Specialty Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 37.36 Billion |

| Market Size (2031) | USD 52.06 Billion |

| Growth Rate (2026 - 2031) | 6.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Specialty Coffee Market Analysis by Mordor Intelligence

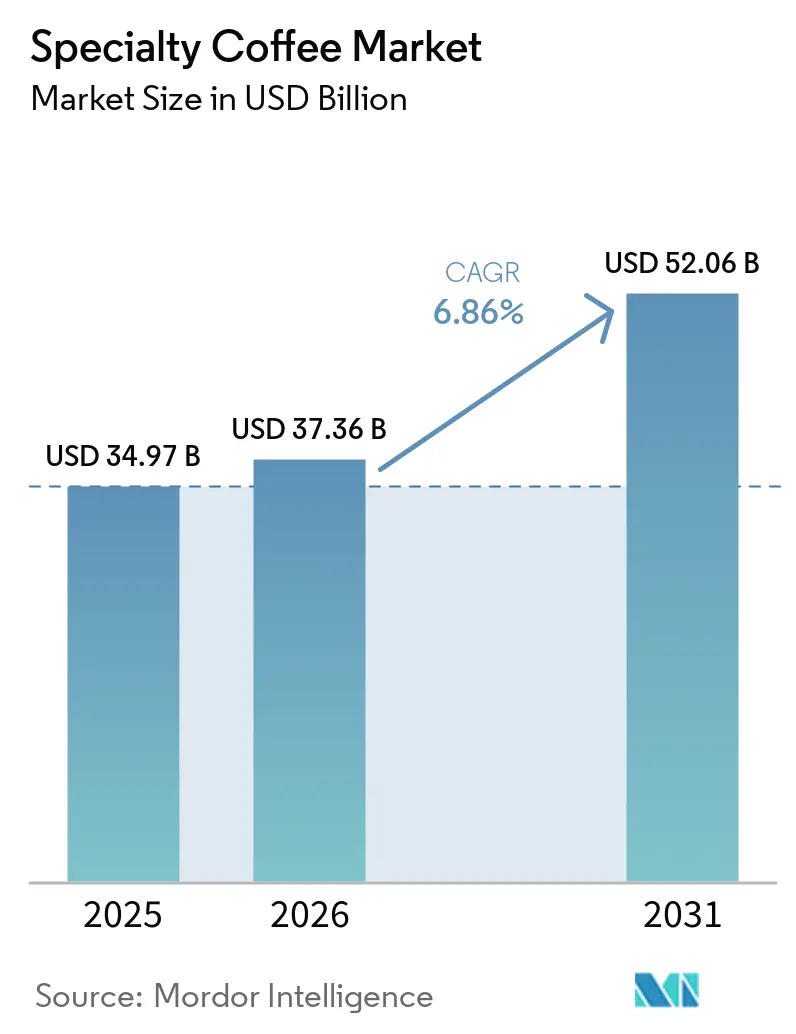

The specialty coffee market was valued at USD 35.0 billion in 2025 and is estimated to grow from USD 37.4 billion in 2026 to reach USD 52.1 billion by 2031, at a CAGR of 6.9% during the forecast period (2026-2031). The specialty coffee market is being shaped by premiumization, as consumers are spending more on coffees with clearer origin, better taste, and stronger sourcing credentials. In the United States, specialty coffee maintained its lead over traditional coffee in daily consumption in 2026, indicating that the specialty coffee market has moved beyond a niche position in a key demand center. The specialty coffee market is also absorbing supply pressure from weather-related crop disruptions in Brazil and Vietnam, yet premium pricing has continued to protect value realization for stronger brands. At the same time, functional positioning, single-serve innovation, and cold-format development are widening the addressable use cases for the specialty coffee market beyond the café occasion. Large branded players are responding with pod partnerships, store expansion, and loyalty-led customer retention, while smaller roasters continue to compete on provenance, roast identity, and local relevance

Key Report Takeaways

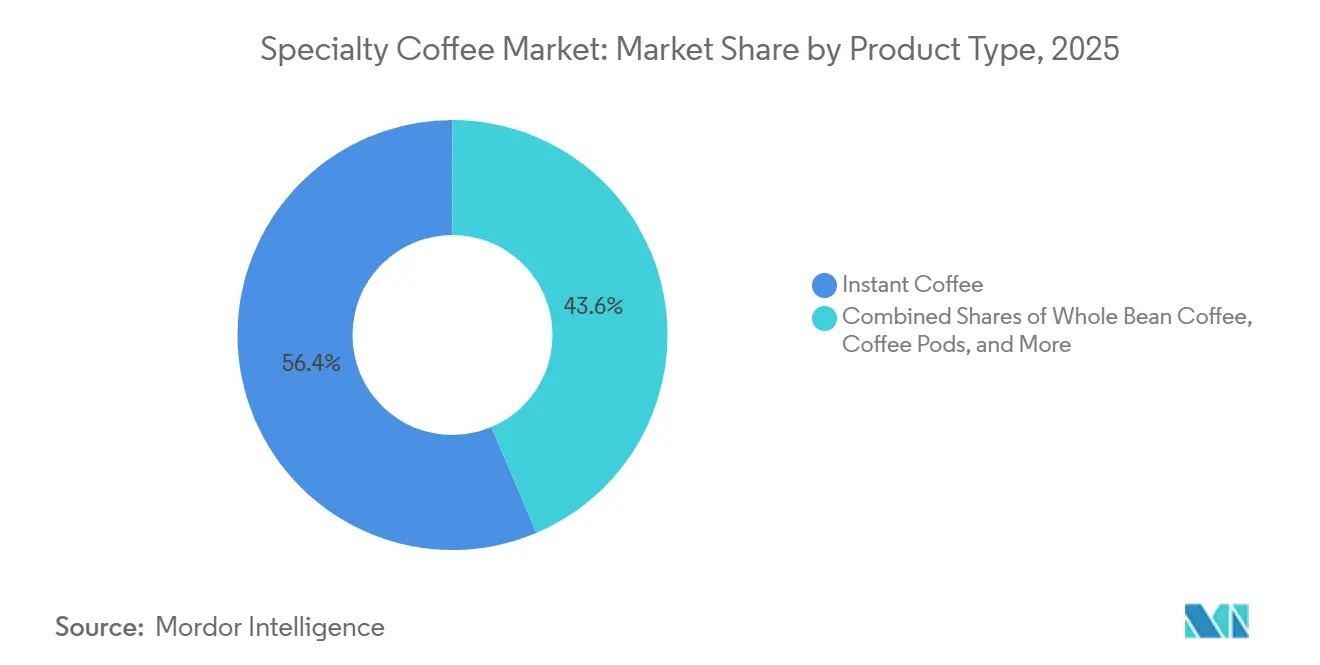

- By product type, instant coffee accounted for 56.38% of the specialty coffee market in 2025, while coffee pods and capsules recorded the highest projected CAGR at 7.65% through 2031.

- By category, conventional coffee accounted for 75.47% of revenue in 2025, while organic coffee is forecast to expand at an 8.02% CAGR through 2031.

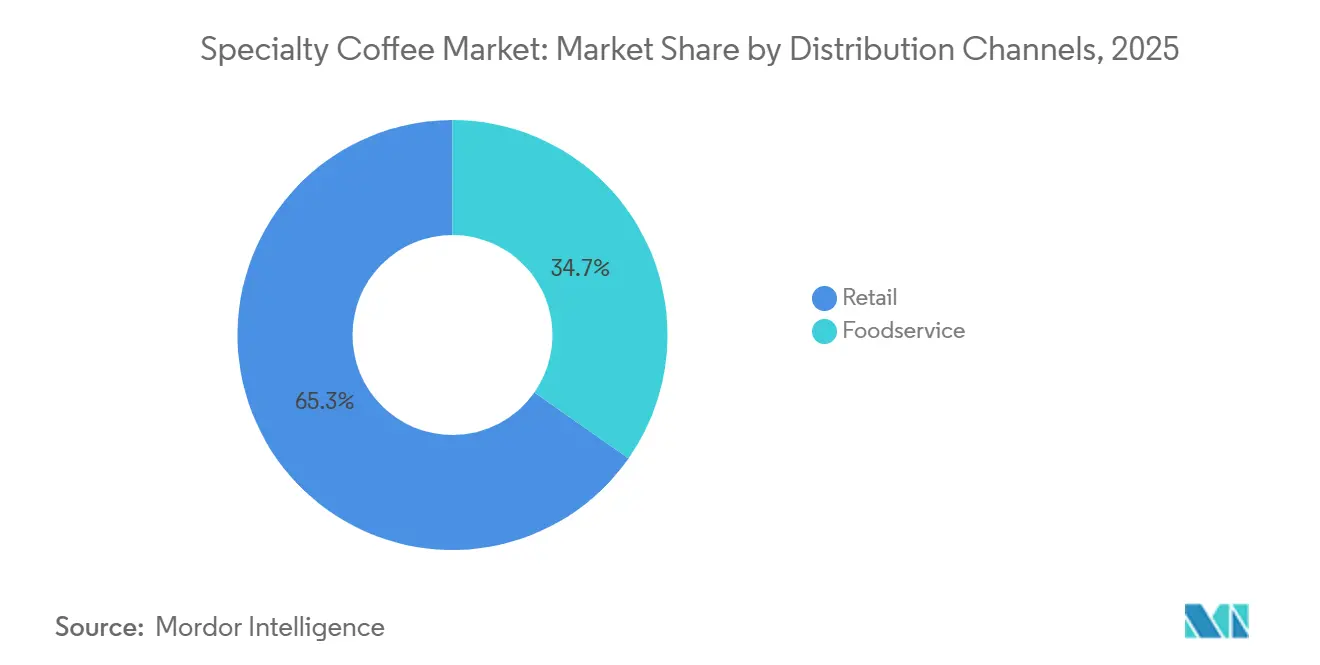

- By distribution channel, retail represented 65.27% of revenue in 2025, while foodservice is advancing at a 7.85% CAGR through 2031.

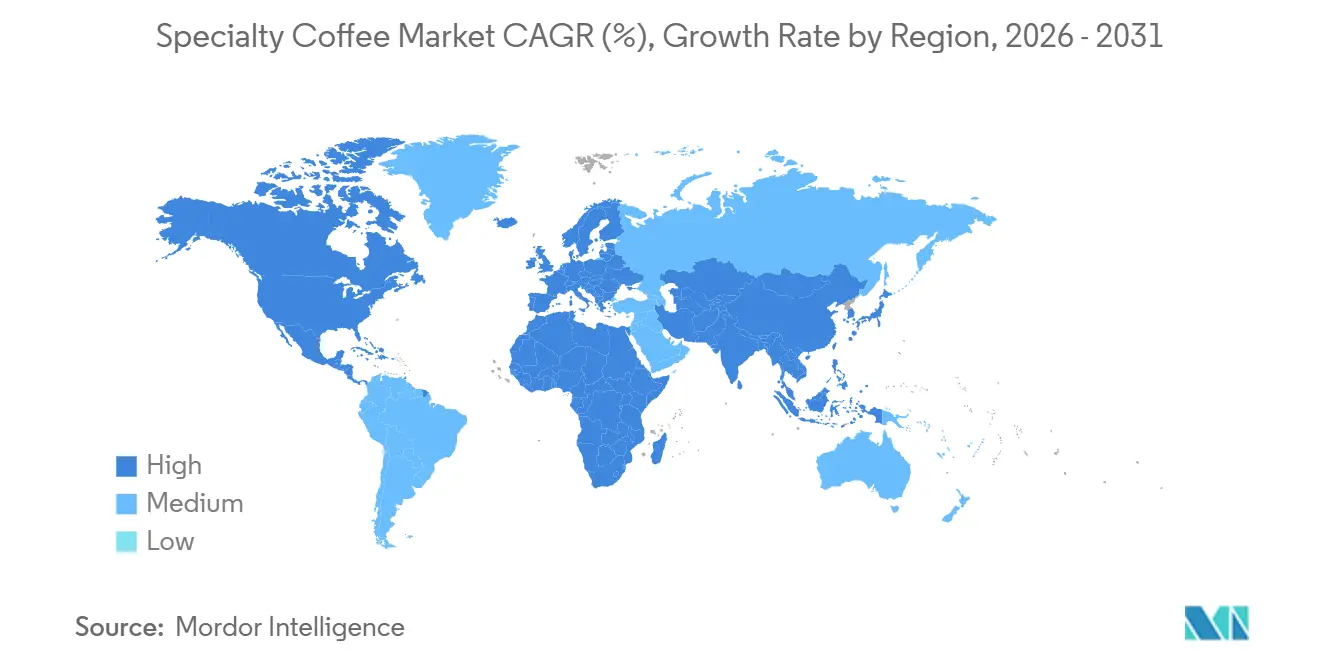

- By geography, North America held 34.25% of the specialty coffee market share in 2025, while Asia-Pacific registered the fastest projected CAGR at 8.03% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Specialty Coffee Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Preference for Premium Coffee Products | +1.4% | Global, concentrated in North America, Europe, and APAC urban centres | Long term (≥ 4 years) |

| Rising Coffee Culture and Café Consumption | +1.3% | Global, accelerating in APAC, MEA, and South America | Medium term (2–4 years) |

| Expansion of Specialty Coffee Chains and Independent Cafés | +0.9% | APAC, MEA, South America | Medium term (2–4 years) |

| Increasing Demand for Single-Origin Coffee | +0.8% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Product Innovation in Brewing Methods | +0.7% | Global, led by North America, Europe, and South Korea | Short to medium term |

| Health and Wellness Perceptions of Coffee | +0.6% | North America and Europe, with emerging traction in APAC | Medium to long term |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Premium Coffee Products

Premium coffee has moved from an occasional purchase to a more regular habit for a wider set of consumers, and that shift is strengthening pricing power across the specialty coffee market. Past-week specialty coffee consumption reached 58% among U.S. adults in 2026, which was 10 percentage points higher than in 2021[1]Source: National Coffee Association, “Specialty Coffee Holds Lead Over Traditional Coffee in the U.S.,” National Coffee Association, ncausa.org. The age profile also matters because 64% of consumers aged 25 to 39 drank specialty coffee in the past week in 2025, which supports long-duration demand visibility for the specialty coffee market. This pattern favors brands that can explain farm origin, roasting approach, and sourcing standards in a simple way that consumers trust. It also makes premium coffee less dependent on discounting because buyers are increasingly choosing taste, transparency, and quality cues before price. As a result, the specialty coffee market is becoming harder for purely value-led brands to defend, especially when input costs are rising.

Rising Coffee Culture and Café Consumption

Café network expansion is making coffee discovery more routine, and that is broadening the consumer base for the specialty coffee market. Local chains in China continued to scale rapidly in 2025, which helped normalize high-frequency espresso-based consumption and improved category familiarity in everyday routines. Starbucks also used its January 2026 Investor Day to outline long-term plans for up to 5,000 additional U.S. coffeehouses and a significant increase in its international footprint, including large expansion targets in China. This dual expansion model, with convenience-led local brands and premium international brands growing at the same time, is enlarging the audience for the specialty coffee market across income tiers. Consumers often enter through a convenient café format and later move into branded beans, capsules, or subscriptions for home use. That progression keeps café growth closely linked to retail demand growth in the specialty coffee market.

Health and Wellness Perceptions of Coffee

Health-focused messaging is becoming a stronger purchase support factor, and that is giving the specialty coffee market a broader reason to command premium pricing. According to the Food Standards Agency data from 2025, 26% of women had greater knowledge of their recommended daily calorie intake than men in the United Kingdom[2]Source: Food Standards Agency, "Making Food Better Tracker Survey, 2024", science.food.gov.uk. The National Coffee Association reported in 2025 that 61% of specialty coffee consumers believed coffee was beneficial to their health. That perception is encouraging more overlap between specialty coffee and functional coffee, especially in formats that include adaptogens, probiotics, nootropics, or plant-based protein additions. The taste story still matters, but the consumer justification is becoming wider because buyers can now connect quality, indulgence, and wellness in one purchase. This creates room for roasters and capsule makers to launch higher-value products without moving too far from the existing identity of the specialty coffee market. It also helps explain why premium formats are extending into more dayparts and more home-based consumption occasions.

Product Innovation in Brewing Methods

Brewing innovation is changing the format mix inside the specialty coffee market and is creating new competition around convenience and sustainability. Lavazza introduced Tablì in the United States in June 2026 as a coffee tab system built from 100% coffee, with more than 15 patents supporting the format and a full U.S. launch scheduled for August 2026. This matters because it challenges the long-standing tradeoff between pod convenience and packaging waste. Nestlé also expanded its focus on cold coffee and at-home format development, including espresso concentrate and added production capacity in Malaysia, which shows how product architecture is widening inside the specialty coffee market. These launches are not only about new products because they also redefine how consumers access premium coffee at home. Brands that can combine consistency, convenience, and a cleaner sustainability message are likely to gain an advantage as the specialty coffee market shifts further toward repeatable home rituals.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Prices Compared to Conventional Coffee | -1.2% | Global, with stronger drag in price-sensitive parts of Asia-Pacific and South America | Long term (≥ 4 years) |

| Supply Chain Complexity | -1.0% | Global, with sharper pressure in North America and Europe due to import dependence | Short term (≤ 2 years), Medium term (2-4 years) |

| Regulatory and Sustainability Compliance Costs | -0.7% | Europe and increasingly North America, with indirect effects on exporter countries | Medium term (2-4 years) |

| Availability of Alternative Specialty Drinks | -0.6% | North America and Europe, with rising traction in Asia-Pacific and South America | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Complexity

Supply chain pressure is one of the clearest near-term limits on volume growth in the specialty coffee market. Climate-linked stress in Brazil has become especially important because arabica supply remains central to premium sourcing. Research published in Climatic Change in 2025 showed that higher temperatures and altered precipitation patterns reduced arabica yields in Brazil, with some farms in Cerrado Mineiro reporting harvest declines of up to 44% during the 2025 season. Weather-related shortfalls in Vietnam have added to the problem by keeping green coffee prices elevated across product tiers. Specialty roasters are more exposed than many commodity players because they depend on specific lots, farms, and cooperatives that cannot be replaced with broad forward-buying strategies. This means the specialty coffee market must manage higher sourcing risk without losing the traceability and quality cues that justify premium pricing.

High Product Prices Compared to Conventional Coffee

Price remains a structural limit on how widely the specialty coffee market can penetrate daily consumption. Specialty products already carry a 20% to 50% premium over commodity-grade coffee in many established markets, and recent green coffee inflation has widened that gap further. JDE Peet’s reported substantial cost inflation in FY2025 due to green coffee price developments, while also implementing 19.5% price increases and absorbing a 4.3% volume decline, which shows how difficult price pass-through has become even for large branded operators. This dynamic is especially relevant in South America and Southeast Asia, where consumer aspiration is rising faster than disposable income in many urban markets. The result is a two-tier structure in which affluent consumers can sustain specialty purchases more easily than the wider middle-income base. Brands that bring specialty cues into accessible pods, subscriptions, and private-label formats are likely to capture the next layer of demand in the specialty coffee market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pods and Capsules Redefine At-Home Specialty Occasions

Coffee pods and capsules are projected to be the fastest-growing product type in the specialty coffee market, with a 7.65% CAGR from 2026 to 2031. This is the only product segment that clearly outpaces the overall growth rate of the specialty coffee market. The gain reflects a strong consumer push toward café-style quality at home, especially where convenience matters as much as taste. It also reflects the larger installed base of single-serve machines in mature households and the increasing affordability of entry-level systems in newer demand centers. For consumers with limited access to specialty cafés, pod ecosystems often serve as the first practical step into the specialty coffee market. Keurig Dr Pepper and Nestlé USA reinforced this path in April 2026 by extending their strategic partnership around Starbucks K-Cup manufacturing, distribution, and innovation in the United States and Canada.

Instant coffee remained the largest product segment and held 56.38% of the specialty coffee market size in 2025. That leadership still reflects instant coffee’s reach, portability, and ease of use across both mature and frontier markets. The quality gap within instant has narrowed because premium freeze-dried and micro-ground offerings now carry stronger taste credentials and better packaging. Ground coffee and whole bean coffee continue to represent the artisanal center of the specialty coffee market, especially among home brewers and café operators who value freshness and roast control. Whole bean products benefit from a growing consumer interest in grind-to-order routines and extraction accuracy. Other products, including ready-to-drink cold brew and nitrogen-infused coffee, remain smaller by value but are becoming more relevant for convenience-led premium purchases in urban retail and delivery channels.

By Category: Organic’s Outperformance Points to a Structural Trade-Up

Organic coffee is forecast to grow at an 8.02% CAGR through 2031, which makes it the fastest-growing category in the specialty coffee market. Conventional coffee still held 75.47% of revenue in 2025, so the current structure remains broad-based rather than niche. The difference is that organic is gaining from stronger certification trust, wider sustainability awareness, and a growing willingness to pay for traceable production standards. In the specialty coffee market, certification is becoming part of both product differentiation and supply-chain credibility. illycaffè showed this direction in December 2025 when it launched Arabica Selection Brasile Cerrado Mineiro capsules sourced from regenerative agriculture certified by regenagri®, which raised the visibility of multi-layered premium claims in capsules. This shift suggests that organic growth is not just label-led, but tied to a deeper change in what consumers expect from premium coffee.

Conventional coffee remains dominant because it benefits from wider shelf presence, more stable distribution, and long-standing consumer familiarity. Yet the strongest movement inside conventional is happening in premium conventional products that borrow specialty cues such as single-origin sourcing, small-batch roasting, and limited regional editions. That allows the specialty coffee market to extend premium value without requiring every product to carry organic certification. In Asia-Pacific, this matters because food safety awareness and imported premium consumption patterns are rising together. In Europe, stronger retailer support for certified and traceable coffee is also making better-quality products easier to find in everyday shopping channels. As due diligence rules and sourcing audits become more demanding, the specialty coffee market is likely to reward supply chains that can prove both compliance and provenance with less friction.

By Distribution Channel: Foodservice Channels Accelerate Trade-Up

Retail remained the largest distribution channel in the specialty coffee market and represented 65.27% of revenue in 2025. Supermarkets and hypermarkets still lead in volume because they offer the widest physical reach and the most consistent purchase frequency. Online retail, however, is becoming more influential in higher-value niches because it supports subscriptions, sample packs, and better assortment depth. This is important for the specialty coffee market because premium shoppers often want curation, story, and access to limited roasts that general retail cannot always provide. Specialty stores also continue to matter in urban areas because they combine product education with a more guided purchase experience. Together, these channels are making retail broader and more layered than simple packaged-coffee distribution.

Foodservice is the fastest-growing channel in the specialty coffee market and is projected to rise at a 7.85% CAGR through 2031. Café visits often work as the first real tasting event for a new roaster, flavor profile, or brewing method. That makes foodservice a discovery engine as well as a sales channel. Once consumers find a coffee they trust in a café, they are more willing to buy the same roaster’s beans, pods, or ground coffee for home use. This feedback loop is helping the specialty coffee market convert out-of-home trial into repeat at-home purchasing. The pattern is especially relevant in fast-growing urban centers across Asia-Pacific, the Middle East, and South America, where café expansion is raising category familiarity at the same time that retail access is improving.

Geography Analysis

North America was the largest regional market in the specialty coffee market and held 34.25% of revenue in 2025. The United States remained the clear anchor because specialty coffee reached 47% past-day consumption among U.S. adults in 2026, while traditional coffee stood at 42% for the second straight year. That demand pattern shows that specialty coffee has become embedded in everyday beverage behavior rather than being limited to occasional indulgence. Starbucks also reported USD 6.9 billion in North America revenue in Q2 FY2026, up 7.0%, with comparable store sales up 7.1%, which confirms resilient consumer traffic and spend in the region. Canada is the fastest-growing submarket within the region, supported by urban café density and a growing base of independent roasters.

Europe remained the second-largest region in the specialty coffee market and continued to benefit from long-standing café culture and stronger retail support for premium formats. According to the British Coffee Association data from 2025, the United Kingdom consumers drank 98 million cups of coffee per day[3]Source: British Coffee Association, "Coffee Consumption", britishcoffeeassociation.org. Demand is supported by consumers who are already familiar with espresso, roast variation, and café-led quality signals. Germany, Italy, the United Kingdom, France, and the Netherlands continue to anchor regional consumption. France stands out as one of the faster-moving specialty markets as third-wave café culture extends beyond major city centers. This keeps Europe important not only as a large consumption base, but also as a region where quality expectations and sustainability claims are shaping the broader direction of the specialty coffee market.

Asia-Pacific is the fastest-growing region in the specialty coffee market, with an 8.03% CAGR projected through 2031. China is building coffee habits through both premium international chains and large convenience-led local formats, which is widening category familiarity at scale. Starbucks completed its joint venture with Boyu Capital in April 2026 and moved its China retail operations toward a licensed model, which is intended to accelerate expansion in lower-tier cities. India is the fastest-growing country in the region, while Japan, South Korea, Vietnam, and Indonesia each show different but meaningful stages of specialty adoption. South America and the Middle East and Africa also remain important to the specialty coffee market, with Brazil and Colombia shaping supply conditions and domestic demand, while Saudi Arabia and other urban Gulf markets continue to strengthen café-centered premium consumption.

Competitive Landscape

The specialty coffee market remains fragmented, with scale advantage concentrated more in distribution, systems, and branded reach than in any single dominant brand position. Nestlé, Starbucks, and JDE Peet’s remain important because they can fund innovation, manage broad retail relationships, and sustain visibility across multiple formats. Nestlé reported 7.3% organic growth in its coffee business in 2025, which shows that global incumbents are still expanding even in a volatile sourcing environment. Starbucks reported USD 9.5 billion in consolidated net revenue in Q2 FY2026, which highlights the continued power of branded coffee platforms with strong retail and digital engagement. At the same time, a long tail of independent roasters continues to define the specialty coffee market through local credibility, micro-lot sourcing, and roast transparency.

Strategic moves in 2025 and 2026 show that competition in the specialty coffee market is being shaped by format control, system access, and customer retention tools. Keurig Dr Pepper and Nestlé USA extended their Starbucks K-Cup partnership in April 2026, which strengthened one of the largest licensed pod ecosystems in North America. Lavazza’s June 2026 launch of Tablì in the United States was another important move because it challenged plastic-heavy single-serve systems with a new tab-based format. Starbucks also launched a redesigned three-tier loyalty structure in March 2026, which showed how digital retention and premium tiering are becoming more important in the specialty coffee market. These moves matter because taste alone is no longer enough to secure long-term advantage.

JDE Peet’s added another layer to the competitive picture by pairing brand focus with portfolio reshaping. Its July 2025 brand-led strategy centered investment around Peet’s, L’OR, and Jacobs, while productivity savings were meant to support reinvestment into growth drivers. The planned combination with Keurig Dr Pepper also points to a larger push toward system strength and broader household reach inside the specialty coffee market. This leaves meaningful room for mid-sized roasters that can offer specialty quality at more accessible price points without losing origin credibility.

Specialty Coffee Industry Leaders

-

Nestle S.A.

-

JDE Peet's N.V.

-

Luigi Lavazza S.p.A.

-

Keurig Dr Pepper Inc.

-

The J.M. Smucker Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Keurig Dr Pepper and Nestlé USA extended their strategic partnership for the manufacturing and distribution of Starbucks K-Cup pods in the US and Canada, adding new programs to expand distribution and innovation within the Keurig brewing system, reinforcing the licensed pod-retail ecosystem as a primary specialty revenue channel

- March 2026: Bulletproof introduced Coffee + Creatine, a first-of-its-kind functional coffee product that combines premium instant Arabica coffee with 5 grams of creatine monohydrate and 250 mg of electrolytes per serving.

- February 2026: M2 Ingredients introduced M2Brew™, a proprietary functional mushroom ingredient engineered specifically for brewed coffee formats, including drip coffee, coffee pods, pour-over systems, and foodservice applications. The ingredient is designed to ensure that bioactive mushroom compounds successfully pass through brewing filters and remain present in the finished beverage, addressing a longstanding challenge in the mushroom coffee category.

Global Specialty Coffee Market Report Scope

| Whole Bean Coffee |

| Ground Coffee |

| Instant Coffee |

| Coffee Pods and Capsules |

| Other Product Types |

| Conventional |

| Organic |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Channels | |

| Other Distribution Channels | |

| Foodservice |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Whole Bean Coffee | |

| Ground Coffee | ||

| Instant Coffee | ||

| Coffee Pods and Capsules | ||

| Other Product Types | ||

| Category | Conventional | |

| Organic | ||

| Distribution Channels | Retail | Supermarkets/Hypermarkets |

| Specialty Stores | ||

| Online Retail Channels | ||

| Other Distribution Channels | ||

| Foodservice | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of specialty coffee in 2026 and where is it heading by 2031?

The specialty coffee market stands at USD 37.36 billion in 2026 and is forecast to reach USD 52.06 billion by 2031 at a 6.86% CAGR.

Which product type is growing the fastest in specialty coffee?

Coffee pods and capsules are the fastest-growing product type, with a projected 7.65% CAGR through 2031, supported by home brewing demand and single-serve system expansion.

Why does instant coffee still lead revenue despite premium trends?

Instant coffee held 56.38% of 2025 revenue because it combines convenience, affordability, and broad access, while premium instant formats are narrowing the quality gap.

Which region leads demand and which one is growing the fastest?

North America led with 34.25% revenue share in 2025, while Asia-Pacific is projected to expand the fastest at an 8.03% CAGR through 2031.

Page last updated on: