Food And Beverage Processing Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

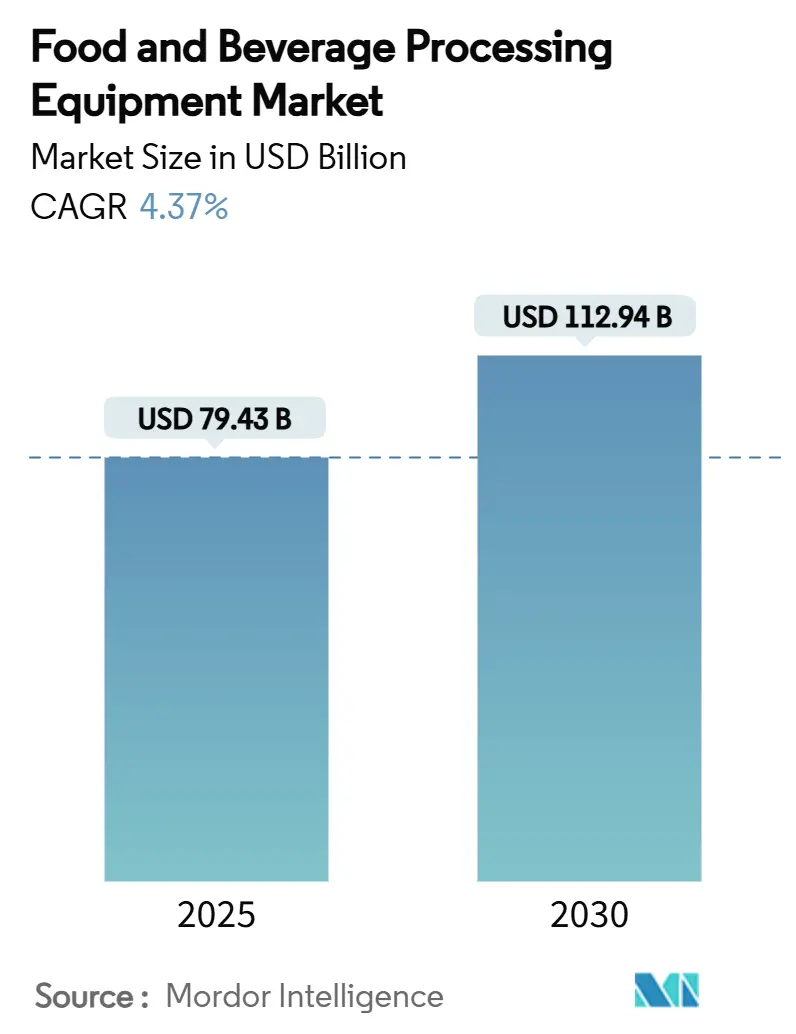

| Market Size (2025) | USD 79.43 Billion |

| Market Size (2030) | USD 112.94 Billion |

| Growth Rate (2025 - 2030) | 4.37% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food And Beverage Processing Equipment Market Analysis by Mordor Intelligence

The food and beverage processing equipment market size is anticipated to be valued at USD 79.43 billion in 2025 and is projected to reach USD 112.94 billion by 2030, advancing at a 4.37% CAGR through the period. Rising automation initiatives, sustainability mandates, and an expanding demand-supply gap for processed foods anchor this growth. Buyers are increasingly channeling their budgets towards smart systems, aiming for shorter payback periods, reduced operating costs, and adherence to stringent energy-efficiency targets. Suppliers adept in blending mechanical expertise with AI-driven diagnostics are gaining traction, particularly in areas grappling with labor shortages and stringent traceability regulations. While growth is widespread, there's a notable shift: Asia-Pacific's domestic producers are leaning towards mid-tier machinery, whereas North American and European processors are upgrading from legacy lines to premium solutions. Sustainability metrics, specifically kilowatts consumed per ton processed, have emerged as critical benchmarks for buyers, rivaling traditional metrics like throughput and uptime during tender evaluations.

Key Report Takeaways

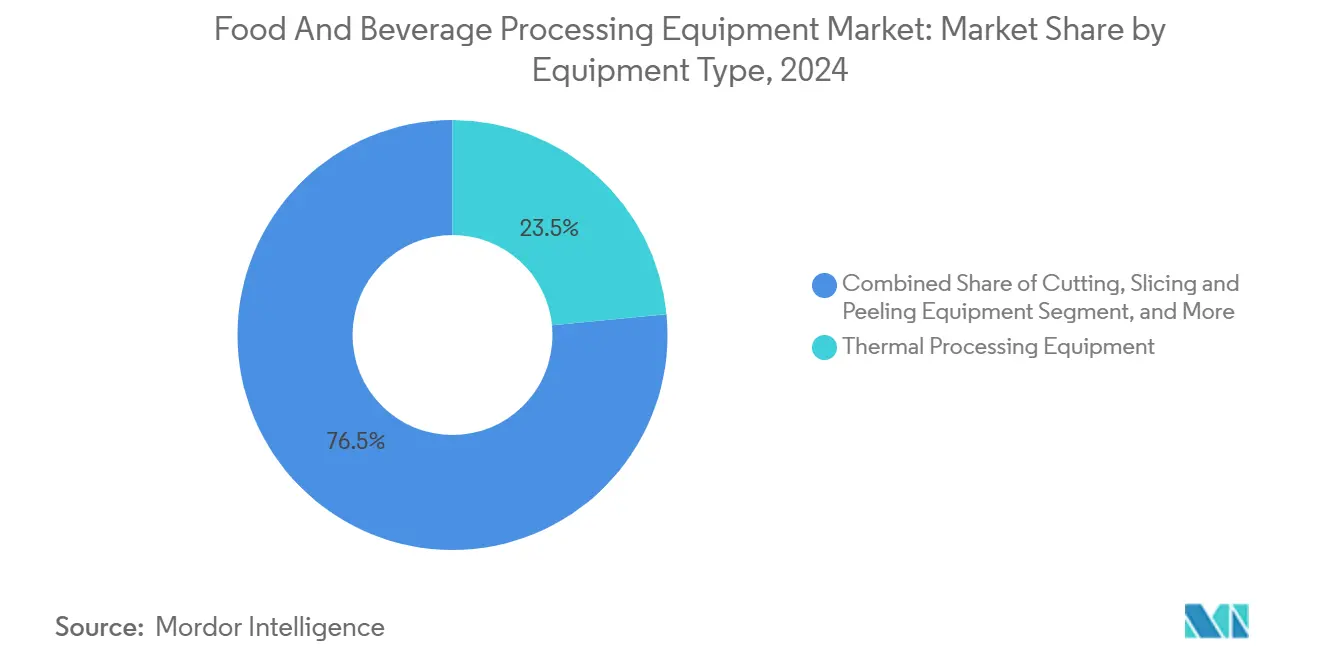

- By equipment type, thermal processing led with 23.46% revenue share in 2024; extrusion and forming is forecast to expand at an 8.86% CAGR to 2030.

- By mode of operation, semi-automatic systems held 71.39% of the food and beverage processing equipment market share in 2024, while fully automatic units record the highest projected CAGR at 7.54% through 2030.

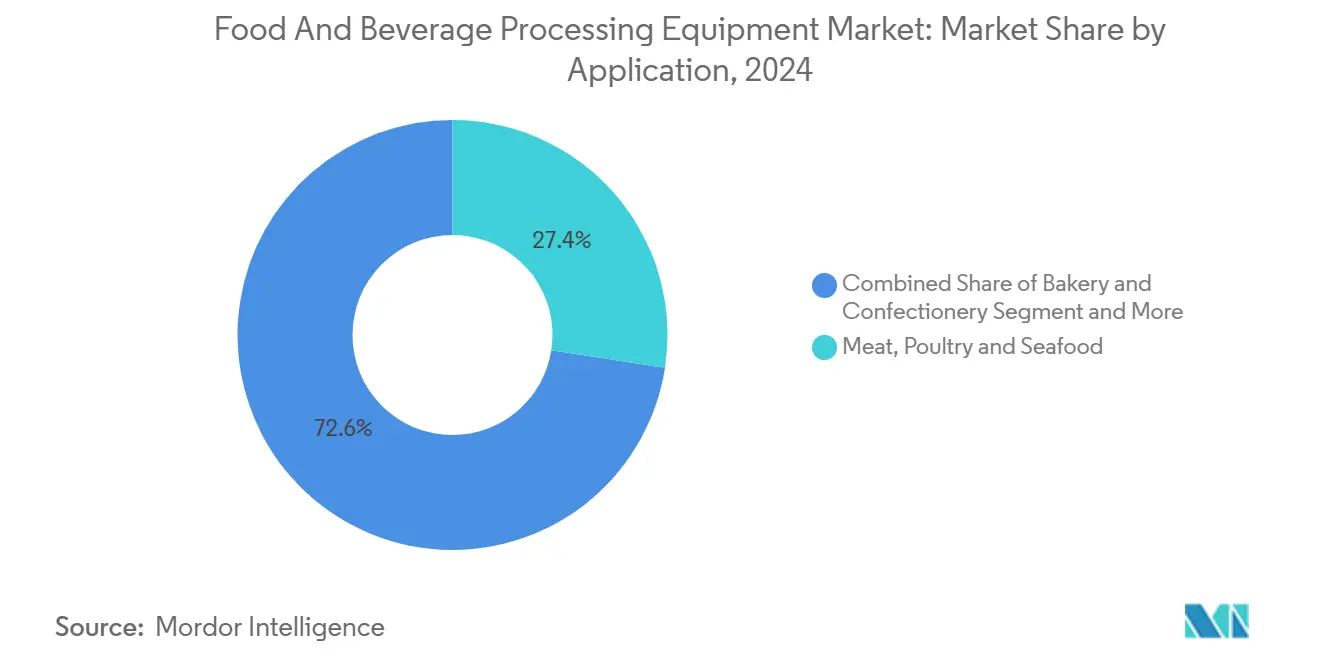

- By application, the meat, poultry, and seafood segment accounted for a 27.43% share of the food and beverage processing equipment market size in 2024, and plant-based proteins are advancing at a 9.35% CAGR through 2030.

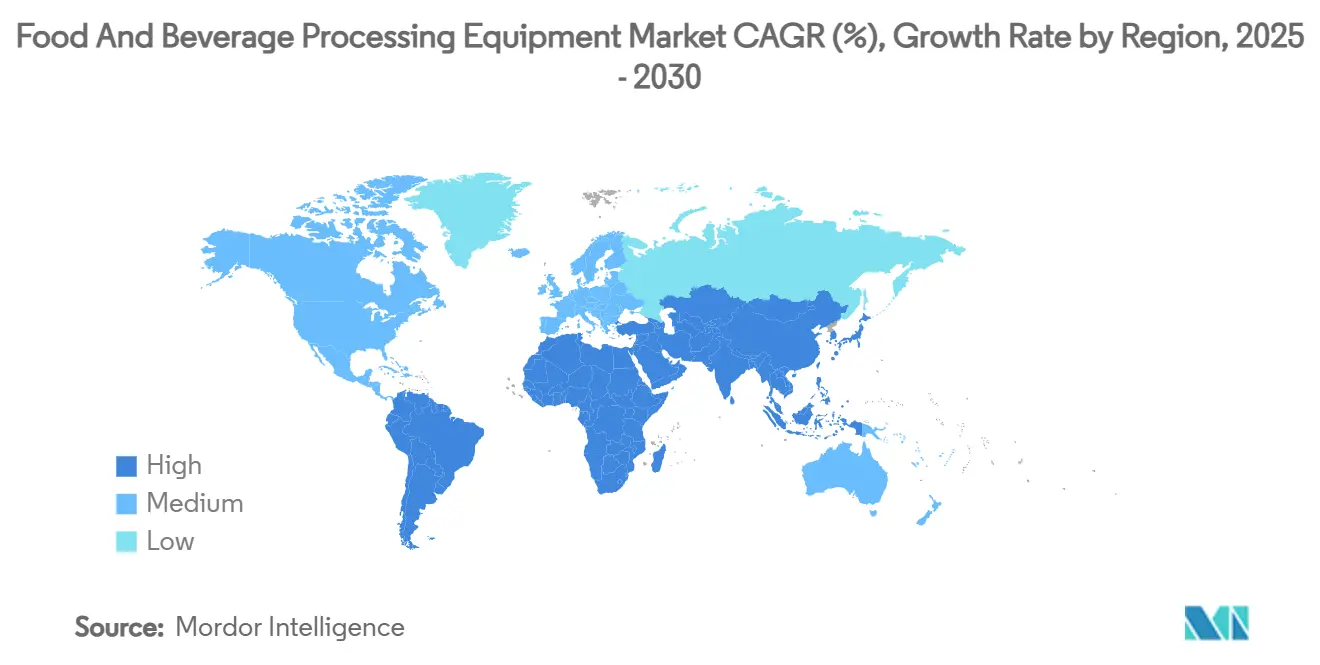

- By geography, Asia-Pacific commanded 34.75% of 2024 revenue; the Middle East and Africa food and beverage processing equipment market size is forecast to post an 8.14% CAGR to 2030.

Global Food And Beverage Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Automation and Smart Manufacturing | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid Expansion of Bakery and Confectionery Industry | +0.8% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Premiumisation of Infant-nutrition Products | +0.6% | Global, particularly developed markets | Long term (≥ 4 years) |

| Rising Demand for Clean-label Dairy Ingredients | +0.5% | North America and EU primary, expanding to APAC | Medium term (2-4 years) |

| Surge in Customised Melting-point Fractions for Laminated Doughs | +0.4% | Europe and North America | Short term (≤ 2 years) |

| Growth of Medium/Short-chain Enriched Milk fat for Metabolic-health SKUs | +0.3% | Developed markets globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Automation and Smart Manufacturing

Manufacturing executives are now seeing returns on automation investments in just 18 months, a significant shift from the traditional 3-year payback period. This change is reshaping capital allocation strategies throughout the industry. Studies from Dairy Processing highlight that AI-driven predictive maintenance systems have slashed unplanned downtimes by 50-75% and trimmed maintenance costs by as much as 35%[1]Source: Dairy Processing, “Dairy processors look to optimize operations with AI,” dairyprocessing.com. Meanwhile, in meat processing, 3D vision-equipped smart robots are making waves. They adjust in real-time to variations in animal sizes, optimizing yields and reducing reliance on labor, as reported by Food Engineering. The trend of collaborative robotics is especially evident in packaging and material handling. Here, flexible automation systems swiftly adapt to evolving product demands, sidestepping the need for extensive reprogramming. Furthermore, machine learning algorithms are making a mark by cutting quality variability by 65% and boosting processing throughput by up to 10%. These advancements not only offer cost benefits but also enhance product consistency and elevate customer satisfaction.

Rapid Expansion of Bakery and Confectionery Industry

Consumer demand for artisanal products at an industrial scale is driving the modernization of equipment in the bakery sector. This shift presents unique engineering challenges, favoring specialized processing solutions over generic machinery. Advanced mixing and blending equipment now boasts precision temperature control and atmospheric modification capabilities. These innovations help preserve delicate flavor compounds and ensure consistent texture profiles across large production runs. Manufacturers, leveraging extrusion technology tailored for laminated dough, can now craft croissants and pastries with customized melting-point fractions. This advancement enhances shelf stability without sacrificing sensory attributes, as noted by Food Engineering. Furthermore, the integration of IoT sensors across bakery production lines facilitates real-time monitoring of humidity, temperature, and dough consistency. This not only upholds product quality standards but also curtails waste by up to 15%. Automated packaging systems, now equipped with gentle handling mechanisms, are designed for delicate baked goods. These systems ensure product integrity while achieving throughput rates that manual operations previously deemed impossible.

Premiumization of Infant-nutrition Products

Driven by regulatory mandates for better traceability and nutritional accuracy, the infant formula industry is witnessing a technological overhaul, necessitating advanced processing equipment. High-pressure processing systems are now being embraced to safeguard heat-sensitive nutrients, marking a departure from traditional thermal methods that often compromise essential vitamins and proteins. According to the FDA, spray drying technology has advanced, now offering precise particle size control and encapsulation features, enhancing nutrient bioavailability and ensuring product stability over extended storage. The rise of blockchain-enabled traceability systems mandates that processing equipment seamlessly integrates with digital platforms, monitoring everything from ingredient sourcing to quality metrics throughout production. Furthermore, membrane filtration and separation tools, tailored for infant nutrition, now boast advanced cleaning-in-place systems, upholding rigorous hygiene standards and reducing cross-contamination risks.

Rising Demand for Clean-label Dairy Ingredients

Driven by the clean-label movement, dairy processors are now investing in equipment that delivers traditional functionality sans chemical additives. This shift has spurred a demand for cutting-edge separation and concentration technologies. As highlighted by Tetra Pak, membrane filtration systems are now being utilized to concentrate proteins and eliminate unwanted components without resorting to heat treatment[2]Source: Tetra Pak, “Factory Sustainable Solutions,” foodengineeringmag.com. This approach not only preserves the natural flavors but also the nutritional properties that consumers are increasingly prioritizing. Furthermore, non-thermal processing technologies, such as high-pressure processing and pulsed electric fields, are empowering dairy manufacturers to prolong shelf life while upholding a clean-label status. However, it's worth noting that the costs of this equipment are still considerably steeper than their conventional counterparts. Additionally, the adoption of enzyme-based processing systems facilitates the precise modification of dairy proteins without the need for synthetic additives. This process demands specialized equipment to ensure optimal enzyme activity is sustained throughout the processing cycles. Lastly, quality control systems that leverage real-time spectroscopic analysis are proving invaluable. They not only help processors confirm clean-label adherence but also ensure production efficiency. Yet, it's essential to recognize that such implementations come with significant investments in both equipment and the requisite operator training.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Butterfat Prices | -0.7% | Global, particularly impacting dairy-focused regions | Short term (≤ 2 years) |

| Consumer Perception of Saturated-fat Health Risks | -0.5% | North America and Europe primarily | Medium term (2-4 years) |

| Tightening Asian AMF Import Quotas | -0.4% | Asia-Pacific, with spillover effects globally | Medium term (2-4 years) |

| Competitive Encroachment from High-oleic Specialty Vegetable Fats | -0.3% | Global, concentrated in processed food applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Butterfat Prices

Food processors are increasingly investing in flexible equipment systems to navigate raw material price volatility. These systems can seamlessly switch between different fat sources without the need for extensive reconfiguration or compromising on quality. To implement real-time cost optimization algorithms, processing equipment must integrate with supply chain management systems. This integration allows for adjustments in formulations based on ingredient pricing fluctuations, all while upholding product specifications. Advanced blending systems now feature precision dosing capabilities. This innovation empowers manufacturers to tailor fat blend compositions in line with market conditions, thereby reducing their vulnerability to price swings of individual ingredients, as highlighted by Food Processing. In response, equipment manufacturers are crafting modular processing lines. These lines can swiftly adapt to various fat sources with minimal downtime, albeit at a higher initial capital investment. Furthermore, by embedding predictive analytics into processing equipment, manufacturers can foresee trends in raw material costs and adjust their production schedules. This foresight not only enhances operational flexibility but also cushions the blow from price volatility.

Consumer Perception of Saturated-fat Health Risks

As health consciousness rises, there's a growing demand for processing equipment that can produce reduced-fat products without sacrificing taste or texture. This trend presents technical challenges, pushing the industry towards innovative engineering solutions. Technologies for fat replacement, such as protein-based and fiber-enhanced systems, rely on specialized mixing and homogenization equipment. These tools are essential for achieving stable emulsions with alternative ingredients, as highlighted by the Annual Review of Food Science and Technology. Creating low-fat dairy products demands advanced separation technologies. These technologies selectively remove fat while maintaining protein functionality and sensory attributes. However, it's worth noting that the equipment for these advanced processes can be 40-60% pricier than traditional systems. Manufacturers are turning to texture modification equipment, like high-pressure homogenizers and ultrasonic processors. These tools allow the creation of mouthfeel characteristics typically linked to higher-fat products, even in reduced-fat formulations. Furthermore, to ensure the quality of these reduced-fat products, quality control systems need an upgrade. Monitoring texture, flavor, and stability becomes paramount, necessitating additional analytical equipment and enhanced process monitoring. This evolution inevitably adds complexity and cost to the overall system.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Thermal Processing Drives Innovation

In 2024, thermal processing equipment, which includes pasteurizers and cookers, commands a leading 23.46% market share. However, as the industry pivots towards energy-efficient and sustainable technologies, the competitive landscape is undergoing significant shifts. By integrating heat recovery systems and sophisticated temperature control algorithms, processors have slashed energy consumption by up to 50%, all while upholding food safety standards[3]Source: CIMCO Refrigeration, “Decarbonizing Food Processes with Industrial Heat Pumps,” cimcorefrigeration.com. This achievement not only underscores the importance of energy efficiency but also presents a compelling ROI, hastening equipment replacement cycles. Meanwhile, the extrusion and forming equipment segment is on a rapid ascent, projected to grow at an 8.86% CAGR through 2030. This surge is largely fueled by innovations in plant-based protein processing, which demand specialized texturization capabilities. Notably, high-moisture extrusion technology is pivotal in crafting meat-like textures for alternative protein products, boasting impressive throughput capabilities of 400 kg per hour for commercial use.

AI-driven vision systems are revolutionizing cutting, slicing, and peeling equipment, especially in produce processing. These systems optimize yield and minimize waste, addressing challenges posed by traditionally irregular shapes. In the realm of dicing, grinding, and milling, precision particle size control is paramount, allowing manufacturers to maintain consistent texture profiles across a wide array of products. Mixing and blending systems have advanced, now boasting atmospheric control features that safeguard delicate ingredients while ensuring uniform distribution – a crucial factor for clean-label formulations. The evolution of homogenizing and emulsifying equipment is noteworthy, as it now adeptly manages intricate plant-based formulations, fine-tuning processing parameters to secure stable emulsions. Membrane filtration and separation equipment is witnessing a surge in dairy and beverage sectors, capitalizing on the selective concentration of beneficial compounds to craft premium products. Furthermore, the integration of IoT connectivity and predictive maintenance across all equipment types is unlocking new service revenue streams, enhancing the traditional equipment sales model.

By Mode of Operation: Automation Acceleration

In 2024, semi-automatic systems hold a commanding 71.39% share of the market. This dominance highlights the industry's adeptness at balancing operational flexibility with labor cost management. However, it also conceals a significant and accelerating shift towards full automation, outpacing traditional adoption curves. Fully automatic systems, buoyed by persistent labor shortages—now at crisis levels in pivotal manufacturing regions, especially where food processing unemployment rates flirt with historic lows—are set to expand at a robust 7.54% CAGR through 2030. In developed markets, the shift from manual to semi-automatic operations is largely complete[4]Source: ProFood World, “Addressing the Workforce Crisis in Food Processing,” profoodworld.com. Yet, some manual processes remain, nestled in specialized applications that demand human dexterity and judgment—qualities current robotics struggles to replicate cost-effectively.

As reported by Food Manufacturing, the economics of automation have undergone a seismic shift. Collaborative robots now boast payback periods of under 12 months in high-volume settings. Simultaneously, cutting-edge machine learning algorithms empower automated systems to seamlessly adapt to product variations, sidestepping the need for extensive reprogramming. Semi-automatic systems are now weaving in AI-assisted decision support tools, bolstering operator efficiency while ensuring human oversight in quality-critical processes. Manual operations still thrive in artisanal and small-batch productions, where the need for flexibility and customization trumps labor cost concerns. Yet, even these sectors are embracing automated systems for quality control and packaging. Furthermore, augmented reality training systems are bridging skill gaps in operating automated equipment. This integration not only accelerates workforce adaptation to emerging technologies but also curtails training expenses and enhances safety outcomes.

By Application: Plant-based Proteins Transform Processing

The meat, poultry, and seafood segment holds 27.43% market share in 2024. The plant-based and alternative proteins segment presents substantial growth potential, with a projected CAGR of 9.35% through 2030. This growth is driven by advancing processing technologies and increasing consumer adoption. According to GEA, manufacturers are modifying traditional protein processing equipment to handle plant-based materials, which require specific processing parameters to achieve desired textures and flavors. The integration of precision fermentation and cell cultivation technologies is generating new equipment categories that merge bioreactor capabilities with conventional food processing functions.

Dairy processing equipment incorporates membrane filtration systems to concentrate functional proteins and bioactive compounds, supporting clean-label trends and premium product development. In bakery and confectionery, advanced mixing technologies maintain flavor compounds while ensuring consistent textures in large-scale production. Non-alcoholic beverage processing utilizes cold-processing technologies to extend shelf life and preserve nutrients without heat treatment. The frozen food sector implements cryogenic and impingement freezing systems to minimize ice crystal formation and maintain product quality. Ready meals production requires versatile processing lines that handle multiple ingredients and packaging formats. Baby food and infant formula manufacturing employs precise processing controls and automated monitoring systems. The nutraceuticals and functional foods segment requires specialized equipment to maintain bioactive compounds while meeting safety and stability requirements.

Geography Analysis

Asia-Pacific holds a dominant 34.75% share of the food and beverage processing equipment market in 2024. This leadership position stems from rapid industrialization and urbanization that are transforming food production systems across the region. India's food processing industry has received significant foreign direct investment since 2000, supported by the government's 'Make in India' initiative. In Japan, food processing companies are investing in automation and quality control systems to address rising labor costs. The region's expansion continues through increasing consumer demand for processed and convenience foods, particularly in urban areas with growing disposable incomes.

The Middle East and Africa region is projected to grow at 8.14% CAGR through 2030. In Saudi Arabia, Balady Poultry Trading Co. demonstrates this growth with a SAR 1.14 billion investment in new processing facilities, set to increase production capacity by 200 million birds annually, according to Wattagnet. Africa presents substantial opportunities, with UNCTAD identifying over USD 1.8 billion in potential export value within the African Continental Free Trade Area. Nigeria, Egypt, and Morocco are developing food processing infrastructure as part of their economic diversification plans to reduce reliance on raw commodity exports.

North America and Europe represent mature markets where equipment upgrades are driven by efficiency improvements and regulatory compliance. The United States food processing sector shows increasing consolidation, favoring larger operators who can invest in automated systems, while FDA regulatory changes require enhanced traceability systems. European markets emphasize energy-efficient processing technologies to meet carbon reduction requirements, particularly through heat pump systems and renewable energy integration. The region's commitment to circular economy principles drives innovations in waste reduction and byproduct valorization. South America displays varied growth patterns, with Brazil and Argentina expanding agricultural processing capacity while smaller economies focus on value-added processing to minimize commodity price exposure.

Competitive Landscape

The food and beverage processing equipment market is moderately fragmented, presenting significant consolidation opportunities. As technology becomes more complex and capital-intensive, larger players with the capacity for sustained R&D investments and expansive global service networks are gaining an edge. Industry leaders like GEA Group, Tetra Laval, Buhler Holding AG, The Middleby Corporation (Baker Perkins), and JBT Corporation are shifting their focus. Instead of competing mainly on price, they're emphasizing AI-driven process optimization, energy efficiency, and holistic automation solutions. This strategy not only differentiates them but also allows them to command premium pricing for their advanced offerings.

Competitive dynamics are evolving, with a noticeable tilt towards technology partnerships and acquisitions. A case in point is JBT Corporation's acquisition of Marel, which underscores the trend of melding complementary capabilities to offer richer value propositions. As food processors grapple with the dual challenge of minimizing environmental impact and ensuring operational efficiency, there's a pronounced shift towards sustainability and circular economy solutions. Notably, there's a gap in the market: specialized processing equipment tailored for alternative proteins and personalized nutrition. Here, traditional manufacturers find themselves at a disadvantage, lacking both the necessary expertise and established customer ties.

New entrants, particularly from the realms of robotics and AI software, are making waves. By forging alliances with seasoned equipment manufacturers, they're infusing the market with cutting-edge automation, enhancing the traditional mechanical engineering landscape. Digital twin technology and predictive analytics are emerging as pivotal differentiators. Companies are channeling significant investments into software capabilities, aiming to boost equipment performance and curtail ownership costs. As equipment becomes more intricate, the importance of service revenue models is surging. Customers, keen on ensuring uninterrupted operations, are gravitating towards comprehensive maintenance contracts, especially those that offer remote monitoring and predictive maintenance features.

Food And Beverage Processing Equipment Industry Leaders

GEA Group

JBT Corporation

Tetra Laval

The Middleby Corporation (Baker Perkins)

Buhler Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Chobani breaks ground on USD 1.2 billion dairy processing plant in Rome, NY, with capacity to process 12 million pounds of milk daily, representing one of the largest food processing facility investments in recent years.

- February 2025: Nestlé USA announces over USD 675 million investment in new beverage processing facility in Arizona for creamer production, demonstrating continued capacity expansion in high-growth product categories.

- February 2025: Agristo invests USD 450 million in new processing facility in Grand Forks, ND, highlighting significant foreign investment in US food processing infrastructure.

- January 2025: JBT Corporation finalizes acquisition of Marel, creating JBT Marel Corporation and expanding capabilities in food processing equipment through strategic consolidation.

Global Food And Beverage Processing Equipment Market Report Scope

| Cutting, Slicing and Peeling Equipment |

| Dicing, Grinding and Milling Equipment |

| Mixing and Blending Equipment |

| Extrusion and Forming Equipment |

| Thermal Processing Equipment (Pasteurizers, Cookers) |

| High-pressure and Other Non-thermal Processing Equipment |

| Homogenizing and Emulsifying Equipment |

| Membrane Filtration and Separation Equipment |

| Drying, Dehydration and Evaporation Equipment |

| Mechanical Conveying and Handling Systems |

| Cleaning, Sanitization and CIP Systems |

| Auxiliary Pumps, Valves and Fittings |

| Others |

| Manual |

| Semi-automatic |

| Fully Automatic |

| Meat, Poultry and Seafood |

| Bakery and Confectionery |

| Dairy Products |

| Non-alcoholic Beverages |

| Alcoholic Beverages |

| Fruit and Vegetable Products |

| Snacks and Savory Products |

| Frozen Foods |

| Ready Meals and Convenience Foods |

| Plant-based and Alternative Proteins |

| Baby Food and Infant Formula |

| Nutraceuticals and Functional Foods |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Equipment Type | Cutting, Slicing and Peeling Equipment | |

| Dicing, Grinding and Milling Equipment | ||

| Mixing and Blending Equipment | ||

| Extrusion and Forming Equipment | ||

| Thermal Processing Equipment (Pasteurizers, Cookers) | ||

| High-pressure and Other Non-thermal Processing Equipment | ||

| Homogenizing and Emulsifying Equipment | ||

| Membrane Filtration and Separation Equipment | ||

| Drying, Dehydration and Evaporation Equipment | ||

| Mechanical Conveying and Handling Systems | ||

| Cleaning, Sanitization and CIP Systems | ||

| Auxiliary Pumps, Valves and Fittings | ||

| Others | ||

| Mode of Operation | Manual | |

| Semi-automatic | ||

| Fully Automatic | ||

| Application | Meat, Poultry and Seafood | |

| Bakery and Confectionery | ||

| Dairy Products | ||

| Non-alcoholic Beverages | ||

| Alcoholic Beverages | ||

| Fruit and Vegetable Products | ||

| Snacks and Savory Products | ||

| Frozen Foods | ||

| Ready Meals and Convenience Foods | ||

| Plant-based and Alternative Proteins | ||

| Baby Food and Infant Formula | ||

| Nutraceuticals and Functional Foods | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the food and beverage processing equipment market?

The food and beverage processing equipment market is valued at USD 79.43 billion in 2025.

Which region generates the highest demand for equipment?

Asia-Pacific leads with 34.75% of global revenue thanks to rapid industrialization and supportive government incentives.

Which equipment segment is growing fastest?

Extrusion and forming equipment, propelled by plant-based protein production, is advancing at an 8.86% CAGR to 2030.

How quickly are fully automatic lines being adopted?

Fully automatic systems are projected to grow at a 7.54% CAGR as processors seek labor savings and quality consistency.

Page last updated on: