Dipping Sauces Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

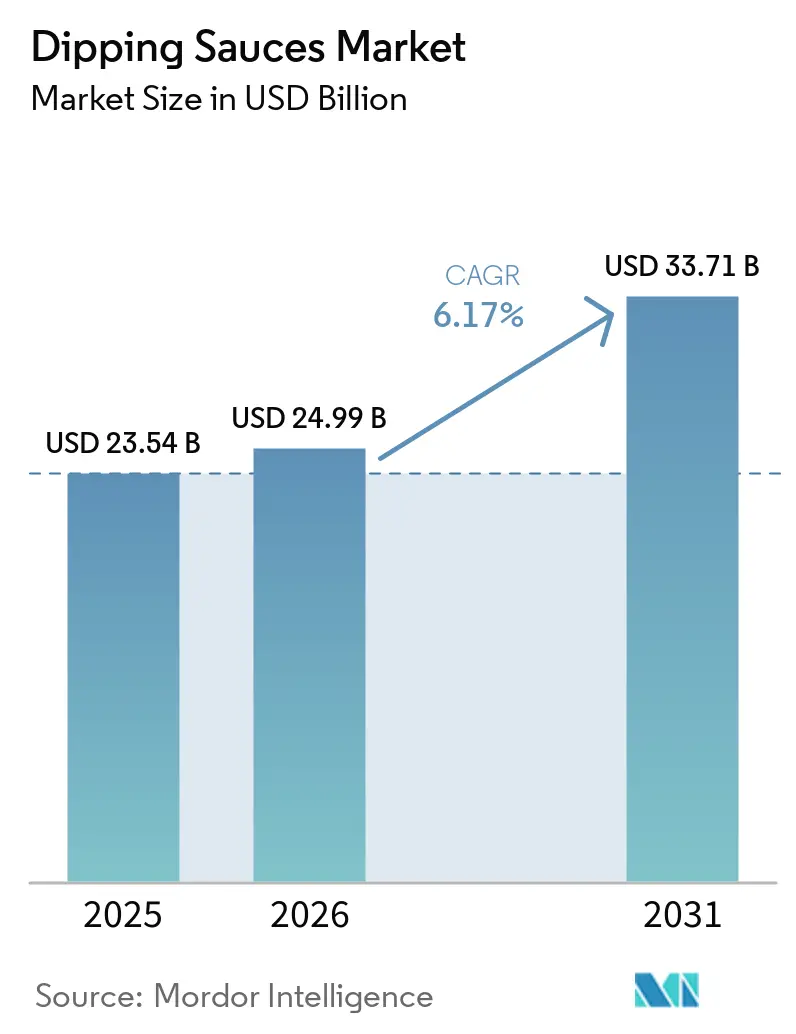

| Market Size (2026) | USD 24.99 Billion |

| Market Size (2031) | USD 33.71 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

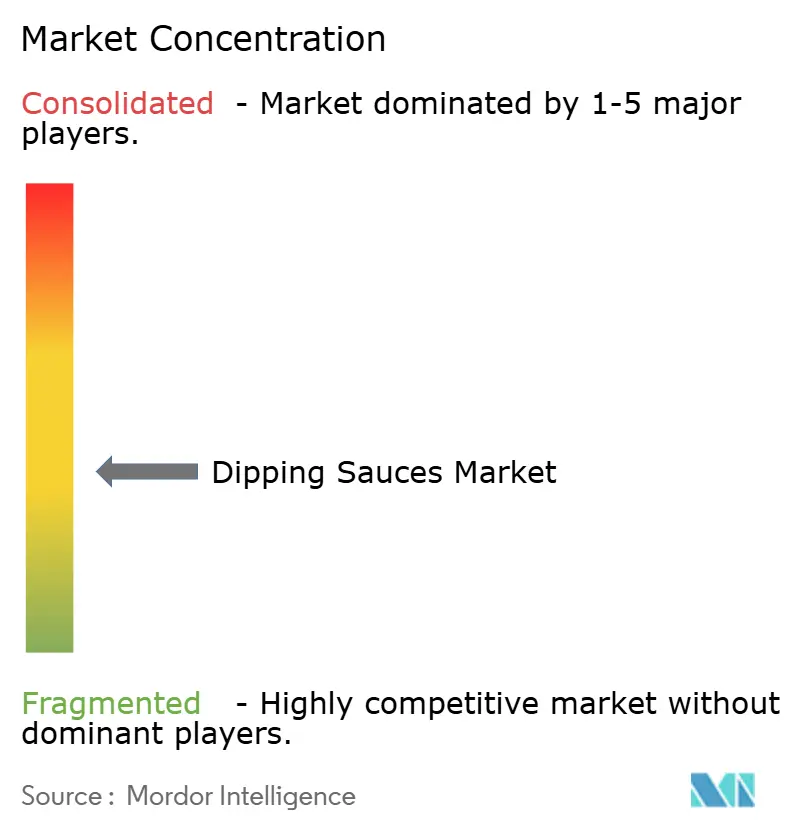

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dipping Sauces Market Analysis by Mordor Intelligence

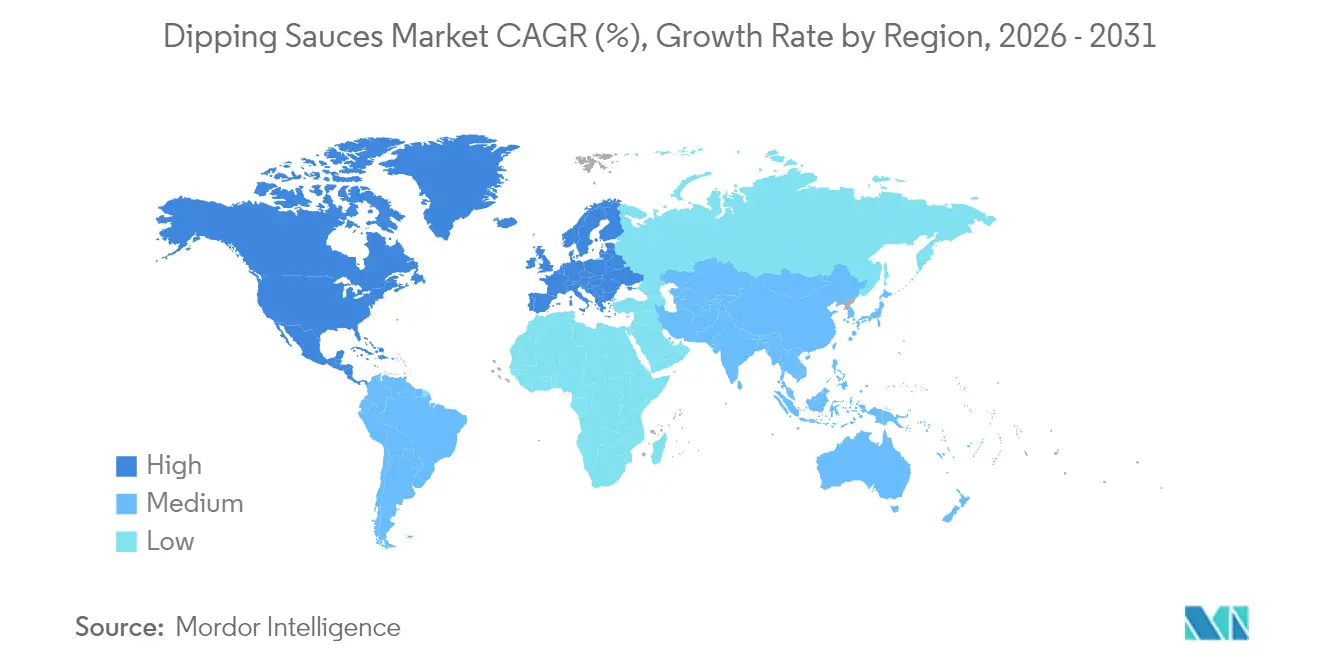

Dipping sauces market size in 2026 is estimated at USD 24.99 billion, growing from 2025 value of USD 23.54 billion with 2031 projections showing USD 33.71 billion, growing at 6.17% CAGR over 2026-2031. This growth is fueled by an uptick in quick-service restaurants, a burgeoning interest in global cuisines, and urban snacking trends. For instance, the International Franchise Association reported a rise in quick-service restaurant franchises in the U.S., from 195,245 in 2023 to an estimated 199,931 in 2024[1]Source: International Franchise Association, "2025 Franchising Economic Outlook", franchise.org. North America commanded a dominant 45.43% share of the dipping sauces market in 2024, while the Asia-Pacific region is set to outpace with a robust 7.66% CAGR, driven by a burgeoning working-age demographic and rising disposable incomes. While tomato-based sauces lead the pack, soy-derived options and organic variants are swiftly gaining ground, blending health consciousness with flavor exploration. The market, underscored by consolidations among major packaged-food players and a flurry of new product launches, signals a disciplined yet opportunity-laden phase.

Key Report Takeaways

- By product type, tomato sauce commanded 34.71% of the dipping sauces market share in 2025, while soy sauce is forecast to accelerate at a 6.81% CAGR through 2031.

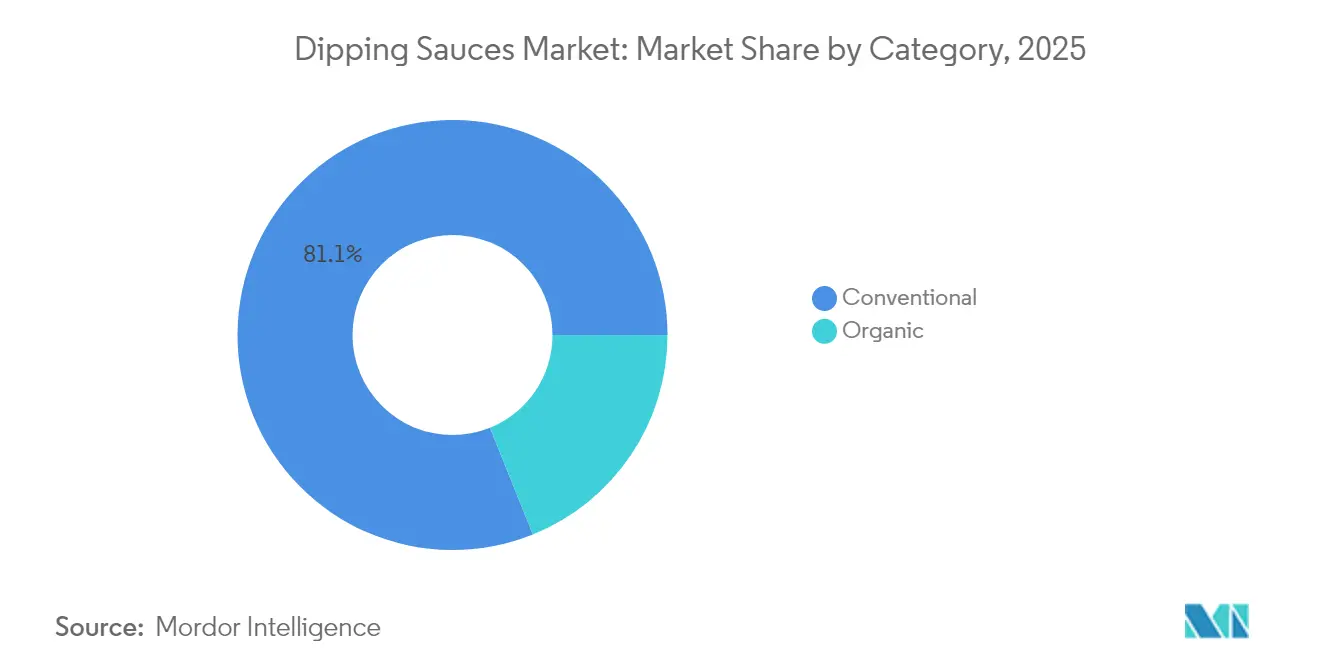

- By category, conventional offerings held 81.10% of the dipping sauces market size in 2025, but organic formulations are projected to expand at a 6.69% CAGR during the outlook period.

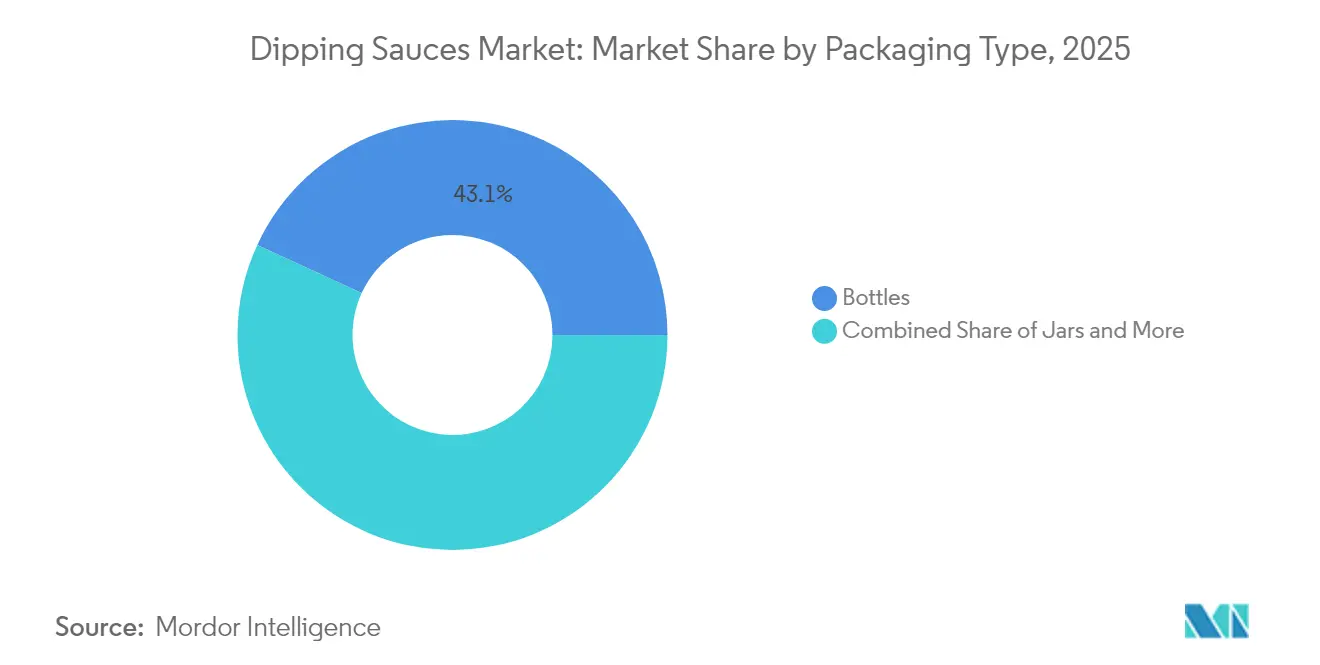

- By packaging, bottles led with a 43.12% revenue share in 2025; jars are the fastest-growing format, advancing at a 7.03% CAGR to 2031.

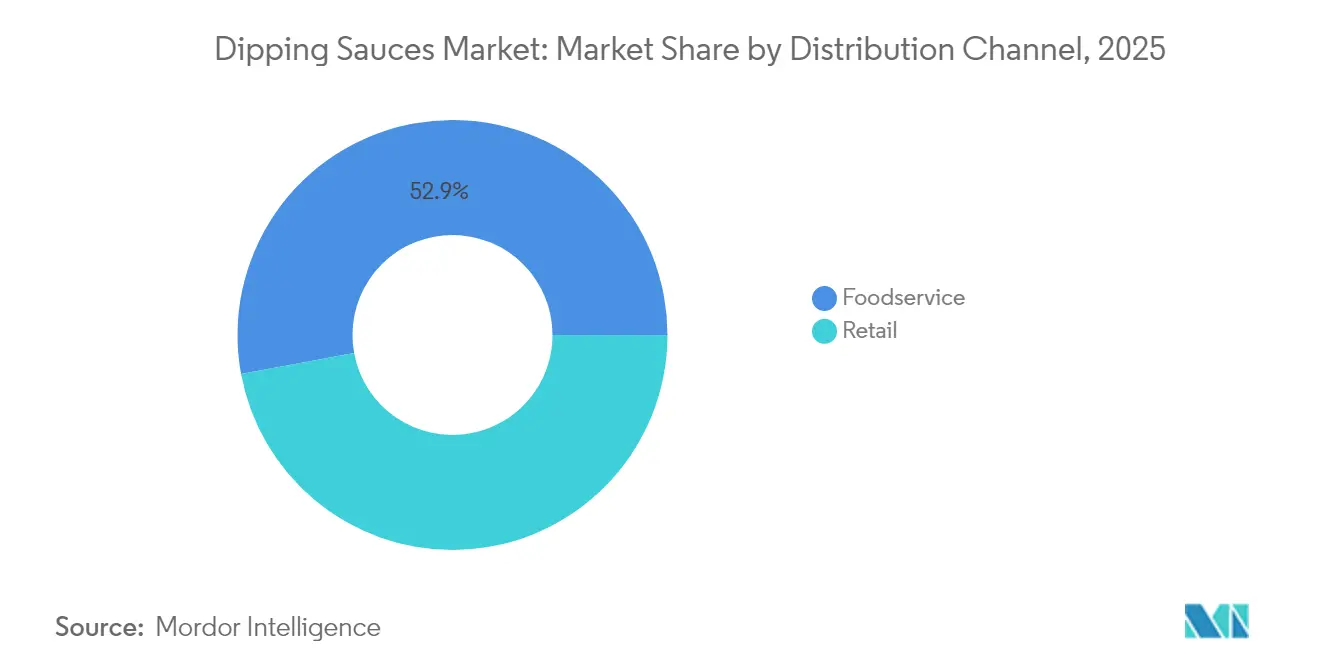

- By distribution channel, retail accounted for 47.10% of the dipping sauces market size in 2025, whereas foodservice is set to rise at a 7.18% CAGR on the back of QSR proliferation.

- By geography, North America dominated the dipping sauces market with 44.86% revenue share in 2025; Asia-Pacific will register the highest 7.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dipping Sauces Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in flavors and formats | +1.2% | Global, with early adoption in North America & Asia-Pacific | Medium term (2-4 years) |

| Expansion of fast-food and quick-service restaurants | +1.5% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Growing appetite for international cuisines | +0.9% | Global, concentrated in urban centers | Medium term (2-4 years) |

| Rise of plant-based and vegan diets | +0.7% | North America & Europe, expanding to urban Asia-Pacific | Long term (≥ 4 years) |

| Advancements in packaging | +0.6% | Global, with regulatory drivers in Europe and North America | Short term (≤ 2 years) |

| Rise in snacking and convenience foods | +1.1% | Global, accelerated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Innovation in Flavors and Formats

Market expansion is being driven by flavor innovation, with manufacturers introducing variants like Korean BBQ, General Tso, and Mango Habanero to cater to evolving palates. Frank's RedHot exemplifies this trend with its April 2025 launch of six new sauces, specifically targeting younger demographics in search of Instagram-worthy food experiences. The rise of single-serve packaging and squeeze bottles caters to on-the-go consumption. Meanwhile, fermentation technologies are making it possible to achieve authentic, shelf-stable flavors that were once only available in fresh preparations. This cycle of innovation is especially advantageous for Asian-inspired sauces. With 82% of consumers showing a preference for hot and spicy flavors, there's a burgeoning market for sriracha variants, gochujang blends, and sambal-inspired formulations.

Expansion of Fast-Food and Quick-Service Restaurants

As quick-service restaurants (QSRs) expand, they're not just boosting their own sales; they're also fueling a growing appetite for sauces. This surge is evident both in foodservice procurement and in the retail sector, as consumers increasingly buy sauces to replicate dining experiences at home. Take, for example, the data from the U.S. Securities and Exchange Commission: In 2024, the U.S. and Canada boasted 7,082 Burger King outlets. Meanwhile, McDonald's, with a global footprint, expanded its reach to 43,477 restaurants, up from 41,822 the prior year[2]Source: U.S. Securities and Exchange Commission, "Restaurant Brands International Form 10-K 2024", sec.gov. The UK’s QSR market is on an upswing, with the burger segment leading the charge and boosting condiment sales. Asian markets, especially with the rise of Japanese restaurants beyond Japan, are witnessing a QSR boom. This growth not only drives bulk purchases for foodservice but also sees consumers turning to retail, eager to recreate their favorite dining moments at home.

Growing Appetite for International Cuisines

As the global Asian food market expands, cultural globalization and shifting migration patterns are driving a heightened demand for both authentic and adapted international sauces. Culinary diversity, spurred by migration, is introducing regional specialties to fresh markets. At the same time, the rise of fusion cuisine is birthing hybrid sauce categories that meld traditional profiles with local tastes. Notably, Filipino flavors are carving out a significant niche, with establishments like Oko and Kasama championing the mainstream acceptance of adobo and bagoong-inspired sauces. This burgeoning trend isn't limited to Asian cuisines alone; it's also embracing flavor profiles from Latin America, the Middle East, and Africa, as urban dwellers become more adventurous in their culinary pursuits.

Rise of Plant-Based and Vegan Diets

As plant-based diets gain traction, manufacturers are reformulating products with vegan-friendly ingredients, paving the way for innovative vegetable-based sauces. In 2024, the FDA issued plant-based labeling guidance, offering manufacturers clarity on crafting dairy-free and egg-free products. Simultaneously, the USDA's organic certification processes are adapting to embrace these plant-based ingredients. This trend is especially pronounced in premium sauce segments, where consumers are willing to pay a premium for clean-label, plant-forward products. In response, manufacturers are rolling out cashew-based creamy sauces, umami profiles enhanced with nutritional yeast, and dips fortified with vegetable proteins, catering to both dedicated vegans and flexitarians who occasionally opt for plant-based choices.

Restrains Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeiting and quality concerns | -0.8% | Global, concentrated in developing markets | Short term (≤ 2 years) |

| High sugar and salt content concerns | -1.1% | Global regulatory pressure in developed markets | Medium term (2-4 years) |

| Varying and strict regulatory standards | -0.7% | Global, complexity is highest in multi-market operations | Long term (≥ 4 years) |

| Consumer skepticism towards additives | -0.6% | Developed markets, spreading to urban emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeiting and Quality Concerns

Food fraud detection has unveiled notable adulteration threats within the spice and condiment supply chains. Surveys from the EU highlight suspicious rates of adulteration, with paprika products at 6% and oregano-based seasonings soaring to 48%. In 2024, the FDA intensified its scrutiny, taking enforcement actions against sauce manufacturers for violations related to process filing and labeling. Such actions underscore the growing regulatory oversight in the industry. Official food fraud reports globally rank processed foods second, posing challenges to consumer trust. This issue is particularly pronounced in the premium and organic sauce segments. While authentication technologies, such as qPCR testing methods from the EU Joint Research Centre, offer detection capabilities, their implementation costs pose a challenge for smaller manufacturers. This financial burden inadvertently grants larger producers, equipped with advanced quality control systems, a competitive edge.

High Sugar and Salt Content Concerns

Regulatory bodies worldwide are tightening their grip on high-sodium condiments. Mexico's NOM-051 mandates front-of-pack warnings for products with sodium levels exceeding 300mg per 100g. Meanwhile, Argentina's ANMAT has rolled out modified labeling requirements, and Indonesia is crafting an all-encompassing Nutri-Level system. These regulations are nudging manufacturers towards reformulation, but this shift risks altering traditional flavor profiles that have long depended on salt for both preservation and taste enhancement. In a related move, the FDA's decision in January 2025 to revoke the authorization for Red Dye No. 3 underscores the growing scrutiny on food additives. Concurrently, several US states have taken a stand, banning a range of food additives in school programs. While there's a rising consumer demand for reduced-sodium alternatives, achieving this isn't straightforward. The challenge lies in ensuring shelf stability and flavor integrity without leaning on traditional preservatives. This complexity not only escalates production costs but also curtails opportunities for product differentiation, leading to a notable dip in global production. Data from the Office for National Statistics (UK) reveals a decline in tomato ketchup sales volume, dropping from 164.8 thousand tons the previous year to around 150 thousand tons in 2023[3]Source: Office for National Statistics (UK), "UK Manufacturers' Sales by Product Survey (Prodcom), Provisional Results 2022", www.ons.gov.uk. Echoing this trend, the Istituto Nazionale di Statistica reports a significant dip in Italy's annual production, plummeting to about 142,000 tons in 2023, a stark contrast to the 191,000 tons recorded in 2022.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tomato Dominance Faces Asian Sauce Surge

In 2025, tomato sauce holds a commanding 34.71% share of the market, underscoring its culinary versatility and deep-rooted consumer familiarity. Meanwhile, soy sauce is making waves as the fastest-growing segment, boasting a 6.81% CAGR projected through 2031. Tomato sauce's prominence is anchored in its foundational role in Western cuisines, its seamless adaptability to fusion dishes, and the backing of robust supply chains and cost-effective production. Soy sauce's ascent is fueled by the global embrace of Asian cuisine, notably with a surge in Japanese restaurants popping up beyond Japan's borders. While mustard sauce enjoys consistent demand in Europe and North America, barbecue sauce's popularity shifts, influenced by regional taste preferences and the expanding grilling culture.

The "Other Product Types" segment is a melting pot of emerging fusion sauces and ethnic specialties. This includes everything from sriracha variants and gochujang blends to tahini-based concoctions, all echoing the cultural diversification of urban dining. Manufacturers are increasingly tapping into traditional fermentation techniques, not just for authenticity but to craft shelf-stable flavors that emphasize umami. While tomato-based products benefit from established agricultural networks in the supply chain, specialty Asian sauces grapple with ingredient sourcing challenges. These complexities not only pose barriers to entry but also present opportunities for premium positioning, especially for those seeking authentic formulations.

By Category: Conventional Strength Meets Organic Acceleration

In 2025, conventional sauces hold an 81.10% market share, while organic alternatives grow at a 6.69% CAGR through 2031, reflecting a shift toward clean-label products despite premium pricing. The conventional segment benefits from production economies, extensive distribution, and competitive pricing, appealing to diverse economic groups. Organic growth is driven by health consciousness, environmental awareness, and USDA organic certification, which boosts consumer trust. Premium positioning enables organic manufacturers to secure higher margins and target affluent urban consumers willing to pay for health and environmental benefits.

Conventional manufacturers counter organic competition by reformulating products to reduce artificial additives while maintaining costs, creating "natural" lines that bridge conventional and organic. The organic segment faces supply chain issues, including limited certified ingredients and seasonal production, complicating inventory management. Regulatory compliance costs burden smaller organic producers, while large conventional manufacturers leverage scale to enter the organic market through acquisitions or dedicated production lines serving both categories.

By Packaging Type: Bottles Lead While Jars Gain Traction

In 2025, bottles command a 43.12% market share, thanks to established consumer familiarity and cost-effective manufacturing. Meanwhile, jars are on a trajectory, growing at a 7.03% CAGR through 2031, driven by consumer preferences for resealability and portion control. Bottle packaging leads the pack, capitalizing on production efficiency, optimized transportation, and convenient dispensing, all tailored for high-volume foodservice consumption. The surge in jar popularity mirrors evolving consumption trends, with smaller household sizes gravitating towards premium products. Glass packaging, often associated with quality, bolsters these premium price points. In the Asia-Pacific, sachet formats cater to emerging markets and single-serve needs, where affordability and portion control reign supreme.

Innovations in sustainable packaging are reshaping format choices. In July 2024, MasterFoods, backed by a USD 3 million investment, piloted paper-based tomato sauce packs, slashing plastic content by 58%. Meanwhile, smart packaging, featuring freshness indicators and traceability, gains traction, buoyed by USDA NIFA's funding for advanced printed electronics and sensors, underscoring product safety and boosting consumer trust. Yet, the rising costs of packaging materials pose challenges. Manufacturers find themselves at a crossroads, weighing sustainability aspirations against price competitiveness, all while navigating margin pressures in sensitive market segments.

By Distribution Channel: Retail Dominance Challenged by Foodservice Growth

In 2025, retail channels capture a 47.10% market share, bolstered by supermarket penetration and e-commerce growth. Meanwhile, the foodservice sector, driven by the rise of quick-service restaurants (QSRs) and the integration of delivery platforms, is set to grow at a 7.18% CAGR through 2031. Retail's robust performance mirrors a consumer shift towards home cooking and bulk buying, emphasizing cost savings and personalized flavors. On the other hand, the foodservice sector is buoyed by an uptick in dining out, especially among Gen Z, who, despite spending less annually than Millennials, are driving demand for single-serve and delivery-friendly packaging. Within the retail sphere, online sales are surging, thanks to the rise of digital commerce and subscription services, which enhance convenience and spotlight specialty sauces.

The foodservice domain not only includes traditional restaurant sourcing but also the burgeoning ghost kitchen trend, both of which prioritize standardized flavors and dependable supply chains. As delivery platforms gain traction, there's a heightened demand for packaging that's leak-proof and temperature-stable, ensuring product integrity en route. While retail faces challenges from private label rivals and heightened promotions, foodservice channels present a more stable volume and lower marketing costs. This stability is enticing for manufacturers, offering them a chance at consistent revenue, albeit with slimmer margins per unit.

Geography Analysis

North America, with a mature QSR landscape and a diverse, immigrant-driven palate, commands a dominant 44.86% market share. The region's robust cold-chain infrastructure supports a wide variety of refrigerated dips, while omnichannel retail strategies ensure these products maintain a strong shelf presence. Innovations are increasingly centered around sodium-reduced and non-GMO offerings, catering to the discerning, label-conscious consumer. In Canada, there's a noticeable uptick in the popularity of plant-based sauces. Meanwhile, in Mexico, the NOM-051 labeling regulation has prompted local producers to reduce salt content.

Asia-Pacific is on an impressive trajectory, projected to grow at a 7.51% CAGR through 2031, driven by urbanization and a burgeoning middle class. China's advanced e-commerce platforms ensure imported gourmet sauces are just a day away, while India's expanding organized retail sector provides a platform for foreign brands, especially those tweaking their heat levels. Southeast Asia, with its swift smartphone adoption and a culture that embraces adventurous street food, sees a surge in demand for chili-infused dips, especially in convenient sachet formats. For foreign brands, localizing offerings—be it through spice adjustments, halal certifications, or region-specific packaging—is crucial.

Europe showcases steady volume growth, yet leans towards premium products, underscoring its commitment to stringent food quality and sustainability. While German consumers are gravitating towards biodynamic tomato ketchup and French households remain loyal to traditional Dijon mustard, there's a growing curiosity for Japanese yuzu miso sauces. In the wake of Brexit-induced customs challenges, U.K. retailers are diversifying their sourcing strategies, inadvertently paving the way for U.S. and Asian exporters. While Latin America and the Middle East & Africa (MEA) present long-term growth potential, challenges like currency fluctuations and fragmented logistics temper immediate market entry enthusiasm.

Competitive Landscape

The dipping sauces market sees moderate concentration, with Kraft Heinz, Unilever, McCormick, and PepsiCo dominating key supermarket lanes. In November 2024, PepsiCo's acquisition of Sabra broadened its reach into refrigerated hummus, complementing its Frito-Lay snacking empire. Advent International's buyout of Sauer Brands in January 2025 highlights private equity's keen interest in scaling condiments, paving the way for supply-chain synergies and cross-category innovations. In 2025, Campbell's acquisition of Sovos Brands integrates the premium Rao's marinara into a wider sauce portfolio, positioning the group for higher-margin opportunities.

Regional experts like Kikkoman in soy, Lee Kum Kee in oyster sauce, and Tiger Brands in chutneys command strong home-market shares and are increasingly turning to e-commerce for exports. Plant-based newcomers, such as JUST Sauce, are sidestepping shelf fees with direct-to-consumer strategies, while restaurant chains like Nando's are capitalizing on their brand equity by offering retail packs. Intellectual-property trends reveal a focus on extending shelf life using natural antimicrobials and developing recyclable barrier layers. New entrants grapple with challenges in procurement scale and understanding label compliance, but savvy social-media strategies can rapidly shift niche segments.

Dipping Sauces Industry Leaders

-

Kraft Heinz Company

-

Unilever plc

-

McCormick & Company Inc.

-

Kikkoman Corporation

-

Conagra Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Heinz introduced a new line of dipping sauces called "Flavor Remix," targeting Gen Z and Millennial consumers. The line featured unique flavor combinations like "Spicy Pickle Ketchup" and "Sweet & Tangy Chipotle Mayo," designed to elevate everyday meals and snacks. These sauces were made available in both retail stores and are being rolled out to select foodservice partners.

- March 2025: Taco Bell expanded its partnership with Beyond Meat and rolled out a new line of plant-based cheese dips and creamy sauces across its U.S. locations. This move catered to the growing vegan and flexitarian customer base, integrating alternative protein options into their popular menu items.

- February 2025: Kikkoman expanded its soy sauce and related dipping sauce production facility in Singapore. This multi-million dollar investment aimed to increase capacity to meet surging demand across the Asia-Pacific region, particularly for its various dipping sauces used in both home cooking and Asian-inspired foodservice.

- January 2025: Organic Valley, a leading organic food co-operative, acquired "Creamy Delights," a regional brand specializing in organic dairy-based dips (e.g., ranch, French onion). This acquisition strengthened Organic Valley's position in the premium organic dipping sauces segment and expanded its distribution network within the retail sector.

Global Dipping Sauces Market Report Scope

A dipping sauce is a popular condiment for a variety of foods. Dips are used to enhance the flavor or texture of foods such as pita bread, dumplings, crackers, chopped raw vegetables, shellfish, meat, and cheese. Dips are also frequently used for finger snacks and appetizers.

The dipping sauce market is segmented by category, product type, distribution channel, and geography. By category, the market is segmented into organic and conventional. By product type, the market is segmented into Tomato Sauce, Mustard Sauce, Soy Sauce, Barbecue Sauce, and Others. By Distribution Channel Supermarkets/Hypermarkets, Convenience/ Grocery Stores, Online Retail Stores, and Other distribution channels. The market study also covers the analysis with respect to regions such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa. For each segment, the market sizing and forecasts are carried out on the basis of value (in USD millions).

| Tomato Sauce |

| Mustard Sauce |

| Soy Sauce |

| Barbecue Sauce |

| Other Product Types |

| Conventional |

| Organic |

| Bottles |

| Jars |

| Sachets |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Tomato Sauce | |

| Mustard Sauce | ||

| Soy Sauce | ||

| Barbecue Sauce | ||

| Other Product Types | ||

| By Category | Conventional | |

| Organic | ||

| By Packaging Type | Bottles | |

| Jars | ||

| Sachets | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the dipping sauces market and its expected 2031 level?

The market stands at USD 24.99 billion in 2026 and is projected to reach USD 33.71 billion by 2031.

Which region is growing fastest in dipping sauces?

Asia-Pacific leads with a forecast 7.51% CAGR through 2031, driven by urbanization and rising household incomes.

Which product type delivers the highest dipping sauces market share today?

Tomato-based sauces remain dominant, holding 34.71% of 2025 revenue.

How significant is organic penetration within dipping sauces?

Organic lines represent under one-fifth of revenue but are expanding at a 6.69% CAGR, outpacing conventional growth.

What packaging format is gaining popularity for sauces in retail?

Glass jars are the fastest-growing format owing to resealability and premium cues, posting a 7.03% CAGR to 2031.

Which companies recently made strategic acquisitions in dipping sauces?

PepsiCo bought Sabra in 2024, Advent International acquired Sauer Brands in 2025, and Campbell Soup picked up Sovos Brands in 2025.

Page last updated on: