Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

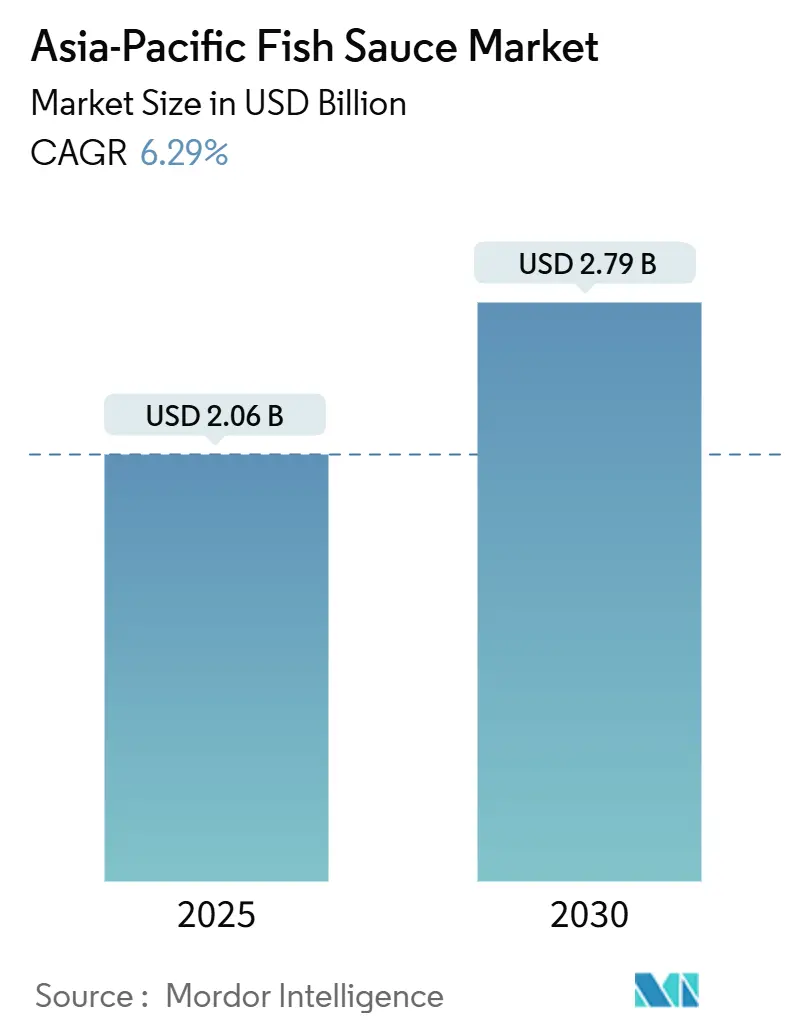

| Market Size (2025) | USD 2.06 Billion |

| Market Size (2030) | USD 2.79 Billion |

| Growth Rate (2025 - 2030) | 6.29% CAGR |

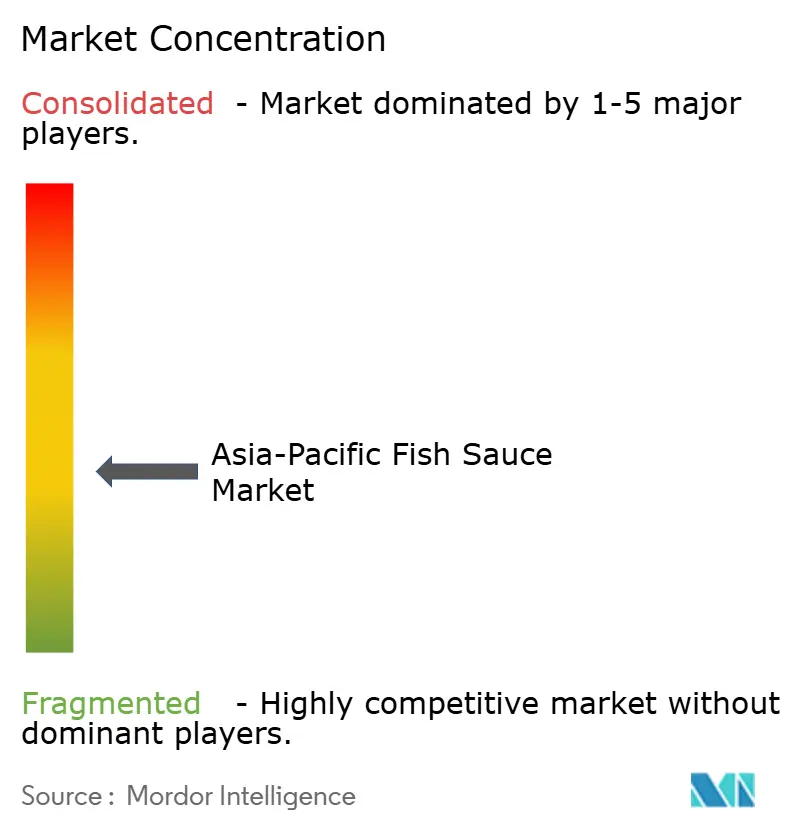

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Fish Sauce Market Analysis by Mordor Intelligence

The Asia-Pacific fish sauce market was valued at USD 2.06 billion in 2025 and is projected to reach USD 2.79 billion by 2030, registering a compound annual growth rate (CAGR) of 6.29%. This growth underscores the significance of fish sauce in regional diets and its growing presence in packaged food products. The market's steady expansion is driven by consistent seafood availability in countries like Vietnam and China, government initiatives to modernize fisheries, and a strong consumer preference for umami-rich flavours. These flavours not only enhance the taste of food but also reduce cooking time, making them popular in snacks and quick-service meals. In terms of flavour profiles, manufacturers are introducing differentiated variants to attract convenience-focused consumers. The demand for organic-certified fish sauce is opening up opportunities in the premium segment, as health-conscious buyers seek high-quality options. The market remains moderately fragmented, with national brands maintaining strong local loyalty. However, production processes are becoming more industrialized.

Key Report Takeaways

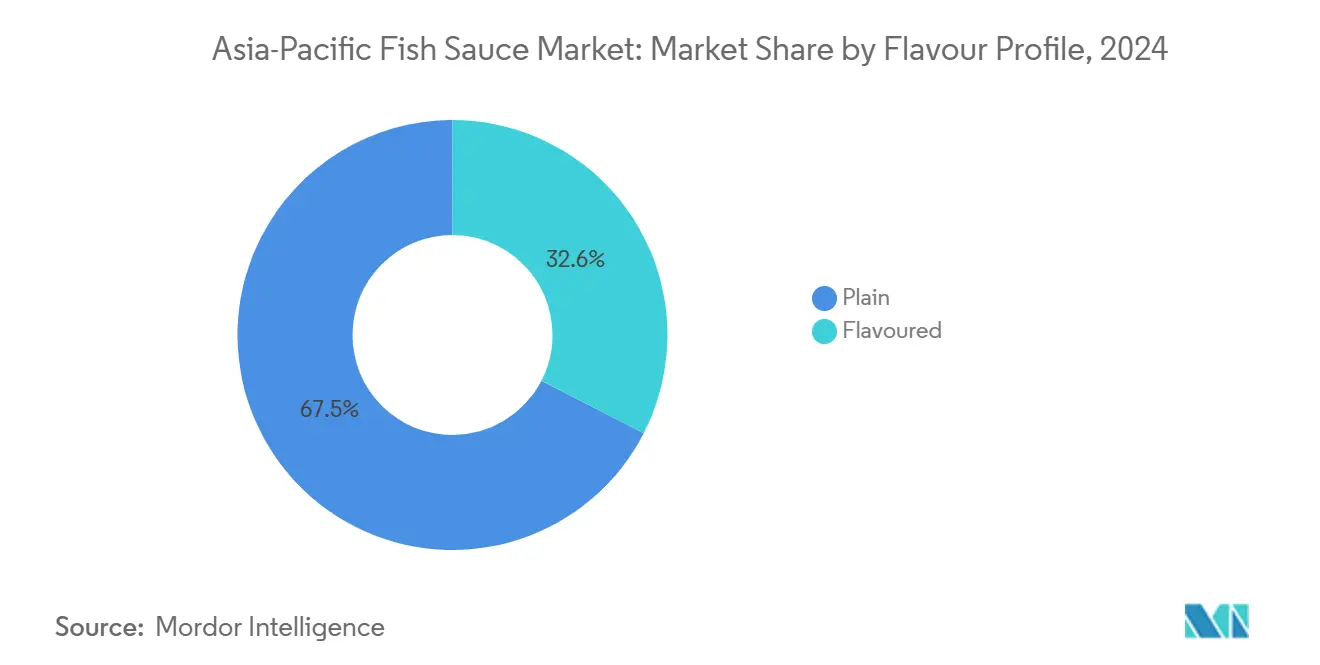

- By flavour profile, plain fish sauce accounted for 67.45% of the Asia-Pacific fish sauce market share in 2024, while flavoured variants are projected to expand at a 7.54% CAGR through 2030.

- By category, conventional products accounted for 85.73% of the Asia-Pacific fish sauce market size in 2024, whereas organic lines are forecast to grow at an 8.35% CAGR between 2025 and 2030.

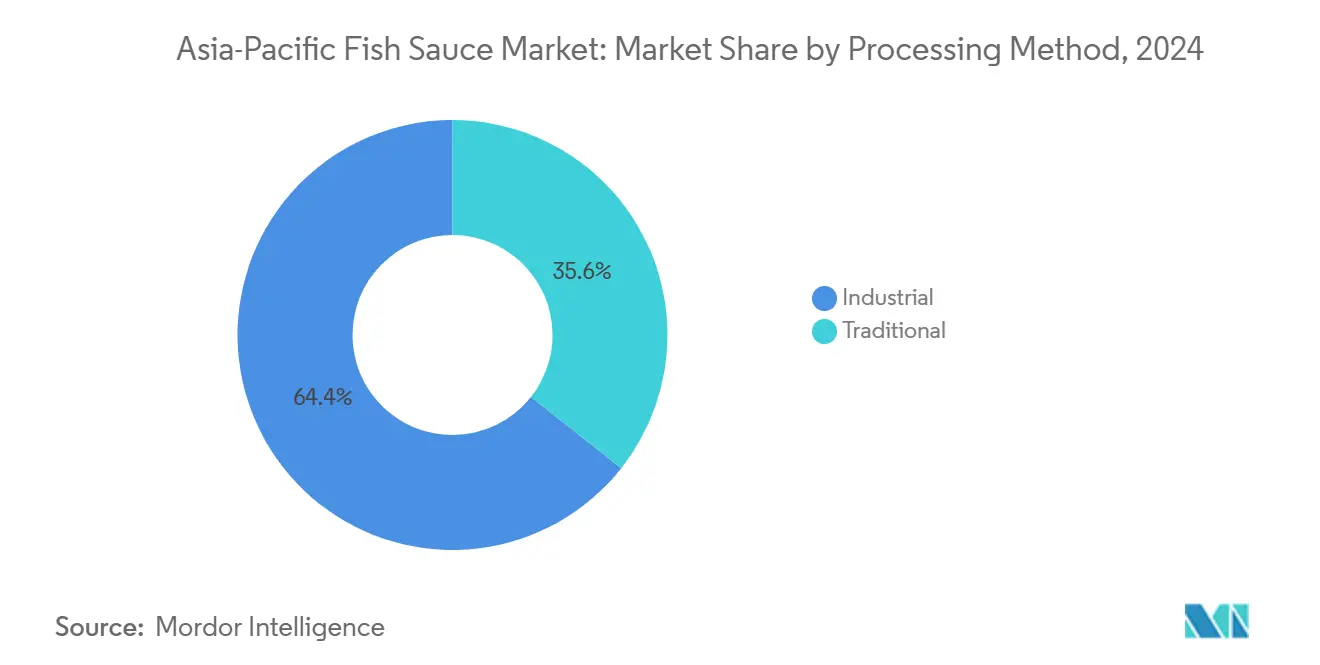

- By processing method, industrial output accounted for a 64.36% share of the Asia-Pacific fish sauce market size in 2024, while traditional fermentation is expected to advance at an 8.28% CAGR through 2030.

- By distribution channel, retail captured a 45.73% revenue share in 2024, and the horeca sector is expected to grow at a 7.65% CAGR through 2030.

- By country, China led the Asia-Pacific fish sauce market with a 36.91% share in 2024, and Vietnam is the fastest-growing market, projected to grow at a 7.83% CAGR to 2030.

Asia-Pacific Fish Sauce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong intergenerational consumption habits support consistent demand for fish | +1.2% | Vietnam, Thailand, Philippines, China (coastal provinces) | Long term (≥ 4 years) |

| Rising popularity of fermented foods for their umami profile | +1.5% | Concentration in Japan, South Korea, urban China | Medium term (2-4 years) |

| Increasing demand from quick-service Asian cuisine chains | +1.3% | Concentration in Singapore | Medium term (2-4 years) |

| Rising popularity of home cooking and culinary experimentation | +0.9% | Accelerated in India, Indonesia, Malaysia | Short term (≤ 2 years) |

| Increasing use of fish sauce as a flavour enhancer in non-traditional dishes | +0.8% | Early adoption in Asia-Pacific | Medium term (2-4 years) |

| Government support for fisheries and food processing industries | +0.6% | Vietnam, Thailand, Indonesia, Philippines, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong intergenerational consumption habits support consistent demand for fish sauce

Traditional food habits passed down through generations continue to drive steady demand for fish sauce in the Asia-Pacific region. This is particularly noticeable in countries like Vietnam, Thailand, and the Philippines, where fish sauce is a key ingredient in everyday cooking and is viewed as a necessity rather than an optional item. Families often stick to trusted brands, creating strong brand loyalty and ensuring consistent purchases over time. Moreover, with increasing urbanization, manufacturers are adapting by offering more convenient packaging and smaller sizes to suit modern lifestyles and compact kitchens. In India, the rising consumption of seafood is further fueling the demand for fish-based seasonings. Fish consumption in the country is expected to almost double, reaching 26.50 million metric tons by 2047–2048, with annual per capita consumption projected to grow to 16.07 kg as per Global Seafood Alliance[1]Source: Global Seafood Alliance, "Fish consumption in India projected to double by 2048", globalseafood.org. This growing trend indicates a widening consumer base, presenting significant opportunities for fish sauce producers to expand their market presence as more households incorporate it into their cooking habits.

Increasing demand from quick-service Asian cuisine chains

The growth of quick-service Asian cuisine chains is driving consistent demand for fish sauce, as these chains rely on it to maintain uniform flavours across their menus. Many large operators now use centralized purchasing systems, focusing on suppliers that can provide full traceability and meet food safety standards like Food Safety System Certification (FSSC) 22000[2]Source: Food Safety System Certification, "Providing Trust and Impact for Global Food Safety with FSSC 22000", fssc.com. This trend is shifting sourcing away from small, traditional producers toward larger, industrial-scale manufacturers that can meet these requirements. Institutional buyers are increasingly opting for bulk packaging, such as 10-liter and 20-liter drums, to support high-volume kitchens and reduce handling costs. While some quick-service chains are experimenting with fish sauce in fusion dishes, its primary use remains in traditional recipes. This highlights its importance as a reliable ingredient in kitchen operations rather than as a trendy or experimental flavour addition.

Rising popularity of fermented foods for their umami profile

The growing popularity of fermented foods is driving the increased acceptance of fish sauce as a natural source of umami. Once primarily used in ethnic cuisines, fish sauce is now gaining recognition in mainstream cooking and health-focused diets. Research has shown that fermentation microbes, such as Tetragenococcus halophilus and Lactiplantibacillus plantarum, play a significant role in producing natural glutamates, which enhance flavour. This has allowed brands to highlight the clean and naturally derived qualities of their products. Consumers are becoming more conscious of product labels. For instance, a survey conducted in Indonesia in March 2025 revealed that 13% of consumers actively check nutrition information on packaged foods, as per PubMed Central[3]Source: PubMed Central, "Indonesian Adolescents’ Perceptions of Front-of-Package Labels on Packaged Food and Drinks", pmc.ncbi.nlm.nih.gov. This trend highlights the importance of clear labeling, including details about fermentation processes, ingredients, and the absence of artificial additives, in order to meet consumer demand for transparency and trust in food products.

Rising popularity of home cooking and culinary experimentation

Home cooking plays a significant role in increasing the use of fish sauce, as many families continue to prepare meals at home on a regular basis. This trend is further supported by a growing interest in experimenting with different cuisines and flavours. For instance, a February 2023 survey in Japan revealed that 60% of people living with their families cooked at home 3-4 days a week, according to the PubMed Central[4]Source: PubMed Central, "Associations between Cooking at Home and Nutrient and Food Group Intake among Female University Students: A Cross-Sectional Analysis on Living Arrangements", pmc.ncbi.nlm.nih.gov. This consistent engagement with home-cooked meals drives the demand for staple seasonings like fish sauce. Social media platforms and online cooking content are expanding the ways fish sauce is used, introducing it in recipes beyond traditional Asian dishes. Premium and specialty brands are capitalizing on this trend by offering smaller trial packs and emphasizing the unique origins of their products to attract consumers. Furthermore, flavoured and low-odor variants are being introduced to make fish sauce more appealing to new users, particularly in markets like Australia and New Zealand, where it is less commonly used.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong odor associated with fish sauce limits acceptance | -0.7% | Particularly acute in non-Asian markets (Australia, New Zealand, urban India) | Medium term (2-4 years) |

| Availability of alternative seasonings such as soy sauce, oyster sauce, and synthetic flavour enhancers | -0.9% | Highest substitution in China, Japan, South Korea | Long term (≥ 4 years) |

| High sodium content raises health concerns and discourages consumption | -1.1% | Singapore, Australia, New Zealand, urban China, South Korea | Short term (≤ 2 years) |

| Growing preference for plant-based and vegan diets | -0.5% | Led by urban centers in India, Singapore, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong odor associated with fish sauce limits acceptance

The strong smell of fish sauce remains a challenge for gaining acceptance among consumers who are not accustomed to fermented seafood products. While regular users often view the strong aroma as a sign of authenticity and high quality, many consumers, especially in Western-leaning households and newer markets, find the smell off-putting. This hesitation impacts both initial trials and repeat purchases. To address this issue, manufacturers are introducing milder versions of fish sauce, creating blends infused with citrus flavours, and utilizing innovative packaging, such as activated-carbon vent caps, to minimize odor release while maintaining the product's signature taste. Retailers are also promoting the product by offering small trial-size bottles placed near familiar condiments, such as soy sauce, to encourage consumers to experiment. However, a lack of awareness about how to use fish sauce and manage its aroma continues to limit its broader adoption in the Asia-Pacific market.

High sodium content raises health concerns and discourages consumption

High salt levels in traditional fish sauce pose a significant challenge, as both health authorities and consumers are growing increasingly concerned about sodium intake. Traditional fish sauce recipes rely heavily on salt, which has led to stricter regulations, including enhanced front-of-pack labeling and sodium reduction policies by governments. To address these concerns, manufacturers are adopting advanced processing techniques, such as membrane filtration and enzymatic hydrolysis. These methods aim to reduce sodium content while maintaining the rich umami flavour that defines fish sauce. However, this reformulation comes with risks. Many loyal consumers are highly sensitive to changes in taste, and even small reductions in salt can make the product feel less authentic. Public health studies in emerging markets continue to emphasize that condiments, including fish sauce, are significant contributors to daily sodium intake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavour Profile: Differentiated Variants Capture Convenience-Seeking Buyers

Plain fish sauce remains the leading product in the Asia-Pacific fish sauce market in 2024, contributing 67.45% of total sales. Its popularity stems from its essential role in traditional regional cuisines, such as pho in Vietnam, som tam in Thailand, and sinigang in the Philippines. Consumers continue to prefer plain fish sauce for its authentic flavour and versatility in cooking. This strong demand is consistent across both households and the foodservice sector, ensuring steady sales despite challenges such as price fluctuations and regulatory changes. Plain fish sauce is widely available in both traditional markets and modern retail outlets, further supporting its dominance.

On the other hand, flavoured fish sauce is gaining traction and is expected to grow at a 7.54% CAGR from 2025 to 2030 as consumer preferences evolve and diversify. These variants are particularly appealing to younger and urban consumers who seek convenience and unique taste profiles, such as garlic, chili, or citrus-infused options. Flavoured fish sauce is expected to grow, driven by product innovation and targeted marketing strategies. Smaller packaging sizes and tailored positioning are helping these products attract new users, including those less familiar with traditional fish sauce. This growing interest is expanding the category beyond its traditional consumer base, contributing to its rising popularity in the market.

By Category: Organic Certification Unearths Premium Windows

Conventional production remains the largest segment in the Asia-Pacific fish sauce market in 2024, contributing 85.73% of the total volume. This dominance is attributed to its affordability and long-standing manufacturing practices. Countries like China, Thailand, and Indonesia benefit from strong supply chains and extensive distribution networks, ensuring that conventional fish sauce is widely available at competitive prices. It is particularly favored by mass-market consumers and foodservice operators who prioritize cost efficiency and consistent supply. Despite the rising interest in premium alternatives, conventional production remains the foundation of the market due to its scalability and accessibility.

Organic fish sauce is projected to grow at a CAGR of 8.35% through 2030 as consumers increasingly prefer healthier and more sustainable options. The segment is projected to grow, driven by regulatory agreements with regions like the European Union and Canada that streamline certification and export processes. These agreements encourage producers to adopt organic fermentation techniques and invest in high-quality production methods. Organic fish sauce is particularly appealing to health-conscious consumers and brands targeting premium export markets, especially in developed countries where demand for clean-label and sustainable products is on the rise.

By Processing Method: Traditional Fermentation Retains Aspiration Value

In 2024, industrial processing methods accounted for 64.36% of the total fish sauce production, primarily due to their efficiency and ability to ensure consistent quality. These methods shorten the fermentation and maturation period from the traditional 12–18 months to about six months, enabling faster production cycles. This efficiency enables producers to manage resources more effectively and cater to large-scale buyers, such as hotels, restaurants, and catering (HoReCa) businesses, which require consistent taste and controlled sodium levels. As a result, industrial processing continues to dominate the fish sauce supply for both retail and foodservice sectors.

Traditional production methods are expected to grow at a CAGR of 8.28% between 2025 and 2030, driven by increasing consumer demand for authentic and culturally rich products. Many consumers, including tourists and online shoppers, prefer fish sauce made using traditional techniques, as it often carries a regional identity and artisanal value. The longer natural fermentation process used in traditional methods enhances the flavour, creating a deeper and more complex taste. Studies have shown that this process results in higher natural glutamate levels, which appeal to consumers seeking premium and flavourful options. This combination of authenticity and superior taste allows traditional producers to carve out a niche in the premium segment of the market.

By Distribution Channel: HoReCa Surge Mirrors QSR Roll-Out

In 2024, retail outlets, including supermarkets, hypermarkets, and convenience stores, contributed 45.73% of the total fish sauce revenue. This dominance is due to the widespread use of fish sauce in households and its regular inclusion in grocery shopping. The growing popularity of online grocery platforms has further boosted retail sales, as consumers increasingly purchase essential condiments online. The availability of smaller pack sizes and multipack options has encouraged repeat purchases, especially in urban and semi-urban areas. Retail channels continue to be the primary drivers of both sales volume and value in the fish sauce market.

The HoReCa (Hotels, Restaurants, and Catering) segment is expected to grow at a 7.65% CAGR through 2030, fueled by the expansion of regional restaurant chains and quick-service outlets. Many foodservice operators are now collaborating with certified distributors, such as Dusit Foods and Green House Japan, to ensure a consistent supply of high-quality fish sauce. Bulk packaging, such as 20-liter drums, is preferred in this segment as it enhances operational efficiency and ensures uniform flavour in dishes. Furthermore, adherence to food safety standards, such as FSSC 22000, is driving a shift toward organized and contract-based sourcing, making the HoReCa channel a significant growth area for the fish sauce market.

Geography Analysis

China was the largest market for fish sauce in the Asia-Pacific region in 2024, accounting for 36.91% of the market share. This dominance is due to its large-scale production capabilities, abundant aquatic resources, and extensive distribution networks. While consumption growth in China is relatively slow, domestic producers maintain strong sales by offering a wide range of condiments and leveraging their nationwide retail presence. However, smaller producers are struggling to keep up with rising costs related to reformulation and regulatory compliance, leading to a market shift favoring larger, well-funded companies.

Vietnam is the fastest-growing market in the region, with a projected CAGR of 7.83%. The country’s growth is driven by its strong export potential and the increasing demand for premium fish sauce products. Vietnamese fish sauce is highly regarded internationally for its quality, particularly for products tied to specific regions of origin. Producers in Vietnam benefit from integrated supply chains and multiple manufacturing facilities, which ensure consistent production and quality. These advantages allow Vietnamese companies to meet growing export demand while staying competitive in domestic and neighboring markets.

Thailand, Indonesia, and the Philippines are important contributors to the regional fish sauce supply, supported by their established fishing industries and improving food safety regulations. The expansion of modern retail outlets and foodservice channels in these countries is also boosting demand. In Japan and South Korea, fish sauce remains a complementary seasoning to traditional soy-based condiments, maintaining its cultural significance. Meanwhile, developed markets like Singapore, Australia, and New Zealand are seeing gradual growth due to stricter sodium regulations and increased interest from immigrant communities. India is emerging as a promising market, where rising incomes and exposure to global cuisines are encouraging consumers to try fish sauce, although the market is still in its early stages.

Competitive Landscape

The Asia-Pacific fish sauce market is moderately fragmented, with competition driven by a mix of domestic producers and exporters focusing on premium products. Key players in the region include Masan Group, Thai Fishsauce Factory (Squid Brand) Co., Ltd., Mega Chef Brand, Pantainorasingh Manufacturer Co., Ltd., and Red Boat Fish Sauce. These companies cater to a diverse range of consumers, from those seeking affordable options to those who prefer high-quality, premium products. Vietnam and Thailand are the main centers of competition due to their strong cultural connection to fish sauce and the deep loyalty of local consumers. The presence of numerous regional brands ensures that no single company dominates the market entirely, maintaining a balanced competitive environment.

To remain competitive, companies are focusing on regulatory compliance and product innovation. Leading brands are working to reduce sodium levels, obtain food safety certifications, and adhere to export regulations to secure their position in modern retail and foodservice channels. Traditional producers highlight their heritage by using authentic fermentation methods and sourcing anchovies locally, which appeals to consumers seeking authenticity. Meanwhile, premium brands are differentiating themselves by emphasizing product quality and unique origin stories, which help justify their higher price points. These strategies enable companies to effectively target different consumer segments, from mass-market buyers to premium customers.

Innovation and regulatory changes are playing a significant role in shaping the fish sauce market. Manufacturers are adopting hybrid fermentation techniques and introducing new flavour variations to improve production efficiency while maintaining the rich, traditional taste of fish sauce. Stricter regulations, such as labeling requirements and halal certifications, are pushing smaller players to adapt or risk losing market share, leading to gradual consolidation. At the same time, plant-based alternatives are slowly emerging as a niche segment. However, these alternatives face challenges in replicating the complex flavours of traditional fish sauce, limiting their appeal to a broader audience for now.

Asia-Pacific Fish Sauce Industry Leaders

-

Masan Group

-

Thai Fishsauce Factory (Squid Brand) Co., Ltd.

-

Mega Chef Brand

-

Pantainorasingh Manufacturer Co., Ltd.

-

Red Boat Fish Sauce

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Phichai Fish Sauce introduced "Powdered Fish Sauce," marking a groundbreaking innovation in the market. This product offered a high-protein, low-sodium alternative, catering to health-conscious consumers while maintaining the essence of traditional fish sauce.

- May 2025: Squid Brand introduced its new product, “Volcano Fish Sauce,” during the Thaifex-Anuga Asia 2025 event. This launch highlighted the company's efforts to innovate within the fish sauce market.

- December 2024: The first-ever Fish Sauce Festival in Vietnam, organized by HCMC, was held. The event garnered widespread attention from both residents and international tourists, showcasing Vietnam's rich culinary heritage.

Asia-Pacific Fish Sauce Market Report Scope

The Asia-Pacific fish sauce market encompasses both plain and flavoured varieties, with various flavour profiles. On the basis of category, the market is segment into organic and conventional. Based on the processing method, the market is segmented into traditional and industrial. The distribution channel segment includes retail, horeca, and food processing. On the basis of country, the market is segmented into China, India, Japan, South Korea, Australia, Indonesia, Thailand, Vietnam, the Philippines, Malaysia, Singapore, New Zealand, and the Rest of the Asia-Pacific.

By Flavour Profile

| Plain |

| Flavoured |

By Category

| Organic |

| Conventional |

By Processing Method

| Traditional |

| Industrial |

By Distribution Channel

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others | |

| Food Processing | |

| HoReCa |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Malaysia |

| Singapore |

| New Zealand |

| Rest of Asia-Pacific |

| By Flavour Profile | Plain | |

| Flavoured | ||

| By Category | Organic | |

| Conventional | ||

| By Processing Method | Traditional | |

| Industrial | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| Food Processing | ||

| HoReCa | ||

| By Country | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Malaysia | ||

| Singapore | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Asia-Pacific fish sauce market?

The Asia-Pacific fish sauce market size is USD 2.06 billion in 2025.

How fast is the category expected to grow over the next five years?

The market is projected to expand at a 6.29% CAGR, reaching USD 2.79 billion by 2030.

Which flavor segment is expanding more quickly?

Flavored variants are forecast to grow 7.54% annually through 2030, outpacing plain products.

Why is Vietnam considered the fastest-growing country market?

Vietnam benefits from EU-recognized Phu Quoc geographic indication and rising exports, supporting a 7.83% CAGR.

Page last updated on: