cartons.

Why is Southern Vietnam so important for cartonboard suppliers?

Southern Vietnam is the main production and consumption hub because it combines dense FMCG and beverage manufacturing, strong FDI inflows, port access, and major liquid packaging investments in Binh Duong and Dong Nai.

What is the main challenge facing converters in Vietnam?

Recovered fiber price volatility and a fragmented converter base remain the main challenges because they compress margins in commodity grades and keep price competition intense in standard folding carton applications.

Page last updated on: